utopia feasibility assessmentsteveshu.typepad.com/steve_shus_weblog/files/dean_report.pdfutopia...

TRANSCRIPT

UTOPIA Feasibility Assessment

– Eleven City Build –

May 13, 2004

DEAN & COMPANYSTRATEGY CONSULTANTS

WASHINGTON, D.C.

1DEAN & COMPANYagenda,05-13-04,UTPDYN01A.ppt npl,

Agenda

• Overview

• Demand Benchmarks

• Cost Benchmarks

• Sensitivities & Scenarios

2DEAN & COMPANY

Summary

• Dean & Company have evaluated the feasibility of UTOPIA’s Eleven City Build with an emphasison the Phase 1 plan. We have evaluated Phase 1 on a standalone basis. It is our understandingthat the future phases will follow, based on Phase 1.

• While it represents a smaller footprint, the Phase 1 plan remains feasible, given the fundamentals:

— Conservative and Expected take rates are within the achievable range given the experience of other broadbandoverbuilders and competitive service providers.

— Planned build out rates are conservative, particularly since the scope of construction is lower than the 18 city plan

— The Open Access, IP-based business model remains consistent with the evolution of competition and technology inthe telephone, internet, and video services markets

— Wholesale price levels are sufficiently low for service providers to become profitable on UTOPIA, and arecomparable to or more attractive than wholesale access over the incumbent telephone and cable networks. Thisholds even considering the price pressure on local and long distance telephone services placed by voice-over-IPservices.

— Active/Ethernet technology choice is well-suited over the long term for UTOPIA’s model, leverages a broadsupplier base, and has minimal risk of obsolescence by other technologies, including wireless

— Projected capital and operating costs are within the range of comparable projects, and take into account theimportant costs drivers for FTTH/B networks (e.g. aerial vs. buried mix, replacement lifecycles). The Phase 1 planis large enough that fixed costs (e.g. NOC) are lower on a per-subscriber basis than the costs that are driven byhomes passed (terminal costs) and by subscriber density (distribution, maintenance) - i.e. Phase 1 is large enough toachieve required economies of scale in construction and operation.

3DEAN & COMPANY

Summary - continued

• The primary areas of risk relate to the competitive environment:

— The competitive response from Comcast and Qwest may be escalated relative to the plan assumptions, potentially drivingdown market price levels, increasing churn, and/or putting pressure on recovery of installation fees. While the serviceproviders on UTOPIA’s network bear the initial impact of these pressures, they could ultimately flow through to UTOPIAin order to maintain service provider profit margins as an incentive to continue their marketing efforts.

— The smaller footprint means that UTOPIA is more dependent on the success of fewer retail service provider tenants in thefirst 2-3 years, vs.the larger build where the diversity of service providers could expand more quickly. On the positiveside, the smaller footprint will facilitate tighter operational coordination in signing up and provisioning subscribersbetween UTOPIA and its initial retail service providers, one of the concerns in the larger build plan.

— The usage-tiered wholesale pricing model for data services is well-structured to capture the value of increasing datatraffic over the long term. This traffic can be expected to grow dramatically with increased internet use and migration ofvoice and video service to internet protocols. However, customer acceptance of usage-based pricing is uncertain givenhistorical experience and counter-marketing by incumbent service providers.

• The Phase 1 plan has a high degree of robustness to these risks

— Downside sensitivity analysis and scenarios show sufficient cash flow to meet the projected debt obligations across thefull range of cases we examined.

— In cases that combine multiple downsides: take rates lower than the conservative view, price war lasting 3 years or morethat flows through to UTOPIA, and construction and operating cost overruns of 10% and 20% respectively, additionalfunding of $1MM to $12MM would be required over the 3rd to 5th year of operation. Past that point, UTOPIA wouldgenerate positive cash surplus even in outcomes with combined downsides.

— While UTOPIA has no control over the competitive environment, UTOPIA is in a position to proactively manage projectcosts and retail tenant performance. Success in managing these two areas of risk would keep the potential for additionalfunding to a level under $1-2 MM.

