united states district court x class action …securities.stanford.edu/filings-documents/1035/...15....

TRANSCRIPT

UNITED STATES DISTRICT COURT

NORTHERN DISTRICT OF GEORGIA

ATLANTA DIVISION

x DOUGLAS R. GLASS, on Behalf of Himself and All Others Similarly Situated,

Plaintiff,

vs.

IMMUCOR INC., EDWARD L. GALLUP, GIOACCHINO De CHIRICO, STEVEN C. RAMSEY and MARK KISHEL,

Defendants.

: : : : : : : : : : : : : x

Civil Action No.

CLASS ACTION

COMPLAINT FOR VIOLATION OF THE FEDERAL SECURITIES LAWS

DEMAND FOR JURY TRIAL

- 1 -

BACKGROUND AND CASE OVERVIEW

1. This is a securities class action on behalf of all persons who purchased

the common stock of Immucor, Inc. (“Immucor” or the “Company”) between

January 7, 2005 and August 29, 2005 (the “Class Period”), against Immucor and

certain of its officers and directors for violation of the Securities Exchange Act of

1934 (the “1934 Act”).

2. Immucor engages in the development, manufacture, and marketing of

immunological diagnostic medical products worldwide. It offers a line of reagents

and automated systems that are used by hospitals, clinical laboratories, and blood

banks in various tests performed to detect and identify certain properties of cell and

serum components of human blood.

3. During the Class Period, defendants caused Immucor’s shares to trade at

artificially inflated levels by issuing a series of materially false and misleading

statements regarding the Company’s financial statements, business and prospects.

This caused the Company’s stock to trade as high as $34.98 per share. Defendants

took advantage of this artificial inflation selling 139,500 shares of their Immucor

stock for proceeds of $4.2 million.

- 2 -

4. On August 12, 2005, defendant Mark Kishel resigned from the Board of

Directors of Immucor at the request of the Board which had requested the resignation

due to potential violations of Immucor’s insider trading policies.

5. On Friday, August 26, 2005, Immucor announced that the SEC had

formalized its probe into payments made by its Italian subsidiary to people associated

with government medical facilities.

6. Then, on August 29, 2005, after the market closed, the Company

announced that it had revised its net income for fiscal 2005 to account for a previously

unrecorded accrual for employee bonuses and furthermore made an announcement

that it had accepted the resignation of defendant Steven Ramsey from the post of

Chief Financial Officer. The release stated in part:

Immucor, Inc., a global leader in providing automated instrument-reagent systems to the blood transfusion industry, today announced a revision in previously-reported net income for fiscal year 2005 to account for a previously-unrecorded accrual for employee bonuses. On an after-tax basis, the accrual for the third fiscal quarter is $0.2 million and the accrual for the fourth fiscal quarter is $0.7 million, for an aggregate bonus accrual of $0.9 million for the fiscal year. As revised, for the year and fourth quarter ended May 31, 2005, net income was $23.9 million for the year and $8.5 million for the fourth quarter; and diluted earnings per share were $0.50 for the year on 47.6 million weighted average shares outstanding, and $0.18 for the fourth quarter on 47.7 million weighted average shares outstanding.

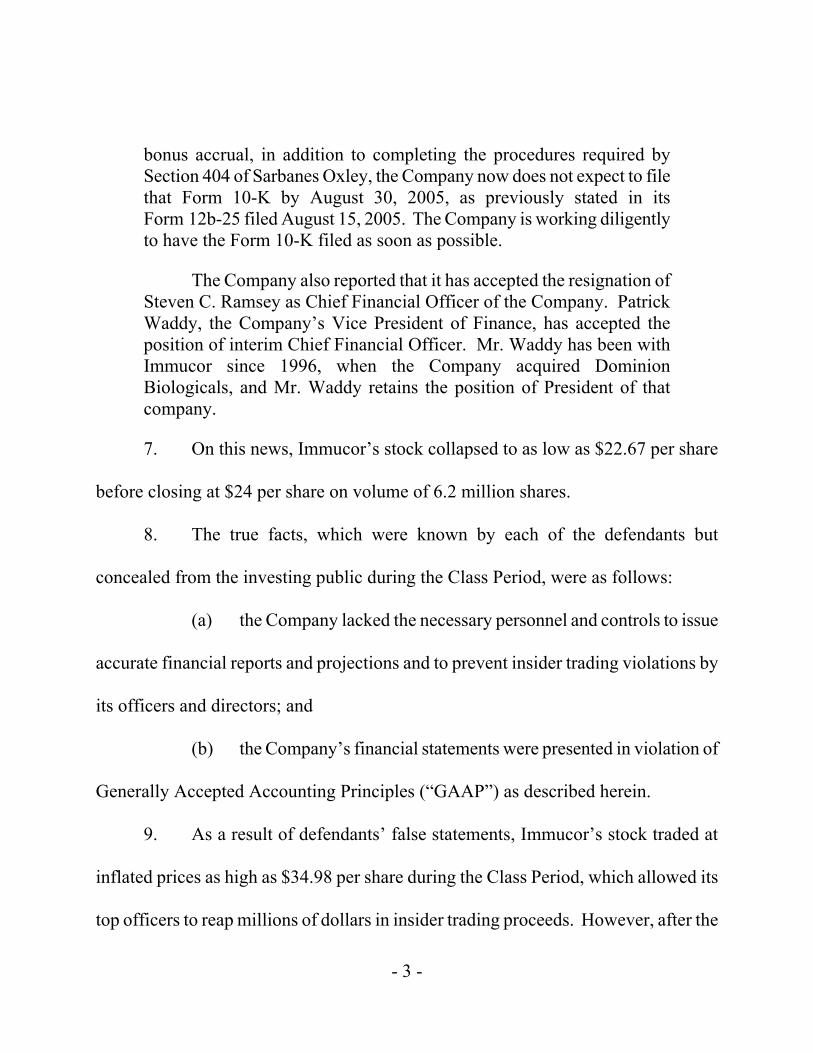

The Company expects to report those revised numbers in its Form 10-K for fiscal year 2005. However, due to the additional accounting and auditing procedures to be completed to account for the

- 3 -

bonus accrual, in addition to completing the procedures required by Section 404 of Sarbanes Oxley, the Company now does not expect to file that Form 10-K by August 30, 2005, as previously stated in its Form 12b-25 filed August 15, 2005. The Company is working diligently to have the Form 10-K filed as soon as possible.

