uncovering gems in an undervalued market - … dotcom ... hub at kuala lumpur international airport...

TRANSCRIPT

Brought to you by

UncoveringGems In AnUndervalued

Market

CONTENT PAGE

Introduction ................................................05

AirAsia ........................................................... 06

Berjaya Food ...............................................09

British American Tobacco ......................11

Bursa Malaysia ...........................................13

CAB Cakaran ...............................................15

Carlsberg Brewery Malaysia ..................18

CB Industrial Product ...............................20

Century Logistics .......................................23

Cypark Resources .....................................25

Dutch Lady Milk .........................................28

Econpile ........................................................ 31

Gadang Holdings .......................................34

GD Express Carrier ...................................36

Genting Berhad .........................................39

Hartalega .....................................................41

Heineken Malaysia ...................................44

Hock Seng Lee ............................................47

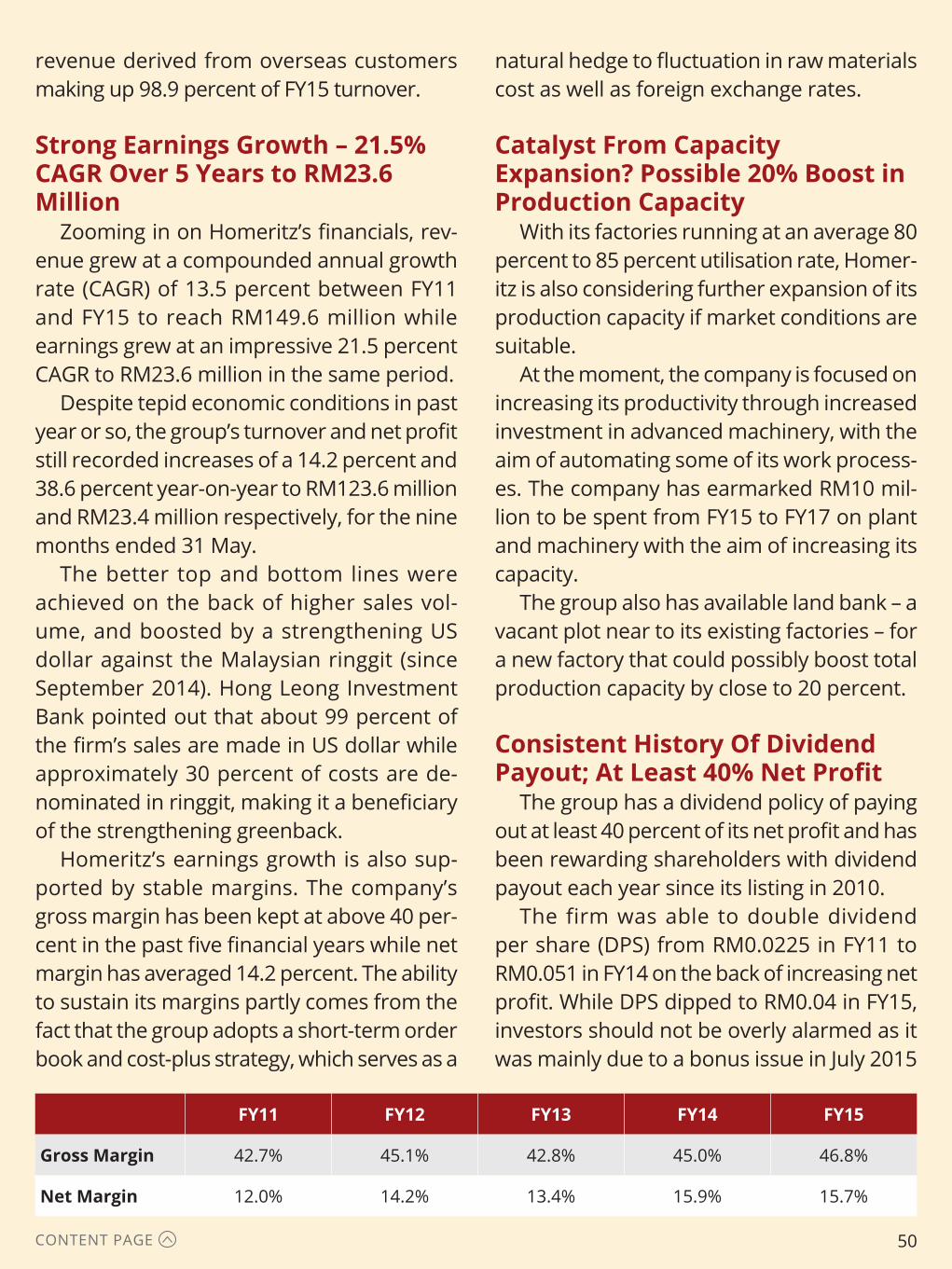

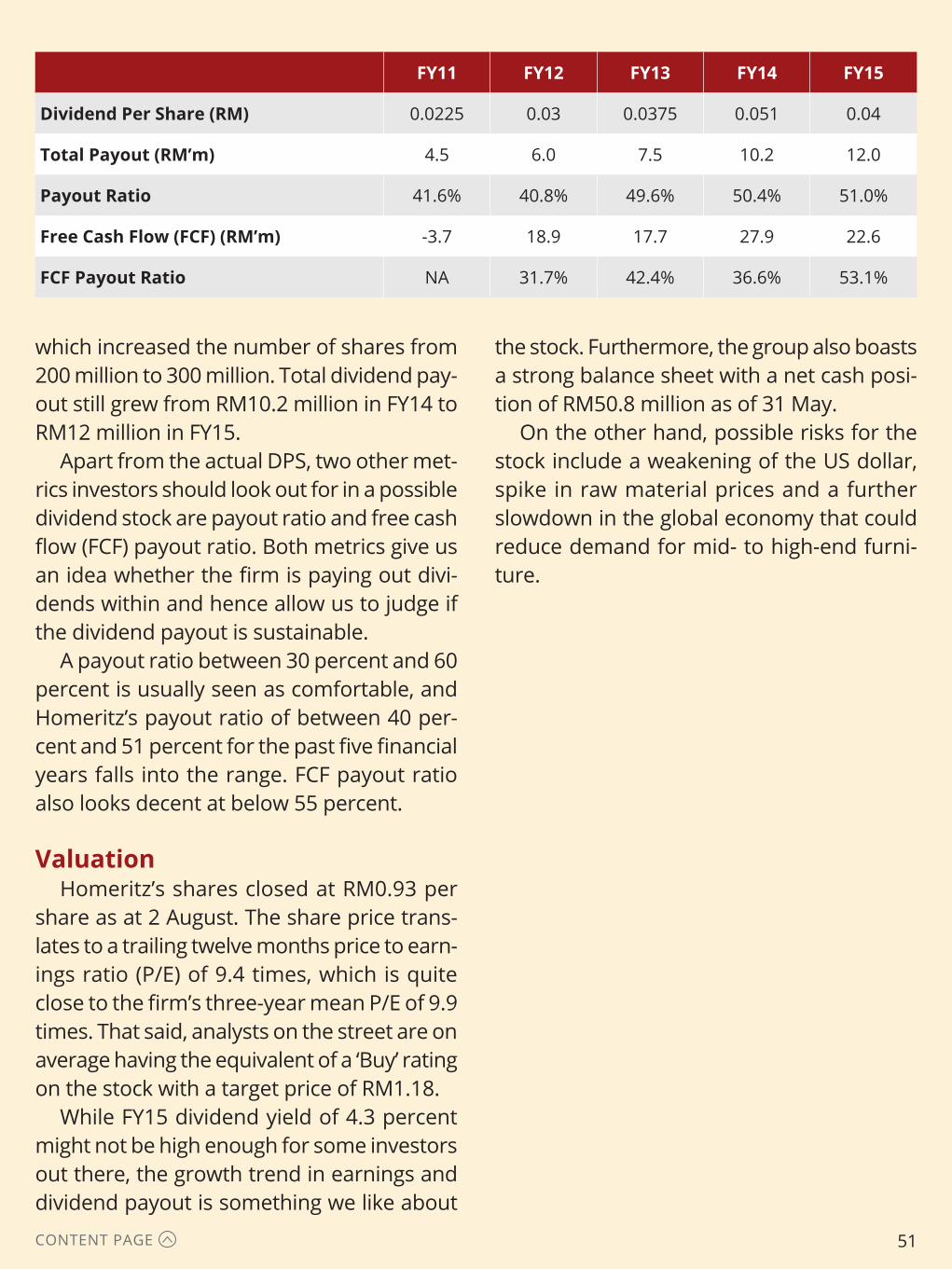

Homeritz Corporation .............................49

IHH Healthcare ..........................................52

CONTENT

CONTENT PAGE

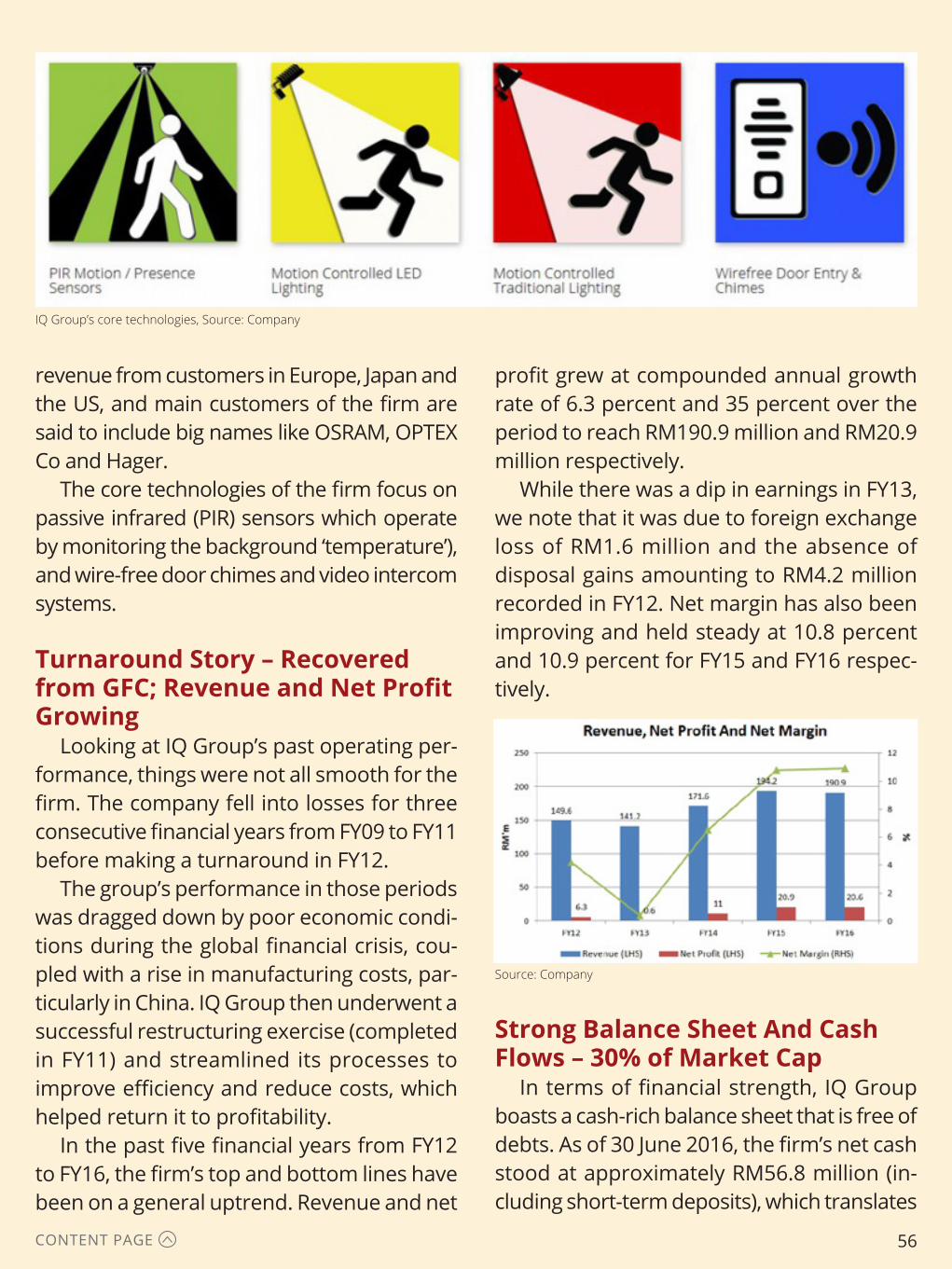

IQ Group Holdings ....................................55

Karex .............................................................58

Kawan Food ................................................60

Kimlun Corporation ..................................62

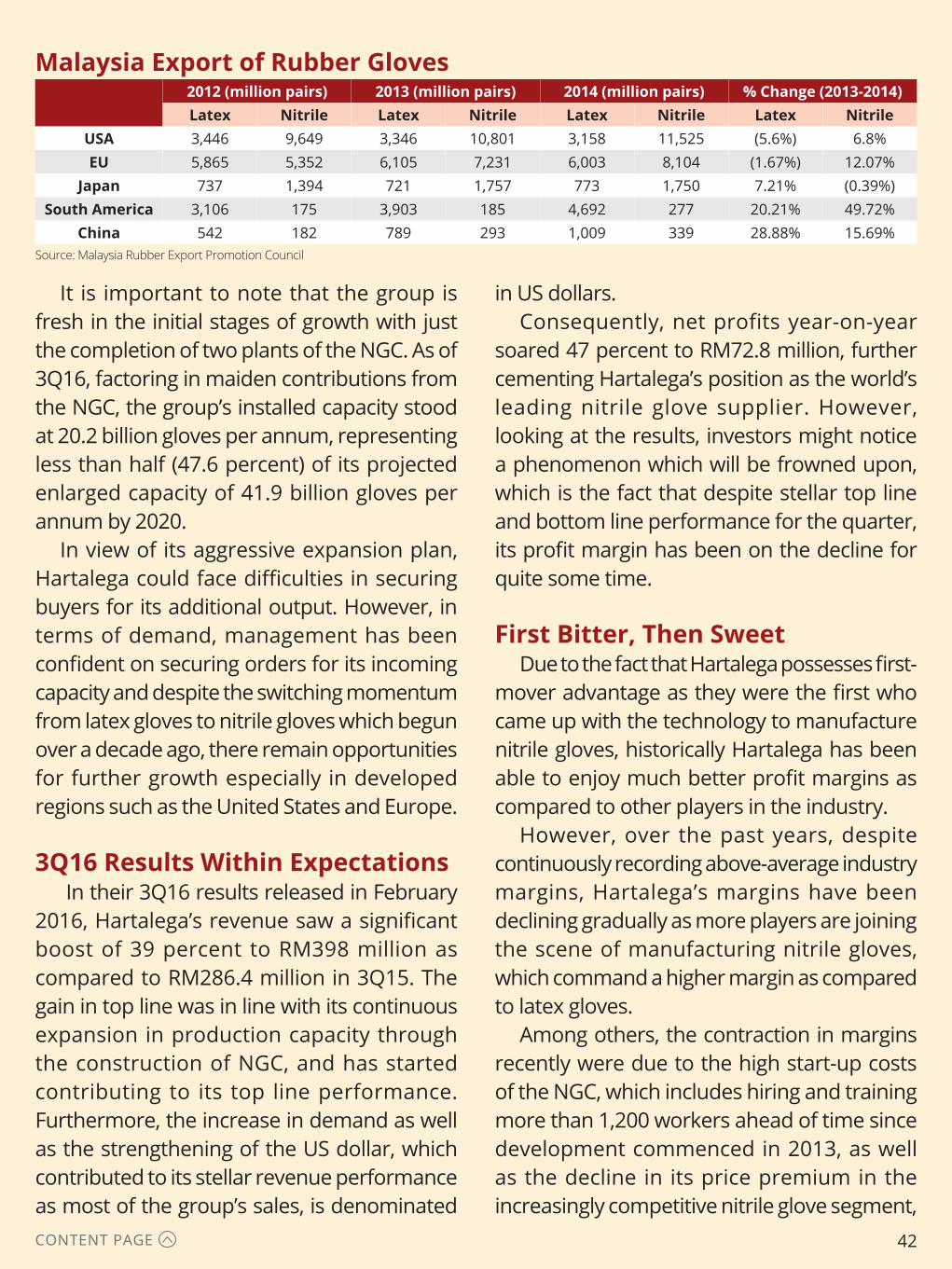

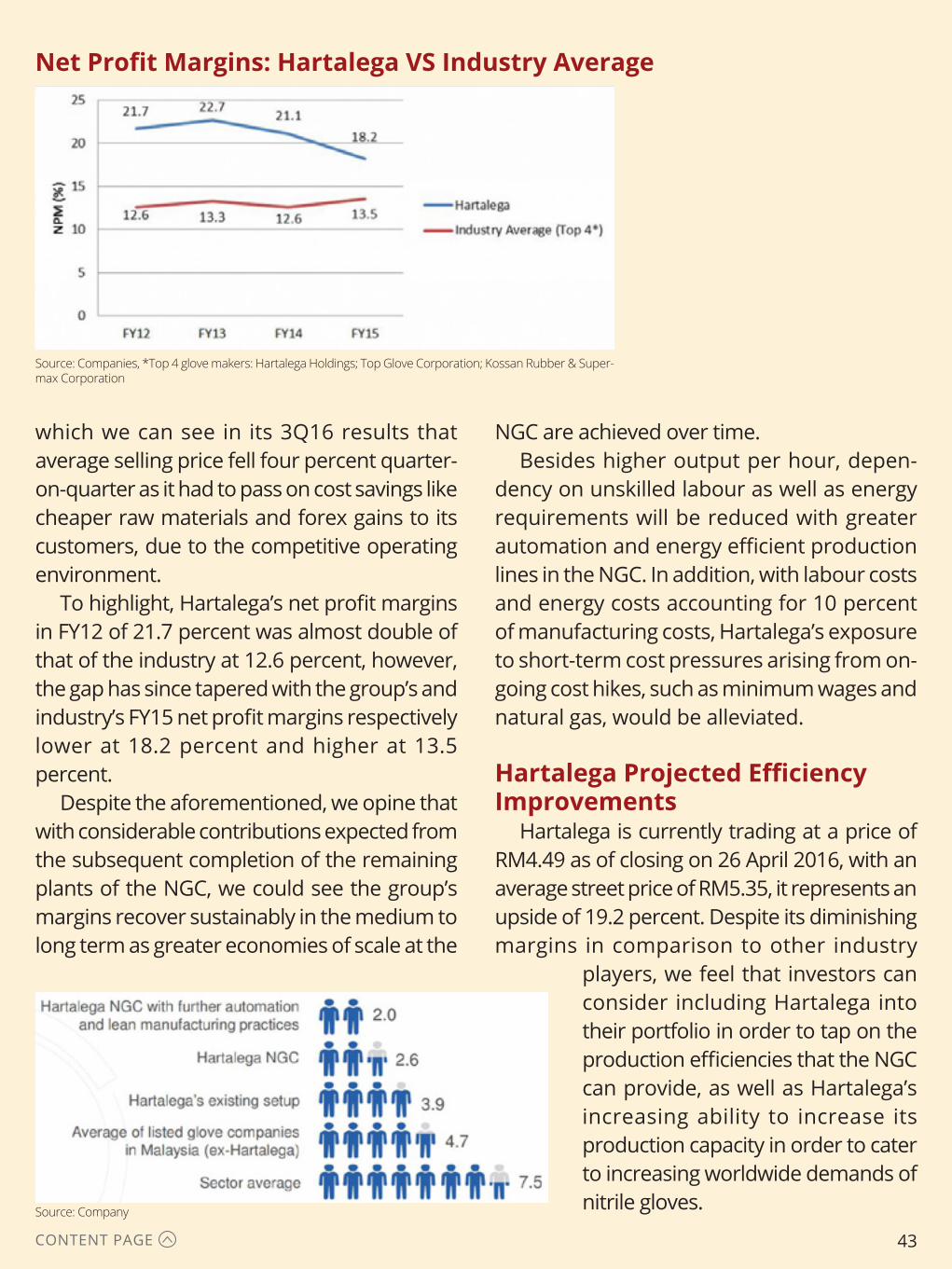

Kossan Rubber Industries ................65/68

LBS Bina .......................................................70

London Biscuits Berhad ..........................73

MMC Corporation .....................................75

Malaysia Airport Holdings ......................78

Nestle (Malaysia) .......................................80

OCK Group ..................................................82

