understanding annuities once and for all

TRANSCRIPT

1

UNDERSTANDING

ANNUITIESYour guide to understanding

the fundamentals of annuities, including their pros and cons, in an easy to understand manner

2

WE ARE ALL FAMILIAR WITH ANNUITY TYPE PAYMENTS

SOCIAL SECURITY

COMPANY PENSIONS

STRUCTURED SETTLEMENTS

LOTTERY WINNER OPTION

ANNUITY TYPE PAYMENTS

A fixed sum of money or income payment paid to someone each year, typically for the rest of their life.

THESE ALL PROVIDE FIXED SUMS OF MONTHLY PAYMENTS AND MAY BE CONSIDERED FORMS OF

ANNUITY PAYMENTS.

3

An annuity can also be a product offered by a life insurance company. Every product has its pros and cons and its proper place, use and function within an individual’s portfolio depending on personal circumstances and core financial priorities. The diagram below provides a general idea of the relative risk and return placements for different products.

PRINCIPAL GUARANTEED OR INSURED* NON-PRINCIPAL GUARANTEED OR INSURED

Checking,Savings,

Money Market

CDs, Treasuries,Fixed Interest

Annuities

Fixed IndexedAnnuities

Cash ValueIndexed/WholeLife Insurance

Cash ValueVariable

Life Insurance

Variable Annuities

Stocks, Bonds,Mutual Funds

REITS,Commodities,

Options+

Lower Risk = Lower Return Potential Higher Risk = Higher Return Potential

WHERE ANNUITY PRODUCTS FIT IN

* Individual guarantees or insurance vary for each product+ While Money Market Funds are not principal guaranteed, we have included them here because of their relatively high level of safety

4

The written agreement between an insurance company and a customer outlining each party’s obligations in an annuity coverage agreement. This document will include the specific details of the contract, such as the structure of the annuity (variable, indexed, or fixed), any penalties for early withdrawal, spousal provisions such as a survivor clause and rate of spousal coverage, and more. Note: Breaking an annuity contract may result in certain penalties or surrender charges.

WHAT IS AN ANNUITY CONTRACT?

“Annuity Contract Definition | Investopedia.” Investopedia. Investopedia, 2014. Web. 02 May 2014

INSURANCE COMPANY

PREMIUM + CREDITED INTEREST

YOU ANNUITY CONTRACT

LIFETIME INCOME OR LUMP SUM

5

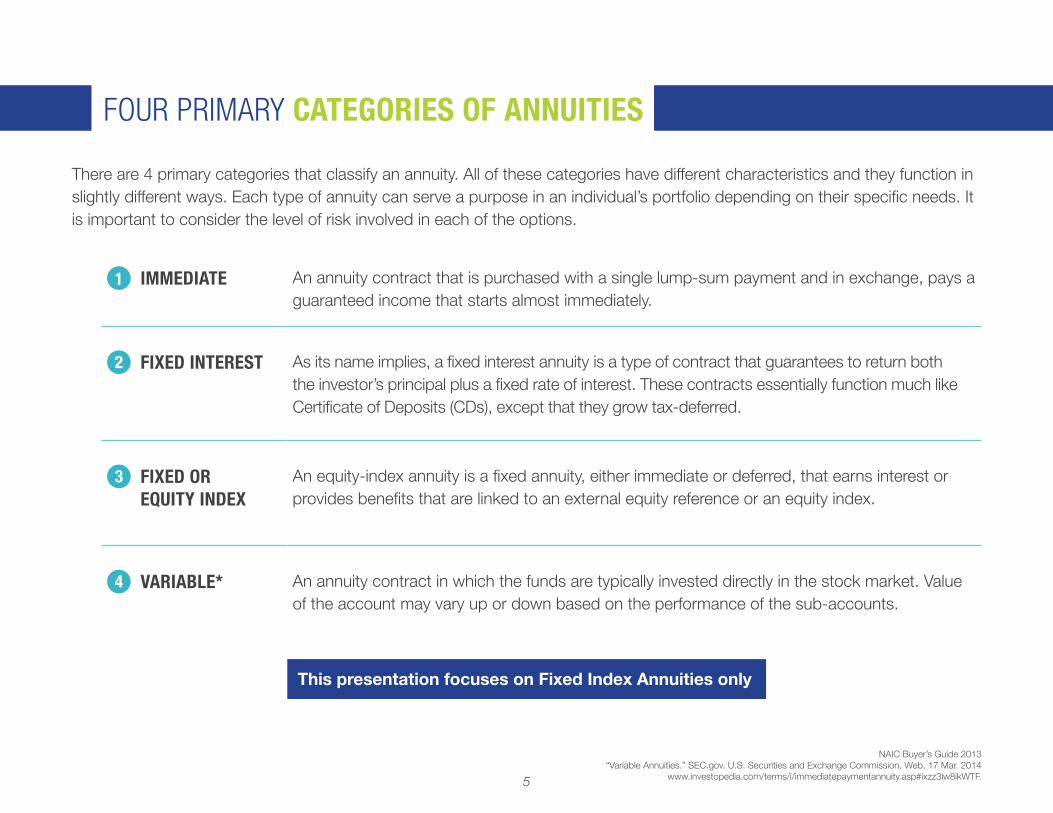

There are 4 primary categories that classify an annuity. All of these categories have different characteristics and they function in slightly different ways. Each type of annuity can serve a purpose in an individual’s portfolio depending on their specific needs. It is important to consider the level of risk involved in each of the options.

1 IMMEDIATE An annuity contract that is purchased with a single lump-sum payment and in exchange, pays a guaranteed income that starts almost immediately.

2 FIXED INTEREST As its name implies, a fixed interest annuity is a type of contract that guarantees to return both the investor’s principal plus a fixed rate of interest. These contracts essentially function much like Certificate of Deposits (CDs), except that they grow tax-deferred.

3 FIXED OR EQUITY INDEX

An equity-index annuity is a fixed annuity, either immediate or deferred, that earns interest or provides benefits that are linked to an external equity reference or an equity index.

4 VARIABLE* An annuity contract in which the funds are typically invested directly in the stock market. Value of the account may vary up or down based on the performance of the sub-accounts.

FOUR PRIMARY CATEGORIES OF ANNUITIES

NAIC Buyer’s Guide 2013“Variable Annuities.” SEC.gov. U.S. Securities and Exchange Commission, Web. 17 Mar. 2014

www.investopedia.com/terms/i/immediatepaymentannuity.asp#ixzz3lw8ikWTF.

This presentation focuses on Fixed Index Annuities only

•

• http://www.investopedia.com/terms/i/immediatepaymentannuity.asp#ixzz3lw8ikWTF

6

FIXED INDEX ANNUITIES:THE ACCUMULATION PHASE

7

ANNUITY IS CONNECTED TO THE MARKET INDEX VIA A CREDITING STRATEGY

Funds deposited in a Fixed Index Annuity are NOT invested directly in the market. Instead, they are linked to a market index (e.g. S&P 500) by a mathematical formula called a Crediting Strategy. This formula determines the interest that will be credited to the annuity based on the performance of the chosen index during a specific time frame during the Accumulation Phase and, in some cases, during the Payout Period as well.

FIXED INDEX ANNUITY

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

FIXED INDEX ANNUITY

STOCK MARKET INDEX (E.G. S&P 500)

8

UNDERSTANDING CREDITING STRATEGIES

To determine how the insurance

company calculates returns it’s

important to understand how the

index is tracked, as well as how

much of the return of the index is

credited to the annuity. Crediting

strategies come in many forms.

Many annuities offer multiple

strategies and typically you can

change or combine strategies

each year on your annuity

anniversary date. Here are

the most common types of

credibility strategies.

Remember, for all Index Annuities,

when the linked market index or

crediting method is negative, your

annuity does not go down in value.

CAP-BASED STRATEGIES

An upper limit put on the return over a certain time period. For example, if the index returned 10% but the annuity had a cap of 5%, you only receive a maximum 5% rate of return. Many index annuities put a cap on the return. There are different kinds of cap strategies—Annual, Average, Monthly, 2 year and 5 year are some examples.

UNCAPPED STRATEGY WITH PARTICIPATION RATE

The percentage of the index’s return that the insurance company credits to the annuity, typically ranging from 80% to 100%. For example, if the market went up 10% and the annuity’s participation rate was 80%, an 8% return (80% of the gain) would be credited.

UNCAPPED STRATEGY WITH SPREAD/ MARGIN/ ASSET FEE

A percentage fee that may be subtracted from the gain in the index linked to the annuity. For example, if an index gained 18% and the spread fee is 3.5%, then the gain credited to the annuity would be 14.5%.

UNCAPPED STRATEGY WITH SPREAD/MARGIN/ASSET FEE PLUS INTEREST BONUS

Works the same way as the illustration above with an added interest bonus. In the above example the annuity was credited with 14.5% interest, and with this strategy an interest bonus would be added. For instance, 50% which would bring the total interest credited to the annuity to 21.75% for the period.

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

9

For illustration purposes only, here is a step by step visual of how Fixed Index Annuities work during the Accumulation Phase. In the second part of this presentation, we’ll take a look at how FIAs work in the Distribution Period. To begin, funds are deposited in the FIA. With most FIAs, the amount deposited is guaranteed never to go down in value except for any withdrawals or fees that may be incurred. Remember, all guarantees are backed by the claims paying ability of the insurance carrier.

