unit 4: inflation, unemployment, and stabilization...

TRANSCRIPT

Test:

UNIT 4: INFLATION,

UNEMPLOYMENT, AND

STABILIZATION POLICIES

This unit accounts for 20-30% of the

AP Macro Test

Long-Run implications of Fiscal Policy: Deficits and

the Public Debt

Learning Goals:

Why governments

calculate the cyclically

adjusted budget balance

Why a large public debt

may be a cause for

concern

Why implicit liabilities of

the government are also

a cause for concern

DAY 1

What does it mean to have a ‘balanced budget?’

Sgovernment = Taxes – Government Spending – Government Transfers

If this number is positive, we have a surplus and a balanced

budget

If the number is negative, now we have a deficit and a negative

budget balance.

THE BUDGET BALANCE

Budget balancing is dif ficult with Fiscal Policy.

Let’s say the government can decide to either increase its own

spending by $1000 OR increase transfers by $1,000. In both

cases, $1,000 will be added to total government spending

BUT they will have a dif ferent impact on the GDP because the

direct government spending will have a greater impact than

the increase transfer.

BUDGET BALANCE AS A MEASURE OF

FISCAL POLICY

Typically, the budget deficit goes up when unemployment goes up, and down when unemployment is down.

Why? Not necessarily because of fiscal pol icy. More of ten, i t is a result of automatic stabil izers (progressive taxes, unemployment, food stamps, etc.)

In order to combat these and figurer out what the balance would be if there was neither a recessionary or an inflationary gap, we can calculate a cyclically adjusted budget balance .

The cyclically adjusted budget takes into account the extra tax revenue that the government would col lect and the transfers i t would save if a recessionary gap were el iminated – or the revenue the government would lose and the extra transfers i t would make if an inflationary gap were el iminated.

I f even af ter a cyclically adjust budget is run and we sti l l have a negative balance…now that might be a ‘bad’ thing.

BUSINESS CYCLE AND THE CYCLICALLY

ADJUSTED BUDGET BALANCE

Most economists believe we

should NOT have a requirement

to balance the budget every

year.

They do believe however that

the budget should be balanced

over all…so maybe not year to

year, but generally speaking,

the government should save

during good times so that it

can spend during the bad.

SHOULD THE BUDGET BE BALANCED?

A short term deficit can be paid off

if the government has some money

in savings. However, if the

government doesn’t have money to

pay, than the deficit becomes debt.

Is today’s debt a big deal??

http://www.usdebtclock.org/

LONG-RUN IMPLICATIONS OF FISCAL

POLICY

Try not to think about

what commentators

think about the

budget…let’s look at

what an economist

might think…

Two reasons to be concerned when a government runs a persistent budget deficit:

1. When the government borrows funds in the financial markets, it is competing with firms that plan to borrow funds for investment spending. As a result, the government’s borrowing may “crowd out” private investment spending, increasing interest rates and reducing the economy’s long -run rate of growth.

2. Today‘s deficits, by increasing the government’s debt, place financial pressure on future budgets. Interest must be paid in the future, and this can take dollars away from other future obligations like education, the military, space exploration, etc.

PROBLEMS POSED BY RISING

GOVERNMENT DEBT

Borrowing to pay off your debt isn’t really an option. That’s

l ike getting a new credit card to pay off the old credit card.

Eventually, that is the road to bankruptcy. Nations have

essentially declared bankruptcy in the past…its not pretty.

(aka Greece)

Increase taxes or cut spending. Probably the best solution,

but it isn’t very politically successful, especially when a

nation has become accustomed to low taxes (like the US has

vs. historical rates today)

Printing money. Basically this means that the FED creates

new money to pay the debts of the Treasury. This may fix debt

problem, but can make money essentially worthless and can

lead to inflation or hyper inflation.

HOW TO PAY OFF GOVERNMENT DEBT

To assess the ability of government to pay their debt, we often

use the debt-GDP ratio.

We use this measure rather than just looking at debt because

GDP is a good indicator of the potential taxes the government

can collect. If the government’s debt grows more slowly than

GDP, the burden of paying the debt is actually falling

compared with the government’s potential tax revenue.

DEFICITS AND DEBT IN PRACTICE

Implicit l iabilities are spending promises made by

governments that are effectively a debt despite the fact that

they are not included in the usual debt statistics.

