u.s. shale gas in contexteia mission: independent statistics and analysis •eia was created by the...

TRANSCRIPT

www.eia.govU.S. Energy Information Administration Independent Statistics & Analysis

U.S. Shale Gas in Context

For

National Conference of State Legislatures – Natural Gas Policy Institute

September 9, 2015| Pittsburgh, Pennsylvania

By

Grant Nülle, Upstream Oil & Gas Economist, Exploration and Production

Analysis Team

Overview of U.S. Natural Gas production and trends

Discussion agenda

• About the U.S. Energy Information Administration

• Fundamentals of shale gas

• Natural gas production and electricity generation outlook

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 2

EIA mission: independent statistics and analysis

• EIA was created by the U.S. Congress in 1977

• EIA collects, analyzes, and disseminates independent and

impartial energy information to promote sound policymaking,

efficient markets, and public understanding of energy and its

interaction with the economy and the environment

• EIA is the nation's premier source of energy information and,

by law, its data, analyses, and forecasts are independent of

approval by any other officer or employee of the U.S.

Government

• EIA does not propose or advocate any policy positions

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 3

EIA produces data series, analyses, and energy projections

• Weekly, monthly, and annual data

– Displays U.S. and regional production, stocks, blender inputs, imports, and exports

• Real-time analyses

– Digests important developments in Today in Energy, This Week in Petroleum, Issues & Trends, Country Analysis Briefs, Drilling Productivity Report

• Short-Term Energy Outlook (STEO)

– Forecasts U.S. supplies, demands, imports, stocks, and prices of energy with a horizon of 12 to 24 months

• Annual Energy Outlook (AEO)

– Presents 25- to 30-year projection and analysis of U.S. energy supply, demand, and prices

• International Energy Outlook (IEO)

– Assesses international energy production and consumption

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 44

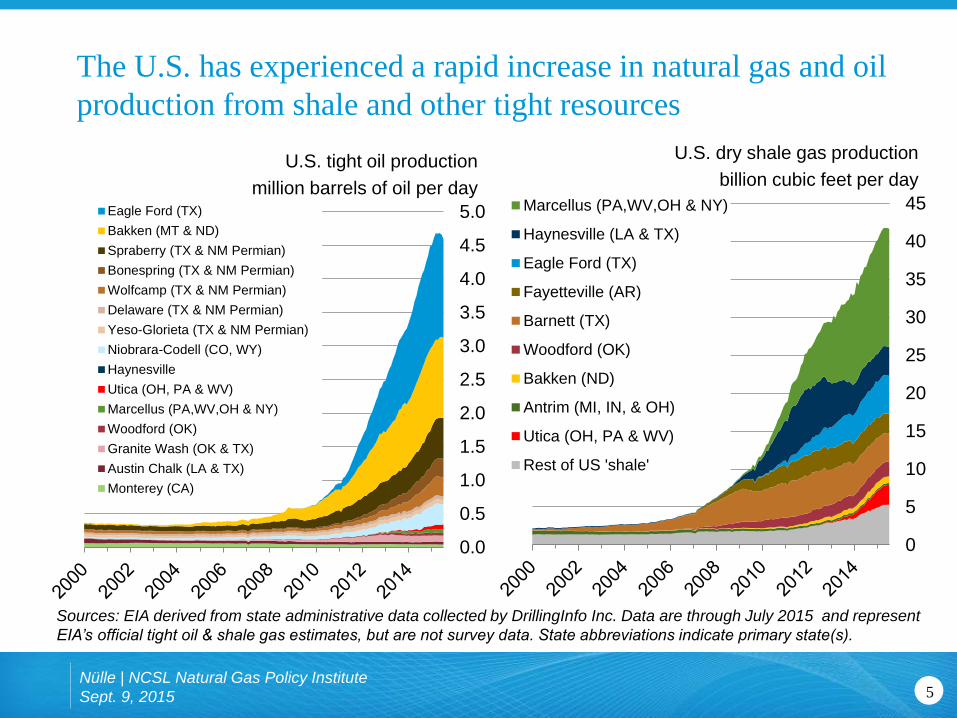

The U.S. has experienced a rapid increase in natural gas and oil

production from shale and other tight resources

5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0Eagle Ford (TX)

Bakken (MT & ND)

Spraberry (TX & NM Permian)

Bonespring (TX & NM Permian)

