u.s. market | industrial

TRANSCRIPT

Second Quarter 2021

COMMERCIAL REAL ESTATE

U.S. MARKET | INDUSTRIAL

U . S . M A R K E T | I N D U S T R I A L | Q 2 2 0 2 1

-50

0

50

100

150

200

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

0

100

200

300

400

500

600

700

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

U.S. TRENDLINES

5-Year Trend Current Quarter

VACANCY

U.S. HIGHLIGHTS

5.2%Lowest level since pandemic began

ECONOMY

• Following disappointing April and May figures, job growth exceeded expectations in June, though the unemployment rate was higher than anticipated.

• Industrial-using employment was virtually unchanged as supply chain challenges adversely affected manufacturing and construction.

• E-commerce’s share of overall retail sales cooled as brick-and-mortar stores reopened.

INDUSTRIAL MARKET

• Q2 marked the third consecutive quarter with over 100 MSF of positive net absorption, which hasn’t occurred since the first three quarters of 2018.

• Occupancy levels increased in all but one market in the past 12 months and 40 of 44 markets during Q2.

• The overall vacancy rate improved in consecutive quarters for the first time in three years.

• New inventory delivered to the market was at its lowest level in more than two years.

• The volume of product under construction is 30% higher YoY and double that of year-end 2015.

• After slowing during much of 2020, rent growth acceleration has returned to pre-pandemic levels.

LOOKING AHEAD

• Most brick & mortar retailers are investing more in e-commerce than on the in-store experience.

• Food/beverage will grow its share of e-commerce.

• As America’s ports continued to report record cargo volumes, the supply chain is still congested, and is anticipated to remain so well into 2022.

• Increased warehouse pricing, coupled with supply chain issues, could create opportunities for other transportation hubs in secondary logistics markets.

VACANCY VS ASKING RENT

0.0%

3.0%

6.0%

9.0%

12.0%

$0

$2

$4

$6

$8

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Average Asking NNN Rent (PSF) Vacancy

NET ABSORPTION (MILLION SF)