OKA Corporation .......................................84

Press Metal .................................................87

Signature International ...........................90

Sime Darby ..................................................93

Spritzer .........................................................95

Tek Seng Holdings ....................................97

Telekom Malaysia .....................................99

TIME dotCom ...........................................102

Top Glove..........................................104/106

Tune Protect Group ................................108

Bursa Malaysia Berhad (“Bursa Malaysia”) has engaged Shares Investment to produce this report. The research in this report was conducted independently by Shares Investment and the views and opinions expressed in this report are Shares Investment’s own and do not represent the views and opinions of Bursa Malaysia. Bursa Malaysia does not warrant or represent, expressly or impliedly as to the accuracy, completeness and currency of the information in this article. In no event shall Bursa Malaysia be liable to the reader or any other third party for any claim howsoever arising out of or in relation to this article.

This is not a recommendation to purchase or sell any of the mentioned securities. The infor-mation contained herein are the opinions and ideas of the authors and is strictly for educational purposes only. This information should not be construed as and does not constitute financial, in-vestment or any other form of advice. Any investment involves substantial risks, including complete loss of capital. Every investor has different strategies, risk tolerances and time frames. You are advised to perform your own independent research or to contact a licensed professional before making any investment decisions.

There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information set forth herein. Shares Investment and Bursa Malaysia, its related and affiliate companies and/or their employees shall in no event be held liable to any party for any direct, indirect, punitive, special, incidental, or consequential damages arising directly or indirectly from the use of any of this material.

