valuation of shares and debenture. need or purpose when two or more companies amalgamate or one...

TRANSCRIPT

VALUATION OF SHARES AND DEBENTURE

NEED OR PURPOSE

When two or more companies amalgamate or one company absorb another company.

When a company has decided to undergo a process of reconstruction.

When preference shares or debentures are converted into equity shares.

Under a scheme of nationalization when the shares of a company are taken over by the government.

NEED OR PURPOSE

Shares are often pledged as security for raising loans.

When one company acquires majority of the shares of another company it is necessary to value such shares.

The survivors of deceased person who get some shares of company made by will.

To declare NAV by the Finance or an Investment Trust Company.

NEED OR PURPOSE

When shares are held by the partners jointly in a company and dissolution takes place., it becomes necessary to value the shares for proper distribution of partnership property among the partners.

Shares of a private companies are not listed on the stock exchange. If such shares are appraisable by the shareholders or if such shares are to be sold, the value of such shares will have to be ascertained.

When shares are received as a gift, To determine the Gift Tax & Wealth Tax the value of such shares will have to be ascertained.

VALUES OF SHARES

Face Value Book Value Cost Value Market Value Capitalised Value Fair Value

VALUES OF SHARES

Face Value A Company my divide its capital into shares of

@10 or @50 or @100 etc. Company’s share capital is shown as per Face

Value of Shares. Face Value of Share = Share Capital

Total No of Share This Face Value is printed on the share certificate. Share may be issued at less (or discount) or more

(or premium) of face value.

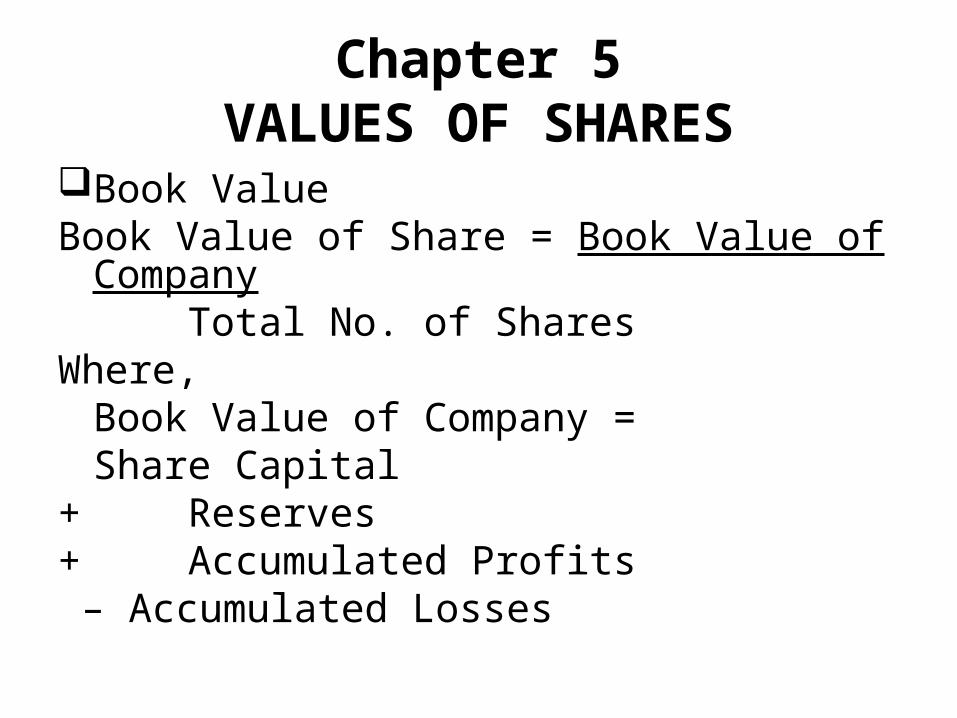

Chapter 5VALUES OF SHARES

Book Value Book Value of Share = Book Value of Company

Total No. of SharesWhere,

Book Value of Company = Share Capital

+ Reserves + Accumulated Profits – Accumulated Losses

VALUES OF SHARES

Intrinsic ValueIntrinsic Value of Share = Net Assets of Company

Total No. of Shareswhere,

Net Assets = Fixed Assets

+ Current Assets+ Investments- Outside Liabilities with Debentures- Preference Share Capital

