vattenfall capital markets day 2009 capital markets day 2009 presentation by: Øystein løseth...

TRANSCRIPT

Vattenfall Capital Markets Day 2009

Presentation by:

Øystein LøsethSenior Executive Vice PresidentHead of Business Group Benelux

Amsterdam, 23 September 2009

Vattenfall Capital Markets Day, 23 September 20092© Vattenfall AB

Contents

• The Benelux Energy Market

• Overview Business Group Benelux

Vattenfall Capital Markets Day, 23 September 20093© Vattenfall AB

Key elements Benelux market

• Well connected to existing Vattenfall markets

• Great CO2 reduction and renewables opportunities

• Emerging as a biomass hub

• Benelux power production capacity needs renewal

• Strengthening its role as a hub for European gas

Vattenfall Capital Markets Day, 23 September 20094© Vattenfall AB

Electricity demand, 2008 (TWh)Electricity generation, 2008 (TWh)

89

France

Belgium

Netherlands

81

495 549

123 103

Source: Eurelectric

Supply and demand fundamental, electricity

Vattenfall Capital Markets Day, 23 September 20095© Vattenfall AB

• Large increase of capacity until 2015 results in sufficient remaining capacity• However, if announced projects are not executed, security of supply is easily in danger,

especially in Belgium• Depending on e.g., execution of nuclear phase out in Belgium (today 55% of the

generation), longer term reserves decline

FRNL B

0

2

4

6

8

10

2009 2010 2013 2015 20200

2

4

6

8

10

2009 2010 2013 2015 20200

4

8

12

16

2009 2010 2013 2015 2020

Remaining capacity*Security level

GW GW GW GW GWGW

Note: *Remaining capacity is defined as Net generation capacity – unavailable capacity – consumptionSource: UCTE

Generation capacity situation Benelux

Vattenfall Capital Markets Day, 23 September 20096© Vattenfall AB

Benelux electricity market: highly interconnected, as well as strongly connected to neighbouring markets

Sources: Datamonitor 2009, Elia, UCTE, ENTSO-E, EnergieNed, Tennet

Current capacity:• NL <> BE: 2200 MW• NL <> GE: 3900 MW• NL <> NO: 700 MW• BE > FR: 1100 MW• FR > BE: 2700 MW• GE > LUX: 980 MW

Planned capacity additions:• NL-UK: 1320 MW (2011)• NL-DK: 600 – 700 MW (2016)• FR-BE: 500 MW (2010)• DE-NL: tbd (2013)• LUX-BE: tbd (2012)• BE-GE: tbd

Interconnectivity of BG Benelux core markets: In 2008, the NL exported 8,1 TWh to Belgium. 3 TWh were exported from Belgium to the Netherlands (total 2008 NL production107 TWh).

Vattenfall Capital Markets Day, 23 September 20097© Vattenfall AB

The Benelux market in general, and the Belgian market in particular, is well connected to the French market…

Source: www.elia.be, System and Market overview 2008

Price convergence with energy exchanges in neighboring countries

In 2008, the price on the Belpex day-ahead market was the same as on the power exchange in the Netherlands and France in 69.1 % of the time. In other words, the markets were coupled at the time. For 15.4 % of the time, Belgium was only coupled with France, and for 14.7 % of the time only with the Netherlands. Only for 0.8% of the time was Belgium not coupled to one of its neighbors.