All content and materials on this report are the exclusive property of Shares Investment or its content suppliers, and may be downloaded or printed for your own personal and non-commercial use only. Any content may not be copied, reproduced, distributed, republished, reposted, modified, transmitted, made available to the public, adapted, created into a derivative work or otherwise used or exploited for any purpose.

Disclaimer

Uncertainty appears to be the new norm these days and you should really get used to expecting the unexpected. Surely, most of you did not foresee the shocking Brexit vote or the surprise win by Donald Trump at the US presidential elections.

If you had been looking at the stock markets in the past year, you would likely agree that it has been a pretty bumpy ride. With all the noises in the market, where should you be seeking out investments?

To help you make better-informed decisions, this report features a wide range of companies listed on the Bursa Malaysia. We handpicked 42 companies, did extensive research on their core businesses and wrote each article to help you quickly understand them through a series of brief intros and financial insights.

Amongst these featured companies, you are likely to find some hidden gems that would make a good addition to your portfolio. So read on to find out more.

• Shares Investment Equities Research Team

• Shares Investment Translation Team

[email protected] Visit Shares Investment for more investment research material at : http://www.sharesinv.com

1 December 2016

Introduction

5

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

BY: JOEY HO

AirAsia, a low-cost airline listed on the Mainboard of Bursa Malaysia, is the largest airline in Malaysia in terms of fleet size and destinations — it is also the largest low-cost carrier in Southeast Asia.

The airline, which dominated the market share of its main hub at Kuala Lumpur International Airport (KLIA) in 2015, operates scheduled domestic and international flights to 100 destinations spanning 22 countries.

In 2016, AirAsia’s share price almost doubled to a high of RM2.50 before closing at RM2.30 on 31 May 2016, still translating to a year-to-date gain of 78.3 percent.

1. Flight Vacancies Improved & Hedged Against Oil Volatility

AirAsia exceeded expectations in 1Q16, registering a stunning net profit of RM877.8 million, an increase of 64 percent from RM541 million in 1Q15.

While the strong performance was partly due to a foreign exchange gain of RM464.1 million, the group also reported an impressive operating profit of RM521.1 million (1Q15: RM236.2 million).

Seat load factor improved five percentage points to 88 percent as the number of passengers carried increased by 17.9 percent.

Margins were further boosted by lower average fuel price of US$58 per barrel, down from US$91 per barrel.

It is notable that the group has hedged 75 percent of FY16’s fuel requirements at an average price of US$55 per barrel, largely protecting the airline from sharp fluctuations in global

4 Reasons Why We Think Airasia Is Poised To Fly Higher

AIRASIA

5099

116.28%

AIRASIA116.28%

KLCI-2.63%

6

CONTENT PAGE

oil prices.Crude oil price is hovering slightly below

US$50 per barrel as at 2 June 2016.

2. Aircraft Leasing UnitFollowing the strong performance in 1Q16,

AirAsia had another piece of good news to share.

While the airline intends to divest the unit, which had 43 A320s in its fleet as of the end of March, at some point, the offer needs to be discussed further with the board.

In recent years, as airlines serving the Asia-Pacific region seek to triple their fleet, many are finding that it could be cheaper to lease instead of buying them.

This has led to the rise of leasing businesses which could be more profitable than operating an airline, prompting conglomerates to enter the industry.

The announcement after BOC Aviation, Asia’s biggest aircraft lessor with more than 100 planes leased out to airlines around the world, is slated to start trading in Hong Kong after a US$1.1 billion initial public offering.

3. 35.7% Market Share at Malaysia’s Largest and Busiest KLIA

KLIA, which is operated by Malaysia Airports Holdings (MAH), is currently the largest and busiest airport in Malaysia, and also the world’s 23rd busiest airport by total passenger traffic.

In May 2016, MAH launched the KLIA Aeropolis as part of its five-year business plan, Runway to Success 2020.

The plan is aimed at transforming an area of roughly 100 square kilometres around KLIA into an airport city which is expected to contribute RM30 billion to the nation’s gross domestic product over a 15 year period,

excluding airport terminal operations.Key projects that would be set up in the

airport city include a theme park, hotel, and cargo and logistics park.

MAH has already signed agreements with well-known names such as German logistics company DHL, Malaysian manufacturing and distribution firm DRB-Hicom and AirAsia to develop cargo facilities.

AirAsia currently holds 35.7 percent of the market share at KLIA, carrying 17.5 million passengers in 2015.

Including its subsidiaries, the group holds a strong lead with close to 50 percent of the total number of passengers carried and is set to benefit strongly from the development, which is expected to drive more business investments and tourist traffic to Malaysia.

4. Senai International Airport Expansion Boosted Tourism

In 2015, Senai International Airport (Senai Airport) served 2.6 million passengers.

While the numbers pale in comparison against KLIA, it is notable that this figure almost doubled the total volume in five years ago.

On 29 May 2016, AirAsia will launch services to Guangzhou, making it the first direct flight to China from Senai Airport.

The airline, which already flies to Hat Yai and Bangkok from Senai Airport, has its sights on more direct flights to India, Myanmar, and the Philippines.

With the introduction of the new direct route to Southern China, the Johor government aims to achieve one million tourist arrivals from China in 2016.

Last year, tourist arrivals from China grew to 797,862 from 628,087 in 2014 after the government waived visas.

Previously, without direct flights from China,

7

CONTENT PAGE

Chinese tourists visited Johor Bahru via KLIA or Changi Airport in Singapore.

AirAsia’s plans to boost connectivity at Senai Airport holds great potential as Malaysians travelling on available routes would not need to cross over to Singapore.

Given the strength of the Singapore dollar, the move is also likely to attract more Singaporeans to use the Senai Airport as their gateway to popular holiday destinations in Southeast Asia.

ValuationBased on the last closing price on 31 May

2016, AirAsia shares currently trade at a price-to-earnings ratio (P/E) of 11.8 times.

A peer in the low-cost carrier industry, Tiger Airways Holdings, last closed at S$0.46 on 4 March 2016 equivalent to a P/E of 143.8 times, before it was taken private by Singapore’s flag carrier, Singapore Airlines.

The flag carrier’s shares are currently trading at a PER of 15.5 times based on the last closing price of S$10.68 on 31 May 2016.

Given the low valuations and strong earnings potential ahead, we believe that AirAsia’s shares should be trading at higher valuations. Currently, the average street target price stands at RM3.06, presenting the potential for an approximate 33 percent upside.

8

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

SI RESEARCH:Berjaya Food – Could Coffee Chain Drive Growth?

BY: JOEY HO

Berjaya Food (BFood), a 50.9 percent-owned Food and Beverage (F&B) arm of Berjaya Corporation, operates well known F&B chains in Malaysia, such as Kenny Rogers Roasters (KRR), Berjaya Starbucks (BStarbucks) and Jollibean. The group’s coverage mainly spans across Malaysia, Indonesia and Singapore. As of FY15, the group derived 84.3 percent of its revenue from its home ground in Malaysia.

Limited Growth DriversBFood has been benefitting from the full control of the

Starbucks Coffee chain of cafes and retail stores in Malaysia since the acquisition of the remaining 50 percent stake in BStarbucks on 18 September 2014. With 195 Starbucks Coffee outlets as at 31 July 2015, the group is currently the market leader in the coffee chain industry in Malaysia garnering over 40 percent market share. BFood also plans to open 25 outlets per annum from FY16 to FY19. The move is likely to boost the revenue contribution from the coffee chain to over 70 percent in the next two years.

While BStarbucks has contributed significantly to the group’s growth, the premium coffee chain is vulnerable to a slowdown in consumer spending as well as fluctuations in costs as approximately 40 percent of BStarbucks cost of goods sold is denominated in US dollars. We view the heavy reliance on this business segment negatively as any adverse factors towards this segment could lead to a significant impact on the

BJFOOD

5196

-24.03%

BERJAYA FOOD-24.03%

KLCI-2.63%

9

CONTENT PAGE

group’s overall earnings.

Dragged Down By Supplementary Segments

Despite a top line growth of 67.1 percent or RM166.7million in 9M16, the latest results fell short of expectations given that an approximate six months contribution from BStarbucks boosted FY15 top line by RM226.4 million. The disappointment was attributed to the group’s supplementary segments.

KRR chain of restaurants in Malaysia recorded negative same store sales growth (SSSG) of 19.4 percent in Malaysia as consumer spending softened following the introduction of goods and services tax as well as the steep depreciation of the Malaysian ringgit. While the group’s Jollibean business in Singapore experienced a negative SSSG of 5.5 percent year-on-year. Operations in both Indonesia and Singapore ended in the red for 9M16 with losses of RM4.2 million and RM0.5 million respectively.

Given the lack of growth catalysts in the two struggling overseas segments, we do not expect a significant recovery in the near term.

Risky Financial PositionThe group’s aggressive expansion has

weakened its financial position. Based on 9M16’s balance sheet, the group’s current ratio stood at 0.6 times. Of the group’s current assets, cash and bank balances of RM36.2 million made up only 30.8 percent. While the debt to total asset ratio stood at 0.47 as of 9M16, it is notable that intangible assets made up 60.7 percent of the group’s total assets.

In addition, net cash inflows from operations in recent years have been insufficient in covering the required capital expenditure, resulting in negative free cash flows since

FY13. Consequently, BFood’s finance costs rose rapidly from a clean slate in FY13 to RM8.9 million in FY15 and tallying with an interest coverage of 4 times as of 9M16.

Demanding ValuationsAs of 18 April 2016, Berjaya Food’s shares

closed at RM1.92, down 34.2 percent from its 52 week high of RM 2.92. Based on the latest FY15 results, the group’s shares are currently valued at a price-to-earnings ratio (P/E) of 3.9 times, including significant re-measurement gains of RM160.5 million. Excluding the one-off gains, the shares would be trading at a P/E of 42.3 times, while the consumer sector P/E is currently pegged at approximately 25 times.

In view of the heavy reliance on a single business segment, loss making supplementary segments as well as the deteriorating financial position, we prefer to stay on the sidelines for now. It is likely that BFood will need to reverse the supplementary segments into the black and show strong growth in its coffee chains before it regains its attractiveness.

10

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

SI RESEARCH:British American Tobacco (Malaysia) – Headwinds Blowing On An Expensive Puff

BY: SUA XIU KAI

British American Tobacco (Malaysia) (BAT), the leading manufacturer and distributor of cigarettes in Malaysia which is principally engaged in the manufacture, importation and sale of cigarettes, pipe tobaccos and cigars, should be no stranger to investors. BAT distributes its products under a portfolio of different popular cigarette brands such as Lucky Strike, Kent, Dunhill and Pall Mall and holds more than 60 percent legal market share in Malaysia.

In recent times, we have seen BAT at the receiving end of some policies by the Malaysian government to curb the consumption of cigarettes. Due to the negative nature of the products sold by the group, the industry is getting more challenging by the day, and we look at how BAT is coping in such uncertain times.