YEARS

1 2 3 4 5 6 7 8

Your deposit is guaranteed never to go down due to the negative performance of the associated index

DEPOSIT$100,000

INDEX

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

FIXED INDEX ANNUITY ILLUSTRATION

10

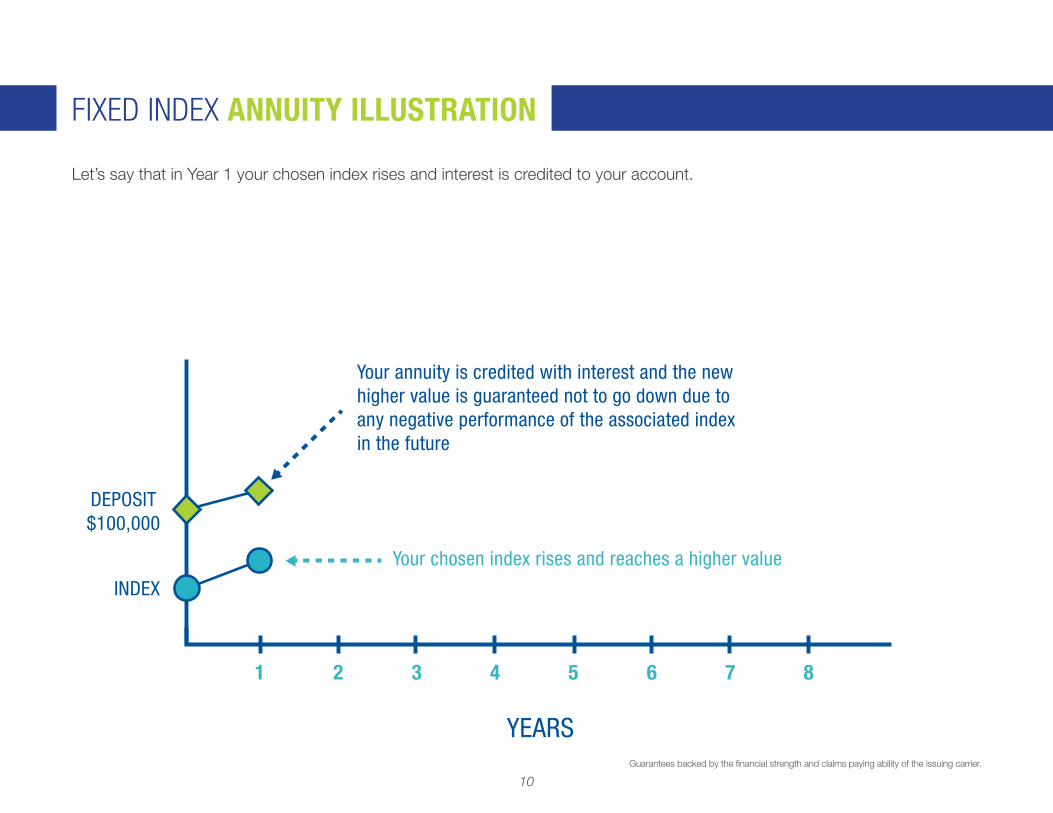

Let’s say that in Year 1 your chosen index rises and interest is credited to your account.

YEARS

DEPOSIT$100,000

INDEX

1 2 3 4 5 6 7 8

Your annuity is credited with interest and the new higher value is guaranteed not to go down due to any negative performance of the associated index in the future

Your chosen index rises and reaches a higher value

FIXED INDEX ANNUITY ILLUSTRATION

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

11

Let’s say that in Year 2 your chosen index rises again and interest is credited to your account.

YEARS

DEPOSIT$100,000

1 2 3 4 5 6 7 8

Your annuity is credited with interest and the new higher value is guaranteed not to go down due to any negative performance of the associated index in the future

Your chosen index rises and reaches a higher value

INDEX

FIXED INDEX ANNUITY ILLUSTRATION

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

12

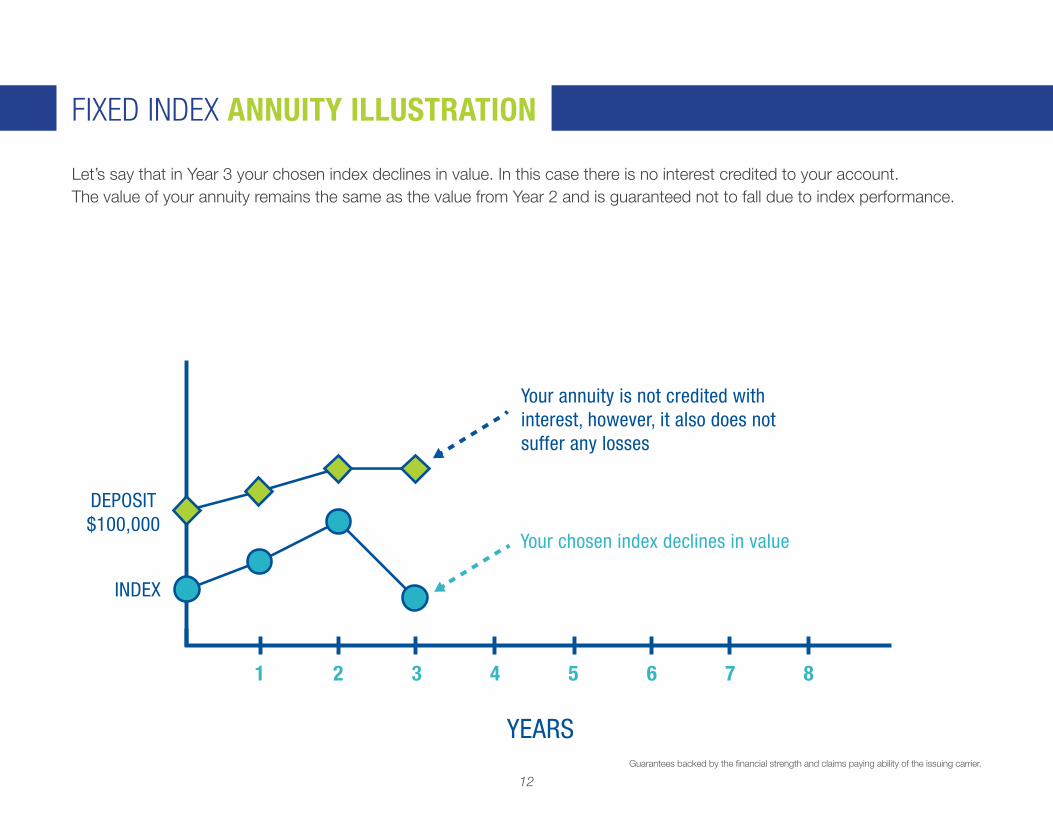

Let’s say that in Year 3 your chosen index declines in value. In this case there is no interest credited to your account. The value of your annuity remains the same as the value from Year 2 and is guaranteed not to fall due to index performance.

YEARS

DEPOSIT$100,000

1 2 3 4 5 6 7 8

Your annuity is not credited with interest, however, it also does not suffer any losses

Your chosen index declines in value

INDEX

FIXED INDEX ANNUITY ILLUSTRATION

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

13

Let’s say that in Year 4 your chosen index declines in value again. In this case there is no interest credited to your account. The value of your annuity remains the same as the value from Year 3 and is guaranteed not to fall due to index performance.

YEARS

DEPOSIT$100,000

1 2 3 4 5 6 7 8

Your annuity is not credited with interest and does not suffer any losses

Your chosen index declines in value

INDEX

FIXED INDEX ANNUITY ILLUSTRATION

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

14

Let’s say that in Year 5 your chosen index rises in value. Interest is credited to your account. The new value is once again guaranteed not to decline in value due to the performance of the chosen index.

YEARS

DEPOSIT$100,000

1 2 3 4 5 6 7 8

Your annuity is credited with interest and the new higher value is, again, guaranteed

Your chosen index rises

INDEX

FIXED INDEX ANNUITY ILLUSTRATION

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

15

Let’s say that in Year 6 your chosen index rises in value again. Interest is credited to your account. The new value is once again guaranteed not to decline in value due to the performance of the chosen index.

YEARS

DEPOSIT$100,000

1 2 3 4 5 6 7 8

Your annuity is credited with interest and the new higher value is, again, guaranteed

Your chosen index rises

INDEX

FIXED INDEX ANNUITY ILLUSTRATION

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

16

Let’s say that in Year 7 your chosen index declines in value again. In this case there is no interest credited to your account. The value of your annuity remains the same as the value from Year 6 and is guaranteed not to fall due to index performance.

YEARS

DEPOSIT$100,000

1 2 3 4 5 6 7 8

Your annuity is not credited with interest, however, it also does not suffer any losses

Your chosen index declines in value

INDEX

FIXED INDEX ANNUITY ILLUSTRATION

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

17

YEARS

DEPOSIT$100,000

INDEX

1 2 3 4 5 6 7 8

Your annuity is credited with interest and the new higher value is, again, guaranteed.

Your chosen index rises

Let’s say that in Year 8 your chosen index rises in value once again. Interest is credited to your account. The new value is once again guaranteed not to decline in value due to the performance of the chosen index.