The Company also reported that it has accepted the resignation of Steven C. Ramsey as Chief Financial Officer of the Company. Patrick Waddy, the Company’s Vice President of Finance, has accepted the position of interim Chief Financial Officer. Mr. Waddy has been with Immucor since 1996, when the Company acquired Dominion Biologicals, and Mr. Waddy retains the position of President of that company.

7. On this news, Immucor’s stock collapsed to as low as $22.67 per share

before closing at $24 per share on volume of 6.2 million shares.

8. The true facts, which were known by each of the defendants but

concealed from the investing public during the Class Period, were as follows:

(a) the Company lacked the necessary personnel and controls to issue

accurate financial reports and projections and to prevent insider trading violations by

its officers and directors; and

(b) the Company’s financial statements were presented in violation of

Generally Accepted Accounting Principles (“GAAP”) as described herein.

9. As a result of defendants’ false statements, Immucor’s stock traded at

inflated prices as high as $34.98 per share during the Class Period, which allowed its

top officers to reap millions of dollars in insider trading proceeds. However, after the

- 4 -

above revelations entered the market, the Company’s stock was hammered by massive

sales of the Company’s shares sending them down 12.85% from their previous day’s

close of $27.54.

JURISDICTION AND VENUE

10. Jurisdiction is conferred by §27 of the 1934 Act. The claims asserted

herein arise under §§10(b) and 20(a) of the 1934 Act and SEC Rule 10b-5.

11. (a) Venue is proper in this District pursuant to §27 of the 1934 Act.

Many of the false and misleading statements were made in or issued from this District.

(b) The Company’s principal executive offices are located in Norcross,

Georgia.

THE PARTIES

12. Plaintiff Douglas R. Glass purchased Immucor common stock as

described in the attached certification and was damaged thereby.

13. Defendant Immucor engages in the development, manufacture, and

marketing of immunological diagnostic medical products worldwide. It offers a line

of reagents and automated systems that are used by hospitals, clinical laboratories, and

blood banks in various tests performed to detect and identify certain properties of cell

and serum components of human blood.

- 5 -

14. Defendant Edward L. Gallup (“Gallup”) is, and at all relevant times was,

the Chief Executive Officer and Chairman of the Board of Directors of Immucor.

During the Class Period, Gallup reaped $4.2 million in insider trading proceeds by

selling 139,500 shares of his Immucor stock at artificially inflated prices.

15. Defendant Gioacchino De Chirico (“De Chirico”) is, and at all relevant

times was, the President of Immucor.

16. Defendant Steven C. Ramsey (“Ramsey”) was, until August 29, 2005, the

Chief Financial Officer, Principal Accounting Officer and Vice President of Immucor,

at which time he submitted his resignation.

17. Defendant Mark Kishel (“Kishel”) was, until his resignation on

August 12, 2005, a member of the Board of Directors of Immucor.

18. Defendants Gallup, De Chirico, Ramsey and Kishel (the “Individual

Defendants”), because of their positions with the Company, possessed the power and

authority to control the contents of Immucor’s quarterly reports, press releases and

presentations to securities analysts, money and portfolio managers and institutional

investors, i.e., the market. They were provided with copies of the Company’s reports

and press releases alleged herein to be misleading prior to or shortly after their

issuance and had the ability and opportunity to prevent their issuance or cause them to

be corrected. Because of their positions as CEO and Chairman, President, CFO and a

- 6 -

director of the Company and their access to material non-public information available

to them but not to the public, the Individual Defendants knew that the adverse facts

specified herein had not been disclosed to and were being concealed from the public

and that the positive representations being made were then materially false and

misleading. Defendants are liable for the false statements pleaded herein at ¶¶21 and

23-24.

FRAUDULENT SCHEME AND COURSE OF BUSINESS

19. The Individual Defendants are liable for: (i) making false statements; or

(ii) failing to disclose adverse facts known to them about Immucor. Defendants’

fraudulent scheme and course of business that operated as a fraud or deceit on

purchasers of Immucor’s common stock was a success, as it: (i) deceived the investing

public regarding Immucor’s prospects and business; (ii) artificially inflated the price

of Immucor’s common stock; (iii) allowed defendants to sell $4.2 million worth of

their Immucor stock at inflated prices; and (iv) caused plaintiff and other members of

the Class to purchase Immucor common stock at inflated prices.

BACKGROUND

20. Defendant Immucor engages in the development, manufacture, and

marketing of immunological diagnostic medical products worldwide. It offers a line

of reagents and automated systems that are used by hospitals, clinical laboratories, and

- 7 -

blood banks in various tests performed to detect and identify certain properties of cell

and serum components of human blood. The Company’s reagent product groups

include ABO blood grouping and Rh blood typing reagents; anti-human globulin

serums; reagent red blood cells; rare serums; antibody potentiators; quality control

systems; monoclonal antibody-based reagents; technical proficiency systems; fetal

bleed screen kit; Capture-P, Capture-R, Capture-CMV, Capture-S, and Capture-R

Select reagents; HLA serums; reagents for infectious diseases clinical chemistry; and

immunofluorescent monoclonal antibodies. These are used in tests performed prior to

blood transfusion in determining the blood group and type of patients’ and donors’

blood, detection and identification of blood group antibodies, detection of platelet

antibodies, and paternity testing. Immucor’s blood bank automation products include

ABS2000, an automated blood bank system; ROSYS Plato, a microplate liquid

handler and sample processor; DIAS PLUS and GALILEO, high volume microplate

processors; and Multireader Plus, a spectra photometric microtitration plate reader.

These products enable blood bank technologists to perform blood compatibility tests.