Unfavorable Government Policies, Illegal Cigarettes On The Rise

In November 2014, the tobacco industry was hit by a 12 percent increase in cigarette excise tax and shortly after in November 2015, the Malaysian government further increased cigarette taxes by more than 40 percent.

This was a move which the group described as an “unprecedented massive increase in cigarette excise”, which came after the implementation of the Goods and Services Tax at 6 percent on 1 April 2015, the group had to increase its prices of its brands after taking into consideration the sum

BAT

4162

2.40%

BRITISH AMERICAN TOBACCO

2.40%

KLCI-2.63%

11

CONTENT PAGE

mandated by the excise increase and its impact on GST and inflationary cost pressure.

The increase in cigarette excise, which ultimately led to the increase in prices, also gave rise to another problem, the expansion of the already large number of illegal cigarettes in the market. According to the Illicit Cigarette Study 2012 by the Confederation of Malaysian Tobacco Manufacturers, every 1 out of every 3 packs of cigarettes sold in Malaysia are smuggled, for which taxes/duties are evaded.

With the rise in excise tax and illegal cigarettes, the group is bound to get affected especially in its sales volume and the impacts can already be felt from the moment the tax hike was exercised. Domestically, the group manufactured 8.2 billion sticks of cigarettes in FY14 and 7.2 billion sticks in FY15, a drop of around 12 percent.

This could imply that consumers are hanging in their habits but are substituting it with cheaper alternatives, as from June to August 2015 the volume of illegal cigarettes increased by 0.2 percentage points quarter by quarter. Do note that illegal can be purchased from RM4 to RM5, significantly cheaper than the group’s cigarettes which retail at RM15 to RM18 after the tax hike.

Ceasing Malaysian Manufacturing, Tougher Times Ahead

On 18 March 2016, the group unexpectedly announced the plans to shut down its plants in Petaling Jaya, Selangor, citing the increasingly challenging business environment. Going forward, the group will source tobacco products from its factories regionally for the Malaysian market.

Though the disposal of the manufacturing plant in Malaysia can be seen as a positive

move to protect the company’s interest in an increasingly challenging industry, it indirectly affirms the pessimistic view of the outlook of the tobacco sector which has already been heavily battered by high excise tax and significant trading of illegal cigarettes.

With volume growth anticipated to decline, the increasingly challenging environment requires the company to restructure and transforms its business, which apart from the winding of factory operations; include the sharpening of its commercial capabilities whilst optimizing the supply chain and transactional activities to ensure that the group remains competitive as a market leader.

Historically, the group has been consistently issuing dividends with dividend yield ranging from 4.4 percent to 5.7 percent in the past 6 years. However, in view of the pessimistic market outlook and future earnings expected to contract, investors should keep a lookout for signs of whether BAT is able to maintain its dividend policy.

With a mean street price of RM59.55, it provides little upside to its current price of RM55.30 as of 23 March 2016. With the market split between “Hold” calls and “Sell” calls, we feel that it is best that investors stay clear of this expensive puff of smoke for now, as it will not just be harmful to your health, it might be detrimental to your portfolio too.

12

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

SI RESEARCH:Bursa Malaysia – Holding Up In Challenging Times

BY: SUA XIU KAI

Bursa Malaysia (Bursa), is the stock exchange operator of Malaysia and just like any stock exchanges around the world such as the New York Stock Exchange, Tokyo Stock Exchange and Singapore Stock Exchange, Bursa is in an industry where it possesses a strong economic moat in the form of strict regulations, and it being the only stock exchange in the country.

Economic moat, a term coined and popularized by billionaire investor Warren Buffett, refers to a business’s competitive advantage that it has over its competitors and new entrants and can be derived in the form of branding, regulation, technological capabilities and economies of scale.

Having established the fact that Bursa practically holds a monopoly position in Malaysia, where strong regulations has made it very tough for new entrants to challenge its position in the market, we look at its recent performance to see if it has lived up to expectations.

Past Growth Tapers To Flattish ResultsFrom FY09 to FY13, Bursa has enjoyed relatively strong gains

in its operating revenue with a Compound Annual Growth Rate (CAGR) of 10.24 percent. At FY09, its operating revenue stood at RM297.8 million and by FY13 it has risen substantially to RM439.8 million.

The same trend for operating revenue was also reflected on Bursa’s net earnings. FY10 recorded a net profit of RM113 million and has risen significantly to RM198.2 million in FY14.

BURSA

1818

2.40%

BURSA MALAYSIA2.40%

KLCI-2.63%

13

CONTENT PAGE

However, the upward trend seems to be a thing of the past when Bursa released its FY15 results earlier this month.

For FY15, Bursa’s operating revenue increased just 3.4 percent to reach RM487.7 million and net profits had a meagre increment of just 0.19 percent to RM198.6 million.

Investors may be wondering what could have happened to bring such a powerhouse with relatively strong performances and strong economic moats to report such flattish results. We found some possible explanations in a part of its financial statements, where it commented about seasonal or cyclical factors:

“The Group’s performance is not affected by any seasonal or cyclical factors but is affected by the activities in the Securities and Derivatives Markets”

Just like all stock exchanges, Bursa has a non-cyclical business model which makes money when companies get listed and when traders perform transactions, regardless of buy or sell. Therefore the flattish results in recent years were actually due to the slowdown in growth of capital market activities.

Lacklustre Results All ExpectedThe lacklustre growth in revenue and net

earnings of Bursa due to the softening of trading activities were actually within the expectations of many brokerage houses in view of many factors in the Malaysian economy.

In recent years, the Malaysian economy has been dealt several blows from plunging commodities prices, weaker Malaysian ringgit, and market sentiments have been depressed by broad macro uncertainties such as the slowdown of China and further potential outflow in foreign funds.

IPO Pipeline Running DryOther than the softening of trading activities,

the weak sentiments of the Malaysian economy has also impacted another source of Bursa’s income, which is from the listing of companies, which allows Bursa to collect listing fees and also benefit from the trading of share of the new listed counters.

In 2015, Bursa had 11 initial public offerings (IPO) as compared to 15 in 2014, and this is of no surprise with investors’ sentiment at a low. Bursa also saw 5 notable IPOs which were planned but ultimately did not materialise – Sime Darby Motors, Edra Global Energy, Weststar Aviation Services, Qualitas Healthcare Corporation and Asian Healthcare Group.

In the beginning of 2016, the delay in the RM637.5 million IPO of energy and water group Ranhill Holdings did no favours in curbing the jitters for investors in what was once the most popular destination in the region.

All in all, Bursa has been hit in recent years mainly due to the slowdown in the growth in trading activities as well as the decrement and delays in IPOs. Moving forward, investors should remain cautious and continue keeping track of the political and economic stability in Malaysia, which will directly translate to investors’ sentiments to the market and affect their trading volume. However on a positive note, the management of Bursa has stated that they expect more active trading of the derivatives market, spurred by volatility in commodity prices.

As of 23 February 2016, Bursa is trading at a P/E of 22.97x and is already trading near its average target price of RM8.66. We believe that any upside will only come in tandem with market optimism affected by the global economy outlook as well as local stability.

14

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

BY: JOEY HO

CAB Cakaran Corporation (CAB), a leading integrated poul-try producer based in Malaysia, also engages in businesses such as supermarkets, food products manufacturing and fast food outlets. As of FY15, the group’s largest segment was the integrated poultry farming and processing division, making up 78.7 percent of total revenue and 97.1 percent of the group’s consolidated segment profit.

Strong Double-Digit Growth and Improved Sales

CAB has registered strong double-digit growth in its revenue while net profit experienced some fluctuations from FY11 to FY15. Despite the poorer bottom line in FY12, the compounded annual growth rate for its revenue and net profit registered a decent 16.1 percent and 6.2 percent respectively. For 9M16, the group reported revenue of RM793.4 million, placing it on track to achieve a record revenue of RM1 billion for FY16.

CAB Cakaran Corporation – Future Muslim Middle Class To Drive Growth

CAB Cakaran 9M16 FY15 FY14 FY13 FY12 FY11Revenue (RM’m) 793.4 891.7 672.4 609 534.6 491

Net Profit (RM’m) 7.2 16 11.2 11.9 -3 12.6

Net Profit Margin (%) - 1.8 1.7 2 - 2.6

Return On Equity (%) - 10.4 6.9 8.6 1.1 13.7

While CAB’s net profit margin levels have not been too impressive, the group expects to see an improvement in net profit for FY16 supported by better sales of broiler meat and improved efficiency in the management of breeder and broiler farms.

Should the group be able to achieve revenue of RM1

CAB

7174

2.55%

CAB CAKARAN CORPORATION

2.55%

KLCI-2.63%

15

CONTENT PAGE

billion this fiscal year ending 30 September 2016, excluding improvement in efficiencies, simply maintaining a net profit margin of 1.8 percent would already net the group a decent profit of RM18 million.

Expansion & Strategic Ventures; Production Capacity Per Month to Double

CAB has recently embarked on an expan-sion spree as well as strategic ventures into the renewable energy business.

In June, the group has signed a conditional agreement to acquire Farm’s Best’s poultry processing unit, Farm’s Best Food Indus-tries (FBF), for RM9.5 million. The purchase, which was originally priced at RM80 million, is expected to boost CAB’s total slaughtering production capacity by approximately 36,000 birds per day to 110,000 birds per day.

Upon completion of the acquisition of FBF, two other letters of intent (LOI) that the group signed in February will come into effect. The two LOIs involve the acquisition of assets owned by Sinmah Breeders and Sinmah Livestocks.

The acquisitions, once completed, are expected to increase CAB’s current produc-tion capacity per month of 4.5 million birds by over 50 percent. The higher production volume is part of CAB’s strategy to achieve economies of scale, leading to improved cost efficiency and profit margins.

On the group’s power generation business venture, despite plans to partner a Japanese company falling through, the group remains confident that the solar farm will be opera-tional by early 2018 and the biomass facility in 2018 or 2019.

We view the biomass facility positively as the group will be using chicken manure pro-

duced by its breeding farms as fuel for the generation of electricity. In addition to gen-erating revenue from waste that previously had little or no market value, the facility will also produce fertiliser as a by-product from the incineration of chicken manure.

Muslim Middle Class to Drive Halal Products Demand

According to a publication by the Pew Re-search Centre, the Muslim population in Sin-gapore is expected to overtake Christians as the second largest faith group by 2050. The projection showed an increase in the propor-tion of Muslims to 21.4 percent in 2050 from just 14.3 percent in 2010, largely supported by migration from Malaysia.

Globally, Muslims have the highest fertility rate at an average of 3.1 children per woman, significantly above the second highest group, Christians at 2.7, as well as the average of all non-Muslims at 2.3.

In addition to the growing Muslim popu-lation, the Muslim middle class is expected to triple to 900 million by 2030, driving the demand for halal products. According to a report by Thomson Reuters, the halal food industry is projected to be worth US$1.6 tril-lion by 2020.

ConclusionBased on a share price of RM1.64, CAB’s

shares are trading at a trailing twelve months price to earnings ratio (P/E) of 15.4 times, which appears to be fairly priced based on the company’s current performance. In com-parison, larger market capitalisation rival QL Resources trades at a trailing twelve months P/E of 26.5.

