united states district court district of nevada · 2013-07-23 · las vegas, nevada 89148 ....

TRANSCRIPT

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

JOSHUA M. DICKEY Bailey Kennedy, LLP Nevada Bar No. 8984 Spanish Ridge Ave. Las Vegas, Nevada 89148 Telephone: (702) 562-8820 Facsimile: (702) 562-8821 Email: [email protected] CONLY SCHULTE Fredericks Peebles & Morgan LLP 1900 Plaza Drive Louisville, CO 80027 Telephone: (303) 673-9600 Facsimile: (303) 673-9155 Email: [email protected]

Attorneys for Defendants AMG Services, Inc.; Red Cedar Services, Inc.; SFS, Inc.; MNE Services, Inc. Additional Counsel Listed on Following Page

UNITED STATES DISTRICT COURT

DISTRICT OF NEVADA

FEDERAL TRADE COMMISSION,

Plaintiff,

v.

AMG Services, Inc., et al.,

Defendants, and

Park 269 LLC, et al.,

Relief Defendants.

Case No.: 2:12-cv-536-GMN-(VCF)

TRIBAL DEFENDANTS’ OPPOSITION TO PLAINTIFF’S AMENDED MOTION

FOR PARTIAL SUMMARY JUDGMENT

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 1 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Additional Counsel SHILEE MULLIN Fredericks Peebles & Morgan LLP 3610 North 163rd Plz. Omaha, NE 68116 Telephone: (402) 333-4053 Facsimile: (402) 333-4761 Email: [email protected] JOHN NYHAN FREDERICKS PEEBLES & MORGAN LLP 2020 L St., Suite 250 Sacramento, CA 95811 Telephone: (916) 441-2700 Facsimile: (916) 441-2067 Email: [email protected] Attorneys for Defendants AMG Services, Inc.; Red Cedar Services, Inc.; SFS, Inc.; MNE Services, Inc.

BRADLEY WEIDENHAMMER RUSH HOWELL MATTHEW MELTZER DEBRA LEFLER CHARLES KALIL ANDREW KASSOF KIRKLAND & ELLIS LLP 300 North LaSalle Chicago IL 60654 Telephone: (312) 862-2000 Facsimile: (312) 862-2200 Email: [email protected] [email protected] [email protected] [email protected] [email protected]

Attorneys for Defendants AMG Services, Inc.; MNE Services, Inc.

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 2 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

i

TABLE OF CONTENTS TABLE OF CONTENTS ................................................................................................................. i

TABLE OF AUTHORITIES .......................................................................................................... ii

I. Introduction ......................................................................................................................... 1

II. Statement of Genuine Issues in Opposition to Partial Motion for Summary Judgment ..... 1

III. Burden of Proof ................................................................................................................... 3

IV. Argument ............................................................................................................................ 4

A. Indian Tribes and Arms of Tribes Do Not Constitute “Persons, Partnerships or Corporations” As Defined by the FTC Act ........................................................ 5

B. The Indian Law Canons of Construction Dictate That Ambiguities In The Act Be Resolved in Favor Of Indian Tribes ................................................................ 10

C. The FTC Relies on a False Presumption that Laws of General Applicability Apply to Indian Tribes. ......................................................................................... 12

D. The FTC Act Is Not A Law of General Applicability .......................................... 14

E. The Legal Determination of Whether the FTC Act Applies to Indian Tribes Cannot Be Determined By So-Called “Admissions” ............................................ 17

V. Conclusion ........................................................................................................................ 21

CERTIFICATE OF SERVICE ..................................................................................................... 23

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 3 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

ii

TABLE OF AUTHORITIES

Cases Allen v. Gold County Casino, 464 F.3d 1044 (9th Cir. 2006)............................................................ 11 Am. Cyanamid Co. v. FTC, 363 F.2d 757 (1966) .............................................................................. 16 California v. Ameriloan, BC373536 (Cal. Super. Ct. May 10, 2012) ............................................... 21 Celotex Corp. v. Catrett, 477 U.S. 317 (1986) .................................................................................... 4 Cmty. Blood Bank of Kansas City Area v. FTC, 405 F.2d 1011 (8th Cir. 1969) ....................... 4, 5, 15 Colorado v. Cash Advance, 05-CV1143 (Dist. Ct., City and County of Denver, Colo.

February 13, 2012) ........................................................................................................................ 21 County of Oneida v. Oneida Indian Nation, 470 U.S. 226 (1985) ..................................................... 11 County of Yakima v. Confederated Tribes and Bands of the Yakima Indian Nation, 502 U.S. 251

(1992) ............................................................................................................................................ 11 Donovan v. Coeur d’Alene Tribal Farm, 751 F.2d 1113 (9th Cir. 1985) ................................... passim Donovan v. Navaho Forest Products Indust., 692 F.2d 709 (10th Cir. 1982) ................................... 18 Equal Employment Opportunity Comm’n v. Cherokee Nation, 871 F.2d 937 (10th Cir. 1989) ........ 12 Fed. Power Comm’n v. Tuscarora Indian Nation, 362 U.S. 99 (1960) ............................. 4, 12, 13, 18 Fisher v. Dist. Ct., 424 U.S. 382 (1976) .............................................................................................. 9 FTC v. AmeriDebt, Inc., 343 F.Supp.2d 451 (D.Md. 2004) ................................................................ 4 Glick v. White Motor Co., 458 F.2d 1287 (3d Cir. 1972) .................................................................. 18 Idaho v. United States, 533 U.S. 262 (2001) ............................................................................... 13, 15 In re Whitaker, 474 B.R. 687 (B.A.R. 8th Cir. 2012) .......................................................................... 7 Inyo County v. Paiute-Shoshone Indians, 538 U.S. 701 (2003) .......................................................... 5 Kerr-McGee Corp. v. Navajo Tribe, 471 U.S. 195 (1985) .................................................................. 9 Kiowa Tribe of Okla v. Mfg. Techs., 523 U.S. 751 (1998) .................................................................. 7 Kohler v. Leslie Hindman, Inc., 80 F.3d 1181 (7th Cir. 1996) .......................................................... 20 Lumber Indus. Pension Fund. v. Warm Springs Forest Prods. Indus., 939 F.2d 683

(9th Cir. 1991) ......................................................................................................................... 14, 15

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 4 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

iii

McClanahan v. Ariz. State Tax Com’n, 411 U.S. 164 (1979) ............................................................ 11 Mescalero Apache Tribe v. Jones, 411 U.S. 145 (1973)...................................................................... 8 Miller v. Wright, -- F.3d --, 2013 WL 174493 (9th Cir. 2013) .................................................... 16, 17 Minn. v. Mille Lacs Band of Chippewa Indians, 526 U.S. 172 (1999) ........................................ 13, 15 N.L.R.B. v. Fortune Bay Resort Casino, 688 F.Supp.2d 858 (D. Minn. 2010) .................................. 17 National Labor Relations Board v. Chapa De Indian Health Program, Inc., 316 F.3d 995

(9th Cir. 2002) ............................................................................................................................... 15 Nero v. Cherokee Nation of Okla., 892 F.2d 1457 (10th Cir. 1989) .................................................. 12 Parker v. Brown, 317 U.S. 341 (1943) .............................................................................................. 17 Perry v. Serenity Behavioral Health Systems, No. 106-172, 2009 WL 1228446

(S.D. Ga. May 4, 2009) ................................................................................................................. 20 Pinebrook Minerals, LLC v. Anadarko E & P Co., LP, No. 11-00177, 2011 WL 3584783

(M.D. Pa. July 25, 2011) ............................................................................................................... 20 Rodriguez v. CHRISTUS Spohn Health System Corp., 874 F.Supp.2d 635 (S.D.Tex. 2012) ........... 20 Rutherford v. McComb, 331 U.S. 722 (1947) .................................................................................... 14 Santa Clara Pueblo v. Martinez, 436 U.S. 49 (1978) ................................................................. passim Snyder v. Navajo Nation, 382 F.3d 892 (9th Cir. 2004) .................................................................... 14 Solis v. Matheson, 563 F.3d 425 (9th Cir. 2009) ......................................................................... 14, 15 Stenberg v. Carhart, 530 U.S. 914 (2000) ........................................................................................... 6 Three Affiliated Tribes of Fort Berthold Reservation v. Wold Engineering, 476 U.S. 877 (1986) ..... 7 Town of Hallie v. City of Eau Claire, 471 U.S. 34 (1985) ................................................................. 17 U.S. Dep’t of Labor v. Occupational Safety & Health Review Comm’n, 935 F.2d 182

