unlocking value in run-off - pwc uk blogsunlocking value in run-off 1 the global economy has...

TRANSCRIPT

A Survey of Discontinued Insurance Business in Europe

Unlocking value in run-off

Third Edition March 2009

Contents

Introduction by Dan Schwarzmann 01

The key findings from the third Survey of Discontinued Insurance Business in Europe 02

View from the Association of Run-Off Companies 04

The year that was... 2008 A brief summary of the key restructuring

activities across Europe 05

Market size: Run-off liabilities in Europe 06Market challenges: What are the major

challenges facing Continental European insurers with run-off business?

07

Management: How do organisations define and manage run-off business? 09

Time and money: How long will it take run-off business to reach natural expiry and what future claims

uncertainties are faced?12

Exit route options: What are the exit strategies for European run-off business? 14

Drivers for change: What factors will promote future insurance restructurings in Europe? 16

The developing regulatory landscape: What impact will Solvency II and the Reinsurance Directive have

on European run-off business?17

What would you like to change? 20

Glossary 21

Appendix 1: Frequently asked questions 22

The PricewaterhouseCoopers team Unlocking value in run-off 24

1Unlocking value in run-off

The global economy has experienced unprecedented financial turmoil in the past 12 months. As an administrator of the Lehman Brothers European companies I am seeing first hand that the financial sector is as vulnerable as any other to these testing times.

As we report the results of this year’s Survey, the “credit crunch” continues unabated and the European economy will continue to face significant challenges as the recession appears set to continue throughout 2009. The global insurance sector has already witnessed some significant turbulence and, whilst we have yet to witness any major exits or failures in the European insurance industry, the market is already being challenged through decreasing investment returns, restricted credit lines and increases in fraudulent claim activity.

Key themes arising out of this year’s Survey include concerns surrounding the current financial crisis and its impact on the insurance industry along with a growing acknowledgment of the need to have a strategic plan for dealing with discontinued business. Achieving an appropriate balance of management time to deal effectively with both emerging and legacy issues is a focus for insurers across Europe. Indeed, globally, 80% of CEOs1 agreed that managing complexity is a high priority for their organisations in the battle to drive value and create competitive advantage.

In light of the current economic climate, there is also an increased requirement for European based insurance and

reinsurance groups to scrutinise their existing structures and consider ways to optimise capital, regulatory, operational and / or tax efficiencies while preserving reputation. With the deadline for Solvency II approaching and Enterprise Risk Management (ERM) high on Board agendas, European insurance organisations also now need to take affirmative action. This will require clear articulation of business objectives, measurements of the risks of that business, (both on-going and discontinued), and closer attention to the trade-offs between risk and reward.

I would like to extend an immense thank you to the 519 individuals who kindly participated in our Survey and I hope that you find this third edition of the Survey informative. It is clear that 2008 was an exciting year for the run-off industry and we take a look at some of the key events and transactions on page 5, as well as looking forward to 2009.

I am also delighted to tell you that Achim Bauer has joined PricewaterhouseCoopers as a partner. Achim has held senior roles in a number of major European businesses including Deutsche Bank, Swiss Re, Allianz / Dresdner Kleinwort and will be splitting his time between Germany and London focussing on insurance restructuring initiatives across Europe. I am pleased that he has been able to take the time to share some of his thoughts on the European insurance landscape in this document.

We have included in the Appendix some answers to questions that we are most frequently asked by our clients, but please do contact any member of our 200-strong team if you would like to discuss further any of the matters highlighted in the Survey.

We are privileged to be able to work with our clients to formulate innovative solutions which address the key issues that they face and we look forward to bringing further new techniques to the Continental European and UK run-off markets in 2009.

Introduction

We anticipate that Solvency II will result in more portfolios of business being discontinued as companies focus on core business activities and increasingly explore methods to bring early finality to run-off in order to recycle capital currently tied up in discontinued operations. Our Survey indicated that our respondents feel the same, with 74% considering that proactive management of their organisation’s run-off business is a priority for senior management.

Welcome to our third edition of the Survey of Discontinued Insurance Business in Europe. Once again the Survey has met with an excellent response and I am pleased to be able to report the results and take this opportunity to share with you PricewaterhouseCoopers’ views on European run-off.

Dan SchwarzmannPartner, PricewaterhouseCoopers

1 Source: 11th annual PricewaterhouseCoopers Global CEO Survey, in which over 1100 CEOs took part

2 PricewaterhouseCoopers

The key findings from the third Survey of Discontinued Insurance Business in Europe

Challenges facing the European insurance industry

Nearly 60% of respondents regarded the financial crisis as one of the key issues facing the insurance industry in Continental Europe

Tied-up capital was ranked the highest challenge facing Continental European insurers with run-off business

Defining and managing run-off

Over 70% of respondents consider that pro-active management of their organisation’s run-off business is a priority for senior management

85% of respondents now define run-off as “lines of business which are no longer written”

86% of organisations have a strategy for dealing with their run-off

Nearly 70% of respondents manage their run-off as a separate business unit or run-off entity

With the financial crisis putting organisations under greater scrutiny from stakeholders and rating agencies, organisations need to consider more deeply the true risk and cost of run-off, how value can be extracted and whether they have the expertise to deal with legacy issues

Across Continental Europe an increasing number of respondents view run-off as a standalone issue. Those organisations that continue to manage run-off alongside live business risk losing value and competitive advantage

These indicators demonstrate that the spotlight on run-off in the European insurance sector is increasing. Compared with last year’s Survey, we are now seeing a greater convergence of views in terms of how run-off is seen and managed across Europe.

3Unlocking value in run-off

Restructuring

Exit strategies

Over 50% of Survey respondents indicated that their run-off would take longer than 10 years to reach natural expiry

Nearly 80% of respondents believe that efficient capital management will be the key driver for restructuring activities across Continental Europe over the next five years

Around 60% of respondents indicated that a strategic commutation programme would be the most frequently used exit mechanism over 2009

Long-tail claims, mostly emanating from the US, were viewed as the biggest challenge to gaining finality for run-off business

An overwhelming 98% of respondents expect an increase in insurance business transfers in Continental Europe over the next five years following the implementation of the Reinsurance Directive

Organisations will face legacy claims issues for many years to come and, given today’s economic climate, now may be the time to consider effective exit strategies so that resources and management attention can be appropriately balanced between legacy and emerging issues. Commutations were seen as the most popular exit strategy evidenced by the buoyant commutation activity in 2008. While this finality activity is impressive, individual commutations continue to be time consuming and only achieve finality on a piecemeal basis

We are increasingly seeing Boards contemplate new restructuring techniques to capture benefits from capital, regulatory, operational and tax efficiencies

an increased focus on run-off business•an increase in the number of organisations •that manage run-off as a separate unit in accordance with a strategic plan

an increased focus on operational •efficiencies and the extraction of capitalan expectation of increased insurance •business transfer activity

Our Survey results show the following key trends:

4 PricewaterhouseCoopers

In contrast to London, which was forced to address run-off in the early 1990’s as a result of a number of insolvencies and the restructuring of Lloyd’s historic liabilities, Continental Europe has historically continued to treat legacy books as a normal part of the business process. However, this approach appears to be changing.