Wolfcamp (TX & NM Permian)

Delaware (TX & NM Permian)

Yeso-Glorieta (TX & NM Permian)

Niobrara-Codell (CO, WY)

Haynesville

Utica (OH, PA & WV)

Marcellus (PA,WV,OH & NY)

Woodford (OK)

Granite Wash (OK & TX)

Austin Chalk (LA & TX)

Monterey (CA)

U.S. tight oil production

million barrels of oil per day

0

5

10

15

20

25

30

35

40

45Marcellus (PA,WV,OH & NY)

Haynesville (LA & TX)

Eagle Ford (TX)

Fayetteville (AR)

Barnett (TX)

Woodford (OK)

Bakken (ND)

Antrim (MI, IN, & OH)

Utica (OH, PA & WV)

Rest of US 'shale'

U.S. dry shale gas production

billion cubic feet per day

Sources: EIA derived from state administrative data collected by DrillingInfo Inc. Data are through July 2015 and represent

EIA’s official tight oil & shale gas estimates, but are not survey data. State abbreviations indicate primary state(s).

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015

0

10

20

30

40

50

60

70

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2002 2004 2006 2008 2010 2012 2014

Rest of US gas production

Marcellus (PA & WV)

Haynesville (LA & TX)

Eagle Ford (TX)

Fayetteville (AR)

Barnett (TX)

Woodford (OK)

Bakken (ND)

Antrim (MI, IN, & OH)

Utica (OH, PA & WV)

Other US 'shale'

Shale gas % of total

Natural gas production (dry)

billion cubic feet per day

Shale gas production as a

percent of total gas production

Sources: EIA Natural Gas Monthly data through December, STEO through June 2015 and Drilling Info.

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 6

Estimated U.S. shale gas production was 41.0 Bcf/d in June 2015

about 56% of total U.S. dry production (73.6 Bcf/d)

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 7

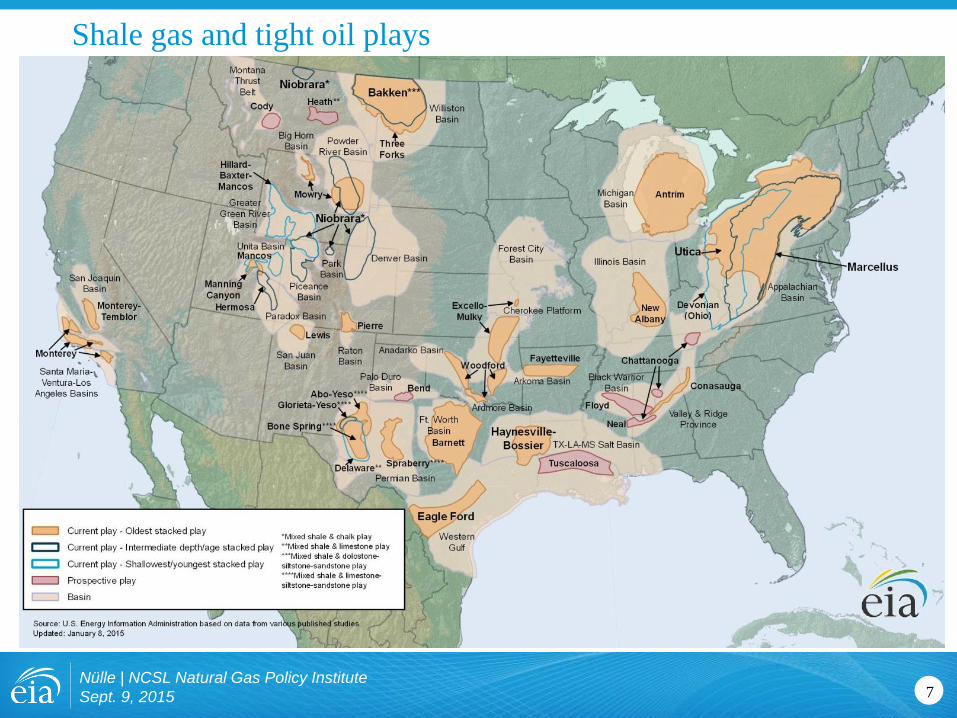

Shale gas and tight oil plays

Tight oil characteristics vary considerably

• Prior to the “shale development breakthrough”

