vey | birmingham€¦ · local effect: norfolk southern selected birmingham to develop one of the...

TRANSCRIPT

I N D U S T R I A L M A R K E T S U R V E Y | B I R M I N G H A M

2012

GRAHAM REPORT • 2012 1EXECUTIVE SUMMARY

GRAHAM REPORT • 2012

GRAHAM REPORT/2012BIRMINGHAM, ALABAMA

Cover: Aerial photograph of Norfolk Southern Intermodal Facility, McCalla, AL – Alabama Air Foto

Copyright 2012. Reproduction, in whole or part, of this report is prohibited.

TABLE OF CONTENTS

EXECUTIVE SUMMARY . . . . . . . . . . . . . . . . . . . . . . . 1

COMMENTARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

INDUSTRIAL GROUP . . . . . . . . . . . . . . . . . . . . . . . . 4

CENTRAL. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

OXMOOR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

WEST . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

SOUTH . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

BUILDING LOCATIONS (CITY MAP). . . . . . . . . . . . 19

EAST . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

INDUSTRIAL BUILDINGS. . . . . . . . . . . . . . . . . . . . 27

FOR SALE OR LEASE. . . . . . . . . . . . . . . . . . . . . . . 28

GRAHAM & COMPANY ACTIVITIES/2011. . . . . . . 35

GRAHAM TEAM . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Graham & Co also publishes the annual Birmingham Offi ce Market Survey.

Information deemed reliable, but not guaranteed.

OVERVIEW: Start – Sputter – Resume

EXECUTIVE SUMMARY 2

The 2011 year kicked off with an improved pace of transactions and demand only to slow in mid

summer. Th e 4th Quarter resumed with improvements in demand as we slowly worked our way through the overhang of inventory. Th e higher quality products tended to have the greatest appeal and several of our long term vacancies are now full. Th e recovery con-tinues, but it will be well into 2012 before we see any chance of new development. Some build-to-suit projects were tempting developers in the closing months of 2011.

Infl ation rates remained low, and interest rates were in step. Rental rates remained depressed, although new deals were factoring modest annual infl ation into the rents. Th ree to fi ve year terms continued as the norm;

longer term commitments commanded strong incen-tives from the Landlord.

Positive absorption was noted for 2011 in all sectors with relatively strong positive movement in Bulk Dis-tribution. Overall occupancies increased from 2010 and were strongest in the West and South submarkets.

Boosted by new construction, the market for free-standing, typically owner-occupied, buildings contin-ued a strong showing in 2011 with over one million sf of positive absorption. Th is market sector stood alone in a state of balance between supply and demand. Other property segments were in a state of oversupply as we closed out 2011. Th e smallest property type, service center, did fi nish in a balanced state with 42,000 sf of positive absorption.

A slow recovery continues in our industrial markets, and 2012 should see increased activity. We look forward to improved market conditions. We take this opportu-nity each year to thank our associates, our clients and our colleagues for their support and best wishes for a good 2012.

Yours truly,

ALL AREASFREESTANDING

INDUSTRIAL BLDGS.TOTAL MULTI-TENANTWAREHOUSE MARKET

BULKDISTRIBUTION

OFFICE/WAREHOUSE

SERVICECENTER

Occupancy Rate 94.6% 82.5% 82.5% 80.1% 89.8%

Status Balanced Oversupply Oversupply Oversupply Balanced

Available Space 4,976,000 2,817,000 2,136,000 583,000 98,000

Total Market 92,890,000 16,075,000 12,181,000 2,937,000 957,000

Average Rate –– –– $3.76 $6.17 $11.47

New Space Rate –– –– $4.50 $6.75 $12.00

Absorption: 2011 1,019,000 259,000 197,000 20,000 42,000

2010 898,000 109,000 301,000 (130,000) (62,000)

2009 (382,000) (327,000) (232,000) (96,000) 2,000

2008 1,361,000 (141,000) (206,000) (11,000) 75,000

2007 798,000 815,000 591,000 159,000 65,000

Annual Absorption:

5 Yr. Avg. (2007-11) 738,800 143,000 130,200 (11,600) 24,400

Steve and Mike GrahamGraham & Company, LLC

GRAHAM REPORT • 2012 3

Ahum is coming from the western side of our great city. Giant earth movers are shaping a former pasture along the Norfolk Southern rail

line into a 350-acre Regional Intermodal Facility, otherwise known as “Th e Hub”. Th e Birmingham community is excited about the upcoming benefi ts from this huge investment in infrastructure.

National Impact: Th e importance of rail in distributing goods across America cannot be underestimated. Th e transfer of the ubiquitous shipping container is now a major economic driver along the main lines of railroads near important cities nationwide. Th e hubs serve as inland ports to move goods into the interior of our country, and away from the expensive and congested seaports.

Th is trend portends well for America’s future. One of our nation’s strengths is its infrastructure system of interstates, intercoastal waterways, and railways. Highly effi cient distribution systems have a direct eff ect on profi ts. Railroads are an increasingly important component of the overall distribution equation. Th e railroad industry estimates its system is 5 times more effi cient than a single truck hauling one container.

Railroad companies have spent billions on upgrading tracks to include squaring off the upper edges of rounded tunnels to accommodate the double stack cars. Th e goal is to allow goods from ships to be brought closer to the markets. Th is trend has been at work for some time in the western U. S. and it is now spreading to the East Coast.

Local Effect: Norfolk Southern selected Birmingham to develop one of the largest hubs along its Crescent Corridor. Our city will be the fi rst major stop for goods coming up from New Orleans, in route through Virginia and eventually to New Jersey.

Th e expanded rail distribution enhances Birmingham’s role in import and export channels. From autos to steel to fi re extinguishers, this city is poised for exciting export opportunities, leading to a bright future for the industrial real estate market in Birmingham.

Mike Graham, CPM, SIOR Steve Graham, MAI, CRE

What Next for Birmingham?

Playing to Our Strengths

COMMENTARY

GRAHAM REPORT • 2012INDUSTRIAL GROUP 4

JORDAN W. TUBBASSOCIATE, INDUSTRIAL GROUP

JOINED GRAHAM & CO: 2007

AFFILIATIONS/HONORS:

• Member, Birmingham Association

of Realtors Commercial Real Estate

Club of Excellence, Rookie of the

Year Award 2008

• Member NAIOP – Alabama Chapter

• Member, Rotaract Club of Birmingham

CLIENTS INCLUDE:

• Applied Ultrasonics • Southern Comfort Conversions

• Unifi ed Design & Manufacturing • Tennessee Valley Metals

• Charter Communications • Ram Tool • AABCO Rents

• Superior Mechanical • Hackbarth Delivery Service

• Heritage Environmental Services • Marjam Supply Co.

• Sears Home Improvement Products • S & B Products, Inc.

JOHN COLEMANVICE PRESIDENT,

INDUSTRIAL GROUP

JOINED GRAHAM & CO: 2006

AFFILIATIONS/HONORS:

• CCIM, Certifi ed Commercial

Investment Member,

Current Candidate

• Member NAIOP – Alabama Chapter

Board Member & Program Chair 2006-2008

• Lifetime Member, Birmingham Association of Realtors

Commercial Real Estate Club of Excellence

• Children’s Hospital of Alabama Committee for the Future

• Eyesight Foundation of Alabama, Trustee

• Kiwanis Club of Birmingham

• National Multiple Sclerosis Advisory Council 2011

• Industrial Advisory Board – Xceligent

CLIENTS INCLUDE:

• Surmodics • CJ*GLS Logistics • DeShazo Crane • Durect

• Fleetpride • Georgia Pacifi c • US Steel

OGDEN S. DEATON, SIOR

SENIOR VICE PRESIDENT,

INDUSTRIAL GROUP

JOINED GRAHAM & CO: 1987

AFFILIATIONS/HONORS:

• Birmingham Association of Realtors

Top Commercial Producer Award:

2001, 2002, 2005, 2007, 2008,

2009, 2010

• Member NAIOP – Alabama Chapter

Broker of the Year 2008, 2009

• SIOR Industrial Specialist Designation 1994,

Chapter President 2007

• Lifetime Member, Birmingham Association of Realtors

Commercial Real Estate Club of Excellence, Vulcan Award 1998,

20-Year Award 2007

• Birmingham Business Journal “Top Forty Under Forty” Award

CLIENTS INCLUDE:

• BNSF Railway • C & S Wholesale • Georgia Pacifi c

• Rainbird • Wells Fargo • AT&T • Sony • Regions Bank

• Caterpillar Logistics • Thyssen Krupp • Goodyear

• O’Neal Steel • Stag Capital • Cascades Sonoco

JACK BROWN, SIOR

SENIOR VICE PRESIDENT,

INDUSTRIAL GROUP

JOINED GRAHAM & CO: 1996

AFFILIATIONS/HONORS:

• SIOR Industrial Specialist

• Member NAIOP – Alabama Chapter

President 2011

• Birmingham Business Alliance,

Board Member 2011

• Lifetime Member, Birmingham Association of Realtors

Commercial Real Estate Club of Excellence,

Vulcan Award 2006

• Industrial Advisory Board – Xceligent

CLIENTS INCLUDE:

• A.M. Castle & Co. • CSX Railroad • Ferguson Enterprises

• American Financial Group • Fuji Film • MacLean-Fogg

• Regions Financial • National Bank of Commerce • Cintas

• Conway Transportation • Waste Pro USA • Nucor Steel

SONNY CULP, SIOR

SENIOR VICE PRESIDENT,

INDUSTRIAL GROUP

JOINED GRAHAM & CO: 1986

AFFILIATIONS/HONORS:

• Birmingham Association of Realtors

Top Commercial Producer Award:

1994, 1995, 2000, 2001, 2002, 2004,

2006, 2007, 2009, 2010

• SIOR Industrial Specialist Designation 1992,

Chapter President 2001, Regional Director 2007

• Lifetime Member, Birmingham Association of Realtors

Commercial Real Estate Club of Excellence,

Vulcan Award 1999, 20-Year Award 2008

• Board Chair, Restoration Academy

www.restorationacademy.org

CLIENTS INCLUDE:

• Mercedes Benz • Norfolk Southern Railroad • Michelin

• Sysco Foods • Ford Motor Land • Isuzu Corporation

• Cardinal Health • Nabisco • Frito Lay • Graybar • UPS

• General Electric • BellSouth • Baxter Healthcare

GRAHAM REPORT • 2012 5CENTRAL

GRAHAM REPORT • 2012

Central(CBD, Southside, Airport, North Birmingham, Ensley, Avondale)

CENTRAL

The Birmingham market is separated for the purposes of this report into fi ve distinct market areas: Central, Oxmoor, West, South and East.

CBDCENTRAL

BULKDISTRIBUTION

OFFICE/WAREHOUSE

SERVICECENTER

TOTALMARKET

Occupancy Rate 81.9% 72.4% 94.9% 81.8%

Status Oversupply Oversupply Shortage Oversupply

Available Space 651,000 97,000 11,000 759,000

Total Market 3,600,000 351,000 215,000 4,166,000

Average Rate $2.93 $4.61 $10.41 ––

New Space Rate $4.75 $6.50 $11.00 ––

Absorption: 2011 (119,000) (31,000) 20,000 (130,000)

2010 54,000 (13,000) (20,000) 21,000

2009 (86,000) (31,000) 2,000 (115,000)

2008 (134,000) (7,000) 25,000 (117,000)

2007 (9,000) 24,000 (4,000) 12,000

Annual Absorption:

5 Yr. Avg. (2007-11) (58,800) (11,600) 4,600 (65,800)

The Central market is characterized by older complexes with a fairly rapid turn-over from new tenants whose businesses tend to either grow or go away. Other

tenants have made the CBD and its extensions home for generations. Th e Central market encompasses some 3.6 million sf, making it the second largest submarket tracked. Occupancy was down for 2011 at just below 82% with the market in a state of oversupply. Rental rates for Service Centers increased, but Bulk Distribution rates fell by 5.5% and rates for Offi ce/Warehouse remained fl at.

Aft er positive absorption for 2010, the pace slowed and 2011 posted negative ab-sorption of 130,000 sf, mostly in the Bulk Distribution sector, falling to its lowest occupancy since 2003.

New leases and/or sales of note for 2011 in this submarket included:• Shook & Fletcher leased 25,000 sf at Avondale Commerce Park.• UAB signed a lease for 90,000 sf at Sloss Docs – a baseball park relocation.

CENTRAL 6

GRAHAM REPORT • 2012 7

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

1Birmingham Food Terminal(EGS Commercial)

1,059,880 Finley Avenue, l-65 N19582003

Dock highDrive-in

Concrete tilt-up Yes 20' Yes 5% 2.95 81% 204,045 sf Available

2Continental Gin(Southpace Properties)

461,000 4500 5th Avenue So.1920’s& 1980

Dock highDrive-in

Block & Brick Yes20'–40'

Yes <5% 2.50Ind Gross

90% 46,166 sf Available

3BN Park(Graham & Co)

453,6112500–270013th Street W, Ensley

19661969

Dock highDrive-in

Concrete tilt-up Yes20'–26'

Yes 2% 2.50 68% 144,300 sf Available

4Airport Highway Park(Graham & Co)

312,1533500 to 3700 Airport Highway

1975, 19791981

Dock highDrive-in

Block,Concrete tilt-up

Yes 22' Yes 5% 2.75 95% 14,686 sf Available

5Doc’s Warehouse(Graham & Co)

209,816 3221 1st Avenue No.19521970

Dock high Concrete tilt-up Yes18'–22'

Yes 1% 3.00 63% 78,000 sf Available

6Avondale Commerce Park(EGS Commercial)

194,200 3900 1st Avenue No.19801991

Dock highDrive-in

Concrete block Yes 18' Yes 15% 3.50 100%

7Post Offi ce Annex(Graham & Co)

178,174 4500 1st Avenue So.19701984

Dock high Concrete tilt-up Yes 30' Yes 5% 4.50 100%Former McRae’sWarehouse

8Vanderbilt Distribution Ctr. (Graham & Co)

161,900 3340 Vanderbilt Rd.19622006

Dock high Block & Brick Yes17'–25'

Yes 5% 2.60 100%

9Roundhouse(Graham & Co)

116,963 Finley Avenue West19521960

Dock high Concrete tilt-up Yes 20' Yes <1% Neg. 0% 116,963 sf Available

108th Ave. Warehouses(Barber Companies)

101,000 3300 8th Avenue No. 1965 Dock high Concrete tilt-up Yes 20' Yes5%– 15%

2.95 100%

11Bermco(Watts Realty)

96,0005th Avenue No.& 32nd Street

1979Dock highDrive-in

Concrete tilt-up No 20' Yes 5% 3.00 100%

12Republic Industrial Park(Engel Realty)

63,000 Republic Blvd., Ensley 1975 Dock high Concrete tilt-up No 20' Yes 15% 3.25 86% 8,716 sf Available

133rd Ave. No. Warehouse(Barber Companies)

48,0002911-29233rd Avenue No.

1960Dock highDrive-in

Metal Yes 15' No Up to 10%

2.95 69% 15,000 sf Available

14Ferguson Warehouse(Sloss Real Estate)

42,000 2800 2nd Avenue So. 1968 Dock high Concrete tilt-up Yes 24' Yes 35% 3.50 100%

153rd Ave. So. Warehouse(Barber Companies)

35,000 3501 3rd Avenue So. 1955 Dock high Block & Brick No15'– 18'

No 10% 3.25 43% 20,000 sf Available

16Montcreek Distribution(Watts Realty)

24,00015th Street &3rd Avenue So.

1979 Dock high Concrete tilt-up No 20' Yes 5% 6.00 100%

17 4001 2nd Ave. So.(EGS Commercial)

22,500 4001 2nd Avenue So. 1975Dock high Drive-in

Block & Brick No 14' No 5% 3.00 100%

18Wahouma Space Center(EGS Commercial)

22,00065th Street &3rd Avenue No.

1979 Dock high Block & Brick No 14' No 5% 3.00 86% 3,200 sf Available

Multi-Tenant Survey/2012

Bulk Distribution (Over 20,000 SF)

CENTRAL

GRAHAM REPORT • 2012

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

6Avondale Commerce Park(EGS Commercial)

281,925 3900 1st Avenue No.1980, 1984

1988Dock highDrive-in

Concrete block No14'–16'

No 20% 5.00 69% 86,554 sf Available

19Graymont Center(EGS Commercial)

69,000Graymont Avenue &8th Street West

1978 Dock high Block No 14' No 10% 3.00 85% 10,500 sf Available

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

20White Dairy(Barber Companies)

86,000 2700 7th Avenue So. 1984 Dock high Concrete tilt-up No 18' No15%–100%

8.75 97% 2,875 sf Available

21University Park(Earl Ryan)

62,500 1200 3rd Avenue So. 1985 Drive-in Concrete tilt-up No 12' No 100% 9.50 87% 8,000 sf Available

22Arlington Business Center(Watts Realty)

45,000 1500 5th Avenue So. 1985 Drive-in Concrete tilt-up No 10' No50%–100%

16.00 100%

23Southside Business Center(EGS Commercial)

21,750 2501 5th Avenue So. 1984 Drive-in Block & Brick No 13' No 80% 8.00 100%

* See Building Location Map, pages 19-20. Properties listed in descending order by size. Rental rates are provided by building’s agent. All rates quoted are Net unless otherwise noted.