UNDER CONSTRUCTION (MILLION SF)3 Yr Qrtly Avg 456.3 MSF 5 Yr Qrtly Avg 413.8 MSF

3 Yr Qtrly Avg 81.3 MSF5 Yr Qtrly Avg 93.3 MSF

NET ABSORPTION 102.2 MSFDemand continued to accelerate

ASKING RENT$6.96 PSF38th consecutive quarterly increase

UNDER CONSTRUCTION

573.7 MSFDevelopers ramp up to record levels

YTD

UNEMPLOYMENT RATE

5.9%Job gains in nearly every sector

RETAIL SALES GROWTH

-0.3%Consumers returned to brick & mortar retail

U.S. HISTORICAL

O V E R V I E W

YTD

U . S . M A R K E T | I N D U S T R I A L | Q 2 2 0 2 1

0

5

10

15

20

25

30

35

40

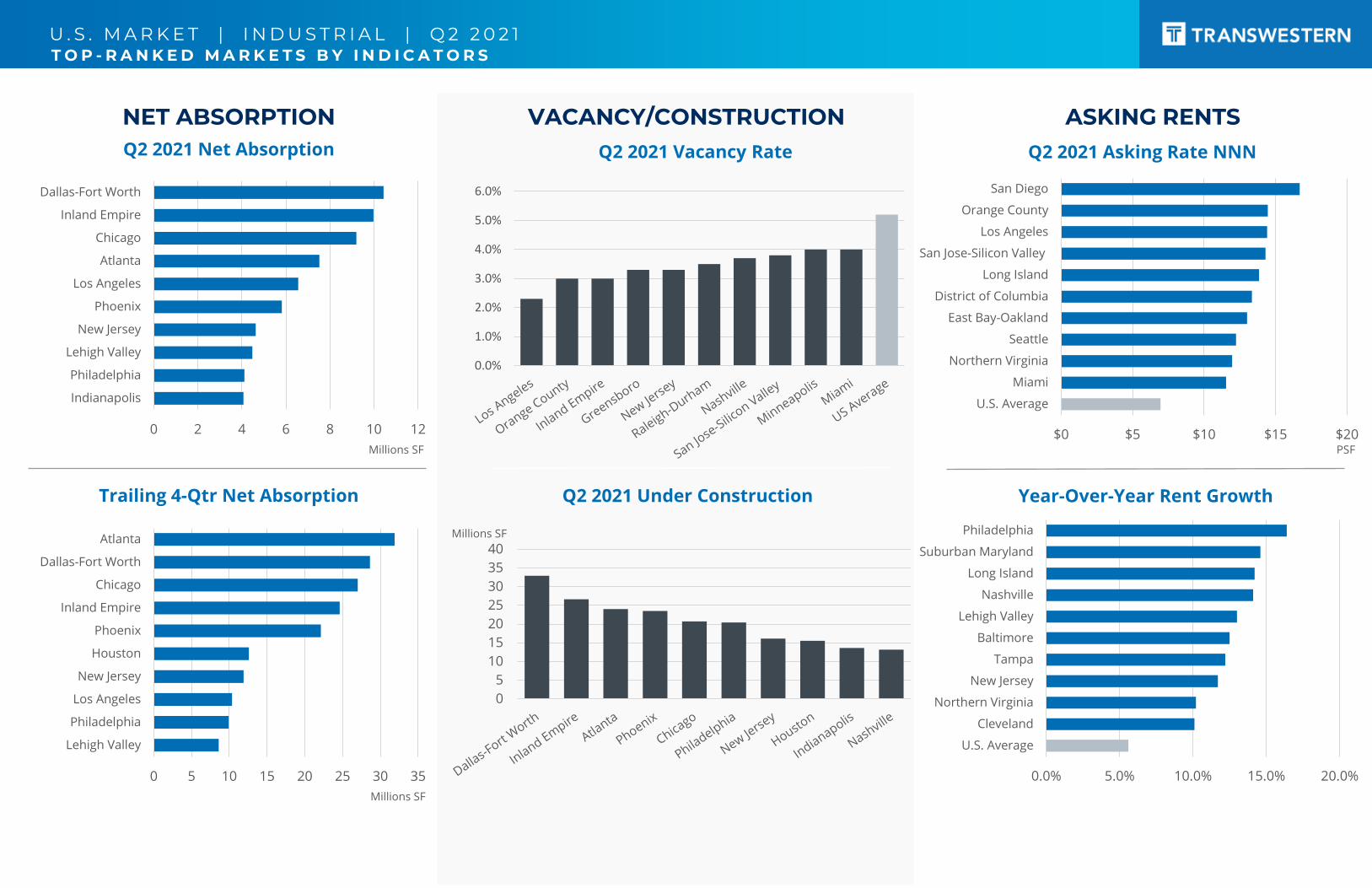

NET ABSORPTIONQ2 2021 Net Absorption

VACANCY/CONSTRUCTION ASKING RENTS

Trailing 4-Qtr Net Absorption Q2 2021 Under Construction

Q2 2021 Vacancy Rate

Year-Over-Year Rent Growth

Q2 2021 Asking Rate NNN

0 2 4 6 8 10 12

Indianapolis

Philadelphia

Lehigh Valley

New Jersey

Phoenix

Los Angeles

Atlanta

Chicago

Inland Empire

Dallas-Fort Worth

0 5 10 15 20 25 30 35

Lehigh Valley

Philadelphia

Los Angeles

New Jersey

Houston

Phoenix

Inland Empire

Chicago

Dallas-Fort Worth

Atlanta

$0 $5 $10 $15 $20

U.S. Average

Miami

Northern Virginia

Seattle

East Bay-Oakland

District of Columbia

Long Island

San Jose-Silicon Valley

Los Angeles

Orange County

San Diego

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0.0% 5.0% 10.0% 15.0% 20.0%

U.S. Average

Cleveland

Northern Virginia

New Jersey

Tampa

Baltimore

Lehigh Valley

Nashville

Long Island

Suburban Maryland

Philadelphia

Millions SF

Millions SF PSF

Millions SF

T O P - R A N K E D M A R K E T S B Y I N D I C A T O R S

U . S . M A R K E T | I N D U S T R I A L | Q 2 2 0 2 1

NET ABSORPTION

MARKET EXPANSION: 3 YEAR NET ABSORPTION % STOCK

K E Y P E R F O R M A N C E I N D I C A T O R S

• Positive annual and quarterly net absorption was reported in most markets as industrial space needs continued to grow.

• Further, net absorption accelerated in Q2 for over 60% of tracked markets. This subset experienced higher net absorption in the past quarter than their quarterly average over the past 12 months.