4DEAN & COMPANYagenda,05-13-04,UTPDYN01A.ppt npl,

Agenda

• Overview

• Demand Benchmarks

• Cost Benchmarks

• Sensitivities & Scenarios

5DEAN & COMPANY

0%

10%

20%

30%

40%

50%

60%

70%

80%

0 1 2 3 4 5 6 7 8

004,05-13-04,UTPDYN01A.ppt JTS, cgL7

Take-Rates Over Time– One or More Services –

Given the experiences of other municipalities and over-builders, UTOPIA’spredicted take-rates over time are feasible

Municipal Networks

TakeRate

(Percentof

HomesPassed)

Years After Availability

Glasgow, KY

Cedar Falls, IA

Newnan, GA

Tacoma, WA

Ashland, OR

Harlan, IA

Overbuilder Networks

Years After Availability

Astound

Scottsboro, AL

AverageTake Rates

29% 42% 45%43%Average

Take Rates16% 46% 45%36% 41% 56%

Bristol, VA

Full Build

Phase 1Expected

Phase 1Conservative

TakeRate

(Percentof

HomesPassed)

UTOPIA Plan

0%

10%

20%

30%

40%

50%

60%

70%

80%

0 1 2 3 4 5 6 7 8

UTOPIA Plan

RCN

Altrio (business case)

Utilicom

EverestCommunications

Knology

SureWest

SpanishForks

Provo

Full Build

Phase 1Expected

Phase 1Conservative

6DEAN & COMPANY008,05-13-04,UTPDYN01A.ppt kaL, jrb5

Overbuilder Customer Demand for Bundles– By Product Mix –

Expectations of selling service bundles are in line with other “triple play”networks

0%

20%

40%

60%

80%

100%

Percent ofSubscriberstaking one,

two, orthree

services

TriplePlay50%

Any 230%

Any 120%

2-3ServiceBundles

63%

1 to 2services

37%

Bundle34%

1 to 2services

66%

3ServiceBundles

50%

A LaCarteand 2

ProductBundles

50%

Any 115%

Any 237%

TriplePlay48%

Any 118%

Any 237%

TriplePlay45%

SureWest RCN Harlan, IAEverestUTOPIA(2009)

UTOPIA(2005)

Source:Company statements, Dean & Company research

7DEAN & COMPANY

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

016a,05-13-04,UTPDYN01A.ppt JTS, jrb2

Product Mix– 2002 vs. UTOPIA Conservative Case Scenario –

The variation between the expected UTOPIA product mix and benchmarks aredirectionally consistent with differences in UTOPIA’s market demographics andbusiness model

Percentof

Customers

Voice Video Data

Utopia 77%

Utopia61%

Utopia 92%

Note: Take rates decline over time.Ashland, OR; Glasgow, KY, and Tacoma, WA assume 12% of Internet customers do not have cable TV. Harlan, IA assumes 1% of Voice customers do not have cable TV.

RC

NA

stou

ndE

vere

st

Ash

land

, OR

Ced

ar F

alls

, IA

Gla

sgow

, KY

Kno

logy

Util

icom

Har

lan,

IAN

ewna

n, G

A

Tac

oma,

WA

Scot

tsbo

ro, A

L

RC

NA

stou

ndE

vere

st

Ash

land

, OR

Ced

ar F

alls

, IA

Gla

sgow

, KY

Kno

logy

Util

icom

Har

lan,

IAN

ewna

n, G

A

Tac

oma,

WA

Scot

tsbo

ro, A

L

RC

NA

stou

ndE

vere

stK

nolo

gyU

tilic

om

Har

lan,

IAN

ewna

n, G

A

Utopia likely to exceedbenchmark average given their

lesser focus on voice

Utopia likely to exceedbenchmarks given higher regional

demand for internet

Utopia likely to come underbenchmarks given their focus

on video

8DEAN & COMPANY

UTOPIA has attractive residential market environment

019,05-13-04,UTPDYN01A.ppt sbg, JTS1

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

UTOPIA Region U.S. Average0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

UTOPIA region U.S. Average

Source: UTOPIA Survey; U.S. Department of Commerce (2002) , MediaWeek

74%

54%

59%

43%

10%

5%

4%

7%

Dial-Up

DSL

Cable Modem

64%

84%

31%

15%

33%

69%

Satellite

Cable

Internet Penetration– % of HH –

Video Services Penetration– % of HH –

U.S. Census %for all Utah

Internet services are thecornerstone for FTTH success

Typical of older TCI cable systems -implies upside for higher quality network

Residential Service Intensity Comparisons– UTOPIA vs. the National Average –

9DEAN & COMPANY

$40 $41

$98

$91

$0

$20

$40

$60

$80

$100

$120

002a,05-13-04,UTPDYN01A.ppt JTS, kaL6

UTOPIA Revenue per Subscriber Benchmarks– Voice, Video, and Data Triple Play Example –