FIXED INDEX ANNUITY ILLUSTRATION

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

18

YEARS

DEPOSIT$100,000

INDEX

1 2 3 4 5 6 7 8

Guaranteed Minimum Interest Rate

While your FIA’s earned interest is the result of the Crediting Strategy and the chosen index’s performance, there is a Guaranteed Minimum Interest Rate that the FIA will earn over the life of the annuity. Many people misunderstand this and think that the Guaranteed Minimum interest rate is earned in years when the Crediting Strategy credits no interest. This is not true. The Guaranteed Interest Rate is for the term of the contract, not year by year.

FIXED INDEX ANNUITY ILLUSTRATION

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

19

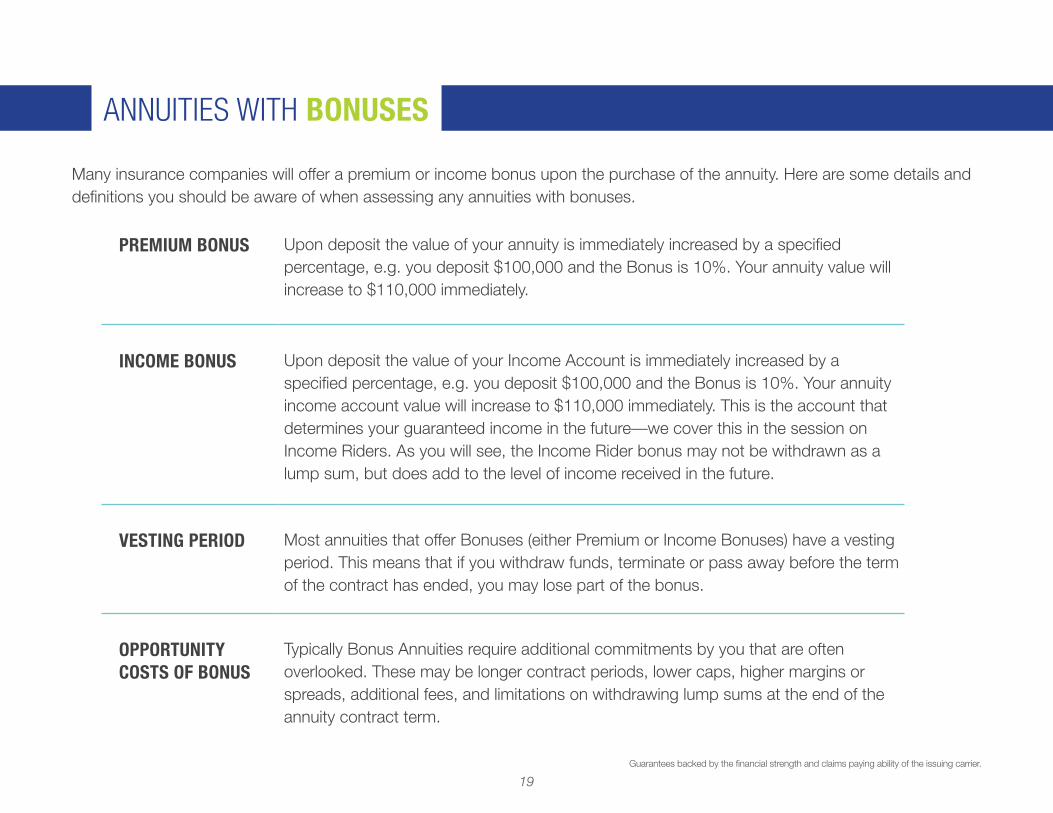

Many insurance companies will offer a premium or income bonus upon the purchase of the annuity. Here are some details and definitions you should be aware of when assessing any annuities with bonuses.

PREMIUM BONUS Upon deposit the value of your annuity is immediately increased by a specified percentage, e.g. you deposit $100,000 and the Bonus is 10%. Your annuity value will increase to $110,000 immediately.

INCOME BONUS

Upon deposit the value of your Income Account is immediately increased by a specified percentage, e.g. you deposit $100,000 and the Bonus is 10%. Your annuity income account value will increase to $110,000 immediately. This is the account that determines your guaranteed income in the future—we cover this in the session on Income Riders. As you will see, the Income Rider bonus may not be withdrawn as a lump sum, but does add to the level of income received in the future.

VESTING PERIOD

Most annuities that offer Bonuses (either Premium or Income Bonuses) have a vesting period. This means that if you withdraw funds, terminate or pass away before the term of the contract has ended, you may lose part of the bonus.

OPPORTUNITY COSTS OF BONUS

Typically Bonus Annuities require additional commitments by you that are often overlooked. These may be longer contract periods, lower caps, higher margins or spreads, additional fees, and limitations on withdrawing lump sums at the end of the annuity contract term.

ANNUITIES WITH BONUSES

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

20

MARKET VALUE ADJUSTMENTS

Annuity contracts often contain a

Market Value Adjustment (MVA)

clause. You should be aware of

what this clause means and how it

may impact you.

MARKET VALUE ADJUSTMENT

Should you decide to withdraw your money outside of the permitted withdrawal privileges provided by the annuity contract, the amount you receive may be more or less than what you invested.

In addition to potential withdrawal charges, if current interest rates move higher than the contract guaranteed rate, you may receive less than the amount you invested.

Conversely, if current interest rates move lower than the contract guaranteed rate, the amount you receive may be more than what you invested. The increase or decrease is called a “market value adjustment.”

2013, March. “Understanding Fixed Annuities and Market Value Adjusted (MVA) Annuities.” Understanding Fixed Annuities and Market Value-Adjusted (MVA) Fixed Annuities Morgan Stanley, Mar. 2013. Web. 27 May 2014.

21

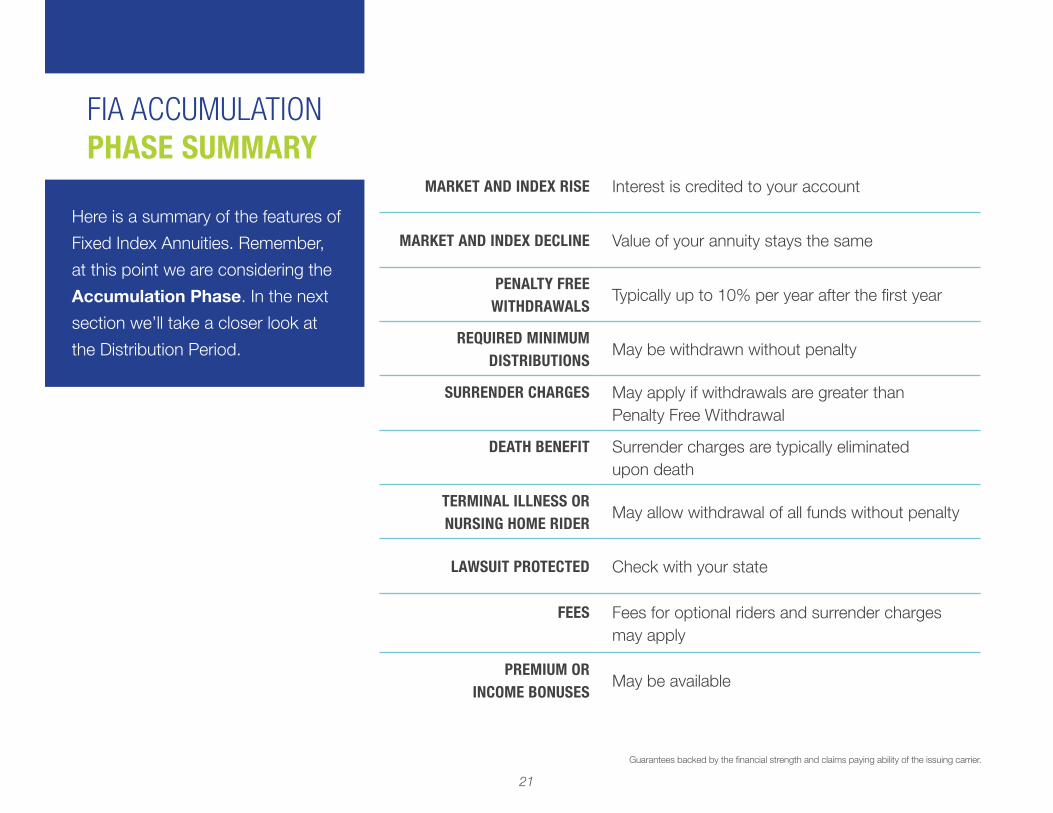

FIA ACCUMULATION PHASE SUMMARY

Here is a summary of the features of

Fixed Index Annuities. Remember,

at this point we are considering the

Accumulation Phase. In the next

section we’ll take a closer look at

the Distribution Period.