As the Survey shows, with the nearing deadline for Solvency II and the accompanying realisation of the amount of capital tied up in discontinued business, an increasing number of respondents now consider pro-active management of legacy liabilities to be a priority for senior management. Add to this the impact of the current economic turbulence, which has driven greater counterparty credit awareness as well as creating concerns about such factors as a surge in Errors & Omissions and Directors & Officers claims, and it is far from surprising that Continental European companies are becoming increasingly attuned to specific issues arising from their legacy liabilities.

Where those in Continental Europe have a significant advantage over their London Market counterparts is the fact that there are already well established techniques for dealing with legacy liabilities on which they can draw. What is more, the tool box that has existed in the UK for some years is becoming ever more accessible – not only have mechanisms such as the business transfer process now become a part of European law, but also recent Court rulings have again clarified that the jurisdiction of solvent schemes of arrangement extends far further than many initially thought.

Continental European initiatives which reflect such developments include the recently sanctioned GLOBALE Re solvent scheme, on which PricewaterhouseCoopers advised. This scheme broke new ground by being the first solvent scheme to focus on business that emanated from the UK, but was written in Germany, and

which was proposed in respect of a standalone German company. Given the significant volume of business ceded to German reinsurers by the London market in recent decades, this development could be the start of an increased trend in such proposals.

Similarly, the Deutsche Rück transfer in late 2007 of all of its third party run-off business to its UK subsidiary, Deutsche Rück UK, the first cross-border reinsurance business transfer under the then newly implemented European Reinsurance Directive legislation, made it clear that the Continental European market has a growing appetite for the kind of legacy initiatives which have become increasingly commonplace in London. It is perhaps, therefore, not that surprising that virtually all respondents to this Survey expect an increase in insurance business transfers in the next five years.

The real question now is how Continental Europe will adapt and develop current techniques to meet local needs and objectives. The evolving Continental European market will be very much one that builds on UK techniques developed to date, rather than one that ‘transplants’ wholesale the London Market experience. Indeed, feedback from ARC’s various Continental European (re)insurer members indicates that the learning aspects of our activities, such as our Academy programmes and Forums, are a particular area of value.

The current uncertainty may also drive renewed focus on commutation programmes. Granted, declining interest rates have greatly diminished the historic benefit of extinguishing a liability at a

present value discount, but this may well be more than offset by increased uncertainty regarding the credit worthiness of reinsurers. The desire to turn a balance sheet recovery asset into hard cash is likely to be an increasingly strong imperative. Fluctuations in exchange rates may also provide additional benefit to a commutation, although in this instance what is good for one side of the equation is likely to be detrimental to the other.

So where next for the European legacy community? Clearly Solvency II is a common opportunity and concern for all. It is also an issue where, unless the legacy community addresses it quickly, there is a real danger that we could end up wrong-footed or disadvantaged.

Over the years ARC has undertaken a number of initiatives in response to regulatory change. Establishing exactly how Solvency II impacts run-off books and ensuring carriers with legacy liabilities are represented at the right level to have an impact, is clearly the next potential priority for ARC. But we should not be working on this purely from a UK perspective.

In this context, it is interesting to note that a key theme identified by the Survey is the possible creation of a market voice representing Continental Europeans. ARC would welcome further input from across the Channel – whether as members or simply regarding a pan-European Solvency II initiative – and would gladly assist in the creation of a Continental European equivalent. We are, after all, one European community.

View from the Association of Run-Off Companies

As a practitioner in the London legacy market for nearly twenty years, the PricewaterhouseCoopers’ Survey of the European market, now in its third year, always provides interesting reading.

Paul Corver Chairman, Association of Run-Off Companies Limited (ARC)

5Unlocking value in run-off

The year that was... 2008 A brief summary of the key restructuring activities across Europe

2008 saw restructuring activity taking place both in the discontinued and live insurance markets. Activities ranged from redomiciling corporate headquarters to implementing closure techniques for long-standing run-off portfolios. We consider below some of the most notable developments and consequences of these activities.

In the previous Survey we reported that the Reinsurance Directive had been implemented in certain territories, namely, the UK, Germany, Ireland, Luxembourg and Spain, but that France, Netherlands and Sweden had yet to complete implementation of this Directive into law.

These countries have now implemented the Directive which, together with the previous Third Non-Life Directive, creates a “single passport” regime allowing insurers and reinsurers to conduct business throughout the EEA without requiring the establishment of a subsidiary in individual territories. In addition, where implemented, these Directives create a uniform framework for insurance and reinsurance companies to transfer their insurance business across EEA countries. Examples of discontinued transfer activity in the last year include Codan Forsikring A/S and Cirrus Reinsurance Company Limited. Each transferred certain portfolios of their insurance business to UK companies as part of a defined run-off strategy. Survey respondents expect transfer activity to increase significantly in Continental Europe over the next five years.

The past 12 months also saw developments within the global insurance market that are impacting Europe. For example, in July 2008 ACE Limited announced that it had completed the re-domestication of its headquarters from the Cayman Islands to Switzerland and had established its holding company in Zurich. Prior to that PartnerRe Limited had announced that its subsidiary in Dublin would be its principal European

reinsurance carrier. 2009 is likely to see further cross-border restructuring as companies explore optimal operating structures. This may result in additional insurance and reinsurance businesses being redomiciled and headquartered within European territories.

The PricewaterhouseCoopers UK Regulatory team is responding to significant activity as insurers and reinsurers prepare for Solvency II’s implementation. This has been accelerated following the FSA’s direct engagement with insurers in September 2008 in order to encourage and ascertain preparation plans for Solvency II. European Regulators have not as yet taken such an approach and our Survey results indicate that organisations across Continental Europe need to consider increasing their engagement in Solvency II.

The increasingly harmonised regulatory framework within the EEA will continue to provide European insurance companies with greater access to restructuring tools. In addition to insurance business transfers and solvent schemes of arrangement (solvent schemes), companies have the option of using the Cross-Border Mergers Directive. Each Member State was required to implement this Directive by mid December 2007 to enable companies to undertake cross-border mergers within the EEA more easily, in the main, by removing legislative obstacles that may have been faced in the past due to different national laws.

Sale activity has also continued to play a part in the European run-off sector in the past year. A recent example is the sale of German marine insurer and reinsurer Deutsche Versicherungs Rück AG (DARAG) to hedge fund Auger Capital. 2008 also saw the sale of Travelers’ UK run-off business to Enstar. This was a transaction on which PricewaterhouseCoopers advised and was seen by many in the market as the largest deal of the year. Whilst we expect to see some further run-off disposals in 2009, with Continental European run-off being an interesting proposition for acquirers, the level of activity will probably be dampened. This is as a result of the effect of the current financial crisis creating a decline in the

competition for deals as capital becomes constrained.

