vietnam infrastructure sua can - world banksiteresources.worldbank.org/inteapinfrastruct/... · as...

TRANSCRIPT

Infrastructure StrategyCross-sectoral issues

As Vietnam becomes richer it faces challenges in adapting its infrastructurepolicies and institutions. While the old challenges of providing basicservices to all remain, new challenges are emerging, such as accessing newsources of finance, refining planning processes, preparing for rapidurbanization, improving the efficiency of infrastructure service providers,developing stronger institutions to encourage private finance ofinfrastructure or direct private provision of infrastructure, and developingmore targeted approaches to poverty alleviation.

This report on Infrastructure Strategy - Cross Sectoral Issues is one of sixvolumes dealing with Vietnam's Infrastructure Challenge. It deals with cross-sectoral issues that are common to all infrastructure sectors, and provides anoverview of recent achievements and emerging challenges. Other volumesdeal with Water and Sanitation, Electricity, Transport, Telecommunications,and Urban Development.

The work for these reports was carried out between 2004 and 2006 byWorld Bank staff and consultants, under the direction of Klaus Rohland,Country Director for Vietnam, and Christian Delvoie, Sector Director forInfrastructure in East Asia and the Pacific. The reports have been revised totake account of comments made by the Government in workshops duringMay 15-17, 2006. The principal author of this volume was Michael Warlters.The comments of numerous colleagues from the World Bank, the UnitedKingdom's Department for International Development Bank, the AsianDevelopment Bank, and the Japan Bank for International Cooperation aregratefully acknowledged.

Vietnam’s infrastructure challenge

ADB Asian Development BankBCC Business Cooperation ContractBOT Build-Own-TransferCPRGS Comprehensive Poverty Reduction and Growth StrategyDAF Development Assistance FundEVN Electricity of VietnamGSO General Statistics Office of VietnamHIFU Ho Chi Minh City Investment Fund for Urban DevelopmentIBRD International Bank for Reconstruction and Development (the World Bank)ICOR Incremental Capital-Output RatioIDA International Development Association (the World Bank)IPP Independent Power ProducerITU International Telecommunications UnionJBIC Japan Bank for International CooperationLDIF Local Development Investment FundMARD Ministry of Agriculture and Regional DevelopmentMCF Marginal Cost of Public FundsMOF Ministry of FinanceMOT Ministry of TransportMPI Ministry of Planning and InvestmentMTEF Medium Term Expenditure FrameworkOBA Output Based AidODA Official Development AssistancePER-IFA Public Expenditure Review and Integrated Fiduciary AssessmentPIP Public Investment ProgramPPI Private Participation in InfrastructureSEDP Socio-Economic Development PlanSOCB State-Owned Commercial BankSOE State-Owned EnterpriseVHLSS Vietnam Household Living Standards SurveyVITRANSS Vietnam’s Transport Strategy StudyVND Vietnamese DongVNPT Vietnam Post and Telecommunications CorporationVRA Vietnam Road AdministrationWDI World Development Indicators

Abbreviations

iii

ABBREVIATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .i

EXECUTIVE SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .vii

Cross-Sectoral Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .viiiSectoral Strategies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xviiReform Prioritization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xxvi

1. ACHIEVEMENTS AND CHALLENGES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

1.1. Growth and Poverty Reduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11.2. Improved Access . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .51.3. Changing Circumstances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61.4. Shared Challenges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

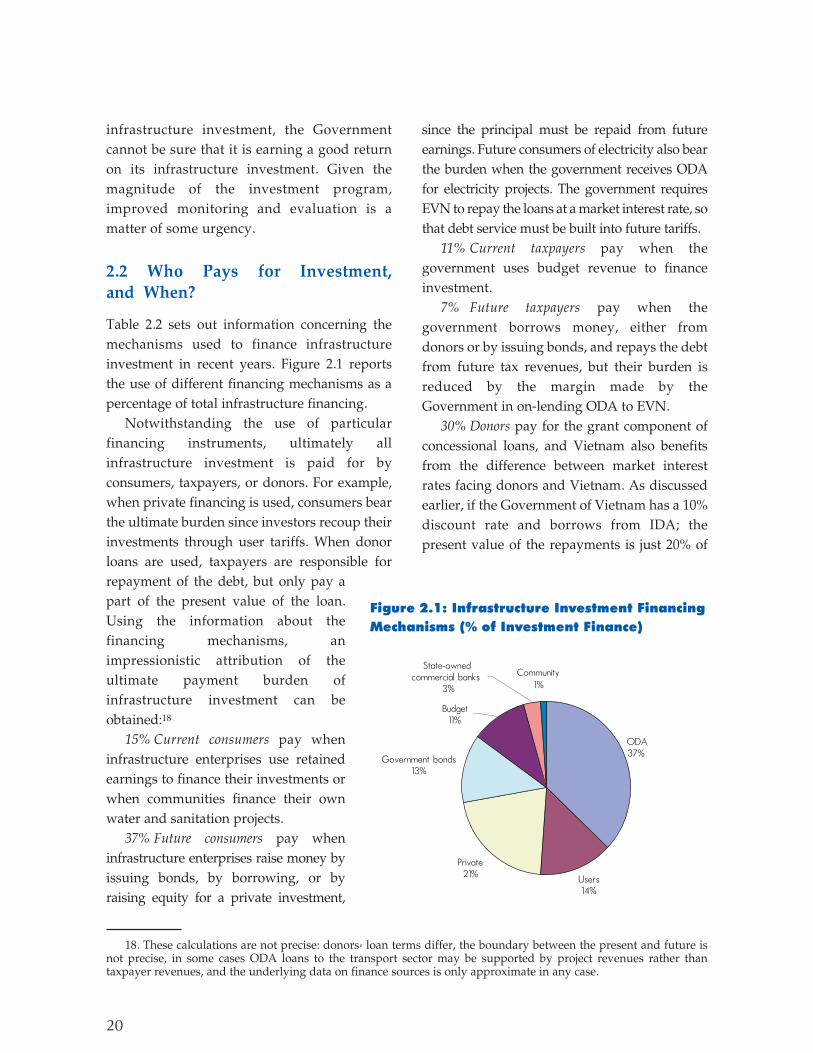

2. FINANCING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17

2.1. Level of Infrastructure Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .172.2. Who Pays for Investment, and When? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .202.3. Financing Institutions and Mechanisms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .212.4. Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39

3. PLANNING AND COORDINATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .43

3.1. Prioritizing Investment Decisions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .433.2. Coordination of Planning Across Ministries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .463.3. Allocation of Responsibilities Across Tiers of Government . . . . . . . . . . . . . . . . . . . . . . . . . . . . .513.4. Urban Planning . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .543.5. Environmental and Social Policies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .563.6. Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .60

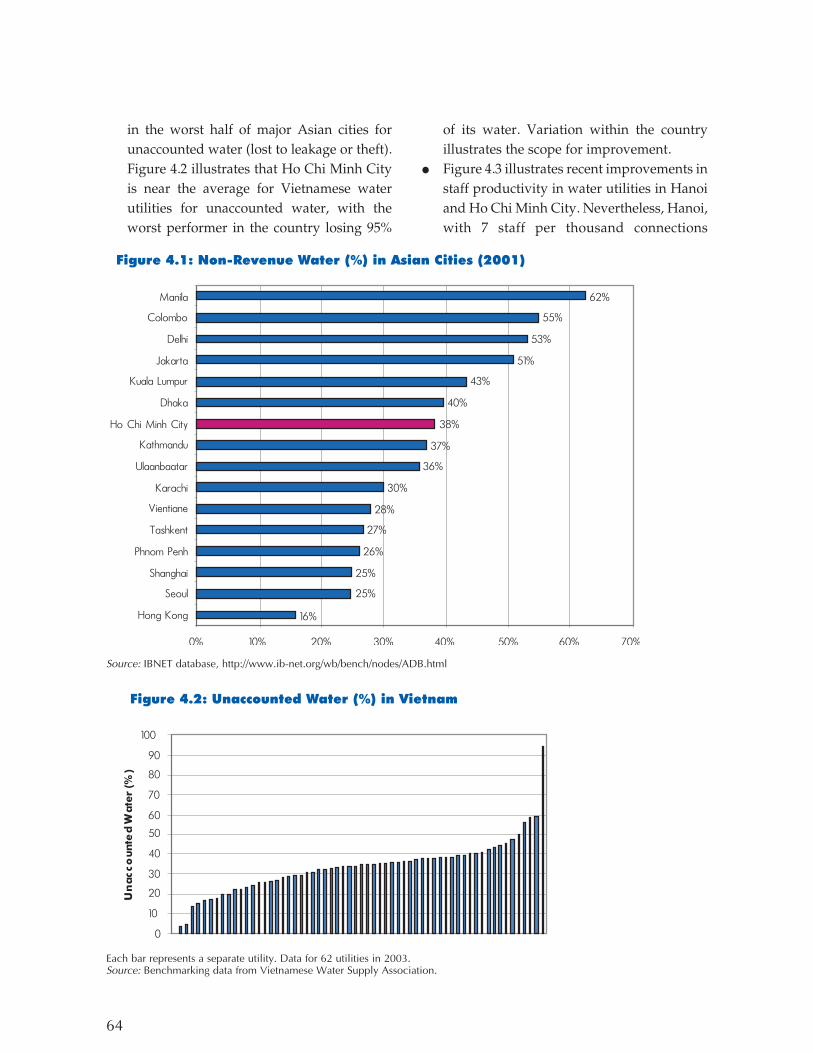

4. EFFICIENCY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .63

4.1. Current Efficiency Levels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .634.2. Reforming Public Infrastructure Enterprises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .674.3. Competition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .704.4. Private Participation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .714.5. Regulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .784.6. Addressing Corruption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .81

