value retail news + august partners€¦ · main st./free-standing stores outlet/factory outlet...

TRANSCRIPT

1

2

Value Retail News + August Partners:

2014 National Online Consumer Study

Top 50 U.S. Markets

Conducted 9/6-9/12, 2014

1,790Responses, Ages 13-65+

Closed-end Responses

Open-end Dialog Boxes

HH Income

Segments

$80K Avg.

FINDINGS

OVERVIEW

3

57.1%

68.2%

68.4%

70.8%

72.4%

75.5%

84.1%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Lifestyle Centers

Outlet Center

Main St./Free-Standing Stores

Online Fashion Sites

Enclosed Malls

Retail Store Websites

Big Box Centers

Tested Venue Visit Incidence Past 12 Months

Tested Venue Visits: 1X or More

4

20.4%

17.9%

16.5%

13.8%

13.3%

9.4% 8.6%

Tested Shopping Venue Visit Share

Big Box Open-Air Ctrs. (Target,Marshalls, etc.)

Online Fashion Retail Sites (Amazon,Rue La La, Gilt, Wanelo, etc.)

Any Retail Store Website (Gap,Aeropostale, Chico's, Macy's, etc.)

Enclosed Mall

Main St./Free-Standing Stores

Outlet/Factory Outlet Centers

Open-Air Lifestyle Fashion Ctr.

Shopping Venue Visit Share

5

Re-based to 100%; 5.1% of respondents had not visited any of these tested venues in the past 12 months

