verde aurora: automated loan underwriting -- verde international llc

TRANSCRIPT

© 2015 Verde International LLC

Phone: 770.804.9363 x15

Fax: 678.658.1960

Verde fills three business-critical gaps unaddressed by virtually every other loan origination platform:

CUSTOM-TAILORED MODELS: YOUR WORLD, YOUR CUSTOMERS.

Conventional lending systems use a series of single- factor cutoffs to limit default risk. To realize acceptable loss rates, this approach must reject a large percentage of good borrowers. Conversely, achieving growth with this approach requires acceptance of undue risk.

Verde models project default odds, dollar default, repayment and other event timing for every loan evaluated. Our models are built for you, leveraging the full credit report (not just scores or select attributes) together with your own market conditions and lending experience. Verde models accurately estimate risk, expenses and revenues to simultaneously reduce losses and accelerate growth.

PROFIT-DRIVEN DECISIONS: UNPARALLELED RISK MANAGEMENT.

Conventional lending systems are credit risk centric. That sounds like a good thing, but managing credit quality alone isn’t good enough. Risk management is just one component in the overall economic outcome of the decision. A full view of revenue and expenses needs to be considered.

Verde estimates the size, timing, and probability of all material events, like early repayment, delinquency and charge off. From that we calculate the expected monthly cash flows from each loan application. Then, our financial models estimate the economic impact of each lending decision. You can treat each transaction and product independently or evaluate the value impact on the full relationship.

OPTIMIZED OFFERS: THE BEST DECISION. FOR EVERYONE.

Conventional lending systems are only designed to say yes or no to a fixed set of terms with little flexibility or support to find a better solution.

Verde understands your interest is to manage business performance and satisfy customers. Verde uses advanced optimization to identify the best options for satisfying the business interest and the applicant. Almost instantly, we can identify viable solutions that meet everyone's objectives. Whether the applicant is first time, subprime, superprime, or anyone in between, the ability to optimize creates the greatest opportunity for everyone.