Vattenfall Capital Markets Day, 23 September 20098© Vattenfall AB

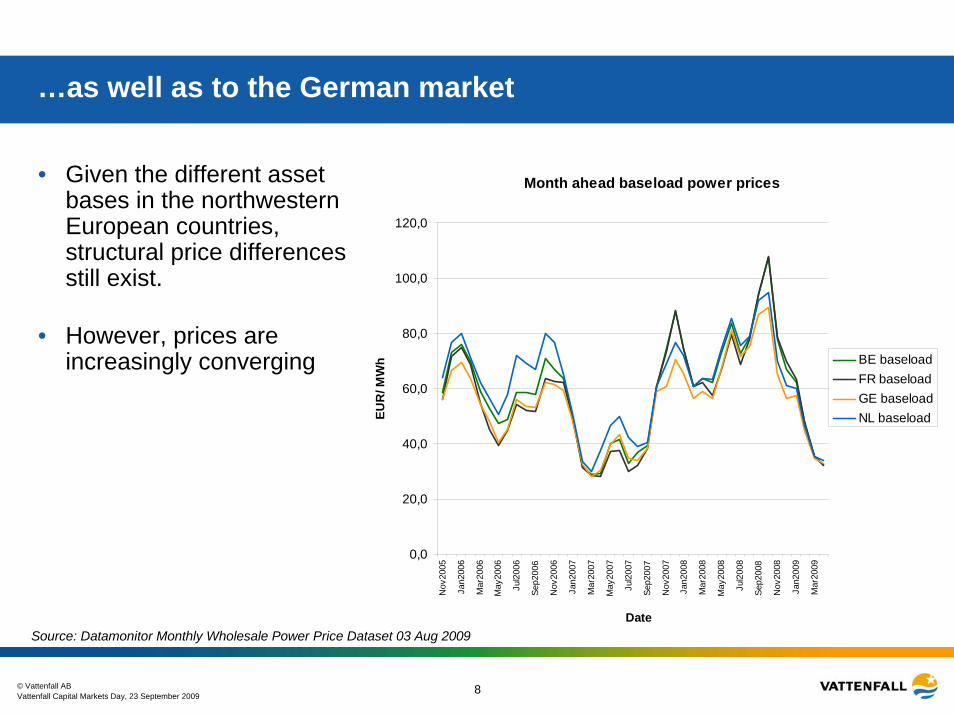

…as well as to the German market

Month ahead baseload power prices

0,0

20,0

40,0

60,0

80,0

100,0

120,0

Nov

2005

Jan2

006

Mar

2006

May

2006

Jul2

006

Sep2

006

Nov

2006

Jan2

007

Mar

2007

May

2007

Jul2

007

Sep2

007

Nov

2007

Jan2

008

Mar

2008

May

2008

Jul2

008

Sep2

008

Nov

2008

Jan2

009

Mar

2009

Date

EUR

/ MW

h BE baseloadFR baseloadGE baseloadNL baseload

Source: Datamonitor Monthly Wholesale Power Price Dataset 03 Aug 2009

• Given the different asset bases in the northwestern European countries, structural price differences still exist.

• However, prices are increasingly converging

Vattenfall Capital Markets Day, 23 September 20099© Vattenfall AB

Supply and demand fundamentals – Gas

Gas demand, 2008 (bcm)Gas production, 2008 (bcm)

18

France

Belgium

Netherlands0

47

2

3568

Source: eurogas, all data 2008 and BP Statistical Review of World Energy June 2009

Vattenfall Capital Markets Day, 23 September 200910© Vattenfall AB

North West Europe will increase its dependency on gas imports

Source: * BP Statistical Review of World Energy June 2009

** Wood Mackenzie 2009 and CERA 2008

• The Netherlands is experiencing a decrease of production • The policy of the Dutch government is designed to guarantee the long term

availability of sufficient gas and to promote diversification of gas supply• France and Belgium already depend on imports. Both countries enjoy a well

diversified sourcing portfolio (LNG, Netherlands, Norway, etc)

Natural gas proven reserves in the NL (Trillion cubic meters)

0,0

0,5

1,0

1,5

2,0

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Increase of annual imports to North-West Europe in 2020 compared to 2005**

Norway33%

Russia18%

NL16%

Algeria15%

Germany5% Others

6%Nigeria7%

Norway7%

NL79%

Germany5%

Russia5%Others

4%

Total: 86 bcm

Total: 49 bcm

Norway38%

UK8%

NL38%

Qatar13%

Others3%

Total: 21 bcm

12 bcm

8 bcm

25 bcm

Increase of annual imports

Vattenfall Capital Markets Day, 23 September 200911© Vattenfall AB

11

As a “gas country”, the Netherlands has an important role in distributing gas flows across Europe

Central role in European gas market

SOURCE: Global Insight

Gas storage

Projected LNG terminal

Gas flows

Trading hub

TTF

ZEE

NBP

VHP

Interconnection capacityGas fields

BBL

IUK

NorpipeNordstream

PEG

36% of total energy use in NL is gas, equal to 39 bcm per year1

26% of total energy use in NWE is gas, equal to 300 bcm per year1

Continued Groningen gas export to Belgium, France, and GermanyNew transit role of mainly Russian gas to UKDevelopment of LNG position to domestic and surrounding markets (e.g., Germany)Strong flexibility position due to high quality gas fields for storage and production swing of Groningen field

1) 2008 figures; relatively low because of drop in gas demand due to financial crisis and high temperatures

Vattenfall Capital Markets Day, 23 September 200912© Vattenfall AB

Regulatory trends/issues in BG Benelux

Focus on removing market barriers to stimulate new entrantsImplementation new G & E law and third packageCongestion managementNo new nuclear plants, replacement has not been ruled outFurther regulation heat supply

14% final energy consumption from renewable energy sources in 2020, translated in a ~30% renewable electricity targetSavings today 1% per year, must reach 2% in 2011-2020Aiming to save 500 PJ

Emissions

Renewables/ energy saving

NLB

Increasing Public Service ObligationAvailability of future cross-border gas capacity remains uncertainFirm exit capacity for gas supplyDebate around the nuclear phase out lawDevelopment Energy Clearing House in 2012

13% final energy consumption from renewable energy sources in 2020Regional system of green and CHP certificates to promote use and development of renewable production