– Drillers targeted either oil or natural gas formations

– Production was relatively stable over a long period from each well

– Simple rig count was sufficient to monitor and forecast production

• Drilling in tight formations

– New applications of technology: Horizontal drilling and hydraulic fracturing

– Pad drilling: Multiple wells per rig from one surface location

– High initial production rates driven by better technology

– Steep production declines

– Formations yielding both oil and natural gas

– Regional differences contrast rig and well productivity

– Higher costs to drill and complete a well

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 8

Shale gas and tight oil trends: production

by geography – the Drilling Productivity

Report (DPR)

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015

http://www.eia.gov/petroleum/drilling/

9

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 10

2 months or more 2 – 4 months 1- 2 months or more

Source: EIA, Drilling Productivity Report, August 2015

Seven key plays account for nearly all recent growth in U.S. oil and

natural gas production

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 11

DPR captures key elements of shale

Source: EIA Drilling Productivity Report, Aug. 2015, DrillingInfo Inc.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Bakken Eagle Ford Haynesville Marcellus Niobrara Permian Utica

August 2014

August 2015

new-well gas production per rig

thousand cubic feet per day

Source: EIA, Drilling Productivity Report, July 2015

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 12

Rig productivity underpins natural gas production gains

Contributing factors to U.S. Shale Gas / Tight Oil production

• Technical expertise and experience

• Extensive transportation capacity

• Price responsiveness of producers

• Regulatory stability & property rights

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 13

Natural gas & electricity generation

outlook

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 14

An increasing amount of electric power generation comes from

natural gas

15

electricity net generation

trillion kilowatthours

Source: EIA, Annual Energy Outlook 2015 Reference case

0

1

2

3

4

5

1990 1995 2000 2005 2010

13%

27%

19%

39%

13%

NuclearPetroleum and other liquids

Natural gas

Coal

Renewables

2013

1%

1993

11%

13%

19%

53%

4%

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015

Low natural gas prices have made natural gas

competitive with coal generation

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 16

Source: U.S. Energy Information Administration, Electricity Data Browser

0

2

4

6

8

10

12

14

Natural Gas

Coal

Average U.S. costs for fossil fuels for generation $/MMBtu

17Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015

Coal38.8%

Petroleum0.7%

Natural gas27.5%

Other gases0.3%

Nuclear19.5%

Conventional hydroelectric

6.3%

Wind4.4%

Solar thermal and PV

0.4%Wood and wood-derived fuels

1.1% Geothermal0.4%

Other biomass0.5%

Other6.9%

In 2014, U.S. electricity generation was 67% fossil fuels, 20%

nuclear, and 13% renewable2014 Total net generation:

4,093 billion kWh 2014 Non-hydro renewable

net generation:

281 billion kWh

Source: EIA, Monthly Energy Review

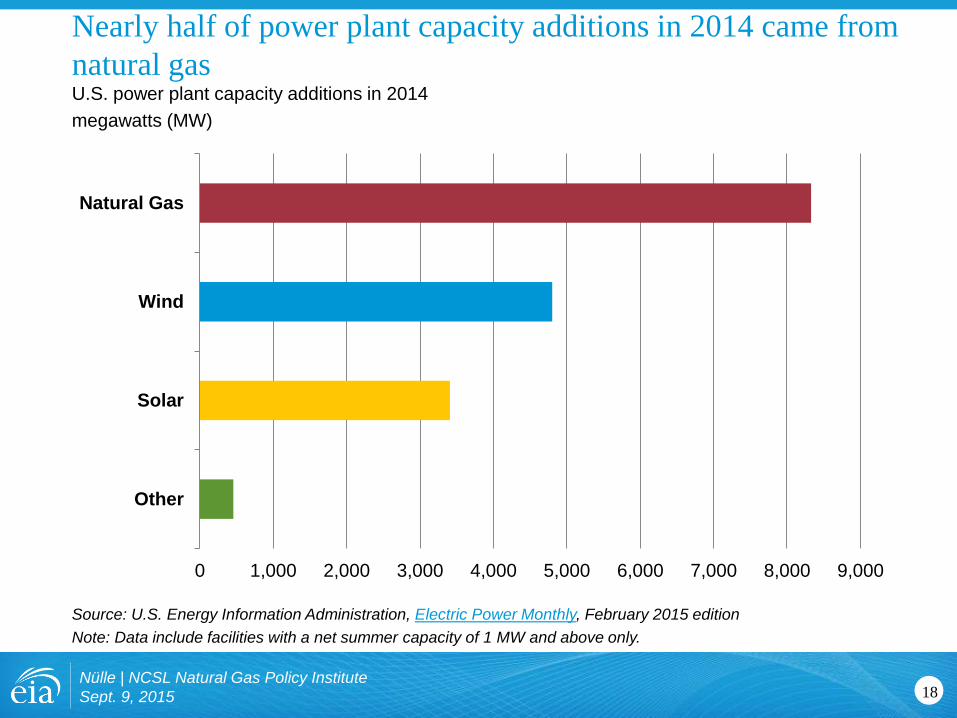

U.S. power plant capacity additions in 2014

megawatts (MW)

Source: U.S. Energy Information Administration, Electric Power Monthly, February 2015 edition

Note: Data include facilities with a net summer capacity of 1 MW and above only.

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 18

Nearly half of power plant capacity additions in 2014 came from

natural gas

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000

Other

Solar

Wind

Natural Gas

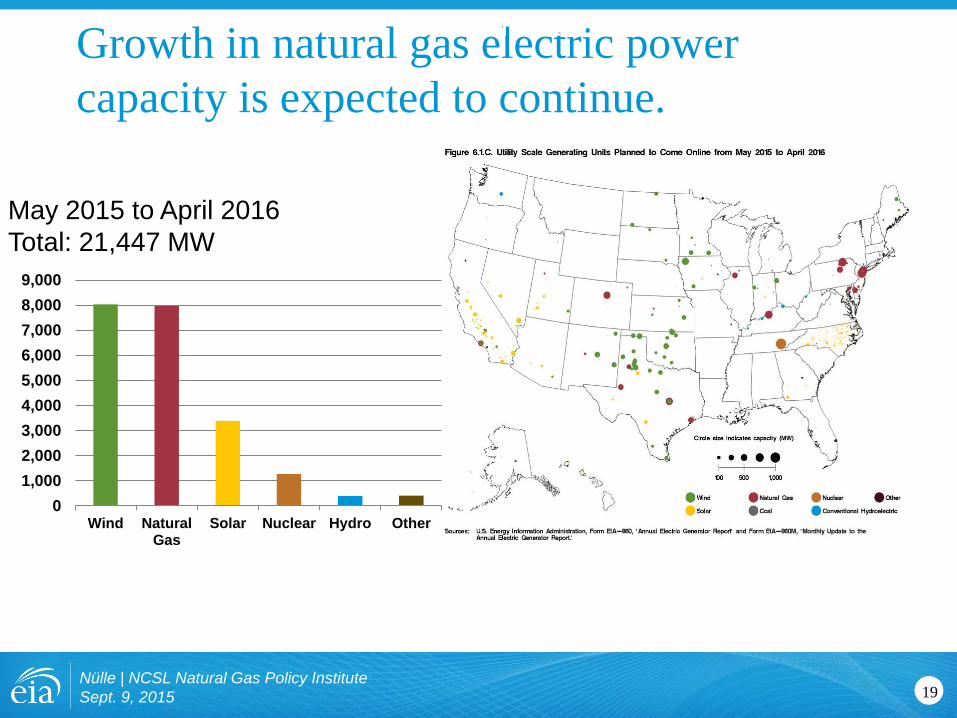

Growth in natural gas electric power

capacity is expected to continue.