In the US, we promise to honor Social Security, Medicare and

Medicaid amount to 40% of federal spending…potentially a

big deal and population ages and gets larger.

IMPLICIT LIABILITIES

The nation of Foxlandia has a closed economy. Given the

information below, calculate the level of investment spending,

private savings, and the budget balance. There are no

government transfers.

PRACTICE PROBLEMS

GDP = $1500 Million

C = $1000 Million

G = $400 Million

T = $300 Million

Monetary Policy and the Interest Rate

Learning Goals:

How the Federal

Reserve implements

monetary policy,

moving the interest rate

to affect aggregate

output.

Why monetary policy is

an important tool for

stabilizing the economy

DAY 2

The Federal Reserve is the central bank of the united states.

A central bank is an institution that oversees and regulates the banking system, and controls the money base. Other central banks include the Bank of England, the Bank of Japan, and the European Central Bank, or ECB.

Fed was created in 1913 by President Wilson in responses to an economic Panic of 1907. During that panic, JP Morgan had to literally save the US banking system, and the US wanted to stabilize itself and create a central bank, which Congress then did.

The Fed isn’t really a government entity, but its not entirely public either. It is made up of a Board of Governors in DC and has 12 member banks around the US.

WHAT IS THE FEDERAL RESERVE?

They oversee the entire system from the offices in DC

7 members are appointment by the President and approved by

Senate; serve 14 year terms (chairman is appointed every 4

years).

THE FED – BOARD OF GOVERNORS

Current chair Janet

Yellen and 4 members of

the board.

Allen

Greenspan

served as

chair from

1987-

2006.

JANET YELLEN MET WITH A SENATE COMMITTEE

LAST WEEK…SHE DOESN’T QUITE UNDERSTAND

YOU YET…

http://www.cnn.com/2015/02/24/politics/j

anet-yellen-capitol-hill-preview/

Provide various banking and supervisory service. For

example: audit the books of private sector banks to ensure

financial health. Each regional bank is run by a board of

directors chosen by the local business community. New York’s

carries out open market operations (deciding when to buy and

sell bonds)

FEDERAL RESERVE – 12 DISTRICT

BANKS

KC Fed head Esther George

The Federal Reserve can literally increase the amount of

money that exists in the United States. This is usually the

result of what is called an ‘open market operation’

The increase in the money supply causes short -term interest

rates to fall in the money market.

MONETARY POLICY AND THE INTEREST

RATE

Would this be an

expansionary or

contractionary policy?

Would this be an expansionary or contractionary policy? Why?

HOW THE FEDERAL RESERVE ‘MAKES’

MONEY

Typically, the Federal reserve has a targets a specific federal

funds rate

The federal funds rate is the interest rate at which the FED

can lend money to other institutions (like the US government,

Bank of America, etc.)

If the current federal funds rate is higher than the target, the FED will

increase the money supply so that the rate falls to the target

If the current federal funds rate is lower than the target, the FED will

decrease the money supply so that the rate rises to the target.

FEDERAL FUNDS TARGET

Monetary policy is a central bank’s use of changes in the

quantity of money or the interest rate to stabilize the

economy. In the United States, our central bank is the Federal

Reserve Bank.

SO WHAT IS MONETARY POLICY?

We have seen how Fiscal policy can be used to stabilize the

economy. Now we will see how monetary policy can play the

same role.

Investment spending is usually very sensitive to changes in

the interest rate. When interest rates fall, we see an increase

in investment spending. Some types of consumption spending

also increase when the interest rate falls. Eg: car buying,

college educations, real estate, etc.

Since both investment spending and consumption spending

are important components of aggregate demand, it would

therefore make sense that when the interest rate falls, AD

should rise.

MONETARY POLICY AND AGGREGATE

DEMAND

Expansionary monetary policy chain of events

1. The Fed observes that the economy is in a recessionary gap

2. The Fed increases the money supply

3. The interest rate falls

4. Investment and consumption increase

5. AD shifts to the right

6. Real GDP increases, unemployment rate decreases, the aggregate price level rises

Contractionary monetary policy chain of events

1. The Fed observes that the economy is in an inflationary gap.

2. The fed decreases the money supply

3. The interest rate rises

4. Investment and consumption decrease

5. AD shifts to the left

6. Real GDP decreases, unemployment rate increases, the aggregate price level falls

EXPANSIONARY AND CONTRACTIONARY

MONETARY POLICY

More

on

how

they

do

this

later

1. Open market operations (buying and selling bonds)

2. Control of the interest rate

3. Control of the reserve ratio

How could each of these ‘make’

money?