UTOPIA’s wholesale service charges are in a range where service providers havesufficient margin to be profitable

NationalAverage

UTOPIASpend

Average RetailConsumer Spend

$/Month/HH

Service Provider GrossMargin opportunitysignificantly greater thanthe 40% baseline neededfor an attractive serviceprovider business case

ConservativeCase ARPU

(2005)1

ConservativeCase ARPU

(2008)

UTOPIA’s WholesaleARPUs

1 Includes Access Charge

10DEAN & COMPANY

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

To evaluate service providers’ business cases, we assumed bundled offers similarto other triple play providers

020a,05-13-04,UTPDYN01A.ppt npl,

Price Comparisons– Triple Play Packages –

Modeled prices for UTOPIAService Providers

Priceper

Month

Source: UTOPIA Model,company websites and representatives

Basic Mid Premium FullCircuit

SuperCharged

TotallyWired

TotallyWired Plus

ResilinkGold

ResilinkPlatinum

Local California National

Everest RCN SureWest

Price $82.05 $119.45 $153.48 $84.95 $109.95 $139.95 $149.95 $135.00 $159.00 $109.95 $119.95 $142.90

Local Phone 1 line 1 line 2 lines 1 line 1 line 1 line 1 line 1 line 2 lines 1 line 1 line 1 lineFeatures 3 3 6 0 6 11 11 3 4 4 including

voicemail4 including voicemail

4 including voicemail

LD - Free Minutes 100 150 120 0 0 Unlimited

Basic Cable Channels 70+ 70+ 70+ 70+ 81, 1 box 81, 2 boxes

Digital Cable Channels 100 150 150 40+ 40+ 40+ 40+ 35 35 150 180 230 +Internet 1M 10 M/Sec,

10G/Mo.10 M/Sec, 20G/Mo.

256K 1.5M 3M 3M 3M 3M 10M 10M 10M

Price $82.05 $119.45 $153.48 $84.95 $109.95 $139.95 $149.95 $135.00 $159.00 $109.95 $119.95 $142.90

Local Phone 1 line 1 line 2 lines 1 line 1 line 1 line 1 line 1 line 2 lines 1 line 1 line 1 lineFeatures 3 3 6 0 6 11 11 3 4 4 including

voicemail4 including voicemail

4 including voicemail

LD - Free Minutes 100 150 120 0 0 Unlimited

Basic Cable Channels 70+ 70+ 70+ 70+ 81, 1 box 81, 2 boxes

Digital Cable Channels 100 150 150 40+ 40+ 40+ 40+ 35 35 150 180 230 +Internet 1M 10 M/Sec,

10G/Mo.10 M/Sec, 20G/Mo.

256K 1.5M 3M 3M 3M 3M 10M 10M 10M

11DEAN & COMPANY

($10)

$0

$10

$20

$30

$40

0 10,000 20,000 30,000 40,000 50,000

017,05-13-04,UTPDYN01A.ppt unk, cgL3

Service Provider Business Case– Combination of Residential and Business Customers –

The first phase plan is large enough to support two to three service providers

ServiceProvider

NPV($MM)

Service Provider Customers (after ramp)

Video Only(renting UTOPIA head-end)

Voice and Internet

Voice Only(Local + LD, Circuit switched)

Triple Play

Internet Only

Note: Based on proposed UTOPIA service charges as of April 2004 plan, assumes that service provider offer 20% discount to standard retail price

Conservative Case:28,752 Connected Homes

Expected Case:29,259 Connected Homes

Additional Subscribers

• Phase 2: 51,167• Phase 3: 82,587

12DEAN & COMPANY

$39.99

$34.99

$24.99

$14.99

$19.95

$29.99

$19.99

$12.25

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

041,05-13-04,UTPDYN01A.ppt JTS, cgL1

VoIP Pricing– Residential Calling Plans –

VoIP offers will continue to provide service providers with sufficient margin forprofitability

