usdp-0036962 geisinger health system

TRANSCRIPT

Geisinger Health SystemConsolidated Financial StatementsJune 30, 2014 and 2013

Geisinger Health SystemIndexJune 30, 2014 and 2013

Page(s)

Independent Auditor s Report ..............................................................................................................1 2

Consolidated Financial Statements

Balance Sheets ............................................................................................................................................3

Statements of Operations and Changes in Net Assets ...........................................................................4 5

Statements of Cash Flows ...........................................................................................................................6

Notes to Financial Statements ...............................................................................................................7 32

Independent Auditor s Report

To the Board of Directors of

Geisinger Health System

We have audited the accompanying consolidated financial statements of Geisinger Health System

(the System ), which comprise the consolidated balance sheets as of June 30, 2014 and June 30, 2013,

and the related consolidated statements of operations and changes in net assets, and cash flows for the

years then ended.

Management s Responsibility for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of the consolidated financial

statements in accordance with accounting principles generally accepted in the United States of America;

this includes the design, implementation, and maintenance of internal control relevant to the preparation

and fair presentation of consolidated financial statements that are free from material misstatement,

whether due to fraud or error.

Auditor s Responsibility

Our responsibility is to express an opinion on the consolidated financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of

America. Those standards require that we plan and perform the audit to obtain reasonable assurance

about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in

the consolidated financial statements. The procedures selected depend on our judgment, including the

assessment of the risks of material misstatement of the consolidated financial statements, whether due to

fraud or error. In making those risk assessments, we consider internal control relevant to the System s

preparation and fair presentation of the consolidated financial statements in order to design audit

procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on

the effectiveness of the System s internal control. Accordingly, we express no such opinion. An audit also

includes evaluating the appropriateness of accounting policies used and the reasonableness of significant

accounting estimates made by management, as well as evaluating the overall presentation of the

consolidated financial statements. We believe that the audit evidence we have obtained is sufficient and

appropriate to provide a basis for our audit opinion.

PricewaterhouseCoopers LLP, Two Commerce Square, Suite 1700, 2001 Market Street, Philadelphia, PA 19103-7042T: (267) 330 3000, F: (267) 330 3300, www.pwc.com/us

2

Opinion

In our opinion, the consolidated financial statements referred to above present fairly, in all material

respects, the financial position of the System at June 30, 2014 and June 30, 2013, and the results of its

operations and its cash flows for the years then ended in accordance with accounting principles generally

accepted in the United States of America.

September 18, 2014

Geisinger Health SystemConsolidated Balance SheetsJune 30, 2014 and 2013

The accompanying notes are an integral part of these consolidated financial statements.

3

(dollars in thousands) 2014 2013

Assets

Current assetsCash and cash equivalents 78,512$ 173,930$Investments 658,653 523,107

Assets limited as to use 6,360 3,143Accounts receivable, net of estimated uncollectibles of$76,879 in 2014 and $73,603 in 2013 391,382 310,019

Inventories and other 79,948 76,001

Total current assets 1,214,855 1,086,200

Long-term investments 1,972,766 1,583,836

Assets limited as to use, noncurrent 134,728 149,595Property and equipment, net 1,128,094 950,662Other assets 153,054 115,963

Assets held in trust 31,084 27,006

Total assets 4,634,581$ 3,913,262$

Liabilities and Net AssetsCurrent liabilities

Current installments of long-term debt 5,103$ 7,357$Estimated third-party payor settlements 130,214 110,304Accounts payable 85,112 88,017

Medical claims payable, accrued expenses and other 516,737 492,548

Total current liabilities 737,166 698,226

Long-term debt, net of current installments 1,079,451 909,212Other liabilities and contingencies 297,210 262,134

Total liabilities 2,113,827 1,869,572

Net assetsUnrestricted 2,386,371 1,931,371Unrestricted - noncontrolling interest 9,039 -

Temporarily restricted 45,770 36,936Permanently restricted 79,574 75,383

Total net assets 2,520,754 2,043,690

Total liabilities and net assets 4,634,581$ 3,913,262$

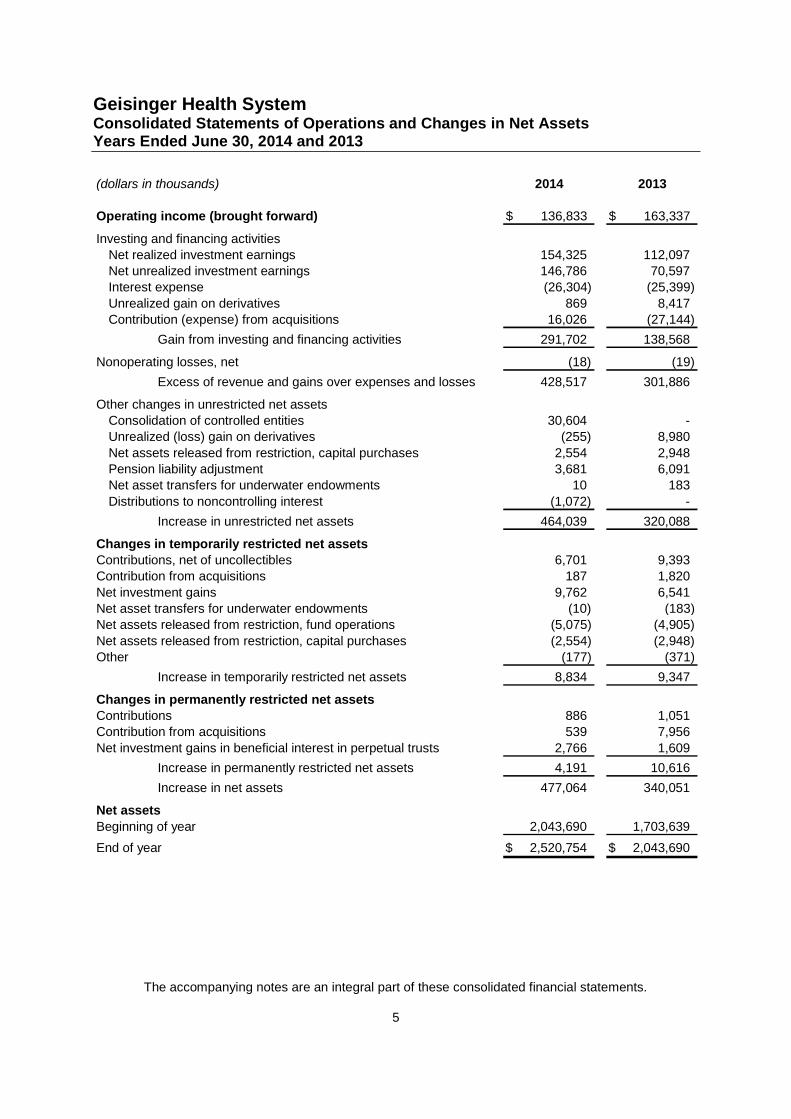

Geisinger Health SystemConsolidated Statements of Operations and Changes in Net AssetsYears Ended June 30, 2014 and 2013

The accompanying notes are an integral part of these consolidated financial statements.

4

(dollars in thousands) 2014 2013

Unrestricted net assets

RevenueNet patient service revenue 1,852,286$ 1,765,831$Provision for bad debts (53,703) (59,108)

Net patient service revenue less provision for bad debts 1,798,583 1,706,723

Premium revenue 2,036,813 1,512,035

Other revenue 142,530 136,308

3,977,926 3,355,066

Expenses

Salaries and benefits 1,598,115 1,420,889Contracted services 1,394,335 1,055,927Supplies and other expenses 726,066 602,728Depreciation and amortization 122,577 112,185

3,841,093 3,191,729

Operating income (carried forward) 136,833$ 163,337$

Geisinger Health SystemConsolidated Statements of Operations and Changes in Net AssetsYears Ended June 30, 2014 and 2013

The accompanying notes are an integral part of these consolidated financial statements.

5

(dollars in thousands) 2014 2013

Operating income (brought forward) 136,833$ 163,337$

Investing and financing activitiesNet realized investment earnings 154,325 112,097Net unrealized investment earnings 146,786 70,597Interest expense (26,304) (25,399)

Unrealized gain on derivatives 869 8,417Contribution (expense) from acquisitions 16,026 (27,144)

Gain from investing and financing activities 291,702 138,568

Nonoperating losses, net (18) (19)

Excess of revenue and gains over expenses and losses 428,517 301,886

Other changes in unrestricted net assetsConsolidation of controlled entities 30,604 -Unrealized (loss) gain on derivatives (255) 8,980

Net assets released from restriction, capital purchases 2,554 2,948Pension liability adjustment 3,681 6,091Net asset transfers for underwater endowments 10 183

Distributions to noncontrolling interest (1,072) -

Increase in unrestricted net assets 464,039 320,088

Changes in temporarily restricted net assetsContributions, net of uncollectibles 6,701 9,393Contribution from acquisitions 187 1,820

Net investment gains 9,762 6,541Net asset transfers for underwater endowments (10) (183)Net assets released from restriction, fund operations (5,075) (4,905)

Net assets released from restriction, capital purchases (2,554) (2,948)Other (177) (371)

Increase in temporarily restricted net assets 8,834 9,347

Changes in permanently restricted net assetsContributions 886 1,051Contribution from acquisitions 539 7,956

Net investment gains in beneficial interest in perpetual trusts 2,766 1,609

Increase in permanently restricted net assets 4,191 10,616

Increase in net assets 477,064 340,051

Net assets

Beginning of year 2,043,690 1,703,639

End of year 2,520,754$ 2,043,690$

Geisinger Health SystemConsolidated Statements of Cash FlowsYears Ended June 30, 2014 and 2013

The accompanying notes are an integral part of these consolidated financial statements.