2008 also saw continued development in the area of solvent schemes, a UK Court-driven procedure which is widely recognised in the UK, and increasingly in Europe, as being a means to unlock value from run-off operations. Solvent schemes have now been used 14 times on a pool basis for Continental European discontinued insurance portfolios. Such schemes have been used widely to extinguish run-off insurance business including complex and long-tail liabilities such as asbestos and climate-related claims. A key development in this area in the past year was the sanction of the Globale Rückversicherungs-AG (GLOBALE Re) solvent scheme in December 2008. This was the first solvent scheme to be proposed in respect of a stand alone German domiciled company using “sufficient connection” to the UK and was also a transaction on which PricewaterhouseCoopers advised.

In contrast to managed exits, we also saw new run-off portfolios emerge, including Bluewater Insurance ASA which ceased all underwriting of its marine and energy risks from 1 October 2008. Lines of business naturally become categorised as legacy or specific lines are withdrawn to reflect changing strategic priorities.

Overall, there has been a great deal of activity in 2008 which has continued to change the face of European run-off. It is already clear from discussions with our clients and from the Survey results that the trend of further restructuring activity is set to continue in 2009, when we should expect some new angles on existing restructuring and exit techniques.

As 2009 progresses, we expect to see companies adopting various techniques in their restructuring activities such as an insurance business transfer followed by a solvent scheme or the use of an insurance business transfer and Cross- Border Merger in parallel.

6 PricewaterhouseCoopers

22%

42%

17%

6%

11%2%

UK and Ireland

Germany and Switzerland

France and Benelux countries

Nordic region

Other Western Europe

Eastern Europe

Figure 1: Spread of European run-off liabilities

Source: PricewaterhouseCoopers

We estimate that the size of the European run-off market is Euros 196 billion compared with Euros 202 billion last year. Figure 1 provides a split of those liabilities between the various countries and continues to demonstrate that the UK and Ireland, Germany, Switzerland, France and the Benelux countries account for the largest shares. The reduction in the size of the liabilities predominantly arises from a marked reduction in the UK run-off market, following pro-active commutations, managed exits and a reduction in the Lloyd’s run-off market. This has been partially offset by a growth in the Continental European run-off market as lines of business naturally enter run-off or are ceased for strategic reasons.

Market sizeRun-off liabilities in Europe

7Unlocking value in run-off

Figure 2: Major challenges facing Continental European insurers

05

04

03

02

01

Given the current economic climate and the continued squeeze on capital, organisations will look for ways to release capital that could be better deployed elsewhere in the business. There will be an increased appetite for European based insurance and reinsurance groups to scrutinise their discontinued operations and consider means by which to optimise capital through use of techniques such as insurance business transfers, disposals or solvent schemes.

Run-off is increasingly being seen as a priority for senior management and it is likely that organisations will look for ways to minimise associated operational costs.

Pro-active management of claims, driven by regular reserve reviews and actuarial assessments of future claims, is key to minimising adverse loss development. The results of this Survey indicate that run-off is receiving more focussed attention and being managed within separate business units.

Managing discontinued insurance business requires certain key skills such as the ability to manage complex long-tail claims and the ability to develop a strategic plan for the run-off. The UK and Continental European run-off markets have both developed over the last decade. Run-off service providers are prevalent in the UK and increasingly so in Continental Europe in areas like Germany and Scandinavia. As such, resourcing may not be seen as such a major challenge.

This was ranked as the least challenging option, which is most likely because of the growing acknowledgement of the availability of various exit mechanisms in Europe such as insurance business transfers, sale and exit via a solvent scheme. We have seen a steady increase in the number of solvent schemes and insurance business transfers for Continental European organisations and a wider awareness of such techniques.

“The insurance and reinsurance industry will be confronted with an extraordinary set of challenges over the next few years. The global market downturn in the context of the insurance sector is likely to limit growth potential, put pressure on reserving levels and increase the risk profile and volatility of the asset base. Upcoming regulatory and accounting changes will emphasise risk management even further and represent a step change as to how capital, and hence business, will in the future be managed on a risk adjusted basis. With capital markets not providing the capacity or liquidity of previous years the cost of capital will increase exponentially.”

Achim Bauer

Partner PricewaterhouseCoopers

Survey respondents were asked to rank a number of potential challenges facing Continental European insurers with their run-off business.

The results are shown below.

Market challengesWhat are the major challenges facing Continental European insurers with run-off business?

Tied-up capital

Operational costs

Adverse loss development

Lack of skilled resource

Availability of exit mechanisms

Source: PricewaterhouseCoopers

8 PricewaterhouseCoopers

70%

53%

14%19%

59%

30%

15%8%

1%

60%

50%

40%

30%

20%

10%

0%Solvency II IFRS II Enterprise

RiskManagement

Pricing /rates

Financial crisis

Emerging risks

OtherAttracting and retainingquality staff

Figure 3: The three key issues currently facing the insurance industry in Continental Europe

Source: PricewaterhouseCoopers

What are the three key issues facing the insurance industry in Continental Europe?

The current financial crisis is the key issue facing the industry. We are seeing our clients experience concerns about asset and litigation risks.

Survey respondents regarded the financial crisis, Solvency II and pricing / rates as the top three issues. Nearly 60% of respondents regarded the current financial crisis as the key issue facing the industry. We believe this results from concerns about asset risk, as investment assets continue to reduce in value, and litigation risk in the form of potential Directors & Officers and Errors & Omissions claims facing the financial services industry. There is currently little empirical evidence to show how severe these claims will be which increases the uncertainty in the insurance market.56% of Continental Europeans regarded Solvency II as a top three issue compared with 44% of UK respondents. Comparatively, Solvency II may be regarded as less of an issue in the UK, perhaps as a result of the FSA having taken steps to engage with organisations to encourage greater participation in the preparations for the Directive’s implementation. 30% of respondents regarded pricing / rates as a key issue. We are increasingly seeing events that challenge our perception of risk. From the failure of highly respected institutions and the volatility in the financial markets to the frequency of natural catastrophes, we appear to have entered a

new era of uncertainty. Tougher economic circumstances lead to scrutiny of expenses and a focus on ensuring even greater value for money from insurance coverage. This is reinforced by the strong line being held by reinsurers in keeping rates hard. Key to the insurance industry’s survival in this new world is ensuring that today’s pricing models are up to speed with the changes and producing an appropriate assessment of risk. We also expect these uncertainties in pricing to increase focus on cost savings in non-core areas such as run-off business, including looking at ways to extract value from this area.

Market challengesWhat are the major challenges facing Continental European insurers with run-off business?

9Unlocking value in run-off

How do organisations define run-off business?

The results of our Survey indicate that views regarding what falls within the definition of run-off business continue to differ between individuals in the same territory as well as between countries. We are, however, seeing some subtle movements towards a convergence of views and consistency in the definitions being applied, as 85% of respondents define run-off as ‘lines of business which are no longer written’. A fifth of Continental European respondents continue to define run-off as “business which is with a party where there is no on-going business relationship”. This might indicate an approach to dealing pro-actively with run-off only when no on-going business relationship exists.

