use benefits that work to achieve your … benefits guide for new employees. ... can help you cover...

TRANSCRIPT

What’s Inside

Your Enrollment Checklist ................ INSIDE

FRONT COVER

Benefits That Work ............................... PAGES 2 – 11

Additional Voluntary Benefits ........ PAGE 12

Who You Can Cover ............................. PAGE 13

Important Notices ................................. BACK COVER

USE BENEFITS THAT WORK TO ACHIEVE YOUR WELLNESS GOALS IN 2018

2018 BENEFITS GUIDE FOR NEW EMPLOYEES

Make choices that enhance your total well-being Your definition of personal wellness is unique. As you prepare to make benefit decisions, think about your wellness goals—physical, emotional and financial—then select the ones that can help you and your family have a healthy 2018.

Your Enrollment Checklist

Make your 2018 benefit elections in the first 30 days of your employment.

PREPARE

Go to MRObenefits.com to:

Review additional information

Use the Health Plan Modeler to compare your potential costs under the Health Plan options

Learn how contributing to a Health Savings Account (HSA) can help you cover out-of-pocket costs—and save for the future

ENROLL

Elect your benefits and complete the Affirmation of Dependents form (if applicable) within 30 days of your date of hire, or you will default to “waived coverage”

Review your confirmation and print a copy for your records prior to exiting

Under Quick Links, click My First Days

CONFIRM

Check your pay stub to make sure your benefit elections are reflected correctly. You will see your benefit contributions as deductions in your paycheck within one to two pay periods after you enroll. Note that your coverage is effective as of your date of hire.

Email Ask HR at [email protected] immediately if you see any problems*

* Marathon Oil cannot make corrections if you did not enroll during your first 30 days of employment.

To stay informed about our benefit plans and make the most of your Marathon Oil benefits, visit MRObenefits.com.

Your next opportunity to enroll won’t be until 2019 Benefits Open Enrollment, unless you experience a qualifying life event, such as marriage, divorce, or the birth or adoption of a child. You have 31 days to notify Marathon Oil of the event, change your benefit elections and have your premiums adjusted accordingly.

Need assistance? Ask HR!

Call 1-855-652-3067 | Email [email protected]

1

HEALTH PLAN OVERVIEW

Marathon Oil offers two Health Investment Plan (HIP) options—HIP Value and HIP Plus. Both plan options are a Preferred Provider Organization, or PPO, type of plan, and cover in-network preventive services at 100% (no deductible). In addition, both combine medical and prescription drugs toward the deductible and out-of-pocket maximum.

Following are key features of each HIP option.

2018 HEALTH PLAN MONTHLY EMPLOYEE CONTRIBUTIONS

The monthly contribution amounts listed below are for regular full-time employees.

Health Plan

2

Feature HIP Value HIP Plus

Contributions Higher Lower

Deductible(combined for medical and prescription drug)

Lower Higher

Health Savings Account (HSA) Yes

Prescription Drugs You pay coinsurance, based on the type of drug.

For non-preventive drugs, you must first meet the Health Plan deductible before cost sharing applies.

Coverage Level HIP Value HIP Plus

Employee Only $124 $94

Employee + Spouse / Domestic Partner $274 $209

Employee + Children $249 $190

Employee + Spouse / Domestic Partner + Children $373 $284

Find the right fit

Go to MRObenefits.com and use the Health Plan Modeler to estimate your potential costs based on your covered family members and expected health care needs.

3

HIP Value HIP Plus

In-Network1 Out-of-Network In-Network1 Out-of-Network

Health Savings Account (HSA) Company Contributions for 2018

Employee Only coverage: $500 Employee Only coverage: $750

Employee + coverage2: $1,000 Employee + coverage2: $1,500

Individual Deductible (Employee Only coverage; combined with prescription drug)

$1,350 $4,050 $2,000 $4,000

Family2 Deductible (Employee + coverage; combined with prescription drug)

$2,700 $8,100 $4,000 $8,000

Coinsurance Plan pays 85% Plan pays 50% Plan pays 80% Plan pays 50%

Individual Out-of-Pocket Maximum(combined with prescription drug)

$2,700 $8,100 $4,000 $8,000

Family2 Out-of-Pocket Maximum(combined with prescription drug)

$5,400 $16,200 $6,850 $16,000

Preventive Services Plan pays 100% (no deductible)