MONETARY TOOLS OF THE FEDERAL

RESERVE (WE WILL TAKE A WHILE TO WORK THROUGH THESE)

Suppose the economy is currently suffering from a very high

rate of inflation caused by aggregate demand that has

increased beyond potential GDP.

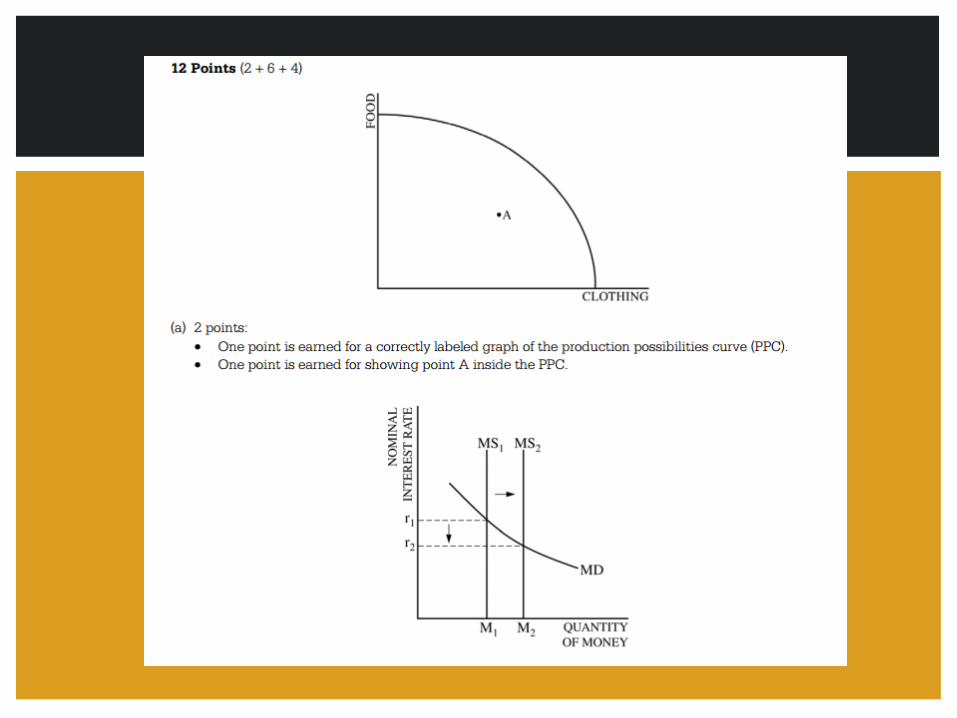

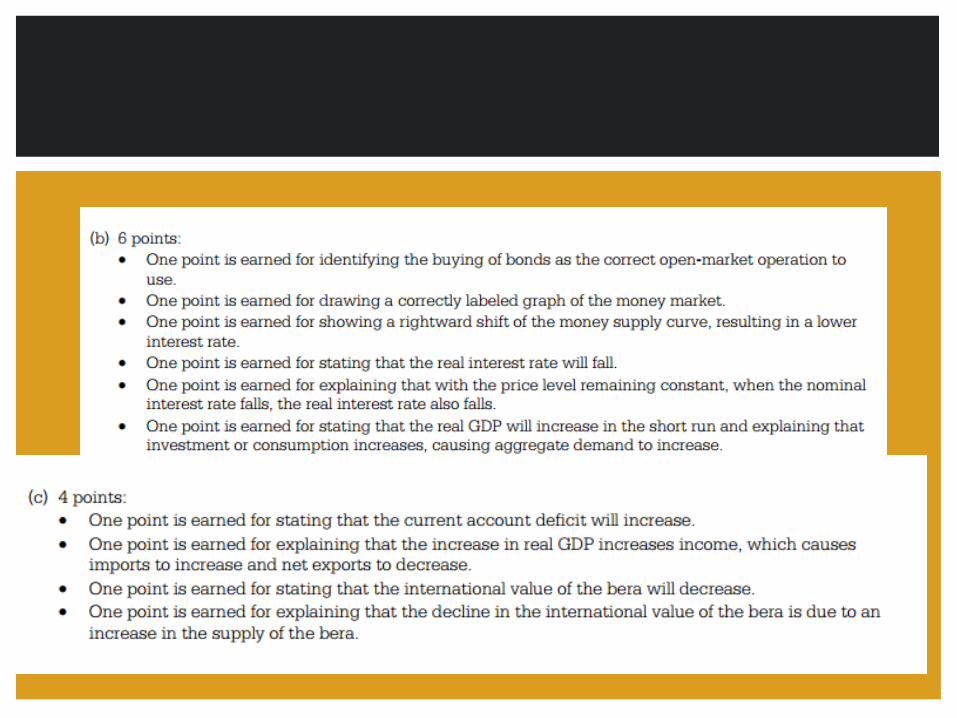

a. In a correctly labeled graph, show equilibrium in the money market.

b. In a correctly labeled AD/AS graph, show the current short -run

equilibrium in the macroeconomy

c. In response to this high inflation rate, should the Fed engaged in

expansionary or contractionary fiscal policy?

d. In your graph from part a show the impact of this monetary policy in

the money market and on the equilibrium interest rate.

e. In your graph from part b show the impact of this monetary policy on

real GDP and the price level.

PRACTICE PROBLEM

RELEASED FRQ PRACTICE

Packets not back from printshop…sorry.

Watch the monetary policy and interest rate video (7 min

Khan academy) and make sure you understand this stuff. Just

write down any questions so we can answer them in class on

Thursday.

LEARNING PREP #1 FOR THURS

Money, Output, and Prices in the Long Run

Learning Goals:

The effect of

inappropriate monetary

policy

The concept of

monetary neutrality and

its relationship to the

long-term economic

effects of monetary

policy

DAY 3

The Federal Reserve can use its monetary policy tools to

change the money supply and cause equilibrium interest rates

in the money market to increase or decrease. But what if a

central bank pursues a monetary policy that is not

appropriate?

Could a counter-productive action by a central bank actually

destabilize an economy in the short run?

Also, what are the long run effects of monetary policy?

MONEY, OUTPUT, AND PRICES

There are t imes when the central bank can engage in monetary pol icy that is actually counter productive. In other words, the pol icy might move the economy AWAY from the potential GDP rather than closer to the potential GDP.

Suppose the economy is currently in LR equil ibrium. If the Fed were to conduct expansionary

monetary policy, the interest rate would fall.

A lower interest rate would shift AD to the right.

In the short run, real GDP would increase, but so would price level.

Eventually, nominal wages would rise in labor markets, shifting SRAS to the left.

