valuation & capital structure - norwea kraft vardar valuation of vardar’s wind power parks and...

TRANSCRIPT

Valuation & Capital Structure Director Power & Renewable Energy Lars Ove Skorpen, Pareto Securities AS

January 31, 2013

Tlf: +47 22 87 87 16 E-mail: [email protected]

Equity: Top 10 deals in Norway Bonds: Top 10 deals in Norway

Source: OSE; Pareto

Pareto is consistently part of the top deals in both equity and debt

0.8

0.9

0.9

1.2

1.3

1.4

1.4

1.5

1.6

2.8

1.2

1.3

1.3

1.3

1.4

1.5

1.5

1.8

2.1

3.0

Chloe Marine

PA Resources

Jasper

BOA

DNO

Songa

FOE

Aker Drilling

Stolt-Nielsen

Ocean Rig

Floatel

Seadrill

Golar LNG

Oro Negro

Deep Drill ing

Aker Solutions

Stolt Nielsen

Pacific Drilling

NAUR

OSX-3

NOKbn

2012

2011

0.4

0.5

0.5

0.6

0.6

0.7

0.9

1.1

2.0

0.4

0.6

0.7

0.7

1.0

1.2

1.3

1.5

1.5

1.9

Prospector

SpB1 NN

DETNOR

Panoro Energy

DOF

Höegh LNG

Archer

Standard Drilling

Sevan Drilling

Aker Drilling

NORECO

Selvaag Bolig

Songa Offshore

SpB1 SMN

DETNOR

Höegh LNG

REC

SpB1 SR

Dockwise

NAUR

NOKbn

2012

2011

4.0

2

M&A – proven capabilities within renewable energy

M&A – Hydro power

M&A - Utilities

M&A – Other renewable/ infrastructurere

Experience to related renewable

and industry sectors

Best-in-class execution within the utility sector

Top-ranked M&A advisor within the

hydro power sector

Financial Advisor to E-Co Energi AS

Sale of E-CO’s 30% stake in EB Kraftproduksjon

Financial Advisor to Fjellkraft AS

Sale of 78% of Fjellkraft

Financial Advisor to Hafslund ASA

Acquisition of Viken Fjernvarme AS from the

City of Oslo

Financial Advisor to Boliden AB

Sale of AS Tyssefaldene and power contract (20

TWh) Financial Advisor to Oslo

kommune

Purchase of 20% of E-CO Vannkraft

Financial Advisor to Orkla ASA

Sale of 7 power plants

Financial advisor to Malvik municipality

Merger of Malvik Everk and TrønderEnergi Nett

Financial advisor to several municipal

owners

Sale of 49% of the company

Financial advisor to several municipal

owners

Sale of shares in the company

Financial advisor to Gjøvik and Østre Toten

kommuner

Share sale

Financial advisor to Eidsiva

Merger of HEAS, HrE and LGE.

Merger with Hedemark Energi (distr. and retail)

Financial advisor to the City of Oslo

Merger with Hafslund

Financial Advisor to Hafslund ASA

Sale of Hafslund’s fiber network activities to EQT

Financial advisor to OCAS

Sale of technology assets from OCAS to Vestas

Financial advisor to Fortum

Sale of Fortum’s ownershare (24,5%)

M&A - Wind Best knowledge within the wind

sector

Financial advisor to TrønderEnergi AS

Acquisition of 100% of the shares in Trondheim

Energi Nett

Financial Advisor to SKS AS

Acquistions of Norsk Hydros’s stake in SKS

Produksjon AS

Financial advisor to Agder Energi

Valuation of Agder Energi’s wind power

portfolio

Financial advisor to Statoil ASA

Sale of Arctic Wind to Finnmark Kraft

Financial advisor to Vardar

Valuation of Vardar’s wind power parks and projects in the Baltic

States

Financial advisor to Statoil ASA

Sale of Sarepta Energi (50%) to TrønderEnergi

Kraft

Financial advisor to Statoil ASA

Sale of smaller wind power parks and

projects

Financial advisor to Havgul AS

Sale of offshore wind project – Havsul I to

Vestavind

Financial advisor to Nettpartner and

Fredrikstad Energi

Merger of Nettpartner and EB Energimontasje

4

Critical assumptions in valuation of a wind park

WACC

Terminal value

Economic lifetime

Other

Wind speed (m/S) and full load hours

Size of park & expansion possibilities

Grid (central & regional)

Access to park (24/7 and seasons)

Climate (temperature, snow, icing, extreme wind, saltcontent)

Geology and topography

Site characteristics

Economic Lifetime of a windpark

6

Critical assumptions in valuation of a wind park

Power price Price area

Seasonality (day/night and season)

Price of ElCert

Power price

Opex

Service agreement with turbine supplier

Feed-in cost and transmission loss

Land lease & property tax

Turbine

Infrastructure costs

Roads & internal roads

Quay (length, depth, storage capability and load capacity)

Grid (investment contribution?)