You pay 50% after deductible is met, plus any

amount over Reasonable & Customary3

Plan pays 100% (no deductible)

You pay 50% after deductible is met, plus any

amount over Reasonable & Customary3

Emergency Room Services (if NOT admitted to hospital)

Plan pays 85% after deductible is met Plan pays 80% after deductible is met

HEALTH PLAN COVERAGE

1 In-network provisions apply if you live in an area with no access to in-network providers.2 Applies to Employee + Spouse/Domestic Partner, Employee + Children, and Employee + Spouse/Domestic Partner +

Children coverage.3 A “Reasonable & Customary” charge is the amount customarily charged for a given service by other physicians in the

area (often defined as a specific percentile of all charges in the community), and the reasonable cost of services for a given patient after review of the case.

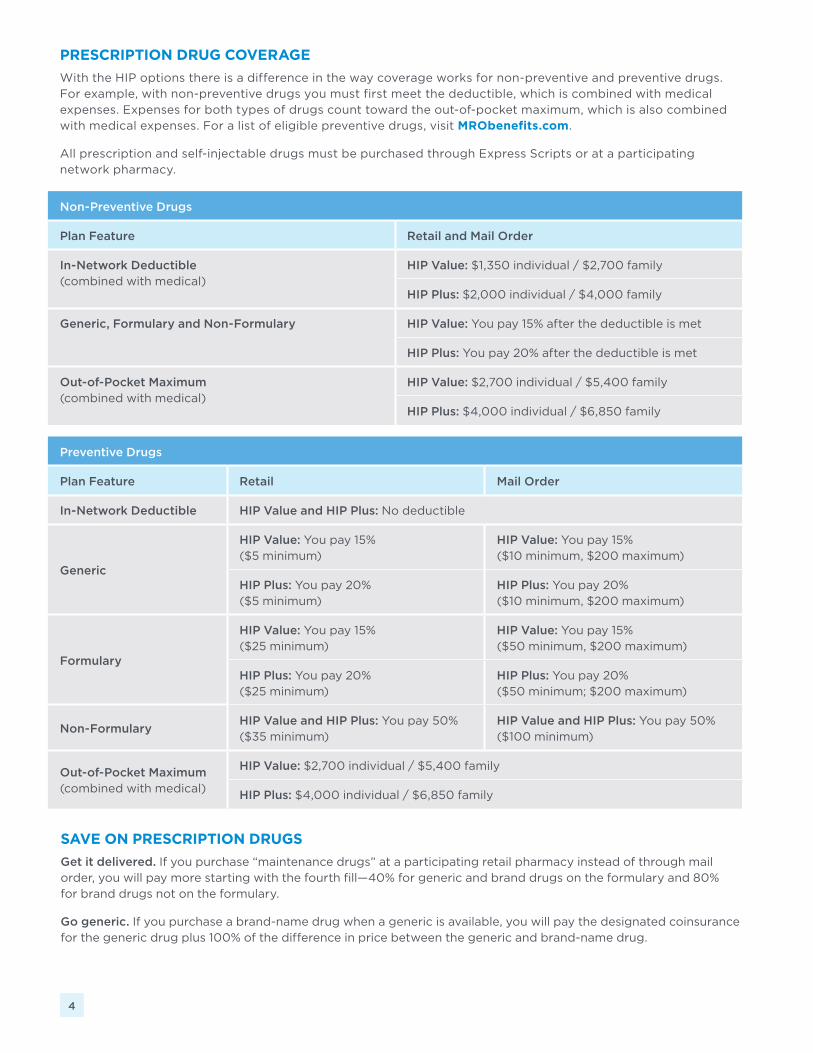

PRESCRIPTION DRUG COVERAGE

With the HIP options there is a difference in the way coverage works for non-preventive and preventive drugs. For example, with non-preventive drugs you must first meet the deductible, which is combined with medical expenses. Expenses for both types of drugs count toward the out-of-pocket maximum, which is also combined with medical expenses. For a list of eligible preventive drugs, visit MRObenefits.com.

All prescription and self-injectable drugs must be purchased through Express Scripts or at a participating network pharmacy.