Long-run equilibrium would be established back at potential GDP and a higher price level.

So in the long run, expansionary monetary policy doesn’t increase real GDP, it only causes inflation.

SHORT-RUN AND LONG-RUN EFFECTS OF

AN INCREASE IN THE MONEY SUPPLY

Money neutrality – changes in the money supply have no real effects on the economy. In the long run, the only effect of an increase in the money supply is to raise the aggregate price level by an equal percentage. Economists argue that money is neutral in the long run.

In other words – no matter what monetary policy the Fed uses, it can only change things in the short run. Markets are self -correcting in the long run.

How does money neutrality work?

Suppose all prices in the economy – prices of final goods and services and also factor prices, such as nominal wages, double

And supply the money supply doubles at the same time

What difference does this make to the economy in real terms? None!

All real variables in the economy – such as real GDP and the real value of the money supply (the amount of goods/services it can buy) are unchanged.

So, there is no reason for anyone to behave any differently.

MONEY NEUTRALITY

In the short run, we have seen that an increase in the Money Supply causes short-term interest rates to fall . But what happens in the long run?

Suppose the money market equilibrium is at an interest rate of i*% Suppose MS increases by 10% to M’.

The short run interest rate falls.

Money neutrality says that in the long run, aggregate price level rises by 10%

When aggregate prices rise by 10%, households will increase their demand for money by 10%

When both MS and MD shift to the right by 10%, the long run equilibrium interest rate returns to i*%

CHANGES IN THE MONEY SUPPLY AND

THE INTEREST RATE IN THE LONG RUN

1

a. Draw a correctly labeled graph of aggregate demand and

supply showing an economy in long run equilibrium

b. Draw a correctly labeled graph of equilibrium in the money

market

c. On your graph in part b, show what happens to the

macroeconomy in the short run if the central bank

decreases the money supply

d. On your graph in part a, show what happens to the

macroeconomy in the short run if the central bank

decreases the money supply

e. On both graphs, show what will happen in the long run.