Overall, we foresee an increasing demand for the CAB’s poultry products as the halal

16

CONTENT PAGE

market maintains its rapid expansion. In ad-dition, the group’s effort to improve efficien-cies, as well as the venture into the renewable energy business, is likely to improve margins in the medium term. Given the strong earn-ings potential ahead, investors could see more value in CAB should the group’s plan to announce an official dividend policy by the end of September materialise.

17

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

SI RESEARCH:Carlsberg Brewery Malaysia – Still Brewing Steadily

BY: JOEY HO

Carlsberg Brewery Malaysia (Carlsberg) was founded in 1969 as part of the Carlsberg Group’s venture into the Southeast Asian market. To-date, the group has been brewing the Carlsberg Green Label Beer for over 40 years. Over the years, the group has also diversified its brands from a single flagship beer brand to a dynamic portfolio of international premium brews and strong local power brands. As of FY15, the group depended heavily on Malaysia, which contributed 64.1 percent of the total revenue.

Weakened Local CurrencyIn FY15, revenue from Singapore grew by 31.8 percent,

offsetting an RM143.3 million decrease in revenue from Malaysia. The lion city’s share of revenue contribution also climbed to 32.9 percent from just 25.3 percent in FY14.

During the same period, the Malaysian ringgit plunged sharply against the Singapore dollar to as low as over three ringgit per Singapore dollar from around RM2.65 in January 2015. While the decline in the local currency benefits export gains, the strongest momentum only began in August. It is likely that such foreign exchange movements only contributed to approximately 10 percent of the revenue growth and the remaining 21.8 percent is likely to be demand driven growth.

Main Markets Hit By HeadwindsCarlsberg boasts a strong market share in the two main

CARLSBG

2836

21.88%

CARLSBERG BREWERY MALAYSIA

21.88%

KLCI-2.63%

18

CONTENT PAGE

geographical segments, Malaysia and Singapore, which contributed a combined 97 percent of total revenue in FY15. The group claims to be the market leader in Malaysia with a share of the Malaysian beer market in excess of 50 percent, while holding second place in market position in Singapore with a market share of 18 percent.

The group has faced a series of headwinds in Malaysia. In March 2016, the Malaysian government revised the existing tax structure for alcoholic beverages which led to a hike in the price of beer by approximately 10 percent. The move comes close to a year after the government implemented a six percent Goods and Services Tax in April 2015. Breweries are likely to report thinner margins in the coming year as they absorb part of the taxes. In addition, breweries are likely to face a stronger competition from contraband beer following the increase in price of beer.

The largest export market, Singapore, saw a Liquor Control (Supply and Consumption) Act which came into force in April 2015 in a bid to minimise public disorder. Under the law, drinking in public places as well as retail sales of alcoholic beverages have been regulated, with stricter rules implemented for popular drinking zones such as Geylang and Little India.

Stable Financial RatiosDespite the headwinds in FY15, the group’s

return on equity (ROE) dipped just 3.9 percentage points to 65.6 percent maintaining an impressive ROE of over 60 percent since FY12.

In FY15, the group paid out a dividend of RM217.1 million, up RM30.6 million from RM186.5 million in FY14. The group also spent RM29.9 million more on the acquisition of property, plant and equipment as part of its investing activities. Due to the higher dividend and capital expenditure, cash and cash

equivalents fell by 53.4 percent to just RM41 million. However, it is notable that despite the lower cash balance, the group still maintains a current ratio of 1.3 times.

In FY15, the group generated an operating profit of RM267.5 million against finance costs of just RM6.8 million, equating to a high interest coverage ratio of over 39 times. Carlsberg’s debt ratio stood strong at 0.48 times, with total assets of RM661.7 million against total liabilities of RM319.2 million. In addition, current assets of RM410.7 million made up a significant 62.1 percent of the group’s total assets.

We view the group’s healthy ratios positively as it will provide much resilience in difficult times.

RisksWhile the weakened Malaysian Ringgit

has been favorable to the group’s exports which currently makes up approximately 35.9 percent of its total revenue, unforeseen foreign exchange movements could lead to volatility in the group’s earnings.

New laws such as the Liquor Control (Supply and Consumption) Act in Singapore could potentially affect the demand and availability of alcoholic drinks. The group’s performance could be negatively affected in the unlikely event that new rules come into force.

Going forward into FY16, domestic consumption in Malaysia is expected to weaken following the price hike, while Singapore operations and exports sales would be the growth driver to support weaker domestic sales. Export sales will also benefit from the new contract starting FY16 with the group’s Hong Kong affiliate.

Carlsberg’s shares closed at RM13.98 on 31 March 2016. Currently, the average street target price stands at RM13.80.

19

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

BY: SUA XIU KAI

As the strongest El Nino phenomenon in almost two de-cades ravaged agricultural production and squeezed inven-tories throughout growers across the globe, we have seen unprecedented fluctuations in commodity prices.

With the recent uptrend in crude palm oil price, brought by the contraction in supply due to unfavourable weather condi-tions and spurring new investments by plantation companies to boost palm oil production, we have identified one Malaysian firm associated with the palm oil business which will fare well.

Today, we zoom in on CB Industrial Product Holding (CBIP) to have a closer look at how this palm oil construction and engineering firm is expected to be able to excel in the highly volatile crude palm oil industry.

What Is CBIP?Established in the 1980s, CBIP is primarily involved in three

main business segments: Palm oil engineering; special pur-pose vehicle retrofitting; and oil palm plantation and milling. It is also the first publicly-listed player in the palm oil engineering sector globally.

The group’s main markets are centralised in Indonesia, Ma-laysia and the African/Central American region. CBIP is also the joint-holders of the Modipalm Continuous Sterilization (MCS) milling system through its wholly-owned subsidiary, Modipalm Engineering, together with the Malaysian Palm Oil Board.

With the MCS milling system patent in hand, CBIP is able

Why This Malaysian Palm Oil Construction And Engineering Firm Is Poised For A 17% Rally

CBIP

7076

-2.09%

CB INDUSTRIAL PRODUCT-2.09%

KLCI-2.63%

20

CONTENT PAGE

to be a one-stop centre for the design, sup-ply, construction and installation of palm oil mills with the capacity to undertake turnkey projects of various sizes, both MCS mills and conventional mills, ranging from capacities of five-tonnes per hour to 120-tonnes per hour.

Backed by the various benefits brought by its patented technology, which ranges from automation of palm oil mills and cost savings in the form of less labour usage to higher oil extraction rate through oil-loss recovery, the group has built more than 80 MCS mills to date globally.

In its special purpose vehicle business, the group focuses on the designing, fabrication, manufacturing, retrofitting and maintenance works of special purpose vehicles. The group’s special purpose vehicles ranges from fire fight-ing and rescue vehicles, utility vehicles, air ground vehicles and even military and infantry vehicles.

Banking on the success of its engineering and equipment segment and special purpose vehicle business, the group has also gradually diversified into the upstream business of oil palm plantation through a series of strategic acquisitions over the years.

For its FY15 revenue breakdown, the palm oil engineering segment contributed 77.4 percent, the special vehicle purpose vehicle business contributed 22.3 percent, and the remaining 0.3 percent was contributed by the relatively new plantation segment.

Uninspiring 1Q16, But Expect Better Quarters Ahead

In its most recent 1Q16 results released in May 2016, the group posted a relatively uninspiring results with revenue for the quar-ter falling 3.8 percent to RM113.2 million, as compared to RM117.6 million from a year ago,

mainly due to lower billing special purpose vehicles division.

Net profits for the quarter took an even big-ger hit with a 57.7 percent plunge, standing at RM9.3 million as compared to RM22 million for 1Q15. Management cited that the poor perfor-mance for the quarter was mainly due to lower margin in the palm oil engineering division. The investment in asset management as well as unrealised foreign exchange translation losses from its palm oil plantation division were the main reasons for lower margins.

Despite mediocre results for the quarter, looking at the group’s past results from FY11 should bring comfort to investors as CBIP has been able to consistently maintain its revenue and profits amidst volatility in the market.

For the past five years, the group’s revenue has been hovering around the range of RM454 million in FY11, and RM554.1 million for FY15. Net profit in the same period also ranged be-tween RM103.9 million in FY11 to RM93.6 mil-lion for FY15 (FY12 net profit was particularly higher at RM240 million due to a one off gain of RM139.6 million from the disposal of its Sarawak palm oil operations).

Although the group had a weak start to the year, we still expect its financial performance to improve in the upcoming quarters, sup-ported mainly by its strong order book in both the palm oil engineering segment as well as its special purpose vehicle segment.

As of the release of its 1Q16 results, man-agement has also shared that for its palm oil engineering segment, order book stood strong at RM495 million. As such, it is expected to keep the group busy for the year, which bodes well for the performance of the segment for FY16 and FY17. Order book for the special purpose vehicles as at 1Q16 stood at approximately RM242 million.

21

CONTENT PAGE

With its healthy order book, the group is poised to improve – if not at least maintain – its performance in time to come. Although no sizeable contract was announced on a year-to-date basis, management is confident of secur-ing about RM400 million worth of contracts in FY16 for its palm oil engineering segment.

Modipalm And Plantations Expected To Take A Hit

As the plantation industry is all about economies of scale and in the palm oil milling process, every drop of oil is expected to be squeezed from the palm fruits. A key measure of the efficiency of palm oil mills is the amount of oil that can be extracted from a fruit bunch.

The higher the extraction rate, the higher the profitability – assuming production costs can be maintained or kept low. And for this particular reason, big plantation companies like Sime Darby, United Plantations and PT Astra Agro Lestari have turned to CBIP for its patented MCS technology to improve their milling process efficiency.

With huge players in the industry using its patented technology, it poses as a great source of recurring income through the replacement of parts and upgrading works of palm oil mills.

However, one important factor investors should note is the expiry of the pioneer tax status for its MCS process this year, which will dent net profit contribution from the division.

Furthermore, higher operating losses from its plantation segment is to be expected. CBIP owns approximately 83,000 hectares of plan-tation land bank in Kalimantan Tengah, Indo-nesia, with about 7,400 hectares planted area (8 percent) as at end-2015 and average age profile of three years.

Upon planting 1,290 hectares in 2015, the group is expected to accelerate its planting

exercise to 3,000 hectares in 2016. The higher operating expenses from the planting exercise are expected to widen the segment’s losses to RM10 million.

As of 9 August, CPIB’s shares closed at RM2.00, representing a stagnant year-to-date (YTD) performance. However CBIP’s shares reached a YTD peak of RM2.30 in April 2016 and has been on the decline since then. At its current share price, it represents a price to earnings ratio (P/E) of 13.2 times.

With its healthy order book in both palm oil engineering and special purpose vehicle divi-sions, investors should be able to see better numbers in time to come, assuming produc-tion costs can be maintained. With a street price of RM2.34, it represents a potential up-side of 17 percent. Looking at the operations of the group, it certainly does not look like a difficult target to hit.

