unit 2 - budgeting: making the most of your money

DESCRIPTION

Objective - Demonstrate the ability to allocate financial resources to meet family needs and goals. Unit 2 - Budgeting: Making the Most of Your Money. Financial literacy is the ability to make informed decisions regarding finances. - PowerPoint PPT PresentationTRANSCRIPT

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

Unit 2 - Budgeting: MakingUnit 2 - Budgeting: Makingthe Most of Your Moneythe Most of Your Money

Objective - Demonstrate the ability to Objective - Demonstrate the ability to

allocate financial resources to allocate financial resources to

meet family needs and goalsmeet family needs and goals

Did You Know?

• Financial literacy is the ability to make informed decisions regarding finances.

• Effective use of resources (time, money, etc) improves success toward a goal.

• Family members share certain resources in order to meet collective needs.

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

2-A-12-A-1

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

??

For an interactive version For an interactive version of this slide, open the of this slide, open the Excel File for this unit Excel File for this unit and go to Excel and go to Excel Worksheet 2-A-1 Worksheet 2-A-1

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

2-A-22-A-2

For an interactive version For an interactive version of this slide, open the of this slide, open the Excel File for this unit Excel File for this unit and go to Excel and go to Excel Worksheet 2-A-2 Worksheet 2-A-2

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

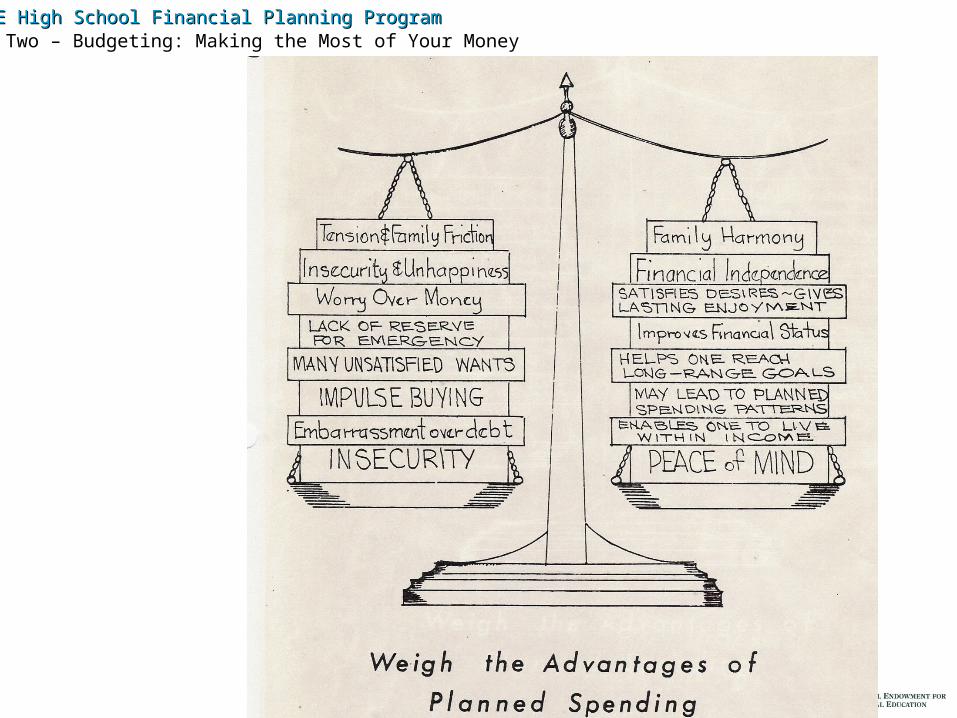

Reasons for a Spending Plan Reasons for a Spending Plan ……Helps you determine where you are Helps you determine where you are

spending your money currently.spending your money currently.

……Helps you decide where to spend your Helps you decide where to spend your money in the future. money in the future.

……You have an organized way to save for You have an organized way to save for things that cost more. things that cost more.

……Puts you in control of your financial Puts you in control of your financial future, beginning NOW.future, beginning NOW.

2-B-1 321

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

People Without a Budget… People Without a Budget…

……Are less likely to know what they have.Are less likely to know what they have.……Have no plan, often coming up short Have no plan, often coming up short

before their next paycheck or allowance.before their next paycheck or allowance.……Are almost certain to have no plan to Are almost certain to have no plan to

save for more expensive spending goals.save for more expensive spending goals.