SAVE ON PRESCRIPTION DRUGS

Get it delivered. If you purchase “maintenance drugs” at a participating retail pharmacy instead of through mail order, you will pay more starting with the fourth fill—40% for generic and brand drugs on the formulary and 80% for brand drugs not on the formulary.

Go generic. If you purchase a brand-name drug when a generic is available, you will pay the designated coinsurance for the generic drug plus 100% of the difference in price between the generic and brand-name drug.

4

Non-Preventive Drugs

Plan Feature Retail and Mail Order

In-Network Deductible (combined with medical)

HIP Value: $1,350 individual / $2,700 family

HIP Plus: $2,000 individual / $4,000 family

Generic, Formulary and Non-Formulary HIP Value: You pay 15% after the deductible is met

HIP Plus: You pay 20% after the deductible is met

Out-of-Pocket Maximum (combined with medical)

HIP Value: $2,700 individual / $5,400 family

HIP Plus: $4,000 individual / $6,850 family

Preventive Drugs

Plan Feature Retail Mail Order

In-Network Deductible HIP Value and HIP Plus: No deductible

Generic

HIP Value: You pay 15% ($5 minimum)

HIP Value: You pay 15% ($10 minimum, $200 maximum)

HIP Plus: You pay 20% ($5 minimum)

HIP Plus: You pay 20% ($10 minimum, $200 maximum)

Formulary

HIP Value: You pay 15% ($25 minimum)

HIP Value: You pay 15% ($50 minimum, $200 maximum)

HIP Plus: You pay 20% ($25 minimum)

HIP Plus: You pay 20% ($50 minimum; $200 maximum)

Non-FormularyHIP Value and HIP Plus: You pay 50% ($35 minimum)

HIP Value and HIP Plus: You pay 50% ($100 minimum)

Out-of-Pocket Maximum (combined with medical)