VERDE AURORA™Decision Optimization

1

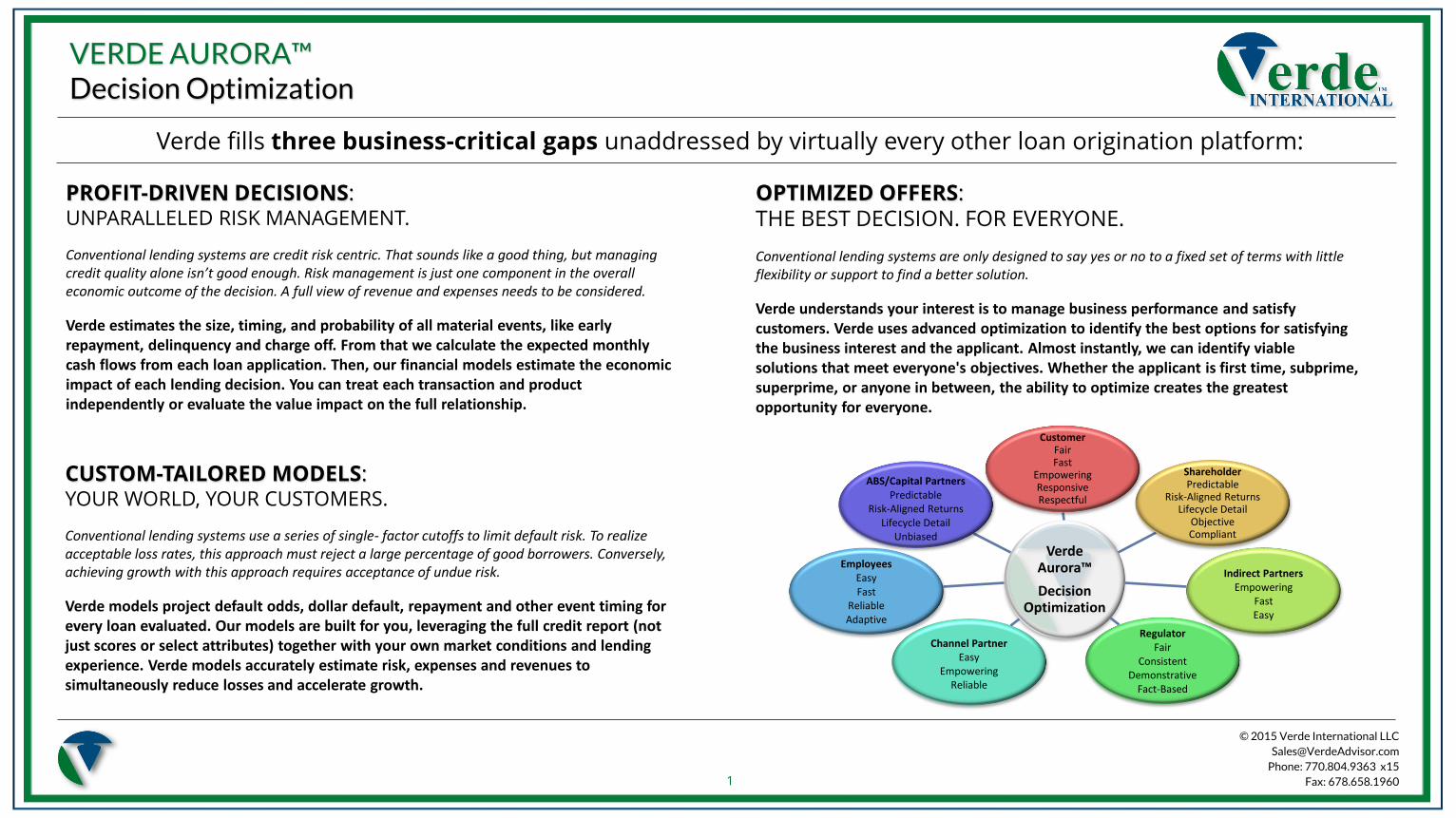

Verde Aurora™

Decision Optimization

CustomerFairFast

EmpoweringResponsiveRespectful

ShareholderPredictable

Risk-Aligned ReturnsLifecycle Detail

ObjectiveCompliant

Indirect PartnersEmpowering

FastEasy

RegulatorFair

ConsistentDemonstrative

Fact-Based

Channel PartnerEasy

EmpoweringReliable

EmployeesEasyFast

ReliableAdaptive

ABS/Capital PartnersPredictable

Risk-Aligned ReturnsLifecycle Detail

Unbiased

© 2015 Verde International LLC

Phone: 770.804.9363 x15

Fax: 678.658.1960

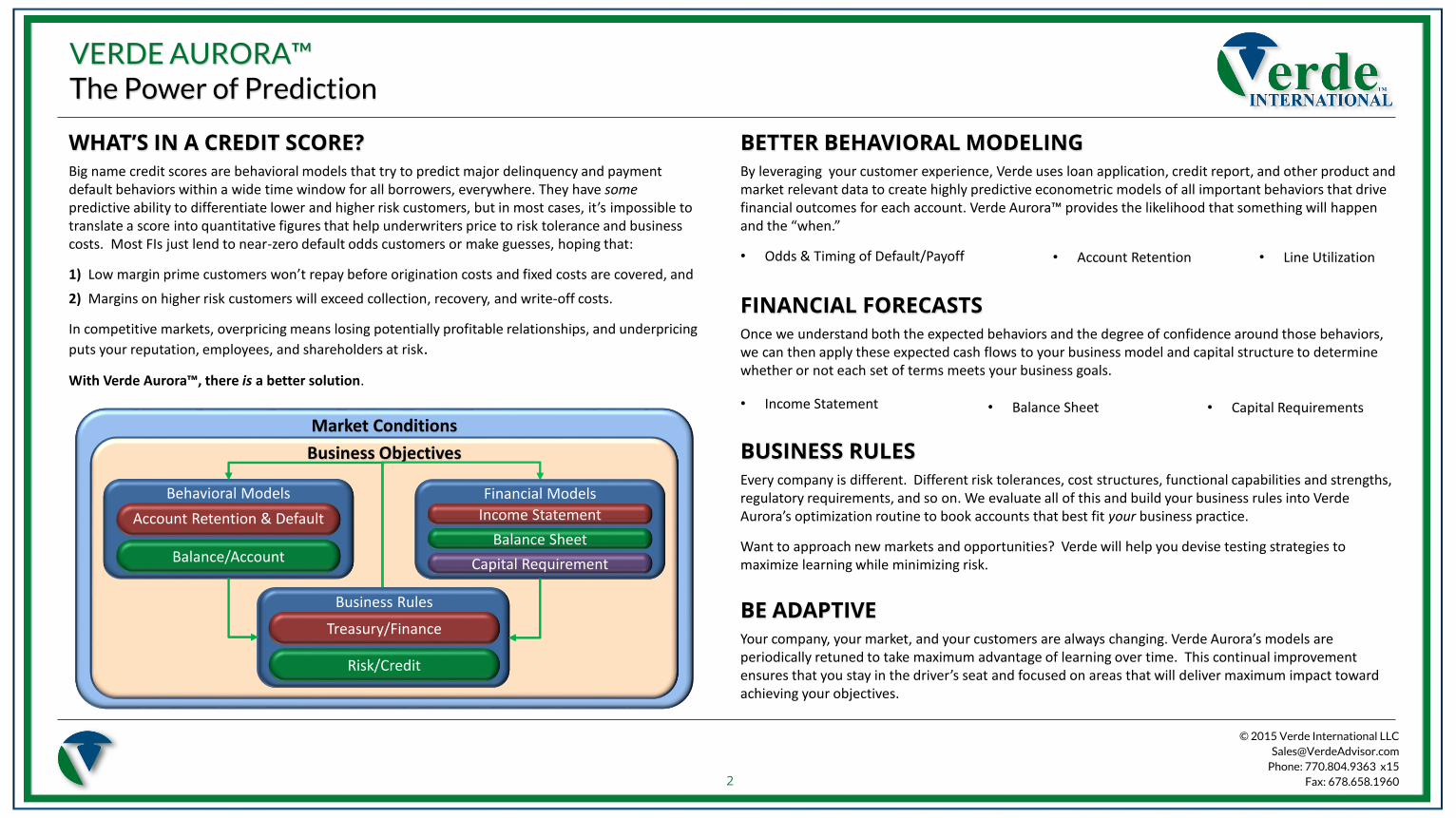

Market Conditions

Business Objectives

Behavioral Models

Account Retention & Default

Balance/Account

Financial Models

Financial Models

Income Statement

Balance Sheet

Capital Requirement

Business Rules

Treasury/Finance

Risk/Credit

WHAT’S IN A CREDIT SCORE?Big name credit scores are behavioral models that try to predict major delinquency and payment default behaviors within a wide time window for all borrowers, everywhere. They have somepredictive ability to differentiate lower and higher risk customers, but in most cases, it’s impossible to translate a score into quantitative figures that help underwriters price to risk tolerance and business costs. Most FIs just lend to near-zero default odds customers or make guesses, hoping that:

1) Low margin prime customers won’t repay before origination costs and fixed costs are covered, and

2) Margins on higher risk customers will exceed collection, recovery, and write-off costs.

In competitive markets, overpricing means losing potentially profitable relationships, and underpricing

puts your reputation, employees, and shareholders at risk.

With Verde Aurora™, there is a better solution.

BETTER BEHAVIORAL MODELINGBy leveraging your customer experience, Verde uses loan application, credit report, and other product and market relevant data to create highly predictive econometric models of all important behaviors that drive financial outcomes for each account. Verde Aurora™ provides the likelihood that something will happen and the “when.”

• Odds & Timing of Default/Payoff

FINANCIAL FORECASTSOnce we understand both the expected behaviors and the degree of confidence around those behaviors, we can then apply these expected cash flows to your business model and capital structure to determine whether or not each set of terms meets your business goals.

• Income Statement

BUSINESS RULESEvery company is different. Different risk tolerances, cost structures, functional capabilities and strengths, regulatory requirements, and so on. We evaluate all of this and build your business rules into Verde Aurora’s optimization routine to book accounts that best fit your business practice.

Want to approach new markets and opportunities? Verde will help you devise testing strategies to maximize learning while minimizing risk.

BE ADAPTIVEYour company, your market, and your customers are always changing. Verde Aurora’s models are periodically retuned to take maximum advantage of learning over time. This continual improvement ensures that you stay in the driver’s seat and focused on areas that will deliver maximum impact toward achieving your objectives.