2-B-2 321

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

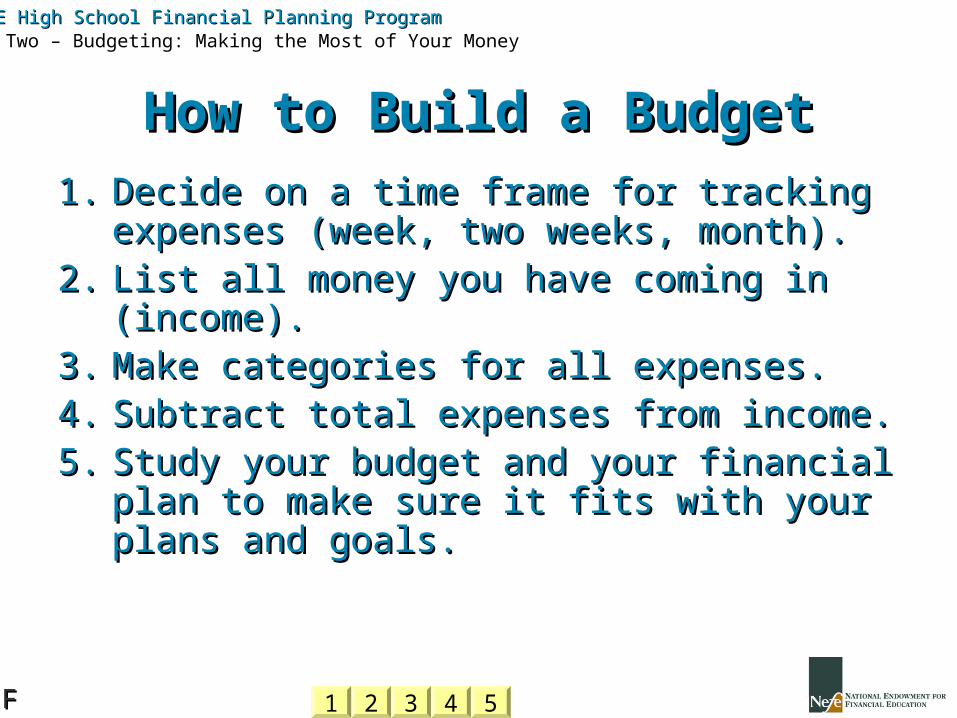

How to Build a BudgetHow to Build a Budget

1.1. Decide on a time frame for tracking Decide on a time frame for tracking expenses (week, two weeks, month).expenses (week, two weeks, month).

2.2. List all money you have coming in List all money you have coming in (income).(income).

3.3. Make categories for all expenses.Make categories for all expenses.4.4. Subtract total expenses from income.Subtract total expenses from income.5.5. Study your budget and your financial Study your budget and your financial

plan to make sure it fits with your plans plan to make sure it fits with your plans and goals.and goals.

2-F2-F 54321

The Costs Add Up

Item Average Yearly Expense

Daily Latte at $2.50

Eating lunch out 5 days per week at a cost of $5.00=$10.00 each time

Daily can of soda or chips at $1.00 each

Daily candy bar at $1.00

Daily can of chew or pack of cigarettes at $3.79

Weekly attendance at a sporting event with $3.50 admission and $5.00 for snacks

Monthly haircut at $25.00 per month

Monthly movie and popcorn for two at $20.00

Monthly gym membership at $38.00

Do not let money fly away! By creating a spending plan, a person can realize everyday expenses, reduce these expenses, and increase current income. Beginning at age 15, if a person saved $547.50 per year by not having a can of soda everyday, they would have $105,504 extra to retire on at age 50 with a 8.5% interest rate compounded yearly.

$912.50

$1,300.00-$2,600.00

$365.00

$365.00

$1,383.35

$442.00

$300.00

$240.00

$456.00

Income & Expense

• Spending Plans have two main components– Income

• Money Earned

– Expense• Money Spent

– Fixed Expenses– Flexible Expenses

Income

• Income is money earned from:– Tips– Wages or salaries– Withdrawal of money from savings– Interest from savings accounts, or

investments– Monetary gifts– Scholarships

Expense

• Money Spent• Fixed Expenses

– Same amount paid each time, usually has a specific due date

• Rent/Mortgage

– Difficult to change in short amount of time

• Flexible Expenses– Different amount paid each time, usually

no specific due date• Clothing

– Easier to change in short amount of time

Spending Plan Activity

• Decide if each item is income, a fixed expense, or a flexible expense

• Indicate a response by holding up the corresponding game card

Spending Plan Activity

Rent

Fixed Expense

Wages

Income

Spending Plan Activity

Groceries

Flexible Expense

Internet Bill

Fixed Expense

Spending Plan Activity

Tips

Income

Utilities

Fixed Expense

Spending Plan Activity

Gift from Family

Income

Savings

Fixed Expense

Spending Plan Activity

Automobile Registration

Fixed Expense

Eating Out/Snacks

Flexible Expense

Spending Plan Activity

Scholarships

Income

Hobbies

Flexible expense

Net Loss & Gain

When finished with the spending plan two outcomes are possible:

• Net Loss– More expenses than income

– An individual needs to increase income or decrease spending

• Net Gain– More income than expenses

– Ideal situation

– Extra money can go into savings, be invested, or spent

Organize• Select categories for the spending plan

• Select a time period– Usually when paychecks are received

• Weekly• Bi-weekly• Monthly

• Keep records of spending and earnings!

