unit 1 com541-a

TRANSCRIPT

Management of Financial Services (MFS - COM 541A)

HARESH RAsst. Professor

Department of CommerceChrist University, Bengaluru

Unit – 1 Introduction to Financial Services

The economic activities are mainly divided into three classes.

They are – Primary, Secondary, and Tertiary. Primary – agriculture, fishing and forestry. Secondary – industry ( manufacturing and construction ).

Tertiary activities includes services.

SERVICE SECTORSERVICES A type of economic activity which is intangible. Services

are one of the key components of economics, the other being goods.

A service is any activity or benefit that one party can offer to another that is essentially intangible and does not result in the ownership of anything. Its production may or may not be tied to physical product. (Eg. Banking, Insurance, Legal, Medical, Education, Telecommunication, ITES…..)

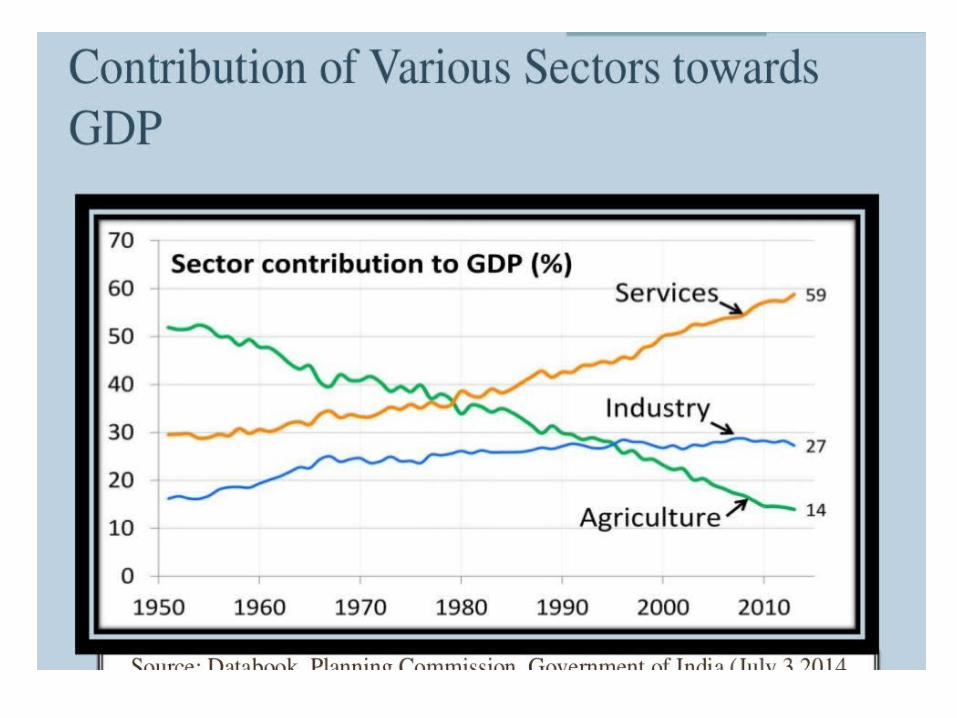

72.4 per cent of the growth in India's GDP in 2014-15 from 15 per cent in 1950. ( Source – UNION BUDGET 2014-15)

(GDP contribution shift from agriculture to services)

Components Of Service SectorService sector can be broadly divided into two parts:

Economic Services - Transport, Storage and Communication - Trade, Hotels and Tourisms - Banking and Insurance ServicesSocial Service - Education - Health - Administration ( UPSC, BDO)

Financial Services• Financial services refer to services provided by

the finance industry. • The finance industry - include banks, credit card

companies, insurance companies, consumer finance companies, stock brokers, investment funds and some government sponsored enterprises.

• Financial services - the products and services offered by financial institutions for the facilitation of various financial transactions and other related activities.

Financial Services - CONTD

• Financial services can also be called financial intermediation. Financial intermediation is a process by which funds are mobilised from a large number of savers and make them available to all those who are in need of it and particularly to corporate customers.

• Various institutions which render financial services are banks, investment companies, accounting firms, financial institutions, merchant banks, leasing companies, venture capital companies, factoring companies, mutual funds etc.