LEGEND Office Warehouse

Service Center (Over 50% Office)

Office/Warehouse (Under 20,000 SF)

8CENTRAL

GRAHAM REPORT • 2012 9OXMOOR

GRAHAM REPORT • 2012

This suburban market was originally confi ned to West Oxmoor Road, and the older warehouse products in this area have carried vacancies for multiple years.

Some of the market overhang began to be absorbed only to have more of this older product come on the market. Overall occupancy continued to fall for 2011 to under 80%, and the submarket continued in a state of oversupply. In a submarket where Landlords continued to struggle with low occupancy, rental rates for Bulk Distribu-tion remained fl at, and rental rates for Offi ce/Warehouse fell 11%. Negative absorp-tion was the story of the day for Oxmoor and a continuation of the soft conditions found here for the past four years.

New leases and/or sales of note for 2011 in this submarket included:• Merit Brass leased 33,000 sf at Oxmoor South.• Yale Carolinas (forklift division) leased 19,000 sf in the former Keebler warehouse.

Oxmoor(Oxmoor Road, West Lakeshore, Homewood)

OXMOOR

CBD

OXMOORBULK

DISTRIBUTIONOFFICE/

WAREHOUSESERVICECENTER

TOTALMARKET

Occupancy Rate 78.7% 72.9% 89.0% 78.1%

Status Oversupply Oversupply Oversupply Oversupply

Available Space 355,000 214,000 32,000 601,000

Total Market 1,663,000 791,000 291,000 2,744,000

Average Rate $4.21 $6.65 $9.89 ––

New Space Rate $4.75 $ 6.95 $12.50 ––

Absorption: 2011 (62,000) 8,000 21,000 (33,000)

2010 (21,000) (37,000) (8,000) (66,000)

2009 (161,000) (15,000) 3,000 (173,000)

2008 (71,000) (24,000) 3,000 (91,000)

2007 123,000 82,000 24,000 229,000

Annual Absorption:

5 Yr. Avg. (2007-11) (38,400) 2,800 8,600 (26,800)

OXMOOR 10

GRAHAM REPORT • 2012 11

Multi-Tenant Survey/2012

Bulk Distribution (Over 20,000 SF)

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

24Oxmoor South Industrial Pk.(EGS Commercial)

528,430 Oxmoor Court1990, 1992

1994Dock highDrive-in

Concrete tilt-up No24'–27'

Yes 5% 3.75 84% 85,400 sf Available

25Distribution Center(Graham & Co)

515,000Distribution Drive,West Oxmoor

1973Dock highDrive-in

Concrete tilt-up Yes 20' Yes 2% 4.50 74% 132,175 sf Available

26Lyon Lane(Graham & Co)

196,120240 Lyon Lane250 Lyon Lane260 Lyon Lane

199819991999

Dock highDrive-in

Concrete tilt-upMetal

No 22' Yes 5% 4.15 75% 48,600 sf Available

27Shades CreekBusiness Park(EGS Commercial)

195,841 Shades Creek Circle 2000Dock highDrive-in

Concrete tilt-upMetal

No24'–25'

Yes 5% 3.95 100%

28Birmingham #2(Graham & Co)

79,095Citation Court,Homewood

1982 Dock high Concrete tilt-up Yes 22' Yes 3% 4.25 77% 17,900 sf Available

29Birmingham #1(Graham & Co)

78,000West Oxmoor& Snow Drive

1980 Dock high Concrete tilt-up No 22' Yes 25% 5.50 81% 14,625 sf Available

30Oxmoor South Building V(Barber Companies)

70,300 Oxmoor Court 1994Dock highDrive-in

Concrete tilt-up No 22' Yes 15% 4.95 62% 26,434 sf Available

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

31Oxmoor Center(Engel Realty)

151,300 131 West Oxmoor 1974Dock highDrive-in

Block & Stucco No 20' Yes25%–30%

7.00 68% 48,679 sf Available

32Oxmoor Business Park(Universal DevelopmentCorporation)

138,110Citation Court,Homewood

197619781982

Dock highDrive-in

Block, Stucco& Glass

No12'–16'

No 25% 5.00 59% 57,300 sf Available

33Oxmoor Warehouses(Engel Realty)

110,188 Oxmoor Circle 1973 Drive-in Precast concrete No 12' No 25% 7.25 71% 32,000 sf Available

Office/Warehouse (Under 20,000 SF)

OXMOOR

GRAHAM REPORT • 2012

Service Center (Over 50% Office)

34Lakeshore CrossingsBusiness Center(Engel Realty)

59,891 1030 London Drive 2003 Dock high Concrete tilt-up No 21' Yes BTS 13.00 100%

35Wilkerson Warehouses(Graham & Co)

55,330115A-GWalter Davis Drive

1983Dock highDrive-in

Metal & Brick No16'–18'

No 5% 5.75 84% 8,750 sf Available

36230 Oxmoor Circle(JH Berry & Gilbert)

49,500 230-232 Oxmoor Circle 1972 Drive-in Precast concrete No 14' No 75% 5.75 46% 26,960 sf Available

37Oxmoor West Service Ctr.(Leitman-Perlman)

45,000 Lyon Lane 1998 Dock high Brick/Metal No 18' No15%–50%

8.00 100%

38Oxmoor Court(Morris Properties)

44,953156 Oxmoor Court130 Oxmoor Court110/120 Oxmoor Court

199519971999

Dock highDrive-in

Concrete tilt-up& Brick

No 14' No 15% 7.50 71% 13,158 sf Available

39Atlas – Industrial Lane(Graham & Co)

35,528 Industrial Lane19881994

Dock highDrive-in

Metal No 16' No 20% 6.25 100%

40Oxmoor Midi Warehouse(Engel Realty)

36,425280 Snow Drive,West Oxmoor

1981Dock highDrive-in

Metal/Block No 20' NoUp to20%

7.00 57% 15,350 sf Available

41West Park Drive(Southpace Properties)

33,300 West Park Drive 2000Dock highDrive-in

Block No 16' No 15% 8.00 100%

42209 Oxmoor Circle(Engel Realty)

32,000 209 Oxmoor Circle 1974 Drive-in Precast concrete No 12' No20%–25%

7.25 62% 12,000 sf Available

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

43Forum Business Park(Barber Companies)

84,180Oxmoor Road& Barber Court

1983 Drive-in Precast concrete No 14' No50%–100%

8.50 98% 1,305 sf Available

44Crescent Center(Barber Companies)

78,000Summit Parkway,Homewood

1988 Drive-in Concrete tilt-up No 13' No 80% 8.50 84% 12,576 sf Available

45Centurion Square(Barber Companies)

70,944Oxmoor Road& Barber Court

1983 Drive-in Precast concrete No 9' No60%–100%

10.54 89% 8,118 sf Available

46201 London Parkway(Engel Realty)

57,650 201 London Parkway 2001 Drive-inBrick &Concrete tilt-up

No 14' Yes70%–100%

13.00 83% 9,925 sf Available

* See Building Location Map, pages 19-20. Properties listed in descending order by size. Rental rates are provided by building’s agent. All rates quoted are Net unless otherwise noted.

LEGEND Office Warehouse

12OXMOOR

GRAHAM REPORT • 2012 13WEST

GRAHAM REPORT • 2012

The West submarket continued its run of positive absorption with over 300,000 sf absorbed in 2011 with occupancy climbing to a balanced state of 86.7%. Major

bulk distribution centers and automotive supplier networks make up the core of this submarket. Rental rates remained essentially unchanged; the strong absorption points to increasing rents in the coming year.

Leasing activity and build-to-suit proposals related to Mercedes suppliers were the market drivers in the West. Announced in 2009, with formal approvals in 2010, the new Norfolk Southern Intermodal Facility broke ground in 2011. At 350 acres, the Intermodal Facility will likely draw even more new development to the West submarket.

New leases and/or sales for 2011 in this submarket included:• Caterpillar Logistics leased 160,000 sf at Jeff Met #3.• L’Oreal (beauty supplies) expanded by 100,000 sf at Jeff Met #3.