MARKET AND INDEX RISE Interest is credited to your account

MARKET AND INDEX DECLINE Value of your annuity stays the same

PENALTY FREE WITHDRAWALS

Typically up to 10% per year after the first year

REQUIRED MINIMUM DISTRIBUTIONS

May be withdrawn without penalty

SURRENDER CHARGES May apply if withdrawals are greater than Penalty Free Withdrawal

DEATH BENEFIT Surrender charges are typically eliminated upon death

TERMINAL ILLNESS OR NURSING HOME RIDER

May allow withdrawal of all funds without penalty

LAWSUIT PROTECTED Check with your state

FEES Fees for optional riders and surrender charges may apply

PREMIUM OR INCOME BONUSES

May be available

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

22

FIXED INDEX ANNUITIES:THE PAYOUT OR DISTRIBUTION PERIOD

23

$

PAYOUT OR DISTRIBUTION PERIOD

INCOMEPAYMENTS

BEGINWITHIN1 YEAR

There are a number of different ways that annuities may pay income during the Payout or Distribution Period. We’ll start with an Immediate Annuity, where payments begin soon after you pay the premium (within 1 year) so there may be a very short Accumulation Phase if any at all. Immediate Annuities require that you pay a lump-sum to the insurance carrier in exchange for a lifetime of payments or payments for a specific period of time. Once payments have begun, there are usually no options by which you can then take your lump sum, or part of your lump payment out. All future payments will be in the form of income payments only.

PAYOUT PERIOD OPTIONS—IMMEDIATE ANNUITY

Guarantees backed by the financial strength and claims paying ability of the issuing carrier. NAIC Buyer’s Guide 2013

Insurer makes payments until the annuitant dies or for a fixed period

24

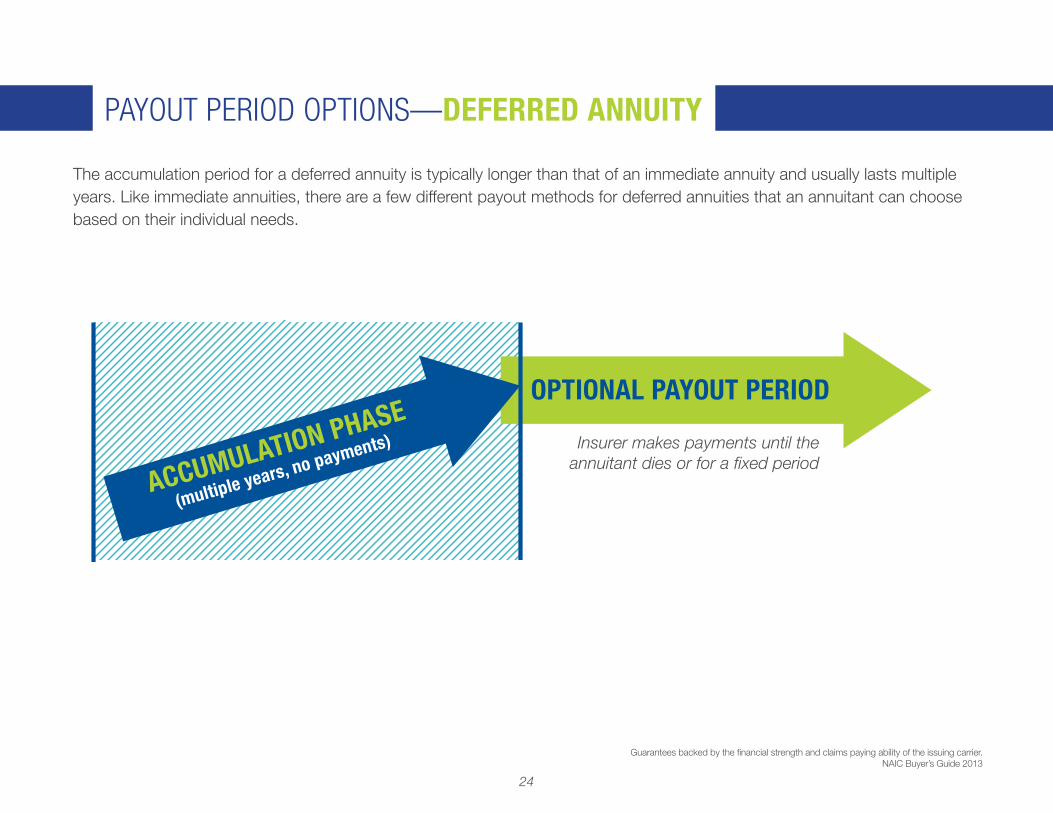

The accumulation period for a deferred annuity is typically longer than that of an immediate annuity and usually lasts multiple years. Like immediate annuities, there are a few different payout methods for deferred annuities that an annuitant can choose based on their individual needs.

PAYOUT PERIOD OPTIONS—DEFERRED ANNUITY

Guarantees backed by the financial strength and claims paying ability of the issuing carrier. NAIC Buyer’s Guide 2013

OPTIONAL PAYOUT PERIOD

ACCUMULATION PHASE

(multiple years, no payments) Insurer makes payments until the annuitant dies or for a fixed period

25

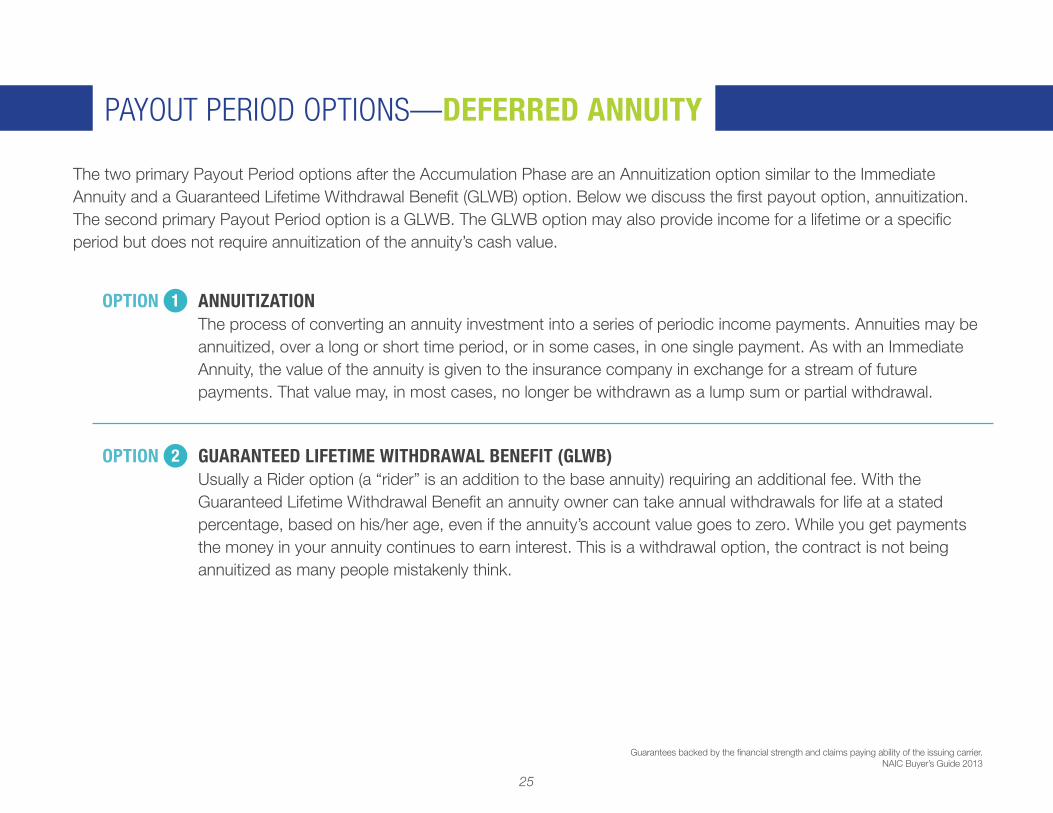

OPTION 2 GUARANTEED LIFETIME WITHDRAWAL BENEFIT (GLWB) Usually a Rider option (a “rider” is an addition to the base annuity) requiring an additional fee. With the Guaranteed Lifetime Withdrawal Benefit an annuity owner can take annual withdrawals for life at a stated percentage, based on his/her age, even if the annuity’s account value goes to zero. While you get payments the money in your annuity continues to earn interest. This is a withdrawal option, the contract is not being annuitized as many people mistakenly think.

The two primary Payout Period options after the Accumulation Phase are an Annuitization option similar to the Immediate Annuity and a Guaranteed Lifetime Withdrawal Benefit (GLWB) option. Below we discuss the first payout option, annuitization. The second primary Payout Period option is a GLWB. The GLWB option may also provide income for a lifetime or a specific period but does not require annuitization of the annuity’s cash value.

PAYOUT PERIOD OPTIONS—DEFERRED ANNUITY

Guarantees backed by the financial strength and claims paying ability of the issuing carrier. NAIC Buyer’s Guide 2013

OPTION 1 ANNUITIZATION The process of converting an annuity investment into a series of periodic income payments. Annuities may be annuitized, over a long or short time period, or in some cases, in one single payment. As with an Immediate Annuity, the value of the annuity is given to the insurance company in exchange for a stream of future payments. That value may, in most cases, no longer be withdrawn as a lump sum or partial withdrawal.

26

Guaranteed Lifetime Withdrawal Benefits have many designs but almost all do the same thing—they provide guaranteed lifetime income in the future which, in most cases, are at predictable levels of income. In other words, it is possible through the use of a GLWB to determine the exact (or minimum) amount of income you will receive at any time in the future, when you decide to begin your income.

The longer you wait to begin your income, the higher the income guarantee. This benefit is sometimes called a Lifetime Income Benefit Rider (LIBR) or Guaranteed Lifetime Income Benefit (GLIB).

