unit 2 capital budgeting decisions module...

TRANSCRIPT

UNIT 2 CAPITAL BUDGETING DECISIONS

MODULE - 1

M

O

D

U

L

E

-

1

Capital Budgeting Decisions

Self-Instructional Material 25

NOTES

UNIT 2 CAPITAL BUDGETINGDECISIONS

Structure

2.0 Introduction2.1 Unit Objectives2.2 Nature of Investment Decisions

2.2.1 Importance of Investment Decisions2.3 Types of Investment Decisions

2.3.1 Expansion and Diversification; 2.3.2 Replacement and Modernisation2.3.3 Mutually Exclusive Investments; 2.3.4 Independent Investments2.3.5 Contingent Investments

2.4 Capital Budgeting Process2.4.1 Capital Investments; 2.4.2 Capital Investment Planning and Control

2.5 Time Value of Money2.5.1 Compounding; 2.5.2 Discounting

2.6 Investment Evaluation Criteria2.6.1 Investment Decision Rule; 2.6.2 Evaluation Criteria

2.7 Net Present Value Method2.7.1 Why is NPV Important?; 2.7.2 Acceptance Rule; 2.7.3 Evaluation of the NPV Method

2.8 Internal Rate of Return Method2.8.1 Uneven Cash Flows: Calculating IRR by Trial and Error; 2.8.2 Level Cash Flows;2.8.3 NPV Profile and IRR; 2.8.4 Acceptance Rule; 2.8.5 Evaluation of IRR Method

2.9 Profitability Index2.9.1 Acceptance Rule; 2.9.2 Evaluation of PI Method

2.10 Payback2.10.1 Acceptance Rule; 2.10.2 Evaluation of Payback;2.10.3 Payback Reciprocal and the Rate of Return

2.11 Discounted Payback Period2.12 Accounting Rate of Return Method

2.12.1 Acceptance Rule; 2.12.2 Evaluation of ARR Method2.13 NPV Versus IRR

2.13.1 Equivalence of NPV and IRR: Case of Conventional Independent Projects2.13.2 Lending and Borrowing-type Projects2.13.3 Non-Conventional Investments: Problem of Multiple IRRs2.13.4 Difference: Case of Ranking Mutually Exclusive Projects

2.14 Reinvestment Assumption and Modified Internal Rate of Return (MIRR)2.15 Varying Opportunity Cost of Capital2.16 ENP Versus PI2.17 Investment Decisions under Capital Rationing

2.17.1 Why Capital Rationing; 2.17.2 External Capital Rationing; 2.17.3 Internal Capital Rationing2.17.4 Use of Profitability Index in Capital Rationing; 2.17.5 Limitations of Profitability Index

2.18 Let us Summarize2.19 Key Concepts2.20 Illustrative Solved Problems2.21 Answers to ‘Check Your Progrees’2.22 Questions and Exercises

2.0 INTRODUCTION

An efficient allocation of capital is the most important finance function in the modern times. Itinvolves decisions to commit the firm’s funds to the long-term assets. Capital budgeting orinvestment decisions are of considerable importance to the firm since they tend to determine its

Financial Management

26 Self-Instructional Material

NOTES

value by influencing its growth, profitability and risk. In this unit we focus on the nature andevaluation of capital budgeting decisions.

2.1 UNIT OBJECTIVES

Understand the nature and importance of investment decisions Understand the capital budgeting and investment proccess including planning and control Explain the methods of calculating net present value (NPV) and internal rate of return (IRR) Show the implications of net present value (NPV) and internal rate of return (IRR) Describe the non-DCF evaluation criteria: payback and accounting rate of return Illustrate the computation of the discounted payback Compare and contract NPV and IRR and emphasise the superiority of NPV rule Understand how to take investment decisions under capital rationing

2.2 NATURE OF INVESTMENT DECISIONS

The investment decisions of a firm are generally known as the capital budgeting, or capitalexpenditure decisions. A capital budgeting decision may be defined as the firm’s decision toinvest its current funds most efficiently in the long-term assets in anticipation of an expected flowof benefits over a series of years. The long-term assets are those that affect the firm’s operationsbeyond the one-year period. The firm’s investment decisions would generally include expansion,acquisition, modernisation and replacement of the long-term assets. Sale of a division or business(divestment) is also as an investment decision. Decisions like the change in the methods of salesdistribution, or an advertisement campaign or a research and development programme have long-term implications for the firm’s expenditures and benefits, and therefore, they should also beevaluated as investment decisions. It is important to note that investment in the long-term assetsinvariably requires large funds to be tied up in the current assets such as inventories andreceivables. As such, investment in fixed and current assets is one single activity.

The following are the features of investment decisions:

The exchange of current funds for future benefits. The funds are invested in long-term assets. The future benefits will occur to the firm over a series of years.

It is significant to emphasise that expenditures and benefits of an investment should be measuredin cash. In the investment analysis, it is cash flow, which is important, not the accounting profit.It may also be pointed out that investment decisions affect the firm’s value. The firm’s value willincrease if investments are profitable and add to the shareholders’ wealth. Thus, investmentsshould be evaluated on the basis of a criterion, which is compatible with the objective of theshareholders’ wealth maximisation. An investment will add to the shareholders’ wealth if it yieldsbenefits in excess of the minimum benefits as per the opportunity cost of capital. In this unit, weassume that the investment project’s opportunity cost of capital is known. We also assume thatthe expenditures and benefits of the investment are known with certainty. Both these assumptionsare relaxed in later units.

2.2.1 Importance of Investment Decisions

Investment decisions require special attention because of the following reasons:1

They influence the firm’s growth in the long run They affect the risk of the firm They involve commitment of large amount of funds They are irreversible, or reversible at substantial loss They are among the most difficult decisions to make.

1. See Quirin, G.D., The Capital Expenditure Decision, Richard D. Irwin, 1977.

Capital Budgeting Decisions

Self-Instructional Material 27

NOTES

Growth The effects of investment decisions extend into the future and have to be endured fora longer period than the consequences of the current operating expenditure. A firm’s decision toinvest in long-term assets has a decisive influence on the rate and direction of its growth. Awrong decision can prove disastrous for the continued survival of the firm; unwanted orunprofitable expansion of assets will result in heavy operating costs to the firm. On the otherhand, inadequate investment in assets would make it difficult for the firm to compete successfullyand maintain its market share.

Risk A long-term commitment of funds may also change the risk complexity of the firm. If theadoption of an investment increases average gain but causes frequent fluctuations in its earnings,the firm will become more risky. Thus, investment decisions shape the basic character of a firm.

Funding Investment decisions generally involve large amount of funds, which make it imperativefor the firm to plan its investment programmes very carefully and make an advance arrangementfor procuring finances internally or externally.

Irreversibility Most investment decisions are irreversible. It is difficult to find a market for suchcapital items once they have been acquired. The firm will incur heavy losses if such assets arescrapped.

Complexity Investment decisions are among the firm’s most difficult decisions. They are anassessment of future events, which are difficult to predict. It is really a complex problem tocorrectly estimate the future cash flows of an investment. Economic, political, social andtechnological forces cause the uncertainty in cash flow estimation.

2.3 TYPES OF INVESTMENT DECISIONS

There are many ways to classify investments. One classification is as follows:

Expansion of existing business

Expansion of new business

Replacement and modernisation.

2.3.1 Expansion and Diversification

A company may add capacity to its existing product lines to expand existing operations. Forexample, the Gujarat State Fertiliser Company (GSFC) may increase its plant capacity to manufacturemore urea. It is an example of related diversification. A firm may expand its activities in a newbusiness. Expansion of a new business requires investment in new products and a new kind ofproduction activity within the firm. If a packaging manufacturing company invests in a new plantand machinery to produce ball bearings, which the firm has not manufactured before, thisrepresents expansion of new business or unrelated diversification. Sometimes a company acquiresexisting firms to expand its business. In either case, the firm makes investment in the expectationof additional revenue. Investments in existing or new products may also be called as revenue-expansion investments.

2.3.2 Replacement and Modernisation

The main objective of modernisation and replacement is to improve operating efficiency and reducecosts. Cost savings will reflect in the increased profits, but the firm’s revenue may remain unchanged.Assets become outdated and obsolete with technological changes. The firm must decide to replacethose assets with new assets that operate more economically. If a cement company changes fromsemi-automatic drying equipment to fully automatic drying equipment, it is an example ofmodernisation and replacement. Replacement decisions help to introduce more efficient andeconomical assets and therefore, are also called cost-reduction investments. However, replacementdecisions that involve substantial modernisation and technological improvements expand revenuesas well as reduce costs.

Yet another useful way to classify investments is as follows:

Mutually exclusive investments

Check Your Progress

1. How do we usually definecapital budgeting decisions?

2. How do we usually definelong term assets?

3. What type of decisions maybe termed as a firm’s longterm investment decisions?

4. Why do investmentdecisions require specialattention from a firm’smanagement?

Financial Management

28 Self-Instructional Material

NOTES

Independent investments

Contingent investments.