June 2014 to May 2015 Additions

EPM maps

May 2015 to April 2016

Total: 21,447 MW

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 19

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Wind NaturalGas

Solar Nuclear Hydro Other

Shale resources remain the dominant source of U.S. natural gas

production growth

20

U.S. dry natural gas production

trillion cubic feet

Source: EIA, Annual Energy Outlook 2015 Reference case

0

10

20

30

40

50

60

70

80

90

100

0

5

10

15

20

25

30

35

40

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Tight gas

Coalbed methane

Other lower 48 onshore

Shale gas and tight oil plays

AlaskaLower 48 offshore

ProjectionsHistory 2013

billion cubic feet per day

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015

21

0

10

20

30

40

50

60

70

80

90

0

5

10

15

20

25

30

35

2005 2013 2020 2025 2030 2035 2040

U.S. dry gas consumption

trillion cubic feet

Source: EIA, Annual Energy Outlook 2015 Reference case

ProjectionsHistory

Industrial*Electric powerResidential Transportation**

10.9

4.2

1.6

9.4

3.6

8.9

4.9

0.9

8.2

3.3

*Includes combined heat-and-power and lease and plant fuel

**Includes pipeline fuel

Natural gas consumption growth is driven by increased use in all

sectors except residential

billion cubic feet per day

Commercial

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015

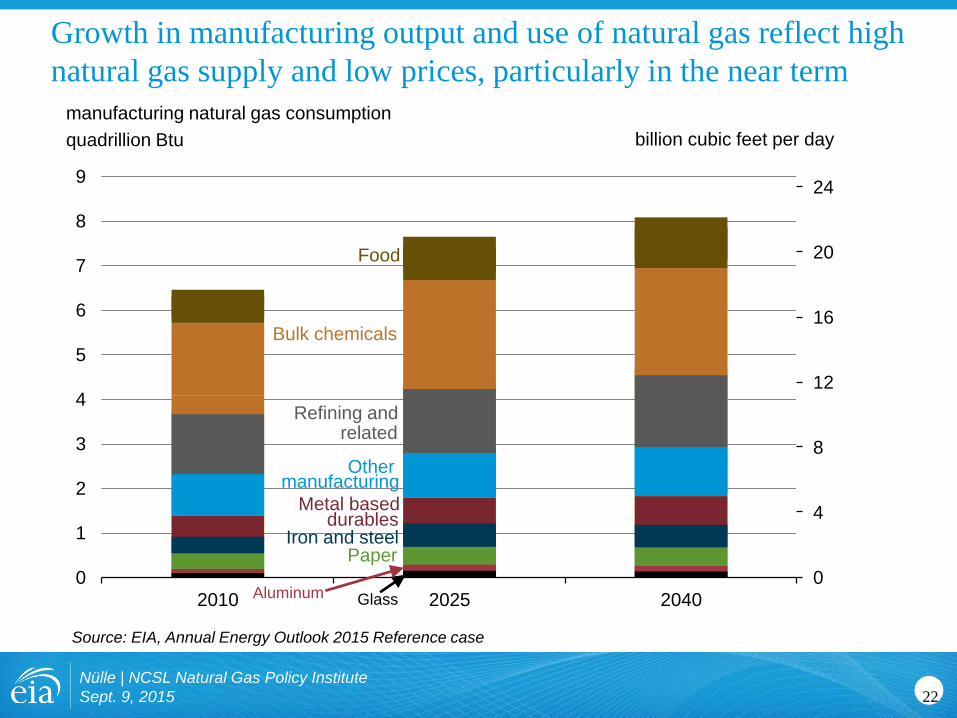

Growth in manufacturing output and use of natural gas reflect high

natural gas supply and low prices, particularly in the near term

22

manufacturing natural gas consumption

quadrillion Btu

Source: EIA, Annual Energy Outlook 2015 Reference case

0

4

8

12

16

20

24

0

1

2

3

4

5

6

7

8

9

2010 2025 2040GlassAluminum

manufacturing

Iron and steel

Refining and

Food

Bulk chemicals

Other

Metal based

billion cubic feet per day

durables

Paper

related

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015

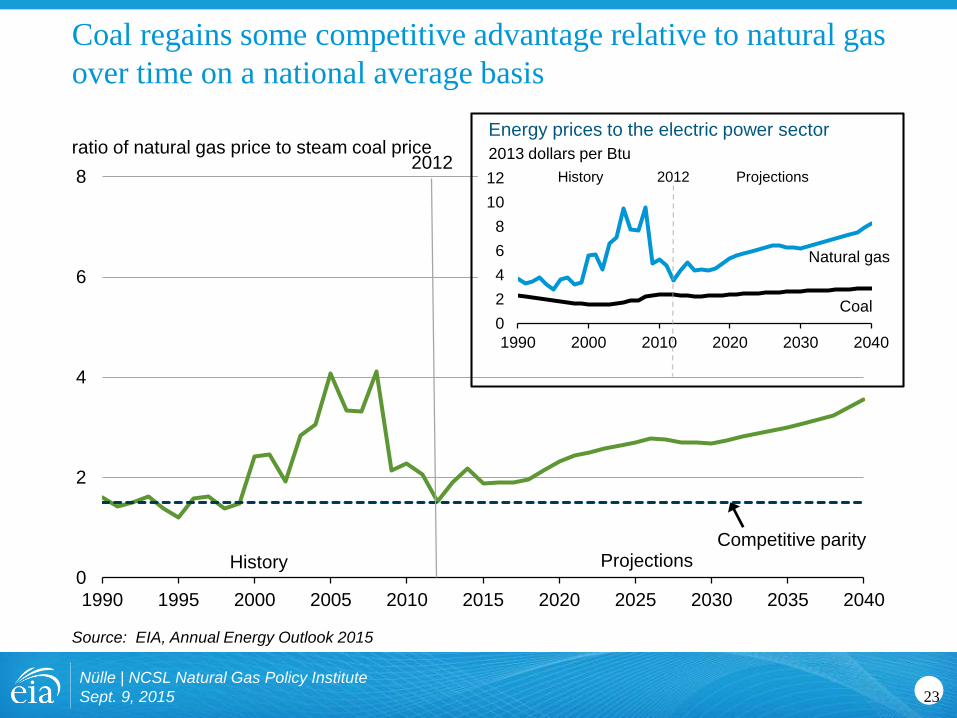

Coal regains some competitive advantage relative to natural gas

over time on a national average basis

0

2

4

6

8

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

ratio of natural gas price to steam coal price

Source: EIA, Annual Energy Outlook 2015

0

2

4

6

8

10

12

1990 2000 2010 2020 2030 2040

History Projections

20122013 dollars per Btu

History Projections2012

Competitive parity

Energy prices to the electric power sector

Coal

Natural gas

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 23

Natural gas is projected to grow faster than other fuels in the

AEO2015 Reference case

billion kilowatthours

Coal

Petroleum

Nuclear

Natural Gas

Renewables

0

500

1000

1500

2000

2500

1980 1990 2000 2010 2020 2030 2040

Note: Includes generation from plants in both the electric power and end-use sectors.

ProjectionsHistory 2013

24

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015

Source: Projections: EIA, Annual Energy Outlook 2015 ; History: EIA, Annual Energy Review;