1.0% 1.7%

11.2%

17.9%

9.4% 8.6%

20.4%

13.8%

0%

5%

10%

15%

20%

25%

Outlets Lifestyle Ctrs. Power Ctrs. Malls

GLA % Visit Share %

Outlets – A Disproportionate Visit Share vs. GLA Percentage

6

Venues Shopped Avg. HH

Income

Avg. Annual

Apparel

Spend

App

Spend/HH

Income Index

Enclosed Malls $82,518 $1,008 122

Lifestyle Centers $88,515 $1,149 130

Outlet Centers $84,500 $1,045 124

Big Box Centers $82,472 $987 120

Main Street/Free-Standing Stores $84,506 $1,029 122

Retail Store Websites $83,905 $1,036 123

Fashion Retail Sites $84,592 $1,052 124

Venues Shopped Comparisons

7

8

Apparel Spend Comps by Census Divisions & Regions

August Partners/ICSC VRN 2014 National Survey Avg. Ann. Apparel

Spend

Respondent Geographic Segmentation

New England Division $799

Middle Atlantic Division $1,024

Subtotal: Northeast Census Region $968

East North Central Division $889

West North Central Division $673

Subtotal: Midwest Census Region $837

South Atlantic Division $940

East South Central Division $1,012

West South Central Division $1,005

Subtotal: South Census Region $964

Mountain Division $844

Pacific Division $987

Subtotal: West Census Region $944

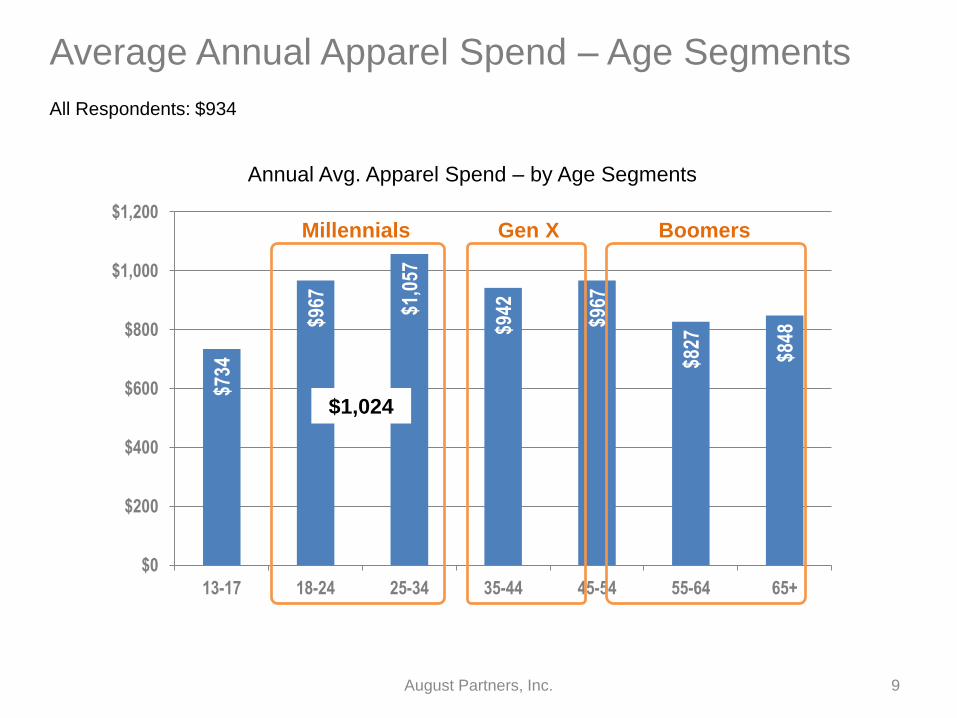

U.S. Top 50 Markets Total: $934

- 6.3%

$734

$967

$1,0

57

$942

$967

$827

$848

$0

$200

$400

$600

$800

$1,000

$1,200

13-17 18-24 25-34 35-44 45-54 55-64 65+

Annual Avg. Apparel Spend – by Age Segments

Millennials Gen X Boomers

Average Annual Apparel Spend – Age Segments

9

All Respondents: $934

August Partners, Inc.

$1,024

Shopper

Characteristics

Low

(38%)

Moderate

(30%)

High

(32%)

(< $500) ($500-$999) (> $1,000)

Avg. HH Income $59,310 $81,240 $107,080

Brand-Influenced 16.2% 31.2% 52.6%

Fashion Forwards™ 16.2% 24.4% 49.3%

Jeanetics™ $44 $51 $74

Correlating Apparel Spend to Shopper Characteristics

10

Apparel Spend by Venue – Past 12 Months

25.9%

28.4%

45.7%

Where Did You Spend Your Apparel, Shoes & Accessories Dollars the Past 12 Months?

Outlet Centers

Online Stores & Sites

All Other Bricks &Mortar

Physical = 71.6%

11

27.5%

44.3%

44.4%

49.2%

53.6%

59.6%

65.6%

0% 10% 20% 30% 40% 50% 60% 70%

Lifestyle Centers

Main Street/Free-Standing Stores

Outlet Centers

Retail Store Websites

Online Fashion Sites

Enclosed Malls

Big Box Centers

Holiday 2014 Projected Shopping Venue Incidence Levels

Christmas 2014 Shopping Venues Projection

12

VALUE

STANCE

13

26.5%

22.9% 18.7%

23.3%

8.6%

Almost Never Buy Full Price

Seldom Buy at Full Price

Occasionally Buy Full Price

Balance Full Price w/ Off-Price

Buy What I Want; Price Not aConcern

Value Stance Segmentation

14

91% of Shoppers are Looking for a Deal Full Price Shoppers

3.3%

7.9%

10.1% 11.3%

15.6%

24.0%

27.8%

0%

5%

10%

15%

20%

25%

30%

Lifestyle Centers Main St./Free-Standing Stores

Retail StoreWebsites

Enclosed Malls Online FashionRetail Sites

Outlet Centers Big Box Centers

Tested Venues - Best Value Delivery Perception

Up from 19.4% in 2013

15

Value Delivery Perceptions

Down from

32.8% in 2013

Down from

19.9% in 2013 Down from

15.8% in 2013 Up from 6.1%

in 2013

18.2%

55.1%

10.7%

16.1%

0% 10% 20% 30% 40% 50% 60%

Delivering Better Value than Past Years

Delivering the Same Value

Delivering Lower Value

Not Sure/Uncertain

How is Your Favorite Outlet Center Doing in Terms of Delivering Value on Apparel Goods?

Outlet Center Value Delivery Perception (cont.)

16

MINDSET

METRICS

17

Respondent Profile Data

Fashion Stance™ Category

Avg. Ann.

Apparel

Spend

Avg. HH

Income

Jeanetics™

(Avg. Jeans

Spend)

Fashion Moderates $789 $79,424 $40

Fashion Forwards™ $1,345 $86,954 $59

All Respondents $934 $80,235 $45

Fashion Forwards apparel spend is 70% higher than Fashion

Moderates, although the segment’s HH income is just 9.5% higher

The Fashion Forwards™ Mindset Metric

18

Venues Shopped

Fashion

Forwards

Percentage

Enclosed Malls 30.7%

Lifestyle Centers 35.6%

Outlet Centers 33.0%

Main Street/Free-Standing Stores 31.0%

Retail Store Websites 31.1%

Fashion Retail Sites 32.4%

Big Box Centers 30.2%

Where Are the Fashion Forwards™ Shopping?