(9th Cir. 1991) ......................................................................................................................... 14, 15 United States v. Shoshone-Pauite Tribes, Duck Valley Indian Reservation, No. 2:10-CV-01890-

GMN, Dec. 26, 2012, 2012 WL 6725682 (D. Nev. 2012) .............................................................. 5 United States v. United States Fidelity & Guaranty Co., 309 U.S. 506 (1940) ................................... 7 Wachovia Bank v. Schmidt, 546 U.S. 303 (2006) ................................................................................ 6 Winnemucca Indian Colony v. U.S. ex. rel. Dep’t of Interior, 837 F.Supp. 2d 1184

(D. Nev. 2011) ............................................................................................................................... 18 Worcester v. Georgia, 31 U.S. 515 (1832) .......................................................................................... 9

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 5 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

iv

Statutes 15 U.S.C § 12 ..................................................................................................................................... 17 15 U.S.C. § 44 ...................................................................................................................................... 6 15 U.S.C. § 45 ................................................................................................................................ 5, 15 15 U.S.C. §§ 41-58 ................................................................................................................... 9, 10, 11 15 U.S.C. § 375 ................................................................................................................................ 6, 8 16 U.S.C. § 470 .................................................................................................................................... 7 25 U.S.C. §§ 461-479 ................................................................................................................. 8, 9, 16 25 U.S.C. § 2702 ................................................................................................................................ 19 25 U.S.C. § 4301 .................................................................................................................................. 8 28 U.S.C. § 516 (2006) ...................................................................................................................... 19 29 U.S.C. § 203 .................................................................................................................................. 15 29 U.S.C. § 652 .................................................................................................................................. 15 29 U.S.C. § 1002 ................................................................................................................................ 15 42 U.S.C. § 8802 .................................................................................................................................. 7 Other Authorities 6 Handbook of Fed. Evid. § 801:26 (7th ed.) .................................................................................... 18 65 Fed. Reg. 67,249 (Nov. 6, 2000) ..................................................................................................... 9 Angelique Eaglewoman, Tribal Nation Economics: Rebuilding Commercial prosperity in Spite of

U.S. Trade Restraint — Recommendations for Economic Revitalization in Indian Country, 44 Tulsa L. Rev. 383 (2008) ............................................................................................................... 16

Bryan H. Wildenthal, How the Ninth Circuit Overruled a Century of Supreme Court Indian

Jurisprudence — And Has So Far Gotten Away With It, 2008 MICH. ST. L. REV. 547 (2008) ...................................................................................................................................... 13, 18

F. COHEN, HANDBOOK OF FEDERAL INDIAN LAW, § 2101 (2012 ed.) .......................................... 10, 16 H.R. REP. NO. 73-1804 (1934) ............................................................................................................. 8 H.R. REP. NO. 533, 63d CONG., 2D SESS. (1914 ................................................................................. 16

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 6 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

v

H.R. REP. NO. 1142, 63d CONG., 2D SESS. (1914) ............................................................................. 16 Indian Citizenship Act of 1924, 43 Stat. 253 ..................................................................................... 10 S. REP. NO. 597, 63d CONG., 2D SESS. (1914) ................................................................................... 16 The Airline Deregulation Act of 1978, Pub. L. No. 95-504, 92 Stat. 1705 ....................................... 20 The Atomic Energy Act of 1946, Pub. L. No. 79-585, 60 Stat. 755 .................................................. 20

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 7 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

1

COME NOW Defendants, AMG Services, Inc.; Red Cedar Services, Inc.; SFS, Inc.; and

MNE Services, Inc. (hereinafter “Tribal Defendants”) and file this Opposition to the Federal Trade

Commission’s Amended Motion for Partial Summary Judgment.

I. Introduction Plaintiff, Federal Trade Commission (“FTC”), moved for partial summary judgment on the

averment that the FTC has authority to enforce the Federal Trade Commission Act (“FTC Act”),

Truth in Lending Act (“TILA”), and the Electronic Fund Transfer Act (“EFTA”) against the Tribal

Defendants. The FTC has conceded that all of its claims against the Tribal Defendants, including

its TILA and EFTA claims, are brought solely pursuant to its authority under the FTC Act. (E.g.,

Doc. 141 at 16.) The issue before the Court on the FTC’s Motion has nothing to do with the

underlying factual allegations in this case (see Doc. 339 at 1), but, as the FTC admits is “purely” a

legal argument. (Doc. 339 at 12.) It is the FTC’s burden to establish that the FTC Act is

applicable to the Tribal Defendants, and the FTC has not met its burden. For this reason, as set

forth fully below, the Tribal Defendants respectfully request that the Court deny the FTC’s

Motion.

II. Statement of Genuine Issues in Opposition to Partial Motion for Summary Judgment

Plaintiff’s Alleged Uncontroverted Facts

Tribal Defendants’ Response

Evidentiary Support

1. Defendants provide loans to and engage in collections activities involving consumers across the country.

1. Undisputed, with the exception of some states.

2. AMG is a shared services provider that runs customer service and collections operations, among other things, for the online payday lending businesses of MNES, Red Cedar, and SFS under the trade names (d/b/as):

2. Undisputed that AMG is a shared service provider that provides customer services and collections operations, inter alia, for MNES, Red Cedar and SFS under the trade names denominated and

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 8 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

2

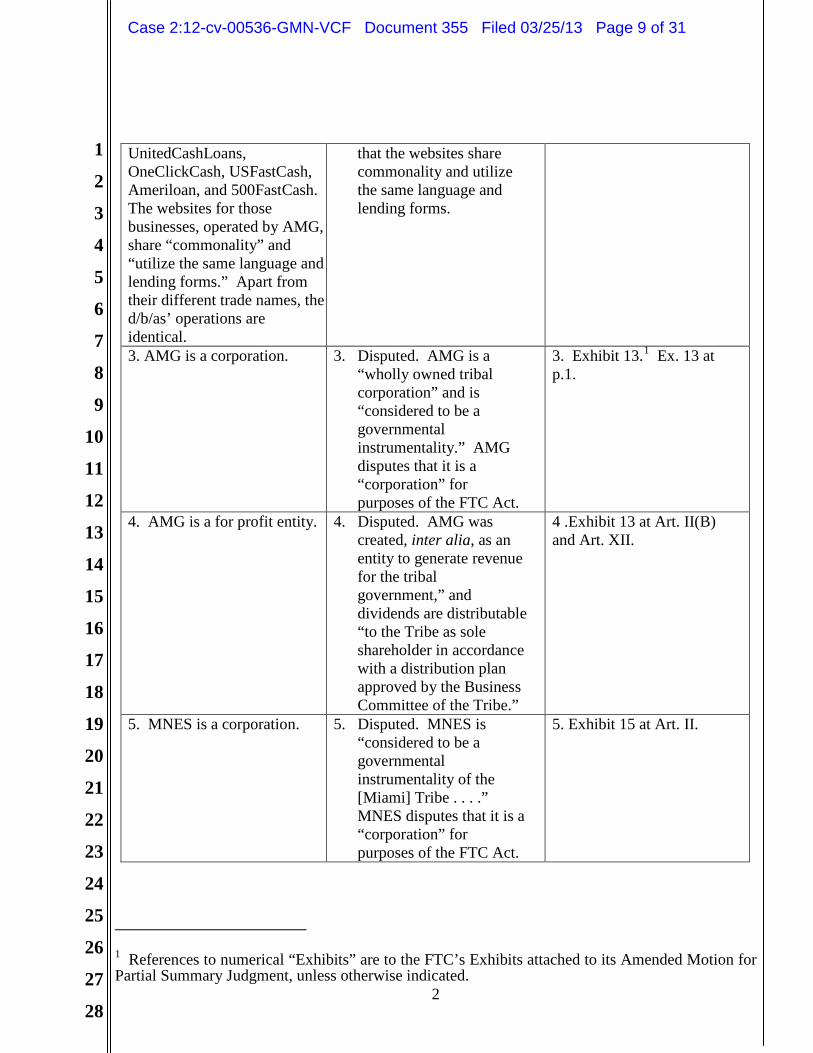

UnitedCashLoans, OneClickCash, USFastCash, Ameriloan, and 500FastCash. The websites for those businesses, operated by AMG, share “commonality” and “utilize the same language and lending forms.” Apart from their different trade names, the d/b/as’ operations are identical.

that the websites share commonality and utilize the same language and lending forms.