2.3.3 Mutually Exclusive Investments

Mutually exclusive investments serve the same purpose and compete with each other. If oneinvestment is undertaken, others will have to be excluded. A company may, for example, eitheruse a more labour-intensive, semi-automatic machine, or employ a more capital-intensive, highlyautomatic machine for production. Choosing the semi-automatic machine precludes the acceptanceof the highly automatic machine.

2.3.4 Independent Investments

Independent investments serve different purposes and do not compete with each other. Forexample, a heavy engineering company may be considering expansion of its plant capacity tomanufacture additional excavators and addition of new production facilities to manufacture anew product—light commercial vehicles. Depending on their profitability and availability offunds, the company can undertake both investments.

2.3.5 Contingent Investments

Contingent investments are dependent projects; the choice of one investment necessitatesundertaking one or more other investments. For example, if a company decides to build a factoryin a remote, backward area, it may have to invest in houses, roads, hospitals, schools etc. foremployees to attract the work force. Thus, building of factory also requires investment in facilitiesfor employees. The total expenditure will be treated as one single investment.

2.4 CAPITAL BUDGETING PROCESS

Capital expenditure or investment planning and control involve a process of facilitating decisionscovering expenditures on long-term assets. Since a company’s survival and profitability hingeson capital expenditures, especially the major ones, the importance of the capital budgeting orinvestment process cannot be over-emphasised. A number of managers think that investmentprojects have strategic elements, and the investment analysis should be conducted within theoverall framework of corporate strategy. Some managers feel that the qualitative aspects ofinvestment projects should be given due importance.

2.4.1 Capital Investments

Strictly speaking, capital investments should include all those expenditures, which are expectedto produce benefits to the firm over a long period of time, and encompass both tangible andintangible assets. Thus R&D (research and development) expenditure is a capital investment.Similarly, the expenditure incurred in acquiring a patent or brand is also a capital investment. Inpractice, a number of companies follow the traditional definition, covering only expenditures ontangible fixed assets as capital investments (expenditures). The Indian companies are also influencedconsiderably by accounting conventions and tax regulations in classifying capital expenditures.Large expenditures on R&D, advertisement, or employees training, which tend to create valuableintangible assets, may not be included in the definition of capital investments since most of themare allowed to be expensed for tax purposes in the year in which they are incurred. From the pointof view of sound decision-making, these expenditures should be treated as capital investmentsand subjected to proper evaluation.

A number of companies follow the accounting convention to prepare asset wise classification ofcapital expenditures, which is hardly of much use in decision-making. Some companies classifycapital expenditures in a manner, which could provide useful information for decision-making.Their classification is (i) replacement, (ii) modernisation, (iii) expansion, (iv) new project, (v)research and development, (vi) diversification, and (vii) cost reduction.

Check Your Progress

5. How do we classifydifferent types ofinvestment decisions?

6. Distinguish betweenexpansion anddiversification projects vis-à-vis replacement andmodernization projects.

Capital Budgeting Decisions

Self-Instructional Material 29

NOTES

2.4.2 Capital Investment Planning And Control

At least five phases of capital expenditure planning and control can be identified:

Identification (or origination) of investment opportunities

Development of forecasts of benefits and costs

Evaluation of the net benefits

Authorisation for progressing and spending capital expenditure

Control of capital projects.

The available literature puts the maximum emphasises on the evaluation phase. Two reasons maybe attributed to this bias. First, this phase is easily amenable to a structured, quantitative analysis.Second, it is considered to be the most important phase by academicians. Practitioners, on theother hand, consider other phases to be more important.2 The capital investment planning andcontrol phases are discussed below.

Investment Ideas: Who Generates? Investment opportunities have to be identified or created;they do not occur automatically.3, 4 Investment proposals of various types may originate atdifferent levels within a firm. Most proposals, in the nature of cost reduction or replacement orprocess or product improvements take place at plant level. The contribution of top managementin generating investment ideas is generally confined to expansion or diversification projects. Theproposals may originate systematically or haphazardly in a firm. The proposal for adding a newproduct may emanate from the marketing department or from the plant manager who thinks of abetter way of utilising idle capacity. Suggestions for replacing an old machine or improving theproduction techniques may arise at the factory level. In view of the fact that enough investmentproposals should be generated to employ the firm’s funds fully well and efficiently, a systematicprocedure for generating proposals may be evolved by a firm.

In a number of Indian companies, the investment ideas are generated at the plant level. Thecontribution of the board in idea generation is relatively insignificant. However, some companiesdepend on the board for certain investment ideas, particularly those that are strategic in nature.Other companies depend on research centres for investment ideas.

Is the investment idea generation primarily a bottom-up process in India? In UK, both bottom-up,as well as top-down processes exist.5 The Indian practice is more like that in USA. Project initiationis a bottom-up process in USA, with about more than three-fourths of investment proposalscoming from divisional management and plant personnel.6 However, we should note that thesmall number of ideas generated at the top may represent a high percentage in terms of investmentvalue, so that what looks to be an entirely bottom-up process may not be really so.

Indian companies use a variety of methods to encourage idea generation. The most commonmethods used are: (a) management sponsored studies for project identification, (b) formalsuggestion schemes, and (c) consulting advice. Most companies use a combination of methods.The offer of financial incentives for generating investment idea is not a popular practice. Otherefforts employed by companies in searching investment ideas are: (a) review of researches donein the country or abroad, (b) conducting market surveys, and (c) deputing executives to internationaltrade fairs for identifying new products/technology.

Once the investment proposals have been identified, they are be submitted for scrutiny. Manycompanies specify the time for submitting the proposals for scrutiny.

2. Hastie, K. L., One Businessman’s View of Capital Budgeting, Financial Management, 3 (Writer 1974),pp. 36, 196.

3. Haynes, W.W. and Solomon, M.B., A Misplaced Emphasis in Capital Budgeting, Quarterly Review ofEconomics and Business, (Jan.-Feb. 1964), pp. 95–106.

4. King, P., Is the Emphasis of Capital Budgeting Theory Misplaced? Journal of Business Finance andAccounting, (Spring 1975), pp. 69–82.

5. Rockley, L.E., Investment for Profitability, Business Books, 1973.6. Petty, J.W., and Scott, D.F., Capital Budgeting Practices in large US Firms: A Retrospective Analysis

and Update, in Derkindem and Crum (Ed.), Readings in Strategy for Corporate Investments, Pitman,1981.

Financial Management

30 Self-Instructional Material

NOTES

Developing Cash Flow Estimates Estimation of cash flows is a difficult task because thefuture is uncertain. Operating managers with the help of finance executives should develop cashflow estimates. The risk associated with cash flows should also be properly handled and shouldbe taken into account in the decision making process. Estimation of cash flows requires collectionand analysis of all qualitative and quantitative data, both financial and non-financial in nature.Large companies would generally have a management information system (MIS) providing suchdata.

Executives in practice do not always have clarity about estimating cash flows. A large number ofcompanies do not include additional working capital while estimating the investment project cashflows. A number of companies also mix up financial flows with operating flows. Although companiesclaim to estimate cash flows on incremental basis, some of them make no adjustment for saleproceeds of existing assets while computing the project’s initial cost. The prevalence of suchconceptual confusion has been observed even in the developed countries. For example, in theseventies, a number of UK companies were treating depreciation as cash flows.7

In the past, most Indian companies chose an arbitrary period of 5 or 10 years for forecastingcash flows. This was so because companies in India largely depended on government-ownedfinancial institutions for financing their projects, and these institutions required 5 to 10 yearsforecasts of the project cash flows.

Project Evaluation The evaluation of projects should be performed by a group of experts whohave no axe to grind. For example, the production people may be generally interested in havingthe most modern type of equipments and increased production even if productivity is expected tobe low and goods cannot be sold. This attitude can bias their estimates of cash flows of theproposed projects. Similarly, marketing executives may be too optimistic about the sales prospectsof goods manufactured, and overestimate the benefits of a proposed new product. It is, therefore,necessary to ensure that projects are scrutinised by an impartial group and that objectivity ismaintained in the evaluation process.

A company in practice should take all care in selecting a method or methods of investmentevaluation. The criterion selected should be a true measure of the investment’s profitability (interms of cash flows), and it should lead to the net increase in the company’s wealth (that is, itsbenefits should exceed its cost adjusted for time value and risk). It should also be seen that theevaluation criteria do not discriminate between the investment proposals. They should be capableof ranking projects correctly in terms of profitability. The net present value method is theoreticallythe most desirable criterion as it is a true measure of profitability; it generally ranks projectscorrectly and is consistent with the wealth maximisation criterion. In practice, however, managers’choice may be governed by other practical considerations also.

A formal financial evaluation of proposed capital expenditures has become a common practiceamong companies in India. A number of companies have a formal financial evaluation of almostthree-fourths of their investment projects. Most companies subject more than 50 per cent of theprojects to some kind of formal evaluation. However, projects, such as replacement or worn-outequipment, welfare and statutorily required projects below certain limits, small value items likeoffice equipment or furniture, replacement of assets of immediate requirements, etc., are not oftenformally evaluated.