Chapter 5VALUES OF SHARES

Capitalised Value

Capitalised Value of Share =

Capitalised Value of Profit

Total No. of Shares

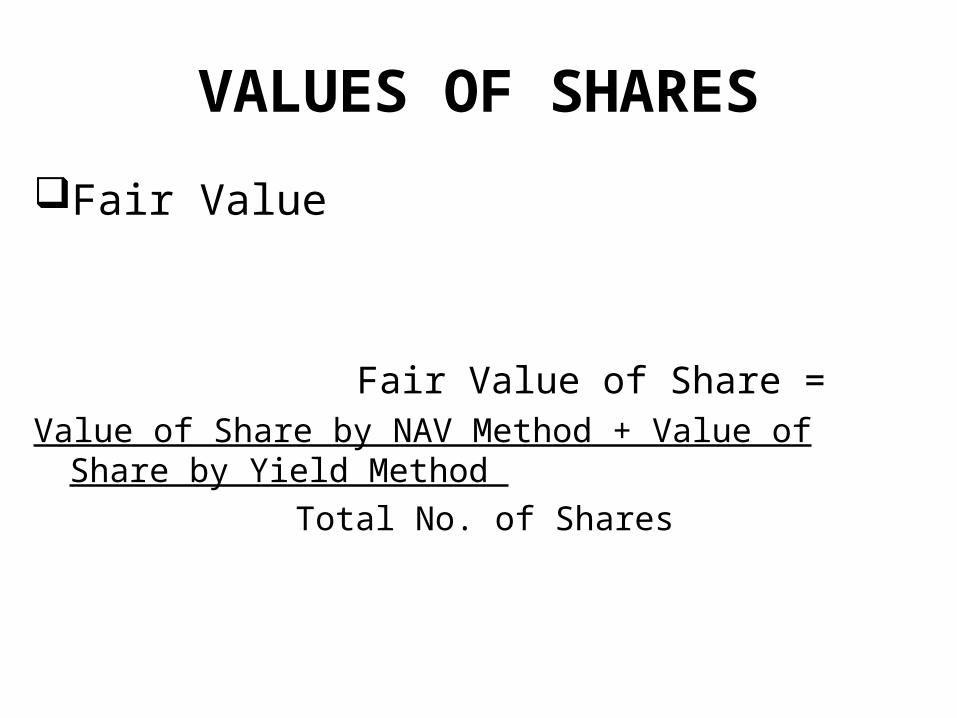

VALUES OF SHARES

Fair Value

Fair Value of Share = Value of Share by NAV Method + Value of Share by Yield

Method

Total No. of Shares

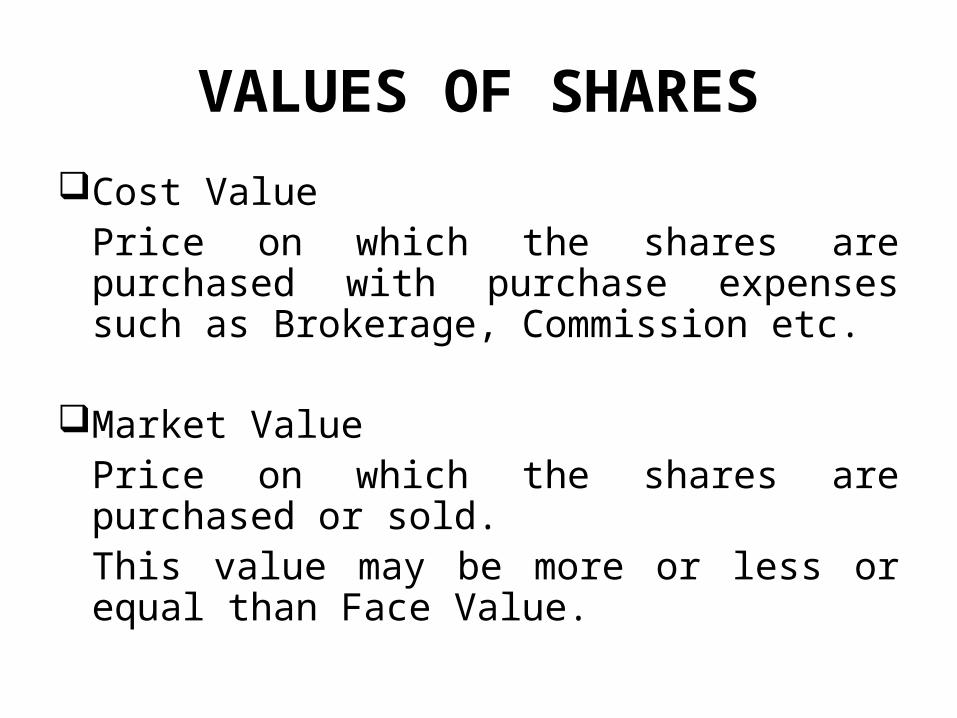

VALUES OF SHARES

Cost ValuePrice on which the shares are purchased with purchase expenses such as Brokerage, Commission etc.