1 Includes a larger local area2 6 months into offer at $19.99/month

MonthlyCharges

RegionalPlan

NationalPlan

NationalPlan

Local Regional1

PlanNational

PlanAT&T

CallVantage2UTOPIA

WholesalePricing

Unlimited0

3.9¢/minute

UnlimitedUnlimited

–

UnlimitedUnlimited

–

Unlimited5003.9¢

Unlimited5003.9¢

UnlimitedUnlimitedUnlimited

UnlimitedUnlimited

–

Local MinutesLD MinutesLD Rate

Voice Glo VonagePacket 8

Access Charge

Line Charge

$1.25

$11.00

13DEAN & COMPANY

Percentage ofPeople WhoTake Service

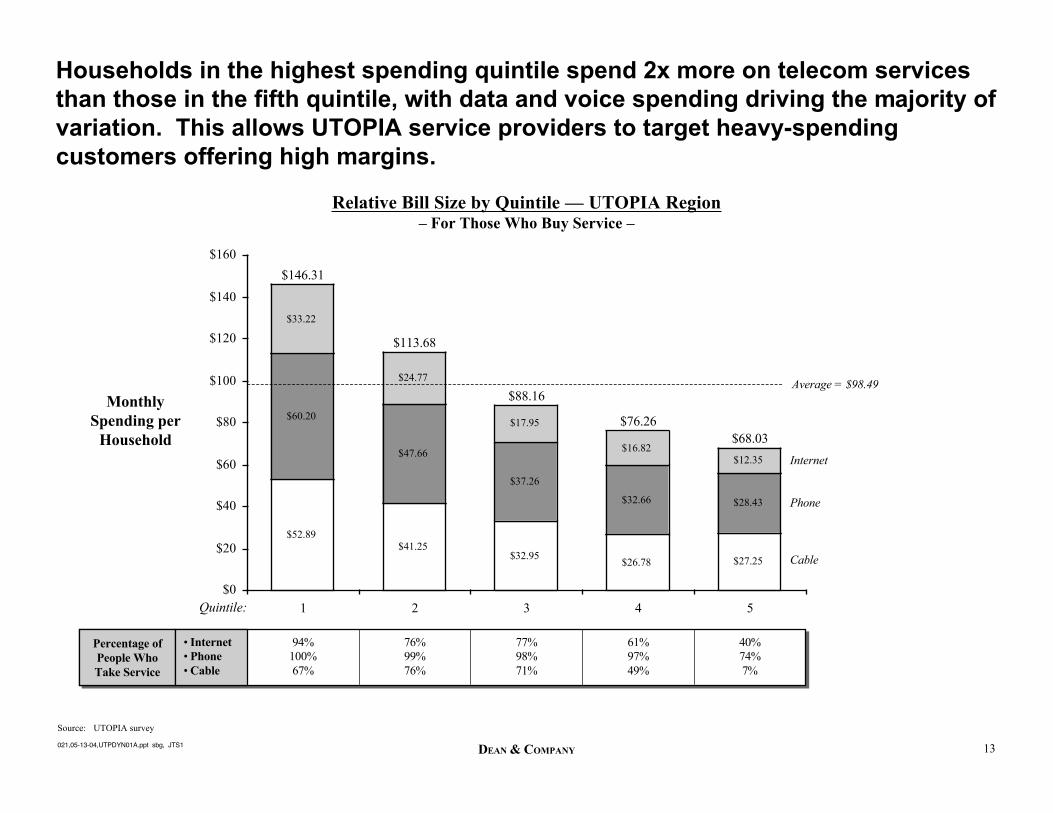

Households in the highest spending quintile spend 2x more on telecom servicesthan those in the fifth quintile, with data and voice spending driving the majority ofvariation. This allows UTOPIA service providers to target heavy-spendingcustomers offering high margins.

021,05-13-04,UTPDYN01A.ppt sbg, JTS1

Relative Bill Size by Quintile — UTOPIA Region– For Those Who Buy Service –

$52.89$41.25

$32.95$26.78 $27.25

$60.20

$47.66

$37.26

$32.66 $28.43

$33.22

$24.77

$17.95

$16.82$12.35

$0

$20

$40

$60

$80

$100

$120

$140

$160

1 2 3 4 5

MonthlySpending per

Household

• Internet• Phone• Cable

$146.31

$113.68

$88.16

$76.26$68.03

Internet

Phone

Cable

94%100%67%

76%99%76%

77%98%71%

61%97%49%

40%74%7%

Quintile:

Average = $98.49

Source: UTOPIA survey

14DEAN & COMPANYagenda,05-13-04,UTPDYN01A.ppt npl,

Agenda

• Overview

• Demand Benchmarks

• Cost Benchmarks

• Sensitivities & Scenarios

15DEAN & COMPANY

$1

$10

$100

10,000 100,000 1,000,000 10,000,000 100,000,000

045,05-13-04,UTPDYN01A.ppt npl,

Network Operating Expense Comparison — NOC and Field– $ per Home Passed –

UTOPIA’s scale-adjusted projected network operations cost is comparable toother operators

Source: UTOPIA cost and revenue model, April 2004; company statements; Dean & Company research

Note: NOC costs include asset management, headend, co-location, and interconnect expense. Field expenses include field maintenance and electronics maintenance.