Table of Contents

iv

4.7. Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .84

5. POVERTY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .87

5.1. Rural Poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .875.2. Urban Poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .905.3. Designing Subsidies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .915.4. Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .95

6. REFORM PRIORITIZATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .97

6.1. International Competitiveness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .976.2. Estimates of Reform Effects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .986.3. Capacity to Manage Reform . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1016.4. Principal Reform Priorities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .101Annex 1 - Scope for Greater Competition in Infrastructure Sectors . . . . . . . . . . . . . . . . . . . . . . . . . . .104Annex 2 - Infrastructure Regulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .108

Boxes

Box 1.1: The Hanoi-Hai Phong northern transport corridor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4Box 2.1: The Marginal Cost of Public Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26Box 2.2: Vietnam's Financial Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27Box 2.3: Ho Chi Minh City Investment Fund for Urban Development (HIFU) . . . . . . . . . . . . . . . . . .30Box 2.4: Using Pension Funds to Finance Infrastructure in Chile . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .34Box 3.1: Common Weaknesses of Vietnamese Feasibility Studies . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44Box 3.2: Development Planning in Malaysia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45Box 3.3: A Medium Term Expenditure Framework (MTEF) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49Box 3.4: Weaknesses in the Coordination of Road Maintenance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .53Box 3.5: Strategic Environmental Assessment in Bali . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .57Box 3.6: Resettlement and Land Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .58Box 4.1: Phu My 2.2 Project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .74Box 4.2 Gujarat Infrastructure Development Board . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .78Box 4.3: Forms of Price Regulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .79Box 4.4: Discretion in the Regulation of Private Infrastructure Enterprises . . . . . . . . . . . . . . . . . . . . .80Box 4.5: Bangladesh Rural Electrification Board . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .82Box 4.6: Opportunities for Corruption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .83Box 5.1: Road Investment-A Case for Further Expenditure Redistribution . . . . . . . . . . . . . . . . . . . . .89Box 5.2: Targeting Effectiveness of Increasing Block Tariffs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .92Box 5.3: Output-based Aid: Tying Subsidies to Service Delivery for the Poor . . . . . . . . . . . . . . . . . . .95Box 6.1: Modeling the Benefits of Reform in Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .100

v

Figures

Figure 1: An Emerging Gap between Investment Plans and Available Financing . . . . . . . . . . . . . .viiiFigure 1.1: Growth of GDP per capita 1990-2003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2Figure 1.2: Growth and Infrastructure Investment, as percent of GDP . . . . . . . . . . . . . . . . . . . . . . . . . .3Figure 1.3: Percent of Population Living in Poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4Figure 1.4: Access to Infrastructure Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6Figure 1.5: Foreign Aid in US$ million . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7Figure 1.6: Urbanization in East Asia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8Figure 1.7: Vietnam's Incremental Capital Output Ratio . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11Figure 1.8: Rural/Urban Poverty Levels and Changes (1993-2002) . . . . . . . . . . . . . . . . . . . . . . . . . . . .12Figure 1.9: Regional Poverty Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12Figure 1.10: Evolution of Contribution to Poverty (percentage points) 1993-2002 . . . . . . . . . . . . . . .13Figure 1.11: Access to Clean Water, by Income Quintile . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13Figure 1.12: Access to Hygienic Latrines, by Income Quintile . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14Figure 1.13: Households living in rural villages with road access, by income quintile . . . . . . . . . . .14Figure 2.1: Infrastructure Investment Financing Mechanisms (% of Investment Finance) . . . . . . . . .20Figure 2.2: Spending on Energy Services (% Household Expenditure) . . . . . . . . . . . . . . . . . . . . . . . . .22Figure 2.3: Average Electricity Tariffs (US$/kWh) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23Figure 2.4: Operating Cost Coverage for 61 Vietnamese Water Utilities . . . . . . . . . . . . . . . . . . . . . . . .24Figure 2.5: Household Spending on Water Services (% Household Expenditure) . . . . . . . . . . . . . . .24Figure 2.6: Average Water Tariff (US$/m3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25Figure 2.7: Average revenues for water (US$/ m3) in 60 utilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25Figure 3.1: Gini Indexes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .46Figure 3.2: Transport Central Government Recurrent versus Capital Expenditure . . . . . . . . . . . . . .50Figure 4.1: Non-Revenue Water (%) in Asian Cities (2001) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .64Figure 4.2: Unaccounted Water (%) in Vietnam . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .64Figure 4.3: Water Utility Staff Ratio (Staff/1000 Connections) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65Figure 4.4: Staff per 1000 water and waste water connections in Vietnam . . . . . . . . . . . . . . . . . . . . . .66Figure 4.5: Telephone Mainlines per Employee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .66Figure 4.6: Transmission and Distribution Losses (% of Electricity Generated) . . . . . . . . . . . . . . . . . .66Figure 4.7: Road Maintenance Expenditure (% Total Road Expenditure) . . . . . . . . . . . . . . . . . . . . . . .67Figure 4.8: Transparency International Corruption Perceptions Index (2000-2004) . . . . . . . . . . . . . .81Figure 5.1: Percent Population with All-Weather Access to Rural Roads (2002) . . . . . . . . . . . . . . . . .89Figure 6.1: Percentage of firms ranking transport a severe or major constraint . . . . . . . . . . . . . . . . . .98Figure 6.2: Businesses' Problems with Infrastructure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .98

vi

Tables

Table 1.1: Investment in East Asia (% of GDP) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3Table 1.2: Present value of repayments on a $1 loan from the World Bank Group . . . . . . . . . . . . . . . .7Table 1.3: Urbanization Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9Table 2.1: Vietnam's Recent Investment in Infrastructure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18Table 2.2: Infrastructure Investment Financing Mechanisms (% of GDP) . . . . . . . . . . . . . . . . . . . . . . .19Table 2.3: Private Investment (Contractual Commitments)-US$ millions . . . . . . . . . . . . . . . . . . . . . . .37Table 4.1: Private Participation Contracts in Vietnam . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .73Table 4.2: Responsibilities under the Main Private Participation Options . . . . . . . . . . . . . . . . . . . . . .76Table 6.1: Benefits of Possible Reforms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .99

ver the past decade Vietnam has madespectacular progress in GDP growth andpoverty reduction. Annual per capita

growth has averaged 5.9%, the eighth highest inthe world over the decade. Since 1990, povertymeasured at the $1 a day threshold has fallenfrom 51% of the population to just 8%.

A critical part of this success has been a highlevel of investment in infrastructure. Around 9-10% of GDP has been invested in transport,energy, telecommunications, water, andsanitation in recent years, a very high level ofinfrastructure investment by internationalstandards. Microeconomic studies provideevidence of a strong link between thisinfrastructure investment and Vietnam'sgrowth and poverty reduction.