HIP Value: $2,700 individual / $5,400 family

HIP Plus: $4,000 individual / $6,850 family

5

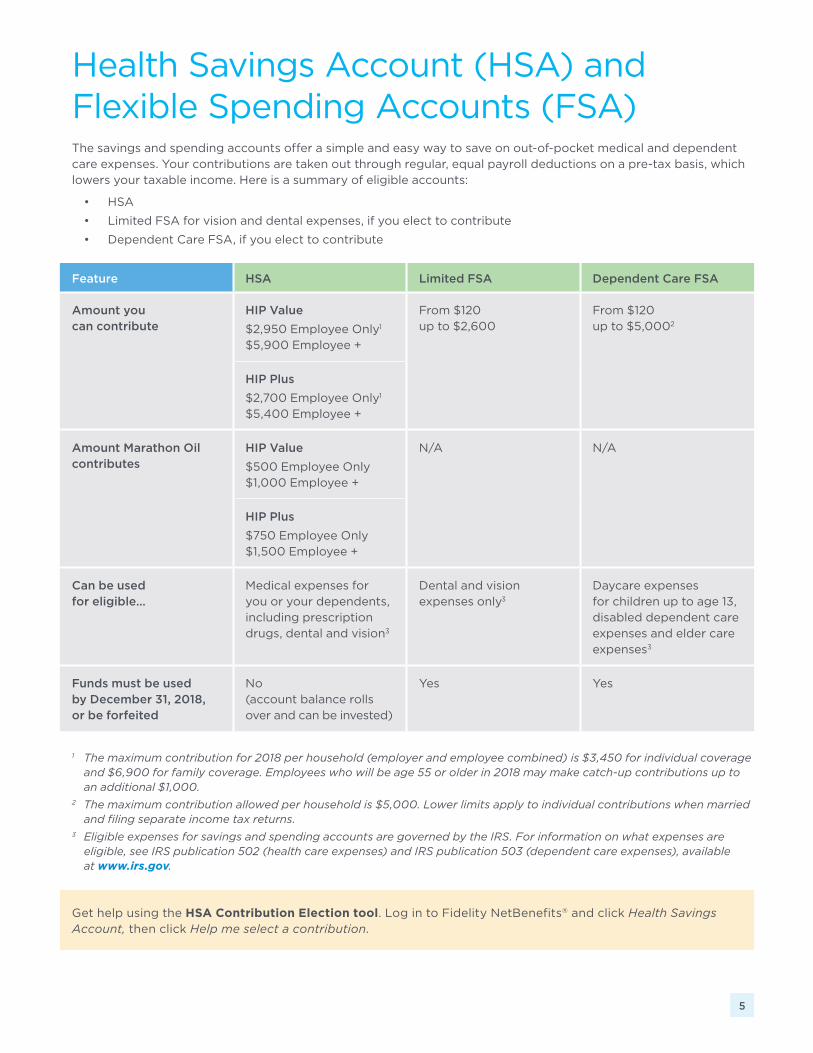

Health Savings Account (HSA) and Flexible Spending Accounts (FSA)The savings and spending accounts offer a simple and easy way to save on out-of-pocket medical and dependent care expenses. Your contributions are taken out through regular, equal payroll deductions on a pre-tax basis, which lowers your taxable income. Here is a summary of eligible accounts:

• HSA

• Limited FSA for vision and dental expenses, if you elect to contribute

• Dependent Care FSA, if you elect to contribute

Feature HSA Limited FSA Dependent Care FSA

Amount you can contribute

HIP Value

$2,950 Employee Only1

$5,900 Employee +

From $120 up to $2,600

From $120 up to $5,0002

HIP Plus

$2,700 Employee Only1

$5,400 Employee +

Amount Marathon Oil contributes

HIP Value

$500 Employee Only$1,000 Employee +

N/A N/A

HIP Plus

$750 Employee Only$1,500 Employee +

Can be used for eligible…

Medical expenses for you or your dependents, including prescription drugs, dental and vision3

Dental and vision expenses only3

Daycare expenses for children up to age 13, disabled dependent care expenses and elder care expenses3

Funds must be used by December 31, 2018, or be forfeited

No (account balance rolls over and can be invested)

Yes Yes

Get help using the HSA Contribution Election tool. Log in to Fidelity NetBenefits® and click Health Savings Account, then click Help me select a contribution.

1 The maximum contribution for 2018 per household (employer and employee combined) is $3,450 for individual coverage and $6,900 for family coverage. Employees who will be age 55 or older in 2018 may make catch-up contributions up to an additional $1,000.

2 The maximum contribution allowed per household is $5,000. Lower limits apply to individual contributions when married and filing separate income tax returns.

3 Eligible expenses for savings and spending accounts are governed by the IRS. For information on what expenses are eligible, see IRS publication 502 (health care expenses) and IRS publication 503 (dependent care expenses), available at www.irs.gov.

DENTAL PLAN OVERVIEW

6

With 127,000 dentists in the Cigna network, you have plenty of choices. For a list of Cigna network dentists in your area, call 1-800-244-6224 or go to www.mycigna.com.

Dental PlanWith the Cigna DPPO, you can receive care from any licensed dentist. However, if you receive care from a dentist in the Cigna DPPO network, your out-of-pocket cost may be reduced. If you use a Cigna Advantage dentist, your costs may be even less.

2018 DENTAL PLAN MONTHLY EMPLOYEE CONTRIBUTIONS

The monthly contribution amounts listed below are for regular full-time employees.

Employee Only Employee + Spouse / Domestic Partner

Employee + Children Employee + Spouse / Domestic Partner + Children

$8 $16 $17 $27

Cigna DPPO

Selecting a dentist You can see any licensed dentist; however, if you receive care from a Cigna DPPO dentist, you pay a discounted rate for services. Look for the Cigna Advantage designation when you search providers to receive the best rates.

If you do not use a Cigna DPPO dentist, you will need to file a claim for reimbursement of charges beyond the deductible.

Benefits • No deductible for preventive and diagnostic services

• $50 deductible per individual on other services

• Family deductible will not exceed $150

• $2,000 calendar year maximum per individual (not including orthodontic expenses)

• $1,750 lifetime orthodontia maximum per individual—you pay the balance

See the DPPO schedule in the Dental Plan SPD for details on plan benefits

Claims You or your provider file a claim form for reimbursement.

VISION ASSISTANCE PLAN OVERVIEW

7

Vision Assistance PlanUnitedHealthcare administers the Vision Assistance Plan. You can receive care from any licensed eye care professional; but if you see a UnitedHealthcare in-network provider, you receive a higher level of benefits and there are no claim forms to file.

If you see an out-of-network provider, you receive a lesser discount on services and must file a claim for reimbursement.

2018 VISION ASSISTANCE PLAN MONTHLY EMPLOYEE CONTRIBUTIONS

The monthly contributions listed below are for regular full- and part-time employees.