• Line Utilization

• Capital Requirements• Balance Sheet

• Account Retention

VERDE AURORA™The Power of Prediction

2

© 2015 Verde International LLC

Phone: 770.804.9363 x15

Fax: 678.658.1960

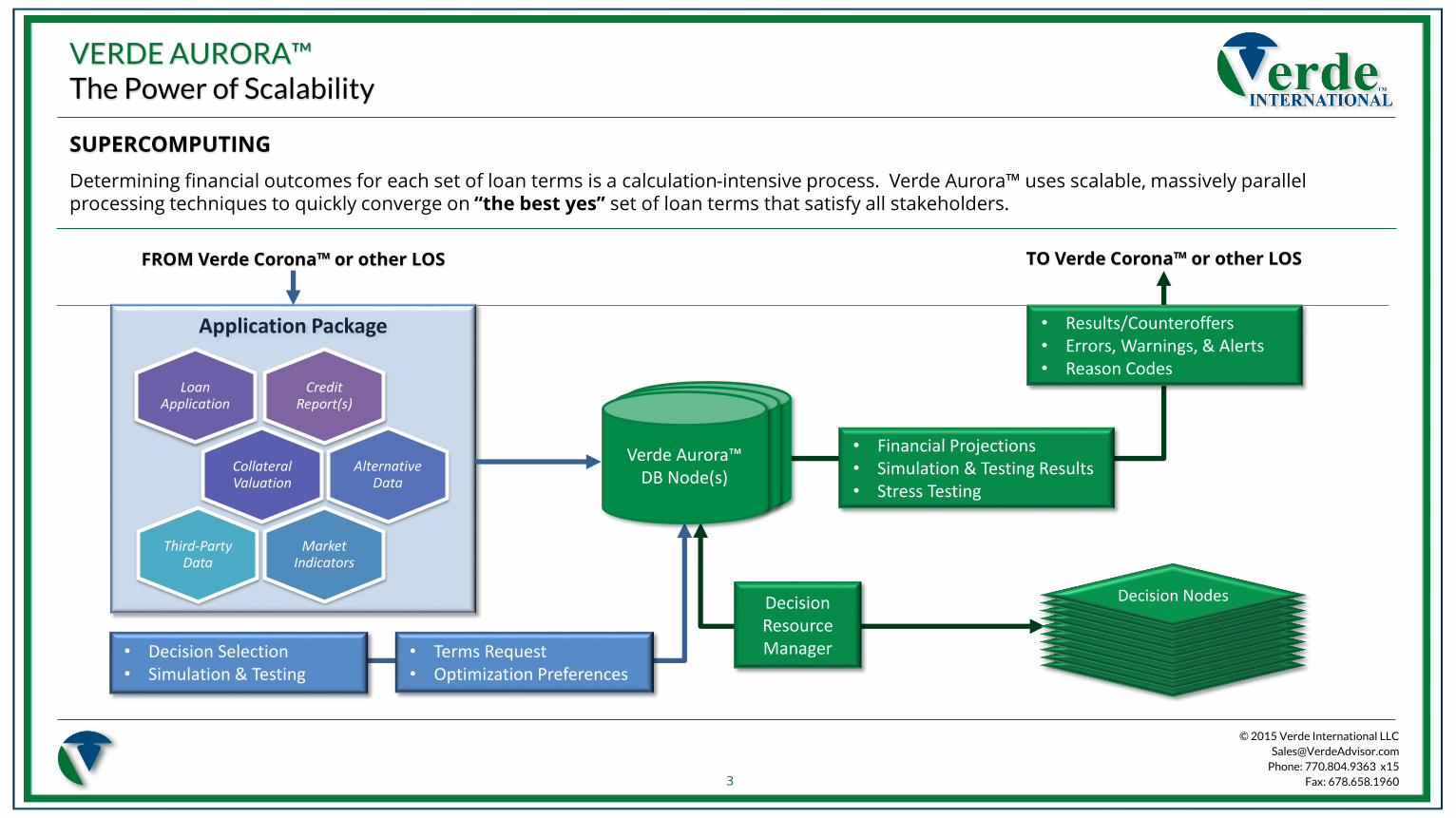

Application Package

SUPERCOMPUTING

Determining financial outcomes for each set of loan terms is a calculation-intensive process. Verde Aurora™ uses scalable, massively parallel processing techniques to quickly converge on “the best yes” set of loan terms that satisfy all stakeholders.

Verde Aurora™ DB Node(s)

Decision Resource Manager

Decision Nodes

• Decision Selection• Simulation & Testing

FROM Verde Corona™ or other LOS

• Results/Counteroffers• Errors, Warnings, & Alerts• Reason Codes

• Financial Projections• Simulation & Testing Results• Stress Testing

TO Verde Corona™ or other LOS

3

• Terms Request• Optimization Preferences

Credit Report(s)