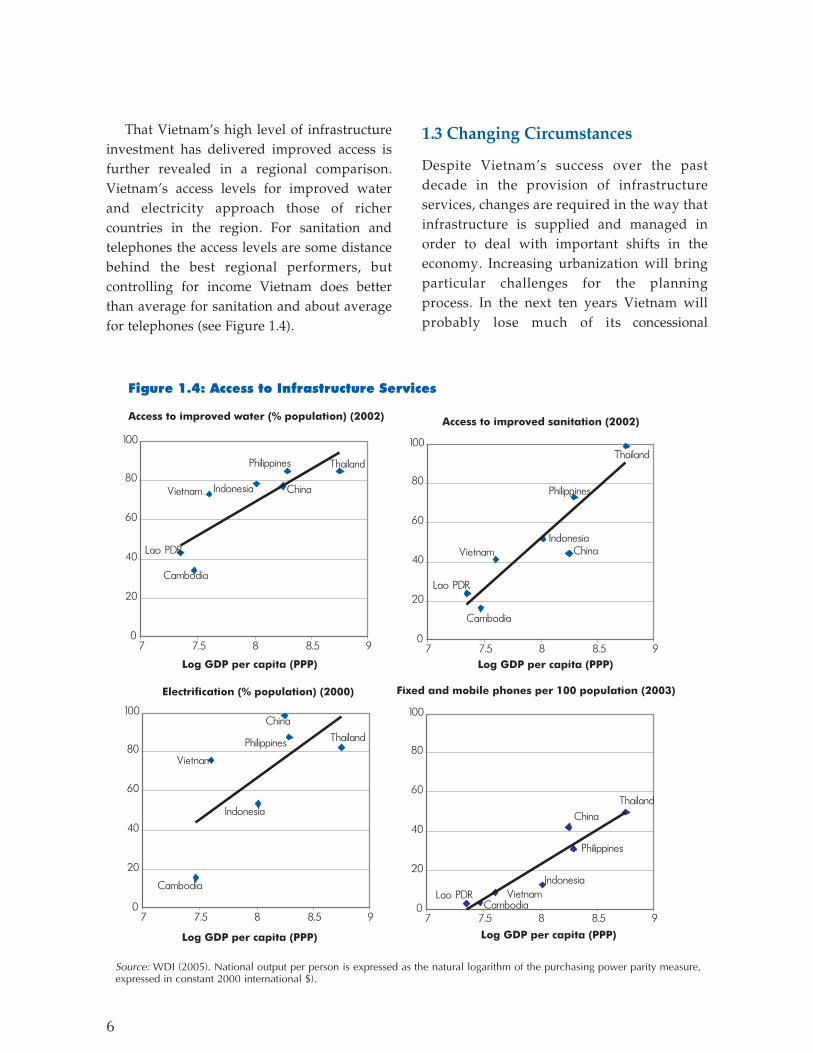

The road network has more than doubled inlength since 1990, and its quality has improvedsubstantially. All urban areas and 88% of ruralhouseholds have access to electricity. Thenumber of fixed and mobile phones per 100people has multiplied nine-fold since 1995.Access to improved water grew from 26% of thepopulation to 49% between 1993 and 2002, andduring the same time access to hygienic latrinesgrew from 10% to 25% of the population.

Vietnam's existing infrastructure strategyhas been a success. And yet, the strategy needsto evolve and adapt as new challenges emerge.

Over the next five to ten years, officialdevelopment assistance (ODA) is unlikely togrow at the same pace as the economy, and willthus occupy a smaller part of totalinfrastructure investment. Grants and the mostconcessional forms of donor financing will

become increasingly difficult to obtain asVietnam's GDP per capita exceeds donorthresholds. In all infrastructure sectors, there isa need to develop new sources of long-termfinance as alternatives to ODA. Much of thatfinance will need to come from financialmarkets or direct private finance, requiringreforms of consumer pricing, enterpriserestructuring, and revised regulation toestablish the credit-worthiness of infrastructureenterprises.

Urbanization is adding a million people peryear to Vietnam's urban centers, providing notonly a financing challenge to meet theirinfrastructure needs, but also a planningchallenge to ensure that infrastructureprovision is timely and avoids the need forexpensive retro-fitting after urban areas arealready settled.

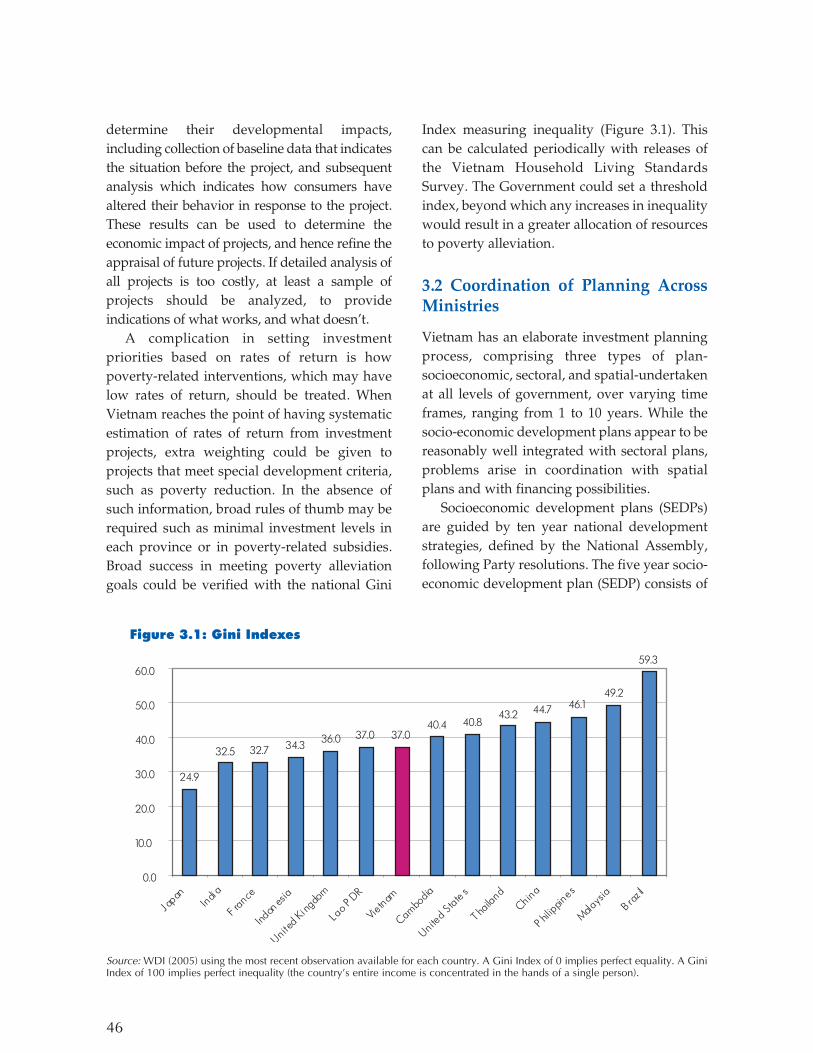

In past years, Vietnam could be reasonably sureof high social returns on public investment byconnecting consumers without access toinfrastructure networks. But as access levels increaseit will become more difficult to find investmentswith high rates of return, necessitating more refinedplanning systems. And as infrastructure networksexpand the cost savings available from moreefficient operation will increase, placing greateremphasis on tasks such as restructuring state-ownedenterprises, equitization, or the introduction ofgreater competition, to provide stronger commercialincentives. The elimination of corruption would alsohave a significant impact on the costs ofinfrastructure services.

Vietnam's approach to the reduction ofpoverty has been one of general reliance on

vii

Executive Summary

O

viii

growth, but with investments beinggeographically spread to ensure that all regionsparticipate in that growth. Increasingly povertyis focused in remote rural areas, ethnic minoritycommunities, and new areas of urban povertyarising from migration. As general poverty levelsfall and infrastructure access increases, theexisting approach to poverty reduction will needto be supplemented with approaches whichmore directly target individual householdsCareful review across infrastructure sectors isrequired to determine how existing subsidiescould be better targeted to address these newconcentrations of poverty, without wastingpoverty alleviation funds on the non-poor.

This report deals with cross-sectoralinfrastructure issues. Chapter 1 sets out theemerging challenges that will require a revisedapproach to Vietnam's infrastructure strategy -a reduction in ODA as a proportion of GDP,urbanization, the challenges of managing moreextensive infrastructure networks, and changesin the nature of poverty in Vietnam. Chapters 2to 5 set out the reform agenda required toaddress these new challenges, organized under

the themes of financing, planning, serviceefficiency, and poverty. Chapter 6 concludeswith a discussion of reform prioritization.

The report is accompanied by five furthervolumes dealing with transport, electricity,telecommunications, water and sanitation, andurban development. This executive summarypresents the main findings of all six volumes.

CROSS-SECTORAL ISSUES1. Investment Needs and Financing

Infrastructure investment in 2002 representedabout 9.4% of GDP. Looking to the future,sectoral plans and forecasts suggest futureannual infrastructure investment summing to11.4% of GDP, an increase of 2% of GDP overrecent levels:1● In September 2005, the Ministry of

Transport estimated future financing needsin a Medium Term Expenditure Framework,which matched proposed investment withpotential financing sources. The proposalsfor capital spending in 2006 to 2008amounted to VND 69,186 billion (US$ 4.3

1. In 2005, 2% of GDP was about VND 15,250 billion (US$ 966 million). Estimates of investment as a proportion ofGDP assume that GDP grows at 7% annually.

Figure 1: An Emerging Gap between Investment Plans and Available Financing

Source: For investment in 2002 see Table 2.1, for investment plans in 2010 see text in section 2.1, for financing sources in 2002 seeTable 2.2. Financing sources for 2010 assume that ODA grows at 2% p.a., while government and user financing (retained earnings)grow at the same pace as GDP (7% p.a.) from their 2002 levels.

ix

billion) over the three years, and averaged4.1% of GDP per year.

● In the electricity sector, investments requiredto meet the Fifth Power Master Plan amountto VND 215,078 billion (US$ 13,743 million)in the years 2005-2010, or about 3.9% of GDP.This figure is now regarded as anunderestimate, because of higher thanexpected demand growth in recent years.The financial model used by EVN to planfuture investments suggests that during2005-2010 capital expenditure will amount toVND 237,246 billion (US$ 16 billion), whichin annual terms is about 4.7% of GDP.

● In the water and sanitation sector theGovernment has set coverage targets toachieve its 2010 development goals. Thetargets are 85% for urban water andsanitation, and 75% for rural water andsanitation, which would require investmentof VND 57,547 billion (US$ 3.62 billion)during 2005-2010, or 1.2% of GDP annually.