Methods of Evaluation As regards the use of evaluation methods, most Indian companiesuse payback criterion. In addition to payback and/or other methods, companies also use internalrate of return (IRR) and net present (NPV) methods. A few companies use accounting rate ofreturn (ARR) method. IRR is the second most popular technique in India.

The major reason for payback to be more popular than the DCF techniques is the executives’ lackof familiarity with DCF techniques. Other factors are lack of technical people and sometimesunwillingness of top management to use the DCF techniques. One large manufacturing andmarketing organisation, for example, thinks that conditions of its business are such that the DCFtechniques are not needed. By business conditions the company perhaps means its marketingnature, and its products being in seller’s markets. Another company feels that replacement projects

7. Rockley, op. cit.

Capital Budgeting Decisions

Self-Instructional Material 31

NOTES

8. Schall, L.D., Sundem, G.L. and Geijsbeak, W.R., Survey and Analysis of Capital Budgeting Methods,Journal of Finance, (March 1978), pp. 281–87.

9. Rockley, op. cit.10. Pike, R.H., Capital Budgeting Survey: An Update, Bradford University Discussion Paper, 1992.11. Pandey, I.M., Financing Decision: A Survey of Management Understanding, Management Review:

Economic & Political Weekly, (Feb. 1984), pp. 27–31.12. Petty and Scott, op. cit.13. Rockley, op. cit.

are very frequent in the company, and therefore, it is not necessary to use the DCF techniques forsuch projects. Both these companies have fallacious approaches towards investment analysis.They should subject all capital expenditures to formal evaluation.

The practice of companies in India regarding the use of evaluation criteria is similar to that inUSA. Almost four-fifths of US firms use either the internal rate of return or net present valuemodels, but only about one-fifth use such discounting techniques without using the paybackperiod or average rate of return methods.8 The tendency of US firms to use naive techniques assupplementary tools has also been reported in recent studies. However, firms in USA have cometo depend increasingly on the DCF techniques, particularly IRR. The British companies use bothDCF techniques and return on capital, sometimes in combination sometimes solely, in theirinvestment evaluation; the use of payback is widespread.9 In recent years the use of the DCFmethods has increased in UK, and NPV is more popular than IRR.10 However, this increase hasnot reduced the importance of the traditional methods such as payback and return on investment.Payback continues to be employed by almost all companies.

One significant difference between practices in India and USA is that payback is used in India asa ‘primary’ method and IRR/NPV as a ‘secondary’ method, while it is just the reverse in USA.Indian managers feel that payback is a convenient method of communicating an investment’sdesirability, and it best protects the recovery of capital—a scarce commodity in the developingcountries.

Cut-off Rate In the implementation of a sophisticated evaluation system, the use of a minimumrequired rate of return is necessary. The required rate of return or the opportunity cost of capitalshould be based on the riskiness of cash flows of the investment proposal; it is compensation toinvestors for bearing the risk in supplying capital to finance investment proposals.

Not all companies in India specify the minimum acceptable rate of return. Some of them computethe weighted average cost of capital (WACC) as the discount rate. Unfortunately, all companiesdo not follow correct methodology of calculating the WACC. Almost all companies use the bookvalue weights.

Business executives in India are becoming increasingly aware of the importance of the cost ofcapital, but they perhaps lack clarity about its computation. Arbitrary judgment of managementalso seems to play a role in the assessment of the cost of capital. The fallacious tendency ofequating borrowing rate with minimum required rate of return also persists in the case of somecompanies.11 In USA, a little more than 50 per cent companies have been found using WACC ascut-off rate.12 In UK, only a very small percentage of firms were found attempting any calculationof the cost of capital.13 As in USA and UK, companies in India have a tendency to equate theminimum rate with interest rate or cost of specific source of finance. The phenomenon of dependingon management judgement for the assessment of the cost of capital is prevalent as much in USAand UK as in India.

Recognition of Risk The assessment of risk is an important aspect of an investment evaluation.In theory, a number of techniques are suggested to handle risk. Some of them, such as the computersimulation technique are not only quite involved but are also expensive to use. How do companieshandle risk in practice?

Companies in India consider the following as the four most important contributors of investmentrisk: selling price, product demand, technological changes and government policies. India isfast changing from sellers’ market to buyers’ market as competition is intensifying in a largenumber of products; hence uncertainty of selling price and product demand are being realised as

Financial Management

32 Self-Instructional Material

NOTES

important risk factors. Uncertain government policies (in areas such as custom and excise dutyand import policy, the foreign investment etc.), of course, are a continuous source of investmentrisk in developing countries like India.

Sensitivity analysis and conservative forecasts are two equally important and widely used methodsof handling investment risk in India. Each of these techniques is used by a number of Indiancompanies with other methods while many other companies use either sensitivity analysis orconservative forecasts with other methods. Some companies also use shorter payback and inflateddiscount rates (risk-adjusted discount rates).

In USA, risk adjusted discount rate is more popular than the use of payback and sensitivityanalysis.14, 15 The British companies hardly use sensitivity analysis.16 The contrasts in riskevaluation practices in India, on the one hand, and USA and UK, on the other, are sharp andsignificant. Given the complex nature of risk factors in developing countries, risk evaluationcannot be handled through a single number such as the NPV calculation based on conservativeforecasts or risk-adjusted discount rate. Managers must know the impact on project profitabilityof the full range of critical variables. An American businessman states: “there appear to be morecorporations using sensitivity analysis than surveys indicate. In some cases firms may not knowthat what they are undertaking is called ‘sensitivity analysis’, and it probably is not in thesophisticated, computer oriented sense... Typically, analysts or middle managers eliminate thealternative assumptions and solutions in order to simplify the decision- making process forhigher management.”17

Capital Rationing Indian companies, by and large, do not have to reject profitable investmentopportunities for lack of funds, despite the capital markets not being so well developed. This maybe due to the existence of the government-owned financial system, which is always ready to financeprofitable projects. Indian companies do not use any mathematical technique to allocate resourcesunder capital shortage which may sometimes arise on account of internally imposed restrictionsor management’s reluctance to raise capital from outside. Priorities for allocating resources aredetermined by management, based on the strategic need for and profitability of projects.

Authorisation It may not be feasible in practice to specify standard administrative proceduresfor approving investment proposals. Screening and selection procedures may differ from onecompany to another. When large sums of capital expenditures are involved, the authority for thefinal approval may rest with top management. The approval authority may be delegated forcertain types of investment projects. Delegation may be affected subject to the amount of outlay,prescribing the selection criteria and holding the authorised person accountable for results.

Funds are appropriated for capital expenditures after the final selection of investment proposals.The formal plan for the appropriation of funds is called the capital budget. Generally, the seniormanagement tightly controls the capital expenditures. Budgetary controls may be rigidly exercised,particularly when a company is facing liquidity problem. The expected expenditure should becomea part of the annual capital budget, integrated with the overall budgetary system.

Top management should ensure that funds are spent in accordance with appropriations made inthe capital budget. Funds for the purpose of project implementation should be spent only afterseeking formal permission from the financial manager or any other authorised person.

In India, as in UK, the power to commit a company to specific capital expenditure and to examineproposals is limited to a few top corporate officials. However, the duties of processing theexamination and evaluation of a proposal are somewhat spread throughout the corporatemanagement staff in case of a few companies.

Senior management tightly control capital spending. Budgetary control is also exercised rigidly.The expected capital expenditure proposals invariably become a part of the annual capital budgetin all companies. Some companies also have formal long-range plans covering a period of 3 to 5

14. Schall et al., op. cit.15. Petty and Scott, op. cit.16. Rockley, op. cit.17. Hastie, op. cit.

Capital Budgeting Decisions

Self-Instructional Material 33

NOTES

years. Some companies feel that long-range plans have a significant influence on the evaluationand funding of capital expenditure proposals.

Control and Monitoring A capital investment reporting system is required to review andmonitor the performance of investment projects after completion and during their life. The follow-up comparison of the actual performance with original estimates not only ensures better forecastingbut also helps to sharpen the techniques for improving future forecasts. Based on the follow-upfeedback, the company may reappraise its projects and take remedial action.

Indian companies practice control of capital expenditure through the use of regular project reports.Some companies require quarterly reporting, others need monthly, half-yearly and yet a fewcompanies require continuous reporting. In most of the companies, the evaluation reports includeinformation on expenditure to date, stage of physical completion, and approved and revised totalcost.

Most of the companies in reappraising investment proposals, consider comparison betweenactual and forecast capital cost, saving and rate of return. They perceive the following advantagesof reappraisal: (i) improvement in profitability by positioning the project as per the original plan;(ii) ascertainment of errors in investment planning which can be avoided in future;(iii) guidance for future evaluation of projects; and (iv) generation of cost consciousness amongthe project team. A few companies abandon the project if it becomes uneconomical. The power ofreview is generally invested with the top executives of the companies in India.