Explain these adjustments

PRACTICE PROBLEM

Types of Inflation, Disinflation, and Deflation

LG’s

The classical model of

the price level

Why efforts to collect an

inflation tax by printing

money can lead to high

rates of inflation and

hyperinflation

The types of inflation:

cost push and demand

pull

DAY 4

http://www.pbs.org/newshour/bb/business-

jan-june09-solman_03-17/

NOT all inflation is created equal. Crazy inflation, like in

Zimbabwe, is associated with rapid increases in the money

supply. Moderate inflation, like here in the US, has a very

dif ferent cause.

MONEY AND INFLATION

As a result of change in the

nominal money supply, leads in

the long run to a change in the

aggregate price level, and that

leaves the real quantity of

money at its original level (both

increase at the same rate)

Problem: the jump from the first

Long Run equilibrium to the

second is not that fast…in large

part because of sticky wages

This model may be true if there

is a lot of inflation, but not as

true during periods of low

inflation

THE CLASSICAL MODEL OF MONEY AND

PRICES

In conservative media, you often hear about the government

‘printing money’ to pay for large budget deficits.

In reality: remember, the Fed issues money, the Treasury

actually prints it.

INFLATION TAX

Fed creates money and

uses it to buy bonds from

private sector

Treasury pays interest on debt

owned by the federal

reserve…but the federal

reserve is required by law to

give any profits to the

treasury…so essentially, the

treasury pays itself.

Many see this as dangerous because more money just

leads to inflation….and it takes the market a while to

adjust to wage increases, so in the short run, goods are

just more expensive.

This process is

called seignorage

People who currently hold money – because it is worth less,

inflation erodes your money’s purchasing power.

This concept is known as an inflation tax. It isn’t actually a

government tax, it is the idea that the government, through its

own monetary policies, can make your money worth less.

WHO PAYS FOR INFLATION?

Let’s say a city wants to increase its revenue so they add a fee

(tax) to all cab fares. People who don’t want to pay it switch

to substitutes (walk, bus, etc). In order to cover the growing

deficit, the city makes the fee on cab fares even HIGHER and

as they do even more people switch to substitutes. No one

wins.

LOGIC OF HYPERINFLATION

This is basically what happens with

hyperinflation. The government prints

more money to cover its debt. But then

prices go up (or currency goes down) by

that same percentage. There is a cycle

of the government trying to cover its

own debt, but as the value of money

depreciates for people, it prints more

money, and so on and so on.

2 possible changes can cause a moderate increase in the

aggregate price level:

MODERATE INFLATION

Cost push inflation is caused by a decrease in SRAS.

This is usually caused by an economy -wide increase in the

price of resources.

COST PUSH INFLATION

Demand pull inflation is caused by an increase in Aggregate

Demand.

This is likely to be caused by economic growth that is coupled

with either expansionary fiscal or monetary policy.

DEMAND PULL INFLATION

DISINFLATION VS DEFLATION

Disinflation is a slowing in the rate of increase in the general price level, as

represented by the average price of goods and services in the consumer

basket. For instance, between 1981 and 1983, the annual rate of increase

in the Canadian total Consumer Price Index (CPI) declined from 12.5 per

cent to just under 6 per cent. Again, from 1990 to 1992, the rate of

inflation slowed from about 5 per cent to 1.5 per cent. This is disinflation.

Deflation, on the other hand, refers to a persistent fall in the level of the

total CPI, with negative inflation being recorded year after year. The one

major episode of sustained deflation in Canada was during the Great

Depression of the 1930s, when the overall level of prices fell by more than

20 per cent over a four year period.

See how much of activity 5 -5 you can tackle.