6

(dollars in thousands) 2014 2013

Cash flows from operating activitiesIncrease in net assets before attribution of noncontrolling interest 477,064$ 340,051$

Change in net assets attributable to noncontrolling interest (9,039) -Change in net assets attibutable to GHS 468,025 340,051

Adjustments to reconcile change in net assets to

net cash provided by operating activitiesDepreciation and amortization 122,577 112,185Provision for bad debts 53,847 59,205

Unrealized gain on derivatives (614) (17,397)Net realized gain on investments (107,487) (71,671)Net unrealized gain on investments (154,318) (74,821)(Contributions) expense from acquisition, net of cash received (5,945) 19,695

Restricted contributions, investment gains and other (19,938) (18,223)Net change in

Noncontrolling interest 10,111 -Accounts receivable (126,316) (157,421)Inventories and other 1,146 (12,226)Estimated third-party payor settlements 11,643 (9,681)

Accounts payable (4,307) (3,054)Accrued expenses and other 18,033 11,612Other assets and liabilities (32,115) (25,370)

Net cash provided by operating activities 234,342 152,884

Cash flows from investing activities

Additions to property and equipment, net (272,236) (182,586)Purchases of investments (1,566,088) (1,418,948)Purchases of assets limited as to use (43,447) (30,599)Sales of investments 1,319,325 1,351,142

Sales of assets limited as to use 70,738 97,948

Net cash used in investing activities (491,708) (183,043)

Cash flows from financing activitiesProceeds from issuance of debt 209,400 24,193Repayment of debt (65,418) (33,578)Proceeds from line of credit draw - 5,600

Repayment of credit draw (900) (4,700)Distributions to noncontrolling interest (1,072) -

Proceeds from restricted contributions, investment gainsand other 19,938 18,223

Net cash provided by financing activities 161,948 9,738

Decrease in cash and cash equivalents (95,418) (20,421)

Cash and cash equivalents

Beginning of year 173,930 194,351

End of year 78,512$ 173,930$

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

7

1. Organization

The consolidated Geisinger Health System1

( GHS ) financial statements include Geisinger HealthSystem Foundation (the Foundation ), located in Danville, Pennsylvania, a tax-exempt entityserving as the corporate parent for the other entities within GHS. The Foundation engages infundraising activities and accepts gifts and bequests on behalf of all GHS entities. Other entities inGHS include: Geisinger Medical Center ( GMC ), with campuses located in Danville and CoalTownship, Pennsylvania; Geisinger Wyoming Valley Medical Center ( GWV ), with campuseslocated in Plains Township and Wilkes-Barre, Pennsylvania; Community Medical Center d/b/aGeisinger Community Medical Center ( GCMC ), located in Scranton, Pennsylvania; Geisinger-

and Geisinger-Bloomsburg; all tax-exempt entities operating acute

health care facilities; Geisinger Clinic (the Clinic ), with clinic locations throughout northeasternand central Pennsylvania, a tax-exempt entity providing physician, urgent care and pharmacyservices and conducting research and education activities; Geisinger Health Plan ( GHP ), locatedin Danville, Pennsylvania, a tax-exempt licensed health maintenance organization ( HMO )providing comprehensive health care to its subscribers through agreements with health careproviders; Geisinger Indemnity Insurance Company ( GIIC ), located in Danville, Pennsylvania, afor-profit, wholly owned subsidiary of Foundation and licensed in Pennsylvania as a CasualtyInsurance Company; Geisinger Quality Options, Inc.( GQO ), located in Danville, Pennsylvania, afor-profit wholly owned subsidiary of the Foundation, a risk-assuming preferred providerorganization( RANLI PPO ); Geisinger System Services ( GSS ), located in Danville, Pennsylvania,a tax-exempt entity providing management and consulting services to affiliated GHS entities;Marworth, located in Waverly, Pennsylvania, a tax-exempt entity operating a residential andoutpatient alcohol and chemical dependency treatment center; Geisinger Medical ManagementCorporation ( GMMC ), located in Danville, Pennsylvania, a for-profit wholly owned subsidiary ofthe Foundation providing contract management, hospitality, clinical engineering, informationtechnology, contact center, and product procurement services; Geisinger Community HealthServices ( GCHS ), located in Danville, Pennsylvania, a tax-exempt entity providing nonacutehealth care services; Geisinger Insurance Corporation, Risk Retention Group ( RRG ), domiciledand licensed in Vermont, a tax-exempt entity registered by the Pennsylvania Insurance Departmentto provide primary professional liability coverage for several entities of GHS; Geisinger AssuranceCompany, Ltd. , a wholly owned subsidiary of the Foundation licensed in the CaymanIslands, British West Indies, providing primary and excess healthcare professional, general liabilityand managed care liability insurance to the Foundation and affiliates; Mountain View NursingHome, Inc. ( MVCC ), located in Scranton, Pennsylvania, a tax-exempt entity operating a long-termcare, skilled nursing, and rehabilitation facility; Community Medical Care, Inc. ( CMCI ), located inScranton, Pennsylvania, a tax-exempt entity providing physician and other healthcare professionalservices; Medical Dimensions, Inc. ( MDI ), located in Scranton, Pennsylvania, a tax-exempt entityoperating as a real estate holding company; Community Medical Center Healthcare System( CMCHS ), located in Scranton, Pennsylvania, a tax-exempt entity that previously served as thecorporate parent of GCMC and affiliated entities; Geisinger SCA Holdings, LLC ,Delaware limited liability company, a joint venture between GCMC and SCA PennsylvaniaHoldings, LLC (a subsidiary of Surgical Care Affiliates, LLC) operating an ambulatory surgerycenter in Dickson City, Pennsylvania; Columbia,Maryland, a for-profit, collaboration between Foundation and Oak Investment Partners providingconsulting and healthcare analytics and care management services; Bloomsburg Physicians

-exempt entity providing physician andother healthcare professional services; Geisinger- G

1

Throughout this document, the acronym "GHS" or the term "System" shall refer to the entire healthcare system comprised of theGeisinger Health System Foundation (the "Foundation") as parent and all subsidiary corporate entities comprising the System.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

8

located in Bloomsburg, Pennsylvania, a tax-exempt entity operating a long-term care nursinghome; Columbia Montour Home Health Services/Visiting Nurses Association, Inc. ,located in Bloomsburg, Pennsylvania, a tax-exempt entity that provides home health and hospiceservices; Lewistown Health Care Foundation -exempt entity that previously served as the corporate parent of GLH and affiliated entities; Health

-profit corporation which operates retail pharmacies with locations inLewistown, Belleville, Mifflintown and McAlisterville, Pennsylvania; Lewistown Ambulatory CareCorporation C -exempt entity operating a realestate holding company; Family Health Associates of Geisinger-Lewistown Hospital ,located in Lewistown, Pennsylvania, a tax-exempt entity which operates a multi-specialty group

Pennsylvania, a tax-exempt entity organized to improve the exchange of health care informationbetween organizations in the GHS service area.

All significant intercompany transactions have been eliminated.

The Foundation, GMC, GWV, GCMC, GLH, G-BH, the Clinic, GSS, Marworth, GCHS, RRG,MVCC, CMCI, CMCHS, CMHH, LHF, FHA, LACC, BPS and BHCC are tax-exempt pursuant toSection 501(c) (3) of the Internal Revenue Code. KeyHei has applied for 501(c) (3) tax-exemptionand is being operated consistently with a 501(c) (3) during 2014. MDI is tax-exempt pursuant to501(c) (2) of the Internal Revenue Code. GHP is tax-exempt pursuant to Section 501(c) (4) of theInternal Revenue Code. The tax-exempt entities did not incur any liability for federal income taxes,except for unrelated business income.

entities subject to corporate, legal and/or regulatory limitations.

2. Summary of Significant Accounting Policies

These financial statements have been prepared in conformity with accounting principles generally. G . The following is a summary of the

significant accounting and reporting policies used in preparing the consolidated financialstatements.

Cash and Cash EquivalentsCash and cash equivalents include investments in highly liquid debt instruments purchased with amaturity of three months or less, exclusive of long-term investments and assets limited as to use.The carrying amount reported approximates fair value.

Investments, Assets Limited as to Use and Investment IncomeInvestments are measured at fair value. All ofclassified as trading. This classification requires GHS to recognize unrealized gains and losses onsubstantially all of its investments in debt and equity securities as net unrealized investmentearnings (losses) in the Consolidated Statements of Operations and Changes in Net Assets.Interest income, dividends and realized and unrealized gains and losses on unrestrictedinvestments are determined on the specific method of identification and are recorded as investmentincome within other revenue or within investing and financing activities in the ConsolidatedStatements of Operations and Changes in Net Assets (net of investment related expenses). In theabsence of donor specification that investment income on donated funds be restricted, interestincome, dividends and realized and unrealized gains and losses on temporarily restrictedinvestments are recorded within investing and financing activities in the Consolidated Statements

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

9

of Operations and Changes in Net Assets. Interest income, dividends and realized and unrealizedgains and losses on trusts held as temporarily restricted and permanently restricted endowmentfunds are recorded as net investment gains (losses) in changes in temporarily restricted net assetsin the Consolidated Statements of Operations and Changes in Net Assets. Interest income,dividends and realized and unrealized gains and losses on trusts held as permanently restrictedare recorded as net investment gains (losses) in changes in permanently restricted net assets inthe Consolidated Statement of Operations and Changes in Net Assets.

Investments are exposed to various risks, such as interest rate, market and credit. Due to the levelof risk associated with investments and the level of uncertainty related to changes in their value, itis at least reasonably possible that changes in market valuations in the near term could materiallyaffect account balances and the amounts reported in the Consolidated Balance Sheet and theConsolidated Statements of Operations and Changes in Net Assets.

Amounts available to meet current liabilities have been reclassified to current investments in theConsolidated Balance Sheets.

Assets limited as to use - internally by the Board are resources that have been designated by theBoard for specific purposes. The Board retains control over designatedassets and may, at their discretion, subsequently use the assets for other purposes. Assets limitedas to use - externally other are primarily investments held by a Trustee under debt agreements fortax-exempt bond proceeds. Assets limited as to use - externally restricted by donors are held tomeet donor restrictions.