FR

Focus on changing tariffs for certain segments to reflect market price (Champseur report)Work to introduce an “Eco tax”Second and third rounds to attribute new licence to operate to be built nuclear plantsFree up of hydro concessions

Further support on renewables production through subsidiesSystem for white labels to stimulate energy savings

Further attention on NOx and SO2emissionsImplementation IPCC and EU-ETSDevelopments around CCSCO2 reduction of 20%

Current key trends

Stricter legislation within the context of climate policy (CO2, RES)

Vattenfall Capital Markets Day, 23 September 200913© Vattenfall AB

NV Nuon Energy: Inclusion in the Vattenfall Group

Nuon Belgium CCC* VAS*Nuon

GermanyRetail

Netherlands

ET&WExploration &

Production Sales

BD&P

Board Nuon Energy(CEO & CFO)

Supply to B2B and B2C customers in the NL

Supply to B2B and B2C customers in Germany

Supply to B2B and B2C customers in Belgium

Customer Care Centre for the Dutch supply activities

Value Added Services

HistoricalShareholders

Grid Company

BG Pan Europe

Vattenfall Energy Trading

Wind activities

Held for sale

Staff*

Power, Heat & Services

Vattenfall

Vattenfall Capital Markets Day, 23 September 200914© Vattenfall AB

Business GroupCentral Europe

Mining & Generation

Transmission

Sales Germany

Distribution Germany

Heat Germany

Sales Poland

Distribution Poland

Heat Poland

Chief Executive Officer

Board of Directors

Group Shared Service

Business GroupNordic

Generation

Distribution

Services

Heat

Sales

Group Functions

Shared Service Centres

Wind

Nuclear

Engineering

Trading

Business Group

Benelux

Power, Heat & Services

Exploration & Production

Sales

Business Group

Pan Europe

Overview Business Group Benelux

Vattenfall Capital Markets Day, 23 September 200915© Vattenfall AB

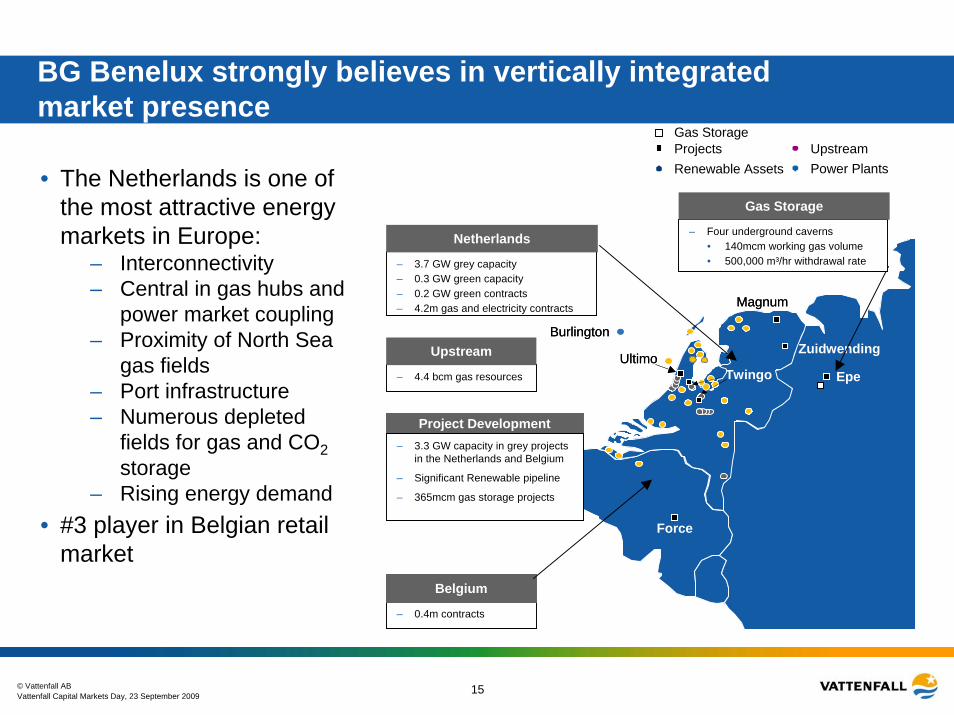

BG Benelux strongly believes in vertically integrated market presence

• The Netherlands is one of the most attractive energy markets in Europe:

– Interconnectivity– Central in gas hubs and

power market coupling– Proximity of North Sea

gas fields– Port infrastructure – Numerous depleted

fields for gas and CO2storage

– Rising energy demand• #3 player in Belgian retail

market

?