• https://www.imf.org/external/pubs/ft/fandd/2011/03/pdf/basics.pdf

Features/Nature/Characteristics of Financial Services

• Intangibility• Inseparability• Perishability• Variability/Dynamism/Heterogeneity• Protect customer’s interest• Geographical dispersion (massive branch network)• Dominance of human element/People intensive• Information based

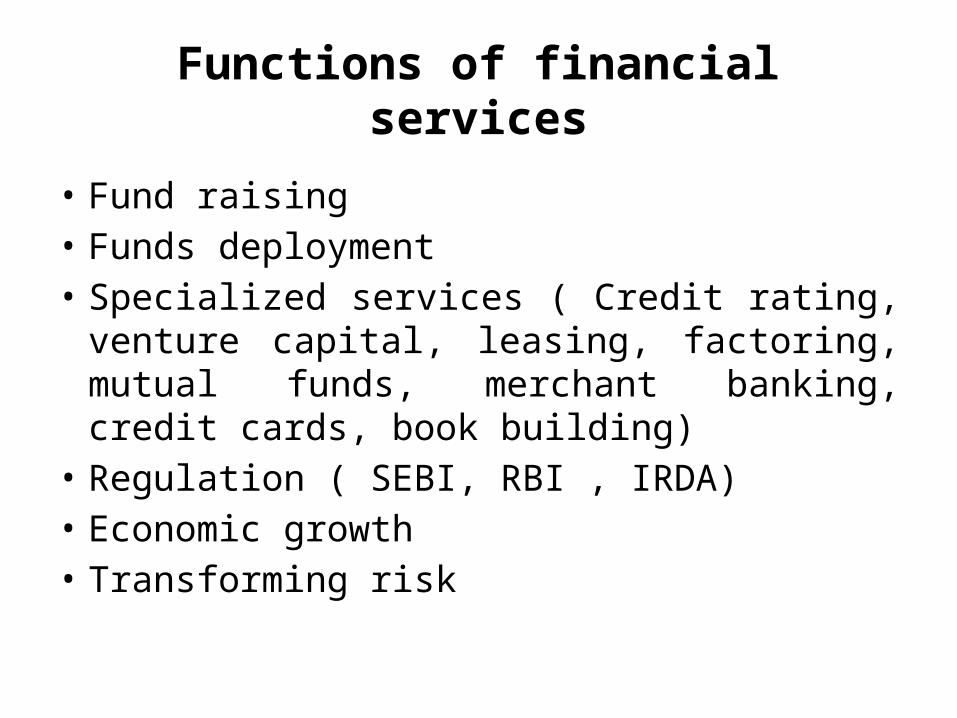

Functions of financial services

• Fund raising• Funds deployment • Specialized services ( Credit rating, venture

capital, leasing, factoring, mutual funds, merchant banking, credit cards, book building)

• Regulation ( SEBI, RBI , IRDA)• Economic growth• Transforming risk

Importance of Financial Services

• Economic growth(savings Investment)• Promotion of savings(transformation services)• Capital formation(Capital market intermediary

services)• Creation of employment opportunities(labour

intensive)• Provision of liquidity(easy conversion of financial

assets into liquid cash)• Contribution to GNP• Financial intermediation

Classification of Financial Services

• Financial service institutions render a wide variety of services to meet the requirements of individual users.– Provision of funds– Managing investible funds– Risk financing– Consultancy services– Market operations– Research and development

1. Provision of funds(a) Venture capital(b) Banking services(c) Asset financing(d) Trade financing(e) Credit cards(f) Factoring and forfaiting