Log/LogLog/Log

$/Home

Passed/Month

Total Homes Passed

UTOPIAPhase 1

ExpectedUTOPIAPhase 3

Expected

RCN

Typical MSO

Qwest

90% Scale

16DEAN & COMPANY

$264

$200

$99$93

$80

$177

$0

$50

$100

$150

$200

$250

$300$37 $37

$32

$17

$0

$10

$20

$30

$40

006a,05-13-04,UTPDYN01A.ppt unk, cgL5

Fiber Construction Costs– Benchmarks –

UTOPIA’s planned fiber construction costs are consistent with our experience

$/Mile(000s)

$/Mile(000s)

Aerial Fiber Underground Fiber

Public UtilityDistrict

Telecommu-nications

Study

BeltwayCable

Services

CableOverbuilder

PublicUtilityDistrict

Telecom-munications

Study

Seattle,Washington

TCSCommu-nications

BeltwayCable

Services

Palo AltoUTOPIA UTOPIA

Note: Contingency has been excluded

17DEAN & COMPANY007,05-13-04,UTPDYN01A.ppt ini, cgL4

Capital Cost Comparison– Distribution, Core, NOC, NIU –

UTOPIA’s projections for total capital cost per subscriber are in the range of otherbroadband and fiber network overbuilds

Note: Palo Alto costs include core network and subscriber drops but not headendCapital cost per subscriber defined as cumulative capital expenditures over installed subscriber base

Capital Costper Subscriber

(Log Scale)

Penetration — Subs per Home Passed

Palo AltoFTTH

RCNHFC

Murray ElectricHFC

Ashland, ORHFC

EverestHFC

Scottsboro, ALHFC

Harlan, IA

ChiliclotheTelephone

VDSL

Eagle BBFTTH

Corning EstimateFTTH in New

Housing Development

Hometown, Morris MNFTTH

Kutztown, PAFTTHAmerican

BroadbandHFC

Palo AltoFTTH

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000$8,000

$9,000

Source: UTOPIA Business Model, Palo Alto business case, company websites

Actual Build CostsPlanned Build CostsUTOPIA 18 City BuildPhase 1 Expected

$1,000

$10,000

20% 30% 40% 50% 60% 70% 80%

18DEAN & COMPANY001,05-13-04,UTPDYN01A.ppt JTS, cgL5

Build-Out Rate Benchmarks

UTOPIA’s build-out rate appears to be achievable

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

0 1 2 3 4 5 6 7 8 9 10

Years of Operations

HomesPassed

UTOPIA 18 city build

RCN(includes

acquisitions inyears 4 & 5)

Altrio - plan

Phase 3Phase 2Phase 1

19DEAN & COMPANY

FTTH deployments appear to be roughly split between Active/Ethernet vsPassive/ATM

023,05-13-04,UTPDYN01A.ppt sbg,

FTTH Deployments– 2002 –

• Grant County - WA (ZIPP)• WIN - Sacramento WA (include HFC drops)• Lyse Tele - Norway• Fastweb - Italy• B2 - Sweden• Competisys - American Canyon/CA

• Palo Alto Utility - Palo Alto, CA

• Bell South - Dunwoody, GA (trial)• Blair Tel. - NE• Rye Tel - Colorado City, CO• NexTech - KA• Itex Communications - TX• Baldwin Telecom - WI• Bristol Utilities - VA• Hometown Solutions - Morris, MN• Kutztown, PA• SBC - Mission Bay, CA

Ethernet/IP

ATM

Active Passive/PON

10-20K80-100K

<10K

• Few

40-60K

Source: Dean & Company Analysis, KMI estimates

20DEAN & COMPANY

Active fiber Ethernet solutions have the advantage of support by establishedsuppliers, and Cisco in particular