The Company distributes laboratory equipment designed to automate certain blood

testing procedures. Its stock is traded in an efficient market on the Nasdaq National

Market System.

- 8 -

FALSE AND MISLEADING STATEMENTS ISSUED DURING THE CLASS PERIOD

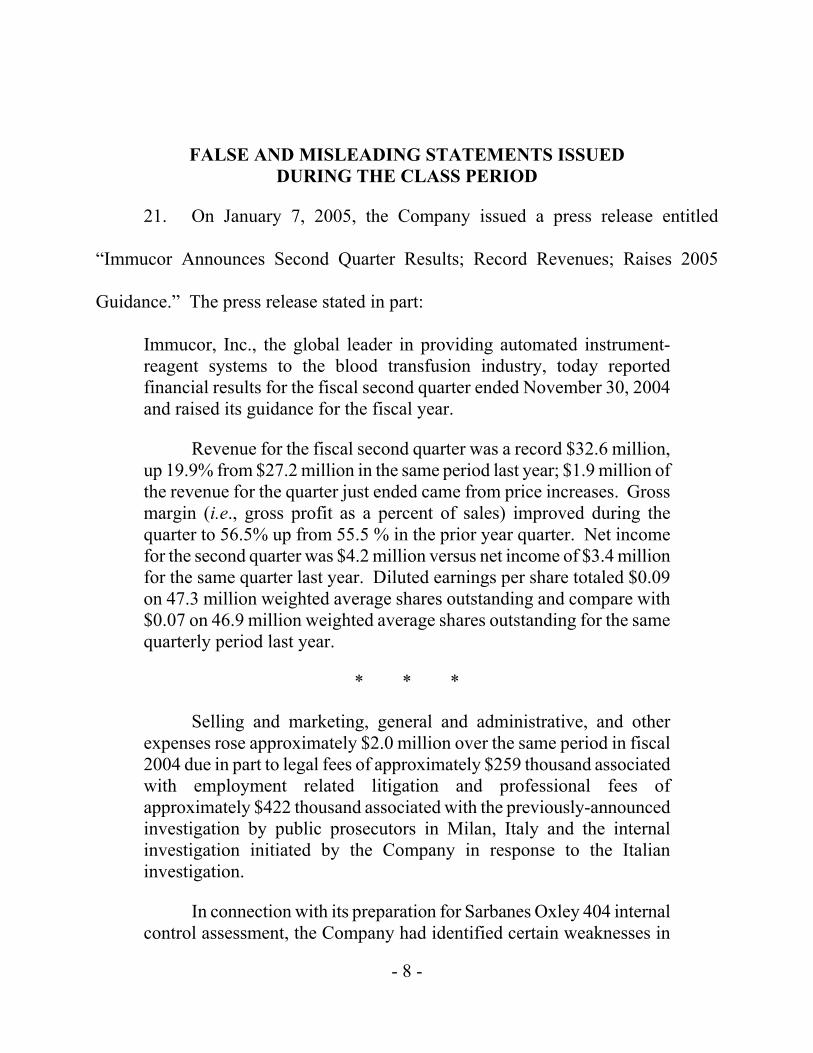

21. On January 7, 2005, the Company issued a press release entitled

“Immucor Announces Second Quarter Results; Record Revenues; Raises 2005

Guidance.” The press release stated in part:

Immucor, Inc., the global leader in providing automated instrument-reagent systems to the blood transfusion industry, today reported financial results for the fiscal second quarter ended November 30, 2004 and raised its guidance for the fiscal year.

Revenue for the fiscal second quarter was a record $32.6 million, up 19.9% from $27.2 million in the same period last year; $1.9 million of the revenue for the quarter just ended came from price increases. Gross margin (i.e., gross profit as a percent of sales) improved during the quarter to 56.5% up from 55.5 % in the prior year quarter. Net income for the second quarter was $4.2 million versus net income of $3.4 million for the same quarter last year. Diluted earnings per share totaled $0.09 on 47.3 million weighted average shares outstanding and compare with $0.07 on 46.9 million weighted average shares outstanding for the same quarterly period last year.

* * *

Selling and marketing, general and administrative, and other expenses rose approximately $2.0 million over the same period in fiscal 2004 due in part to legal fees of approximately $259 thousand associated with employment related litigation and professional fees of approximately $422 thousand associated with the previously-announced investigation by public prosecutors in Milan, Italy and the internal investigation initiated by the Company in response to the Italian investigation.

In connection with its preparation for Sarbanes Oxley 404 internal control assessment, the Company had identified certain weaknesses in

- 9 -

internal controls in the Italian subsidiary at the time it learned of the Italian investigation, and the Company was in the process of strengthening those internal controls. Those efforts were accelerated in connection with the internal investigation, and the Company has undertaken a thorough review of the books and records of the Italian subsidiary with the assistance of forensic audit personnel from PricewaterhouseCoopers LLP. That review has identified a number of improperly recorded transactions totaling approximately $730 thousand, which are included in selling and marketing, general and administrative, and other expenses for the second quarter of fiscal 2005. Due to the fact that the quantification of these items have only recently come to light, the Company expects to file its Form 10-Q for the second quarter of fiscal 2005 with the Securities and Exchange Commission within the 5-day extension period allowed by SEC Rule 12b-25.

* * *

“In general we are pleased with our progress in the quarter regarding gross margin improvement, Galileo orders and our overall strategy in growing the business” said Edward L. Gallup, Chairman and Chief Executive Officer. “However we are obviously disappointed with the number of unusual charges experienced in the quarter.”

Dr. Gioacchino De Chirico, President said, “Sales of our Galileo high volume instrument were very strong in the United States and Japan. During the quarter, 9 Galileo instrument sales met the criteria for revenue recognition – 5 in the United States and 4 in Japan. To date we have received binding purchase orders for 49 Galileo instruments in North America; almost 35% of these purchase orders will result in competitive takeaways. We are very proud of the job our sales team has done in converting leads into orders. Demand for our Galileo high volume instrument continues to be robust in the European market. Today there are 190 Galileo placements worldwide: 168 in Europe, 13 in North America of which six have been recorded as sales in the first six months of the fiscal year, and 9 in Japan.”