Loan Application

Collateral Valuation

Alternative Data

Market Indicators

Third-Party Data

VERDE AURORA™The Power of Scalability

© 2015 Verde International LLC

Phone: 770.804.9363 x15

Fax: 678.658.1960

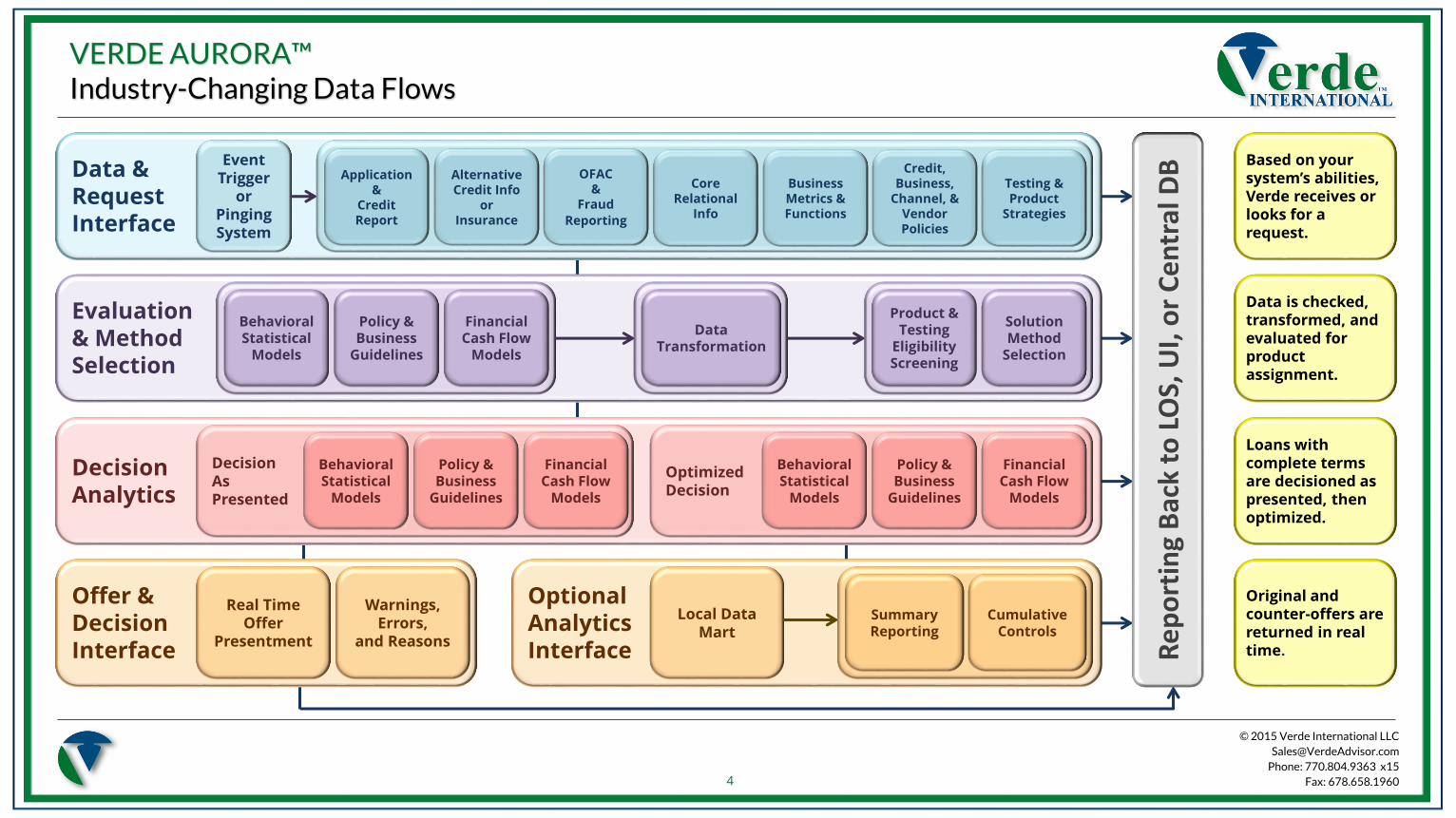

Data &RequestInterface

VERDE AURORA™Industry-Changing Data Flows

4

Evaluation & Method Selection

Offer & DecisionInterface

OptionalAnalyticsInterface

Based on your system’s abilities, Verde receives or looks for a request.

Data is checked, transformed, and evaluated for product assignment.

Loans with complete terms are decisioned as presented, then optimized.

Original and counter-offers are returned in real time.