West (I-459 west and I-59 west to Vance)

WEST

CBD

WESTBULK

DISTRIBUTIONOFFICE/

WAREHOUSETOTAL

MARKET

Occupancy Rate 86.7% 86.4% 86.7%

Status Balanced Balanced Balanced

Available Space 461,000 24,000 484,000

Total Market 3,474,000 176,000 3,650,000

Average Rate $4.34 $5.64 ––

New Space Rate $4.35 $6.50 ––

Absorption: 2011 334,000 17,000 351,000

2010 221,000 (12,000) 295,000

2009 138,000 (4,000) 134,000

2008 78,000 9,000 87,000

2007 304,000 (18,000) 286,000

Annual Absorption:

5 Yr. Avg. (2007-11) 215,000 (1,600) 230,600

14WEST

GRAHAM REPORT • 2012 15

Multi-Tenant Survey/2012

Bulk Distribution (Over 20,000 SF)

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

47Jefferson Metropolitan ParkPhases 1, 2 & 3(Graham & Co)

920,920Jefferson MetropolitanParkway, McCalla

200420052006

Dock highDrive-in

Concrete tilt-up No 32' Yes 0% 3.95 94% 60,060 sf Available

48Perimeter Industrial Park(EGS Commercial)

606,850I-459 & EasternValley Rd., Bessemer

19891994

Dock highDrive-in

Concrete tilt-up Yes 24' Yes 3% 2.95 50% 305,000 sf Available

49ACI(Synchronous)

600,00010095 Brosse Dr.,Vance

2004 Dock high Concrete tilt-up No 34' Yes 1% 5.10 100%MercedesSequencing Facility

50Mercedes-BenzService Parts Warehouse(Graham & Co)

518,40011146 W Walker Rd.,Vance

2005 Dock highDuraluminum metal wall/band-ed windows

No 24' Yes 2% 4.50 100%U.S. Distribution Center, all AC

51Parkwest Distribution Center

208,0006000 GreenwoodParkway, Bessemer

2003Dock highDrive-in

Concrete tilt-up No 30' Yes 5% 3.95 100% Owner-occupied

52Parkwest Corporate CenterBuilding III(EGS Commercial)

127,500I-459 at Morgan Road,Bessemer

2008Dock highDrive-in

Concrete tilt-up No 24' Yes BTS 6.35 50% 64,800 sf Available

53BLG Facility(Synchronous)

122,500Legacy Industrial Park,Vance

2010 Dock high Metal No 24' Yes 8% 5.20 100%

54Legacy Building(Synchronous)

120,00010097 Brosse Dr.,Vance

2004Dock highDrive-in

Concrete tilt-up No 30' Yes 5% 5.10 100%

55Perimeter Industrial ParkBuilding 2(Barber Companies)

110,800I-459 & EasternValley Road, Bessemer

1991 Dock high Concrete tilt-up Yes 27' Yes 5% 4.25 100%

56Parkwest Corporate CenterBuildings I & II(EGS Commercial)

82,000I-459 at Morgan Rd.,Bessemer

19902007

Dock high Jumbo Brick No19'–21'

Yes 20% 6.50 100%

57Academy Business Park(Southpace Properties)

57,600900 Powder Plant Rd.,Bessemer

2005Dock highDrive-in

Block & Metal No 24' Yes5%–10%

6.25 92% 4,800 sf Available

WEST

GRAHAM REPORT • 2012

* See Building Location Map, pages 19-20. Properties listed in descending order by size. Rental rates are provided by building’s agent. All rates quoted are Net unless otherwise noted.

LEGEND Office Warehouse

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

58Brooklane Business Center(Lumpkin Development)

107,150Brooklane Road,Hueytown

1981, 19901993, 1994

Dock highDrive-in

Block & StuccoMetal

No12'–16'

No 24% 4.80 92% 8,750 sf Available

57Academy Business Park(Southpace Properties)

68,600Powder Plant Road &Shirley Park DriveBessemer

2005Dock highDrive-in

Block & Metal No 20' Yes 20% 6.95 78% 15,000 sf Available

Office/Warehouse (Under 20,000 SF)

WEST 16

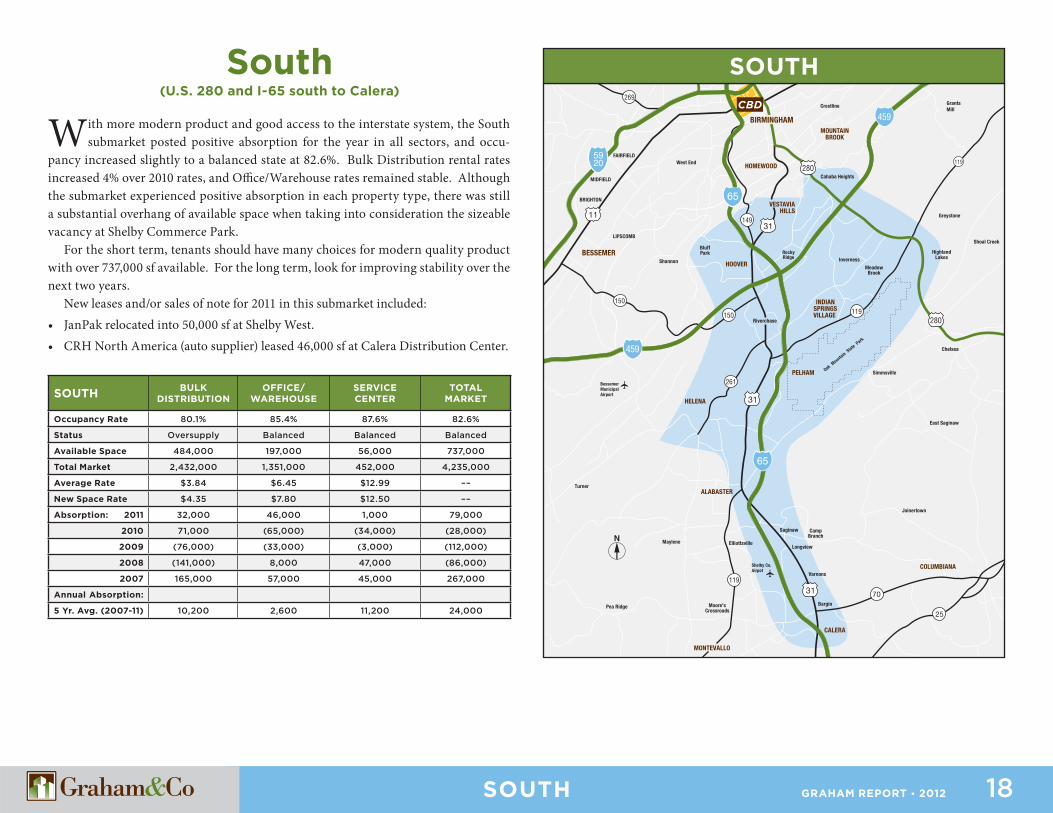

GRAHAM REPORT • 2012 17SOUTH

GRAHAM REPORT • 2012

With more modern product and good access to the interstate system, the South submarket posted positive absorption for the year in all sectors, and occu-

pancy increased slightly to a balanced state at 82.6%. Bulk Distribution rental rates increased 4% over 2010 rates, and Offi ce/Warehouse rates remained stable. Although the submarket experienced positive absorption in each property type, there was still a substantial overhang of available space when taking into consideration the sizeable vacancy at Shelby Commerce Park.

For the short term, tenants should have many choices for modern quality product with over 737,000 sf available. For the long term, look for improving stability over the next two years.

New leases and/or sales of note for 2011 in this submarket included:• JanPak relocated into 50,000 sf at Shelby West.• CRH North America (auto supplier) leased 46,000 sf at Calera Distribution Center.