Employee Only Employee + Spouse / Domestic Partner

Employee + Children Employee + Spouse / Domestic Partner + Children

$4.97 $8.29 $9.11 $13.26

Plan Features Cost of Service

Type of Service Frequency of Service In-Network Out-of-Network

Exams Once every calendar year

$10 copay Up to a maximum allowance of $35

Frames Once every other calendar year

No copay, when purchased with lenses (up to $120 retail)

Up to a maximum allowance of $45

Single Vision Lenses

Once every calendar year

$10 copay

Up to a maximum allowance of $25

Bifocal Lenses Up to a maximum allowance of $40

Trifocal Lenses Up to a maximum allowance of $55

Contact Lenses (in lieu of prescription glasses)

• Up to a maximum allowance of $105

• This benefit applies to one order of contact lenses per calendar year

8

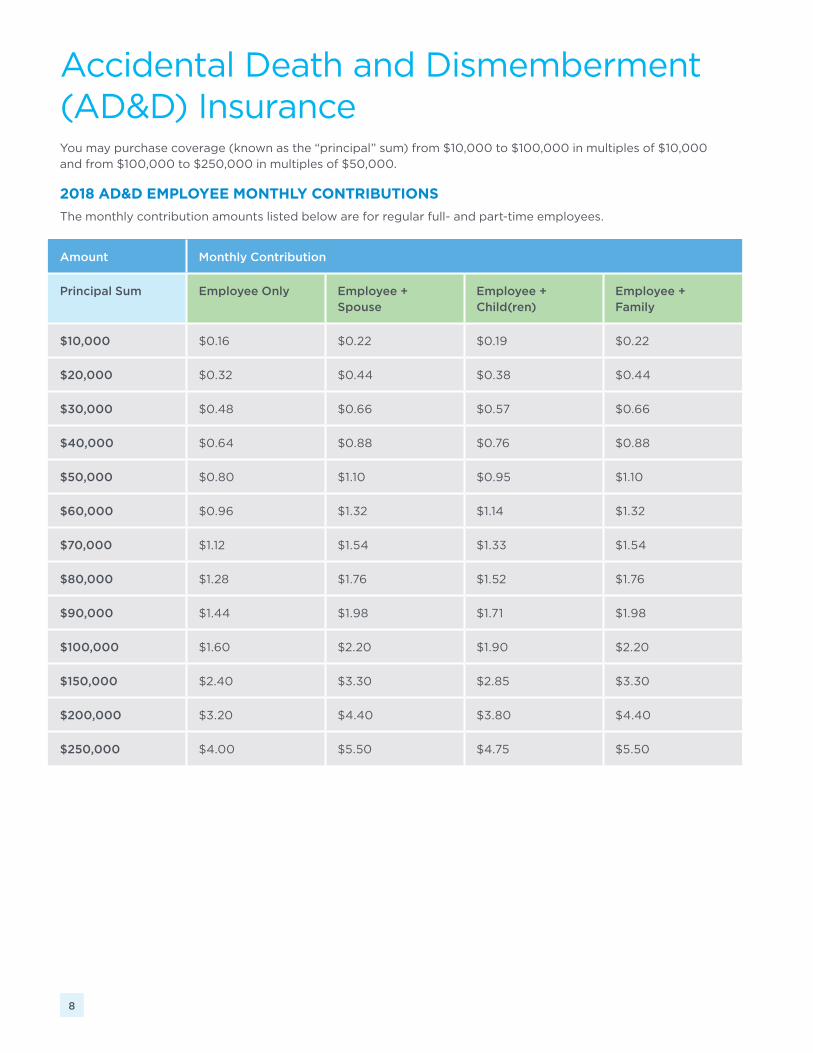

Accidental Death and Dismemberment (AD&D) InsuranceYou may purchase coverage (known as the “principal” sum) from $10,000 to $100,000 in multiples of $10,000 and from $100,000 to $250,000 in multiples of $50,000.

2018 AD&D EMPLOYEE MONTHLY CONTRIBUTIONS

The monthly contribution amounts listed below are for regular full- and part-time employees.