DecisionAnalytics

Re

po

rtin

g B

ack

to L

OS,

UI,

or

Ce

ntr

al D

B

Real Time Offer

Presentment

Warnings,Errors,

and Reasons

Local Data Mart

DecisionAsPresented

Optimized Decision

Behavioral Statistical

Models

Policy & Business

Guidelines

Financial Cash Flow

Models

Behavioral Statistical

Models

Policy & Business

Guidelines

Financial Cash Flow

Models

Behavioral Statistical

Models

Policy & Business

Guidelines

Financial Cash Flow

Models

Data Transformation

Product & Testing

Eligibility Screening

Solution Method

Selection

Event Trigger

or PingingSystem

Summary Reporting

Application &

Credit Report

Alternative Credit Info

or Insurance

OFAC&

Fraud

Reporting

Core Relational

Info

Business Metrics & Functions

Credit, Business,

Channel, & Vendor Policies

Testing & Product

Strategies

Cumulative Controls

© 2015 Verde International LLC

Phone: 770.804.9363 x15

Fax: 678.658.1960

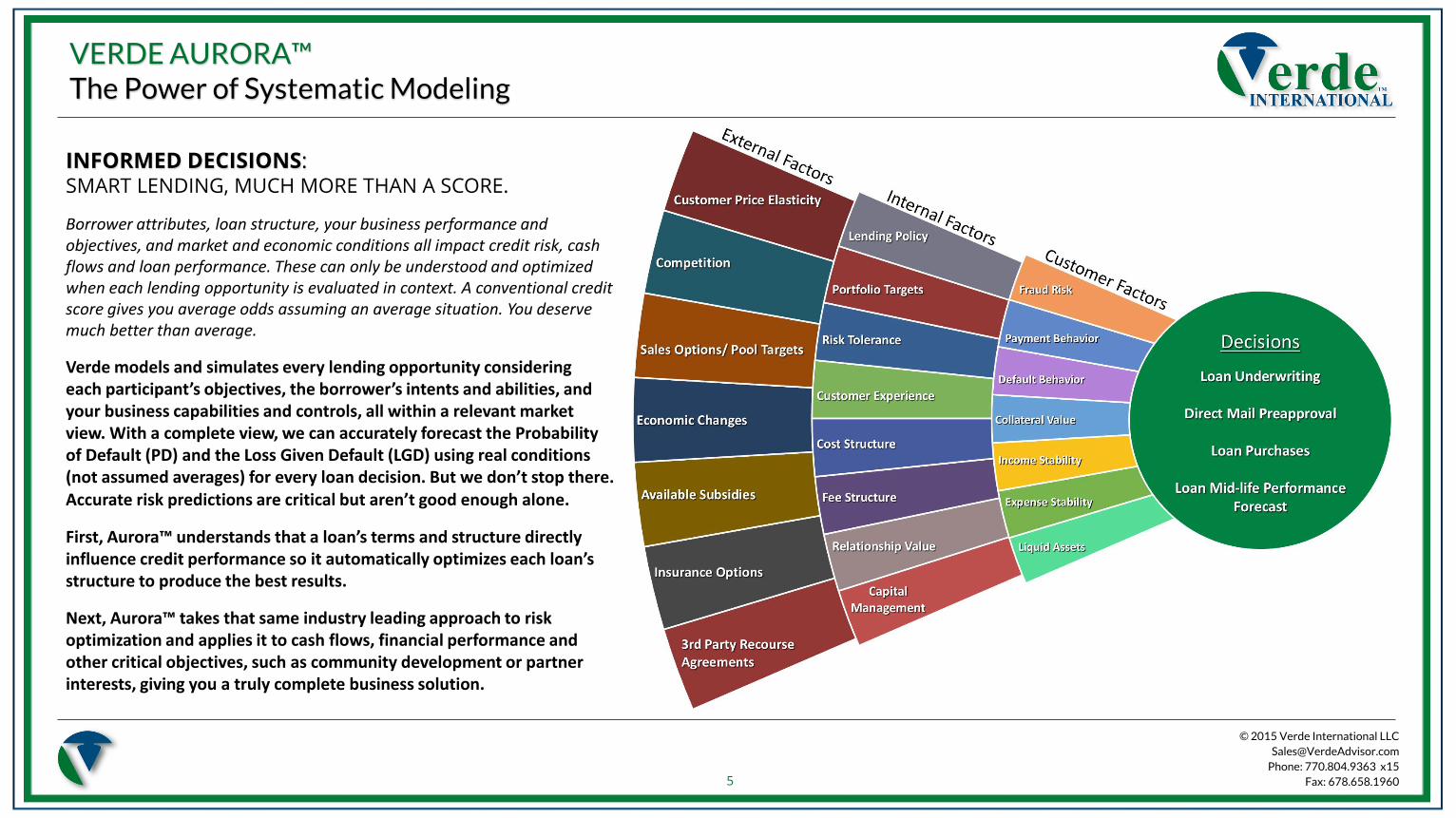

VERDE AURORA™The Power of Systematic Modeling

INFORMED DECISIONS: SMART LENDING, MUCH MORE THAN A SCORE.

Borrower attributes, loan structure, your business performance and objectives, and market and economic conditions all impact credit risk, cash flows and loan performance. These can only be understood and optimized when each lending opportunity is evaluated in context. A conventional credit score gives you average odds assuming an average situation. You deserve much better than average.

Verde models and simulates every lending opportunity considering each participant’s objectives, the borrower’s intents and abilities, and your business capabilities and controls, all within a relevant market view. With a complete view, we can accurately forecast the Probability of Default (PD) and the Loss Given Default (LGD) using real conditions (not assumed averages) for every loan decision. But we don’t stop there. Accurate risk predictions are critical but aren’t good enough alone.

First, Aurora™ understands that a loan’s terms and structure directly influence credit performance so it automatically optimizes each loan’s structure to produce the best results.