INCO

ME

BENE

FIT

ACCUMULATION PHASE

Guarantees backed by the financial strength and claims paying ability of the issuing carrier. NAIC Buyer’s Guide 2013

For illustration purposes only

THE GUARANTEED LIFETIME WITHDRAWAL BENEFITS (GLWB)

27

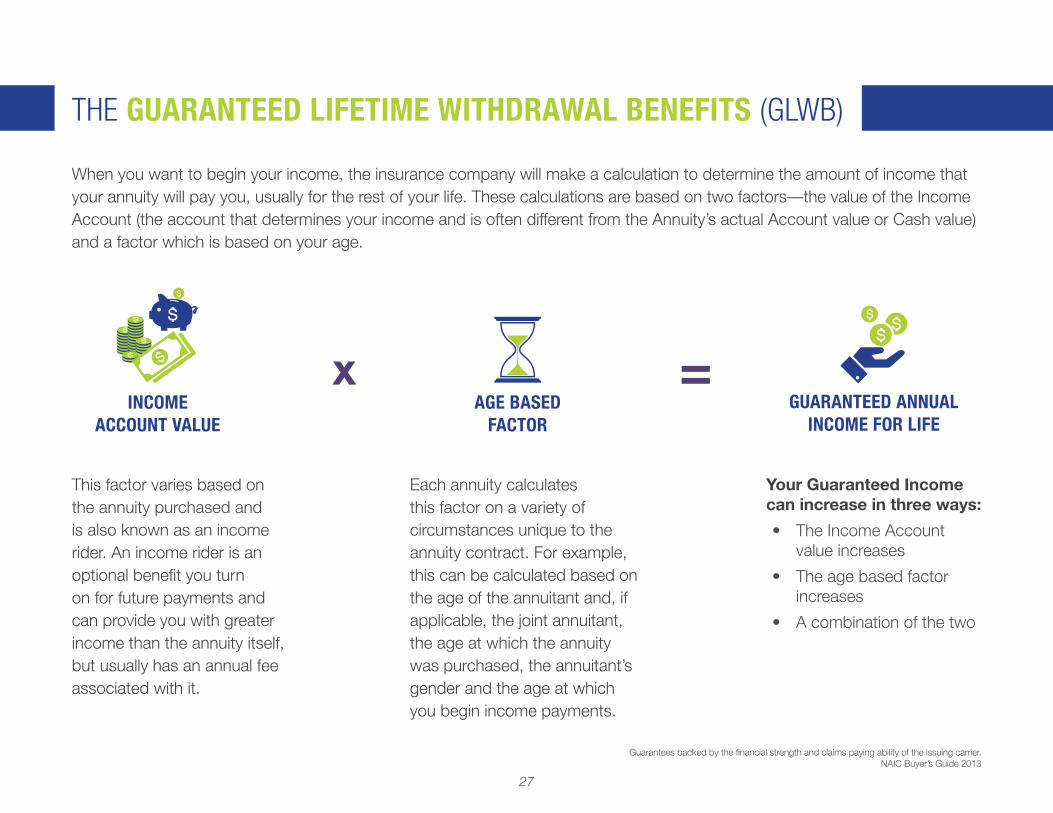

When you want to begin your income, the insurance company will make a calculation to determine the amount of income that your annuity will pay you, usually for the rest of your life. These calculations are based on two factors—the value of the Income Account (the account that determines your income and is often different from the Annuity’s actual Account value or Cash value) and a factor which is based on your age.

THE GUARANTEED LIFETIME WITHDRAWAL BENEFITS (GLWB)

Guarantees backed by the financial strength and claims paying ability of the issuing carrier. NAIC Buyer’s Guide 2013

x =

Each annuity calculates this factor on a variety of circumstances unique to the annuity contract. For example, this can be calculated based on the age of the annuitant and, if applicable, the joint annuitant, the age at which the annuity was purchased, the annuitant’s gender and the age at which you begin income payments.

AGE BASED FACTOR

Your Guaranteed Income can increase in three ways:

• The Income Account value increases

• The age based factor increases

• A combination of the two

GUARANTEED ANNUAL INCOME FOR LIFE

This factor varies based on the annuity purchased and is also known as an income rider. An income rider is an optional benefit you turn on for future payments and can provide you with greater income than the annuity itself, but usually has an annual fee associated with it.

INCOME ACCOUNT VALUE

28

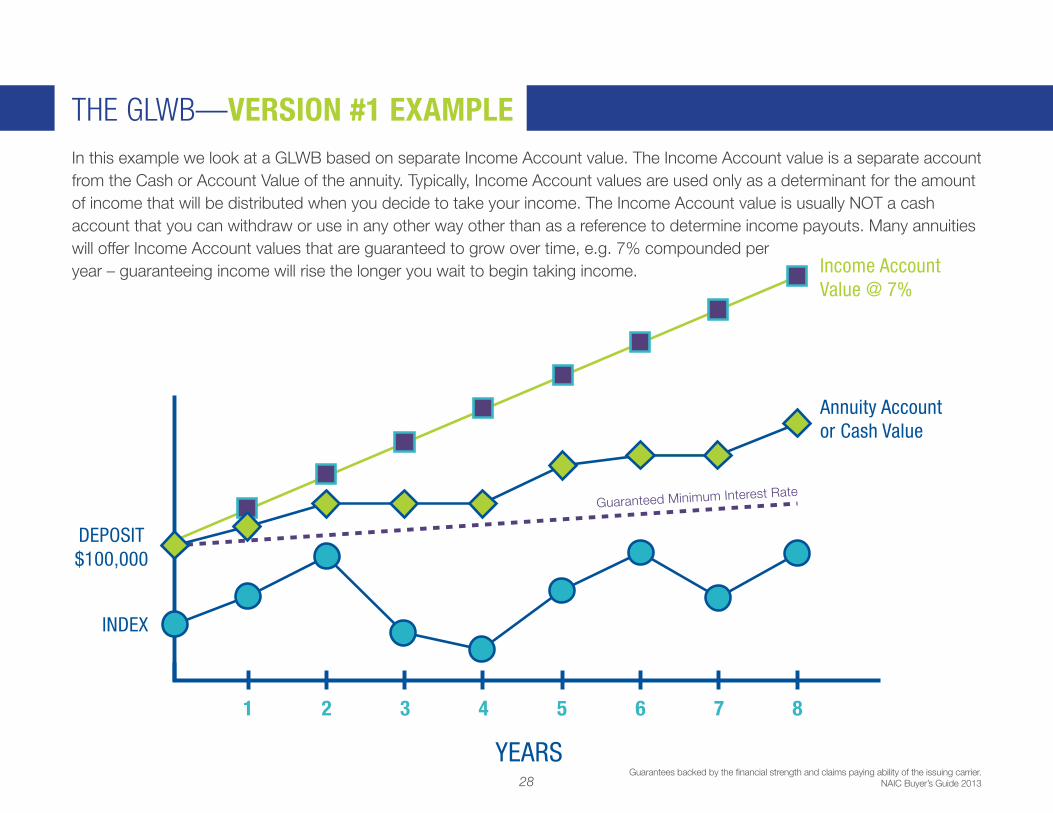

In this example we look at a GLWB based on separate Income Account value. The Income Account value is a separate account from the Cash or Account Value of the annuity. Typically, Income Account values are used only as a determinant for the amount of income that will be distributed when you decide to take your income. The Income Account value is usually NOT a cash account that you can withdraw or use in any other way other than as a reference to determine income payouts. Many annuities will offer Income Account values that are guaranteed to grow over time, e.g. 7% compounded per year – guaranteeing income will rise the longer you wait to begin taking income.

THE GLWB—VERSION #1 EXAMPLE

Guarantees backed by the financial strength and claims paying ability of the issuing carrier. NAIC Buyer’s Guide 2013