For more information

U.S. Energy Information Administration home page | www.eia.gov

Annual Energy Outlook | www.eia.gov/forecasts/aeo

Short-Term Energy Outlook | www.eia.gov/forecasts/steo

International Energy Outlook | www.eia.gov/forecasts/ieo

Today In Energy | www.eia.gov/todayinenergy

Monthly Energy Review | www.eia.gov/totalenergy/data/monthly

State Energy Portal | www.eia.gov/state

Drilling Productivity Report | www.eia.gov/petroleum/drilling

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 25

26

Supplemental Slides

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015

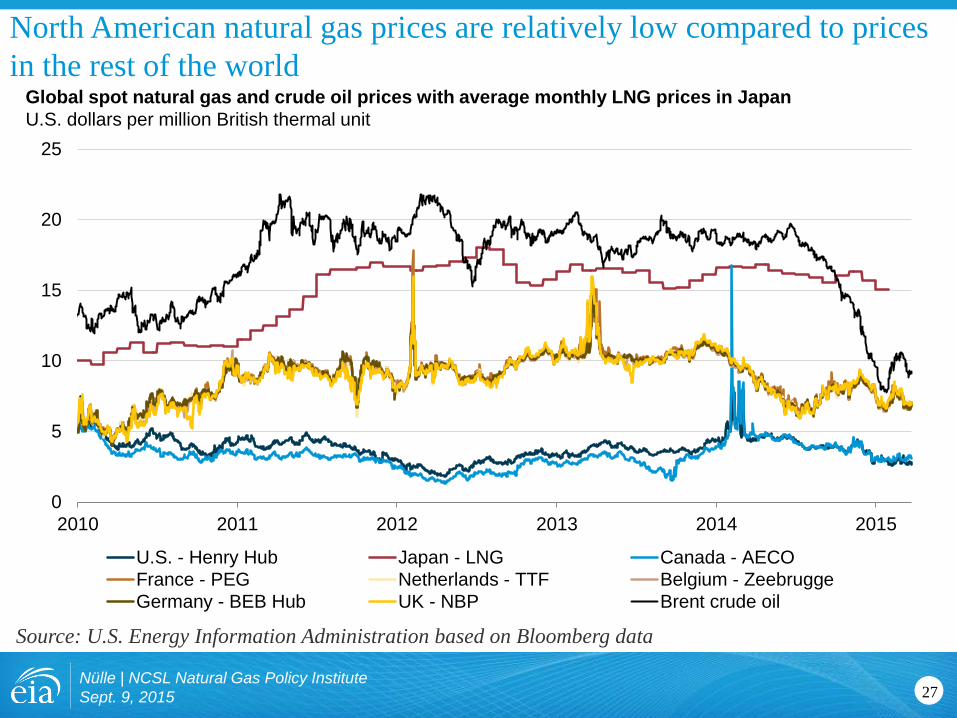

North American natural gas prices are relatively low compared to prices

in the rest of the world

Source: U.S. Energy Information Administration based on Bloomberg data

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 27

0

5

10

15

20

25

2010 2011 2012 2013 2014 2015

U.S. - Henry Hub Japan - LNG Canada - AECO

France - PEG Netherlands - TTF Belgium - Zeebrugge

Germany - BEB Hub UK - NBP Brent crude oil

Global spot natural gas and crude oil prices with average monthly LNG prices in Japan