22

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

BY: JOEY HO

Century Logistics Holdings (Century), listed on the Mainboard of Bursa Malaysia, is a leading provider of supply chain solutions. Founded in 1970 as a forwarding agent, Century now runs eight logistics centres and a fleet of 600 delivery trucks. The group also has a Halal certification, which is beneficial for businesses in a largely Islamic community.

The wide range of services offered is classified into two main categories, total logistics services and procurement logistics services. The total logistics services segment involves the main supply chain of the group’s customers, while the procurement logistics services segment takes on a more comprehensive scope of the supply chain including procurement, assembly and repackaging services.

As of FY15, the total logistics services segment made up 82.3 percent and 83.8 percent of total revenue and net profit respec-tively. Apart from the procurement logistics services segment, Century has also recently ventured into the business of data management solutions, though the new segment has yet to contribute to the group’s performance as at FY15.

Stable PerformanceCentury has displayed a stable performance over the past

three years with revenue growing at a compounded annual

Century Logistics Holdings – Could E-Commerce Be The Key?

Century Logistics Holdings 1H16 FY15 FY14 FY13 FY12Revenue (RM’m) 152.1 297.9 275.2 255.8 256.9

Net Profit (RM’m) 9.9 31.9 33.3 22.6 17.6

Gross Profit Margin (%) 27.7 28.2 28.4 31 28.1

Net Profit Margin (%) 6.5 10.7 12.1 8.8 6.9

Dividend (sen) 2.5 5.5 8 11 8

CENTURY

7117

11.98%

CENTURY LOGISTICS HOLDINGS11.98%

KLCI-2.63%

23

CONTENT PAGE

growth rate of 5.1 percent to RM297.9 million in FY15, while net profit almost doubled to RM31.9 million. In addition, the group is also able to maintain its gross profit margin level at around 28 percent.

While there certainly have been some fluctua-tions in the group’s net profit margin, we have noted that these were due to gain on sale of assets of RM11.1 million and RM14.6 million in FY15 and FY14 respectively.

Despite the lower dividends, Century’s shares are commanding a dividend yield of 6 per-cent based on the latest full year dividends of RM0.055 and the latest closing price of RM0.915 as of 3 October 2016.

South Korean PartnershipCJ Korea Express Corporation (CJ Korea),

South Korea’s largest courier service company, has recently acquired a 31.4 percent stake in Century through its Singapore-based subsid-iary, CJ Korea Asia. The deal, valued at RM174.8 million, has made the Korean firm the largest shareholder in Century. The deal is part of CJ Korea’s strategy to achieve its goal of becom-ing a dominant player in the Malaysian logistics sector.

Through the new partnership, Century will be able to leverage on CJ Korea’s strengths such as its technology systems and solutions, while the latter plans to leverage on Century’s strong local customer base.

The Korean firm also anticipates continued e-commerce growth and plans to equip Century for the e-commerce and parcel delivery busi-ness through the introduction of its advanced technology, engineering, system and solution.

Going forward, both firms will also integrate their logistics and administrative activities, result-ing in a larger network and more cost-efficient operation through the sharing of key logistics

hubs and networks, cross-selling and new busi-ness opportunities.

While there have not been any immediate visible benefits, given that CJ Korea paid a 39.4 percent premium, it is likely that the Korean firm has some well thought-out plans in store.

e-Commerce GrowthCould the Korean firm’s vision on the e-

commerce and parcel delivery business spell a brighter future for Century?

According to statistics portal, Statista, e-com-merce revenue in Malaysia is expected to hit US$894 million in 2016, up 30.1 percent from 2015. With the increasing smartphone and user penetration, the country’s e-commerce revenue is also expected to exceed US$2.5 billion in 2021.

As such, we believe that Century’s strong po-sition in the logistics sector could pave the way for much gain in the future.

The Bottom LineBased on the latest closing price of RM0.915

as of 3 October 2016, Century’s shares are fairly valued at a price to earnings ratio of 10.7 times with a dividend yield of 6 percent.

While there does not seem to be any near term catalyst for Century, the growing e-com-merce business appears promising for the group’s planned expansion into the e-com-merce and parcel delivery business. Meanwhile, dividend investors could enjoy the 6 percent dividend yield as they look forward to potential capital appreciation in the longer term.

24

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

BY: JOEY HO

Cypark Resources (Cypark) is one of Malaysia’s largest environmental technology and engineering specialist.

Founded in 1999, Cypark started its main business in the closure and restoration of landfills as well as the provision of management services. Despite being in the business for only more than 15 years, the group has built itself a strong track record ranging from various environmental management projects to renewable energy projects.

Malaysian Environmental Tech Company To Benefit From Increased Green Energy Demand

In recent years, the group has also been working to diversify into the less cyclical business of renewable energy generation and waste management concession business to strengthen its income generating capability.

Net Profit Doubled Over 5 Years; 1H16 Net Profit 58.6% of FY15

In FY15, contributions from the environmental engineering

CYPARK

5184

16.22%

CYPARK RESOURCES

16.22%

KLCI-2.63%

25

CONTENT PAGE

segment made up 53.9 percent of total revenue, down from 63.4 percent in FY14, as the segment registered a decline of 10.3 percent. However, the renewable energy segment accelerated 13.5 percent, to make up 15.7 percent of total revenue, offsetting the decline in the environmental engineering segment.

The group boasts a strong track record with a consistent improvement in revenue, net profit, dividend as well as net income margin over the past four years. Net profit more than doubled from FY11 to FY15 while revenue increased by 56 percent as the group’s business continues to grow.

Although dividends remained flat at RM0.05 for the last two years, the payout has in fact increased at a compounded annual growth rate of 17.4 percent to RM0.05 in FY15 from just RM0.0263 in FY11. The group also managed to add a modest 4.9 percentage points to its net income margin during the same period.

In the latest 1H16 financial results release, the group’s net profit of RM25.5 million already made up 58.6 percent of the previous full year net profit, positioning it to soar through FY16.

Cypark’s management is currently bullish about its dividend policy due to the stronger cash flow and shareholders could expect a dividend payout of 30 percent to 40 percent, up from the current 25 percent should the group see a strong end to the year.

Apart from the overall performance, the group maintains a stable balance sheet

Cypark Resources 1H16 FY15 FY14 FY13 FY12 FY11Revenue (RM’m) 145.2 251.9 238.8 220.7 195.8 161.5

Net Profit (RM’m) 25.5 43.5 39.9 35.9 25.6 20.1

Dividend (sen) - 5 5 4 3.75 2.63

Net Income Margin (%) 17.6 17.3 16.7 16.3 13.1 12.4

position with a current ratio of 1.2 times as of 1H16, with cash and equivalents of RM114.6 million making up 36.8 percent of total current assets.

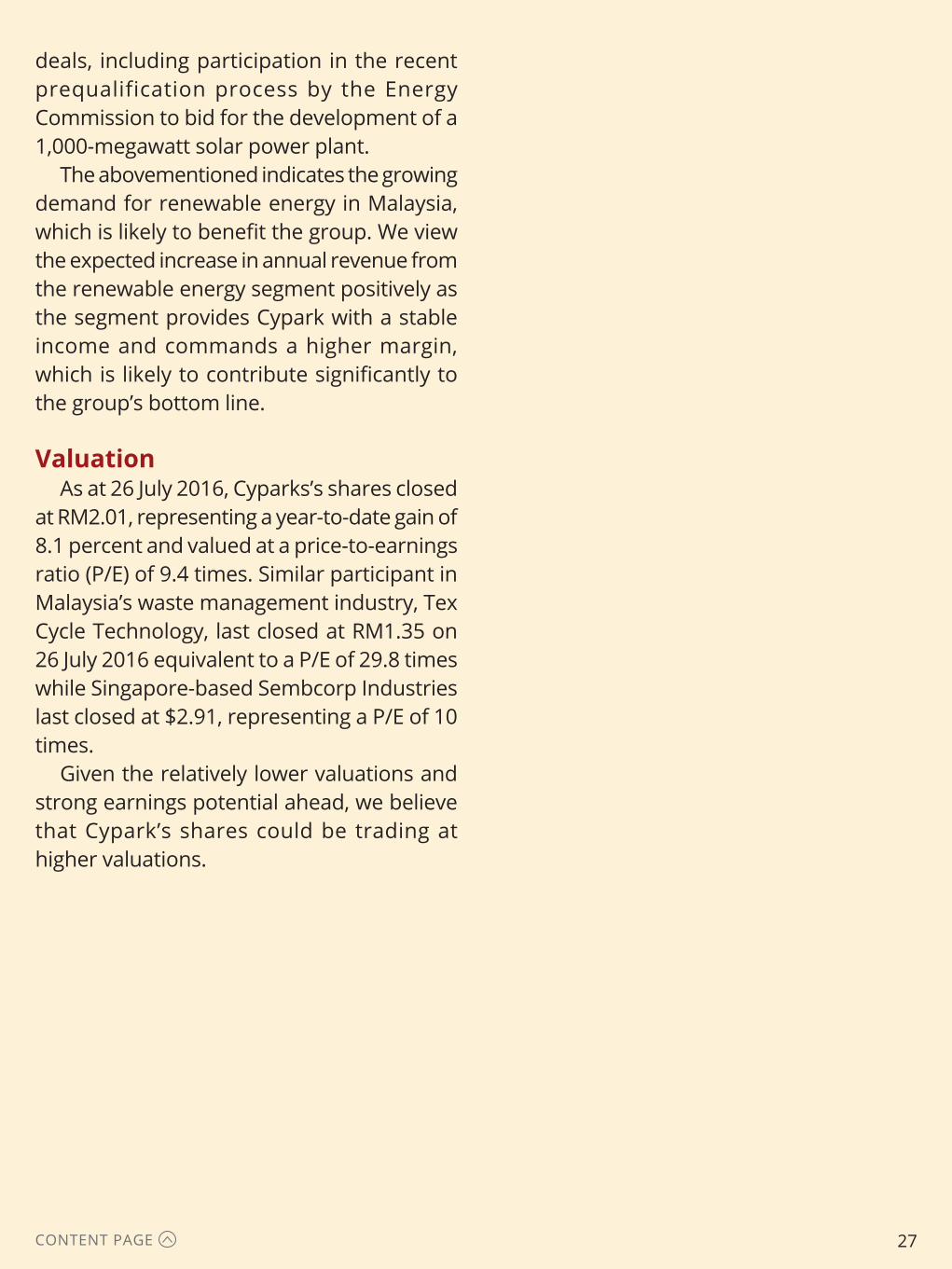

Growing Renewable Energy Segment to Generate RM150 Million by End-2017

Cypark expects the renewable energy segment to generate annual revenue of up to RM150 million by the end of next year and to contribute more than 60 percent of total revenue, largely supplemented by its Solid Waste Modular Advanced Recovery and Treatment Systems (SMART) waste-to-energy (WTE) project and other contracts.

In November last year, Cypark secured a 25-year concession to treat and dispose solid waste at a SMART WTE plant to be built in Ladang Tanah Merah, Negri Sembilan. Under the agreement, Cypark will be paid an agreed fee and also be generating revenue from sales of electricity for converting the waste to clean renewable energy.