• Here we consider 3-year net absorption as a percent of stock. A higher percentage indicates that a market is more expansionary.

• Markets experiencing the most growth include Savannah, Lehigh Valley, Las Vegas, Inland Empire, Charleston, and Phoenix.

-5%

0%

5%

10%

15%

20%

25%

30%

Sava

nn

ah

Leh

igh

Val

ley

Las

Ve

gas

Inla

nd

Em

pir

e

Ch

arle

sto

n

Ph

oen

ix

San

An

ton

io

No

rth

ern

Vir

gin

ia

Dal

las

/ Fo

rt W

ort

h

Atl

anta

Au

stin

Ind

ian

apo

lis

Ral

eigh

-Du

rham

Ho

ust

on

Nas

hvi

lle

Orl

and

o

Mia

mi

Tam

pa

Co

lum

bu

s

Bal

tim

ore

Ch

icag

o

Kan

sas

Cit

y

Jack

son

ville

Ch

arlo

tte

Ne

w J

ers

ey

St. L

ou

is

Den

ver

Ph

ilad

elp

hia

Gre

ensb

oro

San

Die

go

Cin

cin

nat

i

Seat

tle

Milw

auke

e

Bo

sto

n

Sub

urb

an M

aryl

and

San

Jo

se/S

ilico

n V

alle

y

Los

An

gele

s

Det

roit

Cle

vela

nd

Min

ne

apo

lis

East

Bay

/Oak

lan

d

Ora

nge

Co

un

ty

Dis

tric

t o

f C

olu

mb

ia

Lon

g Is

lan

d

T-3

6 N

et

Ab

sorp

tio

n P

erc

en

t St

ock

-5

0

5

10

15

20

25

30

35A

tlan

ta

Dal

las

/ Fo

rt W

ort

h

Ch

icag

o

Inla

nd

Em

pir

e

Ph

oen

ix

Ho

ust

on

Ne

w J

ers

ey

Los

An

gele

s

Ph

ilad

elp

hia

Leh

igh

Val

ley

Co

lum

bu

s

Las

Ve

gas

Ind

ian

apo

lis

Mia

mi

St. L

ou

is

Nas

hvi

lle

Orl

and

o

Ral

eigh

-Du

rham

Au

stin

No

rth

ern

Vir

gin

ia

Bal

tim

ore

Kan

sas

Cit

y

Cin

cin

nat

i

San

An

ton

io

Ch

arlo

tte

Sava

nn

ah

San

Die

go

Tam

pa

Gre

ensb

oro

Seat

tle

Milw

auke

e

Ora

nge

Co

un

ty

Ch

arle

sto

n

Jack

son

ville

Bo

sto

n

East

Bay

/Oak

lan

d

Cle

vela

nd

Det

roit

Min

ne

apo

lis

Den

ver

Sub

urb

an M

aryl

and

San

Jo

se/S

ilico

n V

alle

y

Dis

tric

t o

f C

olu

mb

ia

Lon

g Is

lan

d

Squ

are

Fe

et

(mill

ion

s)

T12 Month Net Absorption T3 Month Net Absorption Quarterly Avg T12 Month Net Absorption

U . S . M A R K E T | I N D U S T R I A L | Q 2 2 0 2 1

RENTAL RATES (NNN)

RENTAL RATE CHANGE

K E Y P E R F O R M A N C E I N D I C A T O R S

• Markets with the highest rental rates were located on the West coast and near Washington, D.C., and New York.

• Some Midwest markets with low rental rates saw relatively high rent growth over the past year, including Cleveland, Chicago, and Columbus.

• More than half of the tracked markets saw rental growth for the year surpass 5%, with all but three experiencing increases over the past 12 months.

• While a few of the markets with low or negative rental-rate changes may be reacting to recent strong supply (e.g., Raleigh-Durham, Savannah), others may be adjusting to low or negative net absorption (e.g., Washington, D.C., Minneapolis).