70%

90%

80%

100%

85%

15% 20%15%

60%

50%

40%

30%

20%

10%

0%Lines of business

which are no longer written

Business which generates no further income

OtherBusiness which is with a party where

there is no on-going business relationship

2008 2009

Figure 4: Definition of run-off in Europe

Source: PricewaterhouseCoopers

We are seeing a convergence of views and consistency in the definitions of run-off being applied across Europe.

ManagementHow do organisations define and manage run-off business?

To what extent is the pro-active management of your organisation’s run-off business a priority for senior management?

Our Survey results show that 74% of all respondents consider that proactive management of their organisation’s run-off business is a priority for senior management within their organisation compared with 63% in last year’s Survey. 84% of UK respondents consider that proactive management of their organisation’s run-off business is a priority for senior management compared with 71% of Continental European respondents. However, 22% of Continental European respondents indicated that the level of attention is increasing. These results support the view that run-off management is moving up the agenda of senior management. Organisations are recognising the need to focus on their discontinued business in order to minimise the risks and maximise the value associated with it.

70%

90%

80%

100%

74%

20%

1% 2% 3%

60%

50%

40%

30%

20%

10%

0%

A priority for senior management

Not a priority for senior management

but the level of attention is increasing

OtherNot a priority for senior management

but should be

Not a priority for senior level

management and does not need to be

2008 2009

Figure 5: Is run-off a priority for senior management?

Source: PricewaterhouseCoopers

These results reflect our dealings with clients where run-off is moving up the corporate agenda.

10 PricewaterhouseCoopers

How is your organisation’s run-off business managed?

The results of this year’s Survey indicate a more consistent approach by respondents to the way run-off is managed in Continental Europe. 67% of Continental European and UK respondents manage their run-off as a separate business unit or run-off entity compared to 57% of respondents to the Survey last year. 20% of overall respondents manage their run-off business separately from their on-going business but within the same business unit compared to 22% last year. 13% of overall respondents manage their run-off alongside their on-going business compared to 21% last year.

70%

67%

20%

13%

60%50%50% 40%40% 30%30% 20%20% 10%10% 0%

As a separate business unit or run-off entity

Separately from on-going business but within the same business unit

Alongside on-going business

39%

49%

12%

On aterritory

by territorybasis

On aconsolidatedcross-border

basis

Other

Figure 6: Management of run-off in Europe

Operationally

Source: PricewaterhouseCoopers

In the main, organisations look at business on a Europe-wide basis ensuring that maximum benefits can be gained in terms of capital, operational costs, tax and regulatory efficiencies.

The results of the Survey illustrate an increasing similarity between how UK and Continental European respondents organise the management of their run-off business. Around 50% of both UK and Continental European respondents manage their business on a consolidated cross-border basis whilst around 40% manage their business on a territory by territory basis. The remaining UK and Continental European respondents selected the “Other” option, giving answers that included “consolidated cross-border basis with exceptions where local units are still in place”, “line of business basis”, “globally” and “differs by entity – focus is usually on cedent / insured”. These results indicate that, in the main, organisations look at business on a Europe-wide basis which suggests that there is a focus on ensuring that maximum benefits can be gained in terms of capital, regulatory, operational and tax efficiencies.

ManagementHow do organisations define and manage run-off business?

Geographically

These results support the view that run-off is receiving greater attention within Continental European organisations and that the benefits of dealing proactively with run-off business, such as the creation of a ‘centre of excellence’, have become more widely recognised across Continental Europe. The results also indicate that best practice in run-off management is steadily being adopted across organisations and territories in Continental Europe and the UK. However, given that a rump of run-off business remains under management alongside live business, our view that visible run-off in Europe is ‘only the tip of the iceberg’ continues to hold true.

11Unlocking value in run-off

70%

80%

90%

100%

8% 2%4%

60%

50%

40%

30%

20%

10%

0%

Yes No – but one is currently

being developed

No – but we expect one will be

needed in the next 12-24 months

No – we do not consider it is

required at this time

2008 2009

86%

Figure 7: Does your organisation have a strategic plan for run-off?

Source: PricewaterhouseCoopers

The results of the Survey showed a marked improvement from last year with 86% of overall respondents indicating that a strategic run-off plan existed compared with 72% in last year’s Survey. Only 4% of overall respondents did not consider a plan was required at this time compared with 9% last year.

These results are encouraging. However, when considered alongside Survey respondents’ views that commutations will be the most frequently used exit mechanism over the next year, this leaves us to question the depth of those strategies and whether they have been developed sufficiently to seek to achieve exit in the most efficient and effective manner.

Does your organisation have a strategic plan for dealing with its run-off business?

Organisations are taking a much closer look at their run-off and more are formulating strategic plans to deal with their discontinued operations.

12 PricewaterhouseCoopers

How long do you expect your run-off business to take to reach natural expiry?

Over 50% of Survey respondents indicated that their run-off would take longer than 10 years to reach natural expiry compared with 70% of respondents last year. This would seemingly indicate that organisations have begun to take steps to implement exit mechanisms to reduce the run-off tail. The reduction may well stem from the continued commutation activity in the past year, which is viewed by

organisations as the form of exit that will be used most frequently in the short term, probably fuelled by the need for cash and concerns about their reinsurers’ financial security given the current economic environment.

Many organisations are currently viewing commutation and settlement offers very differently compared to previous years, and the appetite for commutations has

increased. A deal that was unacceptable 12 months ago could now look much more attractive to cash constrained businesses. Given current attitudes to concluding deals, now may also be a good time for management to consider possible wider exit solutions from their discontinued business whilst there is momentum towards gaining finality.

Figure 8: European run-off tail

Source: PricewaterhouseCoopers

Run-off is an issue that will remain with senior management for years to come. However, as strategic plans to deal with run-off increasingly recognise alternative exit methods, then the length of time business will take to reach expiry might be expected to decline further in future years.

0-3 years

4% 16% 28% 52%

3-6 years 6-10 years >10 years

Time and moneyHow long will it take run-off business to reach natural expiry and what future claims uncertainties are faced?

Where do you think the major claims exposures will emanate from for Continental European insurers over the next five years?

United States

1%

56%

1%

9%23%

BRIC countries (Brazil, Russia, India, China)

Asia

Continental Europe

London Market

Figure 9: Prediction of major claims exposures by territory over the next five years

Source: PricewaterhouseCoopers

Our Survey results suggest that major claims exposures are likely to emanate from a variety of sources over the next five years. Some 56% of respondents believe that the major claim exposures will come from the US but there are some differences in views between Continental European respondents and UK respondents. Whilst 61% of Continental European respondents believe that the US will generate the major claim exposures over the next five years, only 44% of UK respondents hold this view. In contrast 23% of respondents believe claims will mainly emanate from the London Market with 19% believing claims will emanate from Continental Europe.