3. AMG is a corporation. 3. Disputed. AMG is a “wholly owned tribal corporation” and is “considered to be a governmental instrumentality.” AMG disputes that it is a “corporation” for purposes of the FTC Act.

3. Exhibit 13.1

4. AMG is a for profit entity.

Ex. 13 at p.1.

4. Disputed. AMG was created, inter alia, as an entity to generate revenue for the tribal government,” and dividends are distributable “to the Tribe as sole shareholder in accordance with a distribution plan approved by the Business Committee of the Tribe.”

4 .Exhibit 13 at Art. II(B) and Art. XII.

5. MNES is a corporation. 5. Disputed. MNES is “considered to be a governmental instrumentality of the [Miami] Tribe . . . .” MNES disputes that it is a “corporation” for purposes of the FTC Act.

5. Exhibit 15 at Art. II.

1 References to numerical “Exhibits” are to the FTC’s Exhibits attached to its Amended Motion for Partial Summary Judgment, unless otherwise indicated.

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 9 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

3

6. MNES is a for profit

entity. 6. Disputed. MNES is an

entity that was created, inter alia, to generate revenue for distribution to the tribal government.

6. Exhibit 15 at Art. II(B).

7. Red Cedar is a corporation. 7. Disputed. Red Cedar is “considered to be a governmental instrumentality of the [Modoc] Tribe . . . .” Red Cedar disputes that it is a “corporation” for purposes of the FTC Act.

7. Exhibit 18 at Art. III.

8. Red Cedar is a for profit entity.

8. Disputed. Red Cedar is an entity that was created, inter alia, to generate revenue for distribution to the tribal government.

8. Exhibit 18 at Art. III(B).

9. SFS is a corporation. 9. Disputed. SFS is “deemed an economic and political subdivision of the Santee Sioux Nation . . . .” SFS disputes that it is a “corporation” for purposes of the FTC Act.

9. Resolution 2005-27 of the Santee Sioux Nation, attached as Exhibit A to the Declaration of Shilee Mullin filed concurrently herewith.

. 10. SFS is a for profit entity. 10. Disputed. SFS is an entity that was created to “facilitate the achievement of goals relating to the Tribal economy, self-government, and sovereign status of the Santee Sioux Nation . . . .”

10. Ex. 21 at Art. 4.1

III. Burden of Proof The standards governing summary judgment are well-established and mandate that the

moving party, here the FTC, bear the initial burden of showing that there is an absence of any

genuine issue of material fact and that the moving party is entitled to judgment as a matter of law.

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 10 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

4

Celotex Corp. v. Catrett, 477 U.S. 317, 323 (1986). Also, when the FTC’s jurisdiction is

challenged, as it is here, the FTC bears the burden of establishing jurisdiction. Cmty. Blood Bank

of Kansas City Area v. FTC, 405 F.2d 1011, 1015 (8th Cir. 1969). Thus, it is the FTC’s burden to

establish that the FTC Act applies to the Tribal Defendants under applicable principles of statutory

construction, and/or that the Tribal Defendants qualify as a “person, partnership or corporation”

under the FTC Act. See id.; FTC v. AmeriDebt, Inc., 343 F.Supp.2d 451, 460 (D.Md. 2004).

IV. Argument

The FTC does not claim that the Tribal Defendants are “persons or partnerships”; but

instead mistakenly claims that Indian tribes and their entities— which are expressly granted the

sovereign powers of their respective sovereign Tribal governments — are the type of private

“corporations” that Congress intended to regulate when it enacted the FTC Act in 1914. As

demonstrated below, such assertion simply is not credible when considering federal policies and

the historical position that Indian tribes occupied in our nation’s economy at that time.

The FTC relies on an alleged presumption that laws of general applicability apply to Indian

tribes — yet it is clear that this presumption is false, for several reasons. First, the alleged

presumption is derived from the FTC’s misinterpretation of dicta from a Supreme Court decision

in Fed. Power Comm’n v. Tuscarora Indian Nation, 362 U.S. 99 (1960) — a misinterpretation that

is inconsistent with Supreme Court decisions both before and after Tuscarora. Second, even if the

Court’s dicta in Tuscarora should be given the force of law, this so-called presumption applies

solely to individual “Indians,” not sovereign Indian tribes or their subordinate governmental

entities. Third, even assuming the FTC’s misreading of Tuscarora (and the few lower courts that

have shared the FTC’s misreading) were correct, it would — at best — stand for the proposition

that federal laws of general applicability apply to Indian tribes. The FTC Act, however, by its

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 11 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

5

own terms, is not a law of general applicability, for, unlike many other statutes that truly are

generally applicable, the FTC Act expressly does not apply to many categories of legal entities. In

fact, by its own terms, the FTC Act applies (with gaping exceptions) only to “persons,

partnerships and [some] corporations.” In the event that, somehow, it is unclear whether the term

“corporation” could encompass an Indian tribe, the Indian canons of construction dictate the FTC

Act be interpreted in favor of Indian tribes.

For these reasons and others expressed herein, the Tribal Defendants respectfully request

that the Court deny the FTC’s Amended Motion for Partial Summary Judgment.

A. Indian Tribes and Arms of Tribes Do Not Constitute “Persons, Partnerships or Corporations” As Defined by the FTC Act

Under the express terms of the Act, the FTC only has authority to enforce the Act upon

“persons, partnerships or corporations” as defined in the Act, 15 U.S.C. § 45(a)(2),2 which clearly

does not encompass Indian tribes or arms of Indian tribes. The FTC assumes —without offering

any analysis — that the FTC Act applies to “tribes3

2 The FTC does not allege that the Tribal Defendants are “persons or partnerships” pursuant to 15 U.S.C. § 45(a)(2). Moreover, it is clear that the Tribal Defendants are not “persons.” Inyo County v. Paiute-Shoshone Indians, 538 U.S. 701, 709 (2003); United States v. Shoshone-Pauite Tribes, Duck Valley Indian Reservation, No. 2:10-CV-01890-GMN, Dec. 26, 2012, 2012 WL 6725682, * 2 (D. Nev. 2012).

or tribal businesses” because they constitute

“corporations” within the meaning of the FTC Act. (See Doc. 339 at 7, 12.) A thorough review of

3 The FTC’s seems to assert that the FTC Act applies to Indian tribes, as it states that there is no exception in the FTC Act for Indian tribes. (Doc. 339 at 12, 13.) This statement assumes that the FTC Act applies to Indian tribes and whether there is an exception in the FTC Act for Indian tribes misses the point. The FTC Act does not apply to Indian tribes to begin with. The FTC “has only such jurisdiction as Congress has conferred upon it by the Federal Trade Commission Act.” Cmty. Blood Bank of Kansas City Area v. F.T.C., 405 F.2d 1011, 1015 (1969). The Federal Trade Commission Act conferred the FTC jurisdiction only over “persons, partnerships, or corporations [with numerous exceptions] . . . .” 15 U.S.C. § 45(a)(2). The Tribal Entities contend that the FTC Act, on its face, does not apply to Indian tribes, as Indian tribes are not “persons, partnerships, or corporations.” The FTC has not argued that an Indian tribe is a partnership or a person, and has not provided any cogent argument for how an Indian tribe could be considered a corporation.

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 12 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

6

the definition of “Corporation” in 15 U.S.C. § 44, in conjunction with principles of statutory

construction and principles of Federal Indian law, reveals that the FTC’s conclusory assertions are

legally false (Doc. 39 at 12) — the tribal businesses do not fall within the Act’s rubric.