0

2

4

6

8

10

12

14

16

18Sa

n D

iego

Ora

nge

Co

un

ty

Los

An

gele

s

San

Jo

se/S

ilico

n V

alle

y

Lon

g Is

lan

d

Dis

tric

t o

f C

olu

mb

ia

East

Bay

/Oak

lan

d

Seat

tle

No

rth

ern

Vir

gin

ia

Mia

mi

Au

stin

Sub

urb

an M

aryl

and

Bo

sto

n

Ne

w J

ers

ey

Inla

nd

Em

pir

e

Las

Ve

gas

Den

ver

Ral

eigh

-Du

rham

Ph

oen

ix

Ph

ilad

elp

hia

Ho

ust

on

Orl

and

o

Bal

tim

ore

Nas

hvi

lle

Tam

pa

Leh

igh

Val

ley

Ch

icag

o

Det

roit

San

An

ton

io

Ch

arle

sto

n

Jack

son

ville

Dal

las

/ Fo

rt W

ort

h

Min

ne

apo

lis

Atl

anta

Ch

arlo

tte

Sava

nn

ah

St. L

ou

is

Kan

sas

Cit

y

Milw

auke

e

Cin

cin

nat

i

Co

lum

bu

s

Cle

vela

nd

Ind

ian

apo

lis

Gre

ensb

oro

Ave

rage

Re

nt

Pe

r Sq

uar

e F

oo

t ($

)

-10%

-5%

0%

5%

10%

15%

20%

Ph

ilad

elp

hia

Sub

urb

an M

aryl

and

Lon

g Is

lan

d

Nas

hvi

lle

Leh

igh

Val

ley

Bal

tim

ore

Tam

pa

Ne

w J

ers

ey

No

rth

ern

Vir

gin

ia

Cle

vela

nd

Mia

mi

Los

An

gele

s

Orl

and

o

Seat

tle

Ch

icag

o

Ora

nge

Co

un

ty

East

Bay

/Oak

lan

d

Bo

sto

n

Las

Ve

gas

Inla

nd

Em

pir

e

Atl

anta

Co

lum

bu

s

Dal

las

/ Fo

rt W

ort

h

Gre

ensb

oro

Den

ver

Ph

oen

ix

Ch

arle

sto

n

Cin

cin

nat

i

San

Jo

se/S

ilico

n V

alle

y

Ind

ian

apo

lis

St. L

ou

is

San

Die

go

Jack

son

ville

Det

roit

Ho

ust

on

Ch

arlo

tte

San

An

ton

io

Au

stin

Ral

eigh

-Du

rham

Milw

auke

e

Kan

sas

Cit

y

Min

ne

apo

lis

Sava

nn

ah

Dis

tric

t o

f C

olu

mb

ia

Ye

ar O

ver

Ye

ar C

han

ge (

%)

Rental Rate T12 Percent Change Deliveries T12 as a Percent of Stock

U . S . M A R K E T | I N D U S T R I A L | Q 2 2 0 2 1

CONSTRUCTION PIPELINE

AVAILABILITY

K E Y P E R F O R M A N C E I N D I C A T O R S

• Many coastal markets where the busiest U.S. container ports are located reported the lowest availability as a percent of stock.

• Markets seeing the largest increases in availability include Savannah, Kansas City, and Seattle – all of which also have higher than average overall availability as a percent of stock as well. Those seeing the largest decreases include St. Louis, Austin, San Antonio, and Los Angeles.

• Under construction stock is indicative of future expansion.

• Savannah and Austin are growing relatively quickly with under construction stock exceeding 12%.

• Growth in the Sun Belt is evidenced here, as Savannah, Austin, Phoenix, San Antonio, Charleston, and Charlotte have seen the most acceleration of under construction SF as a percent of stock over the past year.