Amount Monthly Contribution

Principal Sum Employee Only Employee + Spouse

Employee + Child(ren)

Employee + Family

$10,000 $0.16 $0.22 $0.19 $0.22

$20,000 $0.32 $0.44 $0.38 $0.44

$30,000 $0.48 $0.66 $0.57 $0.66

$40,000 $0.64 $0.88 $0.76 $0.88

$50,000 $0.80 $1.10 $0.95 $1.10

$60,000 $0.96 $1.32 $1.14 $1.32

$70,000 $1.12 $1.54 $1.33 $1.54

$80,000 $1.28 $1.76 $1.52 $1.76

$90,000 $1.44 $1.98 $1.71 $1.98

$100,000 $1.60 $2.20 $1.90 $2.20

$150,000 $2.40 $3.30 $2.85 $3.30

$200,000 $3.20 $4.40 $3.80 $4.40

$250,000 $4.00 $5.50 $4.75 $5.50

9

Life InsuranceBasic Non-Contributory Life Insurance

Marathon Oil provides you with Life Insurance coverage of two times your base annual pay, at no cost to you. The plan pays benefits to your named beneficiaries if you die. Minnesota Life Insurance Company, an affiliate of Securian Financial Group, Inc., will contact you via email about electing your beneficiary(ies).

For added protection, you may purchase the following optional coverage described below.

Optional Contributory Life Insurance—Employee (Age-Based)

During the New Employee Benefits Enrollment period you can enroll for coverage of up to six times your annual pay. Coverage elected in excess of $750,000 requires proof of good health (evidence of insurability).

Age Category Cost per $1,000 of Coverage per Month*

< 25 $0.012

25–29 $0.014

30–34 $0.019

35–39 $0.021

40–44 $0.023

45–49 $0.036

50–54 $0.054

55–59 $0.102

60–64 $0.156

65–69 $0.300

70 + $0.516

SMART TIP!

How much life insurance do you need? Get an estimate using the online Life Insurance Calculator at www.lifebenefits.com.

Minnesota Life Insurance Company, an affiliate of Securian Financial Group, Inc.

Website: www.lifebenefits.com

Phone: 1-866-293-6047

Hours of Operation: 7:00 a.m.—6:00 p.m. CST, Monday through Friday

2018 OPTIONAL CONTRIBUTORY LIFE INSURANCE EMPLOYEE MONTHLY CONTRIBUTIONS

The monthly contribution amounts listed below are for regular full- and part-time employees.

* Based on your age as of January 1

Dependent Life InsuranceYou may also purchase Dependent Life Insurance coverage for your spouse and/or eligible child(ren)—no evidence of insurability (e.g., a physical exam) is required. You pay premiums via after-tax payroll deductions.

To elect dependent coverage, you must be participating in Optional Contributory Life Insurance (either Age-Based or Level Premium) and your dependent must meet the definition of an “eligible dependent” (see “Who You Can Cover” on page 13).

Any dependent coverage elected during the New Employee Benefits Enrollment period becomes effective the latest of:

• The date your benefits become effective as a result of employment, or

• The date you are actively at work, as defined in the Life Insurance Plan, or

• The date your eligible dependent(s) are “free from confinement”* as established by Minnesota Life.

* Dependents are covered, provided the individual has not been ordered or advised by a medical doctor to remain at his/her home, hospital or other place of residence, unless a departure for a limited period of time is necessary to improve his/her physical or mental status.

DEPENDENT LIFE INSURANCE OPTIONS

Spouse Life Insurance

For an eligible spouse you can:

• Elect coverage from $10,000 to $50,000 in $10,000 increments. Coverage can be increased during Benefits Open Enrollment by an additional $10,000 up to a maximum of $100,000, or

• Waive Spouse Life Insurance coverage.

Child Life Insurance

For eligible children you can:

• Elect coverage of $10,000, $20,000 or $30,000. Premiums are a fixed amount and do not vary with the number of children covered (benefits are payable based on the level of coverage for each child), or

• Waive Child Life Insurance coverage.

Please note: The combined total of Spouse Life and Child Life Insurance coverage cannot exceed the sum of your Basic Life Insurance plus your Optional Age-Based or Level Premium Life Insurance.