South (U.S. 280 and I-65 south to Calera)

SOUTH

CBD

SOUTH BULKDISTRIBUTION

OFFICE/WAREHOUSE

SERVICECENTER

TOTALMARKET

Occupancy Rate 80.1% 85.4% 87.6% 82.6%

Status Oversupply Balanced Balanced Balanced

Available Space 484,000 197,000 56,000 737,000

Total Market 2,432,000 1,351,000 452,000 4,235,000

Average Rate $3.84 $6.45 $12.99 ––

New Space Rate $4.35 $7.80 $12.50 ––

Absorption: 2011 32,000 46,000 1,000 79,000

2010 71,000 (65,000) (34,000) (28,000)

2009 (76,000) (33,000) (3,000) (112,000)

2008 (141,000) 8,000 47,000 (86,000)

2007 165,000 57,000 45,000 267,000

Annual Absorption:

5 Yr. Avg. (2007-11) 10,200 2,600 11,200 24,000

SOUTH 18

GRAHAM REPORT • 2012

GRAHAM REPORT • 2012

19

BIRMINGHAM, AL

BUILDING LOCATIONS

20BUILDING LOCATIONS

GRAHAM REPORT • 2012 21

Multi-Tenant Survey/2012

Bulk Distribution (Over 20,000 SF)

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

59Shelby Commerce Park(Graham & Co)

1,530,082U.S. Highway 31,Calera

2001, 2002,2005

Dock highDrive-in

Concrete tilt-up No30'–32'

Yes 0% 3.75 88% 184,000 sf Available

60Calera Distribution Center(Graham & Co)

270,60041 North IndustrialParkway, Calera

2000Dock highDrive-in

Concrete tilt-upMetal

No 28' Yes 4% 3.65 56% 119,700 sf Available

61Shelby West Distribution Ctr.(EGS Commercial)

250,0001840 Corporate Woods Drive, Alabaster

2006Dock highDrive-in

Concrete tilt-up No 30' Yes 3% 3.95 87% 33,750 sf Available

62Shelby West Commerce Ctr.(EGS Commercial)

154,000175 Airview Lane, Alabaster

2009Dock highDrive-in

Concrete tilt-up No 24' Yes BTS 4.25 31% 106,700 sf Available

63Cahaba Valley Business Park(EGS Commercial)

117,244200 Cahaba ValleyParkway, at I-65Pelham

1994Dock highDrive-in

Brick & Block No 24' Yes 100% 4.50 100%

64Valleydale Business Center(EGS Commercial)

110,000Business Center Drive, Pelham

1989Dock highDrive-in

Concrete tilt-up No 24' Yes 10% 3.95 64% 40,000 sf Available

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

63Cahaba Valley Business Park(EGS Commercial)

443,630 200 Cahaba ValleyParkway, at I-65Pelham

1992–2000

Dock highDrive-in

Block & Brick No13'–18'

No 15% 6.75 84% 71,830 sf Available

65Chandalar Business Park(Lumpkin Development)

161,100Chandalar Drive, Pelham

1993, 19941996

Drive-inDock well

Metal No 16' No 85% 6.20 93% 12,000 sf Available

66Riverchase Business Park(Engel Realty)

158,500 255 Riverchase Pkwy.1979, 1980

1982Dock highDrive-in

Precast concrete No 15' Yes 50% 7.50 90% 16,000 sf Available

67Alabaster South(Lumpkin Development)

144,700Scotland DriveAlabaster

2001Drive-inDock well

Metal No 16' No 24% 4.25 72% 39,900 sf Available

64Valleydale Business Center(EGS Commercial)

76,600Business Center Drive,Pelham

1989Dock high Drive-in

Block & Brick No13'–18'

Yes 20% 6.00 95% 3,975 sf Available

68Oak Mountain Business Park(Lumpkin Development)

71,250Commerce Parkway,Pelham

19941996

Drive-in Metal No 16' No 24% 5.25 100%

69Hoover East(Joseph Companies)

67,000 2260 Rocky Ridge Rd.19801986

Drive-in Metal & Brick No14'–16'

No 25% 6.25 93% 4,800 sf Available

Office/Warehouse (Under 20,000 SF)

SOUTH

GRAHAM REPORT • 2012

70Lorna Lane(Graham & Co)

54,3983419-3441 Lorna Lane,Hoover

19681980

Dock highDrive-in

Block & Metal No14'–18'

No 20% 4.85 69% 16,900 sf Available

71Hoover Business Park(Hoover Business Ctr., Ltd.)

47,4003500 Lorna Ridge Rd.Hoover

1986 Drive-in Concrete tilt-up No14'–19'

No 40% 8.90 88% 5,800 sf Available

72Cahaba Valley Service Ctr.(Graham & Co)

42,173Cahaba Valley,I-65 & Highway 119

1993 Dock high Block No16'–20'

No 50% 8.95 91% 4,000 sf Available

73Commerce Park(Wyatt Realty)

34,0751001-57 CommerceCircle, Pelham

1987, 19881989

Drive-in Metal No 14' No 30% 7.50 82% 6,000 sf Available

74Champion Boulevard(Graham & Co)

25,4197004 Champion Blvd.,U.S. 280

1997Dock highDrive-in

Concrete tilt-up No 16' No 33% 9.50 51% 12,406 sf Available

75Lorna Eight(Watts Realty)

25,0003403-17 Lorna Lane,Hoover

1981 Dock high Block No 16' No 50% 4.50 88% 3,125 sf Available

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

762100/2200/2300Riverchase Center(Colonial Properties)

305,6112100-2300Riverchase Center

1980, 1984 1991

Dock highDrive-in

Brick & BronzeGlass

No11'–15'

No80%–100%

13.50 88% 38,325 sf Available

77Riverhills Business Center(Barber Companies)

109,825 U.S. Highway 280 1986 Drive-in Brick No 14' Yes 100% 13.00 97% 3,775 sf Available

78Brook Highland Center(JH Berry & Gilbert)

22,0007051 Meadowlark Dr.U.S. Highway 280

2001 Drive-in Brick No 12' No 75% 13.50 73% 6,000 sf Available

70Lorna Lane(Graham & Co)

14,2203433-3443 Lorna Lane,Hoover

19681982

Dock highDrive-in

Block & Metal No12'–14'

No 50% 7.50 47% 7,500 sf Available

Service Center (Over 50% Office)

* See Building Location Map, pages 19-20. Properties listed in descending order by size. Rental rates are provided by building’s agent. All rates quoted are Net unless otherwise noted.

LEGEND Office Warehouse

SOUTH 22

GRAHAM REPORT • 2012 23EAST

GRAHAM REPORT • 2012

This submarket is the smallest in the metro area and typically trails other areas in terms of rent and pace of absorption. Th e 2011 year refl ected that pattern with the

overall occupancy at 81.5% in a state of oversupply and lower average rents. Rents for Bulk Distribution remained fl at and rents for Offi ce/Warehouse dropped by just under 4% for the year.

Absorption was modest at only 13,000 sf for Bulk Distribution and negative absorp-tion for the other products. Th e new products on the I-20 corridor noted some net gains as a result of required relocations aft er tornado damage from the April storms.

New leases and/or sales of note for 2011 in this submarket included:• Jones Stevens Plumbing leased 78,000 sf (tornado relocation) at Moody.• Maintenance Plus leased 100,000 sf at former Meadowcraft (tornado relocation).

East (Pinson Valley Parkway, Tarrant, Roebuck, Irondale, Trussville)

EAST

CBD

EASTBULK

DISTRIBUTIONOFFICE/

WAREHOUSETOTAL

MARKET

Occupancy Rate 81.7% 81.0% 81.5%

Status Oversupply Oversupply Oversupply

Available Space 185,000 51,000 236,000

Total Market 1,011,000 268,000 1,279,000

Average Rate $3.77 $5.69 ––

New Space Rate $4.35 $6.50 ––

Absorption: 2011 13,000 (19,000) (6,000)

2010 (23,000) (3,000) (26,000)

2009 (48,000) (14,000) (61,000)

2008 62,000 4,000 66,000

2007 8,000 0 7,000

Annual Absorption:

5 Yr. Avg. (2007-11) 2,400 (6,400) (4,000)

EAST 24

GRAHAM REPORT • 2012 25

Multi-Tenant Survey/2012

Bulk Distribution (Over 20,000 SF)

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

79Moody Commerce ParkPhases 1 & 2(Graham & Co)

384,000US 78 at I-20 Exit 47,Moody

20032007

Dock highDrive-in

Concrete tilt-up No 32' Yes 5% 3.95 87% 52,000 sf Available

80Cleage Drive(Graham & Co)

178,650170 Cleage Drive,Pinson Valley

19722007

Dock highDrive-in

Metal Yes17'–32'

Yes 2% 3.75 100%

81Multiple Distribution Center(Southpace)

152,000165 Goodrich Drive,Pinson Valley

19721978

Dock high Concrete block Yes 21' Yes 4% 3.00Ind Gross

44% 85,816 sf Available

82Roebuck PlazaDistribution Center(Barber Companies)

92,500RoebuckIndustrial Parkway,US 11 & I-459

1979 Dock high Concrete tilt-up Yes 18' Yes 10% 3.95 100%

83Irondale Distribution Center(Graham & Co)

78,0002503 1st Avenue South,Irondale

1974 Dock high Concrete tilt-up Yes 20' Yes 2% 3.95 54% 36,000 sf Available

84Old Leeds Distribution Ctr. (Graham & Co)

71,000 4759 Alton Court 2000Dock highDrive-in

Concrete tilt-up No 24' Yes 5% 8.75 84% 11,052 sf Available

85Commerce SquareBusiness Park(EGS Commercial)

56,000Commerce Blvd.,Irondale

1987Dock highDrive-in

Concrete tilt-up No 22' Yes 10% 4.95 100%

EAST

GRAHAM REPORT • 2012

No.*Property(Leasing)