2.5 TIME VALUE OF MONEY

The DCF criteria of investment evaluation are based on the concept of time value of money. Thetime value of money has its logic in the fact that investors have ample investment opportunitiesavailable to them, and therefore, one rupee received today is not same in value as one rupeereceived after a period of time since one rupee received today can be invested at a rate of interest.The rate of interest depends on the risk of investment. Higher the risk, higher the rate of interestexpected. If there is no risk, the rate of interest (called risk-free rate) will be low, say, 5–10 per cent.

There are basically two ways for accounting for the time value of money:

Compounding

Discounting

2.5.1 Compounding

Suppose that an investor can invest Rs 100 today in a bank at an interest of 12 per cent for oneyear. How much amount would he receive after a year? He will receive his principal as well asinterest on the principal. That is; 100 + 12% × 100 = 100 × 112% = 100 × 1.12 = Rs 112. Notice thatRs 112 is the compound or future value (F) of the present amount (P) of Rs 100 at an interest rateof (i) of 12 per cent for a period (n) of one year. Thus

F = P + iP = P (1 + i) = 100 (1.12) = Rs 112.

If the investment is made for two years, the investor will receive interest on the interest amountearned during the first year:

F = P (1 + i) (1 + i) = P (1 + i)2 = 100 (1.12)2 = 100 (1.2544) = Rs 125.44

Similarly the present amount of Rs 100 invested at 12 per cent for 3 years will grow to:F = 100 (1.12) (1.12) (1.12) = 100 (1.12)3 = 100 (1.4049) = Rs 140.49; for 4 years:100 (1.12) (1.12) (1.12) (1.12) = 100 (1.12)4 = 100 (1.5735) = Rs 157.35 and so on.

Compound Value of a Lump Sum From the preceding discussion, we can write the formulafor calculating the future value (F) of a lump sum today (P) at a given rate of interest (i) for givenperiod of time (n) as follows:

F = P (1 + i)n (1)

Check Your Progress

7. What type of expendituresshould be included in capitalinvestments?

8. List the major phases ofcapital expenditure planningand control.

9. What are the main methodsof evaluating capitalinvestment projects?

Financial Management

34 Self-Instructional Material

NOTES

The term (1 + i)n is the compound (future) value factor, of Re 1 for a given rate of interest, i andtime period, n, i.e. CVF, i, n. It always has a value greater than 1 for positive i, indicating that CVFincreases with increase in either i or n or both.

In the earlier example, the values 1.12, 1.2544, 1.4049 and 1.5735 are CVF of Re 1 at 12 per cent rateof interest respectively for year 1, 2, 3 and 4. Using Eq. (1) CVFs can be calculated for anycombination of interest rate and time period. Table A in Appendix at the end of the book providesprecalculated CVFs for a range of periods and rates of interest.

Illustration 2.1

Jacob is considering investing of Rs 15,000 in a public sector company’s bonds at a rate of interest of 16 percent per year for 7 years. How much amount would he get after 7 years? The compound value can be foundas follows:

F = 15,000 (1.16)7 = 15,000 × CVF, .16, 7

The term (1.16)7 gives CVF, which can be obtained from Table A in the Appendix. Reading through seventhrow for 7 year period and 16 per cent column, we get CVF of 2.826. Thus the compound half-yearly, forfinding out the compound value of the lump sum of Rs 15,000 invested today at 16 per cent per annum for7 years is:

F = 15,000 × 2.826 = Rs 42,390

Multiperiod Compounding Let us assume in Illustration 2.1 that the company will compoundinterest half-yearly (semi-annually) instead of annually. Investor will gain as he will get intereston half-yearly interest. Since interest will be compounded half-yearly, for finding out the compoundvalue in Illustration 2.1, the half-yearly interest rate of 8 per cent and 14 half yearly periods will beconsidered:

F = 2

12

niP (2)

= 7 2

.1615,000 12

= 15,000 (1.08)14

From Table A in the Appendix, we find that CVF at 8 per cent interest for 14 periods is 2.937. Thus,the compound value of Rs 15,000 is:

F = 15,000 × 2.937 = Rs 44,055

Would the compound value of Jacob’s investment of Rs 15,000 be different if the companycompounds interest quarterly? The quarterly rate of interest will be 4 per cent and number ofquarterly periods will be 28. Thus

F = 4

14

niP = 15,000

7 4.1614

= 15,000 (1.04)28 = 15,000 (2.999) = Rs 44.995

We can observe that the compound value increases further under quarterly compounding.

The phenomenon of compounding interest more than once in a year is called multiperiodcompounding. The compound value increases as the frequency of compounding in a year increases.Eq. (1) can be modified as follows to find compound value under multiperiod compound:

F = 1

n miPm

where m is the number of compounding in a year.

Compound Value of an Annuity An annuity is a fixed payment or receipt of each period fora specified number of periods. Let us assume that an investor decides to deposit Rs 100 at the endof each for 4 years at 10 per cent rate of interest. Thus Rs 100 deposited at the end of first year willcompound for 3 years, Rs 100 at the end of second year for 2 years, Rs 100 at the end of third yearfor one year and Rs 100 at the end of fourth year would remain constant. Thus the compoundvalue will be as given below:

Capital Budgeting Decisions

Self-Instructional Material 35

NOTES

End of year 1F = 100 (1.10)3 = 100 (1.331) = 331.1

2F = 100 (1.10)2 = 100 (1.210) = 121.0

3F = 100 (1.10)1 = 100 (1.100) = 110.0

4F = 100 (1.10)0 = 100 (1.000) = 100.0

Total compound value 100 (4.641) = 464.1

As can be observed from the table, we can obtain the compound value of an annuity (A) byaggregating CVFs for the given periods and then multiplying by the amount of annuity. Forexample:

F = A (1 + i)3 + A (1 + i)2 + A (1 + i) + A = A [(1 + i)3 + (1 + i)2 + (1 + i) + 1]

= 100 [(1.10)3 + (1.10)2 + (1.10)1 + 1] = 100 [1.331 + 1.210 + 1.100 + 1]

= 100 (4.641) = Rs 464.1

The factor 4.641 is the compound value factor of an annuity of Re 1 for 4 years at 10 per cent rateof interest. A short-cut formula for calculating the compound value of an annuity is as follows:

F = A(1 ) 1

ni

i(3)

The expression [(1 + i)n – 1] i gives the compound value factor for an annuity of Re 1 for a givenrate of interest, i and time period, n, i.e., CVAF, i, n. Table B in the Appendix at the end of the bookprovides precalculated compound value factor for an annuity, CVFA, of Re 1 for a range ofinterest rates and periods of time.

Illustration 2.2

A person deposits Rs 10,000 at the end of each year for 5 years at 12 per cent rate of interest. How muchwould the annuity accumulate to at the end of the fifth year?

Looking up the fifth row and 12 per cent column in Table B, we obtain CVAF of 6.353. Thus

F = A (CVAF, 12%, 5) = 10,000 × 6.353 = Rs 63,530

If the interest is compounded quarterly, how much will be the compound value? For quarterly compounding,interest rate of 3 per cent and time period of 20 periods will be considered. Returning to Table B we find that:

F = 2,500 × 26.870 = Rs 67,175

Sinking Fund Suppose you want to accumulate Rs 4,00,000 at the end of 10 years to pay forthe acquisition of a flat. If the interest rate is 12 per cent, how much amount should you investeach year so that it grows to Rs 4,00,000 at the end of 10 years? This is a sinking fund problem.A fund which is created out of fixed payments each year for a specified period of time is calledsinking fund.

The desired sum of Rs 4,00,000 is the compound value of an annuity, say, A, at 12 per cent rate ofinterest for 10 years. Thus

F = A (CVAF, 12%, 10)

4,00,000 = A (17.549)

A = 4,00,000 (1/17.549)

= 4,00,000 (0.57) = Rs 22,800

It may be noticed that the future sum, Rs 4,00,000, is multiplied by the reciprocal of the compoundvalue annuity factor (CVAF, .057 = (1/17.549), to obtain the amount of annuity.

The reciprocal of CVAF is called the sinking fund factor (SFF).

2.5.2 Discounting

Suppose a bank offers to an investor to return a sum of Rs 115 in exchange for Rs 100 to bedeposited by the investor today. Should he accept the offer? His decision will depend on therate of interest which he can earn on his Rs 100 from an alternative investment of similar risk.