Beneficiaries

You are the designated beneficiary of any payable Dependent Life Insurance benefits. If you die before benefits become payable, benefits will be paid by survivor class, in the following order, to your:

• Spouse

• Child(ren)

• Parents

• Brothers and sisters

• Executors or administrators

10

Long-Term Disability (LTD) PlanMarathon Oil provides you with LTD coverage at no cost to you. LTD coverage helps provide income protection if you’re unable to work due to a disabling condition. The benefit will pay you 60% of your monthly earnings, to a maximum of $12,000 per month, after you have exhausted a six-month waiting period.

Spouse Child(ren)

Age of Spouse Cost per $1,000 of Coverage per Month*

Coverage Cost per Month

< 25 $0.012 $10,000 $0.76

25–29 $0.014 $20,000 $1.52

30–34 $0.019 $30,000 $2.28

35–39 $0.021

40–44 $0.023

45–49 $0.036

50–54 $0.054

55–59 $0.102

60–64 $0.156

65–69 $0.300

70 + $0.516

11

2018 DEPENDENT LIFE INSURANCE EMPLOYEE MONTHLY CONTRIBUTIONS

The monthly contribution amounts listed below are for regular full- and part-time employees.

* Based on spouse’s age as of January 1

Additional Voluntary BenefitsBack-up Child and Adult / Elder Care

Through Bright Horizons, you have access to up to 15 days of back-up child care and adult/elder care services at child care centers in your area or from screened in-home caregivers. Enrollment is free and you can enroll at any time. You pay only when you use the service (or if you have a late cancellation). Cost for center-based care is $15/child or $25/family; in-home care is $6/hour with a four-hour minimum.

A contact center is available 24 hours a day, seven days a week, 365 days a year, to coordinate all care arrangements—even the night before a service is needed. Bright Horizons also gives you access to Sitter City, an online caregiver locating service.

Learn more online at http://www.careadvantage.com/marathonoil and enter username TotalRewards and password Cares4you. You can also call the toll-free number at 1-877-BH-CARES (1-877-242-2737).

12

Go to MRObenefits.com to learn more about other benefits, including adoption assistance, flexible work arrangements and the Educational Reimbursement Plan.

ELIGIBLE DEPENDENTS

For the Health, Dental and Vision Assistance Plans

• Your spouse, to whom you are lawfully married under the law of any domestic or foreign jurisdiction that has the legal authority to sanction marriages.

• Your domestic partner (as determined by the criteria established in the “Marathon Oil Affidavit of Domestic Partner Relationship”).

• Your children (and/or children of your domestic partner), which include your:

– Natural children of the first degree,

– Legally adopted children,

– Stepchildren, and

– Children whose parents are both deceased for whom you have legal custody as determined by a court of competent jurisdiction.

For the Life Insurance and AD&D Plans

• Your spouse, to whom you are lawfully married under the law of any domestic or foreign jurisdiction that has the legal authority to sanction marriages.

• Your children, which include your:

– Natural children of the first degree,

– Legally adopted children,

– Stepchildren, and

– Children whose parents are both deceased for whom you have legal custody as determined by a court of competent jurisdiction.

Additional Dependent Eligibility Requirements for Marathon Oil’s Health and Welfare Plans

• Adult child up to age 26, regardless of marital or student status or access to other coverage;

• A dependent disabled child who has reached age 26 but is less than age 65 and is incapable of self-support due to a mental or physical disability.