YEARS

DEPOSIT$100,000

INDEX

1 2 3 4 5 6 7 8

Guaranteed Minimum Interest Rate

Income AccountValue @ 7%

Annuity Accountor Cash Value

29

xAGE BASED

FACTORGUARANTEED ANNUAL

INCOME FOR LIFEINCOME

ACCOUNT VALUE

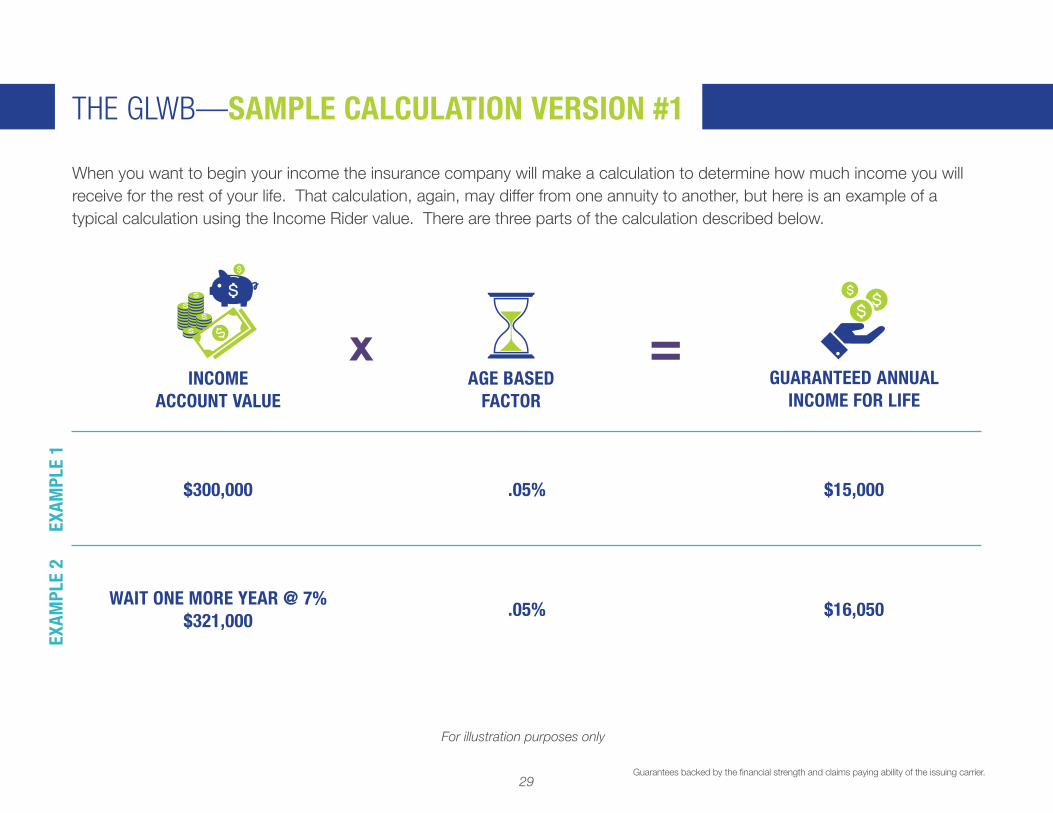

When you want to begin your income the insurance company will make a calculation to determine how much income you will receive for the rest of your life. That calculation, again, may differ from one annuity to another, but here is an example of a typical calculation using the Income Rider value. There are three parts of the calculation described below.

$300,000

WAIT ONE MORE YEAR @ 7% $321,000

EXAM

PLE

1EX

AMPL

E 2

$15,000

$16,050

.05%

.05%

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

For illustration purposes only

THE GLWB—SAMPLE CALCULATION VERSION #1

=

30

THE GLWB—VERSION #2 EXAMPLE

Guarantees backed by the financial strength and claims paying ability of the issuing carrier. NAIC Buyer’s Guide 2013

YEARS

DEPOSIT$100,000

INDEX

1 2 3 4 5 6 7 8

Guaranteed Minimum Interest Rate

Income Account and Annuity Account Value with Interest Bonus

Income Account andAnnuity Account Value

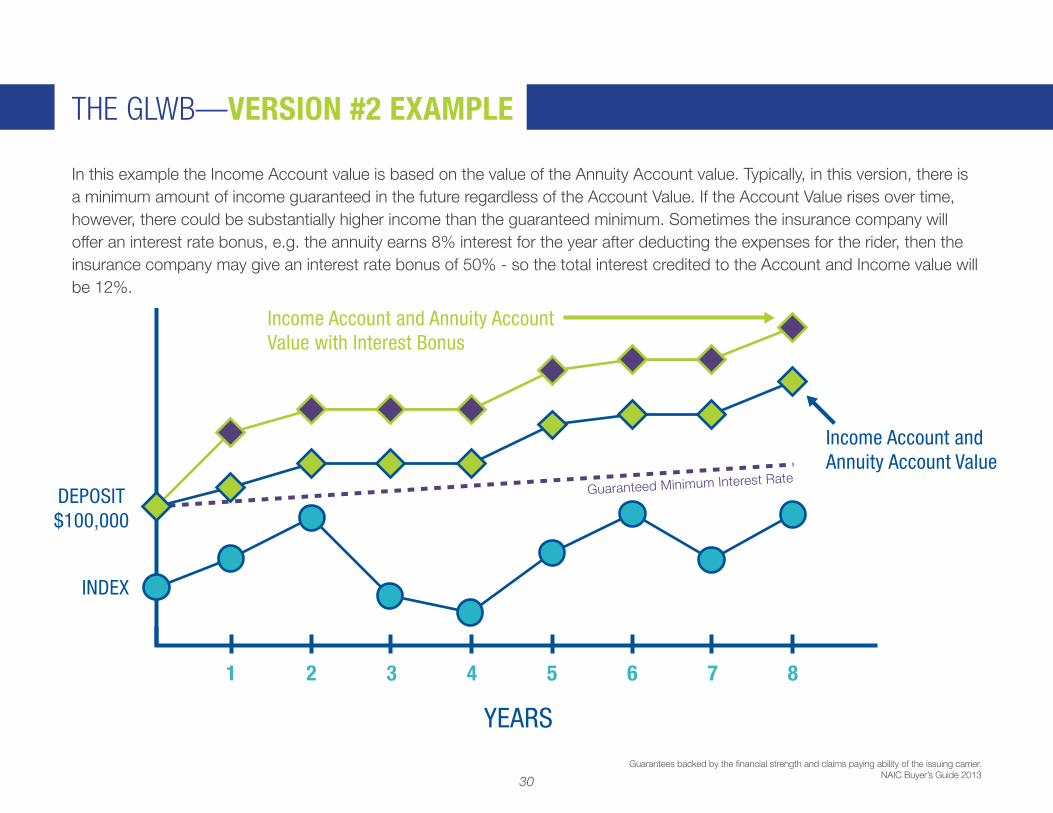

In this example the Income Account value is based on the value of the Annuity Account value. Typically, in this version, there is a minimum amount of income guaranteed in the future regardless of the Account Value. If the Account Value rises over time, however, there could be substantially higher income than the guaranteed minimum. Sometimes the insurance company will offer an interest rate bonus, e.g. the annuity earns 8% interest for the year after deducting the expenses for the rider, then the insurance company may give an interest rate bonus of 50% - so the total interest credited to the Account and Income value will be 12%.

31

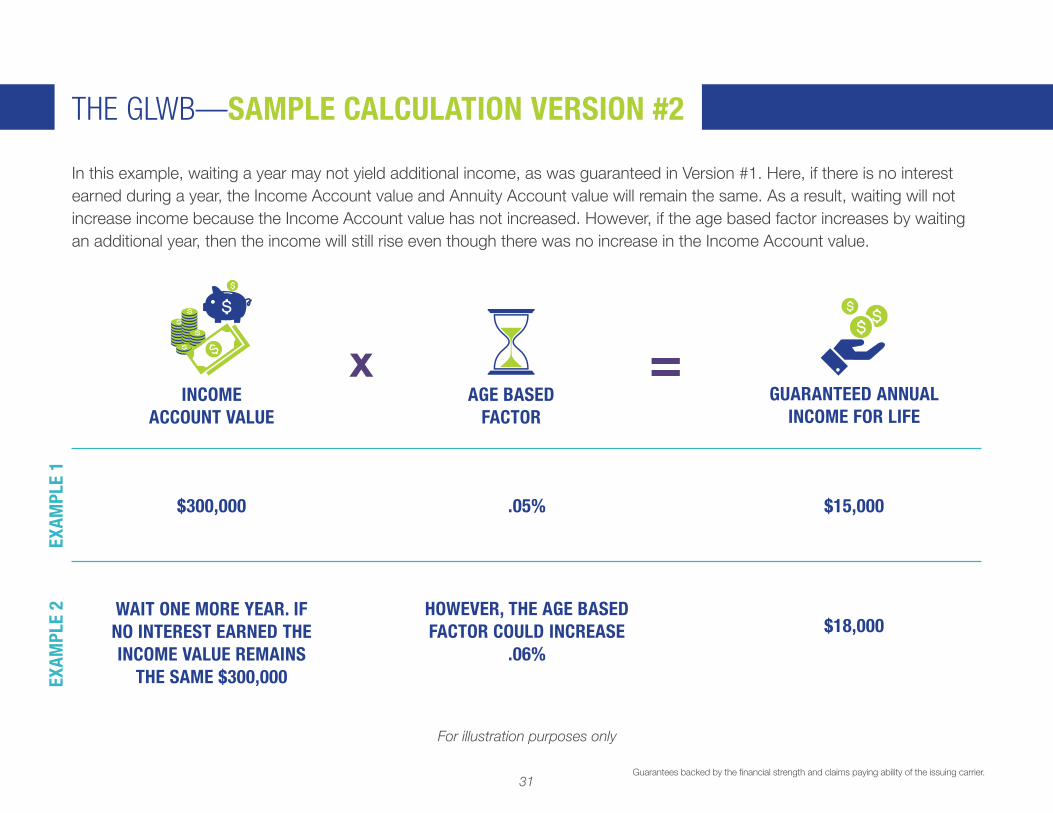

In this example, waiting a year may not yield additional income, as was guaranteed in Version #1. Here, if there is no interest earned during a year, the Income Account value and Annuity Account value will remain the same. As a result, waiting will not increase income because the Income Account value has not increased. However, if the age based factor increases by waiting an additional year, then the income will still rise even though there was no increase in the Income Account value.

THE GLWB—SAMPLE CALCULATION VERSION #2

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

For illustration purposes only

xAGE BASED

FACTORGUARANTEED ANNUAL

INCOME FOR LIFEINCOME

ACCOUNT VALUE

$300,000

WAIT ONE MORE YEAR. IF NO INTEREST EARNED THE INCOME VALUE REMAINS

THE SAME $300,000

EXAM

PLE

1EX

AMPL

E 2

$15,000

$18,000

.05%

HOWEVER, THE AGE BASED FACTOR COULD INCREASE

.06%

=

32

Unlike Annuitization, the GLWB is a withdrawal benefit. That means that funds are withdrawn from your Annuity Account or Cash Value each time a distribution is made. It also means that if there is interest credited to your account that the balance of your money is still earning interest. If the Cash value of your annuity should go to zero, under the GLWB the insurance company will continue to pay you income for the rest of your life.