During the group’s annual general meeting in April this year, chief executive officer Datuk Daud Ahmad said that Cypark has secured and signed other renewable energy

26

CONTENT PAGE

deals, including participation in the recent prequalification process by the Energy Commission to bid for the development of a 1,000-megawatt solar power plant.

The abovementioned indicates the growing demand for renewable energy in Malaysia, which is likely to benefit the group. We view the expected increase in annual revenue from the renewable energy segment positively as the segment provides Cypark with a stable income and commands a higher margin, which is likely to contribute significantly to the group’s bottom line.

ValuationAs at 26 July 2016, Cyparks’s shares closed

at RM2.01, representing a year-to-date gain of 8.1 percent and valued at a price-to-earnings ratio (P/E) of 9.4 times. Similar participant in Malaysia’s waste management industry, Tex Cycle Technology, last closed at RM1.35 on 26 July 2016 equivalent to a P/E of 29.8 times while Singapore-based Sembcorp Industries last closed at $2.91, representing a P/E of 10 times.

Given the relatively lower valuations and strong earnings potential ahead, we believe that Cypark’s shares could be trading at higher valuations.

27

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

BY: SUA XIU KAI

Dutch Lady Milk Industries (Dutch Lady) – a company no stranger to consumers – manufactures and distributes a wide range of dairy products, such as specialised powders for infant and children, liquid milk in different packaging formats and yoghurts.

The company has been offering its products to generations of Malaysians and Singaporeans under a wide range of brand names such as Dutch Lady, Dutch Baby, Frisolac, Frisco and Dutch Lady PureFarm.

With its 1Q16 financial results released in February 2016, we take a look at why this dairy giant may not just be healthy to your bones and teeth; it may prove valuable to portfolio as well.

Increasing Market Presence And ShareDespite its established market presence, Dutch Lady has

been active in heightening the awareness of the benefits of consuming dairy products. The firm has launched several initiatives targeted at children in cooperation with Malaysian government bodies.

Over the years, Dutch Lady has been working with the Malaysian Ministry of Education in the Program Susu 1Malaysia in order to spread the goodness and benefits of milk to school children. Through the programme, the group has provided milk to more than 238,000 selected school children from primary schools with a series of educational road shows. Through a specially designed project in 2014, Dutch Lady put forth its Drink.Move.BeStrong proposition that encourages school children to get proper nutrition and to lead a healthier

Why Dutch Lady Milk Industries Is Good For Your Bones And Portfolio

DLADY

3026

24.09%

DUTCH LADY MILK24.09%

KLCI-2.63%

28

CONTENT PAGE

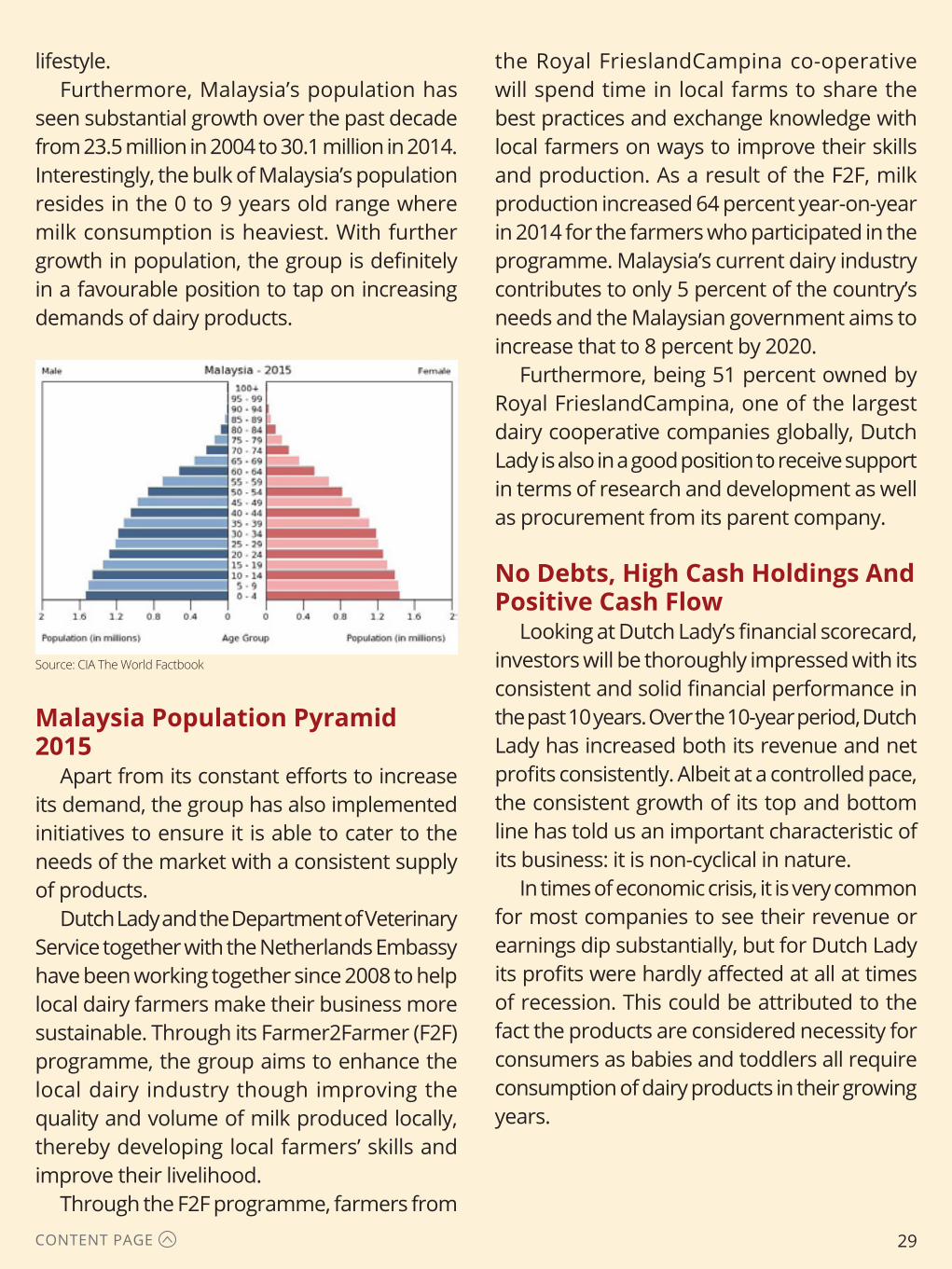

lifestyle.Furthermore, Malaysia’s population has

seen substantial growth over the past decade from 23.5 million in 2004 to 30.1 million in 2014. Interestingly, the bulk of Malaysia’s population resides in the 0 to 9 years old range where milk consumption is heaviest. With further growth in population, the group is definitely in a favourable position to tap on increasing demands of dairy products.

Source: CIA The World Factbook

Malaysia Population Pyramid 2015

Apart from its constant efforts to increase its demand, the group has also implemented initiatives to ensure it is able to cater to the needs of the market with a consistent supply of products.

Dutch Lady and the Department of Veterinary Service together with the Netherlands Embassy have been working together since 2008 to help local dairy farmers make their business more sustainable. Through its Farmer2Farmer (F2F) programme, the group aims to enhance the local dairy industry though improving the quality and volume of milk produced locally, thereby developing local farmers’ skills and improve their livelihood.

Through the F2F programme, farmers from

the Royal FrieslandCampina co-operative will spend time in local farms to share the best practices and exchange knowledge with local farmers on ways to improve their skills and production. As a result of the F2F, milk production increased 64 percent year-on-year in 2014 for the farmers who participated in the programme. Malaysia’s current dairy industry contributes to only 5 percent of the country’s needs and the Malaysian government aims to increase that to 8 percent by 2020.

Furthermore, being 51 percent owned by Royal FrieslandCampina, one of the largest dairy cooperative companies globally, Dutch Lady is also in a good position to receive support in terms of research and development as well as procurement from its parent company.

No Debts, High Cash Holdings And Positive Cash Flow

Looking at Dutch Lady’s financial scorecard, investors will be thoroughly impressed with its consistent and solid financial performance in the past 10 years. Over the 10-year period, Dutch Lady has increased both its revenue and net profits consistently. Albeit at a controlled pace, the consistent growth of its top and bottom line has told us an important characteristic of its business: it is non-cyclical in nature.

In times of economic crisis, it is very common for most companies to see their revenue or earnings dip substantially, but for Dutch Lady its profits were hardly affected at all at times of recession. This could be attributed to the fact the products are considered necessity for consumers as babies and toddlers all require consumption of dairy products in their growing years.

29

CONTENT PAGE

Revenue & Net Profits (RM ‘millions)

Source: Company

Looking at its balance sheet, Dutch Lady also has an exceptional ability to retain a substantial amount of cash holdings. From their 1Q16 results, Dutch Lady currently holds RM169.6 million in cash and equivalents and although it represents a mere 4.7 percent of its towering market capitalization of RM3.6 billion, it is definitely helps to provide some sort of buffer during crisis periods, given the fact that this behemoth of a company currently holds zero debt as well.

Moving down the checklist of things investors love, Dutch Lady also boasts 10 consecutive years of increasing operating cash flow and free cash flow. As of FY15, its operating cash flow stood at a record high of RM200.6 million, and with a capital expenditure of RM24.5 million, the group ended the year with a remarkable free cash flow of RM176.4 million.

Final TakeawayAs of 17 May’s close, Dutch Lady’s shares

closed at RM55.80; with an average street price of RM58.15 it represents an upside potential of approximately 4.2 percent.

Although investors may argue that growth for this giant may be slightly limited due to the lack of any short term catalyst, Dutch lady has proven itself with a resilient business model that is able to generate profits and cash even

during recessions, which is further cemented from its return on equity of 75.3 percent and return on asset of 31.2 percent.

Given its strong cash generation ability, as well as the more than sufficient residual cash even after setting aside the money required to maintain or expand its asset base, Dutch Lady has been paying out dividends consistently to shareholders. For FY15, the group distributed dividends of RM2.20 per share, inclusive of two RM0.60 special dividends, bringing the total amount distributed to RM140.8 million, representing a payout ratio of approximately 100 percent.

With a price of RM55.80 per share, Dutch Lady has a price to earnings ratio (P/E) of 22.6 times. In comparison, the consumer sector P/E is pegged at 25 times and its closest competitor, Nestle (Malaysia) trades at a P/E of 30.2 times. In short, Dutch Lady is an extremely stable company with strong fundamentals which would definitely suit the palette of investors who prefer less volatility and looking for steady investments.

30

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

BY: TAN JIA HUI

Piling and other foundation works form the basis of construction and property development projects, helping to provide the support needed for structures being built. Hence, as long as there are construction projects going on, it would create demand for piling and foundation services.

Founded in 1987 and listed in 2014, Econpile Holdings is a leading provider of piling and foundation services in Malaysia. The company provides a whole range of services including earthworks, substructure, and basement construction works and has been involved in the construction of bridges, highways, and buildings amongst others.