13Unlocking value in run-off

What do you think the major claims exposures will be for Continental European insurers over the next five years?

Figure 10: Types of claims anticipated over the next five years

30% of respondents believe that the major claim type over the next five years will be climate related, such as hurricane claims and flood damage claims, and 28% believe there will be an increase in claims related to the current financial crisis.

Although the Survey results indicate that climate and financial crisis related claims will be the biggest issues, our conversations with clients and wider market evidence suggests that asbestos claims are still a major problem for many insurers. Only 19% of respondents identified asbestos claims as a major exposure. In our experience there is still significant exposure arising from the US in respect of asbestos claims with All Sums allocations having increased the claim amounts many direct policyholders are seeking to recover from insurers. Many

UK and Continental European insurers still have significant exposures to asbestos or other such latent claims within their run-off portfolios. These risks should not be ignored or overshadowed by the current market issues as they are likely to remain a major area of claims activity for insurers and reinsurers alike for several years to come. Organisations need to consider appropriate exit solutions for such legacy issues within their strategic plans to ensure legacy exposures are eliminated and resources are made available to deal effectively with new and emerging claims.

Legacy claims are still a major problem for many insurers and these risks should not be overshadowed by the current market issues as they are likely to remain a major area of claims activity. Such issues can however be curtailed using appropriate exit strategies so that valuable resources can be directed towards dealing with new and emerging issues.

3%4%

16%

19%

28%30%

0%

5%

10%

15%

20%

25%

30%

35%

Pharmaceuticalclaims

Other D&O claims Asbestos Financial crisis

Climate related e.g. floods and

hurricanes

Source: PricewaterhouseCoopers

14 PricewaterhouseCoopers

Which exit mechanism do you think will be the most frequently used in relation to run-off business in Continental Europe over the next 12 months?

70%

58%

3% 5%

17% 16%

1%

60%

50%

40%

30%

20%

10%

0%Strategic

commutation programme

SaleBusiness transferReinsurance Solvent scheme of arrangement

Other

Figure 11: Most frequently used exit route over the next 12 months in Continental Europe

Source: PricewaterhouseCoopers

“Given the current constraints of the capital markets and the limited ability to generate organic capital due to depressed financial performances, options available to the broader insurance sector in dealing with discontinued operations include the transfer of legacy business to reinsurers or specialist run-off buyers as a means to achieve some capital relief. Alternative methodologies for transferring and closing discontinued books or vehicles in run-off, including solvent schemes, have been tested in a number of transactions during the past few years, and provide a viable option to achieve the desired capital and cost benefit in the current market environment.”

Achim Bauer

Partner PricewaterhouseCoopers

58% of respondents indicated that a strategic commutation programme would be the most frequently used exit mechanism during 2009. Europe has seen an increasing number of rendez-vous events in Norwich, London and Cologne where considerable commutation activity takes place.

Following commutations, 33% of respondents regarded sale or insurance business transfer as being the most frequently used. We have seen a number of insurance business transfers in the last year and, more recently, the German marine insurer and reinsurer, DARAG, was sold to hedge fund Auger Capital. The introduction of the Reinsurance Directive has fuelled the steady flow of reinsurance

business transfers and has increased expectation that this will be a frequently used exit strategy.

Only 5% of respondents viewed solvent schemes (which are in summary a wholesale commutation of a company’s liabilities) as the most popular exit option in the next year despite the focus on individual commutations. However, from our discussions with clients, we expect to see a further steady flow of schemes into the market in 2009 following the recent sanction of the GLOBALE Re solvent scheme. We anticipate further innovations in solvent schemes for larger and / or more complex books and pools to be seen in the next 12 months.

Exit route options What are the exit strategies for European run-off business?

15Unlocking value in run-off

Long-tail claims were regarded by 34% of the Continental European respondents to be the single most important issue influencing their ability to gain finality for their run-off liabilities compared with only 15% of UK respondents. UK respondents may view long-tail claims as less of an issue because the UK run-off market has seen numerous insurance business exits via a solvent scheme for books with complex long-tail claims.

Overall, 26% of respondents regarded counterparty interest as the single most important issue influencing their ability to gain finality.

We were surprised to see that the availability of exit mechanisms was the

third most important issue influencing the ability to gain finality. It is clear that there is now a proven track record of utilising business transfers, sales and solvent schemes to exit Continental European discontinued insurance business. The Appendix to this Survey includes commentary on exit via solvent schemes for Continental European companies.

In addition, whilst 15% of UK respondents regarded reputation as a key factor, this was regarded as a major issue by only 5% of Continental Europeans. We found this at odds with our own experience where reputation has been identified as a major factor when exploring finality options for discontinued business in Europe.

What is the single most important issue influencing your ability to gain finality for your run-off liabilities? 30%

3%

14%

26%

4% 6% 7% 10%

50%

40%

30%

20%

10%

0%Long-tail

claimsAvailability

of exit mechanisms

Counterparty interest

Litigation /disputed claims

Incomplete records

Reputational risk

OtherSkilled resources

Figure 12: The single most important issue influencing the ability to gain finality

Source: PricewaterhouseCoopers

Long-tail claims were regarded by Continental European respondents to be the single most important issue influencing their ability to gain finality for their run-off liabilities. However, there are tried and tested exit strategies that enable organisations to remove these liabilities from their balance sheet.

As mentioned earlier in the Survey, there has been significant commutation activity in the run-off sector. This is demonstrated in the Survey by 43% of respondents having entered into more than 30 inwards commutation agreements in the past year. The overall run-off liabilities in Europe have reduced, particularly in the UK, indicating that the increased commutation

activity is driving the liabilities down, albeit at a slow rate as individual commutation negotiations are time consuming and only achieve closure on a piecemeal basis.

Last year our Survey highlighted that some 40% of Continental European respondents believed that strategic commutation programmes would be the most frequently utilised exit mechanism over the next five years. The results of our Survey this year continue to support this trend. The current high degree of commutation activity may not only be driven by insurers trying to bring finality to their run-off business, but also by policyholders, particularly those with exposure to latent claims, viewing

commutation offers in a different light due to the current economic environment.

Our Survey suggests that the levels of outwards reinsurance commutations have been comparatively lower than inwards commutation agreements, with only 21% of overall respondents participating in over 30 commutations. This may reflect the need for insurers to initially focus on reducing uncertainty and releasing reserves by making inwards commutations a priority. However, this could simply be a result of the number of direct policies being larger than the corresponding outwards reinsurance treaties.

How many inwards commutations / policy buy-backs and outwards commutations have you completed in the last 12 months?

16 PricewaterhouseCoopers

Drivers for changeWhat factors will promote future insurance restructurings in Europe?

We asked Survey respondents what drivers will influence the restructuring activities of Continental European insurance groups over the next five years?

77% of respondents indicated that efficient capital management would be the key driver for restructuring activities across Continental Europe over the next five years. It is likely that there will be an increased keenness by European insurance groups to look at ways of optimising capital by analysing their current organisational structure and making the best use of the increasingly homogeneous framework operating in the EEA.