Commenting further, Dr. De Chirico stated, “Based on our current view of the business we are raising our revenue and earnings guidance

- 10 -

for the year. We now believe we will have 60 Galileo instruments installed in North America by the end of our fiscal year. Based on the strong demand for Galileo we have begun to increase the number of installation personnel.”

* * *

2005 Guidance

The following guidance reflects Immucor’s expectations as of January 7, 2005 and is being provided so that the Company can discuss its future outlook during its upcoming conference call with investors, potential investors, the media, financial analysts and others. These forward-looking statements are subject to the cautionary paragraph at the end of this press release and assume that the factors mentioned in that paragraph will not have a material impact on expected results. Investors are cautioned against attributing undue certainty to management’s assessment of the future and that actual results could differ. The Company does not intend to update its outlook until its third quarter earnings announcement, which is tentatively planned for early-April 2005.

The Company expects revenues for the fiscal year ending May 31, 2005 to range from $138 million to $143 million, an increase of approximately 22% to 27% over fiscal 2004 revenues. Gross margin is expected to be in the range of 58% to 59%. Net income is expected to be in the range of $24.6 million to $26.0 million, an approximate 96% to 108% increase over fiscal 2004. We expect to generate earnings per diluted share in the range of $0.51 to $0.55 for the fiscal year. We base our projections on our history of operations and experience, the recurring nature of our revenues, including contractually committed purchases from large customers, and the predictability of our expenses through the fiscal year. In making this projection, management has made the following assumptions:

With respect to revenues, the Company has extrapolated recent past results and assumed the Company will generate additional revenues from the renewal of customer contracts at higher prices, the continuing

- 11 -

sales of ABS2000 in the United States, the continuing sales of the Galileo instrument in Europe and new Galileo sales in Japan and the United States, the associated reagent growth associated with these instrument placements, and sales of the human collagen product. The Company has also assumed 2005 sales of human collagen to range between $3.0 million and $4.0 million.

22. The Company’s stock reacted favorably to these announcements and

within the hour of the announcement was trading above $26.15 per share. Defendants

needed to report favorable results to support their past statements about the success of

Immucor.

23. On April 6, 2005, the Company issued a press release entitled “Immucor

Announces Record Third Quarter Results; Provides Fiscal 2006 Guidance.” The press

release stated in part:

Immucor, Inc., the global leader in providing automated instrument-reagent systems to the blood transfusion industry, today reported financial results for the fiscal third quarter ended February 28, 2005, revised its guidance for the fiscal year 2005 and provided guidance for the fiscal year 2006.

Revenue for the fiscal third quarter was a record $38.0 million, up 36.3% from $27.9 million in the same period last year. Of the $10.1 million total increase in revenues, approximately $5.1 million came from price increases, approximately $4.6 million came from volume increases, and $0.4 million came from the effect of the change in the Euro exchange rate. Gross margin (i.e., gross profit as a percent of sales) improved during the quarter to 63.1% up from 52.9 % in the prior year quarter. This increase was driven by price increases in the United States, increased sales of Capture® products, and increased manufacturing efficiencies due in part to the consolidation of the manufacture of red blood cell products into the Norcross facility.

- 12 -

Net income for the third quarter was $6.5 million versus net income of $2.0 million for the same quarter last year. Diluted earnings per share totaled $0.14 on 47.6 million weighted average shares outstanding compared to $0.04 on 47.1 million weighted average shares outstanding for the same quarterly period last year. Prior year share and per share amounts have been adjusted to reflect the 3-for-2 stock splits affected in the form of 50% stock dividends which were distributed on July 16, 2004 and December 13, 2004.

* * *

General and administrative expenses for the quarter ended February 28, 2005, rose approximately $2.9 million over the same period ended February 29, 2004. The quarter increase was due in part to legal and professional fees of approximately $1.1 million associated with the previously-announced investigation by public prosecutors in Milan, Italy and the internal investigation initiated by the Company in response to the Italian investigation. Higher audit and tax fees, due in large part to Sarbanes-Oxley Section 404 internal control assessment, also contributed $0.9 million to the overall rise in these expenses.

* * *

“We are extremely pleased with our quarterly and year-to-date results,” said Edward L. Gallup, Chairman and Chief Executive Officer. “All-time highs were achieved in revenues, gross margin, income from operations, and net income for both the three-month and the nine-month periods ended February 28, 2005. We look forward to continuing this momentum into fiscal 2006.”

Dr. Gioacchino De Chirico, President said, “Our revenue-growing and margin-expansion strategies are working. Demand for our Galileo high volume instrument continues to be robust in the European market and is continuing to build in the U.S. and Japanese markets. Today there are 231 Galileo placements worldwide: 182 in Europe, 38 in North America of which 15 have been recorded as sales in the first nine months of the fiscal year, and 11 in Japan.”

- 13 -

Commenting further, Dr. De Chirico stated, “We are pleased that the pricing increases are occurring earlier than expected. Based on the reagent price increases affected by the termination in January of two large group purchasing contracts, we are revising our 2005 revenue and gross margin guidance upward.”

* * *

2005 Guidance

The following guidance reflects Immucor’s expectations as of April 6, 2005 and is being provided so that the Company can discuss its future outlook during its upcoming conference call with investors, potential investors, the media, financial analysts and others. These forward-looking statements are subject to the cautionary paragraph at the end of this press release and assume that the factors mentioned in that paragraph will not have a material impact on expected results. Investors are cautioned against attributing undue certainty to management’s assessment of the future and that actual results could differ.