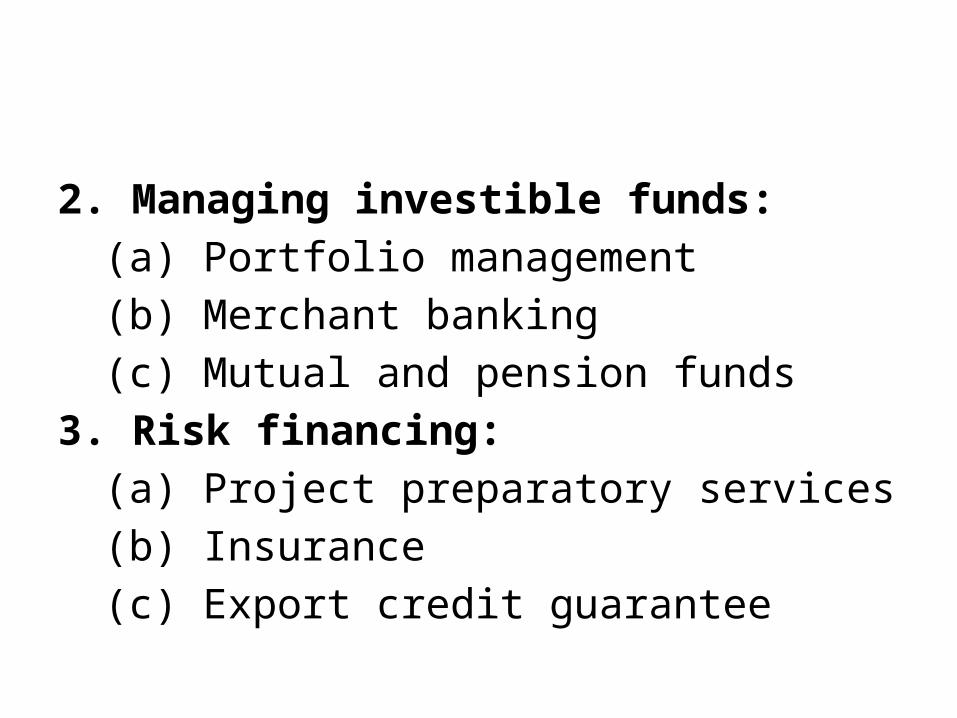

2. Managing investible funds:(a) Portfolio management(b) Merchant banking(c) Mutual and pension funds

3. Risk financing:(a) Project preparatory services(b) Insurance(c) Export credit guarantee

4. Consultancy services:(a) Project preparatory services(b) Project report preparation(c) Project appraisal(d) Rehabilitation of projects(e) Business advisory services(f) Valuation of investments(g) Credit rating(h) Merger, acquisition and reengineering

5. Market operations:(a) Stock market operations(b) Money market operations(c) Asset management(d) Registrar and share transfer agencies(e) Trusteeship

6. Research and Development:(a) Equity and market research(b) Investor education(c) Training of personnel(d) Financial information services

Scope of Financial Service Industry

The scope of financial services is very wide. This is because it covers a wide range of services. The financial services can be broadly classified into two: (a) Fund based services and (b)non-fund services (or fee-based services)

Fund Based Services

1. Underwriting2. Dealing in secondary market activities3. Participating in money market instruments like CPs, CDs etc.4. Equipment leasing or lease financing5. Hire purchase

6. Venture capital7. Bill discounting.8. Insurance services9. Factoring10. Forfaiting11. Housing finance12. Mutual fund

Non-fund Based Services (Fee based)

1. Securitisation2. Merchant banking3. Credit rating4. Loan syndication5. Business opportunity related services6. Project advisory services7. Services to foreign

companies and NRIs.8. Portfolio management9. Merger and acquisition10. Capital restructuring11. Debenture trusteeship12. Custodian services13. Stock broking

Financial Innovation

• Financial innovation can be defined as the act of creating and then popularising new financial instruments as well as new financial technologies, institutions and markets. It includes institutional, product and process innovation.

Financial Engineering

• The design, the development and the implementation of innovative financial instruments and processes and the formulation of creative solutions to problems in finance.

Causes for Financial Innovation

• Low profitability• Keen competition• Economic liberalisation• Improved communication technology• Customer service• Global impact• Investor awareness

Innovative Financial Instruments• Commercial Paper• Treasury Bill• Certificate of deposit• Inter-Bank Participations(IBPs)• Zero Interest convertible debenture/bonds• Deep Discount Bonds• Index-Linked gilt bonds• Option Bonds• Secured premium notes• Medium term debentures• Variable rate debentures

Innovative Financial Instruments• Non-convertible debentures with equity warrants• Convertible bonds• Carrot & stick bonds• European Currency Unit Bonds• Yankee Bonds(USA)• Samurai Bonds(Japan)• Floating Rate Notes (FRNs)• Loyalty Coupons• Global Depository Receipt(GDR)

Zero Interest Convertible Debenture/Bonds

• A zero-coupon convertible note can be converted into shares.

• A fixed income instrument that is a combination of a zero-coupon bond and a convertible bond.

• The bond pays no interest and is issued at a discount to par value, while the convertible feature means that the bond is convertible into equity shares after a period of time.

Deep Discount Bonds• Deep-discount bonds (also called as Zero coupon

or discount bonds) refer to bonds which do not pay any interest (or coupons) during the life of the bonds.

• The bonds are issued at a discount to the face value and the face value is repaid at the maturity.

• The return to the bondholder is the discount at which the bond is issued, which is the difference between the issue price and the face value.

Yankee Bonds• Yankee bonds are simply bonds issued by foreign

companies in the U.S. • According to the Securities Act of 1933, these bonds

must first be registered with the Securities and Exchange Commission (SEC) before they can be sold.

• Yankee bonds are issued by foreign firms who register with the SEC and borrow U.S. dollars, using issues underwritten by a U.S. syndicate for delivery in the United States.

• Over 60 percent of Yankee bonds are issued by Canadian corporations and typically have shorter maturities and longer call protection than U.S. domestic issues. These features increase their appeal.

Samurai Bonds• Samurai bonds are yen-denominated bonds

sold by non-Japanese issuers and mainly sold in Japan.

• Samurai bonds give issuers the ability to access investment capital available in Japan.

• Samurai bonds can also be used to hedge foreign exchange rate risk.

• The market is fairly small and has limited liquidity.

