us lodging industry overview - hotelnewsnow.com€¢ segmentation review ... hamburg paris lux &...

TRANSCRIPT

1

US Lodging Industry Overview

Jan D. Freitag

Senior Vice President

2

www.hotelnewsnow.com Click on “Hotel Data Presentations”

3

Agenda

• Global Review

• Total US Review

• Chain Scale Review

• Segmentation Review – Group & Transient

• 2012 / 2013 Forecast

4

2011: The World Recovered

Markets with Positive REVPAR % Change

Americas: 194 of 212

Europe: 84 of 98 AsiaPac: 38 of 47

Middle East / Africa: 19 of 33

*RevPAR in local currency Source: STR Global

5

Major Global Markets Did Well

*2011 % Change, ADR & RevPAR in local currency Source: STR Global

Market OCC ADR RevPAR

Beijing 8.2 5.8 14.6 Berlin 0.9 -2.0 -1.1 Dubai 7.0 3.4 10.7

Hong Kong 2.4 23.1 26.0 London -0.1 8.5 8.4

Mexico City 7.9 2.9 10.9 Moscow 2.7 5.4 8.3

Sao Paulo 2.9 17.7 21.1 Sydney -0.1 5.2 5.1 Tokyo -8.5 -6.7 -14.7

Toronto -0.6 0.6 0.0

6

-12

-8

-4

0

4

8

2004 2009 2014

GDP Demand

Expect Slowing Eurozone GDP / Demand % Change

*Eurozone Demand & GDP % Change, Quarterly 2004 – 2014F GDP Source: Oxford Economics

7

STR Global Forecast – Selected Cities 2012 RevPAR forecast % chg, local currency

-5% to -10% -5% to 0% 0% to +5%

Athens

Amsterdam Berlin

Brussels Frankfurt

Budapest London

Dublin Moscow

Dusseldorf Munich

Hamburg Paris Lux & Up Up

Madrid Prague

Warsaw Rome

Zurich Stockholm

Vienna

8

Total US Review

9

Supply / Demand Imbalance Drove 2011 Results

% Change

• Room Supply* 1.8 bn 0.6%

• Room Demand* 1.06 bn 5.0%

• Occupancy 60.1% 4.4%

• A.D.R. $102 3.7%

• RevPAR $61 8.2%

• Room Revenue* $108 bn 8.8%

Full Year 2011 Total US Results * All Time High

10

January 2012:

Highest January Demand - EVER

(73.4 Million Rooms Sold)

11

ADR Discounting at Twice The Speed of ADR Increases

95

100

105

110

2008 2009 2010 2011

*Total US, ADR $, 12 MMA 2007 - 2011

Apr ‘10 $97

Sept ‘08 $108

Dec ‘11 $102

+4.6%

-10%

19 Months

19 Months

12

3.1

2.6

3.9

2.9

4.1

3.7

4.0

3.5

4.1 4.0

4.4

3.5

3.9

3.1

3.8

2.9

4.6

* Total US, ADR $ % Change, by Month, 1/11 – 1/12, by Week 2/4 – 2/25

... That Being Said, ADRs Are Growing ...

2/4 2/11 2/18 2/25 1/12 1/11 4/11 7/11 9/11 Weekly data

13

Chain Scale Review

14

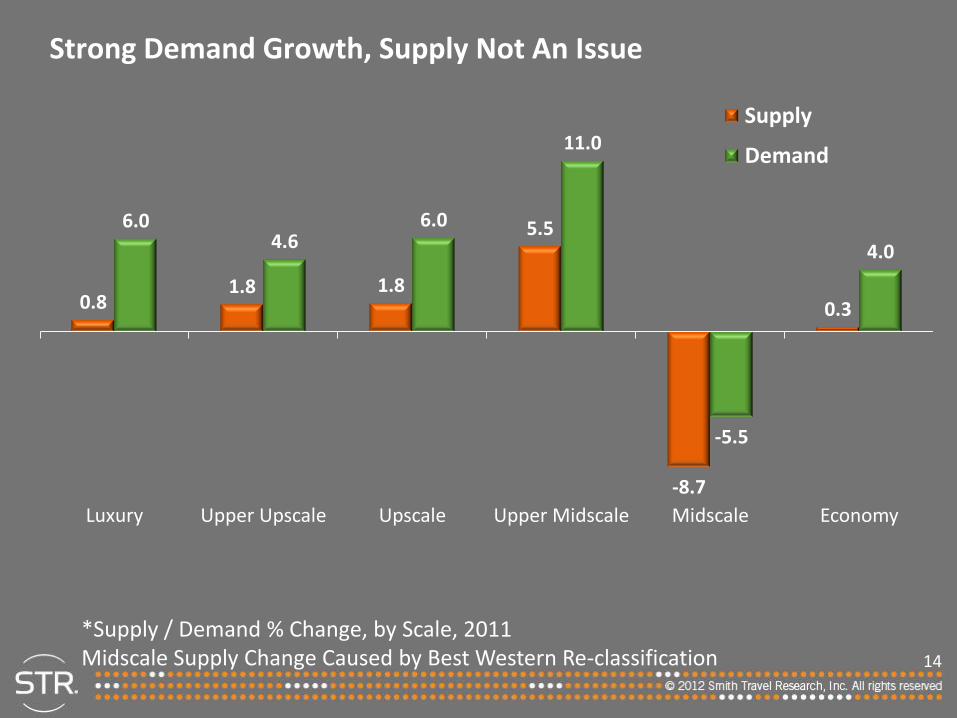

Strong Demand Growth, Supply Not An Issue

0.8 1.8 1.8

5.5

-8.7

0.3

6.0 4.6

6.0

11.0

-5.5

4.0

Luxury Upper Upscale Upscale Upper Midscale Midscale Economy

Supply

Demand

*Supply / Demand % Change, by Scale, 2011 Midscale Supply Change Caused by Best Western Re-classification