● In the telecommunications sector, in October2005 the Ministry of Post and Telematicsadopted a target of 32-42 total telephonelines per 100 population by 2010. To achieve35 lines per 100 population would requireabout VND 57,000 billion (US$ 3.6 billion).Spread over the period 2006-2010, thiswould amount to around 1.4% of GDPannually.The forecasts should not be interpreted as an

endorsement of sectoral investment proposals.Closer analysis of the individual sector plansmay find ways of economizing on investments,increases in user tariffs could reduce demandand hence defer investment, and budgetingdecisions could result in indefinite deferral ofsome investment proposals. Nevertheless,investments dealing with electricity, water, andtelecommunications access targets are largelyunavoidable if the government's statedobjectives are to be met and should generally

yield high returns. Failure to keep pace with thegrowth of demand for electricity would likelyhave high economic costs. And the transportinvestment proposals have already beenprioritized to match existing sources of finance.

So, for purposes of thinking about financemobilization, a figure of about 10-11% of GDPseems reasonable. Nevertheless, a moredefinitive appraisal of the appropriate level ofinvestment would require a concerted effort tomonitor investment and maintenance activitiesand evaluate their financial and economicreturns.

Figure 1 illustrates the financing challengeimplied by this increase in investment. Thesources of finance in 2002 are summarized infour categories, with the category "Government"incorporating budget funding, governmentbond issues, as well as financing by State-Owned Commercial Banks. The category"Users" incorporates the retained earnings ofinfrastructure enterprises as well as communityfinancing of facilities such as small-scale ruralwater systems. The illustration supposes that thefinancing contribution by Government andUsers will grow with the economy, at 7% p.a.,but that ODA will only grow at 2% p.a. Underthese assumptions, ODA, Government and Userfinancing combined would fall short of the totalplanned/needed investment in 2010 by US$ 3billion, or 5.1% of GDP. In order to meet theGovernment's infrastructure goals, thisfinancing gap will need to be filled withexpanded Government financing, higher usertariffs, or an expanded role for the private sector.

An important source of this financingchallenge lies in the likely relative decline ofODA as a proportion of GDP. The assumptionthat ODA will grow at 2% of GDP, is purelyillustrative, and is by no means clear.Nevertheless, as discussed in Chapter 1, sometime druing 2010-2013, Vietnam is likely to begina "graduation" process in which it moves from

concessional IDA financing, to more expensiveIBRD financing. Internationally, the experiencehas been that when countries graduate, theytend to rely much less on ODA financing, and torely more on private financial markets.

While the levels of ODA in the future cannotbe predicted precisely, the overall nature of thefinancing challenge is clear. Vietnam must usethe coming years to develop financial institutionscapable of providing long-term finance forinfrastructure, and must reform its infrastructurebusinesses to become credit-worthy enterprisescapable of borrowing long-term.

Need to Increase Cost Recovery

A prerequisite for alternative financingmechanisms is cost-covering tariffs. Ensuringfull cost recovery through tariffs opens up arange of financing options that are otherwisegenerally impossible. The proportion of costsrecovered differs from sector to sector, and onlyin some sectors can it be increased. ● The principle is well established in

telecommunications and electricity. ● Charges associated with road transport,

such as vehicle registration and petrol tax,more than cover road maintenance costs,but do not cover the full cost of capitalinvested. There is scope to increase thesecharges, and there are many possibilities forrevenue to be raised from toll-roads.

● In the water sector, cost-covering tariffs havebeen embraced in the water sector in Ministryof Finance guidelines for water tariffs, and theprinciple is being considered forimplementation in a draft Government decree.But current water tariffs typically only coveroperational costs, while capital costs canoccupy 80% of total costs of a water utility.Considerable tariff increases would be requiredin the sector to achieve full cost recovery.

● In areas such as sanitation, waste water

treatment, and solid waste management, theability to raise revenues is constrained byconsumers' willingness to pay. The socialbenefits of these services typically exceedprivate willingness to pay, so a level of budgetsupport is appropriate. In these sectors thekey to mobilizing alternative financing is toprovide clear and predictable rules for theallocation of budget support, so that thefuture public revenue stream providessufficient security to mobilize investment. It ispossible to combine user payments withbudget revenues to meet the costs of serviceby means such as competitive bidding forservice delivery on a least-subsidy basis.

Other Sources of Finance

Wide-ranging reforms are required to developstronger institutions for infrastructure finance.

Governance reforms are needed for thestate-owned commercial banks to eliminateinformal pressures for "policy-lending",otherwise known as lending to projects that arenot commercially justified. In any case, directlending by banks is likely to play a relativelysmall role in infrastructure financing, because ofthe mismatch between short-term deposits heldby the banks and the long-term needs ofinfrastructure.

Bonds are a useful form of financing forinfrastructure, since they can provide long-termfinancing. The Government is making goodprogress in this area, but more needs to be donein the way of information disclosure concerningthe ability of public authorities to repay debt;and to increase the secondary activity andliquidity of the government bond marketthrough enhancements to the legal framework,improved debt issuance and management bythe Treasury, and strengthened intermediaryfunctions. As a means of limiting fiscal risks itwould be desirable for the Government to shift

x

from general obligation bonds (backed bytaxation powers) to revenue bonds (backed byinfrastructure revenues) where possible.

Decentralization has shifted greaterinvestment responsibilities to provincialgovernments. The extent to which thesegovernments have the financial resources tomeet their new responsibilities is unclear. Thesystem of transfers from the central governmentshould not undermine the incentives of localgovernments to raise their own revenues.Limits on their borrowing should be assessedbased on their ability to repay debt, rather thanthe current limits based on investment budgets.An expansion of property taxes could serve as auseful tax base to efficiently consolidate avariety of existing charges, and to provide areliable source of local government revenue.

Both central and provincial governments haveestablished specialist investment institutions,with an emphasis on infrastructure investment:the DAF and the 13 local developmentinvestment funds (LDIFs). Rationales for theseinstitutions include pooling finance from avariety of sources (reducing the risks taken by theindividual financing sources), and providingcenters of technical capacity for developinginfrastructure financing schemes. But:● They also expose the governments to fiscal risks

in the event of financing defaults. Measures areneeded to distance these institutions from thegovernments through clearer governancearrangements, and to install professionalmanagement practices to reduce risks ofdefault. Improved reporting is required toensure that the institutions' liabilities are takeninto account in assessments of thegovernment's fiscal position.

● In the case of the DAF, on-lending occurs atsubsidized rates. If investment subsidies areto be offered, differing levels of subsidiesshould be offered to different sectors inaccordance with the extent of externality or

other public finance rationale, andaccording to objective criteria.Equitization is a potential means of raising a

limited amount of infrastructure financing.Equity inputs can be used to increaseinvestment, or to retire public capital for useelsewhere. But the highest financing benefitswill not be realized if investors discount theprice they pay for the risks arising frominadequate disclosure of accountinginformation, or if investors are unable to obtainmanagement control rights.

There is great potential for more privateinvestment in infrastructure. But takingadvantage of this potential requires carefultransaction preparation and sound regulatoryenvironments. Vietnam should experimentmore with private financing than it has in thepast, developing a number of transactionsacross sectors, using competitive bidding, andcarefully monitoring the lessons learned.

Allied to the use of private financing,Vietnam should develop a risk managementframework that permits the appropriate use ofcontingent liabilities (such as guarantees) inattracting finance, but monitors and limits thegovernment's exposure.

Finally, efficiency improvements inprocurement and operation of infrastructureservices can be thought of as an alternative tothe mobilization of finance. Improvements inefficiency can increase output from existing andproposed facilities, and thereby lessen the needfor new investments.

2. Planning and Coordination

There is room for improvement in many aspectsof Vietnam's planning processes. As a result ofsuccess in increasing levels of access toinfrastructure services, it is becomingincreasingly difficult to select investmentprojects with high economic returns, requiringincreased emphasis on economic considerations

xi

in project selection. Rapid urbanization requiresimprovements in both the speed of urbanplanning processes, and also its responsivenessto local conditions. In addition to these reformsaddressing emerging challenges, there are long-standing needs to improve coordinationbetween spatial and sectoral master plans, todevelop tools to achieve national objectives inprovincial and municipal projects, and tointegrate environmental considerations intobroader investment planning.

Integrating Economic Criteria into ProjectSelection

The importance of economic criteria forchoosing between investment projects willincrease as the infrastructure stock increases.Identifying high return projects was easy whenmuch of the population lacked access toinfrastructure services. As the access rolloutadvances, choosing between investments willbecome more difficult. For example, it is noteasy to compare the social returns betweenproviding new connections in high costlocations or providing improved service qualityin areas already connected.