BuildingSize (SF)

LocationYearBuilt

Loading Construction RailHeadRoom

Sprinklered%

OfficeRent/

SFOccupancy Remarks

86Commerce SquareBusiness Park(EGS Commercial)

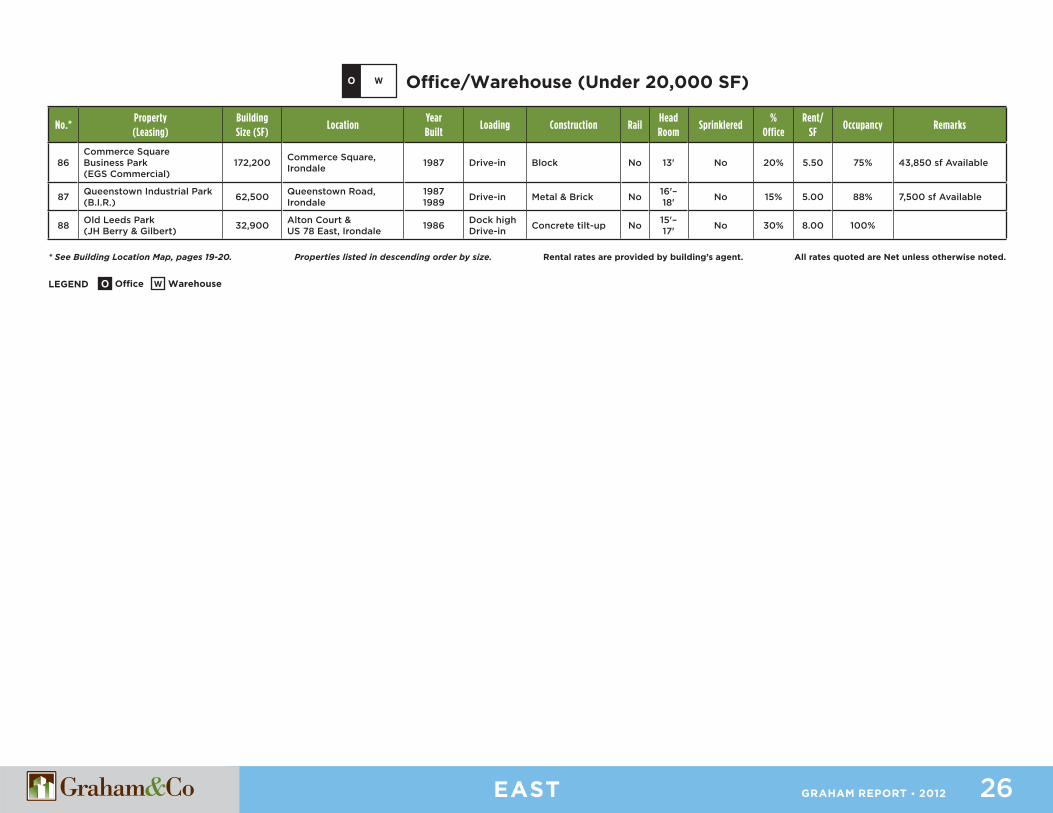

172,200Commerce Square,Irondale

1987 Drive-in Block No 13' No 20% 5.50 75% 43,850 sf Available

87Queenstown Industrial Park(B.I.R.)

62,500Queenstown Road,Irondale

19871989

Drive-in Metal & Brick No16'–18'

No 15% 5.00 88% 7,500 sf Available

88Old Leeds Park(JH Berry & Gilbert)

32,900Alton Court &US 78 East, Irondale

1986Dock highDrive-in

Concrete tilt-up No15'–17'

No 30% 8.00 100%

Office/Warehouse (Under 20,000 SF)

* See Building Location Map, pages 19-20. Properties listed in descending order by size. Rental rates are provided by building’s agent. All rates quoted are Net unless otherwise noted.

LEGEND Office Warehouse

EAST 26

GRAHAM REPORT • 2012 27

Industrial Buildings for Sale or Lease

The 2011 year continued to track improvements from the previous year, and new absorption of over 1,000,000 sf was posted for the Birmingham market. With a

market of over 92,000,000 sf, available space for 2011 increased slightly over 2010, remaining in a balanced state. Th e drop in occupancy from 2010 to 2011 resulted from the demolition, and subsequent removal from our database, of three buildings totaling over 800,000 sf. Sales prices seemed to have slowed/stopped a free fall, and brokers have managed increased activity from pent up demand.

Our industrial group closely tracks this market segment, and while many bargains have been snapped up, there are plenty of opportunities for investors and users ready to lock in low prices still lingering in the Birmingham area.

Sales for 2011 picked up, and several notable transactions are summarized below:• Dollar General completed a 960,000 sf distribution center along Lakeshore Parkway.• Constar’s 184,000 sf building fi nally found a user. Priority Wire purchased this former manufacturing building in September 2011.• Posco Steel constructed a new building at Jeff Met Park of 150,000 sf.• Crown Distributing completed a new 155,000 sf distribution center at Shelby West.

INDUSTRIAL BUILDINGS

SALE OR LEASE GRAHAM REPORT • 2012

All offerings subject to prior sale or lease.

28

Shelby Commerce Park

Marjam Facility

Former Keebler Facility

Former AGC Flatglass

Contact:

John Coleman(205) [email protected]

1,530,069 SFAVAILABLE:52,000 TO 375,000 SFU.S. Highway 31, One mile off I-65Calera, AL 35040

• Concrete tilt-up• 32' Clear height• 180' Truck court• Built 2001, 2003, 2005, 2006• ESFR sprinkler• 146-Acre class-A bulk park• Dock high & drive-in• Cross dock loading• Trailer storage• Site available for additional 800,000 sf Contact:

Ogden Deaton, SIOR

(205) [email protected]

19,346 SFAVAILABLE: 19,346 SF101 Cahaba Valley Parkway WestPelham, AL 35124

• 8,141 sf offi ce• 22’-24’ ceiling heights• (2) grade level loading doors• 1.38 acre site• 3-phase electrical service• Excellent visibility on Hwy 31/Pelham Pkwy• Excellent interstate access; located 1 mile from 1-65 via Exit 246

Contact:

Jordan Tubb(205) [email protected]

41,190 SFAVAILABLE:19,620 SF165 West Oxmoor RoadBirmingham, AL 35209

• Excellent access & visibility• Freestanding• Effi cient layout• Fenced yard area• Monument signage• Dock high loading (8)• City of Homewood• Can be subdivided

70,268 SFAVAILABLE: 70,268 SF

3350 Ball StreetBirmingham, AL 35234

• 70,268 sf Total, including ± 4,000 sf offi ce• M-2 Heavy Industrial zoning, City of Birmingham• CSX Rail spur with rail loading doors• Interior truck well under 3-ton bridge crane• Dock & grade level loading• Excellent access to I-20/59

Contact:

Jack Brown, SIOR

(205) [email protected]

SALE OR LEASE GRAHAM REPORT • 2012 29

All offerings subject to prior sale or lease.

BN ParkIn 2 Connect

Moody Commerce ParkFormer Tennessee Valley Metals Facility

443,000 SFAVAILABLE: Up to 83,000 SFRoberts Industrial ParkBirmingham, AL 35208

• Cooler/freezer available• Ceiling heights: 22' to 35' clear• Concrete tilt-up • 1/2 Mile from I-59• Dock high & drive-in loading• BNSF rail

Contact:

Ogden Deaton, SIOR

(205) [email protected]

71,795 SFAVAILABLE: 71,795 SF2304 Industrial DriveCullman, AL 35055

• Constructed 1988, addition 1998• 8.2 Acre site• Excellent interstate access• Substantial power

Contact:

John Coleman(205) [email protected]

AVAILABLE: 143,000 SF Proposed Phase ThreePrepared Building Pad

I-20 Brompton @ Exit #147Moody, AL 35004

Proposed Features• 32' Clear height• ESFR sprinkler• Phase III planned• No occupational tax St. Clair County• Superb interstate access• 13,000 sf per Bay• Interstate visibility

Contact:

Sonny Culp, SIOR

(205) [email protected]

25,500 SFAVAILABLE: 25,500 SF2720 Southeastern CircleBirmingham, AL 35215

• Located in unincorporated Jeff erson County• 4.8 Acre site• Dock high & drive-in loading• Excellent condition

Contact:

Jack Brown, SIOR

(205) [email protected]

LEA

SED

SALE OR LEASE GRAHAM REPORT • 2012

All offerings subject to prior sale or lease.