-3%

2%

7%

12%

17%

22%

Sava

nn

ah

Ho

ust

on

Ch

arlo

tte

Ph

oen

ix

Bal

tim

ore

Leh

igh

Val

ley

Den

ver

Kan

sas

Cit

y

Dal

las

/ Fo

rt W

ort

h

Ch

icag

o

Ch

arle

sto

n

Sub

urb

an M

aryl

and

Dis

tric

t o

f C

olu

mb

ia

Seat

tle

Tam

pa

Cle

vela

nd

Det

roit

St. L

ou

is

Atl

anta

Bo

sto

n

Au

stin

Ph

ilad

elp

hia

Orl

and

o

Nas

hvi

lle

Milw

auke

e

San

An

ton

io

East

Bay

/Oak

lan

d

Cin

cin

nat

i

Ind

ian

apo

lis

No

rth

ern

Vir

gin

ia

Co

lum

bu

s

San

Die

go

Min

ne

apo

lis

Ral

eigh

-Du

rham

Mia

mi

Las

Ve

gas

Inla

nd

Em

pir

e

Lon

g Is

lan

d

Jack

son

ville

Ne

w J

ers

ey

Gre

ensb

oro

San

Jo

se/S

ilico

n V

alle

y

Ora

nge

Co

un

ty

Los

An

gele

s

Availability % Stock T12 Change in Availability % Stock

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Sava

nn

ah

Au

stin

Ph

oen

ix

San

An

ton

io

Leh

igh

Val

ley

Nas

hvi

lle

Ch

arle

sto

n

Las

Ve

gas

Inla

nd

Em

pir

e

Ind

ian

apo

lis

Ch

arlo

tte

Ph

ilad

elp

hia

Kan

sas

Cit

y

Dal

las

/ Fo

rt W

ort

h

Seat

tle

Atl

anta

Ral

eigh

-Du

rham

Sub

urb

an M

aryl

and

San

Die

go

Den

ver

Tam

pa

Jack

son

ville

Ho

ust

on

Ne

w J

ers

ey

Co

lum

bu

s

Mia

mi

Bal

tim

ore

No

rth

ern

Vir

gin

ia

Cin

cin

nat

i

Orl

and

o

Ch

icag