The Company expects revenues for the fiscal year ending May 31, 2005 to range from $143.0 million to $146.0 million, an increase of approximately 26.5% to 29.2% over fiscal 2004 revenues. Gross margin is expected to be in the range of 60% to 61%. Net income is expected to be in the range of $25.5 million to $26.0 million, an approximate 103.4% to 108.0% increase over fiscal 2004. We expect to generate earnings per diluted share in the range of $0.54 to $0.55 for the fiscal year. We base our projections on our history of operations and experience, the recurring nature of our revenues, including contractually committed purchases from large customers, and the predictability of our expenses through the fiscal year. In making this projection, management has made the following assumptions:

With respect to revenues, the Company has extrapolated recent past results and assumed the Company will generate additional revenues from the renewal of customer contracts at higher prices, the continuing sales of ABS2000 in the United States, the continuing sales of the Galileo instrument in Europe and new Galileo sales in Japan and the

- 14 -

United States, the associated reagent growth associated with these instrument placements, and sales of the human collagen product.

With respect to operating expenses the Company believes that professional fees associated with the ongoing Italian investigation will contribute an additional $750,000 in expense over the balance of the fiscal year. In addition, based upon our estimate of the fourth quarter it now appears that certain Company managers will earn a bonus for fiscal 2005. This bonus will be the first paid since fiscal 2002.

With respect to diluted earnings per share, the Company’s projection assumes that there will not be additional capital stock issued.

2006 Outlook

The following guidance reflects Immucor’s expectations as of April 6, 2005 and is being provided so that the Company can discuss its future outlook during its upcoming conference call with investors, potential investors, the media, financial analysts and others. These forward-looking statements are subject to the cautionary paragraph at the end of this press release and assume that the factors mentioned in that paragraph will not have a material impact on expected results. Investors are cautioned against attributing undue certainty to management’s assessment of the future and that actual results could differ. The Company does not intend to update its outlook until its year-end earnings announcement, which is tentatively planned for early-August 2005.

The Company expects revenues for the fiscal year ended May 31, 2006 to range from $181 million to $195 million, an increase of approximately 26.6% to 33.6% over expected fiscal 2005 revenues. Gross margin is expected to be in the range of 65% to 66%. Net income is expected to be in the range of $45.2 million to $50.0 million an approximate 77.3% to 92.3% increase over expected fiscal 2005 net income. We expect to generate record earnings per diluted share in the range of $0.95 to $1.05 for the fiscal year. We base our projections on our history of operations and experience, the recurring nature of our revenues, including contractually committed purchases from large customers, and the predictability of our expenses through the fiscal year.

- 15 -

In making this projection, management has made the following assumptions:

With respect to revenues, the Company has extrapolated recent past results and assumed the Company will generate additional revenues from the renewal of customer contracts at higher prices; the continuing sales of ABS2000 in the United States; the continuing sales of the Galileo instrument in Europe, Japan and the United States; the associated reagent growth associated with these instrument placements; and the continuing sales of the human collagen product.

24. On August 3, 2005, the Company issued a press release entitled

“Immucor Announces Record Fiscal Fourth Quarter and Record Year End Results.”

The press release stated in part:

Immucor, Inc., the global leader in providing automated instrument-reagent systems to the blood transfusion industry, today reported financial results for the fiscal fourth quarter and year ended May 31, 2005 and provided updated guidance for the fiscal year 2006.

Revenue for the fiscal fourth quarter was a record $42.1 million, up 39.2% from $30.2 million in the same period last year. Of the $11.8 million total increase in revenues, approximately $9.8 million came from price increases, approximately $1.5 million came from volume increases, and $0.5 million came from the effect of the change in the Euro exchange rate. The impact of a recent change in interpretation of EITF Issue No. 00-21 reduced revenues and gross margins by $2.6 million. Gross margin (i.e., gross profit as a percent of sales) improved during the quarter to 64.4% up from 56.7% in the prior year quarter. This increase was driven by price increases in the United States, increased sales of Capture® products, and increased manufacturing efficiencies due in part to the consolidation of the manufacture of red blood cell products into the Norcross facility.

Net income for the fourth quarter was a record $9.2 million versus net income of $3.4 million for the same quarter last year. Diluted

- 16 -

earnings per share totaled $0.19 on 47.7 million weighted average shares outstanding compared to $0.07 on 47.4 million weighted average shares outstanding for the same quarterly period last year. Prior year share and per share amounts have been adjusted to reflect the 3-for-2 stock splits affected in the form of 50% stock dividends which were distributed on July 16, 2004 and December 13, 2004.

* * *

General and administrative expenses for the quarter ended May 31, 2005, rose by approximately $2.1 million over the quarter ended May 31, 2004. Higher audit and consulting fees, due in large part to Sarbanes-Oxley Section 404 internal control assessment, contributed $1.3 million to the overall rise in these expenses. The quarter increase was due in part also to legal and professional fees of approximately $0.3 million associated with the previously-announced investigation by public prosecutors in Milan, Italy and the internal investigation initiated by the Company in response to the Italian investigation.

For the year ended May 31, 2005, revenues totaled a record $144.8 million, a 28.6% increase over the prior year. Net income was $24.9 million, a $12.3 million increase over the prior year. Diluted earnings per share totaled $0.52 on 47.6 million weighted average shares outstanding for the year ended May 31, 2005 as compared to diluted earnings per share of $0.27 on 47.0 million weighted average shares outstanding for the prior year.

“Overall we are very pleased with our results, particularly those for this last quarter of fiscal 2005,” said Edward L. Gallup, Chairman and Chief Executive Officer. “The fourth quarter represented another all-time record high for us in revenues, gross margin, income from operations, and net income. Record highs in these areas were also achieved for the year ended May 31, 2005, with net income almost doubling from that of fiscal 2004. We continue to be excited about our Company’s future going into fiscal 2006 and beyond.”

Dr. Gioacchino De Chirico, President said, “Our strategies to grow our business in terms of both revenues and gross margin have been quite

- 17 -

successful to date. Demand for our Galileo® high volume instrument has continued to build in our primary markets. As of May 31, 2005, we have 251 Galileo® placements worldwide: 190 in Europe, 59 in North America and 2 in Japan. We previously reported 11 placements in Japan but have learned that nine of the Galileo® instruments sold to our former Japanese distributor were either held in inventory or were being evaluated by potential customers. These nine instruments are expected to be transferred to our new majority-owned affiliate – Immucor-Kainos, Inc. – by the end of the first quarter of fiscal 2006.”