15

Early Recovery: OCC % > ADR %

5.2

2.8

4.1

5.2

3.5 3.7

5.7

3.6 3.8 3.3

-0.5

2.2

Luxury Upper Upscale Upscale Upper Midscale Midscale Economy

Occupancy

ADR

*OCC / ADR % Change, by Scale, 2011

16

Upper End Sells 7 out of 10 Rooms Every Night

71.7

70.5 69.6

65.3

58.4 57.0

69.9 69.3 69.5

61.5

53.5 53.5

Luxury Upper Upscale Upscale Upper Midscale Midscale Economy

2007 2011

*Absolute OCC %, by Scale, 2007 & 2011

17

ADR Growth Is Strong – But Not Strong Enough (...yet)

$286

$159

$121

$94 $77

$54

$257

$148

$112 $94

$73

$50

Luxury Upper Upscale Upscale Upper Midscale Midscale Economy

2007 2011

*Absolute ADR $, by Scale, 2007 / 2011

18

Segmentation Review

19

Transient Demand Breaks Records, But....

10

12.5

15

17.5

20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 2010 2011

*Transient Demand in Millions of Rooms; 2007, 2010, 2011 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

Mill

ion

s

1/12

20

… Transient ADR Still Lags 2007 Results

$140

$150

$160

$170

$180

$190

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 2010 2011

*Transient ADR $, 2007, 2010, 2011 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

1/12

21

5.0

4.0

5.9

5.1

5.6

4.8 4.9

3.5

4.4 4.1

4.4

3.2

3.8

1.4

3.3

2.2

4.5

*Transient ADR % by Month, 1/11 – 1/12, by Week 2/4 – 2/25 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

We Expect Transient ADR Growth To Continue

2/4 2/11 2/18 2/25 1/12 1/11 4/11 7/11 9/11 Weekly data

22

Group Demand Has Not Changed Over Time, But…

4

6

8

10

12

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Millio

ns

2007 2010 2011

*Group Demand in Millions of Rooms, 2007, 2010, 2011 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

1/12

23

… Group ADR Does Not Increase (& Could Depress Future Absolute ADRs)

$130

$140

$150

$160

$170

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008 2010 2011

*Group ADR $, 2008, 2010, 2011 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

1/12

24

2.3 1.9

2.2

0.1

3.4

1.9 1.9 1.6

2.8 2.4

3.3

-0.7

2.8

-0.1

5.0

0.7

2.7

*Group ADR % by Month, 1/11 – 1/12, by Week 2/4 – 2/25 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

Group ADR Growth Is Tepid So Far

2/4 2/11 2/18 2/25 1/12 1/11 4/11 7/11 9/11 Weekly data

25

2012 / 2013 Forecast

26

Rooms Pipeline Still Not An Issue in 2012

Phase Dec 2011 Dec 2010 Dec 2007

In Construction 54 52 211

“Planned Pipeline” 254 265 204

Active Pipeline 308 317 415

*Total US Pipeline, in ‘000s of rooms, by Phase by Year Planned Pipeline includes projects in Final Planning and Planning phases Source: STR / McGraw-Hill Construction Dodge

27

Total United States Forecast 2012 / 2013 Key Performance Indicator % Change

2012 Forecast

2013 Forecast

Supply 0.8% 1.4%

Demand 1.3% 2.0%

Occupancy 0.5% 0.5%

ADR 3.8% 4.4%

RevPAR 4.3% 4.9%

28

Publicly Traded Company 2012 RevPAR Guidance

Company Name Guidance 2012

HOST Hotels & Resorts

Choice Hotels

DiamondRock Hospitality +4-6%

FeCor Lodging Trust

Sunstone Hotel Investors

Marriott International

LaSalle Hotel Properties +5-7%

Starwood Hotels

Wyndham Worldwide +5-8%

Chatham Lodging Trust

Hersha Hospitality +6-8%

Strategic Hotels

Chesapeake Lodging Trust +6.5–8.5%

Pebblebrook Hotel Trust +8-10%

29

Total United States Chain Scale Key Performance Indicator Outlook 2012F by Chain Scale

Chain Scale Occupancy

(% chg) ADR

(% chg) RevPAR (%chg)

Luxury 2.7% 4.7% 7.4%

Upper Upscale 0.1% 3.5% 3.6%

Upscale 2.0% 4.5% 6.6%

Upper Midscale -0.3% 3.7% 3.4%

Midscale 1.0% 0.8% 1.8%

Economy 0.7% 2.4% 3.1%

Independent -0.3% 3.4% 3.1%

Total United States 0.5% 3.8% 4.3%

30