Accounts Receivable and AllowancesGHS s policy is to write off all patient accounts that have been identified as uncollectible. Anallowance for uncollectibles is recorded for accounts not yet written off that are anticipated tobecome uncollectible in future periods.

Insurance coverage and credit information are obtained from patients when available. No collateralis obtained for accounts receivable. Accounts receivable from third-party payors have beenadjusted to reflect the difference between charges and the estimated reimbursable amounts.

Insurance premiums that are past due greater than 60 days are written off as uncollectible and aresubject to subsequent contract cancellation under terms of the insurance contract.

InventoriesInventories are stated at the lower of cost or market. Cost is determined primarily on a first-in, first-out basis.

Property and Equipment and Long-Lived AssetsProperty and equipment and construction in progress are recorded at the lower of cost or fair value,if impaired. Depreciation is recorded using the straight-line method over the estimated useful livesof the respective assets. Leasehold improvements are amortized over the shorter of their usefullife or the term of the lease and renewal periods that are deemed to be reasonably assured at thedate the leasehold improvements are purchased using the straight-line method. Capital leases andsoftware licenses are amortized over the shorter of their useful life or the term of the lease usingthe straight-line method. The cost of assets and the related accumulated depreciation are removedfrom the Balance Sheet upon retirement or disposition and any gain or loss is reported in otherexpenses in the Consolidated Statements of Operations and Changes in Net Assets.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

10

GHS recognizes an impairment loss if the carrying amount of a long-lived asset is not recoverablefrom its future undiscounted cash flows and measures any impairment loss as the differencebetween the carrying amount and the fair value of the asset. No significant impairment losses onproperty and equipment were recorded during 2014 or 2013.

Pledges Receivable and ContributionsUnconditional donor promises to give cash, marketable securities and other assets are reported atfair value and discounted to present value at the date the promise is received to the extentestimated to be collectible. Conditional donor promises to give and indications of intentions to giveare not recognized until the condition is satisfied. Pledges received with donor restrictions that limitthe use of the donated assets are reported as temporarily restricted net assets. When a donorrestriction expires, that is, when a stipulated time restriction ends or purpose restriction isaccomplished, temporarily restricted net assets are transferred to unrestricted net assets andreported in the Consolidated Statements of Operations and Changes in Net Assets as net assetsreleased from restriction.

No amounts have been reflected in the financial statements for donated services. GHS pays formost services requiring specific expertise. However, many individuals volunteer their time andperform a variety of tasks that assist GHS with various programs.

Assets Held in Trustbeneficial interest in perpetual and other trusts that are

maintained and administered by independent trustees and are valued based on the fair value of theassets held in trust. Trusts that are perpetual, whereby the original corpus cannot be expended,are reported as permanently restricted net assets. Other trusts are reported as temporarilyrestricted net assets until they are liquidated. Distributions from trusts are recorded as investmentearnings if unrestricted or as net investment gains (losses) in temporarily restricted net assets iftheir use is restricted by the donor.

Accrued Medical ClaimsGHP, GIIC and GQO are at risk for certain medical costs of its members up to reinsurance limits.Accrued medical claims and related expenses (hospitalization and other outside medical services)are recorded in medical claims payable, accrued expenses and other liabilities. This liabilityincludes amounts billed from other medical providers and not yet paid and estimates of costsincurred for obligations to provide services under contracts as of the balance sheet dates.

GHP, GIIC and GQO record a liabilitexpected to be paid after the end of the period for services provided to members during the policyperiod. The estimate of costs incurred for obligations to provide services is based on historicaldata, current membership, health service utilization statistics and other related information. Theseaccruals are continually monitored and reviewed and, as settlements are made or accrualsadjusted, differences are reflected in current operations. Changes in assumptions for medicalcosts as well as changes in actual experience could cause these estimates to change in the nearterm.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

11

Derivative InstrumentsInterest rate swap agreements are used by GHS to manage interest rate exposures and to hedgethe changes in cash flows on variable rate debt. Derivative financial instruments involve, to avarying degree, elements of market and credit risk. The market risk associated with theseinstruments resulting from interest rate movements is expected to offset the market risk of theliabilities being hedged. The counterparties to the agreements relating to the interest rate swapsand option are major financial institutions with high credit ratings. GHS continually monitors thecredit ratings of the counterparties and does not believe that there is significant risk ofnonperformance by these counterparties.

All derivatives are reported in the Consolidated Balance Sheets at fair value, including those thatare designated and qualify as a cash flow hedging instruments. The gain or loss on the effectiveportion of the derivative is reported as an unrealized gain or loss on derivative in other changes inunrestricted net assets in the Consolidated Statements of Operations and Changes in Net Assets.The gain or loss on the ineffective portion of the derivative and changes in value of derivatives notdesignated as hedging instruments are recognized as an unrealized gain or loss on derivativesunder investing and financing activities in the Consolidated Statements of Operations and Changesin Net Assets.

Net Asset ClassificationUnrestricted net assets are not restricted by donors, or the donor-imposed restrictions have beensatisfied.

Temporarily restricted net assets are those whose use by GHS has been limited by donors to aspecific time period or purpose, primarily to support operations and for property and equipmentpurchases.

Permanently restricted net assets have been restricted by donors to be maintained by GHS, or adesignated trustee, in perpetuity.

Permanently restricted nets assets represent the original value of gifts donated to GHS throughendowments. GHS s permanently restricted net assets consist of approximately 200 endowmentsand trusts. Unless otherwise directed by the donor, gifts received for endowments are invested inaccordance with GHS s investment policy. From time to time, the fair value of investmentsassociated with individual donor-restricted endowments may fall below the original gift amount.Deficiencies of this nature, which are referred to as underwater funding, are reported as changes inunrestricted and temporarily restricted net assets in the Consolidated Statements of Operationsand Changes in Net Assets.

GHS annually appropriates a certain percentage of each endowment for spending in accordancewith the donor s intent. In order to preserve the real value of a donor s gift and to sustain fundingconsistent with donor intent, the annual appropriation rate is set to strike a reasonable balancebetween long-term objectives of preserving and growing each endowment for the future andproviding stable, annual appropriations. The difference between the endowment original value andthe market value of the endowment is recorded as temporarily restricted endowments.

The Board has designated certain Clinic unrestricted investments as quasi-endowments to supportresearch and other programs.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

12

The composition of and changes in endowment net assets, excluding trusts, by type of fund, is asfollows:

Permanently

Unrestricted Restricted

(Board Temporarily (Excluding

Designated) Restricted Trusts) Total

Endowment net assets at June 30, 2012 21,880$ 5,997$ 52,209$ 80,086$

Investment return

Realized investment gains (losses) 972 3,298 (1) 4,269

Unrealized investment gains 1,424 2,854 710 4,988

Total investment return 2,396 6,152 709 9,257

Contributions received from acquisition - - 7,956 7,956

Contributions received - - 977 977

Underwater funding - (316) - (316)

Annual appropriations (791) (2,507) - (3,298)

Endowment net assets at June 30, 2013 23,485 9,326 61,851 94,662

Investment return

Realized investment gains 1,765 4,456 58 6,279

Unrealized investment gains 1,933 4,621 1,047 7,601

Total investment return 3,698 9,077 1,105 13,880

Contributions received from acquisition - - 539 539

Contributions received - - 886 886

Underwater funding - (110) - (110)

Annual appropriations (727) (2,685) - (3,412)

Endowment net assets at June 30, 2014 26,456$ 15,608$ 64,381$ 106,445$

Noncontrolling InterestNoncontrolling interest represents the proportionate share of the equity of certain ventures that isowned by third parties. The net income or loss of these ventures is allocated to the noncontrollinginterest holders based on their percentage of ownership.

In fiscal 2014, previously unconsolidated xG came under GHS control and accordingly, thebusiness is now reflected in these financial statements with noncontrolling interest identified. Alsoincluded in the noncontrolling interest is the portion of a Dickson City, Pennsylvania ambulatorysurgery center not owned by GHS.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

13

For the years ended June 30, 2014 and 2013, components of the changes in consolidated netassets impacting the controlling financial interest and noncontrolling interest are:

Non-Controlling Controlling

Total Interest Interest

Balance July 1, 2013 1,931,371$ 1,931,371$ -$

Excess (deficiency) of revenue and gains over

expenses and losses 428,517 435,665 (7,148)Other changes in unrestricted net assets

Consolidation of controlled entities 30,604 13,345 17,259Unrealized (loss) on derivatives (255) (255) -

Net assets released from restriction, capital purchases 2,554 2,554 -Pension liability adjustment 3,681 3,681 -Net asset transfers for underwater endowments 10 10 -

Distributions to noncontrolling interest (1,072) - (1,072)

Increase in unrestricted net assets 2,395,410$ 2,386,371$ 9,039$

Net Patient Service RevenueNet patient service revenue is reported at the estimated net realizable amounts from patients,third-party payors, and others for services rendered, including estimated retroactive adjustmentsunder reimbursement agreements with third-party payors. Retroactive adjustments are accrued onan estimated basis in the period the related services are rendered and adjusted in future periods asfinal settlements are determined.

Premium RevenueGHP, GIIC and GQO recognize premiums from members as revenue in the period to which healthcare coverage relates. Premiums billed and collected in advance are recorded as unearnedpremiums.

Charity CareGHS provides servicesa patient is classified as a charity patient based on income eligibility criteria. GHS also providesfree care to patients that either do not pursue charity care eligibility or are otherwise determined tobe in need. GHS uses the services of a vendor to identify such additional patients who arepresumptively determined to qualify for charity care. Because GHS does not pursue collection ofamounts determined to qualify as charity care, they are not reported as revenue.

Additionally, GHS sponsors other charitable programs that provide substantial benefit to thebroader community. Such programs include services to the needy and elderly population requiringspecial support, various clinical outreach programs, and health education and promotion.