Debentures with “Call” & “Put” Feature

• Call Feature– In case the company issues debentures with call

features, the issuing company itself enjoys the right of exercising the option to redeem the debentures well before the specified due date of redemption, at a certain price, specified at the time of issue.

• Put Feature– The investors are given the right to exercise their option

to ask for redemption of the amount after expiry of certain specified period at pre-determined prices.

Secured Premium Notes (SPN) • Secured premium notes are nothing but a share

warrant which are only issued by the listed companies after getting the approval from the central government.

• SPN is a secured debenture redeemable at premium issued along with a detachable warrant, redeemable after a notice period, say four to seven years.

• The warrants attached to SPN gives the holder the right to apply and get allotted equity shares; provided the SPN is fully paid.

• There is a lock-in period for SPN during which no interest will be paid for an invested amount.

Secured Premium Notes (SPN) • The SPN holder has an option to sell back the SPN

to the company at par value after the lock in period. If the holder exercises this option, no interest/ premium will be paid on redemption.

• In case the SPN holder holds it further, the holder will be repaid the principal amount along with the additional amount of interest/ premium.

• The conversion of detachable warrants into equity shares will have to be done within the time limit notified by the company.

Carrot & Stick Bonds• A convertible bond that comes with a carrot-and-stick

provision. Differently stated, its carrot provision provides for a low conversion premium to allure holders to exercise conversion earlier than usual (the carrot).

• The stick provision allows the issuer to call the bond at a specified premium if the common stock of the issuer is trading at a certain percentage above the conversion price (the stick).

• This structure combines both rewards and punishments and it is up to the holder to go either course as its investment policy dictates.

Floating Rate Bonds• Bonds that make coupon payments that vary

through time. The coupon payments are usually tied to a benchmark market interest rate. Also called variable-rate bonds

• The rate on the floating Rate Bond is linked to a benchmark interest rate like the prime rate in USA or LIBOR in eurocurrency market.

• When rates are fixed, they are likely to be inequitable to the borrower when interest rates fall subsequently, and the same bonds are likely to be inequitable to the lender when interest rates rise subsequently.

Dual Currency Bond• A debt instrument that has coupons denominated

in a different currency than its principal amount.• They have been popular funding instruments,

particularly in the Euromarkets, and have been designed to include virtually all world’s major currencies.

• These bonds can be viewed as a combination of two simpler financial instruments:– Single currency coupon bond, and– A forward contract to exchange the bonds principal

into a predetermined amount of a foreign currency.

Challenges in the Financial Service Sector

Lack of qualified personnel in the financial service sector. Lack of investor awareness about the various financial

services. Lack of transparency in the disclosure requirements and

accounting practices relating to financial services. Lack of specialization in different financial services

(specialization only in one or two services). Lack of adequate data to take financial service related

decisions. Lack of efficient risk management system in the financial

service sector.

Present Scenario of Financial Service Sector in India

• Conservatism to dynamism– Process of rapid transformation– Reforms in the financial sector (to promote an efficient,

competitive and diversified financial system in the country.)

– Phenomenal changes in the Money market, securities market, capital market, debt market and the foreign exchange market.

– The emergence of various financial institutions and regulatory bodies have transformed the financial services sector from being a conservative industry to a very dynamic one.

• Emergence of primary equity markets– The number of stock exchanges in the country has

gone up from 9 in 1980 to 22 at 2010.– The aggregate funds raised by the industries have

increased many folds.– Emerged as an important vehicle to channelize the

savings of the individuals and corporates for productive purposes and to promote the industrial and economic growth.

• Concept of Credit Rating– Investment decisions have been based on factors

like name recognition of the company, operations, market sentiment, reputation of the promoters, etc.

– Grading from an independent agency plays a significant role in investment decision making.

– Mandatory for NBFC’s to get credit rating for their debt instruments. (CRISIL, CARE, ICRA, DCR)

• Process of Liberalisation– Interest rate deregulation– Private sector participation in banking & mutual

funds– SEBI has liberalised many stringent conditions.

• Process of Globalisation– Entry of new financial products– Inflow of foreign capital.

FINANCIAL SECTOR IN INDIA : REGULATIONS AND REFORMS

• FSI is the main pillar of any economy.• India’s financial sector is diversified and

expanding rapidly. • It comprises commercial banks, insurance

companies, non-banking financial companies, cooperatives, pensions funds, mutual funds and other smaller financial entities.

• IFMs are highly regulated• Stock markets SEBI (Securities & Exchange

Board of India)• Insurance industry IRDA (Insurance

Regulatory & Development Authority)• Indian Banking Sector RBI• Mutual Funds in India AMFI(Association of

Mutual Funds in India)• New Pension Scheme PFRDA (Pension Fund

Regulatory & Development Authority)