Commenting further, Dr. De Chirico stated, “As of May 31, 2005, 191 of the 251 placed Galileo® instruments were generating reagent revenues. Although we are quite pleased with the number of Galileo® instruments placed to date, we are disappointed in the length of time our customers are taking to validate these instruments. Based on feedback from our sales and technical support staffs, the significant lag time we are experiencing appears to be, in almost all cases, due to the customer’s lack of committed internal resources resulting from a lack of priority to validate in a timely manner. Therefore, we have adopted two strategies to induce more timely instrument validation. First, we have agreed to contribute $3,000 to the education fund of any hospital who validates a Galileo® within 60 days after installation. Second, all future instrument contracts will stipulate that shipment and billing of the committed reagent volumes will begin 60 days after installation, whether or not the instrument has been validated. We strongly believe these new strategies will achieve the desired results. We are updating our fiscal 2006 revenue guidance to include the impact of the acquisition of Immucor-Kainos, Inc. – our new majority-owned subsidiary. Based on our current pricing plan as well as the impact of EITF Issue No. 00-21 and the delays encountered regarding Galileo® validations, we believe almost 58% of revenues and earnings will occur in the second half of the fiscal 2006. The second half of fiscal 2006 will also include the full impact of the acquisition of Immucor-Kainos, Inc.”

- 18 -

25. On August 12, 2005, defendant Kishel resigned, at the request of the

Board of Directors due to a possible violation of the Company’s insider trading

policies.

26. On August 26, 2005, the Company announced that the Securities and

Exchange Commission (“SEC”) had commenced a formal investigation relative to

payments made by one of the Company’s foreign subsidiaries to individuals

associated with government medical facilities.

27. Then, on August 29, 2005, after the market closed, the Company

announced that it had revised its net income for fiscal 2005 to account for a previously

unrecorded accrual for employee bonuses and furthermore made an announcement

that it had accepted the resignation of defendant Ramsey from the post of Chief

Financial Officer. The release stated in part:

Immucor, Inc., a global leader in providing automated instrument-reagent systems to the blood transfusion industry, today announced a revision in previously-reported net income for fiscal year 2005 to account for a previously-unrecorded accrual for employee bonuses. On an after-tax basis, the accrual for the third fiscal quarter is $0.2 million and the accrual for the fourth fiscal quarter is $0.7 million, for an aggregate bonus accrual of $0.9 million for the fiscal year. As revised, for the year and fourth quarter ended May 31, 2005, net income was $23.9 million for the year and $8.5 million for the fourth quarter; and diluted earnings per share were $0.50 for the year on 47.6 million weighted average shares outstanding, and $0.18 for the fourth quarter on 47.7 million weighted average shares outstanding.

- 19 -

The Company expects to report those revised numbers in its Form 10-K for fiscal year 2005. However, due to the additional accounting and auditing procedures to be completed to account for the bonus accrual, in addition to completing the procedures required by Section 404 of Sarbanes Oxley, the Company now does not expect to file that Form 10-K by August 30, 2005, as previously stated in its Form 12b-25 filed August 15, 2005. The Company is working diligently to have the Form 10-K filed as soon as possible.

The Company also reported that it has accepted the resignation of Steven C. Ramsey as Chief Financial Officer of the Company. Patrick Waddy, the Company’s Vice President of Finance, has accepted the position of interim Chief Financial Officer. Mr. Waddy has been with Immucor since 1996, when the Company acquired Dominion Biologicals, and Mr. Waddy retains the position of President of that company.

28. On this news, the Company’s shares fell $3.54 per share, or 12.85%, to

$24 per share on volume of 6.2 million shares.

29. The true facts, which were known by each of the defendants but

concealed from the investing public during the Class Period, were as follows:

(a) the Company lacked the necessary personnel and controls to issue

accurate financial reports and projections and to prevent insider trading violations by

its officers and directors; and

(b) the Company’s financial statements were presented in violation of

GAAP as described herein.

- 20 -

IMMUCOR’S FALSE FINANCIAL REPORTING DURING THE CLASS PERIOD

30. In order to inflate the price of Immucor’s stock, defendants caused the

Company to falsely report its results for its Q3 fiscal 2005 through Q4 fiscal 2005

through improper accounting for bonuses to employees.

31. The Q3 fiscal 2005 through Q4 fiscal 2005 results were included in press

releases disseminated to the public and a Form 10-Q as to the Q3 fiscal 2005 result.

32. Immucor has now admitted that it inappropriately failed to record

bonuses in its Q3 fiscal 2005 through Q4 fiscal 2005 results, and will revise its

financial results for those quarters.

33. GAAP are those principles recognized by the accounting profession as

the conventions, rules and procedures necessary to define accepted accounting

practice at a particular time. SEC Regulation S-X (17 C.F.R. §210.4-01(a)(1)) states

that financial statements filed with the SEC which are not prepared in compliance

with GAAP are presumed to be misleading and inaccurate, despite footnote or other

disclosure. Regulation S-X requires that interim financial statements must also

comply with GAAP, with the exception that interim financial statements need not

include disclosure which would be duplicative of disclosures accompanying annual

financial statements. 17 C.F.R. §210.10-01(a).

- 21 -

34. The fact that Immucor will restate its financial statements is an admission

that (i) the financial statements originally issued were materially false and misleading;

and (ii) the Q3 fiscal 2005 and Q4 fiscal 2005 financial statements disseminated

during the Class Period were incorrect based on information available to defendants at

the time the results were originally reported. Pursuant to GAAP, as set forth in

Accounting Principles Board Opinion (“APB”) No. 20, the type of restatement

announced by Immucor was to correct for material errors in its previously issued

financial statements. See APB No. 20, ¶¶7-13. As recently noted by the SEC,

“GAAP only allows a restatement of prior financial statements based upon

information ‘that existed at the time the financial statements were prepared,’” and

“restatements should not be used to make any adjustments to take into account

subsequent information that did not and could not have existed at the time the original

financial statements were prepared.”1 The Accounting Principles Board has defined

the kind of “errors” that may be corrected through a restatement: “‘Errors in financial

statements result from mathematical mistakes, mistakes in the application of

accounting principles, or oversight or misuse of facts that existed at the time that the 1 In re Sunbeam Sec. Litig., No. 98-8258-Civ.-Middlebrooks, SEC Amicus Curiae Brief regarding Defendants’ Motions In Limine to Exclude Evidence of the Restatement and the Restatement Report (S.D. Fla., filed Jan. 31, 2002).