Bad DebtIn evaluating the collectability of accounts receivable, the System analyzes its past history andidentifies trends for each of its major payor sources of revenue to estimate the appropriateallowance for doubtful accounts and provision for bad debts. Management regularly reviews dataabout these major payor sources in evaluating the sufficiency of the allowance for doubtfulaccounts. For receivables associated with self-pay patients which include both patients withoutinsurance and patients with deductible and copayment balances due after third-party coverage, theSystem records a provision for bad debts in the period of service on the basis of its pastexperience, which indicates that many patients are unable or unwilling to pay the portion of their bill

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

14

for which they are financially responsible. The difference between discounted rates charged tothese patients and the amounts actually collected after all reasonable collection efforts have beenexhausted is charged off against the allowance for doubtful accounts.

Nonoperating LossesFor purposes of display, transactions deemed by management to be ongoing, major, or central tothe provision of health care services are reported as revenue and expenses. Other transactionsare reported as nonoperating losses, net.

Operating IndicatorThe excess of revenue and gains over expenses and losses, consistent with industry practice,includes all unrestricted revenue, expenses, and net gains and losses for the reporting period,except for net assets released from restriction to fund purchases of capital, defined benefit pensionliability adjustment, net asset transfers for underwater endowments, unrealized gains (losses) onthe effective portion of derivatives and distributions to noncontrolling interest.

Use of EstimatesThe preparation of financial statements in conformity with U.S. GAAP requires management tomake estimates and assumptions that affect the reported amounts of assets and liabilities anddisclosure of contingent assets and liabilities at the date of the financial statements and thereported amounts of revenue and expenses during the reporting period. Actual results could differfrom those estimates. Significant estimates include contractual allowances, estimated amountsdue to third-party payors, bad debt reserves, accrued medical claims, medical legal liabilities,swaps and option valuations, alternative investments valuation and expected rate of return oninvestments used to value defined benefit pension liabilities.

ReclassificationsCertain amounts and balances in the 2013 consolidated financial statements have beenreclassified to conform to the 2014 presentation.

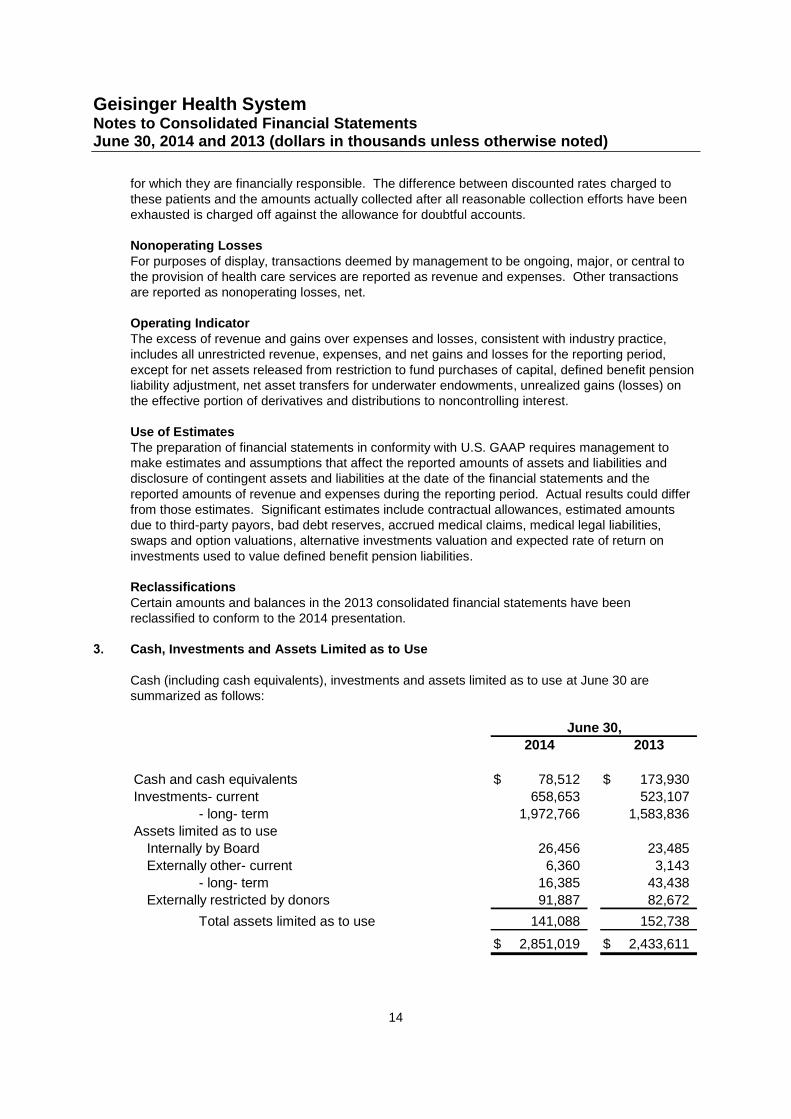

3. Cash, Investments and Assets Limited as to Use

Cash (including cash equivalents), investments and assets limited as to use at June 30 aresummarized as follows:

2014 2013

Cash and cash equivalents 78,512$ 173,930$

Investments- current 658,653 523,107

- long- term 1,972,766 1,583,836

Assets limited as to use

Internally by Board 26,456 23,485

Externally other- current 6,360 3,143

- long- term 16,385 43,438

Externally restricted by donors 91,887 82,672

Total assets limited as to use 141,088 152,738

2,851,019$ 2,433,611$

June 30,

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

15

Cash and cash equivalents, investments and amounts internally designated by the Board availablefor capital and operating expenditures total $2.7 billion and $2.3 billion at June 30, 2014 and 2013,respectively. GHS values certain financial and non-financial assets and liabilities by applying theFASB pronouncement on Fair Value Measurements. The pronouncement defines fair value andestablishes a framework for measuring fair value. That framework includes a hierarchy thatcategorizes and prioritizes the sources used to measure and disclose fair value. Fair value isdefined as the price that would be received to sell an asset or paid to transfer a liability in anorderly transaction between market participants at the measurement date (an exit price).

The hierarchy is broken down into three levels based on inputs that market participants would usein valuing the asset based on market data obtained from sources independent of GHS as follows:

Level 1: Unadjusted quoted market prices in active markets for identical assets or liabilities.

Level 2: Unadjusted quoted prices in active markets for similar assets or liabilities, unadjustedquoted prices for identical or similar assets or liabilities in markets that are not active, or inputsother than quoted prices that are observable.

Level 3: Unobservable inputs for the asset or liability.

Inputs broadly refer to the assumptions that market participants use to make valuation decisions,including assumptions about risk. Inputs may include price information, volatility statistics, specificand broad credit data, liquidity statistics and other factors. GHS is tomaximize the use of observable inputs (Levels 1 and 2) and minimize the use of unobservableinputs (Level 3). GHS considers observable data to be that market data which is readily available,regularly distributed or updated, reliable and verifiable, not proprietary and provided byindependent sources that are actively involved in the relevant market. The categorization of afinancial instrument within the hierarchy is based upon the pricing transparency of the instrumentand does not necessarily correspond to GHS s perceived risk of that instrument.

Assets are disclosed within the hierarchy based on the lowest (or least observable) input that is

judgment, which may affect the valuation and categorization within the fair value hierarchy. Thefair value of assets and liabilities using Level 3 inputs are generally determined by using pricingmodels, discounted cash flow methods or calculated net asset value (NAV) per share, which allrequire significant management judgment or estimation.

As a practical expedient, GHS is permitted under the pronouncement to estimate the fair value ofan investment in hedge funds and private equity at the measurement date using the reported NAV.Adjustment is required if GHS expects to sell the investment at a value other than NAV or if theNAV is not calculated in accordance with U.S. GAAPcertain hedge funds are generally valued based on the most current NAV adjusted for cash flowswhen the reported NAV is not at the measurement date. This amount represents fair value ofthese investments at June 30, 2014.

GHS performs additional procedures including due diligence reviews on its investments in hedgefunds and private equity and other procedures with respect to the capital account or NAV providedto ensure conformity with U.S. GAAP. GHS has assessed factors including, but not limited to,

fair value measurement standard, price transparency and valuationprocedures in place, the ability to redeem at NAV at the measurement date and existence ofcertain redemption restrictions at the measurement date.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

16

Fair values are provided by the custodian. Management believes that fair values provided by thecustodian are a reasonable estimation of such fair values.

Cash and Cash EquivalentsCash and cash equivalents include short-term investments and fixed income investments withmaturities of less than three months, which were purchased within three months of fiscal year end.Cash and cash equivalents are valued using observable market data and are categorized as Level1 based on quoted market prices in active markets. The majority of these investments are held inmoney market accounts.

Equity FundsEquity funds consist of mutual funds whose underlying securities are valued on quoted marketprices in active markets obtained from exchange or dealer markets for identical assets and areaccordingly categorized as Level 1 with no valuation adjustments applied. Certain equity mutualfunds also include individual securities with Level 2 characteristics resulting in the fundscategorized as Level 2.

Marketable Equity SecuritiesMarketable equity securities consist of individual securities that are generally valued based onquoted market prices in active markets obtained from exchange or dealer markets and areaccordingly categorized as Level 1 with no valuation adjustments applied.

Corporate ObligationsCorporate obligations consist of individual securities that are valued based on quoted market pricesor dealer or broker quotations and are categorized as Level 2 or in the cases where they tradeinfrequently as Level 3.

Fixed Income FundsFixed income funds consist of mutual funds whose underlying securities are valued on quotedmarket prices in active markets obtained from exchange or dealer markets and are categorized asLevel 2.

U.S. Government and Agency ObligationsU.S. Government and agency obligations consist of individual securities and are valued based onquoted market prices or dealer/broker quotations and are categorized as Level 2 or in the caseswhere they trade infrequently as Level 3.