Financial Management

36 Self-Instructional Material

NOTES

Suppose the investor’s rate of interest is 11 per cent. The alternative investment opportunitywill provide the investor Rs 100 (1.11) = Rs 111 after a year. Since the bank is offering more thanthis amount, the investor should accept the offer. Let us ask a different question. Betweenwhat amount today (P) and Rs 115 after a year (F ), will the investor be indifferent? He will beindifferent to that amount of which Rs 115 is exactly equal to 111 per cent or 1.11 times. Thus

F = P (1 + i)

P = (1 )

Fi

115 = P (1.11)

P = 1151.11

= Rs 103.60

Note that Rs 103.60 invested today at 11 per cent grows to Rs 115 after a year. Rs 103.60 is thepresent or discounted value of Rs 115. That is:

F = P (1 + i)2

115 = P (1.11)2

therefore, P = 2(1 )

F

i

P = 2

115

(1.11) = 115 × 0.912

The formula for calculating the present value (P) of a lump sum in future (F) at a given rate ofinterest (i) for given periods of time is as follows:

F = P (1 + i)n

P = F1

(1 )

ni

(4)

The term 1/(1 + i)n provides the present value factor of Re 1 for a given rate of interest, i and timeperiod, n, i.e. PVF, i, n, (it may be written as PVF, i, n). It always has a value lesser than 1 forpositive i, indicating that PVF decreases with increase in either i or n or both. Table C in theAppendix at the end of the book provides precalculated PVFs.

Present Value of an Annuity Suppose Narsimham pays Rs 10,000 at the end of each year for5 years into a public provident fund. The interest rate being 12 per cent per year. What is thepresent value of the series of Rs 10,000 paid each year for 5 years? We can treat each payment asa lump sum and calculate the present value as follows:

End of year 1P = 1

110,000 = 10,000 0.893 = Rs 8,930(1.12)

2P = 2

110,000 = 10,000 0.797 = Rs 6,360(1.12)

3P = 3

110,000 = 10,000 0.712 = Rs 7,120(1.12)

4P = 4

110,000 = 10,000 0.636 = Rs 6,360(1.12)

5P = 5

110,000 = 10,000 0.576 = Rs 5,760(1.12)

10,000 × 3.614 = Rs 36,140

Capital Budgeting Decisions

Self-Instructional Material 37

NOTES

Aggregating PVFs (of a lump sum of Re 1) for the given periods and then multiplying by theamount of annuity. Thus

2 3 4 5

2 3 4 5

2 3 4 5

(1 ) (1 ) (1 ) (1 ) (1 )

1 1 1 1 1(1 ) (1 ) (1 ) (1 ) (1 )

1 1 1 1 110,000(1.12) (1.12) (1.12) (1.12) (1.12)

10,000 [0.893 0.797 0.712 0.636 0.576]

10,000 3.614 Rs

A A A A APi i i i i

Ai i i i i

36,140

The factor 3.614 is the present value factor of an annuity of Re 1 for 5 years at 12 per cent rate ofinterest. A short-cut formula for calculating the present value of an annuity is as follows:

11(1 )

niP A

i (5)

Table D in the Appendix at the end of the book provides precalculated present value factor for anannuity of Re 1 for a given rate of interest, i and time period, n, i.e. PVFA i, n, for a range of interestrates and periods of time.

Illustration 2.3

Anant Rao is considering of paying Rs 5,000 half-yearly into his public provident fund for 10 years.Suppose the interest rate is 12 per cent per annum. How much is the present value of his payment? Sincethe annuity is in terms of half-yearly payments, the number of periods to be considered is 20 and half-yearly interest to be 6 per cent. Referring to Table D of Appendix, the present value may be calculated asfollows:

P = 5,000 × PVAF, 6%, 20 = 5,000 × 11.470 = Rs 57,350

Capital Recovery The reciprocal of the present value annuity factor is called the capitalrecovery factor (CRF). It is useful in determining the income to be earned to recover an investmentat a given rate of interest.

Suppose Priyan is considering investing Rs 20,000 today for a period of 3 years. If he expects areturn of 16 per cent per year, how much annual income should he earn? The amount of Rs 20,000is the present value of a 3-year annuity, A, given the rate of interest of 15 per cent. Thus

= (PVAF, 16%, 3)

20,000 = (2.246)

120,000 20,000 0.445 Rs 8,9002.246

P A

A

A

It may be observed that the present sum, Rs 20,000, is multiplied by the reciprocal of the presentvalue annuity factor, PVAF, 0.445 = (1/2.246) to obtain the amount of annuity.

2.6 INVESTMENT EVALUATION CRITERIA

Three steps are involved in the evaluation of an investment:

Estimation of cash flows

Estimation of the required rate of return (the opportunity cost of capital)

Application of a decision rule for making the choice.

Financial Management

38 Self-Instructional Material

NOTES

The first two steps, discussed in the subsequent units, are assumed as given. Thus, our discussionin this unit is confined to the third step. Specifically, we focus on the merits and demerits ofvarious decision rules.

2.6.1 Investment Decision Rule

The investment decision rules may be referred to as capital budgeting techniques, or investmentcriteria. A sound appraisal technique should be used to measure the economic worth of aninvestment project. The essential property of a sound technique is that it should maximise theshareholders’ wealth. The following other characteristics should also be possessed by a soundinvestment evaluation criterion:18

It should consider all cash flows to determine the true profitability of the project.

It should provide for an objective and unambiguous way of separating good projects frombad projects.

It should help ranking of projects according to their true profitability.

It should recognise the fact that bigger cash flows are preferable to smaller ones and earlycash flows are preferable to later ones.

It should help to choose among mutually exclusive projects that project which maximises theshareholders’ wealth.

It should be a criterion which is applicable to any conceivable investment project independentof others.

These conditions will be clarified as we discuss the features of various investment criteria in thefollowing pages.

2.6.2 Evaluation Criteria

A number of investment criteria (or capital budgeting techniques) are in use in practice. They maybe grouped in the following two categories:

1. Discounted Cash Flow (DCF) Criteria

Net present value (NPV)

Internal rate of return (IRR)

Profitability index (PI)

2. Non-discounted Cash Flow Criteria

Payback period (PB)

Discounted payback period

Accounting rate of return (ARR).

Discounted payback is a variation of the payback method. It involves discounted cash flows,but, as we shall see later, it is not a true measure of investment profitability. We will show in thefollowing pages that the net present value criterion is the most valid technique of evaluating aninvestment project. It is consistent with the objective of maximising the shareholders’ wealth.

2.7 NET PRESENT VALUE METHOD

The net present value (NPV) method is the classic economic method of evaluating the investmentproposals. It is a DCF technique that explicitly recognises the time value of money. It correctlypostulates that cash flows arising at different time periods differ in value and are comparable onlywhen their equivalents—present values—are found out. The following steps are involved in thecalculation of NPV:

Check Your Progress

10. Which are the two maincategories in which wedivide the evaluationcriteria of capitalbudgeting decisions?

18. See Porterfield, J.T.S., Investment Decisions and Capital Costs, Prentice-Hall, 1965.

Capital Budgeting Decisions

Self-Instructional Material 39

NOTES

Cash flows of the investment project should be forecasted based on realistic assumptions.

Appropriate discount rate should be identified to discount the forecasted cash flows. Theappropriate discount rate is the project’s opportunity cost of capital, which is equal to therequired rate of return expected by investors on investments of equivalent risk.

Present value of cash flows should be calculated using the opportunity cost of capital as thediscount rate.

Net present value should be found out by subtracting present value of cash outflows from presentvalue of cash inflows. The project should be accepted if NPV is positive (i.e., NPV > 0).

Let us consider an example.

Illustration 2.4: Calculating Net Present Value

Assume that Project X costs Rs 2,500 now and is expected to generate year-end cash inflows of Rs 900,Rs 800, Rs 700, Rs 600 and Rs 500 in years 1 through 5. The opportunity cost of the capital may beassumed to be 10 per cent.

The net present value for Project X can be calculated by referring to the present value table (Table C at theend of the book). The calculations are shown below:

2 3 4 5

1, 0.10 2, 0.10 3, 0.10

4, 0.10 5, 0.10

Rs 900 Rs 800 Rs 700 Rs 600 Rs 500NPV Rs 2,500

(1+0.10) (1+0.10) (1+0.10) (1+0.10) (1+0.10)

NPV [Rs 900(PVF )+Rs 800(PVF )+Rs 700(PVF )

+Rs 600(PVF )+Rs 500(PVF )]

Rs 2,500

NPV [Rs 900 0.909+Rs 800 0.826+Rs 700 0.751+Rs 600 0.683+Rs 500 0.620] Rs 2,500

NPV Rs 2,725 Rs 2,500=+ Rs 225

Project X’s present value of cash inflows (Rs 2,725) is greater than that of cash outflow (Rs 2,500). Thus,it generates a positive net present value (NPV = + Rs 225). Project X adds to the wealth of owners;therefore, it shoul d be accepted.

The formula for the net present value can be written as follows:

n

tt

t

nn

Ck

C

Ck

C

k

C

k

C

k

C

10

033

221

)1(NPV

)1()1()1()1(NPV

(6)

where C1, C2... represent net cash inflows in year 1, 2..., k is the opportunity cost of capital, C0 isthe initial cost of the investment and n is the expected life of the investment. It should be notedthat the cost of capital, k, is assumed to be known and is constant.