The Act provides that a “Corporation” is “any company, trust, so-called Massachusetts

trust, or association, incorporated or unincorporated, which is organized to carry on business for

its own profit or that of its members.” 15 U.S.C. § 44. Not only does this definition fail to include

tribal governmental subdivisions or sovereign entities on its face,4

Furthermore, contrary to the FTC’s assertion, it is absolutely irrelevant that there is “no

exception in the FTC Act for Indian tribes or tribal businesses.” (Doc. 339 at 12.) That is not the

question. See Santa Clara Pueblo v. Martinez, 436 U.S. 49, 58 (1978). The question is whether

the FTC Act purports to apply to tribal businesses to begin with. The issue of whether a federal

statute applies to Indian tribes and its businesses is considered in the milieu of decades of case law

and considerations of tribal sovereignty. Id. at 61 (stating that considerations of “Indian

but it also bears a stark contrast

to other federal statutes that differentiate between corporations and Indian tribes and their

subdivisions. See 15 U.S.C. § 375(10) (“The term ‘person’ means an individual, corporation,

company, association, firm, partnership, society, State government, local government, Indian

tribal government, governmental organization of such a government, or joint stock company.”

(emphasis added)). As 15 U.S.C. § 375(10) “address[es] the same subject matter generally” as the

FTC Act, namely, entities covered by the statute and involved in certain commercial transactions,

the two statutes should be read in pari materia. See Wachovia Bank v. Schmidt, 546 U.S. 303,

315-316 (2006) (citation and internal quotation marks omitted).

4 Even if this Court believed for some reason that Indian tribes can be considered corporations in the typical case, “[w]hen a statute includes an explicit definition . . . we must follow that definition, even if it varies from that term’s ordinary meaning.” Stenberg v. Carhart, 530 U.S. 914, 942 (2000).

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 13 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

7

sovereignty” are the backdrop against which the statute must be read). The United States Supreme

Court has reiterated that abrogation of Tribal rights by Congress “cannot be implied,” but must be

“unequivocally expressed” (Santa Clara Pueblo, 436 U.S. at 58) in “explicit legislation” (see

Kiowa Tribe of Okla v. Mfg. Techs., 523 U.S. 751, 756-59 (1998).5

Still more to the point in this case, Congress has shown the ability to encompass tribal

instrumentalities that take the form of corporations. See, e.g., 16 U.S.C. § 470bb(7) (“The term

‘person’ means an individual, corporation, partnership, trust, institution, association, or any other

private entity or any officer, employee, agent, department, or instrumentality of the United States,

of any Indian tribe, or of any State or political subdivision thereof.” (emphasis added)).

Courts have found abrogation

where Congress has included “Indian tribes” in definitions of those who may be sued under

specific statutes. In re Whitaker, 474 B.R. 687, 691 (B.A.R. 8th Cir. 2012) (citing cases). It is

undisputed that the FTC Act does not include “Indian tribes” within the definition of persons who

may be sued under the FTC Act (again, the FTC Act allows “persons, partnerships, or

corporations” to be sued).

6

5 Santa Clara and Kiowa in the sections cited above discuss tribal sovereign immunity. However, of necessity they also concern tribal sovereignty generally, as “common law sovereign immunity possessed by the Tribe is a necessary corollary to Indian sovereignty and self-governance.” Three Affiliated Tribes of Fort Berthold Reservation v. Wold Engineering, 476 U.S. 877, 890 (1986). The two concepts are so intertwined that courts discussing abrogation routinely interpret them together. See, e.g. Wold Engineering, 476 U.S. 877, 890 (1986); Santa Clara, 436 U.S. at 56-60; United States v. United States Fidelity & Guaranty Co., 309 U.S. 506, 512 (1940); In re Whitaker, 474 B.R. 687, 696 (B.A.R. 8th Cir. 2012) (citing cases). Sovereignty, including sovereign immunity, is subject only to the plenary control of Congress, and while Congress may abrogate tribes’ sovereignty (which is often mistakenly referred to as abrogation of sovereign immunity), the law of abrogation of sovereignty is the same. C.f. Wold, 476 U.S. at 890-891 (discussing Congress’ plenary control); Santa Clara, 436 U.S. at 56-57 (discussing Congress’ plenary control). As such, sovereign immunity and general sovereignty are grounded in the same argument.

In other

6 See also, e.g., 42 U.S.C. § 8802(17) (“The term ‘person’ means any individual, company, cooperative, partnership, corporation, association, consortium, unincorporated organization, trust, estate, or any entity organized for a common business purpose, any State or local government

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 14 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

8

statutes, Congress has even defined “Indian tribe,” another notable contrast to the corresponding

omission in the FTC Act. See 15 U.S.C. § 375(8). That Congress has not done so in the FTC Act

ends the query and requires denial of the instant Motion for Partial Summary Judgment.

Considering the Supreme Court’s mandate to “tread lightly” over matters of tribal

sovereignty “in the absence of clear indication of legislative intent” in this area, Santa Clara, 436

U.S. at 58, the nomenclature that the Tribe chooses to use for its entities cannot be determinative of

whether Congress intended to abrogate the Tribe’s sovereignty. Congress clearly intends to enable

Indian tribes to engage in business development in commercial markets. See, e.g., Native American

Business Development, Trade Promotion, and Tourism Act of 2000, 25 U.S.C. §§ 4301, et seq.;

Mescalero Apache Tribe v. Jones, 411 U.S. 145, 152 (1973) (describing Congressional intent in the

Indian Reorganization Act, 25 U.S.C. §§ 461-479, to encourage and support tribal business

development while freeing tribal business enterprises from bureaucratic control by the federal

government of the details of those enterprises). Thus, it would be contrary to congressional policy,

which is, inter alia, “to grant to those Indians living under Federal tutelage and control the freedom

to organize for the purposes of local self-government and economic enterprise”7

It makes sense that Indian tribes and tribal instrumentalities (arms of tribes) are not

“corporations” under the Act, because they are wholly unlike private corporations that Congress

intended to be covered by the FTC Act. Of course, Indian tribes are “distinct, independent political

— to abrogate the

Tribe’s sovereignty because of the mere name that the tribe chose for its governmental business

development entity.

(including any special purpose district or similar governmental unit) or any agency or instrumentality thereof, or any Indian tribe or tribal organization.”). 7 H.R. Rep. No. 73-1804, at 1 (1934).

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 15 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

9

communities,”8 that have the power to constitute and regulate its form of government.9

The same argument applies with equal force to the FTC’s Truth In Lending Act (TILA) and

Electronic Funds Transfer Act (EFTA) claims. The FTC has now unmistakably stated that it brings

its TILA and EFTA claims “under the FTC Act.” (Doc. 141 at 16.) Counsel for the FTC reiterated

to the Court that “the notion that we’re – that the FTC is bringing those [EFTA and TILA] two

statutory claims under its powers under 15 U.S.C. 53(b), that’s been there all along.” (Doc. 326-3 at

61:23-25.) (However, the FTC only clarified this position in its Opposition to the Joint Motion for

Protective Order, which was filed on August 13, 2012 (Doc. 141). Prior to that time, although

Plaintiff mentioned in its Complaint that the TILA and EFTA claims were alleged as FTC Act

Tribes have

the power to tax and legislate — including the power to make criminal and civil laws, not otherwise

preempted by federal law, and to administer justice. See, e.g., Fisher v. Dist. Ct., 424 U.S. 382, 386

(1976); Kerr-McGee Corp. v. Navajo Tribe, 471 U.S. 195, 198-200 (1985). And, numerous

Executive Orders acknowledge the “unique legal and political relationship” that the United States

has with Indian tribal governments and require executive departments and agencies to engage in

regular consultation and collaboration with tribal officials, which is also unlike private corporations.

Exec. Order 13,175, 65 Fed. Reg. 67,249 (Nov. 6, 2000). None of the characteristics of Indian

tribes are shared by private “corporations,” and were certainly shared with corporations that existed

in 1914 when Congress enacted the FTC Act, when the notion of a tribal corporation was virtually

nonexistent. See The Indian Reorganization Act of 1934, 25 U.S.C. § 467 (creating the concept of a

tribal corporation). These characteristics demonstrate that Indian tribes, and their instrumentalities,

are not “corporations” as defined in the FTC Act.

8 Worcester v. Georgia, 31 U.S. 515, 559 (1832) (emphasis added). 9 Santa Clara Pueblo, 436 U.S. at 62-63.

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 16 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

10

violations, it was unclear as to whether the FTC would attempt to enforce the EFTA and TILA

claims under those statutes as well.) The FTC offers no support for the proposition that it need not

comply with 15 U.S.C. § 53(b), when using its statutory powers thereunder, as it is with its EFTA

and TILA claims. The FTC cannot have it both ways — either it is bringing its TILA and EFTA

claims under the FTC Act or it is not.