Absolute and Total Return Hedge FundsAbsolute and total return hedge funds consist of equity and fixed income managed funds consistingof limited partnership interests in hedge funds. The fund managers invest in a variety of securitiesbased on the strategy of the fund which may or may not be quoted in an active market. The hedgefunds are valued at NAV. The investments are categorized as Level 3.

Private EquityPrivate equity investments are in the form of limited partnership interests. The fund managersprimarily invest in private investments for which there is no readily determinable market value. Thefund manager may value the underlying private investments based on an appraised value,discounted cash flow, industry comparables or some other method. These limited partnershipinvestments are valued at NAV and are categorized as Level 3.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

17

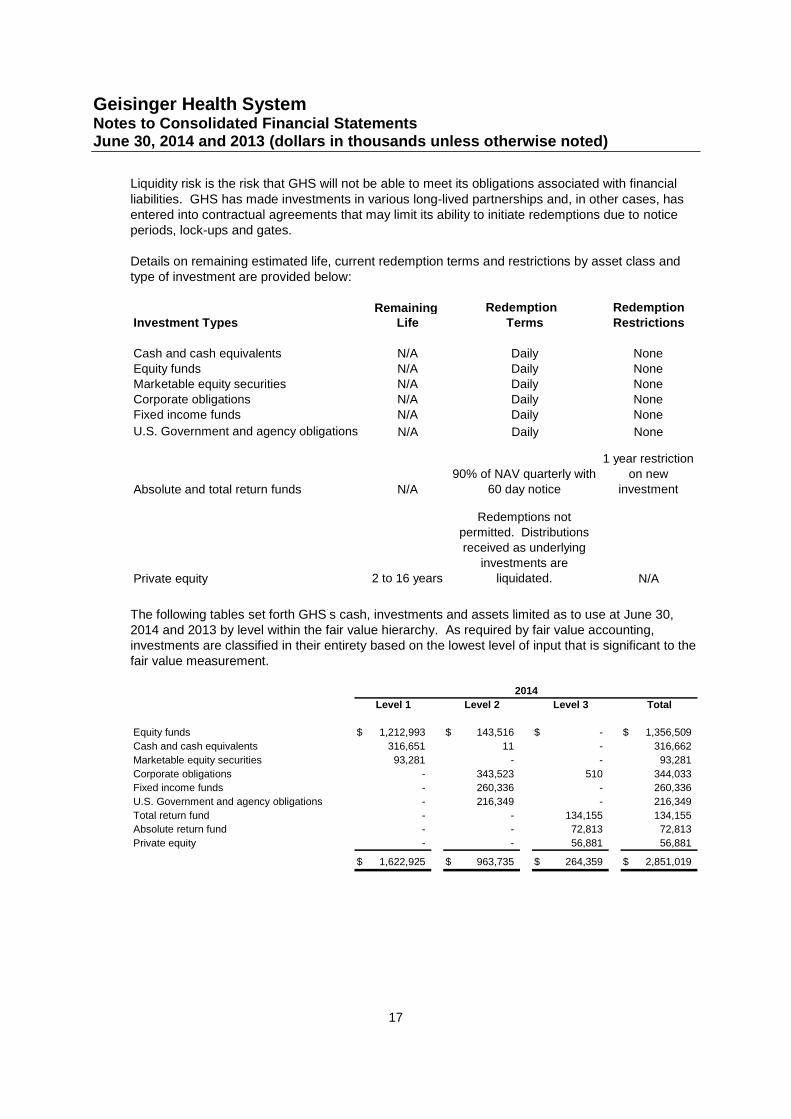

Liquidity risk is the risk that GHS will not be able to meet its obligations associated with financialliabilities. GHS has made investments in various long-lived partnerships and, in other cases, hasentered into contractual agreements that may limit its ability to initiate redemptions due to noticeperiods, lock-ups and gates.

Details on remaining estimated life, current redemption terms and restrictions by asset class andtype of investment are provided below:

Remaining Redemption RedemptionInvestment Types Life Terms Restrictions

Cash and cash equivalents N/A Daily NoneEquity funds N/A Daily NoneMarketable equity securities N/A Daily NoneCorporate obligations N/A Daily NoneFixed income funds N/A Daily None

U.S. Government and agency obligations N/A Daily None

Absolute and total return funds N/A

90% of NAV quarterly with60 day notice

1 year restrictionon new

investment

Private equity 2 to 16 years

Redemptions notpermitted. Distributionsreceived as underlying

investments areliquidated. N/A

The following tables set forth GHS s cash, investments and assets limited as to use at June 30,2014 and 2013 by level within the fair value hierarchy. As required by fair value accounting,investments are classified in their entirety based on the lowest level of input that is significant to thefair value measurement.

Level 1 Level 2 Level 3 Total

Equity funds 1,212,993$ 143,516$ -$ 1,356,509$

Cash and cash equivalents 316,651 11 - 316,662

Marketable equity securities 93,281 - - 93,281

Corporate obligations - 343,523 510 344,033

Fixed income funds - 260,336 - 260,336

U.S. Government and agency obligations - 216,349 - 216,349

Total return fund - - 134,155 134,155

Absolute return fund - - 72,813 72,813

Private equity - - 56,881 56,881

1,622,925$ 963,735$ 264,359$ 2,851,019$

2014

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

18

Level 1 Level 2 Level 3 Total

Equity funds 984,535$ 98,100$ -$ 1,082,635$

Cash and cash equivalents 376,606 13 - 376,619

Marketable equity securities 77,955 - - 77,955

Corporate obligations - 320,988 - 320,988

Fixed income funds - 209,394 - 209,394

U.S. Government and agency obligations - 177,191 - 177,191

Total return fund - - 84,711 84,711

Absolute return fund - - 50,160 50,160

Private equity - - 53,958 53,958

1,439,096$ 805,686$ 188,829$ 2,433,611$

2013

The following table shows the changes in Level 3

Fixed Income

Equity Managed

Managed Funds and Partnership

Funds Investments Investments Total

Level 3 balances at June 30, 2012 75,913$ 47,724$ 51,301$ 174,938$

Net realized gains - - 2,488 2,488

Net unrealized gains 8,798 3,194 879 12,871

Purchases - - 6,742 6,742

Settlements - (758) (7,452) (8,210)

Level 3 balances at June 30, 2013 84,711 50,160 53,958 188,829

Net realized gains - - 2,020 2,020

Net unrealized gains 4,444 2,654 4,002 11,100

Purchases 45,000 20,509 6,186 71,695

Sales - - (9,285) (9,285)

Level 3 balances at June 30, 2014 134,155$ 73,323$ 56,881$ 264,359$

As of June 30, 2014 and 2013, there were no transfers between Level 1 and Level 2. GHS hascommitted to fund certain partnership investments, which were not yet drawn at June 30, 2014.These unfunded commitments totaled $30.6 million at June 30, 2014. Such commitments haveterms from two to sixteen years.

Market risk exists to the extent that the values of GHS s monetary assets fluctuate as a result ofchanges in market prices. Changes in market prices can arise from factors specific to individualsecurities or their respective issuers or factors affecting all securities traded in a particular market.Relevant factors for GHS are both volatility and liquidity of specific securities and markets in whichGHS holds investments. GHS employs the services of professional investment managers and hasestablished investment guidelines to ensure that the portfolio is diversified and exposure to marketrisk is managed.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

19

Unrealized investment earnings represent the change in fair value of investments calculated wherea security is held at the beginning of the period or acquired during the period and is also held at theend of the period. Realized gains or losses on the sale of investments are the difference betweensale proceeds (net of any transaction costs) and original/amortized cost. Interest and dividendincome is recorded on the accrual basis and includes the net accretion of discounts andamortization of premiums on debt securities.

Investment income and realized and unrealized gains and losses on cash and cash equivalents,investments, assets limited as to use and assets held in trust consist of the following:

2014 2013

Other revenueInterest and dividend income 708$ 832$

Investment and financing activities

Interest and dividend income 50,556$ 43,137$Net gains on the sale of securities 103,769 68,960Net unrealized investment gains on securities 146,786 70,597

301,111$ 182,694$

Temporarily restricted net assetsInterest and dividend income 1,543$ 1,504$

Net gains on the sale of securities 3,206 2,142Net unrealized investment gains on securities 5,013 2,895

9,762$ 6,541$

Permanently restricted net assetsTrust distributions, net of interest and dividend income (264)$ (289)$Net gains on securities held in beneficial interest

in perpetual trusts 3,030 1,898

2,766$ 1,609$

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

20

4. Property and Equipment

Property and equipment and accumulated depreciation and amortization consist of:

EstimatedUseful Lives 2014 2013

Land 41,378$ 37,136$Land improvements 57,480 45,675Buildings and building improvements 601,973 488,433

Equipment 1,086,387 951,427Computer software (5 years) 161,140 139,387

1,948,358 1,662,058

Less: Accumulated depreciation and amortization (937,180) (821,089)

1,011,178 840,969

Construction in progress 116,916 109,693

1,128,094$ 950,662$

June 30,

Depreciation and amortization expense related to property and equipment for the years endedJune 30, 2014 and 2013 was $121.6 million and $111.4 million, respectively. At June 30, 2014 and2013, $21.2 million and $23.3 million, respectively, of construction related purchases had not beenpaid, and accordingly, were accrued in medical claims payable, accrued expenses and otherliabilities.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

21

5. Long-Term Debt

Long-term debt consists of:

Carrying Fair Carrying Fair

Value Value Value Value

Series A of 2013 Bonds 65,000$ 65,000$ -$ -$

Series B of 2013 Bonds 50,000 50,000 - -

Series C of 2013 Bonds 51,265 51,265 - -

Series D of 2013 Bonds 43,135 43,135 - -

Series A-1 of 2011 Bonds 100,000 109,777 100,000 105,542

Series A-2 of 2011 Bonds 29,235 32,334 31,850 34,243

Series B of 2011 Bonds 50,000 50,000 50,000 50,000

Series C of 2011 Bonds 50,000 50,000 50,000 50,000

Series A of 2009 Bonds 157,000 170,330 157,000 163,447

Series B of 2009 Bonds 50,000 50,000 50,000 50,000

Series C of 2009 Bonds 65,000 65,000 65,000 65,000

Series 2007 Lewistown 19,215 20,011 - -

Series 2007 Bonds 68,850 52,980 68,850 59,202

Series A of 2005 Bonds 65,000 65,000 65,000 65,000

Series B of 2005 Bonds 62,300 62,300 62,300 62,300

Series C of 2005 Bonds 62,700 62,700 62,700 62,700

Series 2002 Bonds 50,000 50,000 50,000 50,000

Series A of 1998 Bonds 27,700 33,201 27,700 33,129

Total tax-exempt revenue bonds 1,066,400 1,083,034 840,400 850,563

Other long-term debt

Bank loans - - 56,668 56,668

Notes payable 15,191 15,191 17,009 17,009

Capital leases 1,465 1,465 569 569

Total debt 1,083,056 1,099,690 914,646 924,809

Less: current installments (5,103) (5,103) (7,357) (7,357)

Unamortized premium 1,498 1,498 1,923 1,9231,079,451$ 1,096,085$ 909,212$ 919,375$

2014 2013

June 30,

Maturities of long-term debt for the next five years and thereafter for the years ending June 30 areas follows:

2015 5,103$2016 5,0612017 1,987

2018 5,0732019 5,336

Thereafter 1,060,496

1,083,056$

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

22

Montour County established the Geisinger Authority (the Authority ) for the purpose of financingcertain capital projects of GHS and other nonprofit organizations within the Commonwealth ofPennsylvania. All but the Series 2007 Lewistown tax exempt revenue bonds were issued throughthe Authority. The Foundation has entered into a Master Trust Indenture with the bond trusteedated as of August 1, 1998 that governs all debt issued there under. Under the terms of the MasterTrust Indenture, substantially all indebtedness is a joint and several obligation of the ObligatedGroup, whose sole present member is the Foundation. Additional indentures were issued witheach new bond issuance. The proceeds from the issuance of the bonds were used for the purposeof financing capital projects or to refinance other bonds.

Fixed rate bonds have various installments of principal due prior to maturity. Variable rate demandVRDB , bank held rate and index floating rate bonds have balloon payments due upon

maturity. The following table provides information on each bond issue. Average interest ratesinclude the impact of a discount or premium and remarketing and liquidity fees.

Final

Bond Issue Interest Rate Mode Par Maturity 2014 2013

Series A of 2013 Bonds VRDB 65,000$ 10/1/43 0.4 % N/A

Series B of 2013 Bonds VRDB 50,000 10/1/43 0.4 % N/A

Series C of 2013 Bonds Bank Held Rate 51,265 10/1/43 0.8 % N/A

Series D of 2013 Bonds Bank Held Rate 43,135 10/1/43 0.9 % N/A

Series A-1 of 2011 Bonds Fixed Rate 100,000 06/01/41 4.8 % 4.8 %

Series A-2 of 2011 Bonds Fixed Rate 29,235 06/01/28 3.8 % 3.6 %

Series B of 2011 Bonds VRDB 50,000 06/01/41 0.4 % 0.5 %

Series C of 2011 Bonds VRDB 50,000 06/01/41 0.5 % 0.5 %

Series A of 2009 Bonds Fixed Rate 157,000 06/01/39 5.2 % 5.2 %

Series B of 2009 Bonds Bank Held Rate 50,000 06/01/39 0.7 % 0.7 %

Series C of 2009 Bonds Bank Held Rate 65,000 06/01/39 0.7 % 0.7 %

Series 2007 Lewistown Bonds Fixed Rate 19,215 07/01/30 5.1 % N/A

Series 2007 Bonds Index Floating Rate 68,850 05/01/37 0.9 % 1.0 %

Series A of 2005 Bonds VRDB 65,000 05/15/35 0.6 % 0.6 %

Series B of 2005 Bonds VRDB 62,300 08/01/22 0.5 % 0.5 %

Series C of 2005 Bonds VRDB 62,700 08/01/28 0.5 % 0.6 %

Series 2002 Bonds VRDB 50,000 11/15/32 0.5 % 0.5 %

Series A of 1998 Bonds Fixed Rate 27,700 08/15/23 5.2 % 5.2 %

Average Interest Rate

All VRDB are supported by standby bond purchase agreements. The standby bond purchaseagreements provide loans to GHS in the amounts necessary to purchase variable rate bonds thatare not remarketed.

The debt documents include the requirement for GHS to maintain a historical debt coverage ratio,as defined in the Master Trust Indenture, of 1.1 to 1. GHS is in compliance with the covenant as ofJune 30, 2014.

Net interest paid including swap agreements was $26.2 million and $25.7 million in 2014 and 2013,respectively.

The fair value of long-term debt is estimated using quoted market prices, where applicable. Ifquoted market prices are not available, fair values are based on quoted market prices ofcomparable instruments. Accordingly, the fair value of long-term debt is considered Level 2.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

23

6. Interest Rate Swaps and Option

During 2007, GHS entered into two interest rate swap agreements with a total outstanding notionalamount of $68.9 million at both June 30, 2014 and June 30, 2013 remaining in effect until May 1,2037. During the term of the swap, the swap effectively converts variable rate debt to a fixed rate.Under the swap, GHS pays a fixed rate of 4.40% times the notional amount and receives a floatingrate equal to 67% of the London Inter-Bank Offer Rate ( LIBOR ) plus 0.77%. Net interest paid orreceived under the swap agreement is included in interest expense in the Consolidated Statementsof Operations and Changes in Net Assets. This transaction qualifies as an effective cash flowhedge, and therefore the changes in fair value are reported as unrealized gain or loss on derivativewithin other changes in unrestricted net assets in the Consolidated Statements of Operations andChanges in Net Assets.

In September 2005, GHS entered into an interest rate swap agreement with a total outstandingnotional amount of $33.0 million at June 30, 2014 decreasing incrementally to zero by August 1,2028. During the term of the swap, the swap effectively converts variable rate debt to a fixed rate.Under the swap, GHS pays a fixed rate of 3.40% times the notional amount and receives a floatingrate equal to 68% of the LIBOR. Payments under the swap were exchanged beginningSeptember 2008. Net interest paid or received under the swap agreement is included in interestexpense in the Consolidated Statements of Operations and Changes in Net Assets. Thistransaction does not qualify as an effective cash flow hedge and therefore the changes in fair valueare recognized as an unrealized gain or loss on derivatives within the investing and financingactivities in the Consolidated Statements of Operations and Changes in Net Assets.

During 2001, GHS entered into an interest rate swap agreement with a total outstanding notionalamount of $80.0 million at June 30, 2014. The swap has a notional amount of $80.0 million frominception until August 1, 2022 and $40.0 million from August 1, 2022 to August 1, 2028. During theterm of the swap, the swap effectively converts variable rate debt to a fixed rate. Under the swap,GHS pays a fixed rate of 4.86% times the notional amount and receives a rate equal to theSecurities Industry and Financial Markets Association ( SIFMA ) rate, an index of high-gradetax-exempt variable rate demand obligations. This transaction does not qualify as an effectivecash flow hedge and therefore the changes in fair value are recognized as an unrealized gain orloss on derivatives within the investing and financing activities in the Consolidated Statements ofOperations and Changes in Net Assets.

During 2001, GHS also entered into an option that provides GHS with 0.85% times the samenotional amount of the swap. In exchange for the premium, GHS granted the counterparty the rightto create a derivative transaction with the same remaining terms as the swap, but with thecounterparty as the fixed-rate payer and GHS as the floating-rate payer. This derivative wouldhave cash flows exactly opposite to the swap. The counterparty may only exercise this option ifSIFMA has averaged more than 7% for six consecutive months. As of June 30, 2014, this optionhas not been triggered.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

24

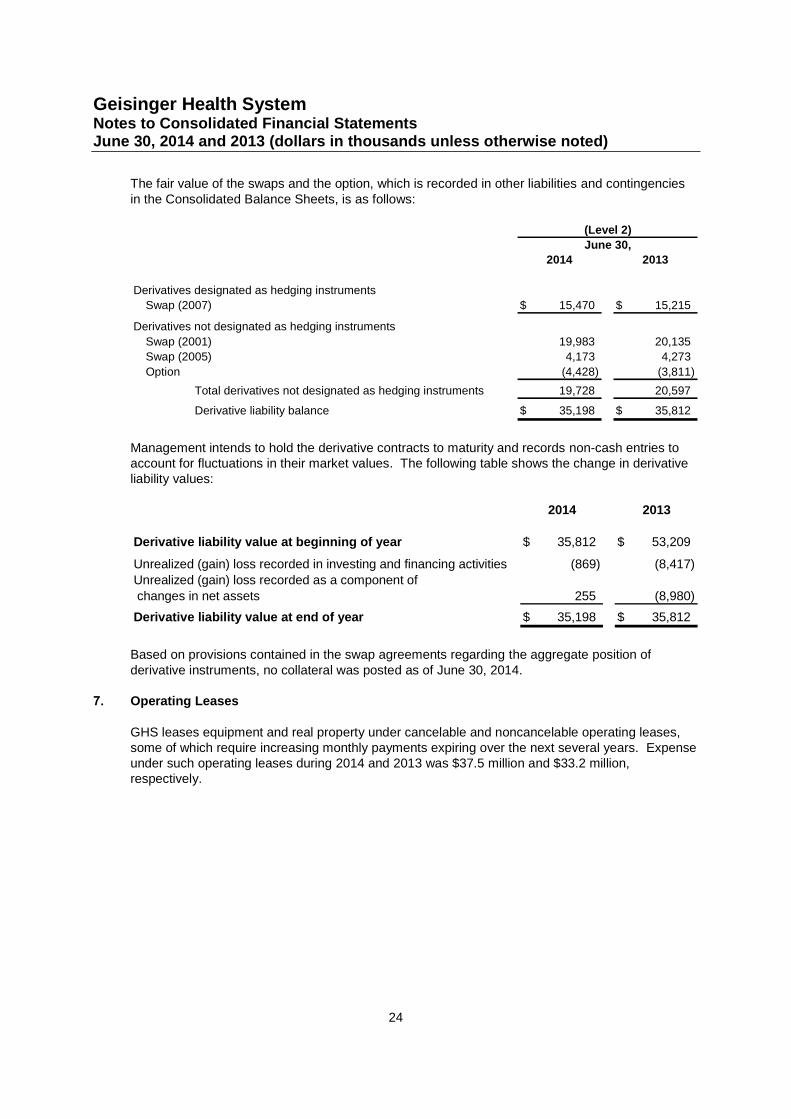

The fair value of the swaps and the option, which is recorded in other liabilities and contingenciesin the Consolidated Balance Sheets, is as follows:

2014 2013

Derivatives designated as hedging instruments

Swap (2007) 15,470$ 15,215$

Derivatives not designated as hedging instruments

Swap (2001) 19,983 20,135

Swap (2005) 4,173 4,273

Option (4,428) (3,811)

Total derivatives not designated as hedging instruments 19,728 20,597

Derivative liability balance 35,198$ 35,812$

(Level 2)

June 30,

Management intends to hold the derivative contracts to maturity and records non-cash entries toaccount for fluctuations in their market values. The following table shows the change in derivativeliability values:

2014 2013

Derivative liability value at beginning of year 35,812$ 53,209$

Unrealized (gain) loss recorded in investing and financing activities (869) (8,417)Unrealized (gain) loss recorded as a component ofchanges in net assets 255 (8,980)

Derivative liability value at end of year 35,198$ 35,812$

Based on provisions contained in the swap agreements regarding the aggregate position ofderivative instruments, no collateral was posted as of June 30, 2014.

7. Operating Leases

GHS leases equipment and real property under cancelable and noncancelable operating leases,some of which require increasing monthly payments expiring over the next several years. Expenseunder such operating leases during 2014 and 2013 was $37.5 million and $33.2 million,respectively.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

25

The following is a schedule by year of future minimum lease payments under operating leases asof June 30, 2014:

Year Ending June 30,

2015 28,781$2016 23,7272017 12,584

2018 8,2042019 5,846

2020 and after 14,188

93,330$

8. Retirement and Deferred Compensation Plans

Substantially all employees participate in defined contribution plans. These plans include the GSS401(k) Savings Plan, the GMMC 401(k) Safe Harbor Plan, the GSS Tax Sheltered Annuity (TSA)Program 403(b) plan, the Community Medical Center 403(b) Supplemental Contributory RetirementPlan, the Community Medical Center 401(a) Supplemental Contributory Retirement Plan, the FHAof Lewistown Hospital 401(k) Defined Contribution Plan, the Lewistown Hospital DefinedContribution Plan (401(k)) and the Bloomsburg Employer Retirement Savings Plan 403(b).Employer contributions to the plans were $64.7 million and $56.2 million in 2014 and 2013,respectively.

Various 457(b) and 457(f) deferred compensation plans are offered to physicians and other highlycompensated employees. The investments held in these deferred compensation plans arerecorded in other assets with a corresponding liability in other liabilities and contingencies in theConsolidated Balance Sheets.

GCMC and G-BH sponsor defined benefit plans that were frozen effective September 30, 2002 andJune 30, 2006, respectively. GLH (acquired by GHS November 1, 2013) sponsors a definedbenefit plan. Effective July 1, 2010, GLH reduced future benefits from the plan by excludingemployees hired on or after that date and by reducing future benefits of those remaining in the planto a 1% of average annual compensation formula.

The projected benefit obligation, the fair value of plan assets, and the amounts recognized in thebalance sheet as accrued pension cost for all GHS defined benefit plans at June 30, 2014 were$173.3 million, $135.2 million and $38.1 million, respectively. The same amounts for 2013 were$69.6 million, $50.8 million and $18.8 million, respectively. The acquisition of GLH resulted in a$22.7 million increase in accrued pension cost at June 30, 2014.

The hospitals intend to contribute approximately $6.1 million to the plans in 2015.

The assumptions used in computing the total net periodic pension cost and total benefit obligationfor the sponsors of the plan at June 30, 2014 and 2013 are as follows:

GCMC GLH GBH GCMC GBH

Discount rate, net periodic pension cost 4.51 % 4.50 % 4.54 % 3.85 % 4.35 %Discount rate, total benefit obligation 4.16 % 4.16 % 4.16 % 4.51 % 4.54 %

Expected long-term return on plan assets 6.50 % 7.50 % 6.00 % 6.50 % 6.00 %

2014 2013

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

26

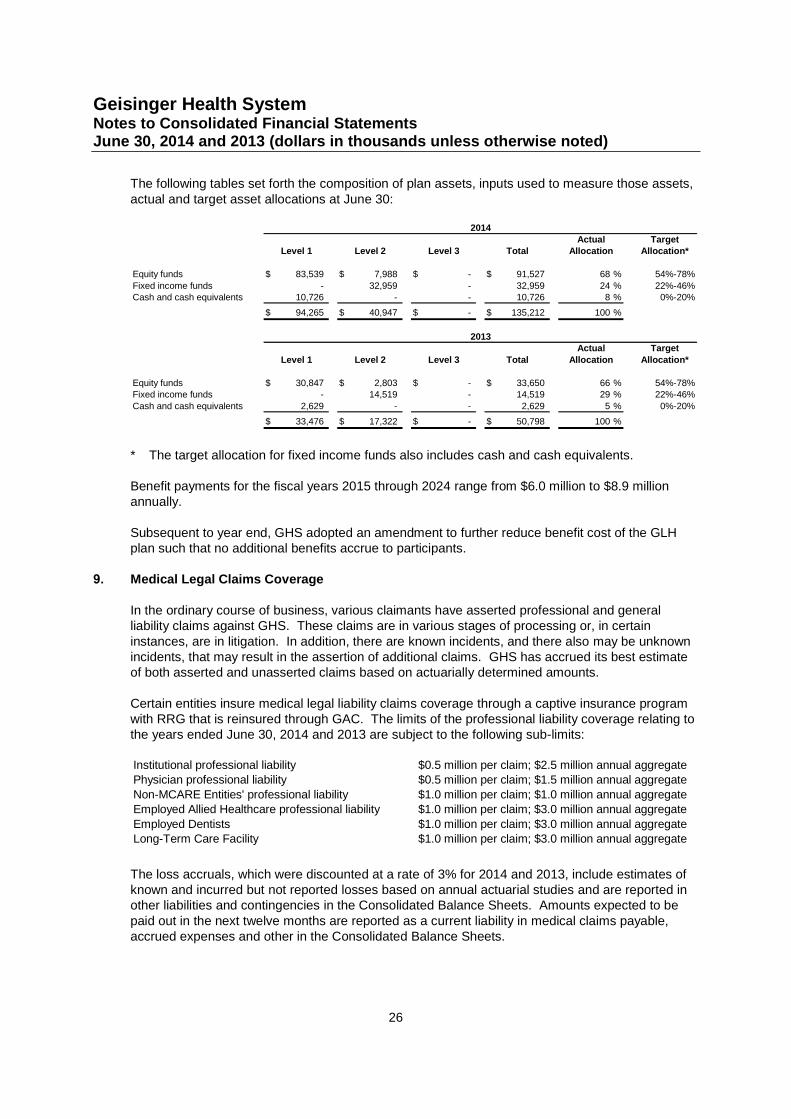

The following tables set forth the composition of plan assets, inputs used to measure those assets,actual and target asset allocations at June 30:

Actual TargetLevel 1 Level 2 Level 3 Total Allocation Allocation*

Equity funds 83,539$ 7,988$ -$ 91,527$ 68 % 54%-78%

Fixed income funds - 32,959 - 32,959 24 % 22%-46%Cash and cash equivalents 10,726 - - 10,726 8 % 0%-20%

94,265$ 40,947$ -$ 135,212$ 100 %

Actual Target

Level 1 Level 2 Level 3 Total Allocation Allocation*

Equity funds 30,847$ 2,803$ -$ 33,650$ 66 % 54%-78%Fixed income funds - 14,519 - 14,519 29 % 22%-46%

Cash and cash equivalents 2,629 - - 2,629 5 % 0%-20%

33,476$ 17,322$ -$ 50,798$ 100 %

2014

2013

* The target allocation for fixed income funds also includes cash and cash equivalents.

Benefit payments for the fiscal years 2015 through 2024 range from $6.0 million to $8.9 millionannually.

Subsequent to year end, GHS adopted an amendment to further reduce benefit cost of the GLHplan such that no additional benefits accrue to participants.

9. Medical Legal Claims Coverage

In the ordinary course of business, various claimants have asserted professional and generalliability claims against GHS. These claims are in various stages of processing or, in certaininstances, are in litigation. In addition, there are known incidents, and there also may be unknownincidents, that may result in the assertion of additional claims. GHS has accrued its best estimateof both asserted and unasserted claims based on actuarially determined amounts.

Certain entities insure medical legal liability claims coverage through a captive insurance programwith RRG that is reinsured through GAC. The limits of the professional liability coverage relating tothe years ended June 30, 2014 and 2013 are subject to the following sub-limits:

Institutional professional liability $0.5 million per claim; $2.5 million annual aggregatePhysician professional liability $0.5 million per claim; $1.5 million annual aggregate

Non-MCARE Entities' professional liability $1.0 million per claim; $1.0 million annual aggregateEmployed Allied Healthcare professional liability $1.0 million per claim; $3.0 million annual aggregate

Employed Dentists $1.0 million per claim; $3.0 million annual aggregateLong-Term Care Facility $1.0 million per claim; $3.0 million annual aggregate

The loss accruals, which were discounted at a rate of 3% for 2014 and 2013, include estimates ofknown and incurred but not reported losses based on annual actuarial studies and are reported inother liabilities and contingencies in the Consolidated Balance Sheets. Amounts expected to bepaid out in the next twelve months are reported as a current liability in medical claims payable,accrued expenses and other in the Consolidated Balance Sheets.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

27

GAC has also issued a direct policy, on a claims-made basis, for miscellaneous professionalliability which is not covered by the Medical Care Availability and Reduction of Error ( MCARE )Fund. The policy provides limits of $1.0 million per occurrence with no aggregate limit. This policyhas a retroactive date of July 1, 1985 and later.