o

Gre

ensb

oro

Det

roit

Min

ne

apo

lis

Bo

sto

n

Lon

g Is

lan

d

Milw

auke

e

Los

An

gele

s

St. L

ou

is

Cle

vela

nd

Ora

nge

Co

un

ty

Dis

tric

t o

f C

olu

mb

ia

East

Bay

/Oak

lan

d

San

Jo

se/S

ilico

n V

alle

y

Under Construction % Stock T12 Change in Under Construction % Stock

U . S . M A R K E T | I N D U S T R I A L | Q 2 2 0 2 1

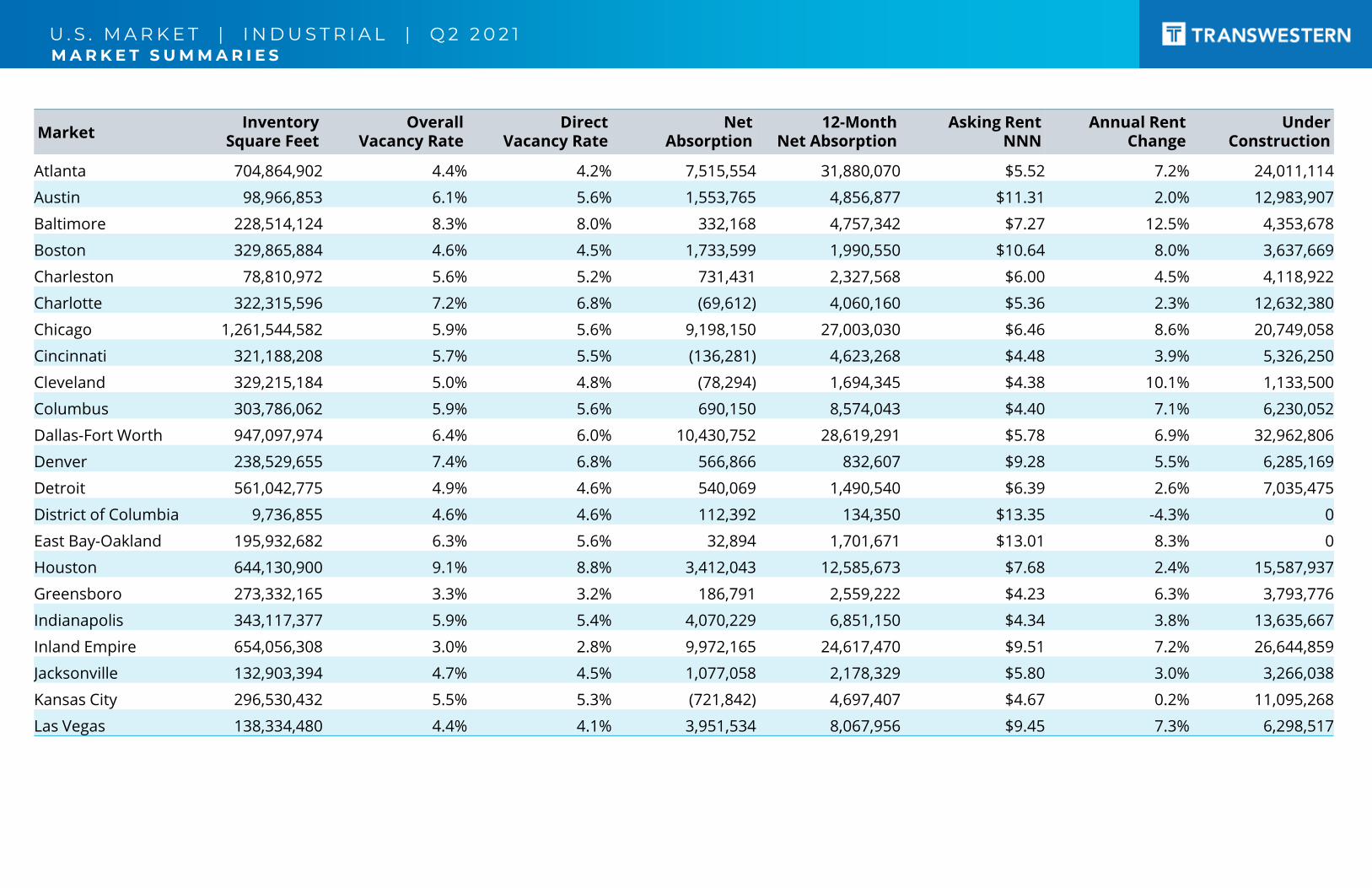

MarketInventory

Square FeetOverall

Vacancy Rate Direct

Vacancy RateNet

Absorption12-Month

Net AbsorptionAsking Rent

NNNAnnual Rent

ChangeUnder

Construction

Atlanta 704,864,902 4.4% 4.2% 7,515,554 31,880,070 $5.52 7.2% 24,011,114

Austin 98,966,853 6.1% 5.6% 1,553,765 4,856,877 $11.31 2.0% 12,983,907

Baltimore 228,514,124 8.3% 8.0% 332,168 4,757,342 $7.27 12.5% 4,353,678

Boston 329,865,884 4.6% 4.5% 1,733,599 1,990,550 $10.64 8.0% 3,637,669

Charleston 78,810,972 5.6% 5.2% 731,431 2,327,568 $6.00 4.5% 4,118,922

Charlotte 322,315,596 7.2% 6.8% (69,612) 4,060,160 $5.36 2.3% 12,632,380

Chicago 1,261,544,582 5.9% 5.6% 9,198,150 27,003,030 $6.46 8.6% 20,749,058

Cincinnati 321,188,208 5.7% 5.5% (136,281) 4,623,268 $4.48 3.9% 5,326,250

Cleveland 329,215,184 5.0% 4.8% (78,294) 1,694,345 $4.38 10.1% 1,133,500

Columbus 303,786,062 5.9% 5.6% 690,150 8,574,043 $4.40 7.1% 6,230,052

Dallas-Fort Worth 947,097,974 6.4% 6.0% 10,430,752 28,619,291 $5.78 6.9% 32,962,806