Next, Aurora™ takes that same industry leading approach to risk optimization and applies it to cash flows, financial performance and other critical objectives, such as community development or partner interests, giving you a truly complete business solution.

5

© 2015 Verde International LLC

Phone: 770.804.9363 x15

Fax: 678.658.1960

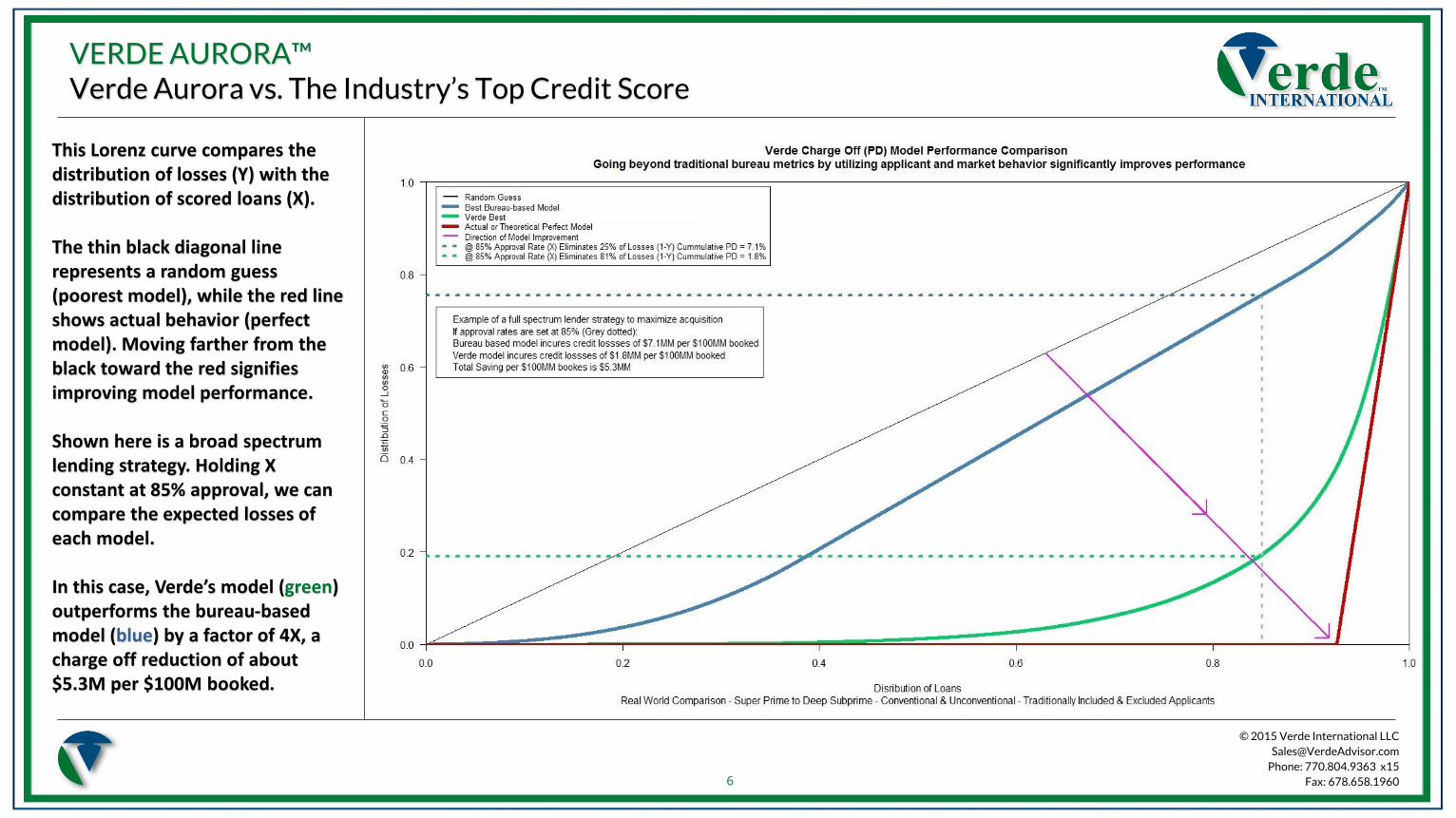

VERDE AURORA™Verde Aurora vs. The Industry’s Top Credit Score

This Lorenz curve compares the distribution of losses (Y) with the distribution of scored loans (X).

The thin black diagonal line represents a random guess (poorest model), while the red line shows actual behavior (perfect model). Moving farther from the black toward the red signifies improving model performance.

Shown here is a broad spectrum lending strategy. Holding X constant at 85% approval, we can compare the expected losses of each model.