19

No Influence

(32%)

Sometimes

Influenced (41%)

Usually-to-Always

Influenced (24%)

Avg. HH Income $74,471 $79,573 $91,475

Avg. Apparel Spend $699 $864 $1,405

Fashion Forwards™ % 16.1% 23.5% 49.2%

The Brand-Influenced Shopper

20

TOP 10

STORE BRANDS

21

Top 10 by Preference

Percentage

Percent

Nike 51.8%

Victoria's Secret 50.8%

GAP 42.9%

H & M 37.9%

Forever 21 36.8%

The North Face 36.1%

Polo Ralph Lauren 34.6%

Adidas 34.3%

American Eagle Outfitters 34.2%

Coach 33.9%

Top 10 by Apparel

Spend

Avg. Ann.

Apparel

Spend

Theory $1,641

Vince $1,611

Tory Burch $1,487

Vineyard Vines $1,436

Cole-Haan $1,427

Burberry $1,410

Aldo $1,348

Prada $1,346

Kate Spade $1,332

Lululemon Athletica $1,316

Preferred Store Brands

22

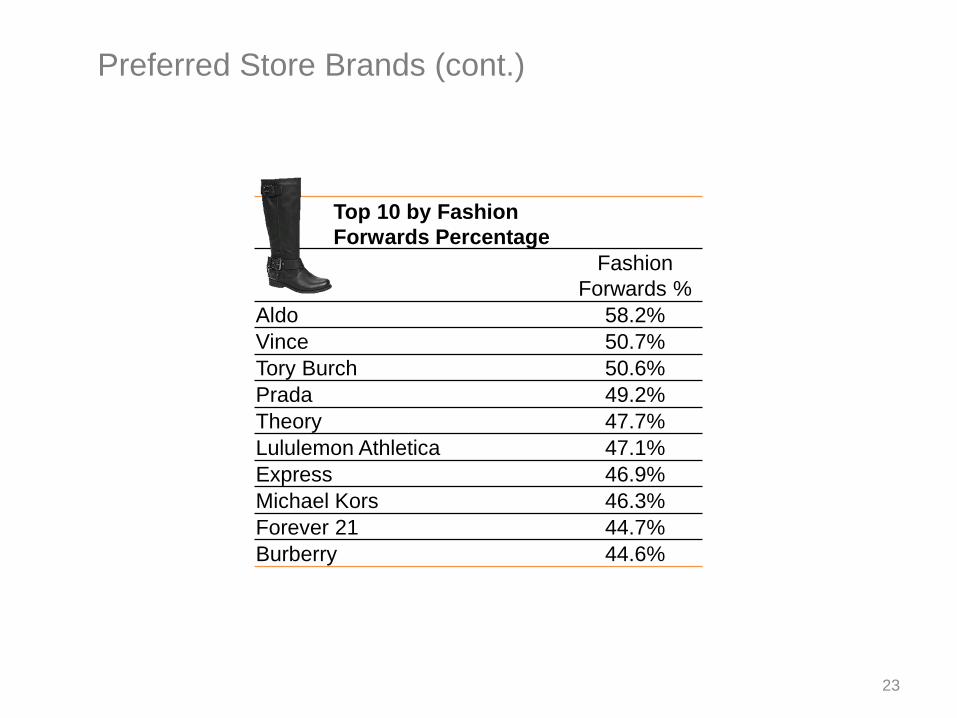

Top 10 by Fashion

Forwards Percentage

Fashion

Forwards %

Aldo 58.2%

Vince 50.7%

Tory Burch 50.6%

Prada 49.2%

Theory 47.7%

Lululemon Athletica 47.1%

Express 46.9%

Michael Kors 46.3%

Forever 21 44.7%

Burberry 44.6%

Preferred Store Brands (cont.)