024,05-13-04,UTPDYN01A.ppt sbg,

FTTH Technology Suppliers– Partial List –

NewAllOptic

One Path

Optical Solutions

Paceon

Quantum Bridge

Salira

Terawave

WWP

Riverstone

Optical Access

Extreme Networks

EstablishedNEC Illuminant

Nortel

Cisco

Pirelli

Lucent

Alcatel

Marconi

APON

+

+

+

+

+

+

+

+

EPON

+

+

+

+

A-Active E-Active

+

+

+

3

+

+

+

+

+

Resolution into a stable marketlikely to wait until RBOCs begin

large scale deploymentLeverages existing

metro-opticalequipment markets

21DEAN & COMPANYagenda,05-13-04,UTPDYN01A.ppt npl,

Agenda

• Overview

• Demand Benchmarks

• Cost Benchmarks

• Sensitivities & Scenarios

22DEAN & COMPANY032a,05-13-04,UTPDYN01A.ppt jrb, jrb2

Phase 1 Downside Scenarios– Details –

The various cases test the Phase 1 plan’s ability to withstand competitivepressures, demand declines, and cost overruns

DemandAssumptions

CostAssumptions

• 100% recovery of premise wiring

• Residential Churn: 16%

• Business Churn: 9%

• No price war

PlanPlan Escalated CompetitiveResponse

Escalated CompetitiveResponse Assumptions DownsideAssumptions Downside

• Marketing War

— 50% recovery of premise wiring

— Residential Churn: 25%

— Business Churn: 20%

• All-out: Marketing War + Price War

— Additional 20% price discount for 3years (on top of 20% discount alreadyassumed) passed through to UTOPIA

• 100% recovery of premise wiring

• Residential Churn: 16%

• Business Churn: 9%

• No price war

• Expected operating cost level

• Expected product mix

• Expected CapEx costs

• 20% higher operating costs

• 10% Higher CapEx costs

• Cap on growth in revenue persubscriber for data (Data mixfrozen in Year 5)

• Expected operating cost level

• Expected product mix

• Expected CapEx costs

23DEAN & COMPANY

0%

10%

20%

30%

40%

50%

60%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

033,05-13-04,UTPDYN01A.ppt jrb, JTS1

Take Rate Scenarios

The business case has been tested at three different take rate scenarios

Expected Case

Conservative Case

Downside ramp(e.g. retail providersdrop the ball)

Take Rate(% of homespassed thattake 1 or

moreservices)

Most likely outcomein this range

24DEAN & COMPANY031,05-13-04,UTPDYN01A.ppt JRB, kaL4

Scenario Overview– Key Financials –

The UTOPIA business model looks robust in all but the most negative cases

1 After Dynamic Cities Deferral2 Includes Price War

Note: Minimum cash balances $500K

• Expected— Minimum Debt Coverage1

— Construction Loan— Bond— Largest Annual Cash Deficit— Largest Cumulative Cash Deficit

Take Rate

1.75 (2008)$80.65MM

$85MM——

1.65 (2008)$86.0MM$88MM

——

1.69 (2008)$83.5MM$86MM

——

1.48 (2008)$85.1MM$88MM

——

1.39 (2008)$91.2MM$91MM

$4.3MM (2007)$4.7MM (2008)

• Conservative Case— Minimum Debt Coverage1

— Construction Loan— Bond— Largest Annual Cash Deficit— Largest Cumulative Cash Deficit

1.44 (2008)$77.25MM

$85MM——

1.29 (2008)$82.4MM$91MM

$3.0MM (2008)$0.2MM (2008)

1.31 (2008)$81.0MM$90MM

——

1.17 (2008)$82.35MM

$91MM$3.8MM (2008)$2.9MM (2009)

1.11 (2008)$87.95MM

$91MM$4.9MM (2007)

$11.3MM (2010)

• Downside— Minimum Debt Coverage1

— Construction Loan— Bond— Largest Annual Cash Deficit— Largest Cumulative Cash Deficit

1.39 (2008)$79.00MM$87.0MM

——

1.30 (2008)$83.6MM$91.0MM

$3.0MM (2008)$1.5MM (2009)

1.30 (2008)$82.6MM$91.0MM

$3.0MM (2008)$0.1MM (2009)

1.18 (2008)$84.3MM$91.0MM

$3.7MM (2008)$4.8MM (2009)

1.12 (2008)$89.0MM$91.0MM

$5.9MM (2007)$12.4MM (2010)

Escalated Competitive Response

Plan All-OutMarketing War

AssumptionsDownside

CombinedDownside andCompetitiveResponse2

25DEAN & COMPANY

Incumbents frequently respond to overbuilders by cutting price and escalatingmarketing efforts