13

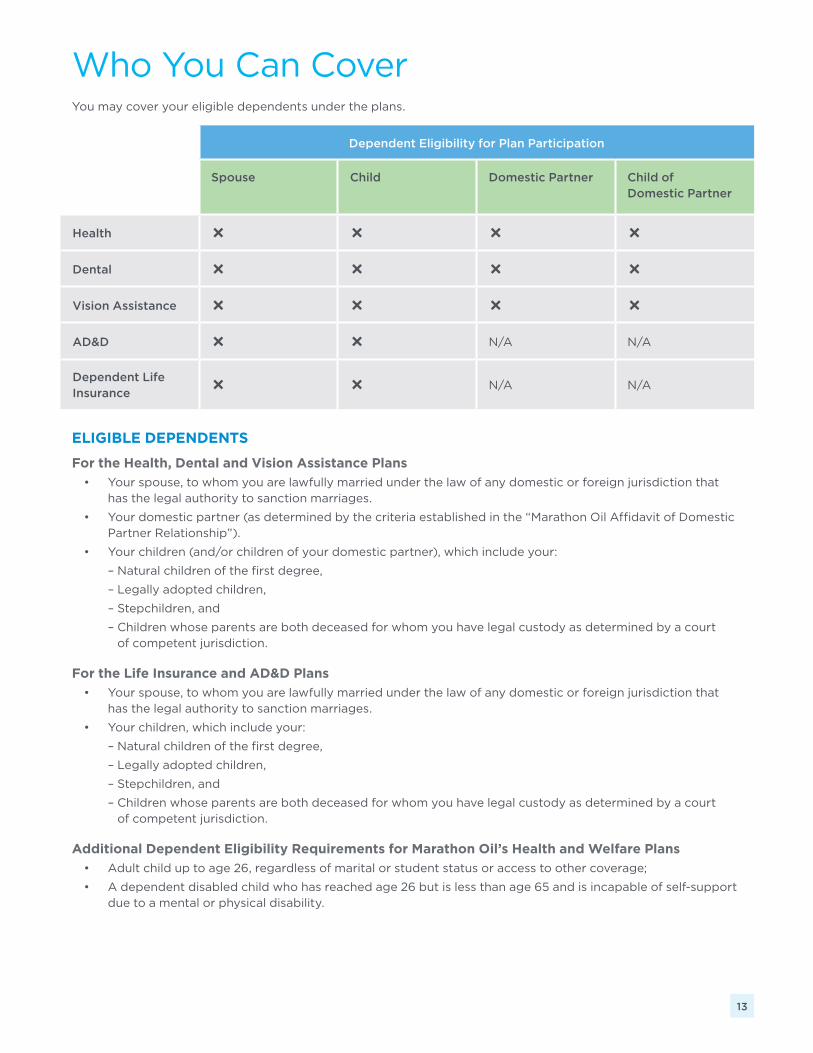

Dependent Eligibility for Plan Participation

Spouse Child Domestic Partner Child of Domestic Partner

Health Ñ Ñ Ñ Ñ

Dental Ñ Ñ Ñ Ñ

Vision Assistance Ñ Ñ Ñ Ñ

AD&D Ñ Ñ N/A N/A

Dependent Life Insurance

Ñ Ñ N/A N/A

Who You Can CoverYou may cover your eligible dependents under the plans.

Important NoticesQualifying Life Events and Special Enrollments

If you have a qualifying life event (e.g., marriage, divorce, birth or adoption), you have 31 days to notify Marathon Oil of the event, change your benefit elections and have your premiums adjusted accordingly. The change in benefit elections must be due to, and consistent with, the qualifying life event. If the event is marriage, birth or adoption, you also may be able to enroll yourself as well as your dependent(s). In addition, if you decline enrollment for yourself and/or your dependents (including your spouse) because of other health insurance coverage or group health plan coverage, you may have a special enrollment opportunity that would allow you to enroll yourself and/or dependents if you or your dependents lose eligibility for that other coverage or if the employer stops contributing toward your or your dependent’s coverage. If you fail to notify Marathon Oil within 31 days of the qualifying life event or loss of coverage, your coverage and premiums will remain the same until the next plan year. To ensure you have the right coverage and are paying the appropriate premiums for your needs, be sure to notify Marathon Oil of any qualifying life event within 31 days. Please note that timing for notifying Marathon Oil is extended to 60 days if your child loses coverage under Medicaid or the Children’s Health Insurance Program (CHIP), or becomes eligible for Medicaid or CHIP coverage.

Women’s Health and Cancer Rights Act of 1998 Notice

The Women’s Health Act requires the publication of the following notice annually:

The plan provides mastectomy coverage and also provides for reconstructive surgery in a manner determined in a consultation with the attending physician and the patient. Coverage includes reconstruction of the breast on which the mastectomy was performed, surgery and reconstruction of the other breast to produce a symmetrical appearance, and prostheses and treatment of physical complications at all stages of the mastectomy, including lymphedemas.

This notice is made solely to satisfy the Act’s requirements. The Health Plan has always covered such procedures and in no way does this reflect a change in plan provisions.

The Company’s policies, plans, practices and procedures may be amended, terminated or changed at any time at the sole discretion of the Company. If that should occur, the material in this document will be superseded and the provisions of the actual official plan documents will control. If there are discrepancies between this document and the official plan documents, the actual plan documents will always govern.

New Hire—12/2017ERNA