Denver 238,529,655 7.4% 6.8% 566,866 832,607 $9.28 5.5% 6,285,169

Detroit 561,042,775 4.9% 4.6% 540,069 1,490,540 $6.39 2.6% 7,035,475

District of Columbia 9,736,855 4.6% 4.6% 112,392 134,350 $13.35 -4.3% 0

East Bay-Oakland 195,932,682 6.3% 5.6% 32,894 1,701,671 $13.01 8.3% 0

Houston 644,130,900 9.1% 8.8% 3,412,043 12,585,673 $7.68 2.4% 15,587,937

Greensboro 273,332,165 3.3% 3.2% 186,791 2,559,222 $4.23 6.3% 3,793,776

Indianapolis 343,117,377 5.9% 5.4% 4,070,229 6,851,150 $4.34 3.8% 13,635,667

Inland Empire 654,056,308 3.0% 2.8% 9,972,165 24,617,470 $9.51 7.2% 26,644,859

Jacksonville 132,903,394 4.7% 4.5% 1,077,058 2,178,329 $5.80 3.0% 3,266,038

Kansas City 296,530,432 5.5% 5.3% (721,842) 4,697,407 $4.67 0.2% 11,095,268

Las Vegas 138,334,480 4.4% 4.1% 3,951,534 8,067,956 $9.45 7.3% 6,298,517

M A R K E T S U M M A R I E S

U . S . M A R K E T | I N D U S T R I A L | Q 2 2 0 2 1M A R K E T S U M M A R I E S

MarketInventory

Square FeetOverall

Vacancy Rate Direct

Vacancy RateNet

Absorption12-Month

Net AbsorptionAsking Rent

NNNAnnual Rent

ChangeUnder

Construction

Lehigh Valley 141,039,681 5.1% 4.7% 4,475,189 8,602,478 $6.86 13.0% 8,833,651

Long Island 154,201,542 4.4% 4.1% 625,423 (236,613) $13.85 14.2% 1,118,412

Los Angeles 846,394,501 2.3% 2.1% 6,558,529 10,362,847 $14.41 9.7% 3,594,580

Miami 232,798,777 4.0% 3.8% 1,805,644 6,657,635 $11.54 9.7% 4,471,180

Milwaukee 242,792,344 4.7% 4.6% 767,629 2,432,352 $4.55 1.8% 1,608,295

Minneapolis 378,152,004 4.0% 3.7% 26,992 1,488,161 $5.62 -1.4% 4,358,745

Nashville 223,874,629 3.7% 3.1% 856,549 6,030,053 $6.89 14.1% 13,196,262

New Jersey 744,299,018 3.3% 3.0% 4,626,136 11,896,114 $9.85 11.7% 16,137,552

Northern Virginia 111,607,278 5.0% 4.7% 1,095,907 4,829,260 $11.97 10.2% 1,952,465

Orange County 273,354,015 3.0% 2.5% 1,106,426 2,351,518 $14.46 8.6% 391,203

Orlando 167,097,956 5.0% 4.7% 1,146,767 5,852,631 $7.66 9.4% 2,753,264

Philadelphia 531,340,472 4.6% 4.5% 4,111,807 9,911,255 $7.88 16.4% 20,467,343

Phoenix 353,036,428 6.1% 5.9% 5,814,504 22,114,343 $7.93 4.9% 23,532,863

Raleigh-Durham 124,281,930 3.5% 3.3% 1,675,298 5,301,116 $8.36 1.8% 4,065,411

San Antonio 116,579,281 6.1% 5.9% 524,216 4,376,453 $6.06 2.0% 7,448,358

San Diego 176,827,382 5.0% 4.6% 1,458,244 3,380,452 $16.69 3.7% 5,358,188

San Jose-Silicon Valley 82,957,183 3.8% 3.4% 172,621 216,366 $14.30 3.9% 0

Savannah 74,413,721 8.8% 7.9% 1,171,403 3,938,167 $4.88 -3.4% 10,780,508

Seattle 308,560,910 5.6% 5.1% 284,327 2,556,103 $12.24 8.7% 10,607,148

St. Louis 298,674,988 4.4% 4.0% 2,267,965 6,399,263 $4.68 3.8% 1,052,300

Suburban Maryland 105,255,098 6.5% 6.2% 98,121 420,420 $11.00 14.6% 3,333,523

Tampa 179,240,706 4.5% 4.3% 1,440,745 3,317,423 $6.89 12.2% 4,471,984

U . S . M A R K E T | I N D U S T R I A L | Q 2 2 0 2 1

RESEARCH METHODOLOGYThe information in this report is a compilation of single and multi-

tenant industrial and flex properties located in select U.S.

metropolitan areas. Government-owned buildings are excluded

from analysis. All rents are reported as triple net.

Copyright © 2021 Transwestern. All rights reserved. No part of this work may be reproduced or distributed to third parties without written permission of the copyright owner. The information contained in this report was gathered by Transwestern from CoStar and other primary and secondary sources believed to be reliable. Transwestern, however, makes no representation concerning the accuracy or completeness of such information and expressly disclaims any responsibility for any inaccuracy contained herein.

TRANSWESTERN LOCATIONS

ABOUT TRANSWESTERNThe privately held Transwestern companies have been delivering a higher level of personalized service and innovative real estate solutions since 1978. Through an integrated, customized approach that begins with good ideas, the firm drives value for clients across commercial real estate services, development, and investment management. Operating from 33 U.S. offices, Transwestern extends its platform capabilities globally through strategic alliance partners whose unique geographic,cultural, and business expertise fuels creative solutions. Learn more at transwestern.com and @Transwestern.

FOR MORE INFORMATION

Matthew DollyResearch Director | Research [email protected] 947 9244

Elizabeth NortonSr. Managing Director | Research [email protected] 775 7026

Laura HaltomManager | Data [email protected] 889 4087