U.S. dollars per million British thermal unit

U.S. becomes a net exporter of natural gas in the near future

U.S. dry natural gas

trillion cubic feet per year

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015

-10

0

10

20

30

40

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

ProjectionsHistory 2013

Consumption

Production

Net exports

100

75

50

25

0

-25

billion cubic feet per day

28

Source: EIA, Annual Energy Outlook 2015

U.S. natural gas imports and exports

trillion cubic feet

-8

-4

0

4

8

12

16

2000 2010 2020 2030 2040 2020 2030 2040 2020 2030 2040

LNG imports

Source: EIA, Annual Energy Outlook 2015

29

billion cubic feet per day

Projected U.S. natural gas exports reflect the spread between domestic

natural gas prices and world energy prices

ProjectionsHistory 2013

-10

0

10

20

2013 2013

30

40

-20Reference Low Oil Price

High Oil and Gas

Resource

Pipeline exports

to Mexico

Lower 48 states

LNG exports

Pipeline exports to Canada Pipeline imports from Canada

Alaska LNG exports

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015

0

3

6

9

12

2005 2010 2015 2020 2025 2030 2035 2040

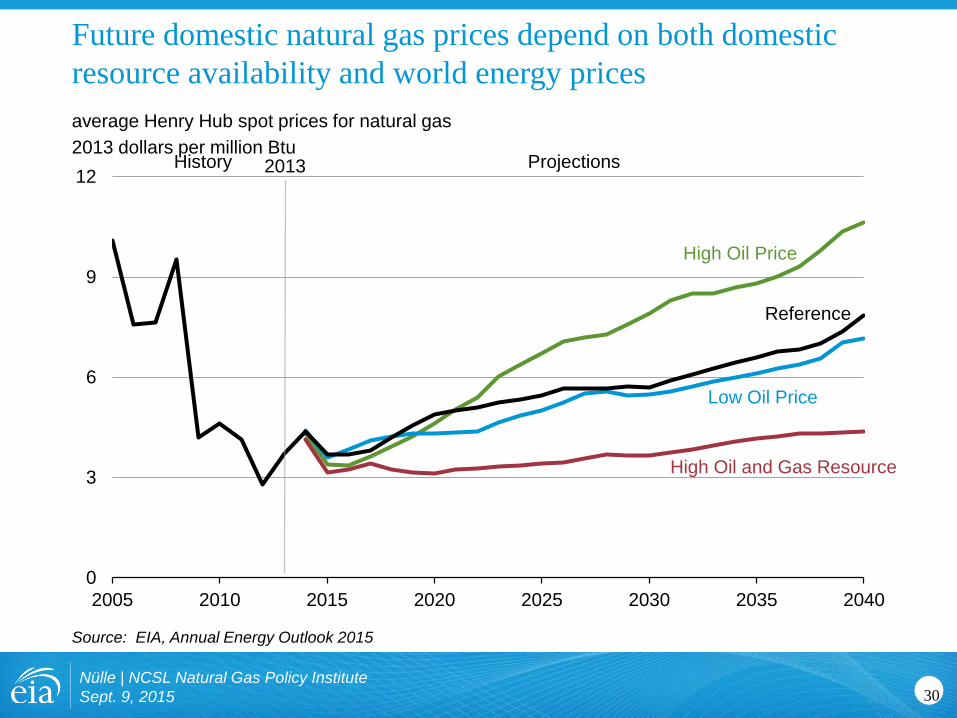

Future domestic natural gas prices depend on both domestic

resource availability and world energy prices

30

average Henry Hub spot prices for natural gas

2013 dollars per million Btu

Source: EIA, Annual Energy Outlook 2015

History Projections2013

High Oil Price

Reference

High Oil and Gas Resource

Low Oil Price

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015

0

5

10

15

20

25

30

35

40

45

2008 2009 2010 2011 2012 2013

Northeast-Plus natural gas supply and demand