Market ValuePrice on which the shares are purchased or sold.This value may be more or less or equal than Face Value.

METHODS OF VALUATION

Net Assets Value (NAV) Method Dividend Yield Method Earning Capacity (Capitalisation) Method Average (Fair Value) Method

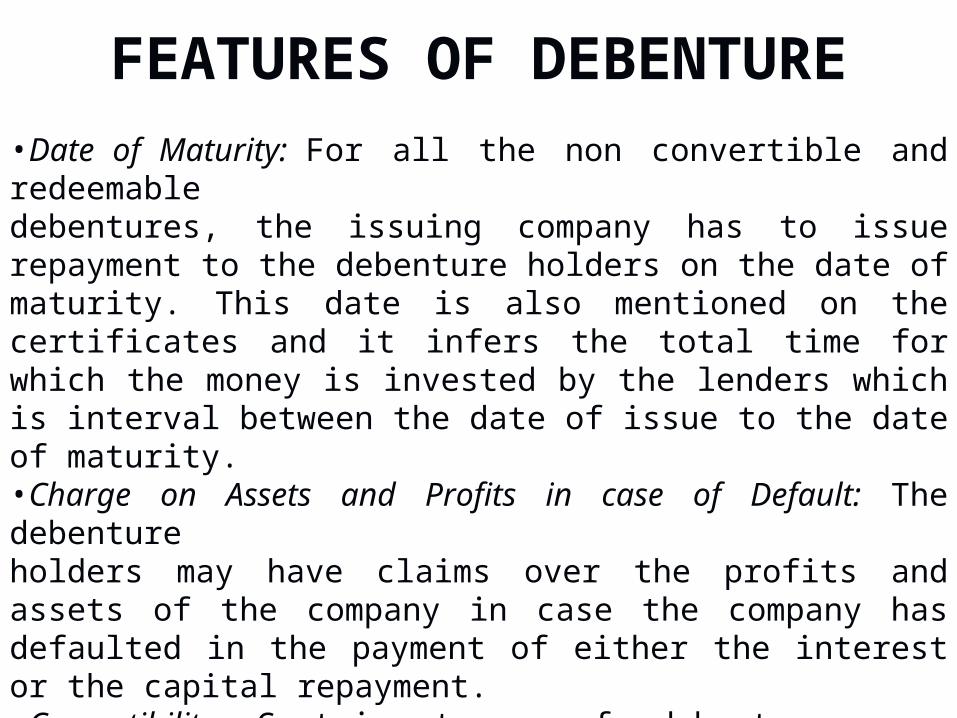

FEATURES OF DEBENTURE•Date of Maturity: For all the non convertible and redeemable debentures, the issuing company has to issue repayment to the debenture holders on the date of maturity. This date is also mentioned on the certificates and it infers the total time for which the money is invested by the lenders which is interval between the date of issue to the date of maturity.•Charge on Assets and Profits in case of Default: The debenture holders may have claims over the profits and assets of the company in case the company has defaulted in the payment of either the interest or the capital repayment.•Convertibility: Certain types of debentures are issued with the option of conversion into equity. The ratio of conversion and the time period after which conversion will take place is mentioned in the agreement of debenture. Debentures may be fully or partly convertible in nature.