- 22 -

financial statements were prepared.’” See APB No. 20, ¶13. The restatement at

issue here was not due to a simple mathematical error, honest misapplication of a

standard or oversight as alleged below, it was due to intentional misuse of the facts

that were known at the time.

35. The SEC has recently reiterated its position that in its investigations of

restated financial statements it often finds that the persons responsible for the

improper accounting acted with scienter:

[T]he Commission often seeks to enter into evidence restated financial statements, and the documentation behind those restatements, in its securities fraud enforcement actions in order, inter alia, to prove the falsity and materiality of the original financial statements [and] to demonstrate that persons responsible for the original misstatements acted with scienter.

In re Sunbeam Sec. Litig., No. 98-8258-Civ.-Middlebrooks, SEC Amicus Curiae Brief

regarding Defendants’ Motions In Limine to Exclude Evidence of the Restatement and

Restatement Report (S.D. Fla., filed Jan. 31, 2002).

36. Due to these accounting improprieties, the Company presented its

financial results and statements in a manner which violated GAAP, including the

following fundamental accounting principles:

(a) The principle that interim financial reporting should be based upon

the same accounting principles and practices used to prepare annual financial

statements was violated (APB No. 28, ¶10);

- 23 -

(b) The principle that financial reporting should provide information

that is useful to present and potential investors and creditors and other users in making

rational investment, credit and similar decisions was violated (FASB Statement of

Concepts No. 1, ¶34);

(c) The principle that financial reporting should provide information

about the economic resources of an enterprise, the claims to those resources, and

effects of transactions, events and circumstances that change resources and claims to

those resources was violated (FASB Statement of Concepts No. 1, ¶40);

(d) The principle that financial reporting should provide information

about how management of an enterprise has discharged its stewardship responsibility

to owners (stockholders) for the use of enterprise resources entrusted to it was

violated. To the extent that management offers securities of the enterprise to the

public, it voluntarily accepts wider responsibilities for accountability to prospective

investors and to the public in general (FASB Statement of Concepts No. 1, ¶50);

(e) The principle that financial reporting should provide information

about an enterprise’s financial performance during a period was violated. Investors

and creditors often use information about the past to help in assessing the prospects of

an enterprise. Thus, although investment and credit decisions reflect investors’

expectations about future enterprise performance, those expectations are commonly

- 24 -

based at least partly on evaluations of past enterprise performance (FASB Statement

of Concepts No. 1, ¶42);

(f) The principle that financial reporting should be reliable in that it

represents what it purports to represent was violated. That information should be

reliable as well as relevant is a notion that is central to accounting (FASB Statement

of Concepts No. 2, ¶¶58-59);

(g) The principle of completeness, which means that nothing is left out

of the information that may be necessary to insure that it validly represents underlying

events and conditions was violated (FASB Statement of Concepts No. 2, ¶79); and

(h) The principle that conservatism be used as a prudent reaction to

uncertainty to try to ensure that uncertainties and risks inherent in business situations

are adequately considered was violated. The best way to avoid injury to investors is to

try to ensure that what is reported represents what it purports to represent (FASB

Statement of Concepts No. 2, ¶¶95, 97).

37. Further, the undisclosed adverse information concealed by defendants

during the Class Period is the type of information which, because of SEC regulations,

regulations of the national stock exchanges and customary business practice, is

expected by investors and securities analysts to be disclosed and is known by

- 25 -

corporate officials and their legal and financial advisors to be the type of information

which is expected to be and must be disclosed.

LOSS CAUSATION/ECONOMIC LOSS

38. During the Class Period, as detailed herein, defendants engaged in a

scheme to deceive the market and a course of conduct that artificially inflated

Immucor’s stock price and operated as a fraud or deceit on Class Period purchasers of

Immucor stock by misrepresenting the Company’s financial results, business success

and future business prospects. Defendants achieved this façade of success, growth

and strong future business prospects by blatantly misrepresenting the Company’s

accounting and falsifying the Company’s financial statements. Later, however, when

defendants’ prior misrepresentations and fraudulent conduct were disclosed and

became apparent to the market, Immucor stock fell precipitously as the prior artificial

inflation came out of Immucor’s stock price. As a result of their purchases of

Immucor stock during the Class Period, plaintiff and other members of the Class

suffered economic loss, i.e., damages, under the federal securities laws.

39. By misrepresenting Immucor’s financial statements and its future

earnings, the defendants presented a misleading picture of Immucor’s business and

prospects. Thus, instead of truthfully disclosing during the Class Period that

- 26 -

Immucor’s business was not as healthy as represented, Immucor falsely overstated its

net income.

40. These claims of profitability caused and maintained the artificial inflation

in Immucor’s stock price throughout the Class Period and until the truth was revealed

to the market.

41. Defendants’ false and misleading statements had the intended effect and

caused Immucor stock to trade at artificially inflated levels throughout the Class

Period, reaching as high as $34.98 per share.

42. On August 29, 2005, Immucor reported that its 2005 results would be

worse than expectations due to miscalculations on accrual of employee bonuses. As

investors and the market became aware that Immucor’s prior financial statements had

been falsified and that Immucor’s actual business prospects were, in fact, poor, the

prior artificial inflation came out of Immucor’s stock price, damaging investors.