Griesheim

Magnum

Epe

Twingo

Burlington

Force

UltimoEpe

Zuidwending

Magnum

Burlington

Ultimo

– 0.4m contracts

Belgium

– 4.4 bcm gas resources

Upstream

– 3.7 GW grey capacity– 0.3 GW green capacity– 0.2 GW green contracts– 4.2m gas and electricity contracts

Netherlands – Four underground caverns• 140mcm working gas volume• 500,000 m³/hr withdrawal rate

Gas Storage

Renewable Assets Power PlantsUpstreamProjects

Gas Storage

Project Development– 3.3 GW capacity in grey projects

in the Netherlands and Belgium

– Significant Renewable pipeline

– 365mcm gas storage projects

Vattenfall Capital Markets Day, 23 September 200916© Vattenfall AB

Leading energy player in the Netherlands…

NL Generation by InstalledCapacity1

Electrabel 22%

Essent21%

Nuon19%

E.ON Benelux9%

Intergen4%

Others 25%

Total: 22.1 GW

NL Retail Electricity Supply by Number of Customers1

NL Retail Gas Supply by Number of Customers1

Essent26%

Eneco27%

Oxxio 3%

Others 14%

Total: 7.6m

Nuon30%

Total: 6.8m

Essent25%

Eneco22%

Oxxio6%

Others 19%

Nuon28%

The #1 player in retail electricity and gas supply in the Netherlands

The #3 player in power generation in the NetherlandsBG Benelux Fuel Mix

production 2008

* Wind activities are managed by BG Pan EuropeGeneration

Coal 22%

Natural gas CHP

10%Natural Gas power plants

28%

Blast furnace gas

20%

Wind

9%

Other

> 1%

Vattenfall Capital Markets Day, 23 September 200917© Vattenfall AB

Back-up

Vattenfall Capital Markets Day, 23 September 200918© Vattenfall AB

0

20

40

60

80

100

120

140

1990 1995 2000 2005 2010 2015 2020Year

Pow

er c

onsu

mpt

ion

(TW

h)

Forecasted demandActual demand

Electricity demand : stable growth expected in the Netherlands, slowing growth expected in Belgium

• Stable growth in demand is expected in the Netherlands, slowing growth in Belgium

• Long term impact of current economic downturn on the one side, and development of mass-demand technologies such as heat pumps and electrical transport is unclear

* http://www.entsoe.eu/_library/news/UCTE_SAF-2009-2020_Report.pdf** Source: Datamonitor 2009

0

20

40

60

80

100

120

1990 1995 2000 2005 2010 2015 2020

Pow

er c

onsu

mpt

ion

(TW

h)

Forecasted demand Actual demand

B

**

0

0,5

1

1,5

2

2,5

2009-2010 2010-2015 2015-2020

FR BE NL

Annual average change in electricity demand in % * NL

Vattenfall Capital Markets Day, 23 September 200919© Vattenfall AB

Gas: increased demand expected in all countries

Source: Datamonitor 2009

• Demand to small and retail customers is expected to slightly decrease in the NL due to increasing efficiency in energy consumption. However demand for industries and power stations is continuing to rise

• In Belgium, demand is expected to grow for all segments. The main growth area is the gas used by power stations due to new developments

0

0,5

1

1,5

2

2,5

3

2009 2010-2015

FR BE NL

Annual average increase in gas demand in %

0

10

20

30

40

50

60

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Year

Annu

al g

as c

onsu

mpt

ion

(bcm

)

NL

02468

101214161820

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Year

Annu

al g

as c

onsu

mpt

ion

(bcm

)

B

Vattenfall Capital Markets Day, 23 September 200920© Vattenfall AB

High level view on renewables in BG Benelux core countries

Netherlands

Strive to meet renewables targets in the NL (based on EU target) by

Belgium

Invest to meet renewables obligations in Belgium, since the costs of non-compliance are too high and the penalty system is expected to remain in place and good incentive

Investing in onshore wind generation ASAP*Developing offshore wind opportunitiesDeveloping biomass cofiring opportunitiesHaving a large enough funnel of options to meet any reasonable target, mostly investing post 2012 but preparing today

* Wind activities are managed by BG Pan Europe

Vattenfall Capital Markets Day, 23 September 200921© Vattenfall AB

Security of supply / shortage in Dutch generation in combination with an ageing asset base

0

500

1000

1500

2000

2500

3000

3500

4000

2008 2009 2010 2011 2012 2013 2014

Evolution BG Benelux generation portfolio without replacement*MW

Note: * based on large scale generation units

** based on current estimates volumes BP sales 2010-2012

16500

17000

17500

18000

18500

19000

19500

20000

20500

21000

2009 2010 2011 2012

Evolution Sales portfolio in the NL**

Some plants in BG Benelux‘ portfolio are expected to be decommissioned during the Business planning period while sales volumes are expected to grow driven by the B2B segment

BG Benelux‘ strategy is to have a balanced position between supply and generation and to maintain its market share in generation, therefore replacement of current generation is planned

GWh