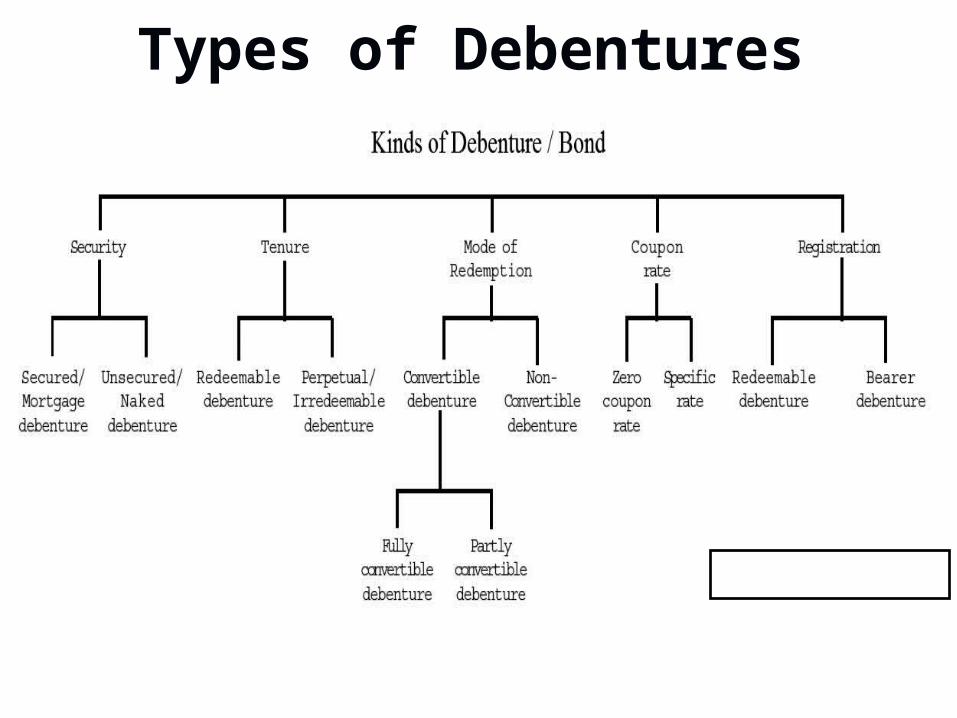

Types of Debentures

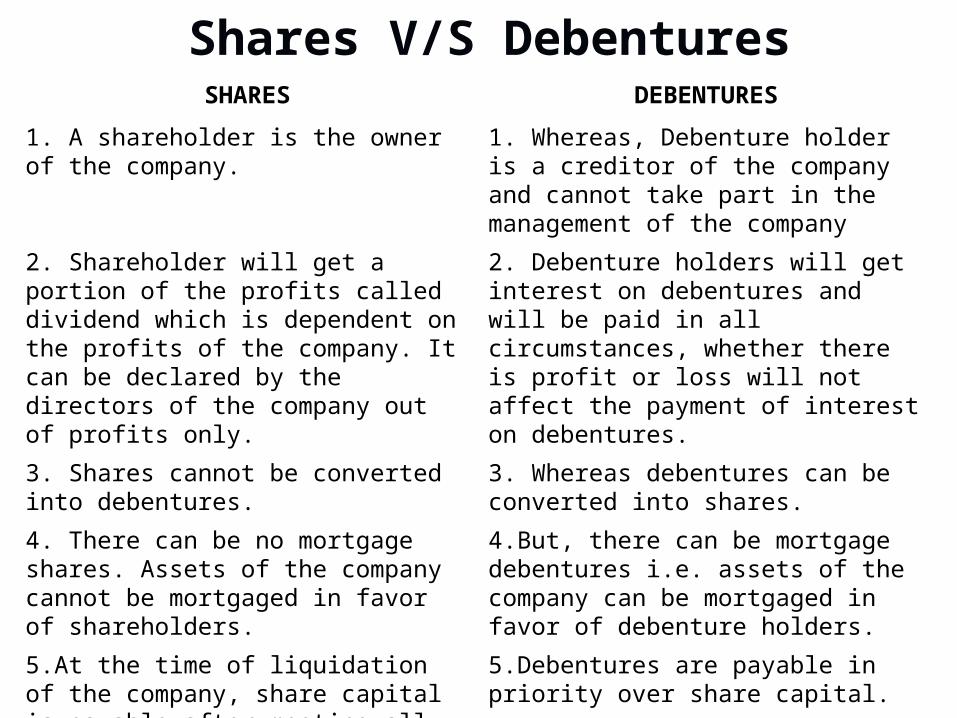

SHARES DEBENTURES

1. A shareholder is the owner of the company.

1. Whereas, Debenture holder is a creditor of the company and cannot take part in the management of the company

2. Shareholder will get a portion of the profits called dividend which is dependent on the profits of the company. It can be declared by the directors of the company out of profits only.

2. Debenture holders will get interest on debentures and will be paid in all circumstances, whether there is profit or loss will not affect the payment of interest on debentures.