balance

billion cubic feet per day

Source: Pipelines posting Information collected by Bentek Energy, LLC

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 31

Increased production in the Northeast-Plus resulted in reduced

net inflows to the region.

Natural gas

demand

Gross

production

Net inflows

Many natural gas pipeline projects are principally developing

because of production growth in the Mid-Atlantic and Northeast

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 32

Notes: Reversal projects are not on the map. ANR, Columbia Gulf Transmission, Iroquois Gas Pipeline, Rockies

Express Pipeline, Tennessee Gas Pipeline, Texas Eastern Transmission, and Transcontinental Gas Pipeline are

planning to reverse their flows

Source : EIA, Natural Gas Pipeline Projects, July 2014

0

2

4

6

8

10

12

14

16

18

2015 2016 2017 2018

Reversal New Pipeline

Lateral Expansion

Natural Pipeline Projects in the Mid-Atlantic and Northeastbillion cubic feet per day

Pipeline capacity is expanding to move more

Marcellus gas to the Northeast…

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 33

Source: U.S. Energy Information Administration

Note: Map is as of October 31, 2013 and only includes projects with at least 0.1 Bcf/d of additional takeaway capacity. Dashed lines indicate

existing pipelines on which expansions are occurring. Solid lines indicate newly built pipeline connections.

…and West...

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 34

Westbound flows on Rockies Express

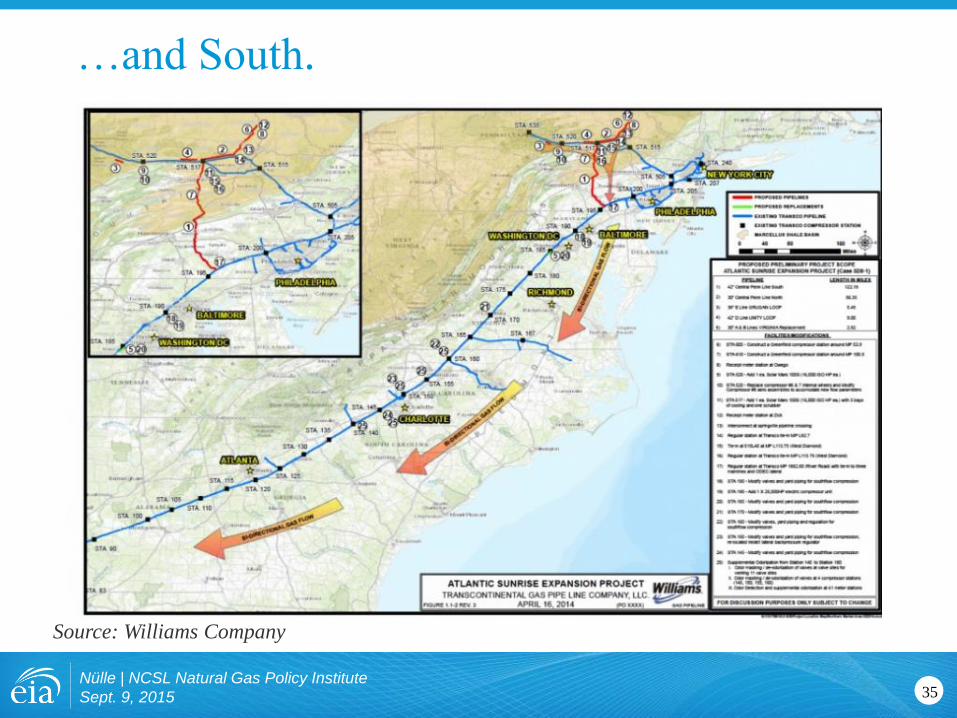

…and South.

Nülle | NCSL Natural Gas Policy Institute

Sept. 9, 2015 35

Source: Williams Company