In fact, as eluded, the FTC’s assumption that Congress intended the term “corporation” to

include tribally-chartered subdivisions flies in the face of history. The FTC Act was enacted in

1914, at a time when the official federal policy toward Indians and Indian tribes was that of

“civilization and assimilation.” COHEN, supra, at 72. The goal of this federal policy “was to end

the tribe as a separate political and cultural unit . . . .” Id. at 75. Indeed, when Congress enacted the

FTC Act, Indians were not even considered United States citizens. Id. at 78; see Indian Citizenship

Act of 1924, 43 Stat. 253. It was not until 1934 — twenty years after the enactment of the FTC Act

— that Congress enacted the Indian Reorganization Act, which, for the first time, encouraged tribes

to reorganize their tribal government structures similar to those of modern business corporations.

COHEN, supra, at 81. Thus, the FTC’s claim that the Tribal Entities are “corporations” within the

meaning of the FTC Act is belied by these undeniable historic facts.

At best, the FTC Act is ambiguous as to its applicability to Indian tribes, which requires the

ambiguity to be resolved in favor of Indian tribes, as set forth below.

B. The Indian Law Canons of Construction Dictate That Ambiguities In The Act Be Resolved in Favor Of Indian Tribes

It is a basic precept of federal Indian law that “the standard principles of statutory

interpretation do not have their usual force in cases involving Indian law.” Mont. v. Blackfeet

Tribe, 471 U.S. 759, 766 (1985). Instead, courts are required to apply Indian canons of

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 17 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

11

construction to cases involving that application of federal statutes to Indian tribes. See id. The

Indian canons are rooted in the unique trust relationship between the United States and Indian

tribes. See, e.g., County of Oneida v. Oneida Indian Nation, 470 U.S. 226, 247 (1985). The

canons include the following fundamental interpretive rules that govern statutory construction

where a question of Indian law is concerned: (1) that courts must resolve ambiguities in a federal

statute in favor of Indian tribes, e.g., County of Yakima v. Confederated Tribes and Bands of the

Yakima Indian Nation, 502 U.S. 251, 268-69 (1992); Blackfeet Tribe of Indians, 471 U.S. at 766;

McClanahan v. Ariz. State Tax Com’n, 411 U.S. 164, 176 (1979); and (2) that a clear expression

of Congressional intent is necessary before a court may construe a federal statute so as to impair

tribal sovereignty, Santa Clara Pueblo v. Martinez, 436 U.S. 49, 59-60 (1978). The Indian canons

of construction must be applied unless the statutory language at issue is clear and unambiguous.

Blackfeet Tribes of Indians, 471 U.S. at 766.

Here, it is manifestly clear that the FTC Act does not apply to Indian tribes. See 15 U.S.C.

§§ 41-58. The FTC’s argument appears more focused on the “structure” that the Tribes have

taken for the Tribal Entities (i.e., “corporation,” Doc. 339 at 2, 10, 12.) But, this disregards that

when an Indian tribe establishes an entity to conduct activities, that entity shares the same

attributes as the tribe itself. Allen v. Gold County Casino, 464 F.3d 1044, 1046 (9th Cir. 2006)

(citing cases). And, because the Act clearly does not apply to Indian tribes, it is simply

incongruent that it would apply to a tribe’s entities. At best, the question of whether the Act

encompasses tribe-owned corporations, companies, entities, subdivisions, or whatever it is that the

tribe chooses to call its business, is ambiguous. Where ambiguity exists, courts are guided by the

Indian canons of construction as set forth above.

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 18 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

12

The FTC has completely disregarded the Indian canons of construction and relies upon a

line of cases that are not applicable to the case at bar because the FTC, incorrectly, assumes

without any analysis that the FTC Act is a statute of general applicability. However, a review of

the cases that the FTC cites reveals that they do not support the FTC’s position that the FTC Act

presumptively applies to Indian tribes.

C. The FTC Relies on a False Presumption that Laws of General Applicability Apply to Indian Tribes.

The FTC’s argument that the FTC Act applies to the Tribal Defendants emanates from an

alleged presumption pronounced in the Supreme Court’s 1960 decision in Fed. Power Comm’n v.

Tuscarora Indian Nation, 362 U.S. 99 (1960). In Tuscarora, the defendant tribe owned property

that the Court held was subject to condemnation under the Federal Power Act. Id. at 116. The

Court held that the Federal Power Act explicitly applied to the Tribe’s fee simple land, and

therefore the condemnation was appropriate. In a passage that has been widely acknowledged as

dicta,10

Notably, in the fifty-three years since deciding Tuscarora, the Supreme Court has never

citied this passage at all. Not once. See Bryan H. Wildenthal, How the Ninth Circuit Overruled a

Century of Supreme Court Indian Jurisprudence — And Has So Far Gotten Away With It, 2008

the Tuscarora court made the rather unremarkable statement that “it is now well settled by

many decisions of this Court that a general statute in terms of applying to all persons includes

Indians and their property interests.” Id (emphasis added). Not only was this statement obiter

dicta, but — by its own terms — this statement only applies to individual Indians, not sovereign

Indian tribal governments or their instrumentalities.

10 See, e.g., Nero v. Cherokee Nation of Okla., 892 F.2d 1457, 1462 (10th Cir. 1989); Equal Employment Opportunity Comm’n v. Cherokee Nation, 871 F.2d 937, 938 n. 3 (10th Cir. 1989); Donovan v. Couer d’Alene Tribal Farm, 751 F.2d 1113, 1115 (9th Cir. 1985).

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 19 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

13

MICH. ST. L. REV. 547, 573 (2008). By contrast, during those fifty-three years, the Supreme Court

has on dozens of occasions reaffirmed the Indian law canons of construction noted above. Id.

Instead of applying the mandatory canons of construction, the FTC relies on further dicta

from lower appellate courts — most prominently, Donovan v. Coeur d’Alene Tribal Farm, 751

F.2d 1113, 1115 (9th Cir. 1985), which purports that laws of general applicability are presumed to

apply not just to individual Indians, but to sovereign Indian tribes. Yet even the court in Donovan

was aware that this novel proposition rested on an illusory foundation, as it expressly

acknowledged that the passage from Tuscarora, upon which it relies for this proposition, is dicta.

Id. Moreover, the Donovan court’s reliance on the Tuscarora dicta was unnecessary, because the

statute at issue in Donovan — OSHA — broadly defined entities covered by that statute as “any

organized group of persons” — but then exempted certain governments — the United States,

States, and political subdivisions of States — indicating that governmental entities not enumerated

(such as Indian tribes) were intended to be covered by the statute. As discussed in detail below,

that is not true of the FTC Act.

Not only has the Supreme Court never cited Tuscarora for the proposition asserted by the

FTC, but, instead, in decisions that post-date Donovan, the Supreme Court has applied the Indian

canons of construction to conclude that statutes of general applicability at issue in those cases do

not apply to Indian tribes. See Wildenthal, 2008 MICH. ST. L. REV. 547, 585; see also Idaho v.

United States, 533 U.S. 262, 270, 272-79, 278-282 (2001) (determining that statehood act that

failed to explicitly address Indian submerged lands did not function to transfer them to the state);

Minn. v. Mille Lacs Band of Chippewa Indians, 526 U.S. 172, 176-77, 185, 202-08 (1999)

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 20 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