43. As a direct result of defendants’ admissions and the public revelations

regarding the truth about Immucor’s misstatements and its actual business prospects

going forward, Immucor’s stock price plummeted 12.85%, falling from $27.54 on

August 29, 2005 to $24 per share on August 30, 2005, a one-day drop of $3.54 per

share. This drop removed the inflation from Immucor’s stock price, causing real

economic loss to investors who had purchased the stock during the Class Period. In

- 27 -

sum, as the truth about defendants’ fraud and Immucor’s business performance was

revealed, the Company’s stock price plummeted, the artificial inflation came out of

the stock and plaintiff and other members of the Class were damaged, suffering

economic losses of up to $3.54 per share.

44. The decline in Immucor’s stock price at the end of the Class Period was a

direct result of the nature and extent of defendants’ fraud finally being revealed to

investors and the market. The timing and magnitude of Immucor’s stock price

declines negate any inference that the loss suffered by plaintiff and other Class

members was caused by changed market conditions, macroeconomic or industry

factors or Company-specific facts unrelated to the defendants’ fraudulent conduct.

During the same period in which Immucor’s stock price fell 12.85% from $27.54 per

share as a result of defendants’ fraud being revealed, the Standard & Poor’s 500

securities index was flat. The economic loss, i.e., damages, suffered by plaintiff and

other members of the Class was a direct result of defendants’ fraudulent scheme to

artificially inflate Immucor’s stock price and the subsequent significant decline in the

value of Immucor’s stock when defendants’ prior misrepresentations and other

fraudulent conduct was revealed.

- 28 -

COUNT I

For Violation of §10(b) of the 1934 Act and Rule 10b-5 Against All Defendants

45. Plaintiff incorporates ¶¶1-44 by reference.

46. During the Class Period, defendants disseminated or approved the false

statements specified above, which they knew or deliberately disregarded were

misleading in that they contained misrepresentations and failed to disclose material

facts necessary in order to make the statements made, in light of the circumstances

under which they were made, not misleading.

47. Defendants violated §10(b) of the 1934 Act and Rule 10b-5 in that they:

(a) employed devices, schemes and artifices to defraud;

(b) made untrue statements of material facts or omitted to state

material facts necessary in order to make the statements made, in light of the

circumstances under which they were made, not misleading; or

(c) engaged in acts, practices and a course of business that operated as

a fraud or deceit upon plaintiff and others similarly situated in connection with their

purchases of Immucor common stock during the Class Period.

48. Plaintiff and the Class have suffered damages in that, in reliance on the

integrity of the market, they paid artificially inflated prices for Immucor common

stock. Plaintiff and the Class would not have purchased Immucor common stock at

- 29 -

the prices they paid, or at all, if they had been aware that the market prices had been

artificially and falsely inflated by defendants’ misleading statements.

49. As a direct and proximate result of these defendants’ wrongful conduct,

plaintiff and the other members of the Class suffered damages in connection with their

purchases of Immucor common stock during the Class Period.

COUNT II

For Violation of §20(a) of the 1934 Act Against All Defendants

50. Plaintiff incorporates ¶¶1-49 by reference.

51. The Individual Defendants acted as a controlling persons of Immucor

within the meaning of §20(a) of the 1934 Act. By reason of their positions as officers

and/or directors of Immucor, and their ownership of Immucor stock, the Individual

Defendants had the power and authority to cause Immucor to engage in the wrongful

conduct complained of herein. Immucor controlled the Individual Defendants and all

of its employees. By reason of such conduct, defendants are liable pursuant to §20(a)

of the 1934 Act.

CLASS ACTION ALLEGATIONS

52. Plaintiff brings this action as a class action pursuant to Rule 23 of the

Federal Rules of Civil Procedure on behalf of all persons who purchased Immucor

- 30 -

common stock (the “Class”) on the open market during the Class Period. Excluded

from the Class are defendants.

53. The members of the Class are so numerous that joinder of all members is

impracticable. The disposition of their claims in a class action will provide substantial

benefits to the parties and the Court. Immucor has more than 45 million shares of

stock outstanding, owned by hundreds if not thousands of persons.

54. There is a well-defined community of interest in the questions of law and

fact involved in this case. Questions of law and fact common to the members of the

Class which predominate over questions which may affect individual Class members

include:

(a) whether the 1934 Act was violated by defendants;

(b) whether defendants omitted and/or misrepresented material facts;

(c) whether defendants’ statements omitted material facts necessary to

make the statements made, in light of the circumstances under which they were made,

not misleading;

(d) whether defendants knew or deliberately disregarded that their

statements were false and misleading;

(e) whether the price of Immucor’s common stock was artificially

inflated; and

- 31 -

(f) the extent of damage sustained by Class members and the

appropriate measure of damages.

55. Plaintiff’s claims are typical of those of the Class because plaintiff and

the Class sustained damages from defendants’ wrongful conduct.

56. Plaintiff will adequately protect the interests of the Class and has retained

counsel who are experienced in class action securities litigation. Plaintiff has no

interests which conflict with those of the Class.

57. A class action is superior to other available methods for the fair and

efficient adjudication of this controversy.

PRAYER FOR RELIEF

WHEREFORE, plaintiff prays for judgment as follows:

A. Declaring this action to be a proper class action pursuant to Fed. R. Civ.

P. 23;

B. Awarding plaintiff and the members of the Class damages, including

interest;

C. Awarding plaintiff’s reasonable costs, including attorneys’ fees; and

D. Awarding such equitable/injunctive or other relief as the Court may deem

just and proper.

- 32 -

JURY DEMAND

Plaintiff demands a trial by jury.

DATED: September __, 2005 CHITWOOD HARLEY HARNES LLP

MARTIN D. CHITWOOD Georgia State Bar No. 124950 2300 Promenade II 1230 Peachtree Street, N.E. Atlanta, GA 30309 Telephone: 404/873-3900 404/876-4476 (fax)

LERACH COUGHLIN STOIA GELLER RUDMAN & ROBBINS LLP WILLIAM S. LERACH DARREN J. ROBBINS 401 B Street, Suite 1600 San Diego, CA 92101-4297 Telephone: 619/231-1058 619/231-7423 (fax)

Attorneys for Plaintiff