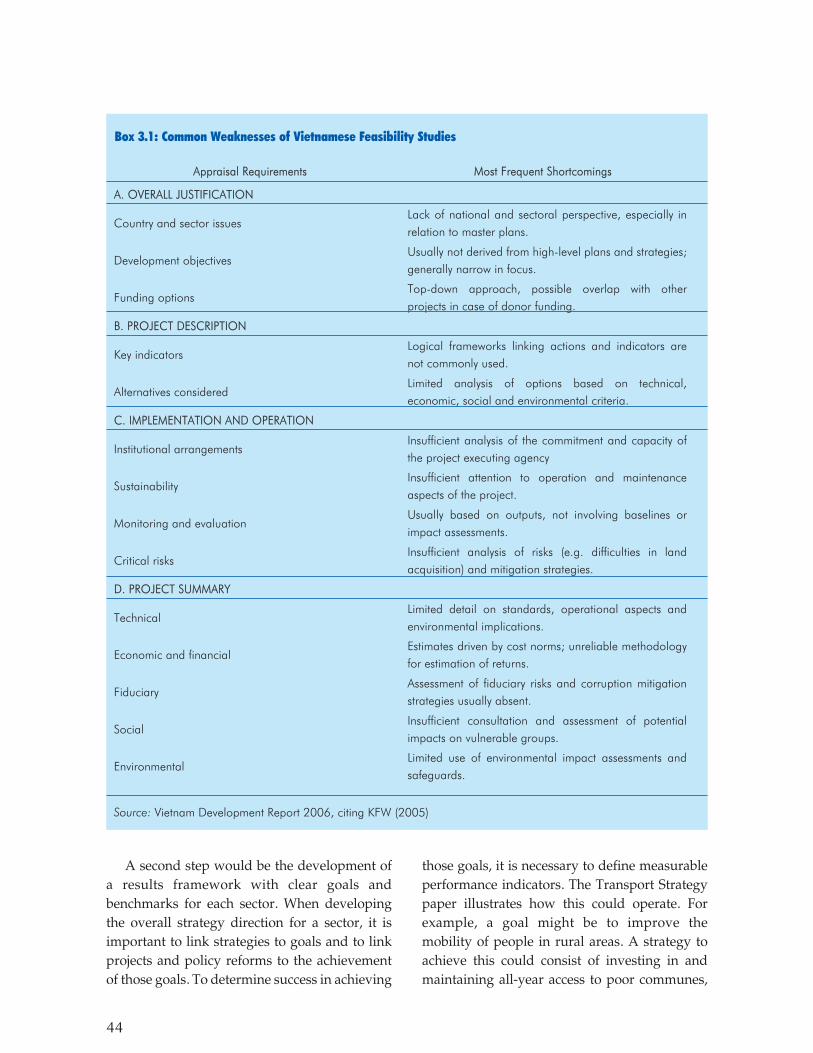

Better processes need to be developed forassessing investment priorities across sectorsand across projects. Ideally this would entailestimation and monitoring of rates of return,permitting an ordering of projects that could beachieved within financing constraints. A seriouseffort to build capacity in assessing economicand financial rates of return will take time. Inthe short term, a high priority should be toimprove the quality of feasibility studies,providing decision-makers with betterinformation about the relative merits ofproposed projects.

Progress is being made in relatinginvestment plans to development goals - theprinciples of the Comprehensive Poverty

Reduction and Growth Strategy (CPRGS) havebeen integrated into the Socio-EconomicDevelopment Plan for 2006-2010. But the linkbetween Vietnam's socio-economicdevelopment goals and investment planningcould be improved with the use of a resultsframework which specifies goals to be achieved(e.g. improve access to hygienic sanitation),strategies for achieving these goals (e.g.investment in sewerage systems in urban areas)and key performance indicators measuringprogress towards the goals (e.g. number ofurban households with sewerage connection).The goals should be comprehensive, andprojects would only be approved if theymapped into the strategies. An increasedemphasis on monitoring project outcomes isalso required, to inform future feasibilitystudies about the likely impact of differenttypes of investments, and to ensure thatprogress towards development goals is reallybeing made.

With improved criteria for distinguishingbetween projects, a framework within which toconsider projects' potential contribution todevelopment goals, there will then be a need fora governmental process that is capable ofallocating funds to the highest priority projects,with lower priorities receiving funding only tothe extent of available funding. Projects thatcould be financed privately should be given lowpriority for receiving public funding.

Budgeting processes need to be betterintegrated with investment planning. There hasbeen a problem with budget discipline in thepast, with transport projects being commencedwithout budget financing authorization.Questions are also raised about whether anappropriate balance is being struck betweennew investment and maintenance, particularlyin the transport sector. The Transport Ministry'srecent experience with preparation of budgetproposals within a medium-term expenditure

xii

framework (MTEF) has been a usefuldevelopment in terms of fitting proposedinvestments within the available financingenvelope and giving greater consideration tomaintenance costs. The MTEF experience shouldbe developed to extend to non-budget financesources, and to provide better information aboutthe trade-off between new investment andmaintenance (ie the relative rates of returnearned by spending in these areas).

Planning for Urbanization

Vietnam's urban population is growing by aboutone million people per year, with much of thatgrowth concentrated in Ho Chi Minh City andHanoi. It is likely that growth of Vietnam's ruralpopulation will level off in the next five to tenyears, with all new population growth beingexpressed as larger urban populations. Based onChina's example, urban growth will present arange of new problems including trafficcongestion, pollution, and the need to roll outinfrastructure services quickly. It is much moreexpensive to provide infrastructure services after

Urban planning is poorly managed atpresent. Centrally prepared spatial plans setunrealistic standards, and partly for this reasonare frequently ignored in practice. There needsto be more flexibility in centrally developedspatial plans, and more enforcement of thoseplans at the local level. Ideally spatial planningshould be devolved to a more local level, toenable greater responsiveness to localcommunities' desires and marketdevelopments. Arrangements under which landis provided to property developers in return forinfrastructure provision should be carried outthrough more transparent procedures involvingcompetition to mitigate potential risks forcorruption, land speculation, or wastedinvestments. Revised tax and fee instruments,such as property taxes, should be studied for

their potential to provide infrastructure moreefficiently and in closer synchronization withcommunity needs.

The need for more refined appraisals ofrates of return to different investments extendsto an assessment of the spatial balance ofinvestments. Vietnam has done well over thepast decade, balancing high-return investmentsin major centers of economic activity with ruralinvestments aimed at reducing poverty, andachieving high aggregate growth with only aslight increase in inter-provincial inequality.But migration to major urban centers has beenimportant in restraining inter-provincialinequality. Continued migration mayoverwhelm planning capacities in the majorcenters resulting in congestion, inadequateprovision of basic services, and environmentaldegradation. One response would be toprovide much more resources to urbanplanning in the major cities. An alternativewould be to divert migration to mid-sizedcities, but this would require wide-rangingpolicies extending beyond mere spatial andsectoral master plans. Assessing whether suchpolicies might be worthwhile would requiremuch better information about the relativesocial rates of return across different urbanareas.

Other Planning Challenges

There are general problems of coordinationacross government ministries. The need forbetter coordination between the Ministry ofPlanning and Investment and the Ministry ofFinance is a key area for better coordination, butthere is also a need to better coordinate spatialplans and sectoral master plans, particularly inurban areas.

Greater effort needs to be made to integrateenvironmental issues and assessments of socialimpacts (particularly resettlement issues) into the

xiii

overall planning environments. Whileenvironmental impact assessment may occur forindividual projects, plans for a series ofinvestment projects similarly need to be subject toassessment. While individual projects may haveonly marginal impacts, and thus be approved, theaggregate effect of a series of projects may bemuch larger, and require modification ofinvestment plans. Recent legislation requiringstrategic environmental assessments -assessments of the most critical environmentalissues in particular areas - is a positive step,

The process of decentralization is ongoing,with a gradual reallocation of spending andinvestment planning responsibilities from thenational government to provincial and localgovernments. Decentralization brings variousrisks of failure to coordinate between lower levelgovernments (eg failure to take account ofenvironmental effects on neighbors, or failure tocoordinate investments). There is a need for thecentral government to develop fiscal tools (suchas matching grants) that would help to coordinatesub-national decisions with national objectives.

3. Efficiency

In general, Vietnam's infrastructure services areprovided relatively efficiently. But as in allcountries, there is room to reduce the costs ofservice. Internationally, experience has been thatthe key to lowering costs is to increase thecommercial focus of infrastructure business entities- through reform of state-owned enterprises ordirect private investment - and the introduction ofcompetition. The sorts of reforms necessary toimprove commercial focus are also the sorts ofreforms needed to increase infrastructureenterprises' access to financial markets.

State-Owned Enterprise Reform

Central to improving efficiency is agovernance structure that improves the focus

on the commercial objectives of increasingrevenues and reducing costs. Internationally, atypical first step towards improvingcommercial incentives is "corporatization" ofbusiness enterprises - subjecting them toprivate corporations law. In Vietnam,subjecting infrastructure enterprises to theproposed Unified Enterprise Law may help toinstall the basics of corporate governance andshould be a minimum step. Additionalpossible measures include specific statementsof corporate objectives, and additionalreporting beyond that required by theEnterprise Law. Governments typically haveadditional non-commercial goals for theirinfrastructure enterprises, and these can beachieved by explicit contracting between theGovernment and the enterprises, withpayment for particular services provided.

Equitization, the sale of shares primarily toworkers and managers, has been used as a toolfor efficiency improvement in many state-owned enterprises in Vietnam. However, theworker motivation incentives that have beeneffective in smaller enterprises may be weakerin large infrastructure enterprises, where thereare greater possibilities to profit from the effortsof others (free-riding). Accordingly, it isimportant that equitization of infrastructureenterprises should involve sales of controllinginterests to general investors, and that it besupplemented by mechanisms to providestronger management incentives, such as stockexchange listing.