Step 5:Control

• Control systems are ways that a person can keep accurate records of spending

• Realize potential problems early if spending too much in one area

• Control systems occur simultaneously with implementation

• A person should keep a credit spreadsheet which logs all credit transactions (charges and payments for each creditor)

Types of Control Systems

• Envelope System– Individuals place actual budgeted cash in a

labeled envelope for a certain expense– Each time $ is taken out of an envelope, write

down amount and place receipt inside– Move money around to meet expenses– Once cash is gone, its gone and there is no

more money in that category

Types of Control Systems

• Spending Plan System– Track expenses on a sheet by entering

amount– Keep daily to know how much is being spent

• Check Register System– Tracks all expenditures in a checkbook

register– Divided into spending plan categories

Organize• Determine the appropriate way of record keeping

– Spreadsheet– Envelopes– Software like Money

• Select categories for the spending plan

• Select a time period– Usually when paychecks are received

• Weekly

• Bi-weekly

• Monthly

• Keep records of spending and earnings!

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

2-E2-E

For an interactive For an interactive version of this slide, version of this slide, open the Excel file for open the Excel file for this unit and go the this unit and go the Excel worksheet #2-EExcel worksheet #2-E

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

Personal Personal Plan for Plan for One WeekOne Week

$20.00Balance

$120.00Savings and Spending

$140.00Income

$120.00Total Savings & Spending

15.00Miscellaneous

33.00Transportation

16.50Gifts and Contributions

10.00Entertainment

14.50Clothing

11.00Food

$20.00Savings (PYF)

Savings and Spending

$140.00Total Income

15.00Allowance

$125.00Part-Time Job

Income (after taxes)

One Week

Personal Spending/Savings Plan

$20.00Balance

$120.00Savings and Spending

$140.00Income

$120.00Total Savings & Spending

15.00Miscellaneous

33.00Transportation

16.50Gifts and Contributions

10.00Entertainment

14.50Clothing

11.00Food

$20.00Savings (PYF)

Savings and Spending

$140.00Total Income

15.00Allowance

$125.00Part-Time Job

Income (after taxes)

One Week

Personal Spending/Savings Plan

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

QuestionsQuestionsDoes it makes sense to create and live Does it makes sense to create and live

within a budget when you don’t have a within a budget when you don’t have a lot of money?lot of money?

What if you find that you are What if you find that you are consistently spending more in one area consistently spending more in one area than you had planned to?than you had planned to?

What if you find that you can’t live What if you find that you can’t live within your budget?within your budget?

2-B-3 321

What is so bad about Debt?

• “Excessive debt eats at the heart of family life. • Without savings, families can’t cope with the

emergencies and unexpected expenses that inevitably occur.

• More than 50% of marriages in the U.S. end in divorce, and the #1 reason for divorces is $ problems.”

What is so bad about Debt?

• “A family that constantly worries about money is a family that has less time to enjoy life and each other.

• Declaring bankruptcy is emotionally painful and throws a family into turmoil and pain.”

What Do We Do About It?

• Examine Your Debts– The goal is to pay them off without having to

go into debt even more.• Pay the most on the balances that are charging the

most

Targets - Suggested Spending Ratios

• 35% for Housing ( mortgage house payment or rent, taxes on the property, home repairs, insurance and utilities (gas for the home, electric, water bill, etc)

• 20% for transportation (car payment, gas for car, car repairs, auto insurance, etc)

Suggested Spending Ratios (cont)

• 15% MAX for other Debt (credit cards and loans) This money would be more valuable used in another way!!

• 20% for other expenses such as Food, Clothes, Life and Health Insurances

• 10% Savings

NEFE High School Financial Planning ProgramNEFE High School Financial Planning ProgramUnit Two – Budgeting: Making the Most of Your Money

SSAAVVEE

etting aside money for “big ticket items”etting aside money for “big ticket items”

voids borrowing, which costs you a lot! It’s avoids borrowing, which costs you a lot! It’s a

ery wise thing to do, becauseery wise thing to do, because

very time you pay yourself first, you are very time you pay yourself first, you are developing adeveloping a saving habitsaving habit that leaves you that leaves you with more money to spend later on for things with more money to spend later on for things that are really important to you!that are really important to you!

PAY YOUR$ELF FIRST!PAY YOUR$ELF FIRST!

2-D-12-D-1.. (2-D-2 and 2-D-3 on Excel file Unit 2 (2-D-2 and 2-D-3 on Excel file Unit 2 Visuals.xls)Visuals.xls)

Cash In on the Benefits of Financial Management:

• Less Stress

• More Fun in your life

• Able to have anything you want – in time

• Waste less money