Transformers & cabling

Capex

Low spot price in 2012 - also in longer perspective

7

11.210.3

18.620.1

29.1

24.223.5

39.1

22.4

36.9

30.6

42.5

36.7

23.4

0

5

10

15

20

25

30

35

40

45

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

øre/kWh

0

10

20

30

40

50

60

70

80

90

100

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Kraftpris Elsertifikat Total pris Årlig gj.snitt og gj.snitt av forwardkursene

Øre / kWh

However the combined price of approx. 50 øre/kWh is challenging with regard to building new capacity

8

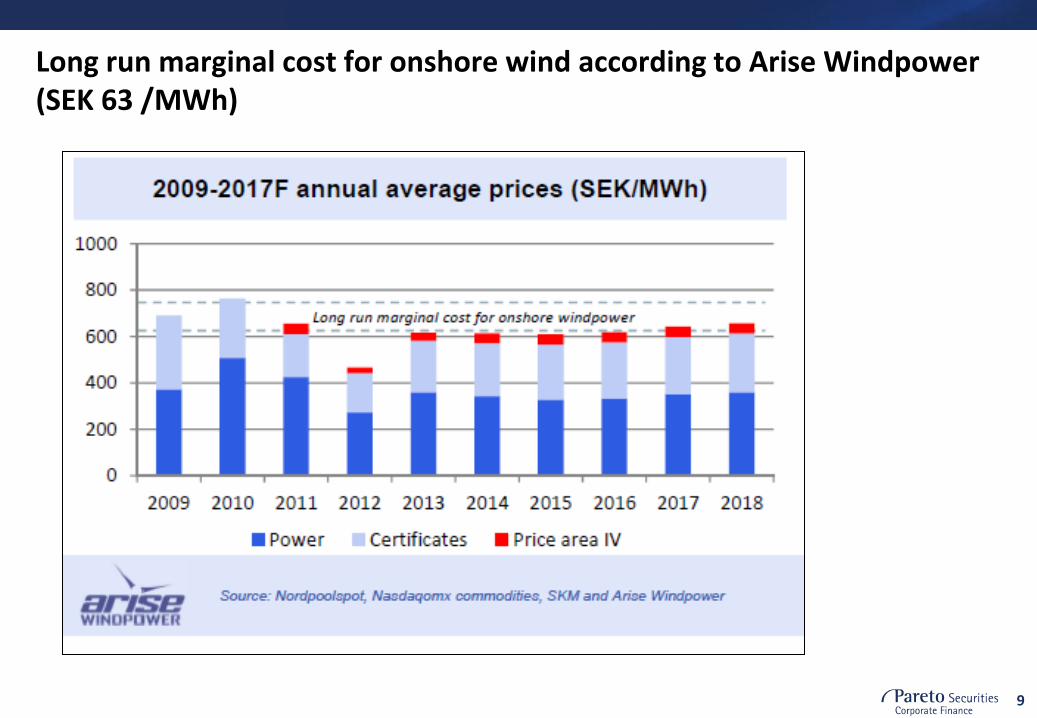

64,7

56,7

63,7

52,7

37,8

49,8

2012

Powerprice ElCert price Tot. price Average price

Long run marginal cost for onshore wind according to Arise Windpower (SEK 63 /MWh)