2.7.1 Why is NPV Important?

A question may be raised: why should a financial manager invest Rs 2,500 in Project X? Project Xshould be undertaken if it is best for the company’s shareholders; they would like their shares tobe as valuable as possible. Let us assume that the total market value of a hypothetical companyis Rs 10,000, which includes Rs 2,500 cash that can be invested in Project X. Thus the value of thecompany’s other assets must be Rs 7,500. The company has to decide whether it should spend cashand accept Project X or to keep the cash and reject Project X. Clearly Project X is desirable sinceits PV (Rs 2,725) is greater than the Rs 2,500 cash. If Project X is accepted, the total market valueof the firm will be: Rs 7,500 + PV of Project X = Rs 7,500 + Rs 2,725 = Rs 10,225; that is, an increaseby Rs 225. The company’s total market value would remain only Rs 10,000 if Project X were rejected.

Why should the PV of Project X reflect in the company’s market value? To answer this question,let us assume that a new company X with Project X as the only asset is formed. What is the valueof the company? We know from our earlier discussion on valuation of shares in Unit 3 that themarket value of a company’s shares is equal to the present value of the expected dividends. SinceProject X is the only asset of Company X, the expected dividends would be equal to the forecastedcash flows from Project X. Investors would discount the forecasted dividends at a rate of return

Financial Management

40 Self-Instructional Material

NOTES

expected on securities equivalent in risk to company X. The rate used by investors to discountdividends is exactly the rate, which we should use to discount cash flows of Project X. Thecalculation of the PV of Project X is a replication of the process, which shareholders will befollowing in valuing the shares of company X. Once we find out the value of Project X, as aseparate venture, we can add it to the value of other assets to find out the portfolio value.

The difficult part in the calculation of the PV of an investment project is the precise measurementof the discount rate. Funds available with a company can either be invested in projects or givento shareholders. Shareholders can invest funds distributed to them in financial assets. Therefore,the discount rate is the opportunity cost of investing in projects rather than in capital markets.Obviously, the opportunity cost concept makes sense when financial assets are of equivalentrisk as compared to the project.

Table 2.1: Interpretation of NPV

Amount outstanding Return on outstanding Total outstanding Repayment from Balancein the beginning amount at 10% flows cash at the end outstanding

Year Rs Rs Rs Rs Rs

1 2,725.00 272.50 2,997.50 900 2,097.50

2 2,097.50 209.75 2,307.25 800 1,507.25

3 1,507.25 150.73 1,657.98 700 957.98

4 957.98 95.80 1,053.78 600 453.78

5 453.78 45.38 499.16 500 (0.84)*

* Rounding off error.

An alternate interpretation of the positive net present value of an investment is that it representsthe maximum amount a firm would be ready to pay for purchasing the opportunity of makinginvestment, or the amount at which the firm would be willing to sell the right to invest withoutbeing financially worse-off. The net present value (Rs 225) can also be interpreted to representthe amount the firm could raise at the required rate of return (10%), in addition to the initial cash

Excel Application 2.1:Calculation of NPV

We can easily calculate NPV using the Excel financialfunction for NPV. The spreadsheet on the right side gives thecash flows of the project. We write the NPV formula in columnC8: =NPV(0.10,C3:C7)+C2. You may note that 0.10(10 per cent) is the discount rate. The project cash flows fromyear 1 through 5 are contained in column C3 through columnC7. The initial cash flow (that is, cash flow in year 0) is added.

A B C D E

1 Year Cash flow PVF at 10% PV

2 0 C0 –2500 1.000 –2500

3 1 C1 900 0.909 818

4 2 C2 800 0.826 661

5 3 C3 700 0.751 526

6 4 C4 600 0.683 410

7 5 C5 500 0.621 310

8 NPV 226 SUM(E2:E7) 226

9 NPV(0.1,C3:C7)+C2

1 0

Capital Budgeting Decisions

Self-Instructional Material 41

NOTES

outlay (Rs 2,500), to distribute immediately to its shareholders and by the end of the projects’ lifeto have paid off all the capital raised and return on it.19 The point is illustrated by the calculationsshown in Table 2.1.

Calculations in Table 2.1 are based on the assumption that the firm chooses to receive the cashbenefit resulting from the investment in the year it is made. Any pattern of cash receipts, suchthat the net present value is equal to Rs 225, can be selected. Thus, if the firm raises Rs 2,500 (theinitial outlay) instead of Rs 2,725 (initial outlay plus net present value) at 10 per cent rate of return,at the end of fifth year after having paid the principal sum together with interest, it would be leftwith Rs 363, whose present value at the beginning of the first year at 10 per cent discount rate isRs 225. It should be noted that the gain to shareholders would be more if the rate of raising moneyis less than 10 per cent. (Why?)

2.7.2 Acceptance Rule

It should be clear that the acceptance rule using the NPV method is to accept the investmentproject if its net present value is positive (NPV > 0) and to reject it if the net present value isnegative (NPV < 0). Positive NPV contributes to the net wealth of the shareholders, which shouldresult in the increased price of a firm’s share. The positive net present value will result only if theproject generates cash inflows at a rate higher than the opportunity cost of capital. A project withzero NPV (NPV = 0) may be accepted. A zero NPV implies that project generates cash flows at arate just equal to the opportunity cost of capital. The NPV acceptance rules are:

Accept the project when NPV is positive NPV > 0

Reject the project when NPV is negative NPV < 0

May accept the project when NPV is zero NPV = 0

The NPV method can be used to select between mutually exclusive projects; the one with thehigher NPV should be selected. Using the NPV method, projects would be ranked in order of netpresent values; that is, first rank will be given to the project with highest positive net presentvalue and so on.

2.7.3 Evaluation of the NPV Method

NPV is the true measure of an investment’s profitability. It provides the most acceptable investmentrule for the following reasons:

Time value It recognises the time value of money—a rupee received today is worth morethan a rupee received tomorrow.

Measure of true profitability It uses all cash flows occurring over the entire life of theproject in calculating its worth. Hence, it is a measure of the project’s true profitability. TheNPV method relies on estimated cash flows and the discount rate rather than any arbitraryassumptions, or subjective considerations.

Value-additivity The discounting process facilitates measuring cash flows in terms of presentvalues; that is, in terms of equivalent, current rupees. Therefore, the NPVs of projects can beadded. For example, NPV (A + B) = NPV (A) + NPV (B). This is called the value-additivityprinciple. It implies that if we know the NPVs of individual projects, the value of the firm willincrease by the sum of their NPVs. We can also say that if we know values of individualassets, the firm’s value can simply be found by adding their values. The value-additivity is animportant property of an investment criterion because it means that each project can beevaluated, independent of others, on its own merit.

Shareholder value The NPV method is always consistent with the objective of the shareholdervalue maximisation. This is the greatest virtue of the method.

Are there any limitations in using the NPV rule? The NPV method is a theoretically sound method.In practice, it may pose some computational problems.

19. Bierman, H. and Smidt, S., The Capital Budgeting Decision, Macmillan, 1975, p. 73.

Financial Management

42 Self-Instructional Material

NOTES

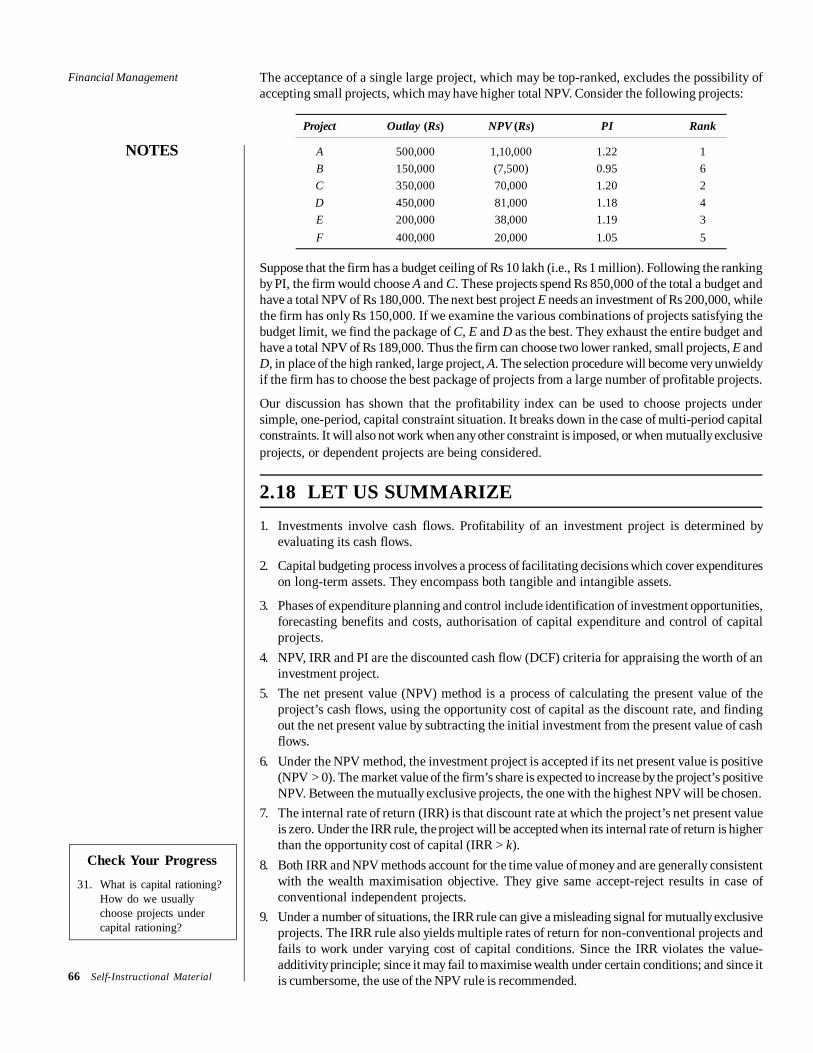

Cash flow estimation The NPV method is easy to use if forecasted cash flows are known. Inpractice, it is quite difficult to obtain the estimates of cash flows due to uncertainty.