028,05-13-04,UTPDYN01A.ppt sbg, cgL2

Municipality/Overbuilder Competitor(s) Lowered Rates

Political Lobbying

Upgraded Network

NoAction

Altrio AdelphiaCharterSBCVerizon

50% discounts(limited time)

--

$200 incentivesLoyalty bonus of every third month free

x

Ashland, OR Charter Communications 25% lower --

Went door-to-door right before AFN came throughInstant installs

Astound AT&T BroadbandPacific BellQwestCharter Communications

- Special customer service centers to dissuade customers from cancelling service

Bristol, VA Charter Communications xCedar Falls, IA Charter Communications

TCI CommunicationsLowered rates

(14% lower than national average)

- Expanded services

Coldwater, MI Lowered rates to $5/month

---

Eliminated monthly fees for additional outletsEliminated franchise fee pass throughAdded additional channels

x

Everest Communications

Time Warner

SBC

20% lower -----

$200 incentive to return (more if write a testimonial)50% discount for signing up for 1 yearInvested in marketing effortsIncumbent monopolizes terrestrially delivered programming & won't sell local regional sports network

x

Glasgow, KY Comcast Cable x Purchased by Glasgow Plant Board

Grande Communications

AT&TTime Warner

Lowered rates by$16-$28/month

Harlan, IA TCI Communications 17% lower($20 lower than

surrounding areas)

--

Expanded basic packageExpanded offerings (compressed digital service)

x

Knology Comcast BellSouthCharter Communications

Predatory Pricing - Selling blocks of long distance x x

LaGrange, GA Charter CommunicationsBell South

Joint Venture

Newnan, GA Charter Communications - $300 to switch x xRCN CableVision

Verizon10-15% lower - Threatened contractors working with RCN, leading contractors to charge

higher pricesScottsboro, AL Charter Communications 50%-66% lower

(limited time predatory pricing)

--

Offered $200 to SEPB customers who switch CATV"Amnesty Program": forgave SEPB customers' old debts to Falcon or Charter

SureWest Pacific BellAT&T Broadband

- SBC is bundling 4 services (DBS, LD/Local, DSL/Dial-up, wireless)

Tacoma, WA AT&T Broadband 20% lower - Funded reports about Click's lack of success xWOW Comcast 50% discount

(limited time)--

Free PPVFree digital upgrade

Marketing

Municipality/Overbuilder Competitor(s) Lowered Rates

Political Lobbying

Upgraded Network

NoAction

Altrio AdelphiaCharterSBCVerizon

50% discounts(limited time)

--

$200 incentivesLoyalty bonus of every third month free

x

Ashland, OR Charter Communications 25% lower --

Went door-to-door right before AFN came throughInstant installs

Astound AT&T BroadbandPacific BellQwestCharter Communications

- Special customer service centers to dissuade customers from cancelling service

Bristol, VA Charter Communications xCedar Falls, IA Charter Communications

TCI CommunicationsLowered rates

(14% lower than national average)

- Expanded services

Coldwater, MI Lowered rates to $5/month

---

Eliminated monthly fees for additional outletsEliminated franchise fee pass throughAdded additional channels

x

Everest Communications

Time Warner

SBC

20% lower -----

$200 incentive to return (more if write a testimonial)50% discount for signing up for 1 yearInvested in marketing effortsIncumbent monopolizes terrestrially delivered programming & won't sell local regional sports network

x

Glasgow, KY Comcast Cable x Purchased by Glasgow Plant Board

Grande Communications

AT&TTime Warner

Lowered rates by$16-$28/month

Harlan, IA TCI Communications 17% lower($20 lower than

surrounding areas)

--

Expanded basic packageExpanded offerings (compressed digital service)

x

Knology Comcast BellSouthCharter Communications

Predatory Pricing - Selling blocks of long distance x x

LaGrange, GA Charter CommunicationsBell South

Joint Venture

Newnan, GA Charter Communications - $300 to switch x xRCN CableVision

Verizon10-15% lower - Threatened contractors working with RCN, leading contractors to charge

higher pricesScottsboro, AL Charter Communications 50%-66% lower

(limited time predatory pricing)

--

Offered $200 to SEPB customers who switch CATV"Amnesty Program": forgave SEPB customers' old debts to Falcon or Charter