The ability to deal more effectively with discontinued business was selected by 41% of respondents. There were some marked differences in the responses provided by UK and Continental European respondents.

Whilst some 54% of UK respondents indicated that the ability to deal more effectively with discontinued business was a key driver for restructuring activities, this was a view held by only 36% of Continental European respondents. However, as awareness of the variety of exit options available to Continental European business grows, it is likely that an increasing proportion of Continental European businesses will also take this view.

The next most popular driver for restructuring activities in Continental Europe was improved operational structuring, which was identified as a driver for restructuring activities by 28% of respondents. This result supports the view that organisations are looking more closely at capital issues and cost efficiencies as a result of the current economic climate.

This driver was closely followed by the easing of regulatory burden, which was selected by 24% of respondents. Historically, Survey respondents may have seen regulatory burden as an issue

because of the lack of homogeneity across EEA territories. However, with the increasingly consistent regulatory framework, this burden may be easing as opportunities for cross-border restructuring become available.

All these factors seem likely to be influenced by Solvency II, which should create an environment of greater focus on capital efficiency, increased awareness of the risks and rewards of discontinued business and, together with ERM, more focus on ensuring that an organisation’s operations are structured in the most effective manner.

Source: PricewaterhouseCoopers

28%

11%

41%

17%24%

77%

70%

80%

90%

100%

60%

50%

40%

30%

20%

10%

0%Improved

tax efficienciesImproved

operational structuring

Wish to operate via a branch

structure

Ability to deal more effectively with

discontinued business

Easing of regulatory

burden

More efficient capital

management

Figure 13: Drivers that will influence restructuring activities in Continental Europe

The current economic climate has focused the minds of respondents more on capital issues and the effective utilisation of this resource.

17Unlocking value in run-off

Solvency II seeks to embed risk awareness into the frameworks organisations use for governance, operations and decision making. In our second Survey we highlighted that most observers expect Solvency II to result in increased levels of discontinued business. This is because of insurers focusing on the risks and rewards of their business lines and seeking to rationalise their portfolios and withdraw from capital intensive lines of business compared to other, more capital efficient, lines. The results of our third Survey continue to support this view. Of the total number of respondents, over 50% indicated that “increased focus on run-off business and exploration of exit options” and nearly 50% indicated that “increased focus on and shedding of underperforming lines of business” would be practical implications of Solvency II. These results, and the activity that we are already seeing, indicate that individuals and organisations believe Solvency II is resulting in more focus on the risk and reward of business lines. Consequently, additional focus is being given to run-off and exit options.

There were some differences in views held between UK respondents and Continental European respondents in respect of Solvency II. 56% of Continental

Europeans regarded “increased focus on run-off business and exploration of exit options” as being a key practical implication of Solvency II compared to 46% of UK respondents, which indicates that this area is gaining increasing recognition in Continental Europe compared to the UK. When asked whether the introduction of Solvency II would result in their own organisation exiting certain lines of business, 16% of respondents answered “yes”, 57% answered “no” and 27% were unsure. This indicates that although respondents believe that across the whole market, the focus on run-off and exploration of exit options would be a realistic and practical implication of Solvency II, organisations are still in the early stages of their thinking on whether they would exit certain lines of business.

The developing regulatory landscape What impact will Solvency II and the Reinsurance Directive have on European run-off business?

36% 34%

17%

54%48%

33%

70%

60%

50%

40%

30%

20%

10%

0%

Increased focus on run-off

business and exploration of

exit options

Consolidation of run-off portfolios and development

of operational centres of excellence

An increase in the cost of

capital

More stringent regulatory

sanctions and penalties

Increased focus on and shedding

of underperforming lines of business

Increased merger and acquisition

activity

Figure 14: Practical impact of Solvency II in Continental Europe

Source: PricewaterhouseCoopers

Solvency II is resulting in more focus on the risk and reward of business lines and will lead to increasing consideration of run-off and exit options.

What do you think the practical implications of Solvency II are likely to be for Continental European insurers?

“Feedback from prominent European businesses suggests that they expect Solvency II will be more costly for run-off businesses from both a capital and profit and loss perspective.”

Mark Batten

Partner PricewaterhouseCoopers

18 PricewaterhouseCoopers

A surprisingly low number of Survey respondents either did not participate or did not know whether their organisation had participated in QIS4, the most recent QIS.

There is a lack of guidance in the Solvency II Directive on legacy business, however, run-off represents a risk to organisations and must not be ignored. Organisations with run-off need to actively participate in Solvency II QIS to ensure that run-off specific issues are addressed.

The developing regulatory landscape What impact will Solvency II and the Reinsurance Directive have on European run-off business?

Did your company participate in QIS4 and did your company consider its legacy business separately?

Of those that did participate, few Survey respondents had considered their legacy business separately and there was little evidence to suggest that this resulted in any significant change to capital charges. These results may have arisen from the lack of differentiation in the QIS approach between live and run-off business but they also tie in with our experience that, to date, there are still a number of key issues which will impact the treatment of run-off business that have yet to be resolved. The guidelines on the treatment of run-off activities are unclear. However, run-off is still likely to represent a risk and will need to be considered in the overall group solvency calculation.

We have seen some pro-active steps by companies preparing for Solvency II, especially in the UK where we have seen a step change following the FSA’s Discussion Paper and direct contact with organisations’ Chief Executive Officers calling for them to take action in this area. If Continental European Regulators follow suit, we expect to see increased activity in preparation for Solvency II across Europe.

As the deadline for the implementation of Solvency II looms (as illustrated in Figure 15), Quantitative Impact Studies (QIS) have been released to assess the impact on balance sheets and solvency positions. Our Survey results indicate that organisations need to be more pro-active in order to meet the ultimate deadline, particularly if they wish to be fully compliant through the use of an internal model. This view is further supported by the results of a recent survey conducted by PricewaterhouseCoopers within the London Market, where only 16% of London Market respondents confirmed

that they had completed an impact assessment that considered how the position of their organisation would be viewed in the context of the current Solvency II arrangements.

Figure 15: Solvency II implementation timeline

Draft FrameworkDirective published

2012201120102007 2008 2009

High Level Principles (Level 1 Directive) adopted

Solvency II systemin operation

(31 October 2012)

QIS 4QIS 3 Detailed rules finalised(Level II implementing measures)

EU member states to transpose into law

Model pre-approval process

Source: PricewaterhouseCoopers

Our Survey results indicate that organisations need to engage more fully in preparation for Solvency II’s implementation.

19Unlocking value in run-off

Do you anticipate that the implementation of the EU Reinsurance Directive will increase the level of insurance business transfers in Continental Europe over the next five years?

An overwhelming 98% of respondents expect an increase in insurance business transfers in Continental Europe over the next five years following the implementation of the Reinsurance Directive. These predictions appear to be in line with activity across Continental Europe at present and we have seen a broad spectrum of transfers ranging from, for example, the likes of Swiss Re’s redomestication of its headquarters to Luxembourg to run-off specific transactions such as Deutsche Rück and Cirrus Re.