14

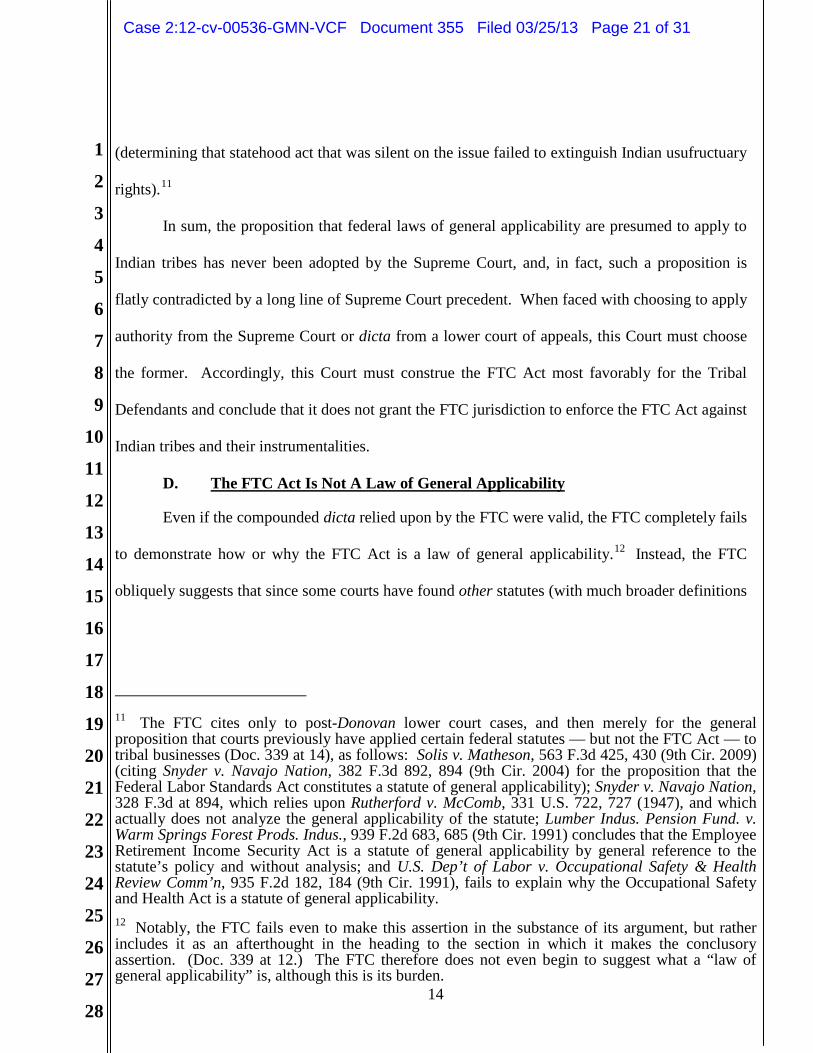

(determining that statehood act that was silent on the issue failed to extinguish Indian usufructuary

rights).11

In sum, the proposition that federal laws of general applicability are presumed to apply to

Indian tribes has never been adopted by the Supreme Court, and, in fact, such a proposition is

flatly contradicted by a long line of Supreme Court precedent. When faced with choosing to apply

authority from the Supreme Court or dicta from a lower court of appeals, this Court must choose

the former. Accordingly, this Court must construe the FTC Act most favorably for the Tribal

Defendants and conclude that it does not grant the FTC jurisdiction to enforce the FTC Act against

Indian tribes and their instrumentalities.

D. The FTC Act Is Not A Law of General Applicability

Even if the compounded dicta relied upon by the FTC were valid, the FTC completely fails

to demonstrate how or why the FTC Act is a law of general applicability.12

11 The FTC cites only to post-Donovan lower court cases, and then merely for the general proposition that courts previously have applied certain federal statutes — but not the FTC Act — to tribal businesses (Doc. 339 at 14), as follows: Solis v. Matheson, 563 F.3d 425, 430 (9th Cir. 2009) (citing Snyder v. Navajo Nation, 382 F.3d 892, 894 (9th Cir. 2004) for the proposition that the Federal Labor Standards Act constitutes a statute of general applicability); Snyder v. Navajo Nation, 328 F.3d at 894, which relies upon Rutherford v. McComb, 331 U.S. 722, 727 (1947), and which actually does not analyze the general applicability of the statute; Lumber Indus. Pension Fund. v. Warm Springs Forest Prods. Indus., 939 F.2d 683, 685 (9th Cir. 1991) concludes that the Employee Retirement Income Security Act is a statute of general applicability by general reference to the statute’s policy and without analysis; and U.S. Dep’t of Labor v. Occupational Safety & Health Review Comm’n, 935 F.2d 182, 184 (9th Cir. 1991), fails to explain why the Occupational Safety and Health Act is a statute of general applicability.

Instead, the FTC

obliquely suggests that since some courts have found other statutes (with much broader definitions

12 Notably, the FTC fails even to make this assertion in the substance of its argument, but rather includes it as an afterthought in the heading to the section in which it makes the conclusory assertion. (Doc. 339 at 12.) The FTC therefore does not even begin to suggest what a “law of general applicability” is, although this is its burden.

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 21 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

15

of entities covered by such statutes)13

Unlike the statutes cited in the post-Donovan cases relied upon by the FTC, the FTC Act

does not apply broadly. See Solis, 563 F.3d at 430 (interpreting the Fair Labor Standards Act);

Lumber Indus. Pension Fund., 939 F.2d at 685 (interpreting the Employee Retirement Income

Security Act). In fact, unlike the statutes at issue in these cases, the FTC Act is riddled with

exemptions, including nonprofits, “banks, savings and loan institutions . . ., Federal credit unions. .

. , common carriers subject to the Acts to regulate commerce, air carriers and foreign air carriers . .

. , and persons, partnerships, or corporations insofar as they are subject to the Packers and

Stockyards Act.” 15 U.S.C. § 45(a).

to be generally applicable, this Court should find the FTC

Act to be generally applicable. The FTC’s failure to even begin analyzing the question of general

applicability falls far short of its burden. There is no presumption of general applicability —

indeed such a presumption would violate the Indian canons of construction firmly established in

Supreme Court jurisprudence. See also Idaho, 533 U.S. at 270, 272-79, 278-282; Mille Lacs Band

of Chippewa Indians¸ 526 U.S. at 176-77, 185, 202-08.

14

13 Solis, 563 F.3d 425 (interpreting the Fair Labor Standards Act, 29 U.S.C. § 203(d), which applies broadly to “employers” with just a single exemption ); Lumber Indus. Pension Fund., 939 F.2d 683 (interpreting the Employee Retirement Income Security Act, 29 U.S.C. § 1002(5), which applies broadly to “employers” without exception); U.S. Dep’t of Labor v. Occupational Safety & Health Review Comm’n, 935 F.2d 182 (interpreting the Occupational Safety and Health Act, 29 U.S.C. § 652, which applies broadly to “employers” with exemptions only for the United States and any State or political subdivision of a State.

That Congress did not intend the FTC Act to be broadly

applicable is evident from the fact that Congress did not even intend that it apply to all

corporations. See Cmty Blood Bank of Kansas City Area Inc., 405 F.2d at 1017 (citing H.R. REP.

14 While the Ninth Circuit in National Labor Relations Board v. Chapa De Indian Health Program, Inc., 316 F.3d 995, 998 (9th Cir. 2002) noted that the issue is “whether the statute is generally applicable, not whether it is universally applicable,” the court emphasized in Chapa De that only two major exemptions applied to the NLRA: public sector employers and church-controlled and operated schools. By contrast, Congress provided for numerous exemptions to the FTC Act across a variety of industries and entity types. 15 U.S.C. § 45(a); see also Cmty Blood Bank of Kansas City Area, Inc. v. FTC, 405 F.2d 1011 at 1017 (1969).

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 22 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