3. Shares cannot be converted into debentures.

3. Whereas debentures can be converted into shares.

4. There can be no mortgage shares. Assets of the company cannot be mortgaged in favor of shareholders.

4.But, there can be mortgage debentures i.e. assets of the company can be mortgaged in favor of debenture holders.

5.At the time of liquidation of the company, share capital is payable after meeting all outside liabilities.

5.Debentures are payable in priority over share capital.

Shares V/S Debentures

Advantages/Merits of Debenture Issue:• It enables a company to raise funds for a specific period.• No dilution of control as debenture holders don’t possess voting rights• Debenture (debt) enables the company to Trade on equity. It can pay dividend to equity shareholders at a rate higher than overall ROI.• Debenture holders entitled to a fixed rate of interest. E.g.: 10% debenture• They enjoy priority over other unsecured creditors with respect to debt repayment.• Suitable for conservative investors who seek steady ROI with little or no risk.• Interest on debentures is treated as expense and is tax deductible.• Company can adjust its gearing in accordance to its financial plan.• Debenture holders are regarded as creditors of the company and they receive preference over equity shareholders and preference share holders.•Opting for debentures over the equity as a source of finance saves the profit shares of existing shareholders. Debenture holders do not share profits of the company. They are liable to receive the agreed amount of interest only.

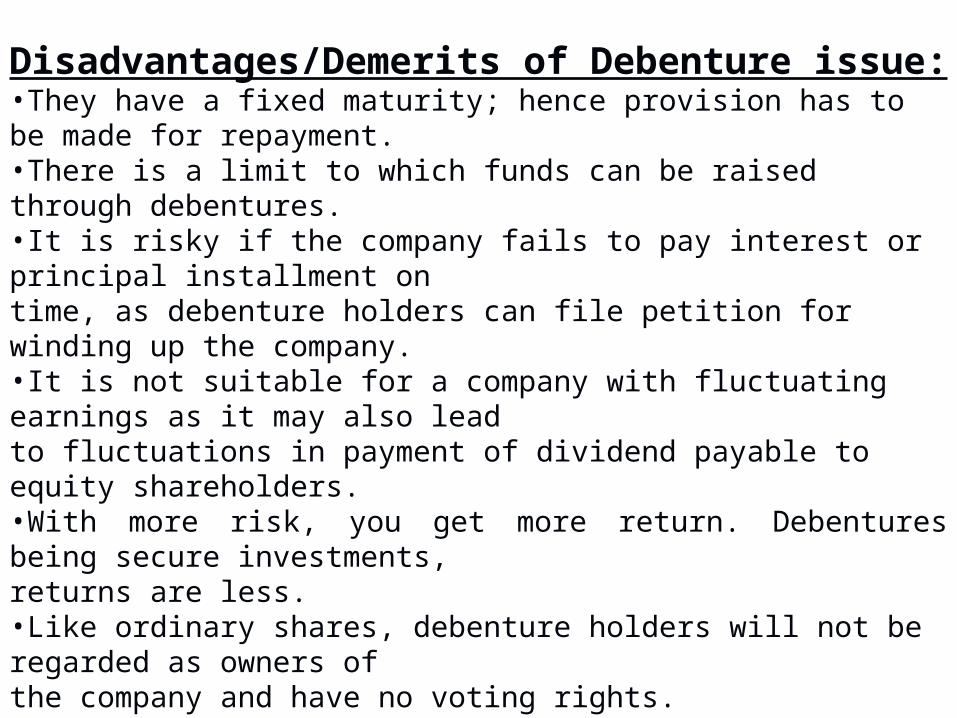

Disadvantages/Demerits of Debenture issue:•They have a fixed maturity; hence provision has to be made for repayment.•There is a limit to which funds can be raised through debentures.•It is risky if the company fails to pay interest or principal installment ontime, as debenture holders can file petition for winding up the company.•It is not suitable for a company with fluctuating earnings as it may also lead to fluctuations in payment of dividend payable to equity shareholders.•With more risk, you get more return. Debentures being secure investments, returns are less.•Like ordinary shares, debenture holders will not be regarded as owners of the company and have no voting rights.•Debenture financing enhances the financial risk.•Debentures are a secured source of raising the long term requirements of funds and usually the security offered to the investors is the fixed assets of the company.•Common people cannot buy debenture as they are of high denominations.