SureWest Pacific BellAT&T Broadband

- SBC is bundling 4 services (DBS, LD/Local, DSL/Dial-up, wireless)

Tacoma, WA AT&T Broadband 20% lower - Funded reports about Click's lack of success xWOW Comcast 50% discount

(limited time)--

Free PPVFree digital upgrade

Marketing

Competitive Response

26DEAN & COMPANY

5%–8%

2%–3% 2.6% 2.5% 2.4% 2.4%

1.7%1.5%

1.2%1.4%

0%

1%

2%

3%

4%

5%

6%

7%

8%

005a,05-13-04,UTPDYN01A.ppt ini, jrb6

Churn Benchmarks– Residential –

Highly competitive markets can see churn levels over 2% per month

Monthly Average Churn Monthly Churn Over Time

ChurnRate

ChurnRate

DigitalCable1

DirecTV

Cable

EchoStar

CLECs

Earthlink/AOL

Wireless

AT&TLD

Cable

DirecTV

EchoStar

UTOPIA(Residential)

1.00%

0.80%

0.60%

1.00%

1.25%

1.70%

1.20%

1.10%

1.50%1.25%

2.00%

2.40%

2.10%

2.00%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

1995 1996 1997 1998 1999 2000 2001

UTOPIA Expected (Business)

TypicalRBO (pre-

competition)

UTOPIA Expected Case(Residential)

27DEAN & COMPANY

($5)

$0

$5

$10

$15

$20

2004 2005 2006 2007 2008 2009 2010 2011

042,05-13-04,UTPDYN01A.ppt JTS,npl1

Scenario Comparison: Business Plan– Expected vs. Conservative vs. Downside –

– First 8 Years –

Year

$MM

Expected

Conservative

RevenueAvailable forDebt Service

Downside

ExpectedConservative

Total Debt

Debt Coverage

($5)

$0

$5

$10

$15

$20

$25

2004 2005 2006 2007 2008 2009 2010 2011

Year

$MM

End-of-Year Cash Position

Downside

Expected

Conservative

Downside

Requires Additional(e.g., City) Capital

28DEAN & COMPANY

($5)

$0

$5

$10

$15

$20

2004 2005 2006 2007 2008 2009 2010 2011

044a,05-13-04,UTPDYN01A.ppt JTS,npl1

Scenario Comparison: Marketing War– Expected vs. Conservative vs. Downside –

– First 8 Years –

Year

$MM

Expected

Conservative

RevenueAvailable forDebt Service

Downside

Expected

ConservativeTotal Debt

Debt Coverage

($5)

$0

$5

$10

$15

$20

2004 2005 2006 2007 2008 2009 2010 2011

Year

$MM

End-of-Year Cash Position

Downside

Expected

Conservative

Downside

Requires Additional(e.g., City) Capital

29DEAN & COMPANY

($5)

$0

$5

$10

$15

2004 2005 2006 2007 2008 2009 2010 2011

043a,05-13-04,UTPDYN01A.ppt JTS,npl1

Scenario Comparison: Combined Downside– Expected vs. Conservative vs. Downside –

– First 8 Years –

Year

$MM

Expected

ConservativeRevenueAvailable forDebt Service

Downside

ExpectedConservative

Total Debt

Debt Coverage

($15)

($10)

($5)

$0

$5

$10

2004 2005 2006 2007 2008 2009 2010 2011

Year

$MM

End-of-Year Cash Position

Downside

Expected

Conservative

Downside

Requires Additional(e.g., City) Capital

30DEAN & COMPANY029,05-13-04,UTPDYN01A.ppt sbg,

Jumpstarting Value– Broadband Economic Development –

Real value creation relies on proactive management of complementors andeconomic development

• Shift of localcommerce and taxesout of region via e-commerce

• Net employment lossin Incumbent serviceproviders

• Broadband-enabledcenters of excellence

– Telemedicine– Software

development

Broadband HighwayOut-of-Town

Broadband Service Zone(Individual Subscriber

Optimized)

Broadband Village(Regionally Optimized)

Broadband Corridor(Export-Led)

• Tele-work• In-region e-

commerce• e-government• e-education• e-health• e-utilities

•••

• Net ValueCreation

– Employment– Wages– Home Value– Quality of Life

+

-

•••

0

Network/Community Effects

• New Services– High Speed

internet– Digital cable

• Price/qualitycompetition

• Choice of providers

Pro-activeCommunity

Strategy Required