The agenda for state-owned enterprisereform varies across sectors. For example,the Ministry of Transport has over 200 SOEs,of which over 100 are engaged inconstruction. Many of these enterprises areexcessively indebted. Competition betweenthese enterprises results in low "survival"bids to secure contracts, a practice whichultimately results in low quality works anddelayed implementation. In a fully

xiv

developed market economy, this situationmight be resolved by bankruptcies of theleast efficient enterprises. But state-ownership tends to delay such politicallydifficult decisions. MoT has plans forequitization of SOEs, but these need to beaccompanied by clear guidelines on debtaccounting, and criteria under which certainenterprises might be declared bankrupt.

In the electricity sector, in contrast, thereform of state-owned enterprises is focused onthe transition to a future competitive market forelectricity. EVN will need to be broken up intotruly separate corporations. Decisions on thesize, structure and operational scope of newlyformed shareholding companies need to ensureadequate competition in different marketsegments, but also adequate resources to ensurefinancial viability. Distribution companies, inparticular, need to have sufficient financialstrength and managerial capacity to beperceived as credible and make long-termcontracts with generating companies.

In the water and sanitation sector, theagenda for SOE reform needs to focus onpreparing the utilities to access financialmarkets. For example, financiers are likely tohave more confidence in the credit-worthinessof water utilities if their accounts are preparedaccording to international accounting standardsand are independently audited.

Competition

Competition is the economic force most likely todeliver sustained efficiency improvements. Butthe possibility to introduce competition islimited in most infrastructure industries.Telecommunications and electricity generationare exceptions.

In telecommunications internationalexperience strongly suggests that the speed ofnetwork rollout is accelerated by greater

competition. Several new entrants have beenauthorized to compete with VNPT in fixed lineand mobile services, but VNPT remainsdominant. Effective regulation, in particularspectrum management and resolution ofinterconnection disputes, will be important infacilitating the progress of the new entrants.Faster progress could be made by allowing theentry of foreign firms. In this respect, the UnitedStates has obtained an early advantage, obtainingpreferential access for its firms under a BilateralTrade Agreement. But even these advantageslimit foreign ownership to 49% and 45% in themobile and fixed line services markets. Theselimits may unnecessarily inhibit market entry.

The 2004 Electricity Law and 2006 Road Mapfor Power Sector Reform set out plans for aphased transition over 20 years to directcompetition in electricity generation, witheventual choice of generators for consumers.There are various obstacles to the implementationof these plans, including the difficulty ofencouraging private investment in IPPs (a majorsectoral priority) when the future marketstructure is uncertain. Managing the transition toa competitive electricity sector will be one of themost difficult policy challenges in infrastructure.

Private participation

In most other infrastructure sectors,competition can only be introduced in the formof "competition for the market": competitivebidding among private investors for a the rightto provide an infrastructure service over a fixedperiod of time. Done well, with well-preparedcompetitive bidding and appropriateregulatory environments, concessions, leases,and management contracts can be strong toolsfor performance improvement as well asinvestment financing.

Vietnam already has experience in the useof BOTs, but at least some of the existing

xv

xvi

BOTs have been negotiated with a preferredoperator. Competitive bidding would providea higher probability of minimizingprocurement costs. A number of BOTs havebeen negotiated with state-ownedconstruction companies. While local financinghas advantages in terms of foreign exchangerisks, the use of foreign enterprises withspecialist infrastructure experience couldprovide more ideas for managementimprovement and utilization of newtechnology. And a difficulty with state-ownedenterprises is that weak governancestructures may provide weak commercialincentives. There is scope for greateropenness toward foreign private enterprisesin infrastructure investment. Vietnam iscurrently revising its BOT decree. A reviseddecree should entrench a requirement forcareful preparation and competitive biddingof BOT contracts.

Beyond the construction of new facilities,various forms of public-private partnershipscan help to improve efficiency of existingfacilities. Vietnam should conduct pilot projectsacross different sectors to gain experience in theuse of public-private partnerships other thanBOTs. An effective process would entail apipeline of projects, and a dedicated unitassociated with the development of public-private partnerships.

Regulation

One form of light-handed regulatory pressurefor efficiency improvements is benchmarking.Vietnam has made significant progress inbenchmarking water utilities, encouragingbetter performance by highlighting wellperforming companies that serve as examplesfor others. This experience could be copied insome other infrastructure sectors, for exampleurban environment companies, port operators,

or electricity distribution operations. Greaterattention to international benchmarking couldalso be used as a spur to improvedperformance.

More generally, performance standards andregulated prices, in addition to theirimplications for investment and financing, canbe used as tools to improve infrastructureservice performance. This is more likely to beeffective in infrastructure enterprises withstronger commercial focus, such as privatefirms. Getting prices right is a complex task,requiring specialist skills.

Regulatory institutional and capacity buildingis required, especially in the areas of cost auditingand economics (to set prices at efficient levels). Ahigh priority is support for the newly establishedElectricity Regulatory Authority, since lessonslearned here will have implications for othersectors. In the telecommunications sector, theMinistry of Post and Telematics' ownership ofVNPT creates a conflict of interest in itsregulation of the sector, for example in theresolution of disputes over access to VNPT'snetwork by new operators. An agencyindependent of the Ministry would be desirable.

Addressing Corruption

Corruption raises the final costs ofinfrastructure services, and is a source ofinefficiency. Opportunities for corruption ariseat most stages of the infrastructure project cycle.In recent years Vietnam has been makinggreater efforts to address corruption. Recentreforms have focused on detection andpunishment, but have been of generalapplication. Closer review could identifyparticular infrastructure activities at risk, anddevelop appropriate responses. Reforms toincrease competitive pressures in infrastructureare likely to complement measures againstcorruption, but should be buttressed by anti-

collusion measures.

4. Poverty

Road and water investments are good meansof targeting particular provinces in whichrural poverty levels are high, suggesting aneed to maintain high priority for theseinvestments.

Urban poverty is likely to increase incoming years. Because of the pace of migrationand urban development, addressing emergingurban poverty issues will requireimprovements in the local planning process toensure that infrastructure networks areinstalled "just in time", and in the right places.

There are many different ways of subsidizinguse of infrastructure services by the poor:● Currently, Vietnam uses increasing block

tariffs in water and electricity. While thedetails need to be studied carefully, suchschemes typically provide greater subsidiesto the relatively well-off, rather than thepoor.

● It would be useful to refocus subsidieson connection, rather than consumption,since those with connections aretypically less poor than those withoutconnections.

● Output-based methods for subsidy deliveryshould also be explored. A classic output-based scheme involves competitive biddingamong private operators for the right toprovide a service (encouraging costreductions in service provision), andpayment of the subsidy only when therequisite outputs have been achieved(transferring the implementation risk to theprivate sector).A general subsidy strategy should be

developed for infrastructure services,identifying whether subsidies are to bedelivered to the poor, and if so, how best tomaximize the benefits of those subsidies.

SECTORAL STRATEGIES

1. TransportFinancing

Transport expenditures reached 4.5% of GDP in2002, although 35% of this expenditure was notallocated budget funding and this in turn led toproblems of indebtedness in the sector. Incoming years, transport expenditure is expectedto be reduced to the order of 3.5-4.0% of GDP,although in a rapidly growing economy thisimplies continued increases in the absolute levelof transport expenditures.

ODA currently finances 37% of centraltransport expenditures. As in other sectors, theexpectation that ODA financing will not grow atthe same pace as GDP means that growingsector expenditure will need to be paid for byeither consumers or the Government. The scopefor direct user payments differs across sectors,but toll-roads are an obvious possibility forgreater direct payments. Fuel taxes (reducedsubsidies) would be a means of generatingadditional government revenue in a way that isrelated to use of infrastructure facilities. Anotheravenue would be to use land taxes to capture aproportion of the increase in land valueassociated with infrastructure improvements.

To ensure affordability of transport projects,the financing burden can be shifted to futuregenerations through government borrowing orby direct private investment. Around 30% of theMinistry of Transport's projects between 2001and 2005 were financed by government bonds,and local development investment funds(LDIFs) are also using bond financing toprovide transport projects in some provinces.The private sector could play an expanded rolein financing highways, ports and airports.

Planning and Coordination

All of the problems of planning and

xvii

coordination affecting infrastructure in generalcan be found in the transport sector. There tendsto be a gap between broad governmentstrategies and detailed sectoral plans, and littlecoordination between spatial and economicdevelopment plans. Poor budget discipline hasbeen the source of unfunded expenditures,giving rise to severe debt problems in thetransport construction industry. There ismisallocation between new investment andmaintenance; among modes, with inlandwaterways receiving a significantly smallershare of funding than is commensurate withtheir important role; and in the selection ofinvestments within each sub-sector.