Shelby Commerce Park • Building 4

Distribution Center

30

Lorna Lane Offi ce/Warehouse

Moody Springs Business Park

500,066 SF on 35.56 AcresAVAILABLE: 500,066 SF3280 US Highway 31 SouthCalera, AL 35040

• 32' clear height• T-5 warehouse lighting• 89 dock doors• ESFR sprinkler• Subdivides easily• Guard house & security fencing• No occupational taxes

Contact:

Sonny Culp, SIOR

(205) [email protected]

515,000 SFAVAILABLE: 3,750 SF & UpDistribution Drive, HomewoodBirmingham, AL 35209

• Prime location• Concrete tilt-up• 20' Clear height• Truck high, drive-in & rail loading• Expansion possibilities

Contact:

Ogden Deaton, SIOR

(205) [email protected]

14,500 SFAVAILABLE: 14,500 SF3419 Lorna LaneHoover, AL 35216

• 2,000 sf Offi ce• 16' Eave heights• (2) Dock high doors• 3-Phase, 240 electrical service• Excellent access to I-459 and US Highway 31• Located in City of Hoover, no city occupational tax

Contact:

Jordan Tubb(205) [email protected]

7.5 AcresAVAILABLE: BUILD-TO-SUIT

25,000 TO 91,250 SFExit 144Moody, AL 35004

• Customized construction & tenant improvements• Distribution or light manufacturing• City of Moody• Less than one mile to I-20• Extra trailer parking• Site graded for construction

Contact:

Jack Brown, SIOR

(205) [email protected]

SALE OR LEASE GRAHAM REPORT • 2012 31

All offerings subject to prior sale or lease.

Lakeshore 150 Business ParkRoomstore

Jefferson Metropolitan Distribution Center Former RockTenn Facility

PINS

ON V

ALLE

Y PK

WY

PINS

ON V

ALLE

Y PK

WY

CLEAGE DR

CLEAGE DR

120 AcresAVAILABLE: 1-20 ACRE PARCELS

Lakeshore Parkway & Highway 150Bessemer, AL 35022

• Pad ready sites, various sizes• All utilities available• Business Park environment• Growth corridor• Great access & visibility• Protective covenants

62,500 SFAVAILABLE: 62,500 SF410 Pine Valley CircleBessemer, AL 35020

• 30'-34' Clear height• Freestanding• Dock high & drive-in loading• Offi ce/warehouse in great condition

Contact:

Ogden Deaton, SIOR

(205) [email protected]

Contact:

John Coleman(205) [email protected]

380,380 SF Phase TwoAVAILABLE: Up to 120,120 SF6600 Jefferson Metropolitan ParkwayMcCalla, AL 35111

153,220 SFAVAILABLE: 153,220 SF3200 Pinson Valley ParkwayBirmingham, AL 35217

• Monumental glass entries• 32' Clear height• Cross loading• (3) Air changes per hour• ESFR sprinkler• TPO membrane roof• 20,020 sf per Bay

• CSX, internal spur• 20'- 26' Clear height• Concrete tilt-up construction• 16 Acres• Dock high & drive-in loading • ESFR sprinkler

Contacts:

Sonny Culp, SIOR

(205) [email protected]

Contacts:

Ogden Deaton, SIOR

Jack Brown, SIOR

(205) [email protected]

LEA

SED

SALE OR LEASE GRAHAM REPORT • 2012

All offerings subject to prior sale or lease.

Former Steven’s Graphics

Distribution Facility on 14.74 Acres

Former A & S Marble

32

Liberty Park Development Site

220,000 SFAVAILABLE: 220,000 SF100 West Oxmoor RoadBirmingham, AL 35209

• CSX rail spur serving warehouse• 13.58 Acre site• 8250 KVA electrical power• Signifi cant areas of conditioned warehouse space• ± 20,000 sf of offi ce area

47,320 SFAVAILABLE: 47,320 SF

315 Highway 433Chelsea, AL 35043

19,200 SFAVAILABLE: 19,200 SF

118 Little Valley CourtBirmingham, AL 35244

• 7,320 sf offi ce• 22'-28' ceiling heights• 3-phase, 480 electrical service• CSX rail spur• ± 7 Acres with compacted gravel• Built 2001• (3) 20'w x14'h grade level loading doors• (4) 9’w x10’h dock high loading doors with levelers

• Unique industrial location in Riverchase, Shelby Co.• (1) 7 ½-ton and (1) 4 ½-ton bridge cranes• (10) 20'x20' drive-in doors• ± 2,750 sf of offi ce space• 1.96 acre site• Excellent interstate access

Contact:

Jack Brown, SIOR

(205) [email protected]

20.38 AcresAVAILABLE: 20.38 ACRES

Liberty ParkwayBirmingham, AL 35242

• Interstate visibility• Excellent topography • Subdivides easily• All utilities available

Contact:

Sonny Culp, SIOR

(205) [email protected]

Contact:

Jordan Tubb(205) [email protected]

Contacts:

Jack Brown, SIOR

Ogden Deaton, SIOR

(205) [email protected]

SALE OR LEASE GRAHAM REPORT • 2012 33

All offerings subject to prior sale or lease.

Former Meadowcraft

Interstate Industrial Park

260 Lyon Lane

Former Norell Facility

324,000 SF AVAILABLE: 324,000 SF4720 Pinson Valley ParkwayBirmingham, AL 35215

• 22' to 40' Clear heights • Built 1996• Building in excellent condition• 27 Acres cleared & fenced• CSX rail possible• Heavy power throughout• Dock high & drive-in loading

1,000,000 SFAVAILABLE: Up to 636,000 SF

5th Avenue & 24th StreetBessemer, AL 35020

• 10 to 20-Ton cranes• Bay widths 90' to 130'• 116 Acres• 32' Hook height• Excellent rail service• Additional 220,000 sf under outside crane• New CSX Intermodal• Buildings can be subdivided 15,000 sf & up

Contact:

Ogden Deaton, SIOR

(205) [email protected]

196,120 SFAVAILABLE: 52,360 SF260-A Lyon LaneBirmingham, AL 35211

• 5,000 sf offi ce• Warehouse conditioned• (7) Dock high doors• (6) Grade level doors• ESFR sprinkler• 25' Clear height

Contact:

Sonny Culp, SIOR

(205) [email protected]

Contact:

Ogden Deaton, SIOR

(205) [email protected]

10,560 SF AVAILABLE: 10,560 SF5540 Parkwood CircleBessemer, AL 35022

• 3,460 sf offi ce• 22'-24' ceiling heights• 3-phase electrical service• 1 acre site• (2) 14'x14' grade level loading doors• Built 2001• Excellent interstate access located 1 mile from 1-459 via Exit 6

Contact:

Jordan Tubb(205) [email protected]

SOLD

SALE OR LEASE GRAHAM REPORT • 2012

All offerings subject to prior sale or lease.

Long’s Electronics

Former Southern Comfort Conversions Calera Commerce Park

Former NSS Warehouse

34

92,000 SFAVAILABLE: 92,000 SF2630 5th Avenue SouthIrondale, AL 35210

• 22,000 sf of Class A offi ce space• 8.27 Acre site allows for expansion or signifi cant parking/storage• 24' Clear height• Concrete tilt-up construction• Fully sprinklered• Excellent interstate access via I-20 Exit 133

Contact:

Jack Brown, SIOR

(205) [email protected]

1,032,000 SFAVAILABLE:150,000 TO 1,032,000 SF4700 Pinson Valley ParkwayBirmingham, AL 35215

• 29' to 39' Clear heights• Class-A distribution/mfg• Huge truck court with trailer storage• Built 1995 & 1996 in excellent condition • Insulated metal construction • Below market rates

Contact:

Ogden Deaton, SIOR

(205) [email protected]

30 AcresAVAILABLE: SALE OR BUILD-TO-SUIT

Highway 22 & George Roy ParkwayCalera, AL 35040

• Excellent interstate visibility from I-65• Pad ready sites available• Build-to-suit up to 250,000 sf• Will subdivide

Contact:

Ogden Deaton, SIOR

(205) [email protected]

194,564 SFAVAILABLE: 194,564 SFRains Air Depot RoadGadsden, AL 35903

• (3) Warehouses, 65,000 sf each• 27' to 34' Clear height• Insulated metal construction• CSX rail served• Dock high & drive-in loading• Built 2000

Contact:

Ogden Deaton, SIOR

(205) [email protected]

GRAHAM REPORT • 2012GRAHAM ACTIVITIES 2011 35

Former RCS: 10,500 sf on 1.5 Acres.Offi ce/warehouse facility located in Trussville.3235 Veterans Circle, Birmingham, ALAgent: Jack Brown, SIOR • Co-Agent: Jordan Tubb