The Survey’s expectation of increased transfer activity is supported by the steady flow of transactions already seen in both live and discontinued sectors.

20 PricewaterhouseCoopers

We asked respondents what they would like to change in respect of the management of run-off business.

Figure 16: What respondents would like to change in respect of run-off management

Our third Survey has demonstrated some convergence of views across Europe in terms of how run-off is defined and managed. The profile of run-off business has continued to increase throughout Europe and 2009 is expected to provide further developments in restructuring and exit of discontinued operations. However, as evidenced by the responses above, further education and understanding of the tools available is required across Europe.

Survey respondents expect 2009 to be challenging in the face of the current financial crisis and it will be interesting to see how the coming year will develop. We have been delighted with the responses that we received to our Survey and look forward to discussing the results with the market over the coming months.

“Availability of exit mechanisms in Europe”

Finality

“Need more exit mechanisms”

“Less complex tools to exit business”

“Would like to see Continental run-off emerging as a market”

The emergence of a Continental

European run-off market

“An industry voice representing the views of Continental Europe”

“More regulatory support”

Regulatory change

“Burdensome regulatory reporting”

“Less regulatory implications”

“Separate run-off to its own business unit with its own balance sheet”

Focus on run-off

“Clearer direction from organisations and their approach to run-off”

“More focus on efficiency”

“Effectiveness”

Operational efficiency

“High quality IT system would make the management much easier”

Key themes

What would you like to change?

Figure 16 provides a selection of answers from the Survey respondents.

Source: PricewaterhouseCoopers

21Unlocking value in run-off

Glossary

for the purposes of our Survey this is all countries in Europe excluding the UK. The countries included in our statistics, other than the UK, are as follows: Austria, Belgium, Bulgaria, Croatia, Cyprus, the Czech Republic, Denmark, Estonia, European Russia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, Montenegro, The Netherlands, Norway, Poland, Portugal, Romania, Serbia, Slovakia, Slovenia, Spain, Sweden, Switzerland, Turkey and Ukraine.

the European Commission’s Directive to establish a framework whereby merging companies are governed by the provisions of its natural law applicable to domestic mergers. The Directive was to be implemented by member states by 15 December 2007.

the European Economic Area which includes all member states of the EU as well as members of the European Free Trade Association (EFTA). Members of the EFTA are Iceland, Liechtenstein, Norway and Switzerland. However, Switzerland is not included in the EEA.

the European Union is a community of 27 members who seek to create a single market by a system of laws that apply in all member states. The members of the EU are currently Austria, Belgium, Bulgaria, Cyprus, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, The Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden and the United Kingdom.

any reference to Europe means Continental Europe plus the UK (as defined below).

the European Commission’s Directive on the supervision of pure reinsurance companies, published in December 2005 and expected to be implemented in the EU member states by the deadline of December 2007.

in line with the definition we used in the first edition of our Survey (published in February 2007) this includes entities that are wholly in run-off as well as discontinued business which forms part of continuing operations. Branch business is included in the domicile in which the branch is regulated. The terms run-off, discontinued and legacy business are used interchangeably.

a draft Directive forming part of the European Commission’s drive for a single European market and the modernisation of regulation. It will create a single risk sensitive EU-wide regulatory framework. The Solvency II project was initiated by the European Commission in 2001 and the Directive is expected to be implemented in 2012.

the European Commission’s Directive on the coordination of laws, regulations and administrative provisions relating to direct insurance other than life assurance, published in June 1992 with an implementation deadline of July 1994.

United Kingdom includes England, Northern Ireland, Scotland and Wales.

Continental Europe

EEA

EU

Cross-Border Mergers Directive

Europe

Reinsurance Directive

Run-off / discontinued business

Solvency II

Third Non-Life Directive

UK

22 PricewaterhouseCoopers

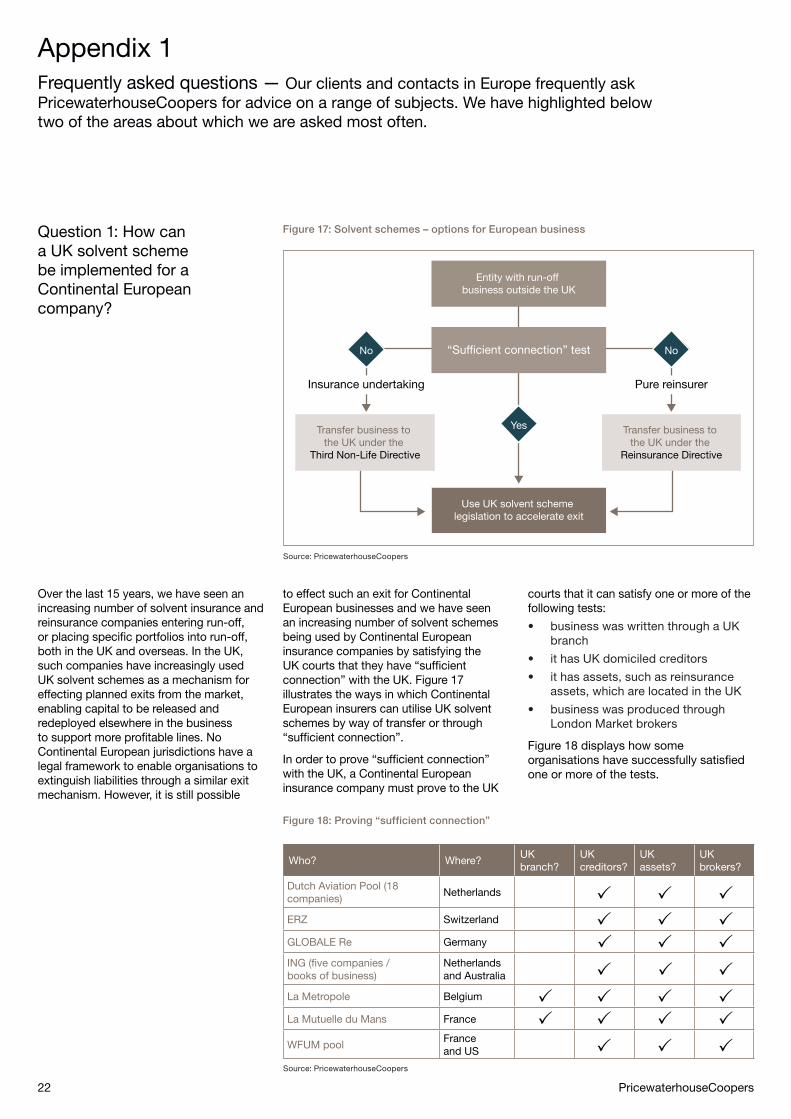

Question 1: How can a UK solvent scheme be implemented for a Continental European company?