The introduction of a results-oriented planningprocess at both the national and provincial levelswould help align expenditure planning with thedesired development goals. The ongoing MediumTerm Expenditure Framework (MTEF) pilotscould help remedy many of the problems in theplanning process by strengthening integratedplanning and developing investment plans withinthe envelope of available resources. Building onthe progress already made with the MTEF pilots isan important priority for the sector. Planningacross transport sectors needs to be betterintegrated, to ensure the development of multi-modal transport systems.

Rigidities in the planning system and thelack of metropolitan or regional institutions thatcan coordinate development acrossjurisdictional boundaries are obstacles to thedevelopment of effective urban transportsystems. Planning processes should encouragegrowth of high density corridors, and establishpublic transport systems to complementinvestments in road infrastructure.

Efficiency

Reform of the Ministry of Transport's State-Owned Enterprises is central to improved

outcomes in the sector. Frequently theMinistry's SOEs are over-indebted and deliverlow quality and delayed work. An equitizationprogram should be designed to close non-viableenterprises, to establish clear lines ofaccountability and improved commercialincentives for the remaining enterprises, and toprovide clear separation between Ministryfinances and enterprise finances. A furtherpossibility would be to remove ownership ofshares in the SOEs to a separate ministry, suchas the Ministry of Finance, to ensure no conflictof interest between the Ministry of Transport'spolicy role and the profit motives of shareownership.

Another important source of inefficiency isinadequate attention to road maintenance.Currently maintenance expenditures are at about50% of the necessary levels. If expenditures onnational road maintenance remain at their currentlevels over the next ten years, the condition of thenetwork would substantially deteriorate, withabout 34% of national roads being in poorcondition, including 55% of the high trafficvolume network.

Currently decisions about whether to paveprovincial and rural roads are distorted by biasin the Government budgetary system againstmaintenance. Knowing that regular budgetallocations are unlikely for ongoingmaintenance, many local governments prefer toconstruct paved roads which require lessongoing maintenance than gravel roads butwhich, depending on local circumstances, mayinvolve higher total costs over the life of theroad. The budgetary system should be revisedto ensure that decisions on road types can bebased on total life cycle cost - ie if on this basis agravel road is cheaper, then the necessarymaintenance budget should be provided.

There are many negative impacts oftransport, such as congestion, pollution, andhigh accident rates, which need to be better

xviii

xix

managed to improve the transport sector'scontribution to aggregate welfare. Efforts tocontrol congestion by limiting vehicleownership or registration in Hanoi and Ho ChiMinh City are not working. Alternativeinstruments, such as higher parking fees, andthe promotion of public transport systems mayprove more effective. Linked to congestion,both Hanoi and Ho Chi Minh City have airquality problems which could be at leastpartially addressed with improved vehicleinspections for emissions. A few relativelysimple measures, such as improved roaddesign and signage and police enforcement ofrules of the road, particularly the requirementfor motorcyclists to wear a helmet, couldsignificantly improve road safety

Building Capacity

A long term capacity development frameworkshould address needs at three main levels: thepolicies and laws governing the sector (buildingon the findings of a recently completedregulatory review); organizationaldevelopment (including stronger separation ofresponsibilities for policy development,enforcement of rules, implementation ofprojects, and operation of services), and humanresource development (training).

Implementation of project works has oftensuffered from inefficiency and low quality.Recent events have also highlighted problemsof governance in relation to projectmanagement units (PMUs). The respective rolesof PMUs, contractors, and supervisionconsultants need to be reviewed.

2. ElectricityFinancing

The capacity of Vietnam's electricity systemneeds to double in just five years, to meet

demand growth projected at 16% per yearduring 2006-2010. While demand-sidemanagement must be pushed as hard aspossible, the main solution lies in a large-scalemedium-term capacity expansion program. In2004 it was estimated that generation capacitywould need to expand from 11,000 MW at thetime, to 24,000 MW by 2010. More recentforecasts suggest this was an under-estimate.Annual power sector investment requirementsduring 2005-2010 are expected to cost over US$3billion.

The three main financing options for thesector are self-financing by EVN using retainedearnings, different types of borrowing, andindependent power investment. EVN exhibitedstrong financial performance during 2002-2004,permitting a substantial self-financingcontribution to the investment program. EVN isalso making extensive use of borrowing, fromdonors and by issuing bonds.

But increases in average retail tariffs arerequired to ensure an expanded contributionfrom self-financing and borrowing. Recent costincreases, stemming in part from powershortages in 2005, of themselves would requiretariff increases. The massive borrowing needswill also require counterpart funds from EVN tobe generated in the next few years, throughtariff increases.

EVN's purchase of power from sourcescurrently independent of EVN, including bothIPPs and imports, is expected to account formore than -half of new power productionduring 1995-2010. New IPPs wholly owned byforeign or private firms are expected to provideseveral thousand megawatts of new build-own-transfer (BOT) IPP capacity. Use of competitivebidding is strongly recommended as thestandard method for awarding new IPP powerpurchase agreements. International experiencehas been that prices and terms awardedthrough competitive bidding have providedlower costs than negotiated deals.

xx

Planning

Vietnam has established a good foundation forthe coming massive capacity expansion programwith the development of the Sixth Power MasterDevelopment Plan, covering 2006-2015, with aview to 2025. The basic institutionalarrangements, analytical capacity and analyticaltools being used are fundamentally sound.

The new Plan emphasizes expansion of allthree electricity generation subsectors - hydro,coal, and gas. Imports from China and otherneighbors are expected to increase considerably inthe future. Demand-side management should playa greater role than in the past - for example shiftingconsumption from peak times can significantlyreduce system capacity requirements.

Ongoing work will be required to ascertainthe optimal balance between coal-fired and gas-fired power plants. A central issue is the relativeeconomic costs of coal and gas - in particular, thecurrent price of coal in Vietnam appears todiverge substantially from its economic value -and this should be carefully reviewed beforesignificant investment in either sector. Greaterinvestment in exploration for gas and gas fielddevelopment will be needed in the longer term,and it is critical for Vietnam to further developthe framework for investment to ensure itremains attractive for international companies

More attention needs to be given to social andenvironmental issues in the planning process.For example: major hydro developments caninvolve significant resettlement and socialdislocation; the choice between coal- and gas-fired power plants has implications for carbonemissions; and siting of power plants andtransmission facilities must be planned withregard to local environmental effects.

Efficiency

The Electricity Law of 2004 and the recently

approved sector Road Map set the direction formajor efficiency improvements through theintroduction of competition in the powerindustry. The reform process is expected tospan twenty years, proceeding through (a)operation of a competitive market for supplyfrom generators to a Single Buyer (EVN); (b)introduction of a wholesale market, allowingbilateral between large consumers andgenerators; and finally (c) introduction ofcompetition at the retail level.

To implement these reforms, EVN will needto be broken up into truly separatecorporations. The model of EVN as a holdingcompany for assets in generation, transmission,and distribution cannot be retained if truecompetition is to be achieved. The corporaterestructuring and equitization involved will ofitself be a significant challenge. Resultingcompanies need to be strong enough to beactive market participants, but should not wieldexcessive market power. In particular,distribution companies need sufficient scale tobe reliable revenue collectors and powerpurchasing agents.

A further implication of the reforms is thatgreater flexibility in retail pricing will need to beintroduced over time, including mechanismswhich allow changes in costs to be passedthrough to consumers, and for consumers torespond.

The approved reforms could be improved bybringing forward at least some directcontracting between generators and largeconsumers and/or distribution companies. It isthis form of competition which is likely to yieldthe main efficiency gains.

A major challenge to the reform will be theexisting tight reserves in the system. In a marketsystem, supply shortages lead to high prices, assignals to induce more investment. It can takeseveral years for new capacity to come on lineand lower prices, during which politicalsupport for reform could be undermined by the

high prices. Alternatively, if prices are kept lowby regulation, additional investment may not beforthcoming from the private sector.

A linked challenge is the need to expandprivate investment. With Vietnam's limitedexperience of international investment in IPPs,there is a need to offer great certainty topotential investors about their future returns.Uncertainty over the nature of future marketdevelopments will increase the perceived risk ofIPP investments. The key here is to design thepower market to mitigate these concerns. Forexample, emphasis may be given in the marketdesign to cover load primarily with contracts,and limit spot trading to non-contractedsurpluses and to clearing differences.

Building Capacity

Existing planning strengths need to besupplemented with greater institutionalcapacity in demand-side management.

Managing the task of competitiveprocurement of a large pipeline of IPP projectswill pose considerable challenges for theMinistry of Industry, requiring much learningfrom international experience and building upof capacity in preparing 'bankable' transactions.Experienced international advisers will be anecessary element of this program, but there isa corresponding need for capacity on theGovernment's side to manage these advisers.

Linked to the reform program, there is aneed for an expansion of regulatory capacity.The Electricity Regulatory Authority ofVietnam was established recently. It needs to bean objective institution, charged withimplementation of the country's laws, with amandate recognized by all parties, andoperating as an agency separate from theMinistry of Industry's regular businessdepartments. Some areas for ERAV's earlyattention include: (a) establishment of itself witha distinct identity; (b) definition and publication

of a clear work program; (c) staff training anddevelopment; (d) agreement with industryparticipants on arrangements for informationcollection and monitoring; (e) definition ofERAV's enforcement powers; and (f) definitionof mechanisms for resolution of disputes.