9

10

Valuation case

ElCert prices + inflation

3200 full load hours

20 years assumed

No terminal value

ElCert price

CAPEX

OPEX

Economical life

All in CAPEX NOK 11m/MW

Assumed 17 øre/kWh

11

Source and use of capital

Many are cautious and scaling down their balance sheet

Good relations to several banks important

Shop around Banks

Increased interest in bonds and new issuers are entering the market

Well functioning market

Construction risk an issue Bonds

Owners will have to adjust their view on future dividends

Utility owners and dividend

Utilities will have to prioritize hard between various projects

Investments

12

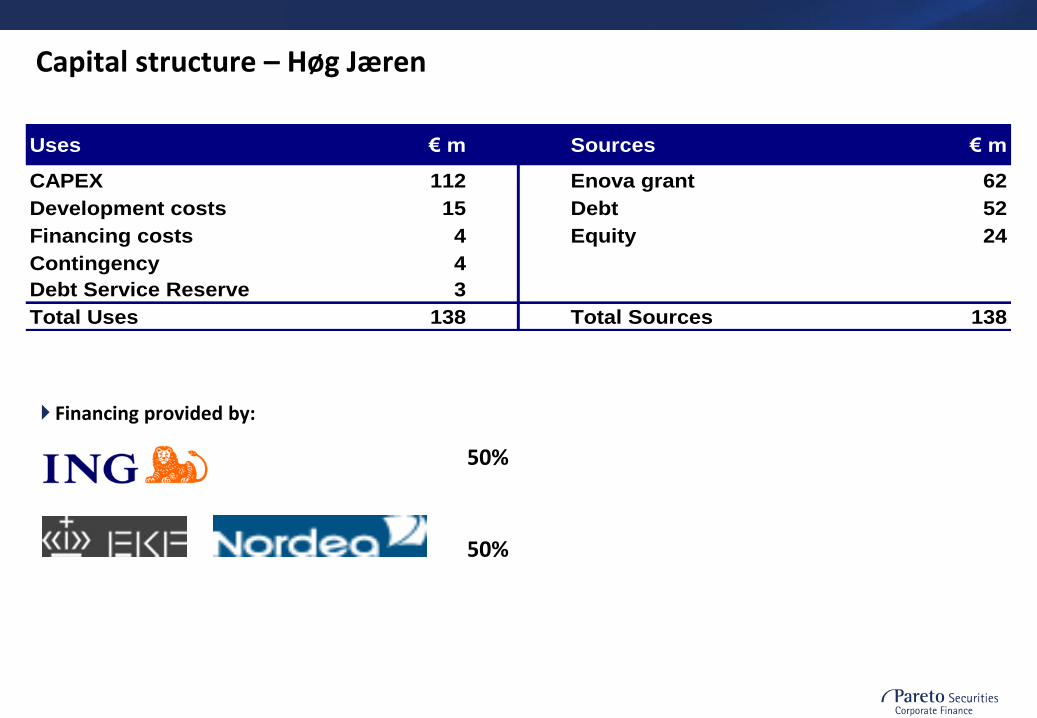

Falling equity ratio for Norwegian utilities together with lower power prices, creates challenges in financing wind parks

Equity % – historical development

Capital structure – Høg Jæren

Financing provided by:

50%

50%

Uses € m Sources € m

CAPEX 112 Enova grant 62

Development costs 15 Debt 52

Financing costs 4 Equity 24

Contingency 4

Debt Service Reserve 3

Total Uses 138 Total Sources 138

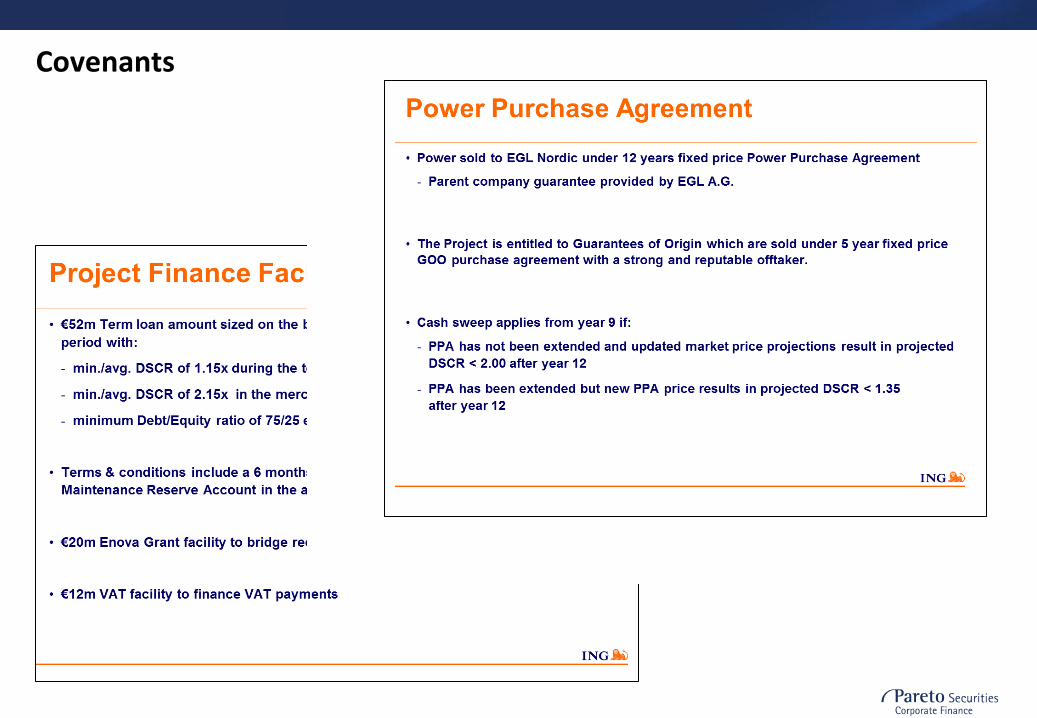

Covenants

Summary - valuation Norway vs. Sweden

15

Norway Sweden

Wind speed Wind speed >

Depreciation Depreciation < Taxes Taxes <

CAPEX pr MW CAPEX pr MW < Feed-in cost Feed-in cost <

Investment contribution Investment contribution >

Permitting process Permitting process ≤

Area prices Area prices ≤

ElCert duration ElCert duration <

Property tax Property tax ≤

Grid access Grid access <

Interest rate Interest rate <

16

Contact details and disclaimer

Disclaimer

These materials have been prepared by Pareto Securities AS and/or its affiliates (together “Pareto”) exclusively for the benefit and internal use of the client named on the cover in order to indicate, on a preliminary basis, the feasibility of one or more potential transactions. The materials may not be used for any other purpose and may not be copied or disclosed, in whole or in part, to any third party without the prior written consent of Pareto.

The materials contain information which has been sourced from third parties, without independent verification. The information reflects prevailing conditions and Pareto’s views as of the date of hereof, and may be subject to corrections and change at any time without notice. Pareto does not intend to, and the delivery of these materials shall not create any implication that Pareto assumes any obligation to, update or correct the materials.

Pareto, its directors and employees or clients may have or have had positions in securities or other financial instruments referred to herein, and may at any time make purchases/sales of such securities or other financial instruments without notice. Pareto may have or have had or assume relationship(s) with or engagement(s) for or related to the relevant companies or matters referred to herein.

The materials are not intended to be and should not replace or be construed as legal, tax, accounting or investment advice or a recommendation. No investment, divestment or other financial decisions or actions should be based solely on the material, and no representations or warranties are made as to the accuracy, correctness, reliability or completeness of the material or its contents. Neither Pareto, nor any of its affiliates, directors and employees accept any liability relating to or resulting from the reliance upon or the use of all or parts of the materials.

Oslo (Norway) Pareto Securities AS Dronning Mauds gate 3 PO Box 1411 Vika N-0115 Oslo NORWAY Tel: +47 22 87 87 00 Fax: +47 22 87 87 10

Stavanger (Norway) Pareto Securities AS Haakon VIIs gate 8 PO Box 163 N-4001 Stavanger NORWAY Tel: +47 51 83 63 00 Fax: +47 51 83 63 51

Bergen (Norway) Pareto Securities AS Olav Kyrres gate 22 PO Box 933 N-5808 Bergen NORWAY Tel: +47 55 55 15 00 Fax: +47 55 55 15 50

Kristiansand (Norway) Pareto Securities AS Vestre Strandgate 19A N-4611 Kristiansand NORWAY Tel: +47 21 50 74 20 Fax: +47 21 50 74 99

Trondheim (Norway) Pareto Securities AS Nordre gate 11 PO Box 971 Sentrum N-7410 Trondheim NORWAY Tel: +47 21 50 74 60 Fax: +47 21 50 74 61

Singapore Pareto Securities Asia Pte Ltd 16 Collyer Quay #27-02 Hitachi Tower Singapore 049318 SINGAPORE Tel: +65 6408 9800 Fax: +65 6408 9819

Malmö (Sweden) Pareto Öhman Stortorget 13 S-211 22 Malmö SWEDEN Tel: +46 40 750 20 Fax: +46 40 750 30

Website: www.paretosec.no Bloomberg: PASE (go) Reuters: PARETO

Pareto Offshore AS Dronning Mauds gate 3 PO Box 1411 Vika N-0115 Oslo NORWAY Tel: +47 22 87 87 00 Fax: +47 22 87 87 10

Pareto Shipping AS Dronning Mauds gate 3 PO Box 1411 Vika N-0115 Oslo NORWAY Tel: +47 22 87 87 00 Fax: +47 22 87 87 10

Stockholm (Sweden) Pareto Öhman Berzelii Park 9 Box 7415 S-103 91 Stockholm SWEDEN Tel: +46 8 402 50 00 Fax: +46 8 20 00 75

New York (US) Pareto Securities Inc 150 East 52nd Street, 29th Floor New York NY 10022 USA Tel: +1 212 829-4200 Fax: +1 212 829-4201