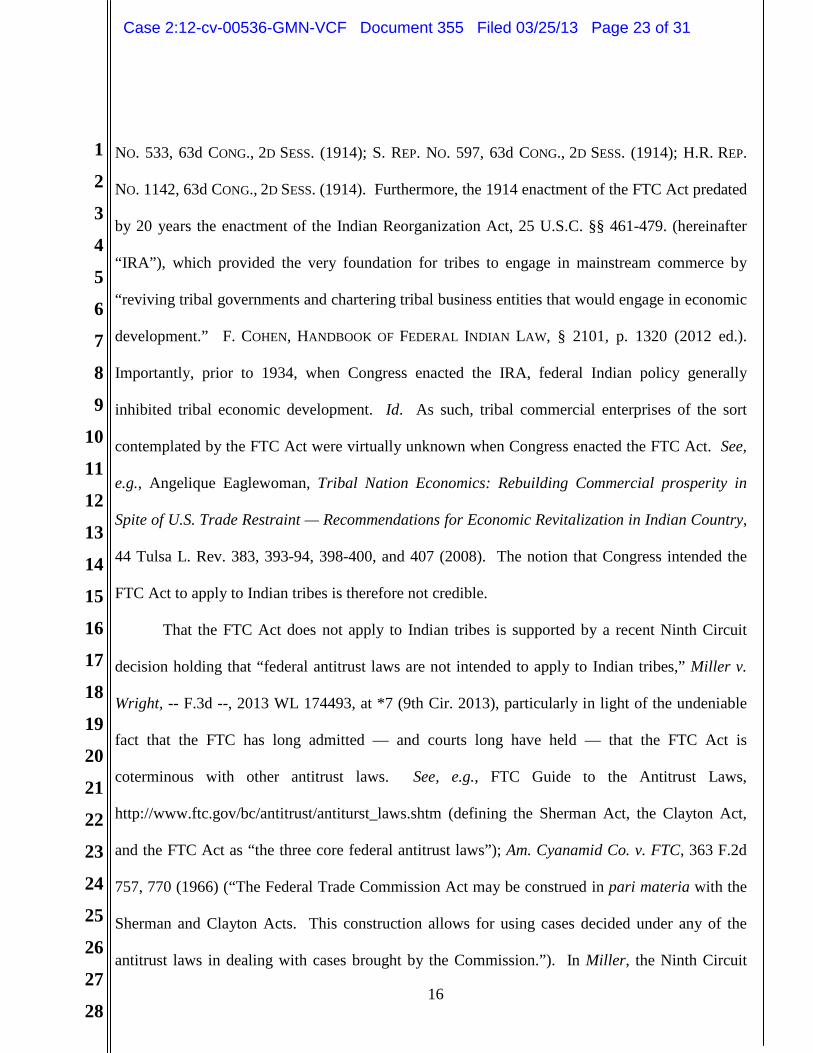

16

NO. 533, 63d CONG., 2D SESS. (1914); S. REP. NO. 597, 63d CONG., 2D SESS. (1914); H.R. REP.

NO. 1142, 63d CONG., 2D SESS. (1914). Furthermore, the 1914 enactment of the FTC Act predated

by 20 years the enactment of the Indian Reorganization Act, 25 U.S.C. §§ 461-479. (hereinafter

“IRA”), which provided the very foundation for tribes to engage in mainstream commerce by

“reviving tribal governments and chartering tribal business entities that would engage in economic

development.” F. COHEN, HANDBOOK OF FEDERAL INDIAN LAW, § 2101, p. 1320 (2012 ed.).

Importantly, prior to 1934, when Congress enacted the IRA, federal Indian policy generally

inhibited tribal economic development. Id. As such, tribal commercial enterprises of the sort

contemplated by the FTC Act were virtually unknown when Congress enacted the FTC Act. See,

e.g., Angelique Eaglewoman, Tribal Nation Economics: Rebuilding Commercial prosperity in

Spite of U.S. Trade Restraint — Recommendations for Economic Revitalization in Indian Country,

44 Tulsa L. Rev. 383, 393-94, 398-400, and 407 (2008). The notion that Congress intended the

FTC Act to apply to Indian tribes is therefore not credible.

That the FTC Act does not apply to Indian tribes is supported by a recent Ninth Circuit

decision holding that “federal antitrust laws are not intended to apply to Indian tribes,” Miller v.

Wright, -- F.3d --, 2013 WL 174493, at *7 (9th Cir. 2013), particularly in light of the undeniable

fact that the FTC has long admitted — and courts long have held — that the FTC Act is

coterminous with other antitrust laws. See, e.g., FTC Guide to the Antitrust Laws,

http://www.ftc.gov/bc/antitrust/antiturst_laws.shtm (defining the Sherman Act, the Clayton Act,

and the FTC Act as “the three core federal antitrust laws”); Am. Cyanamid Co. v. FTC, 363 F.2d

757, 770 (1966) (“The Federal Trade Commission Act may be construed in pari materia with the

Sherman and Clayton Acts. This construction allows for using cases decided under any of the

antitrust laws in dealing with cases brought by the Commission.”). In Miller, the Ninth Circuit

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 23 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

17

found that these antitrust laws (the Sherman and Clayton Acts) were not laws of general

applicability, and therefore Donovan was inapplicable. Id. at *7.15

Based upon the foregoing alone, the FTC has failed to meets its jurisdictional burden and

its Motion for Partial Summary Judgment on this issue must fail.

Miller is even more significant

considering that the statutes at issue in that case contained much broader definitions of entities

covered by those statutes than does the FTC Act. See 15 U.S.C § 12 (“person” or “persons”

wherever used in this Act shall be deemed to include corporations and associations existing under

or authorized by the laws of either the United States, the laws of any of the Territories, the laws of

any State, or the laws of any foreign country.”)

E. The Legal Determination of Whether the FTC Act Applies to Indian Tribes Cannot Be Determined By So-Called “Admissions”

The FTC erroneously argues that the Court should find that the FTC Act applies to Indian

tribes because the Tribal Defendants allegedly “admitted” that they are subject to federal law.

(Doc. 327 at 4-6.) Undoubtedly, the issue of whether a particular federal statute applies to an

Indian tribe may be a complicated legal issue.16

15 In dicta, the Court in Miller opined that the District Court likely was correct that tribes explicitly are excluded from federal antitrust laws and therefore would have satisfied the third Donavan exception even if the antitrust laws represented laws of general applicability. Miller, at *7. Interestingly, the District Court had held that the “state action doctrine” articulated in Parker v. Brown, 317 U.S. 341, 352 (1943), excluded Indian tribes from federal antitrust laws (such as the FTC Act, as discussed above) as tribes constitute sovereign entities. Miller v. Wright, No. 3:11-cv-05395 RBL, 2011 WL 4712245, * 3 (Oct. 6, 2011) (citing Parker, 317 U.S. at 352; Town of Hallie v. City of Eau Claire, 471 U.S. 34, 39 (1985)).

This complexity, coupled with the FTC’s reliance

16 At least one federal agency has itself had difficulty deciding whether it had regulatory jurisdiction over a tribal government entity under the coverage of its enabling federal statute. See N.L.R.B. v. Fortune Bay Resort Casino, 688 F.Supp.2d 858, 865 (D. Minn. 2010) (reiterating that the National Labor Relations Board initially interpreted the National Labor Relations Act to implicitly exclude tribal nations from coverage but then later rejected that interpretation).

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 24 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

18

on a line of cases17 that are “built on a discarded relic of a now-discredited area of American

Indian law,”18 renders this legal argument incapable of simplistic summation, much to the FTC’s

obvious chagrin.19

The FTC does not dispute that the issue before the Court is a “purely legal one,” (Doc. 327

at 18), yet seems to argue that this legal determination may be determined by isolated statements of

Defendants or their counsel made in other proceedings in other jurisdictions involving different

legal issues. (Doc. 327 at 4-6.) For an averment to qualify as a judicial admission, it must be a

clear and unequivocal admission of fact. Judicial admissions are limited in scope to factual matters

otherwise requiring evidentiary proof, and are exclusive of legal theories and conclusions of law.

Glick v. White Motor Co., 458 F.2d 1287, 1291 (3d Cir. 1972); 6 Handbook of Fed. Evid. § 801:26

(7th ed.). Notwithstanding that advocating an issue of law in an unrelated proceeding cannot

constitute an admission for purposes of this proceeding, the FTC makes a puerile attempt to twist a

bowdlerized version of a statement made by counsel and characterize it as an admission. (Doc. 327

at 4.) The FTC, quite disingenuously, failed to mention that the statement that it quotes, id., is in

(See Doc. 327 at 4 (stating that the Tribal Defendants have created “mischief”

with this defense).)

17 Donovan v. Coeur d’Alene Tribal Farms, 751 F.2d 1113 (9th Cir. 1985). 18 Bryan H. Wildenthal, How the Ninth Circuit Overruled a Century of Jurisprudence—And Has So Far Gotten Away With It, 2008 MICH. ST. L. REV. 547, 549 (2008). 19 Courts have recognized that the oft-cited “Tuscarora rule” is dictum and possibly overruled. Donovan v. Navaho Forest Products Indust., 692 F.2d 709 (10th Cir. 1982). The Court need not wade through Tuscarora and its progeny to resolve this issue and, instead, as set forth above, may be guided by several bedrock principles of Federal Indian law. First, it is clear that Congress may abrogate tribal sovereignty, through enactment of a federal statute, but the abrogation must be unequivocally expressed. See Santa Clara Pueblo v. Martinez, 436 U.S. 49, 58, 72 (1978). Another general principle is that Indian tribes continue to possess all the sovereign powers not explicitly taken from them by Congress. Winnemucca Indian Colony v. U.S. ex. rel. Dep’t of Interior, 837 F.Supp. 2d 1184, 1190 (D. Nev. 2011) (summarizing cases). Melding these two general principles can be complicated. However, Congress knows how to abrogate tribal sovereignty, as it has done so in certain federal statutes, like the Indian Gaming Regulatory Act (IGRA).