ACTIVITY PACKET

Day 5

Learning Goals:

What the Phil l ips curve is and the nature of the shor t -run trade-of f between inflation and unemployment

Why there is no long-run trade of f between inflation and unemployment

Why expansionary pol icies are l imited due to the ef fects of expected inflation

Why even moderate levels of inflation can be hard to reduce

Why deflation is a problem for economic pol icy and leads policy makers to prefer a low but posit ive inflation rate

INFLATION AND UNEMPLOYMENT: THE

PHILLIPS CURVE

Shows tradeoff between inflation

and unemployment. What happens to inflation and unemployment when AD

increase?

THE PHILLIPS CURVE

51

In general, there is an inverse relationship

between unemployment and inflation

Inflation

52

SRPC

Short Run Phillips Curve

Unemployment 2% 9%

1%

5%

When the economy is overheating, there is low unemployment but high inflation

When there is a recession, unemployment is high but

inflation is low

Inflation

53

SRPC

Short Run Phillips Curve

Unemployment 2% 9%

1%

5%

What happens when AS falls causing stagflation? Increase in unemployment and inflation

SRPC1

Inflation

54

SRPC

Short Run vs. Long Run

Unemployment 2% 9%

1%

5%

What happens when AD increases?

SRPC1

3%

5%

Long Run Phillips Curve

In the long run, wages

and resource prices

increase. AS falls.

SRPC shifts right.

What happens in the long run?

Inflation

55

Short Run vs. Long Run

Unemployment 2% 9%

1%

5%

3%

5%

Long Run Phillips Curve

In the long run there is no tradeoff between inflation

and unemployment

The LRPC is vertical at

the Natural Rate of

Unemployment

Inflation

56

SRPC

Short Run vs. Long Run

Unemployment 2% 9%

1%

5%

What happens when AD falls?

SRPC1

3%

5%

Long Run

Phillips Curve

In the long run wages

fall and there is no

tradeoff between

inflation and

unemployment

What happens in the long run?

AD/AS AND THE PHILLIPS CURVE

Price

Level

58

AD

AS

AD/AS and the Phillips Curve

GDPR QY

PLe

LRAS Inflation

SRPC

Unemployment

UY

LRPC

Show what happens on both graphs if AD increase

AD1

Price

Level

59

AD

AS

AD/AS and the Phillips Curve

GDPR QY

PLe

LRAS Inflation

SRPC

Unemployment

UY

LRPC

Correctly draw the LRPC and SRPC with the recessionary gap. What happens when AD falls?

AD1

Price

Level

60

AD

AS

AD/AS and the Phillips Curve

GDPR QY

PLe

LRAS Inflation

SRPC

Unemployment

UY

LRPC

Correctly draw the LRPC and SRPC at full employment. What happens when AS falls?

AS1

SRPC1

Price

Level

61

AD

AS

AD/AS and the Phillips Curve

GDPR QY

PLe

LRAS Inflation

SRPC

Unemployment

UY

LRPC

Correctly draw the LRPC and SRPC with an recessionary gap. What happens when AS goes up?