Over the last 15 years, we have seen an increasing number of solvent insurance and reinsurance companies entering run-off, or placing specific portfolios into run-off, both in the UK and overseas. In the UK, such companies have increasingly used UK solvent schemes as a mechanism for effecting planned exits from the market, enabling capital to be released and redeployed elsewhere in the business to support more profitable lines. No Continental European jurisdictions have a legal framework to enable organisations to extinguish liabilities through a similar exit mechanism. However, it is still possible

to effect such an exit for Continental European businesses and we have seen an increasing number of solvent schemes being used by Continental European insurance companies by satisfying the UK courts that they have “sufficient connection” with the UK. Figure 17 illustrates the ways in which Continental European insurers can utilise UK solvent schemes by way of transfer or through “sufficient connection”.

In order to prove “sufficient connection” with the UK, a Continental European insurance company must prove to the UK

courts that it can satisfy one or more of the following tests:

business was written through a UK •branch

it has UK domiciled creditors•

it has assets, such as reinsurance •assets, which are located in the UK

business was produced through •London Market brokers

Figure 18 displays how some organisations have successfully satisfied one or more of the tests.

Appendix 1Frequently asked questions — Our clients and contacts in Europe frequently ask PricewaterhouseCoopers for advice on a range of subjects. We have highlighted below two of the areas about which we are asked most often.

Figure 18: Proving “sufficient connection”

Source: PricewaterhouseCoopers

Source: PricewaterhouseCoopers

Who? Where?UK branch?

UK creditors?

UK assets?

UK brokers?

Dutch Aviation Pool (18 companies)

Netherlands

ERZ Switzerland

GLOBALE Re Germany

ING (five companies / books of business)

Netherlands and Australia

La Metropole Belgium

La Mutuelle du Mans France

WFUM poolFrance and US

Entity with run-off business outside the UK

Yes

“Sufficient connection” test

Use UK solvent scheme legislation to accelerate exit

Transfer business to the UK under the

Third Non-Life Directive

No

Transfer business to the UK under the

Reinsurance Directive

No

Insurance undertaking Pure reinsurer

Figure 17: Solvent schemes – options for European business

Question 2: What does Solvency II mean for run-off?

Solvency II is a catalyst for change, not only in terms of restructuring activity but also in that it complements the current managerial focus on ERM. Solvency II calls for a full evaluation of all the risks faced by the business and the capital needed to support them. Effective ERM can help to provide a sound platform for decision making through a clearer articulation of business objectives and measurement of the risks of that business. We are seeing increasing appetite to consider restructuring options to place businesses in the optimal position to take advantage of future opportunities provided by Solvency II and ERM.

However, there is a lack of clear guidance in the Solvency II Directive on specific treatment of legacy business. Under the Directive, reinsurers in run-off before 10 December 2007 will be exempt in full, although if a run-off organisation subsequently buys another run-off portfolio, the issue of whether it will remain exempt is unclear.

Consider a scenario where a large European organisation has a standalone company which has been in run-off for a number of years as well as a number of large live businesses. Each contain significant amounts of legacy business. The organisation recognises the potential benefits of streamlining that business through transferring all the business in run-off to the existing run-off entity from an operational perspective. In addition, post-Solvency II, completing such a

transfer would mean that the run-off business which had previously been part of live businesses and very much under the scope of Solvency II is now housed in an entity which is exempt from the Solvency II rules….or does it? How will Solvency II impact on this scenario? Questions such as this which address the particular issues of run-off have not as yet been fully debated by policymakers in Europe. Whilst the wide reaching and holistic ambit of Solvency II is helpful in thinking conceptually about a new level playing field of regulation across Europe, it is quickly evident that there are difficulties in translating the high level principles to deal with such a complex market. Given that large pockets of run-off business sit alongside live business in many European businesses, understanding the impact that run-off business may have on overall treatment is an area that needs to be given greater consideration.

It is clear that organisations with significant discontinued elements need to take affirmative action through the QIS programmes to ensure that run-off matters are appropriately tabled, clarity gained and solutions identified. In that regard, organisations should be seen to be pro-active in their engagement with Solvency II which, particularly in respect of discontinued business, has not always been the case to date.

23Unlocking value in run-off

24 PricewaterhouseCoopers

The PricewaterhouseCoopers teamUnlocking value in run-off

The Solutions for Discontinued Insurance Business team has access to more than 200 specialists focusing on providing restructuring and operational consulting services to companies in the insurance industry with run-off business. Issues being faced by operations around the world where the team is able to provide advice, support and assistance include:

the need to bring finality to run-off •and extinguish liabilities

the requirement to release capital •from run-off and consider options such as sale or transfer of liabilities

the need to rationalise operations to •achieve operational efficiency

the need to proactively manage •in-house or outsourced run-off,

including the development of a robust outsourcing contract, to maximise shareholder value

the need to benchmark the claims •and reinsurance functions to assess their effectiveness or otherwise

To find out more, please contact any of the team below or visit our website: www.pwc.co.uk/discontinuedinsurance

Mark Speller Corporate Finance

[email protected]+44 (0) 20 721 31154

Mark Allen Actuarial and Insurance Management Solutions

[email protected]+44 (0) 20 7212 4631

Huw Jenkins Tax

[email protected]+44 (0) 20 7212 5480

Achim Bauer Insurance Advisory

[email protected] +44 (0) 20 7212 1405

Jim Bichard Regulatory

[email protected]+44 (0) 20 7804 3792

Bryan Joseph Actuarial and Insurance Management Solutions

[email protected]+44 (0) 20 7213 2008

Neil Gayner Solutions for Discontinued Insurance Business

[email protected]+44 (0) 20 7212 6117

Clare Whitcombe Solutions for Discontinued Insurance Business

[email protected]+44 (0) 20 7804 4844

Andrew Ward Solutions for Discontinued Insurance Business

[email protected]+44 (0) 20 7213 3197

Dan Schwarzmann Solutions for Discontinued Insurance Business

[email protected]+44 (0) 20 7804 5067

Mark Batten Solutions for Discontinued Insurance Business

[email protected]+44 (0) 20 7804 5635

Peter Greaves Solutions for Discontinued Insurance Business

[email protected]+44 (0) 20 7804 4061

Survey creditWe would like to thank everyone who took the time to participate in our Survey.

In total we surveyed 519 parties during the research for this report.

25Unlocking value in run-off

The member firms of the PricewaterhouseCoopers network provide industry-focused assurance, tax and advisory services to build public trust and enhance value for its clients and their stakeholders. More than 146,000 people in 150 countries across our network share their thinking, experience and solutions to develop fresh perspectives and practical advice.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents accept no liability, and disclaim all responsibility, for the consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2009 PricewaterhouseCoopers LLP. All rights reserved. “PricewaterhouseCoopers” refers to PricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom) or, as the context requires, the PricewaterhouseCoopers global network or other member firms of the network, each of which is a separate and independent legal entity.

Design by hamilton-brown (hb04094)

www.pwc.co.uk/discontinuedinsurance