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 25 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

19

response to a hypothetical question from the court that involved a hypothetical tribal casino. A

more unabridged version than the FTC proffered of the exchange with the court is as follows:

THE COURT: . . . Let’s say the owner and operator of a - - and you have to forget about the Indian Gaming Regulatory Act for a second. I don’t want – let’s assume that never happened. So a casino owner in Las Vegas approaches one of their clients, and says, ‘Look, the Feds are doing an investigation, we’re about to be served with some investigatory subpoenas, we would like to purchase your tribal immunity.’ And they enter into an agreement under which you acquire the – your clients acquire the casino for $100. . . . No matter what MNE does, whether they’re out buying a casino and selling their immunity to a Las Vegas casino operator, or fishing, or painting homes . . . .[t]hey’re immune. Is that the way you see the world?

MR. SCHULTE: Well, Your Honor, if I could qualify that – and it gets

partially to my answer. You had – in your hypothetical, you said that the Feds were after the casino. Tribes are subject to all Federal laws, of course, and so that would not immunize the tribes from any sort of federal action.

(Ex. 2 at 99:5-100:6.) Thus, as set forth above, the FTC took counsel’s statement out of context, as

it was clearly in the milieu of the Indian Gaming Regulatory Act (IGRA).20

20 The FTC’s assertion that counsel’s statement was “not offered in the abstract” is wholly untrue, as the entire argument was focused on a “hypothetical.” Ex. 2 at 99:4.

(In IGRA, Congress

granted a federal agency, the National Indian Gaming Commission, authority to regulate tribal

gaming on Indian lands. 25 U.S.C. § 2702. Moreover, the United States Attorney General has

specific authority to enforce the provisions of IGRA over which the NIGC is empowered to act.

See generally, 28 U.S.C. § 516 (2006).) The point advocated by counsel and quoted by the FTC —

which applies equally here — is the uncontroversial notion Congress has the power to regulate the

Tribal Defendants’ lending activities. It certainly is not a statement that Congress has actually done

so through the FTC Act, or that Congress has empowered the FTC to enforce it against Indian

tribes. In fact, to say that any entity is subject to all federal laws begs the question of whether any

particular federal law applies to that entity in the first place. Indeed, the FTC’s callow argument, if

carried to its logical conclusion, would mean that the Tribal Defendants are subject to a myriad of

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 26 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

20

federal laws that were never intended to apply to them. E.g., The Atomic Energy Act of 1946, Pub.

L. No. 79-585, 60 Stat. 755; The Airline Deregulation Act of 1978, Pub. L. No. 95-504, 92 Stat.

1705. Thus, for these reasons, counsel’s statement is not an admission.

As to the statement that the FTC relies upon from Mr. Brady (Doc. 327 at 5), which

apparently the FTC seeks to have admitted as an admission against interest, that statement was

made in a different proceeding in 2007 and cannot be the subject of a judicial admission. Moreover,

a broad statement that MNE “adhere[s] to all federal laws” or that is “compliant” with federal laws

is a far cry from saying that the FTC has jurisdiction to enforce any law against the Tribal

Defendants. It should not be difficult for the FTC to understand the plain logic of the notion that

the Tribal Defendants may aver compliance with federal laws without conceding that the FTC has

jurisdiction to enforce federal law against them. Again, the issue of whether Indian tribes,

particularly, MNE, is subject to the FTC Act is a question of law. A party is not bound by an

admission regarding a “conclusion” of law because courts determine the legal effect of the facts

adduced. Pinebrook Minerals, LLC v. Anadarko E & P Co., LP, No. 11-00177, 2011 WL 3584783,

*8 (M.D. Pa. July 25, 2011); Perry v. Serenity Behavioral Health Systems, No. 106-172, 2009 WL

1228446, *2 (S.D. Ga. May 4, 2009). Thus, considering that the issue is one of law, the FTC’s

attempt to couch the 2007 statement of Mr. Brady (who is not a lawyer) as an “admission” is amiss.

Kohler v. Leslie Hindman, Inc., 80 F.3d 1181, 1185 (7th Cir. 1996) (holding that statement was not

competent evidence because it states a legal conclusion); Rodriguez v. CHRISTUS Spohn Health

System Corp., 874 F.Supp.2d 635, 656 (S.D.Tex. 2012) (holding that a party may not “judicially

admit a question of law.”).

The FTC also fails to acknowledge that these so-called “admissions” were of absolutely no

consequence in the proceedings from which they arose. The Colorado District Court’s decision did

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 27 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

21

not rely in the least on the hypothetical exchange upon which the FTC places so much significance.

(See Order, Colorado v. Cash Advance, 05-CV1143 (Dist. Ct., City and County of Denver, Colo.

February 13, 2012.), located at Doc. 102-1 at pp. 1-28.) Likewise, Mr. Brady’s statement played

absolutely no role whatsoever in the California Superior Court’s decision. (See Order, California v.

Ameriloan, BC373536 (Cal. Super. Ct. May 10, 2012), located at Doc. 102-1 at RJN Ex. B.) It

bears repeating that, notwithstanding the FTC’s assertions to the contrary, the Tribal Defendants’

statements in these proceedings amounted to nothing more than an affirmation of the unremarkable

fact that the federal government has the power to regulate Indian tribes, not that any particular

statute in fact does so.

In sum, despite the FTC’s attempt to characterize the Tribal Defendants in the pejorative as

flip-floppers, the reality is that this is a complex legal determination, and the determination should

focus on the law, not so-called “admissions” made in a wholly different context.

V. Conclusion

For all of the reasons set forth above, the FTC has not met its burden of showing that the

FTC Act applies to Indian tribes and, thus, its Amended Motion for Partial Summary Judgment

should be denied.

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 28 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

22

Dated: March 25, 2013 /s/ Shilee Mullin Attorneys for Defendants AMG Services, Inc.; Red Cedar Services, Inc.; SFS, Inc.; MNE Services, Inc.

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 29 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

23

CERTIFICATE OF SERVICE Pursuant to Fed. R. Civ. P. 5(b), I hereby certify that on the 25th day of March 2013,

service of the foregoing Tribal Defendants’ Opposition to Plaintiff’s Motion for Partial Summary

Judgment submitted electronically for filing and/or service with the United States District Court

of Nevada. Electronic service of the foregoing document shall be made in accordance with the E-

Service List as follows:

Blaine T. Welsh Julie G. Bush Jason Schall Nikhil Singhvi Helen Wong Ioana Rusu

[email protected] [email protected] [email protected] [email protected] [email protected] [email protected]

Attorneys for Plaintiff Von S. Heinz Darren J. Lemieux E. Leif Reid Nick Kurt Ryan Hudson

[email protected] [email protected] [email protected] [email protected] [email protected]

Attorneys for Defendants AMG Capital Management, LLC; Level 5

Motorsports, LLC; LeadFlash Consulting, LLC; Black Creek Capital Corporation; Broadmoor Capital Partners, LLC; Scott A. Tucker; Blaine A. Tucker

L. Christopher Rose [email protected]

Attorney for Defendants The Muir Law Firm, LLC and Timothy J. Muir

Whitney P. Strack Brian R. Reeve Nathan F. Garrett

[email protected] [email protected] [email protected]

Attorneys for Defendant Don E. Brady

Jay Young [email protected]

Attorney for Defendant Robert D. Campbell

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 30 of 31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

24

Paul C. Ray Alyssa D. Campbell

[email protected] [email protected]

Attorney for Defendant Troy L. Little Axe

Patrick J. Reilly R. Pete Smith Linda C. McFee

[email protected] [email protected] [email protected]

Attorney for Defendants Kim C. Tucker and Park 269 LLC

/s/ Carol Cyriacks Paralegal

FREDERICKS PEEBLES & MORGAN LLP 3610 North 163rd Plz. Omaha, NE 68116

Case 2:12-cv-00536-GMN-VCF Document 355 Filed 03/25/13 Page 31 of 31