AS1

SRPC1

Price Level

62

SRAS

GDPR QY

LRAS Inflation

SRPC

Unemployment UY

LRPC

You need to be able to ‘see’ how this works. Remember, memorizing isn’t the

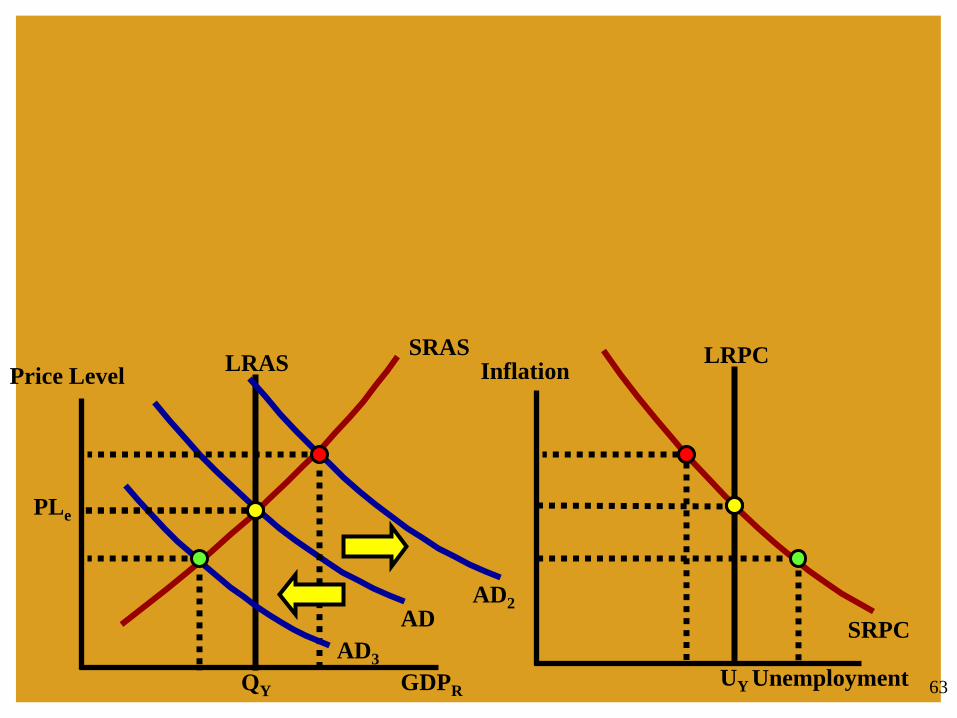

key, it is understanding how it works so you can reproduce it on your own.

AD

Price Level

63

SRAS

GDPR QY

LRAS Inflation

SRPC

Unemployment UY

LRPC

AD2

AD3

PLe

AD

Price Level

64

SRAS

GDPR QY

LRAS Inflation

SRPC

Unemployment UY

LRPC AS1

PLe

AS2

SRPC1

SRPC2

AD

Price Level

65

AS

GDPR QY

LRAS Inflation

SRPC

Unemployment UY

LRPC AS2

PLe

SRPC1 AD2

ANALYZING THE ECONOMY

GRAPHICALLY

66

USE THE FOLLOWING MODELS TO SHOW

FULL EMPLOYMENT, A RECESSIONARY

GAP, AND AN INFLATIONARY GAP.

1. PPC

2. Business Cycle

3. AD/AS

4. Phillips Curve

67

THE GOOD, THE BAD, AND THE UGLY

Unemployment

Inflation

GDP Growth

Good

6% or less

1%-4%

2.5%-5%

Worry

6.5%-8%

5%-8%

1%-2%

Bad

8.5 % or more

9% or more

.5% or less

68

Complete Activities 5-8 and 5-9 (lots of pages) in your activity

packet.

We sort of skipped the idea of ‘crowding out’ – go back and

look at it (activity 5 -7). For your learning prep for Wednesday.

ACTIVITY PACKET

https://www.youtube.com/watch?v=zatnIhw

mu1c

Day 6

See Keynes articles

Learning Goals

Why classical economics wasn’t adequate for the problems posed by the Great Depression

How Keynes and the experience of the Great Depression legitimized macroeconomic pol icy activism what monetarism is and its views about the l imits of discretionary monetary pol icy

How challenges led to a revision of Keynesian ideas and the emergence of the new classical macroeconomics.

HISTORY AND ALTERNATE VIEWS OF

MACROECONOMICS

Prior to the Great Depression, economists didn’t really focus

on the state of the economy in the Short run, only the long

run…they thought the short run was sort of insignificant to

overall output

There was no consensus on the business cycle…what it meant,

how it worked. They did assume a downturn in the economy

was temporary, but didn’t encourage policies to mitigate

them.

Great Depression led many to rethink this model.

CLASSICAL VIEWS OF MACROECONOMCS

The General Theory of Unemployment, Interest, and Money

Said short run shifts in aggregate demand do affect aggregate

output and price level!! Short -run shifts are important!!

Said the AD curve can shift because of many factors (like

confidence of businesses) and that they move the business

cycle.

JOHN MAYNARD KEYNES

Because of what Keynes said, we often see governments

actively working to fight recessions and help use fiscal and

monetary policy to smooth out business cycle

Today there is a very broad consensus on how to use these

policies to help stabilize the economy…the debate comes in at

which ones should be used when (think Obama and auto/bank

‘bailouts’

KEYNES WORK AND ECONOMY POLICIES

During Great Depression – really only fiscal policy (actions by

Congress/President) was used.