Discount rate It is also difficult in practice to precisely measure the discount rate.

Mutually exclusive projects Further, caution needs to be applied in using the NPV methodwhen alternative (mutually exclusive) projects with unequal lives, or under funds constraintare evaluated. The NPV rule may not give unambiguous results in these situations.

Ranking of projects It should be noted that the ranking of investment projects as per theNPV rule is not independent of the discount rates.20 Let us consider an example.

Suppose two projects—A and B—both costing Rs 50 each. Project A returns Rs 100 after oneyear and Rs 25 after two years. On the other hand, Project B returns Rs 30 after one year andRs 100 after two years. At discount rates of 5 per cent and 10 per cent, the NPV of projects andtheir ranking are as follows:

NPV at 5% Rank NPV at 10% Rank

Project A 67.92 II 61.57 I

Project B 69.27 I 59.91 II

It can be seen that the project ranking is reversed when the discount rate is changed from 5 percent to 10 per cent. The reason lies in the cash flow patterns. The impact of the discountingbecomes more severe for the cash flow occurring later in the life of the project; the higher is thediscount rate, the higher would be the discounting impact. In the case of Project B, the larger cashflows come later in the life. Their present value will decline as the discount rate increases.

2.8 INTERNAL RATE OF RETURN METHOD

The internal rate of return (IRR) method is another discounted cash flow technique, which takesaccount of the magnitude and timing of cash flows.21 Other terms used to describe the IRR methodare yield on an investment, marginal efficiency of capital, rate of return over cost, time-adjusted rateof internal return and so on. The concept of internal rate of return is quite simple to understand inthe case of a one-period project. Assume that you deposit Rs 10,000 with a bank and would getback Rs 10,800 after one year. The true rate of return on your investment would be:

8%or,08.0108.1000,10000,10

800,10

000,10

10,00010,800return of Rate

The amount that you would obtain in the future (Rs 10,800) would consist of your investment(Rs 10,000) plus return on your investment (0.08 Rs 10,000):

10,000 (1.08) = 10,800

10,000 = 10,800

(1.08)

You may observe that the rate of return of your investment (8 per cent) makes the discounted(present) value of your cash inflow (Rs 10,800) equal to your investment (Rs 10,000).

We can now develop a formula for the rate of return (r) on an investment (C0) that generates asingle cash flow after one period (C1) as follows:

10

1

0

01

C

C

C

CCr (7)

Equation (7) can be rewritten as follows:

20. Bierman and Smidt, op. cit., p. 31.21. The use of IRR for appraising capital investment was emphasised in the formal terms, for the first time,

by Joel Dean. See, Dean, Joel, Capital Budgeting, Columbia University Press, 1951, and his article,Measuring the Productivity of Capital in Solomon, E. (Ed.), The Management of Corporate Capital.

Check Your Progress

11. Describe the basicapproach of calculatingthe net present value of aninvestment proposal.

12. Why is NPV methodconsidered perhaps thebest method for evaluatingthe profitability of aproject? Are there anydifficulties associated withthis method?

Capital Budgeting Decisions

Self-Instructional Material 43

NOTES)1(

1

10

0

1

r

CC

rC

C

(8)

From Equation (8), you may notice that the rate of return, r, depends on the project’s cash flows,rather than any outside factor. Therefore, it is referred to as the internal rate of return. Theinternal rate of return (IRR) is the rate that equates the investment outlay with the present valueof cash inflow received after one period. This also implies that the rate of return is the discountrate which makes NPV = 0. There is no satisfactory way of defining the true rate of return of along-term asset. IRR is the best available concept. We shall see that although it is a very frequentlyused concept in finance, yet at times it can be a misleading measure of investment worth.22 IRRcan be determined by solving the following equation for r:

n

tt

t

nn

r

CC

r

C

r

C

r

C

r

CC

10

33

221

0

)1(

)1()1()1()1(

0)1(

01

Cr

Cn

tt

t(9)

It can be noticed that the IRR equation is the same as the one used for the NPV method. In theNPV method, the required rate of return, k, is known and the net present value is found, while inthe IRR method the value of r has to be determined at which the net present value becomes zero.

2.8.1 Uneven Cash Flows: Calculating IRR by Trial and ErrorThe value of r in Equation (9) can be found out by trial and error. The approach is to select anydiscount rate to compute the present value of cash inflows. If the calculated present value of theexpected cash inflow is lower than the present value of cash outflows, a lower rate should betried. On the other hand, a higher value should be tried if the present value of inflows is higherthan the present value of outflows. This process will be repeated unless the net present valuebecomes zero. The following illustration explains the procedure of calculating IRR.

Illustration 2.5: Trial and Error Method for Calculating IRRA project costs Rs 16,000 and is expected to generate cash inflows of Rs 8,000, Rs 7,000 and Rs 6,000 atthe end of each year for next 3 years. We know that IRR is the rate at which project will have a zero NPV.As a first step, we try (arbitrarily) a 20 per cent discount rate. The project’s NPV at 20 per cent is:

1, 0.20 2, 0.20 3, 0.20NPV Rs 16,000+Rs 8,000(PVF )+Rs 7,000(PVF ) + Rs 6,000(PVF )

Rs 16,000+Rs 8,000 0.833+Rs 7,000 0.694 + Rs 6,000 0.579Rs 16,000+Rs 14,996= Rs 1,004

A negative NPV of Rs 1,004 at 20 per cent indicates that the project’s true rate of return is lower than 20 percent. Let us try 16 per cent as the discount rate. At 16 per cent, the project’s NPV is:

1, 0.16 2, 0.16 3, 0.16NPV Rs 16,000+Rs 8,000(PVF )+Rs 7,000(PVF )+Rs 6,000(PVF )Rs 16,000+Rs 8,000 0.862+Rs 7,000 0.743+Rs 6,000 0.641Rs 16,000+Rs 15,943= Rs 57

Since the project’s NPV is still negative at 16 per cent, a rate lower than 16 per cent should be tried. Whenwe select 15 per cent as the trial rate, we find that the project’s NPV is Rs 200:

1, 0.15 2, 0.15 3, 0.15NPV Rs 16,000 + Rs 8,000(PVF ) + Rs 7,000(PVF ) + Rs 6,000(PVF )Rs 16,000 + Rs 8,000 0.870 + Rs 7,000 0.756 + Rs 6,000 0.658Rs 16,000 + Rs 16,200 = Rs 200

22. Brealey, R. and Myers, S., Principles of Corporate Finance, McGraw Hill, 1991, p. 8.

Financial Management

44 Self-Instructional Material

NOTES

The true rate of return should lie between 15–16 per cent. We can find out a close approximation of the rateof return by the method of linear interpolation as follows:

Difference

PV required Rs 16,000

200PV at lower rate, 15% 16,200

257PV at higher rate, 16% 15,943

r = 15% + (16% – 15%)200/257

= 15% + 0.80% = 15.8%

2.8.2 Level Cash Flows

An easy procedure can be followed to calculate the IRR for a project that produces level or equalcash flows each period. To illustrate, let us assume that an investment would cost Rs 20,000 andprovide annual cash inflow of Rs 5,430 for 6 years. If the opportunity cost of capital is 10 per cent,what is the investment’s NPV? The Rs 5,430 is an annuity for 6 years. The NPV can be found asfollows:

3,648 Rs=4.3555,430 Rs+20,000 Rs =)5,430(PVFA Rs +20,000 Rs=NPV 6,0.10

How much is the project’s IRR? The IRR of the investment can be found out as follows:

683.35,430 Rs

20,000 RsPVFA

)5,430(PVFA Rs20,000 Rs0=)5,430(PVFA Rs+20,000 RsNPV

6,

6,

6,

r

r

r

The rate, which gives a PVFA of 3.683 for 6 years, is the project’s internal rate of return. Lookingup PVFA in Table (given at the end of the book) across the 6-year row, we find it approximatelyunder the 16 per cent column. Thus, 16 per cent is the project’s IRR that equates the present valueof the initial cash outlay (Rs 20,000) with the constant annual cash inflows (Rs 5,430 per year) for6 years.