THE GLWB—WHERE THE INCOME COMES FROM

YEARS

DEPOSIT$100,000

INDEX

1 2 3 4 5 6 7 8

INCOME OR GLWB PAYMENT

Guarantees backed by the financial strength and claims paying ability of the issuing carrier.

ExampleLet’s say you begin income from your GLWB in Year 4. Each time income is distributed to you it will be deducted from your Annuity Cash Account value. When interest is credited the account value will replenish part or all of the withdrawal amount.

33

Here is a summary of the features and benefits of the Guaranteed Lifetime Withdrawal Benefit (GLWB). Remember, we are discussing the Payout or Distribution Period of the annuity.

INCOME GUARANTEE GLWB guarantees income for life to begin at a selected time

DEDUCTIONS GLWB distributions are deducted from the annuity’s Cash Account value

ACCOUNT VALUE GOES TO ZERO

If the Cash Account value declines to zero, income payments will continue for life*

NO LUMP-SUM WITHDRAWAL

Most often, the Income Account value is different from the Annuity Cash Account value and may not be taken as a lump sum distribution—its only use is to determine your income level when you decide to begin taking it

INCOME ACCOUNT AND ANNUITY ACCOUNT

VALUE THE SAME

In some annuities, the Income Account value and the Annuity Account value are the same. This may offer higher potential income but typically lower guaranteed values

FEES

GLWBs usually require an additional fee. This fee will usually be deducted every year, even in a year when no interest is credited to your account. In these cases, your Annuity Cash Account value will decline

FIA PAYOUT OR DISTRIBUTION PERIOD SUMMARY

*If excess withdrawals decrease the account value below the minimum value as outlined in your specific contract, the rider terminates and your income payments stop.

34

FIXED INDEX ANNUITITES SUMMARY

35

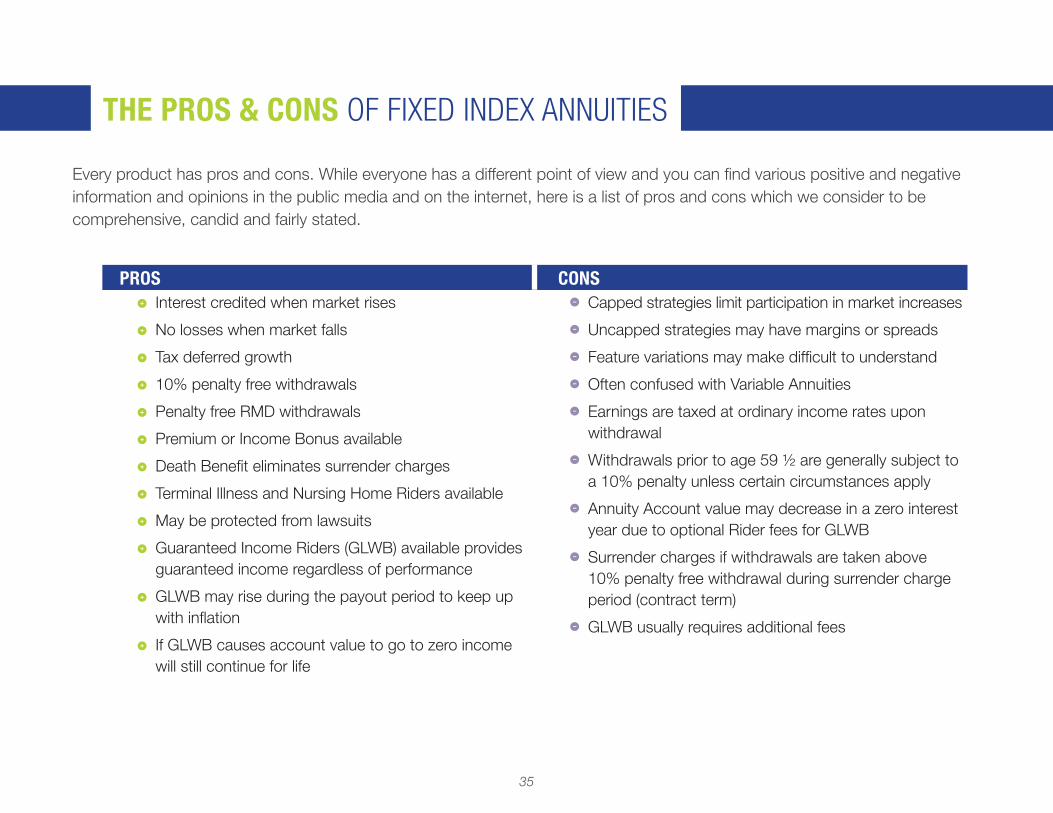

Every product has pros and cons. While everyone has a different point of view and you can find various positive and negative information and opinions in the public media and on the internet, here is a list of pros and cons which we consider to be comprehensive, candid and fairly stated.

PROS CONS Interest credited when market rises

No losses when market falls

Tax deferred growth

10% penalty free withdrawals

Penalty free RMD withdrawals

Premium or Income Bonus available

Death Benefit eliminates surrender charges

Terminal Illness and Nursing Home Riders available

May be protected from lawsuits

Guaranteed Income Riders (GLWB) available provides guaranteed income regardless of performance

GLWB may rise during the payout period to keep up with inflation

If GLWB causes account value to go to zero income will still continue for life

Capped strategies limit participation in market increases

Uncapped strategies may have margins or spreads

Feature variations may make difficult to understand

Often confused with Variable Annuities

Earnings are taxed at ordinary income rates upon withdrawal

Withdrawals prior to age 59 ½ are generally subject to a 10% penalty unless certain circumstances apply

Annuity Account value may decrease in a zero interest year due to optional Rider fees for GLWB

Surrender charges if withdrawals are taken above 10% penalty free withdrawal during surrender charge period (contract term)

GLWB usually requires additional fees

THE PROS & CONS OF FIXED INDEX ANNUITIES

36

HOW THE INSURANCE COMPANY DOES IT

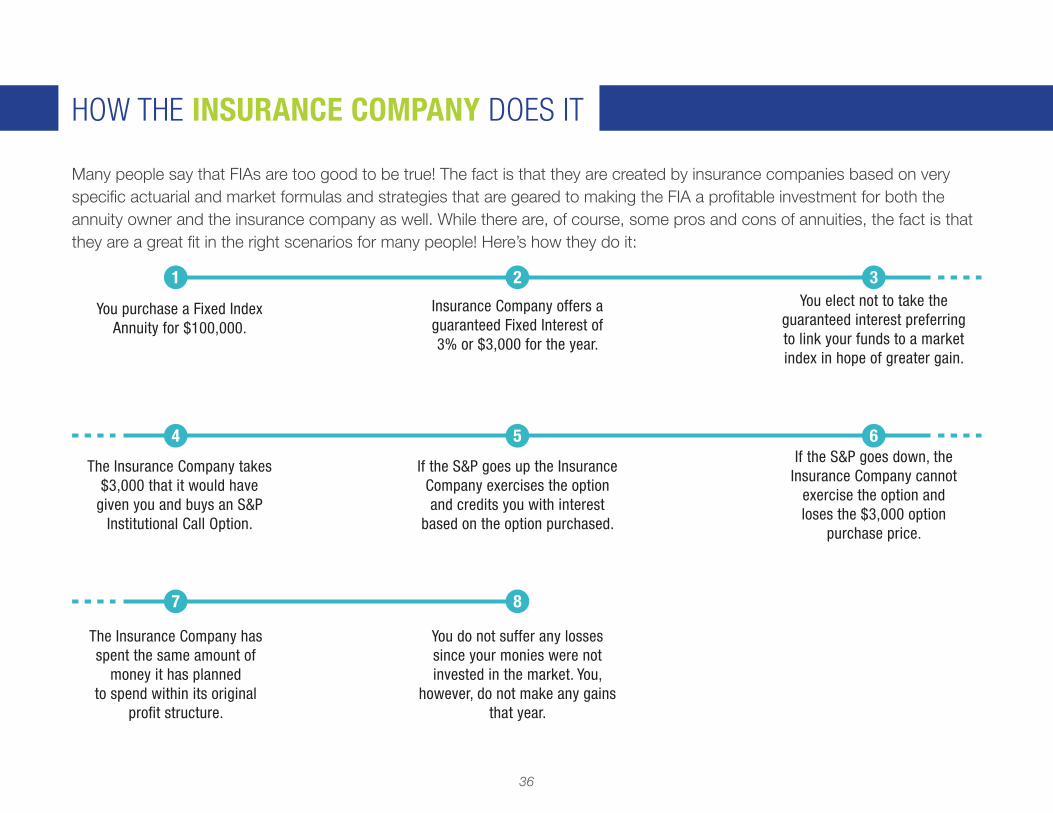

Many people say that FIAs are too good to be true! The fact is that they are created by insurance companies based on very specific actuarial and market formulas and strategies that are geared to making the FIA a profitable investment for both the annuity owner and the insurance company as well. While there are, of course, some pros and cons of annuities, the fact is that they are a great fit in the right scenarios for many people! Here’s how they do it:

The Insurance Company has spent the same amount of

money it has planned to spend within its original

profit structure.