Post WWII we start to see a rise in monetary policy (role of

the FED and the creation of money)

Milton Friedman and Anna Schwartz (1963) publish A

Monetary History of the United States showing how supply of

money can also impact the business cycle – this encouraged

more economists to support monetary policy

MONETARY POLICY POST WWII

Milton Friedman led a movement that sought to eliminate

macroeconomic policy activism while maintaining the

importance of monetary policy

Monetarism asserted that GDP will grow steadily if the money

supply grows steadily

Said that the Fed should have a bank target for a rate of

constant growth of money supply (3% per year) no matter

what fluctuations were in the economy

But this constant rate of growth may cause government

spending to ‘crowd -out’ investment spending

https://www.youtube.com/watch?v=RGlt0nEQdRI

MONETARISM

Researchers have also found a statistical correlation between

upcoming political elections and expansionary fiscal policy

In months leading up to elections, government either cuts

taxes or announces new spending programs. These policies

put more money in pockets of voters and also tend to lower

the unemployment rate. The eventual cost is inflation, but by

then the election is over and inflation is often addressed at a

later date…

POLITICAL BUSINESS CYCLE

2016

In the 70s, 80s, and 90s, more economists used the idea of

‘rational expectations’ – this is the idea that individuals and

firms make optimal decisions using all available information

According to the original version of the natural rate

hypothesis, a government attempt to trade off higher inflation

for lower unemployment would work in the short run but

would eventually fail because higher inflation would get built

into expectations…

Today we say…public gets this…and public wouldn’t wait to

change their expectations…those would change almost

immediately

This is New Keynesian ideas. They take into account price

stickiness.

UPDATES TO EARLY ECONOMIC IDEAS

--------------------

Learning Goals:

The elements of

modern consensus

The main remaining

disputes

MODERN ECONOMIC CONSENSUS

Today…we say that YES it is beneficial…

The only time it is not is when there is a ‘l iquidity trap’ (this is

when injections of cash into the private banking system by a

central bank fail to decrease interest rates and hence make

monetary policy ineffective . But this usually doesn’t happen.

IS EXPANSIONARY MONETARY POLICY

HELPFUL IN FIGHTING RECESSIONS?

Generally, everybody believes YES

They also all seem to agree that balancing the budget isn’t

always a good thing…sometimes the government would need

to spend more depending on the state of the economy…and

then the government should save up when the economy is

doing well.

IS EXPANSIONARY FISCAL POLICY

EFFECTIVE IN FIGHTING RECESSIONS?

Today, almost all macroeconomists now say that there is a

natural rate of unemployment and agree that there are some

limits of fiscal and monetary policies.

They believe that effective monetary and fiscal policy can

l imit the size of fluctuations of the actual unemployment rate

around the natural rate, but can’t keep unemployment below

the natural rate

CAN MONETARY AND/OR FISCAL POLICY

REDUCE UNEMPLOYMENT IN THE LONG

RUN?

Today pretty much everyone agrees that tax cuts and/or

spending can be at least somewhat effective in increasing

aggregate demand

Many (but not all) agree that discretionary fiscal policy is

usually counterproductive: the lags in adjusting fiscal policy

mean that, all too often, policies intended to figh a slump

end up intensifying a boom

As a result, the macroeconomic consensus gives monetary

policy the lead role in economic stabilization. Discretionary

fiscal policy plays the leading role only in special

circumstances when monetary policy is ineffective, (maybe if

there is a liquidity gap)

SHOULD FISCAL POLICY BE USED IN A

DISCRETIONARY WAY?

In the US, the FED doesn’t announce an inflation rate target,

but most people believe their goal is to try and stay at about

2% per year

CENTRAL BANK TARGETS

Should the Fed be pro-actively be influencing the stock

market, real estate market, or any other asset market?

Jury is still out…some people don’t want the Fed to intervene

in these markets, but if the bubble bursts (housing in 2008),

the damage is often really painful so maybe they should???

ASSET PRICES

Desperate times call for desperate measures…in 2008, Fed

took actions that it doesn’t normally…so often times in

extreme cases, people are ok with them being overly involved.

UNCONVENTIONAL MONETARY POLICIES

https://www.youtube.com/watch?v=HGjtcPssfCs

You probably won’t be asked to ‘draw’ this like he says (unless

an FRQ specifically asks for a Keynesian/classical model) but

you will be asked to recognize it on the multiple choice.

MODERN CONSENSUS

STUDY

See practice questions

See videos online for help

Try to complete your entire packet

MC and FRQ test on Thursday!

TO DO

Money

Market

Phillips

Curve

Phillips

Curve

cont.