2.8.3 NPV Profile and IRRWe repeat to emphasise that NPV of a project declines as the discount rate increases, and fordiscount rates higher than the project’s IRR, NPV will be negative. NPV profile of the project atvarious discount rates is shown in Table 2.2 and Figure 2.1. At 16 per cent, the NPV is zero; therefore,it is the IRR of the project. As you may notice, we have used the Excel spreadsheet to make thecomputations and create the chart using the Excel chart wizard.

Table 2.2: NPV Profile

1 NPV Profile

Discount2 Cash Flow rate NPV

3 – 20000 0% 12,580

4 5430 5% 7,561

5 5430 10% 3,649

6 5430 15% 550

7 5430 16% 0

8 5430 20% (1,942)

9 5430 25% (3,974)

Figure 2.1: NPV profile

Capital Budgeting Decisions

Self-Instructional Material 45

NOTES

2.8.4 Acceptance Rule

The accept-or-reject rule, using the IRR method, is to accept the project if its internal rate of returnis higher than the opportunity cost of capital (r > k). Note that k is also known as the required rateof return, or the cut-off, or hurdle rate. The project shall be rejected if its internal rate of return islower than the opportunity cost of capital (r < k). The decision maker may remain indifferent if theinternal rate of return is equal to the opportunity cost of capital. Thus the IRR acceptance rulesare:

Accept the project when r > k Reject the project when r < k May accept the project when r = k

The reasoning for the acceptance rule becomes clear if we plot NPVs and discount rates for theproject given in Table 2.2 on a graph like Figure 2.1. It can be seen that if the discount rate is lessthan 16 per cent IRR, then the project has positive NPV; if it is equal to IRR, the project has a zeroNPV; and if it is greater than IRR, the project has negative NPV. Thus, when we compare IRR of theproject with the opportunity cost of capital, we are in fact trying to ascertain whether the project’sNPV is positive or not. In case of independent projects, IRR and NPV rules will give the sameresults if the firm has no shortage of funds.

2.8.5 Evaluation of IRR MethodIRR method is like the NPV method. It is a popular investment criterion since it measures profitabilityas a percentage and can be easily compared with the opportunity cost of capital. IRR method hasfollowing merits:

Time value The IRR method recognises the time value of money.

Profitability measure It considers all cash flows occurring over the entire life of the projectto calculate its rate of return.

Acceptance rule It generally gives the same acceptance rule as the NPV method.

Shareholder value It is consistent with the shareholders’ wealth maximisation objective.Whenever a project’s IRR is greater than the opportunity cost of capital, the shareholders’wealth will be enhanced.

Like the NPV method, the IRR method is also theoretically a sound investment evaluation criterion.However, IRR rule can give misleading and inconsistent results under certain circumstances.Here we briefly mention the problems that IRR method may suffer from.

Excel Application 2.2:Calculation of IRR

We can easily calculate IRR using the Excel function forIRR. The spreadsheet below gives the cash flows of theproject. We write the IRR formula in column C7:=IRR(C3:C6). The project cash flows, including the cashoutlay in the beginning (C0 in year 0) are contained incolumn C3 through column C6. It is optional to include the“guess” rate in the formula.

Financial Management

46 Self-Instructional Material

NOTES

Multiple rates A project may have multiple rates, or it may not have a unique rate of return.As we explain later on, these problems arise because of the mathematics of IRR computation.

Mutually exclusive projects It may also fail to indicate a correct choice between mutuallyexclusive projects under certain situations. This pitfall of the IRR method is elaborated lateron in this unit.

Value additivity Unlike in the case of the NPV method, the value additivity principle doesnot hold when the IRR method is used—IRRs of projects do not add.23 Thus, for Projects Aand B, IRR(A) + IRR(B) need not be equal to IRR (A + B). Consider an example given below.

The NPV and IRR of Projects A and B are given below:

Project C0 C1 NPV @ 10% IRR

(Rs) (Rs) (Rs) (%)

A – 100 + 120 + 9.1 20.0B – 150 + 168 + 2.7 12.0

A + B – 250 + 288 + 11.8 15.2

It can be seen from the example that NPVs of projects add:

%2.1512%+20%)IRR()IRR(+)IRR(

while,8.117.21.9)(NPV)(NPV)(NPV

BABA

BABA

2.9 PROFITABILITY INDEX

Yet another time-adjusted method of evaluating the investment proposals is the benefit-cost(B/C) ratio or profitability index (PI). Profitability index is the ratio of the present value of cashinflows, at the required rate of return, to the initial cash outflow of the investment. The formula forcalculating benefit-cost ratio or profitability index is as follows:

010 )1(

)(PV

outlay cash Initial

inflows cash of PVPI C

k

C

C

C n

tt

tt

(10)

Illustration 2.6: PI of Uneven Cash FlowsThe initial cash outlay of a project is Rs 100,000 and it can generate cash inflow of Rs 40,000, Rs 30,000,Rs 50,000 and Rs 20,000 in year 1 through 4. Assume a 10 per cent rate of discount. The PV of cash inflowsat 10 per cent discount rate is:

.1235.1100,000 Rs

112,350RsPI

12,350 Rs=100,000 Rs112,350 RsNPV0.6820,000 Rs+0.75150,000 Rs+0.82630,000 Rs+0.90940,000 Rs=

)20,000(PVF Rs+)50,000(PVF Rs+)30,000(PVF Rs+)40,000(PVF RsPV 0.10 4,0.10 3,0.10 2,0.10 1,

2.9.1 Acceptance RuleThe following are the PI acceptance rules:

Accept the project when PI is greater than one PI > 1

Reject the project when PI is less than one PI < 1

May accept the project when PI is equal to one PI = 1

The project with positive NPV will have PI greater than one. PI less than means that the project’sNPV is negative.

2.9.2 Evaluation of PI MethodLike the NPV and IRR rules, PI is a conceptually sound method of appraising investment projects.It is a variation of the NPV method, and requires the same computations as the NPV method.

Check Your Progress

13. Define the basic methodof calculating the internalrate of return (IRR) whileappraising an investmentproject.

14. In the IRR system, howdo we decide whichprojects to accept orreject?

15. What is the maindifference in the conceptsof NPV and IRR?

23. Copeland, T.E. and Weston, J.F., Financial Theory and Corporate Policy, Addison-Wesley, 1983, p. 32.

Capital Budgeting Decisions

Self-Instructional Material 47

NOTES

Time value It recognises the time value of money.

Value maximisation It is consistent with the shareholder value maximisation principle. Aproject with PI greater than one will have positive NPV and if accepted, it will increase share-holders’ wealth.

Relative profitability In the PI method, since the present value of cash inflows is divided bythe initial cash outflow, it is a relative measure of a project’s profitability.

Like NPV method, PI criterion also requires calculation of cash flows and estimate of the discountrate. In practice, estimation of cash flows and discount rate pose problems.

2.10 PAYBACK

The payback (PB) is one of the most popular and widely recognised traditional methods ofevaluating investment proposals. Payback is the number of years required to recover the originalcash outlay invested in a project. If the project generates constant annual cash inflows, the paybackperiod can be computed by dividing cash outlay by the annual cash inflow. That is:

C

C0

Inflow Cash Annual

Investment Initial=Payback (11)

Illustration 2.7: Payback (Constant Cash Flows)

Assume that a project requires an outlay of Rs 50,000 and yields annual cash inflow of Rs 12,500for 7 years. The payback period for the project is:

years 412,000 Rs

50,000 RsPB

Unequal cash flows In case of unequal cash inflows, the payback period can be found out byadding up the cash inflows until the total is equal to the initial cash outlay. Consider the followingexample.

Illustration 2.8: Payback (Uneven Cash Flows)

Suppose that a project requires a cash outlay of Rs 20,000, and generates cash inflows of Rs 8,000; Rs7,000; Rs 4,000; and Rs 3,000 during the next 4 years. What is the project’s payback? When we add up thecash inflows, we find that in the first three years Rs 19,000 of the original outlay is recovered. In the fourthyear cash inflow generated is Rs 3,000 and only Rs 1,000 of the original outlay remains to be recovered.Assuming that the cash inflows occur evenly during the year, the time required to recover Rs 1,000 will be(Rs 1,000/Rs 3,000) 12 months = 4 months. Thus, the payback period is 3 years and 4 months.

2.10.1 Acceptance Rule

Many firms use the payback period as an investment evaluation criterion and a method of rankingprojects. They compare the project’s payback with a predetermined, standard payback. Theproject would be accepted if its payback period is less than the maximum or standard paybackperiod set by management. As a ranking method, it gives highest ranking to the project, whichhas the shortest payback period and lowest ranking to the project with highest payback period.Thus, if the firm has to choose between two mutually exclusive projects, the project with shorterpayback period will be selected.

2.10.2 Evaluation of Payback

Payback is a popular investment criterion in practice. It is considered to have certain virtues.