In this case, Verde’s model (green) outperforms the bureau-based model (blue) by a factor of 4X, a charge off reduction of about $5.3M per $100M booked.

6

© 2015 Verde International LLC

Phone: 770.804.9363 x15

Fax: 678.658.1960

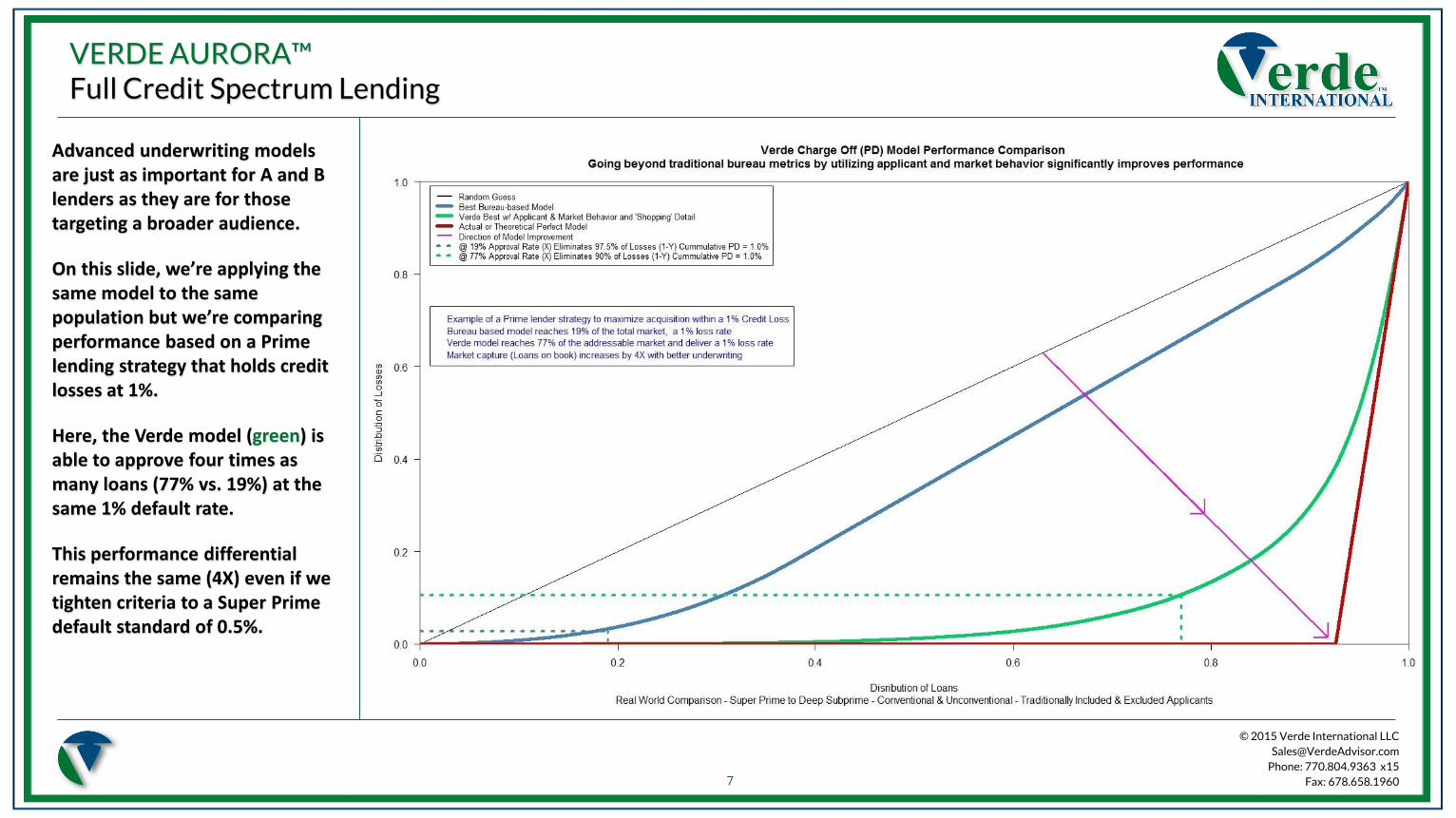

Advanced underwriting models are just as important for A and B lenders as they are for those targeting a broader audience.

On this slide, we’re applying the same model to the same population but we’re comparing performance based on a Prime lending strategy that holds credit losses at 1%.

Here, the Verde model (green) is able to approve four times as many loans (77% vs. 19%) at the same 1% default rate.

This performance differential remains the same (4X) even if we tighten criteria to a Super Prime default standard of 0.5%.

VERDE AURORA™Full Credit Spectrum Lending

7