23

ONLINE

SHOPPING

24

15.4%

16.3%

16.6%

18.0%

20.3%

30.5%

80.9%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Wanelo

Rue La La

Nasty Gal

Gilt

HauteLook

Zulily

Amazon

Fashion Site Visit Incidence Level

Apparel Site Visits – Past 90 Days

25

$114

$125

$151

$159

$163

$174

$189

$0 $20 $40 $60 $80 $100 $120 $140 $160 $180 $200

Amazon

HauteLook

Rue La La

Wanelo

Gilt

Nasty Gal

Zulily

Respondent Spend – Most Recent Visit

Fashion Site Spend from Z to A

26 August Partners, Inc.

If your favorite outlet

center were to develop a

mobile app which could

sense when you were in

the center and notify you

of special retailer sales

and promotions, how likely

would you be to download

and use that app on your

smartphone?

Q: 39.4%

27.7%

32.9%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Would DefinitelyDowload & Use

Would NotDownload &

Use

Undecided

Mobile App Download/Usage Likelihood

The Mobile App Question

27

OUTLET

SHOPPING

INFLUENCERS

28

30.5%

38.7%

42.2%

48.6%

50.3%

0% 10% 20% 30% 40% 50% 60%

The Shopping Experience

Location - Close to Home

Brand Name Stores in Outlets

The Value Outlets Deliver

The Number + Variety of Stores

What Influences Your Choice to Shop at an Outlet Center?

Outlet Shopping Drivers

29

12.0%

12.4%

13.0%

21.0%

30.3%

39.9%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Already Shop at Outlets on a Regular Basis

Do Not Have the Store Brands I Like

Quality of Mdse. - Not Good Value

Don't Like Experience (Parking, Crowds, etc.)

Sometimes Prefer to Shop at Regular Retail Stores

Closest Outlet too Far from Home

What Keeps You from Shopping at Outlets More Frequently?

Outlet Shopping Detractors

30

13.9%

16.5%

17.0%

27.4%

37.3%

55.0%

0% 10% 20% 30% 40% 50% 60%

Improved Center Aesthetics

More Sit-Down Restaurants

More Food Court Eating Places

Easier Shopping Layout

More of Specific Stores I Like

Location Closer to Home

What Would Drive Higher Outlet Center Shopping Frequency?

Outlet Shopping Enhancers

31

13.9%

16.5%

17.0%

27.4%

37.3%

0% 5% 10% 15% 20% 25% 30% 35% 40%

More Restrooms

More Benches & Seating Areas

Children's Play Area

Concierge/Personal Shopper Services

Smartphone Apps - In-Center Deal Alerts

Which of these Features & Amenities would You Like to See in an Outlet Center?

Outlet Features & Amenities Ranking

32

DEVICE &

MEDIA USAGE

33

20.3%

23.2%

33.1%

15.5%

16.6%

19.7%

8.7%

14.5%

15.7%

11.0%

10.3%

22.3%

20.4%

22.4%

7.4%

24.1%

13.0%

1.9

%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Mobile-Tablet

Mobile-Smartphone

At-Home Internet

Device Usage Spectrum

34

35

18.2%

19.4%

20.1%

36.0%

36.8%

37.4%

38.6%

39.0%

42.1%

51.2%

58.2%

75.1%

24.7%

20.0%

14.9%

25.3%

15.4%

25.7%

23.2%

23.6%

18.7%

19.3%

20.3%

10.4%

57.1%

60.6%

65.0%

38.7%

47.8%

37.0%

38.2%

37.4%

39.3%

29.5%

21.5%

14.5%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Hotel staff/In-room guide/Tourist publication

Websites like Rue La La/Gilt Groupe

Shopping center websites

Emails from shopping centers I have chosen

Mobile/smart phone applications

Displays & signage throughout a shopping center

Newspaper

Direct Mail

Customer loyalty clubs/programs

Emails from stores I have chosen

Already Using Don't Use Now, but Likely to Use in Near Future Do Not Use/ Unlikely to Use

Media Usage – Sales Information & Coupons

Yes, Email…

36

6.7%

0.7%

8.9%

14.6%

15.5%

16.3%

22.0%

23.3%

31.1%

64.9%

0% 10% 20% 30% 40% 50% 60% 70%

None of the above/not sure

Other

Shopping center websites

Social sites like Facebook/Pinterest

Newspaper(s)

Emails from centers/malls I have chosen

Mobile/Smart Phone Apps

Direct mail to my home

Emails from stores I have chosen

Most Preferred Media Options

Preferred Method of Communication for Receiving

Sales Coupons/Information for Apparel