Former Steel City Crane: 25,330 sf on 7.5 Acres.Sold to P&S Transportation.2563 Commerce Circle, Birmingham, ALAgent: Jack Brown, SIOR • Co-Agent: Ogden Deaton, SIOR

Faurecia Tuscaloosa: 122,724 sf.Automotive supplier sold as investment property.141 Industrial Drive, Tuscaloosa, ALAgent: John Coleman • Co-Agent: Colliers International

Neff Rental: 24,000 sf.Long term lease with national heavy equipment dealer.3000 Pinson Valley Parkway, Birmingham, ALAgent: Jack Brown, SIOR

Co-Agent: USA Property Consulting Group

Former Johnson Brothers Wine: 64,280 sf.Freestanding industrial building on 3 acres sold to local fooddistribution company. 203 Parker Drive, Pelham, ALAgent: Sonny Culp, SIOR • Co-Agent: Jack Brown, SIOR

5610 Shirley Park Drive: 10,000 sf.Freestanding offi ce/warehouse purchased by American PharmacyCooperative for expansion of corporate headquarters.5610 Shirley Park Drive, Bessemer, ALAgent: Jack Brown, SIOR

Old Leeds Distribution Center: 28,600 sf.American Bottling Company (Dr. Pepper) leased space for aBirmingham distribution location.4759 Alton Court, Irondale, ALAgent: John Coleman • Co-Agent: Sonny Culp, SIOR

Former Alluriam Stone Facility: 74,800 sf on 10.21 Acres.Craned warehouse sold to Precision Grinding.201 Kilsby Circle, Birmingham, ALAgents: Ogden Deaton, SIOR & Jordan TubbCo-Agent: Jack Brown, SIOR

LEASED

LEASED SOLD

SOLD SOLD

SOLD

SOLD

SOLD

JeffMet Distribution Center • Phase Three: 100,100 sf.Expanded L’Oreal by 100,100 sf.6600 Jeff erson Metropolitan Parkway, McCalla, ALAgents: Sonny Culp, SIOR & Jack Brown, SIOR

LEASED

GRAHAM REPORT • 2012

Golden Boy Foods: 80,000 sf.Long term lease for Canadian peanut butter manufacturer.125 Henderson Highway, Troy, ALAgent: Ogden Deaton, SIOR

Calera Box: 156,000 sf.Lease renewal of 156,000 sf for Rainbird regional distribution. 41 North Industrial Blvd., Calera, ALAgent: Sonny Culp, SIOR • Co-Agent: Ogden Deaton, SIOR

Former Constar Plastics Facility:184,723 sf on 12.6 Acres. ± 12.6 Acre rail served sitepurchased by Priority Wire for S.E. distribution.120 West Oxmoor Road, Birmingham, ALAgent: Jack Brown, SIOR

Former Esser Twin Pipes: 17,500 sf on 4.5 Acres.Offi ce/warehouse facility located in Alabaster.147 Airpark Industrial Road, Birmingham, ALAgent: John Coleman • Co-Agent: Jordan Tubb

Rigid Building Systems: 240,000 sf.Crane served manufacturing facility in excellent condition.1305 Airport Industrial Drive, Gadsden, ALAgents: John Coleman & Sonny Culp, SIOR

JeffMet Distribution Center • Phase Three: 160,160 sf.Lease with Caterpillar Logistics.6600 Jeff erson Metropolitan Parkway, McCalla, ALAgents: Sonny Culp, SIOR & Jack Brown, SIOR

Co-Agent: Ogden Deaton, SIOR

Former Roland Pugh Facility: 15,750 sf on 8.2 Acres.Truck service with yard.1280 Powder Plant Road, Bessemer, ALAgent: John Coleman • Co-Agent: Progressive Properties

Fire Rock: 156,000 sf. Sale of 156,000 sf warehouse to Fire Rock, Inc.3100 Commerce Blvd., Birmingham, ALAgent: Ogden Deaton, SIOR

GRAHAM ACTIVITIES 2011 36

SOLD

SOLD SOLD

SOLD

SOLD SOLD

Former Pro Sports Marine: 95,000 sf on 17.6 Acres.Crane served manufacturing facility sold to Pell City based steelfabrication company. 353 Marine Drive, Lincoln, ALAgent: Jack Brown, SIOR

LEASED LEASED

LEASED

GRAHAM REPORT • 2012 37GRAHAM TEAM

Sonny Culp, SIOR

John HagefstrationAlli Gross

Dan Lovell, SIOR, LEED AP

Ogden S. Deaton, SIOR

Claudine Arredondo

Julie Hubbard

Betsy Lumpkin

Robin Domit

DeMarcus Bloxom

Maddie Humphries

Rick Mason

David Thomas

Jay Elliott

Janice Ivy

Jane McGriff

Jordan W. Tubb

Carl Finch

Jack Brown, SIOR

F. Craig Jackson

Hayden Montgomery, RPA

M. List Underwood III

Maria Goldschmidt

Walter Brown, SIOR

Brad Jones, MBA, CCIM

Jason Nairmore

Stacey R. Wadsworth

Mike Graham, CPM, SIOR

Sam J. Carroll IV, SIOR

Michael A. Lawley, CCIM

Christie Neely

Wanda Wanninger

Steve Graham, MAI, CRE

Eleanor Caver

Gardner Lee, CPM, SIOR

Susan Plate

Jamarcus Williams

Taylor Graham

John Coleman Charlie Crane

Jebb Long

Hayden L. Scott, MAI

Beth Gresham

Joelle Stuart

GRAHAM REPORT • 2012 38

110 Offi ce Park Drive

Suite 200

Birmingham, AL 35223

TEL 205.871.7100

FAX 205.871.3331

PRINCIPALS

Steve Graham, MAI, CRE

Mike Graham, CPM, SIOR

MANAGING PARTNER

Gardner Lee, CPM, SIOR

ASSET MANAGER

Taylor Graham

PROPERTY MANAGEMENT

Eleanor Caver

Jay Elliott

Beth Gresham

Hayden Montgomery, RPA

Stacey R. Wadsworth

F. Craig Jackson – Project Coordinator

Alli Gross – Asst.

Wanda Wanninger – Asst.

COMMERCIAL/INDUSTRIAL GROUP

Jack Brown, SIOR

John Coleman

Sonny Culp, SIOR

Ogden S. Deaton, SIOR

Jordan W. Tubb

Robin Domit – Real Estate Asst. – Offi ce Manager

Joelle Stuart – Asst.

OFFICE GROUP

Dan Lovell, SIOR, LEED AP

– Director

Walter Brown, SIOR

Sam J. Carroll IV, SIOR

Maddie Humphries

Brad Jones, MBA, CCIM

Christie Neely – Real Estate Asst.

CORPORATE SERVICES

Michael A. Lawley, CCIM

COMMERCIAL APPRAISALS

Hayden L. Scott, MAI

M. List Underwood III

ACCOUNTING

Maria Goldschmidt – VP Finance/Controller

Charlie Crane

Betsy Lumpkin

Janice Ivy – Asst.

FINANCE & LAW

John Hagefstration

GRAPHIC DESIGN

Jane McGriff

CHIEF INFORMATIONOFFICER

Jebb Long

MARKETING MEDIACOORDINATOR

Julie Hubbard

EXECUTIVE ASST.

Claudine Arredondo

RECEPTIONIST

Susan Plate

FACILITIES

DeMarcus Bloxom

Carl Finch III

Rick Mason

Jason Nairmore

David Thomas

Jamarcus Williams

HUNTSVILLE OFFICEMANAGING BROKER

Bart Smith, CCIM, SIOR

JACKSONVILLE OFFICEMANAGING BROKER

Peter Crolius, SIOR

GULF COAST OFFICE

Jason Carnes

Kevin Williams, CCIM

INDIVIDUALMEMBERSHIPS

INDIVIDUALMEMBERSHIPS

| B I R M I N G H A M

grahamcompany.com

355 Quality Circle

Suite E

Huntsville, AL 35806

TEL 256.382.9010

FAX 256.382.9011

| H U N T S V I L L E

550 Water Street

Suite 1225

Jacksonville, FL 32202

TEL 904.281.0003

FAX 904.281.0849

| J A C K S O N V I L L E

120 Richard Jackson Blvd.

Suite 210

Panama City Beach, FL 32407

TEL 850.563.1500

FAX 850.563.1504

| G U L F C O A S T

GRAHAM & COMPANY PERSONNEL – BIRMINGHAM

MEASURE US BY OUR ACTIONS

110 Offi ce Park Drive, Suite 200Birmingham, AL 35223

TEL 205.871.7100FAX 205.871.3331

grahamcompany.com

BIRMINGHAM HUNTSVILLE JACKSONVILLE GULF COAST