The MCARE Act was enacted by the legislature of the Commonwealth of Pennsylvania( Commonwealth ) in 2002. This act created the MCARE Fund, which replaced The PennsylvaniaMedical Professional Liability Catastrophe Loss Fund (the Medical CAT Fund ), to facilitate thepayment of medical malpractice claims exceeding the primary layer of professional liabilityinsurance carried by GHS and other health care providers practicing in the Commonwealth. The

as a percentage of the rates established by the Joint Underwriting Association (also aCommonwealth of Pennsylvania agency), for basic coverage. The MCARE act provides for thegradual phase-out of Medical CAT Fund coverage, however, this has been deferred by thePennsylvania legislature and will be considered in the future.

The actuarially computed liability for all health care providers (hospital, physicians, and others)participating in the MCARE Fund at December 31, 2013 (the latest date that such information isavailable) was $1.16 billion. Even though the MCARE Fund coverage will eventually be phasedout, the Commonwealth has indicated that the unfunded liability will likely be funded throughassessments in future years as MCARE Fund-covered claims are eventually settled and paid. TheCommonwealth has agreed to devote the proceeds of the Automobile Catastrophe Fundsurcharge, estimated at $40 million per year for 10 years (for a total of $400 million), to help offsetthe MCARE Fund unfunded liability.

nd were $8.0 million and $5.9 million for2014 and 2013, respectively. No provision has been made for any future MCARE Fund

unfunded liability cannot be reasonably estimated.

Certain entities are provided excess coverage through a captive insurance program with GAC andexcess commercial policies. The excess coverage provides coverage above the primary andMCARE Fund layers where applicable. The loss accruals, which were discounted at a rate of 3%for 2014 and 2013, include estimates of known and incurred but not reported losses based onannual actuarial studies. The loss accruals are also reported in other liabilities and contingenciesin the Consolidated Balance Sheets. Amounts expected to be paid out in the next twelve monthsare reported as a current liability in medical claims payable, accrued expenses and other in theConsolidated Balance Sheets.

10. Revenue, Charity Care, and Accounts Receivable, Net

GHS is a physician-led, integrated health services organization that has as its main components:1) an array of health services providers including two tertiary/quaternary care teaching hospitals,three community hospitals, two nursing homes, home health and hospice agencies and an alcoholand chemical dependency treatment center; 2) a multispecialty physician group practice of morethan 1,100 physicians practicing at approximately 83 primary and specialty clinics; and 3) one of

surance organizations with approximately 479,000 members as ofJune 30, 2014.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

28

Major components of revenue consist of the following:

Revenue % of Total Revenue % of Total

Net patient service revenueMedicare (MC) 544,313$ 13.7% 514,044$ 15.3%Medical Assistance (MA) 194,436 4.9% 177,358 5.3%

Other payors 1,059,834 26.6% 1,015,321 30.3%

1,798,583 45.2% 1,706,723 50.9%

Premium revenueMC Advantage 812,795 20.4% 698,205 20.8%Commercial 649,183 16.3% 638,304 19.0%

MA and other state programs 574,835 14.5% 175,526 5.2%

2,036,813 51.2% 1,512,035 45.0%

Other revenue 142,530 3.6% 136,308 4.1%

3,977,926$ 100.0% 3,355,066$ 100.0%

2014 2013

GHS have agreements with third-party payors that provide for paymentsat amounts different from its established rates. Inpatient acute care rehabilitation, psychiatric, andoutpatient services for MC and MA program beneficiaries are paid at prospectively determinedrates per discharge or visit. These rates vary according to a patient classification system that isbased on clinical, diagnostic, and other factors.

Laws and regulations governing MC and MA are complex and subject to interpretation. GHS isaware of these laws and regulations and, to the best of its knowledge and belief, is in compliancewith them. Amounts received from MC and MA are subject to review and final determination byprogram intermediaries or their agents. Generally, tentative settlements of these receivables havebeen completed through June 30, 2013. Provisions have been made in the accompanyingfinancial statements for anticipated adjustments.

In July 2010, the Pennsylvania General Assembly passed the Public Welfare Code amendment(Act 49), which was signed into law by the Governor, establishing a new program referred to asMedicaid Modernization. The program was subsequently approved by the Centers for Medicareand Medicaid Services . The program is designed to provide additional funding toPennsylvania hospitals for the purpose of enhancing access to quality healthcare for qualifying MAbeneficiaries, helping to partially mitigate the losses incurred by hospitals resulting from lowreimbursement rates. To accomplish this objective, the program provides participating hospitalswith improved inpatient fee-for-service hospital payments, establishes enhanced hospital paymentsthrough MA managed care organizations, and secures additional federal matching MA fundsthrough a quality care assessment under which hospitals pay the state a percentage of their netinpatient revenue.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

29

The cost of charity service provided was approximately $36.0 million and $29.7 million in 2014 and2013, respectively. The costs of charity care are derived from both estimated and actual data. Theestimated cost of charity includes the direct and indirect cost of providing such services and isestimated of cost to gross charges, which is then multiplied by the grossuncompensated charges associated with providing care to charity patients. In addition to charityservice, services are provided under the MA program to financially needy patients. The paymentsreceived under this program are less than the cost of providing the services. The unpaid cost ofthis program was approximately $178.1 million and $185.9 million in 2014 and 2013, respectively.In addition, bad debt expense associated with net patient service revenue was $53.7 million and$59.1 million in 2014 and 2013, respectively.

GHS grants credit without collateral to its patients, most of whom are local residents and areinsured under third-party payor agreements. Significant concentrations of net accounts receivablefrom commercial payors due to health service providers that exceed 10% of net accountsreceivable were as follows:

Amount due % of Total Amount due % of Total

Highmark 24,670$ 12.1 % 17,215$ 9.5 %

Capital Blue Cross 15,006$ 7.4 % 18,549$ 10.2 %

June 30,2014 2013

Premium revenue from MC Advantage products is based on a risk-adjustment model according tohealth severity that pays more for enrollees with predictably higher costs. Under this model, ratespaid to MC Advantage plans are based on actuarially determined bids, which include a process

ogram. Under therisk-adjustment model, all MC Advantage plans must collect and submit the necessary diagnosiscode information from hospital inpatient, hospital outpatient, and physician providers to CMS withinprescribed deadlines. The CMS risk-adjustment model uses this diagnosis data to calculate therisk adjusted premium payment to MC Advantage plans.

C Advantage contractsrelated to this risk adjustment diagnosis data. These Risk-Adjustment Data Validation Auditsreview medical record documentation in an attempt to validate provider coding practices and thepresence of risk adjustment conditions which influence the calculation of premium payments to MCAdvantage plans. In February 2012, CMS released a final version of the audit methodology, whichincluded guidance on: 1) a fee for service adjustment factor that will further reduce any identifiedpayment error rate in the event of a CMS audit, 2) the exposure period, which limits exposure toplan payment years 2011 and beyond, and 3) CMS selecting 30 plans for audit in the first year.MC Advantage premiums and liabilities are subject to estimation based upon the diagnosis datasubmitted to CMS and ultimately accepted by CMS.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

30

11. Functional Expenses

GHS provides comprehensive health care services (including primary and tertiary care, traumacare, psychiatric care, and outpatient surgery) and operates a licensed HMO and PPOs providingcomprehensive health care to subscribers. Health care services are provided primarily to residentsin northeastern and central Pennsylvania.

Expenses related to providing these services (including interest expense) are as follows:

2014 2013

Health care and program services 2,304,625$ 2,043,289$HMO and PPO services 1,140,379 822,747

Basic and clinical research 46,733 44,884General and administrative 375,660 306,208

3,867,397$ 3,217,128$

12. Acquisitions

Effective November 1, 2013, GHS acquired LHF and its affiliates (GLH, FHA, LAC, and HEI).

Assets acquired and liabilities assumed in the acquisition were recorded in the accompanying

Consolidated Balance Sheet as of the acquisition date based upon their estimated fair values. The

results of operations of these corporations have been included in the accompanying Consolidated

Statements of Operations and Changes in Net Assets since the acquisition date and are not

GHSF recorded a contribution totaling $16.8 million representing the excess of the fair value of

assets acquired over the fair value of liabilities assumed from the LHF acquisition. Fair value of the

acquired assets and liabilities at November 1, 2013 were as follows:

Unrestricted Temporarily PermanentlyNet Asset Restricted Restricted

Deficit Net Assets Net Assets Total

Cash and cash equivalents 10,808$ -$ -$ 10,808$Investments 28,505 187 539 29,231

Property and equipment, net 28,769 - - 28,769Other assets 18,686 - - 18,686Current and long-term debt (24,724) - - (24,724)

Accrued pension cost (24,998) - - (24,998)Other liabilities and contingencies (21,020) - - (21,020)

16,026$ 187$ 539$ 16,752$

No consideration was exchanged and no goodwill or other intangible assets were recognized as a

result of this acquisition. The unrestricted net asset was recognized as contribution from

acquisitions in arriving at the excess of revenue and gains over expenses and losses in the

accompanying Consolidated Statements of Operations and Changes in Net Assets.

Geisinger Health SystemNotes to Consolidated Financial StatementsJune 30, 2014 and 2013 (dollars in thousands unless otherwise noted)

31

13. Temporarily Restricted Net Assets

Temporarily restricted net assets are available for the following purposes:

2014 2013

Purchase of equipment 19,488$ 12,912$Support operations 26,282 24,024

45,770$ 36,936$

June 30,