You do not suffer any losses since your monies were not invested in the market. You,

however, do not make any gains that year.

You elect not to take the guaranteed interest preferring to link your funds to a market index in hope of greater gain.

If the S&P goes down, the Insurance Company cannot

exercise the option and loses the $3,000 option

purchase price.

If the S&P goes up the Insurance Company exercises the option and credits you with interest

based on the option purchased.

The Insurance Company takes $3,000 that it would have

given you and buys an S&P Institutional Call Option.

You purchase a Fixed Index Annuity for $100,000.

Insurance Company offers a guaranteed Fixed Interest of 3% or $3,000 for the year.

1

4

7

2

5

8

3

6

37

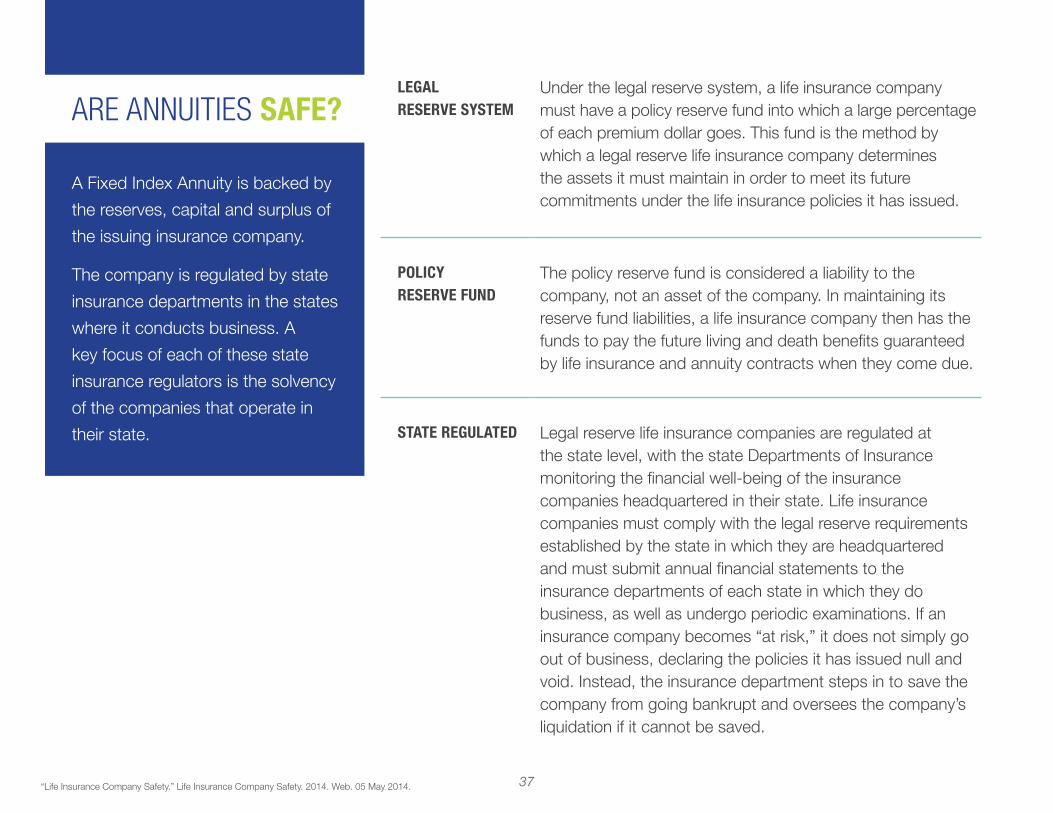

ARE ANNUITIES SAFE?

A Fixed Index Annuity is backed by

the reserves, capital and surplus of

the issuing insurance company.

The company is regulated by state

insurance departments in the states

where it conducts business. A

key focus of each of these state

insurance regulators is the solvency

of the companies that operate in

their state.

LEGAL RESERVE SYSTEM

Under the legal reserve system, a life insurance company must have a policy reserve fund into which a large percentage of each premium dollar goes. This fund is the method by which a legal reserve life insurance company determines the assets it must maintain in order to meet its future commitments under the life insurance policies it has issued.

POLICY RESERVE FUND

The policy reserve fund is considered a liability to the company, not an asset of the company. In maintaining its reserve fund liabilities, a life insurance company then has the funds to pay the future living and death benefits guaranteed by life insurance and annuity contracts when they come due.

STATE REGULATED

Legal reserve life insurance companies are regulated at the state level, with the state Departments of Insurance monitoring the financial well-being of the insurance companies headquartered in their state. Life insurance companies must comply with the legal reserve requirements established by the state in which they are headquartered and must submit annual financial statements to the insurance departments of each state in which they do business, as well as undergo periodic examinations. If an insurance company becomes “at risk,” it does not simply go out of business, declaring the policies it has issued null and void. Instead, the insurance department steps in to save the company from going bankrupt and oversees the company’s liquidation if it cannot be saved.

“Life Insurance Company Safety.” Life Insurance Company Safety. 2014. Web. 05 May 2014.

38

ARE ANNUITIES SAFE?

In the unlikely event that the financial

condition of a carrier becomes

impaired, the State Insurance

department has the ability to take

over the operations of the company

in a process known as rehabilitation.

FAILURE RATES From 1986 through 2011, 31 companies that sold annuities failed. Only 10 of those insolvencies came after 1995. Problems with insurance companies and junk bonds in the early 1990s resulted in state insurance regulators putting tighter capital requirements on insurance companies. Most of the companies that failed were smaller insurance companies with low or no ratings from the agencies. Because of the long-term nature of products such as annuities, regulators hold insurance companies to higher standards of investment and capital reserves.

PROCESS

In most cases, insurance companies under financial duress are simply snapped up by a competitor, and the policies and annuities transfer seamlessly to the new company, with terms and guarantees intact.

“Consumers should feel confident that their life insurance policies are safe. We have a very strict system of state regulation in the U.S. which sees to it that life insurers are adequately capitalized, and that has kept the number of insolvencies to a very minimal level.”

RESULTS

“It’s very, very rare for a life insurer to become insolvent,” says Michael Barry, spokesman for the Insurance Information Institute, an industry trade group. “Life insurers are among the best capitalized insurance companies out there.”

MacDonald, Jay. “Help! My Life Insurance Company Went Broke.” Help! My LIfe Insurance Company Went Broke.

Bankrate.com, 27 Mar. 2013. Web. 27 May 2014.

“National Organization of Life & Health Insurance Guaranty Associations.”Nolhga.com. Web. 06 May 2014.

Plaehn, Tom. “How Safe Is a Lifetime Immediate Annuity From an Insurance Company?” Finance. Zacks Research, 2011. Web. 05 May 2014.

“Life Insurance Company Safety.” Life Insurance Company Safety. 2014. Web. 05 May 2014.

39

Fixed Index Annuities are offered through licensed insurance professionals. Each state has different requirements for licensing and some annuities may or may not offer different features depending on the state in which they are being offered. Regulation of licensing and offerings in a state are governed by the state’s Division of Insurance.

WHO CAN SELL FIAS

Only properly licensed Insurance Agents provide access to the purchase of Fixed Index Annuities

COMMISSION

The Insurance Agent will often receive a one time commission which is paid directly to the agent from the insurance carrier. In other words, you do not pay the commission directly out of your premium. Example: You deposit $100,000 into a Fixed Index Annuity. Your Account Value will be $100,000 even though your agent will have received a commission for the transaction

TRAILER

COMMISSIONS

Some insurance companies offer the option for the agent to take a lower commission up front and earn a trailer over time.

PROS AND CONS

Fixed Index Annuities have become quite popular and are often the main subject at lunch and dinner ‘seminars’ that many insurance agents offer. While you may get good information at these dinner at these events, remember that Fixed Index Annuities have their pros and cons and may or may not be appropriate for your individual circumstances.

HOW FIXED INDEX ANNUITIES ARE SOLD

40

QUESTIONS YOU SHOULD ASK

If you are considering an FIA, make

sure you ask the right questions.

Below is a list of suggested

questions which we recommend

that you ask and have answered to

your satisfaction before purchasing

an FIA.

• What is the guaranteed minimum interest rate?

• What charges, if any, are deducted from my premium?

• What charges, if any, are deducted from my contract value?

• How long is the term?

• What is the participation rate? For how long is the participation rate guaranteed?

• Is there a minimum participation rate?

• Does my contract have a cap?

• Is averaging used? How does it work?

• Is interest compounded during a term?

• Is there a margin, spread, or administrative fee? Is that in addition to or instead of a participation rate?

• Which indexing method is used in my contract?

• What are the surrender charges or penalties if I want to end my contract early and take out all of my money?

• Can I get a partial withdrawal without paying charges or losing interest? Does my contract have vesting?

• Does my annuity waive withdrawal charges if I am confined to a nursing home or diagnosed with a terminal illness?

• What annuity income payment options do I have?

• What is the death benefit?

41

OTHER QUESTIONS ON YOUR MIND

When considering the purchase

of a Fixed Index Annuity make

certain that all your questions are

answered. Use this page to jot

down thoughts and questions

that come up during your

considerations.