3. Water and SanitationFinancing

Investment needs to meet the VietnamMillenium Development Goals in rural andurban water and sanitation by 2020 areestimated at US$ 600 million annually, which isroughly four times the annual investment in thelast ten years. Allowance can be made for agrowing economy, but even as a proportion ofGDP investment in the sector would need todouble, from 0.6% to 1.2%, by 2010. Moreover,nearly 85% of past investment in the sector hascome from ODA, which is unlikely to expandsignificantly in coming years.

Meeting the Government's developmenttargets will require greatly expanded financingfrom either the government or throughborrowing in the capital markets. Forborrowing to occur, the utilities would need togenerate operating surpluses to meetrepayment obligations, which would in turnrequire increased user fees and increasedefficiency of service providers.

One of the keys to the success of the sector ishigher but realistic and affordable tariffs. JointCircular 104 of November 2004 requires thattariffs be set to fully recover costs, which is animportant step in the right direction, butenforcement of the Circular remains an issue.The possibility of automatic indexation of tariffsto match cost increases should be considered.For wastewater, the Government should reviewCircular 67 (2003), which is perceived by localgovernments as a cap on wastewater fees at 10%of water tariffs. Wastewater operations andinvestment typically cost more than equivalent

xxi

water services, and the need for cost-coveringtariffs in the sector is the same.

As the creditworthiness of the sectorimproves, access to longer term local financingwill become important. A staged progressioncould be envisaged over the next 10 years fromcurrent reliance on ODA, through mixedfinancing, to a sector built on local capitalmarkets. Greater access to ODA funds could beprovided to utilities that are able to borrowfrom financial markets, as a means ofencouraging additional finance into the sector.Pilot projects will be required to develop credit-worthy utilities, and to develop capacity on thepart of banks or other financial institutions forloan appraisal. The Government orinternational financial institutions could play arole initially in providing some form ofguarantee to early commercial loans to thesector, in order to build confidence, but suchguarantees should not be seen as a permanentfeature.

Importantly the Government shouldconsider how best to utilize ODA. GraduallyODA should move away from production todistribution, from water supply to sanitationand from investment funding to leveraginglocal capital. Better targeting of ODA to reducepoverty will be important and Output BasedAid (ODA) should be considered as amechanism for the use of grant financing forpoverty interventions.

Planning and Coordination

Over the long term the government shouldconsider rationalizing into one entity thevarious line agencies that are currentlyresponsible for policy and oversight of waterand sanitation in the urban and rural areas. Inthe meantime the existing legal frameworkneeds to be upgraded to support the NationalRural Water and Sanitation Strategy. Inaddition the sector policy/regulatory role of

CERWASS should be more clearly separatedfrom its role as service provider.

Efficiency

Overall, Vietnam's water utilities areperforming well by developing countrystandards. But there remains wide variationbetween utilities in the costs of service andcommercial performance, suggesting significantroom for improvement for many utilities.Possible measures for improving performanceof the utilities include:● More widespread knowledge about the top

performing water companies andbenchmark capital and operating costs. Theexisting benchmarking system could beimproved and made available more widely,to be used by provincial governments andpotential private investors for cross-sectoralcomparison, and by utility managers tohighlight areas for improvement.

● Policies to provide incentives to watercompanies to achieve higher levels ofperformance. A system of incentivesrequires a strict evaluation of performanceand the use of rewards and sanctions whichaffect both the utility and its owners. As afirst step, performance contracts could beestablished between individual ProvincialPeoples Committees and their serviceproviders, with rewards/sanctions forperformance against agreed targets. In thecase of poorly performing water servicecompanies, PPCs could choose tocompetitively bid unserved district towns tonew water supply service companies.

● Competition between water servicecompanies could be also simulated, withrewards (eg greater access to Ministry ofConstruction finance, or donor finance)for companies that meet agreedperformance targets, or are the bestperforming companies in the country, or

xxii

that show the greatest improvement inperformance.

● The country should continue to encouragethe involvement of the private sector as aspur for efficient service delivery, andpossibly as a source of investment financing.The national private sector has a distinct roleto play in providing services to smallertowns and in the rural setting.

● Improved regulation. At present provincialgovernments are effectively both tariffsetters and owners of water servicecompanies, creating a conflict of interestbetween the goal of keeping tariffsaffordable for consumers, and the goal ofprofitable operation of the companies. Anational oversight agency (nascentregulator) could be established to provideadvice/guidance to Peoples' Committees ondesign of performance contracts, andexpected performance of water servicecompanies.

● Focusing on core businesses. Water servicecompanies should divest their constructionand other services from the water business.This would provide the basis for thedevelopment of a competitive market forconstruction services and reduce theopportunity for hidden cross subsidies.Progress on sanitation services is lagging

well behind water services. Establishingbusiness entities responsible for the provisionof sanitation services is the immediate priorityin sanitation reform. Merging wastewateractivities into the business of urban waterservice companies, to take advantage ofoperating and administrative synergies, shouldbe considered in all but the largest cities, whereseparate wastewater companies may beappropriate. The Government should continueto support soft interventions which highlightthe linkages between sanitation, improvedhygiene practices, and health outcomes, andbuild demand for investments in sanitation.

Building Capacity

The provision of incentives to service providerswill only be successful if there is adequateinformation about the sector, and there isadequate capacity to respond to thatinformation in both service providers andoversight agencies. In particular a sanitationstudy is required to develop and keep updatedcomprehensive and reliable data.

The Government needs to be more active incompiling, analyzing and disseminating sectordata. Through such activity the Governmentcan build its capacity to improve policydevelopment and the targeting of ODA funds.

The Peoples Committees need to improvetheir understanding of the opportunities forsector development and how they can benefit.National agencies should take a lead in theprovision of training in introducing andmaintaining commercial relationships, andeffective corporate governance and oversight.

The Vietnam Water Supply Associationcould play a bigger role in building technicaland managerial capacity in service providers. Acoordinated action to reduce non-revenue waterand improve energy efficiency could yieldsignificant benefits. Training for small-scaleproviders should be offered to enhance theirmanagement and financial capability, andcapacity for quality control, contract andcontractor management.

4. TelecommunicationsFinancing

In October 2005 the Ministry of Post andTelematics adopted a target of 32-42telephone lines (fixed plus mobile) per 100population by 2010. The investment requiredto meet this target, given the current level ofabout 20 per 100 population is about VND 57trillion (US$ 3.6 billion) spread over fiveyears. This compares with a total investment

xxiii

budget for VNPT in 2003 of aroundUS$ 313 million.

VNPT's main sources of profits - highlypriced leased lines and international calling -will be reduced as competition is increased, soself-financing of investments will be reduced.New sources of finance will need to bedeveloped. Possible sources of finance couldinclude bonds or issuance of shares. Currentbusiness cooperation contracts (BCCs) withforeign telecommunications companiesgenerate hundreds of millions of dollars ofinvestment, but the restrictions on this sort ofinvestment (such as the absence of managementrights for the foreign investor) means thatbillions of dollars of private investment throughBCCs is unlikely. A move to true joint ventures,desirably with the possibility of majorityprivate ownership, management control rights,and equity returns, would be likely to generatehigher levels of investment.

Following international experience, there isgreat potential for increased direct privateinvestment, domestic and foreign, in the sector,but this would require major improvements inthe regulation and operation of the sector. Thereforms required to encourage privateinvestment are broadly the same as thoserequired to increase access and improveefficiency.

Planning

Market forces, appropriately regulated, couldachieve most of the government'stelecommunications objectives, without theneed for detailed planning of investments andoperations by the Government. To arrive atsuch a position a wide range of policy reforms isrequired to increase access and improveefficiency.

At present there is no roadmap for policychange. Plans and decrees tend to beengineering documents or penetration goals,

not well-thought-out mechanisms using policychanges that reflect international best practice.There is a need for more policy planning andlinking processes and policy changes toanticipated results. Part of this process shouldbe the development of a moderntelecommunications law that the WTO,international best practice, and investors wouldrecognize as a model.

One area where market forces couldpotentially be supplemented with centralplanning is rural access. On this subject, regardshould be had to the WTO Reference Paper,which states that although WTO members mayundertake any universal service obligation(USO) regime they like, the USO scheme mustbe administered in a transparent, non-discriminatory and competitively neutralmanner.

Improving Access and Efficiency

The major priority for the sector should be tointensify and entrench competition in the sector.Competition provides positive incentives forincreased productivity and responsiveness tocustomer needs. Internationally, strongercompetition has also been linked to fasterexpansion of access to telecommunicationsservices.

Many elements are needed to promotecompetition. A clear vision of a future industrystructure needs to be devised and disseminated.This structure should have several viableoperators, each totally independent of eachother, and all subject to impartial regulation.VNPT's multiple ownerships in every marketsegment, particularly mobile telephony, shouldbe eliminated. VNPT's equipmentmanufacturing, postal and postal girobusinesses should be separated from thetelecommunications businesses.

Another key element of achievingcompetition and private entry is licensing. The

xxiv