The group is the holder of a Grade 7 License from the Construction Industry Development Board of Malaysia, allowing it to tender for projects of unlimited values in the categories of building, and infrastructure works.

Strong Track Record – Delivered More Than RM2 Billion Worth of Projects

Econpile has a strong track record in the industry, having delivered more than RM2 billion worth of piling and services for numerous projects across Malaysia. The Klang Valley Mass Rapid Transit (KVMRT1), Port Dickson and Manjung power plants, as well as the Tanjong Agas Oil & Maritime Industrial Park, are some notable projects the firm has undertaken.

Leveraging on its expertise and experience, the group has the ability to handle projects of different complexities. Over the years, the company has also built

Why Construction Servicer Econpile Holdings Could Have A Possible 20% Upside

ECONBHD

5253

71.56%

ECONPILE71.56%

KLCI-2.63%

31

CONTENT PAGE

up good relationships with big names in the construction and property sector including Tropicana Corporation, IOI Properties, Glomac and Putrajaya Perdana.

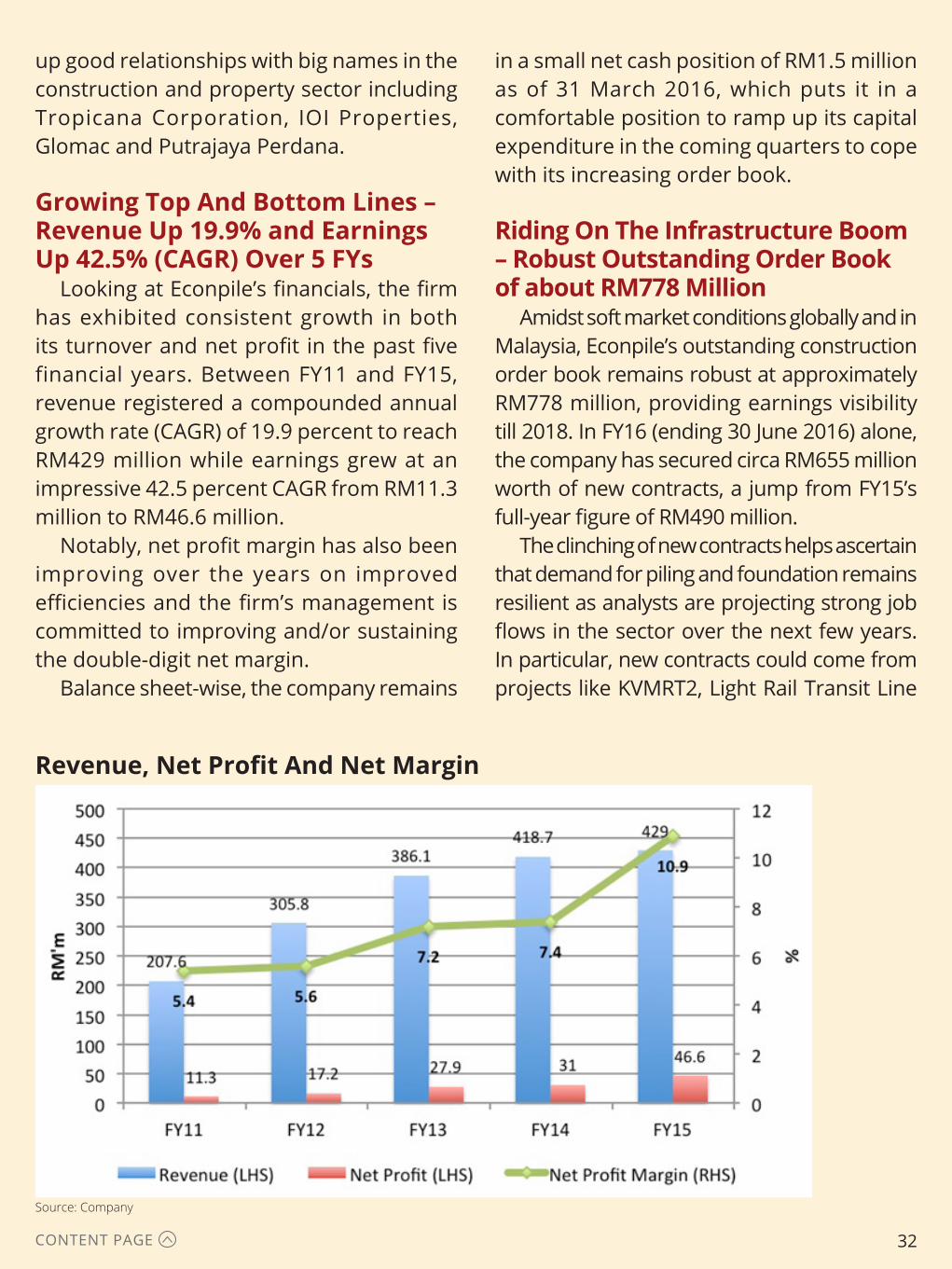

Growing Top And Bottom Lines – Revenue Up 19.9% and Earnings Up 42.5% (CAGR) Over 5 FYs

Looking at Econpile’s financials, the firm has exhibited consistent growth in both its turnover and net profit in the past five financial years. Between FY11 and FY15, revenue registered a compounded annual growth rate (CAGR) of 19.9 percent to reach RM429 million while earnings grew at an impressive 42.5 percent CAGR from RM11.3 million to RM46.6 million.

Notably, net profit margin has also been improving over the years on improved efficiencies and the firm’s management is committed to improving and/or sustaining the double-digit net margin.

Balance sheet-wise, the company remains

Source: Company

in a small net cash position of RM1.5 million as of 31 March 2016, which puts it in a comfortable position to ramp up its capital expenditure in the coming quarters to cope with its increasing order book.

Riding On The Infrastructure Boom – Robust Outstanding Order Book of about RM778 Million

Amidst soft market conditions globally and in Malaysia, Econpile’s outstanding construction order book remains robust at approximately RM778 million, providing earnings visibility till 2018. In FY16 (ending 30 June 2016) alone, the company has secured circa RM655 million worth of new contracts, a jump from FY15’s full-year figure of RM490 million.

The clinching of new contracts helps ascertain that demand for piling and foundation remains resilient as analysts are projecting strong job flows in the sector over the next few years. In particular, new contracts could come from projects like KVMRT2, Light Rail Transit Line

Revenue, Net Profit And Net Margin

32

CONTENT PAGE

Market Capitalisation*(RM’m) TTM Gross Margin TTM Net Margin TTM P/E

Ikhmas Jaya Grp 364.0 26.4% 8.6% 16.0x

Pintaras Jaya 564.2 20.8% 16.8% 23.5x

Econpile Hldgs 771.6 24.2% 14.4% 11.3x

Mean 566.6 23.8% 13.3% 16.9x*Based on close price as at 15 June 2016

3, expressways and the Bukit Bintang City Centre development. The group is in a good position to capture this rising demand, given its experience from KVMRT1 and expertise in executing projects that are over RM100 million in value.

ValuationsFor comparison, we look to Pintaras Jaya

and Ikhmas Jaya Group, listed peers of Econpile who are also mainly involved in the provision of piling and foundation services.

On a relative valuation basis, Econpile is trading at the lowest trailing twelve months (TTM) price-to-earnings ratio (P/E) of 11.3 times. We think the fact that the group has a much higher net margin but still trades at a lower P/E as compared to Ikhmas Jaya (who happens to have a net debt position) is not justified.

Analysts on the streets appear to concur that Econpile deserves a higher valuation than what it is currently trading at, with an average ‘Buy’ rating and a target price of RM1.64, which represents a 23.6 percent upside potential to the stock’s close price of RM1.33 as at 15 June. Risks to the street ratings include a lower than expected job flows, delay in projects and rise in raw material prices.

33

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

BY: SUA XIU KAI

191.3 percent. That is the growth in net profit for the past two years at Gadang Holdings (Gadang), a Malaysian-listed investment holdings company which provides earthwork, civil engineering, and construction projects as well as develops and invests in properties and manufactures ready-mix concrete.

Going back another two years to 2011, Gadang was actu-ally a loss making company with a net loss of RM4.4 million reported for FY11. With a net profit of RM59.6 million reported for FY15, it represents an impressive 4-year compounded an-nual growth rate (CAGR) of 42.52 percent.

Although turnarounds for loss making companies are not exactly uncommon in the market, it is not everyday that we see such a remarkable comeback in such a short period of time.

Property Division’s Revenue Grew 27.1% While Profit Before Tax Grew 23.4%

Gadang’s main business can be broken down into five main categories, namely: 1) Construction Division; 2) Property Division; 3) Utility Division; and 4) Plantation Division.

The biggest contributions to its revenue come from its Con-struction Division and Property Division, which contributed 76.6

This Malaysian Conglomerate’s Share Price Surged 65% In A Year

Year Ended 31 May 2015RM’000

2014RM’000

2013RM’000

2012RM’000

2011RM’000

RevenueConstruction Division 449,662 442,193 265,665 189,127 299,836Property Division 119,721 87,034 73,516 40,890 35,950Utility Division 16,682 14,780 17,151 16,331 14,692Plantation Division 1,333 939 134 - -Investment Holding & Others - - - - 9

587,398 544,946 356,466 246,348 350,487Segmented Revenue Breakdown, Source: Company.

GADANG

9261

34.43%

GADANG HOLDINGS34.43%

KLCI-2.63%

34

CONTENT PAGE

percent and 20.4 percent respectively for FY15.Historically, the two divisions have consistent-

ly contributed to the bulk of Gadang’s revenue and have experienced the most growth, with a 5-year revenue CAGR of 8.44 percent for Con-struction and 27.2 percent for Property.

In its recent release of its 3Q16 financial results, its construction segment reported RM122.7million in revenue and profit before tax of RM22 million, which represented a 70.2-per-cent jump quarter-on-quarter given the lower base last quarter and better construction prog-ress in 3Q16.

For its property division, it recording a rev-enue of RM47.4 million and RM13.3 million of profit before tax for 3Q16, a 98.1 percent and 133.9 percent surge quarter-on-quarter respec-tively in view of the low base in 2Q16.

Gadang has shared that the property divi-sion’s earnings will be underpinned by its un-billed sales of some RM189 million as at end of FY15, located at several strategic locations, namely the Vyne project in Salak South

From the cumulative perspective for 9M16, property division’s revenue achieved growth of 27.1 percent and 23.4 percent in profit before tax year-on-year respectively.

Ongoing RM800 Million Order Book; Profit Before Tax In Utility Division Surged 60.3%

In its construction division, the group has shared with media that it has tendered for over RM10 billion worth of projects, mainly for Petronas’ Refinery and Petrochemical Integrated Development (RAPID), Package V2 of Klang Val-ley Mass Rapid Transit (KVMRT2), as well as the proposed Damansara-Shah Alam (DASH) and Sungai Besi-Ulu Kelang (SUKE) elevated express-way projects.

Given its experience in both KVMRT1 and

RAPID projects, it is highly probable that Gadang can further replenish its order book.

Moreover, the group currently has a balance of construction jobs worth RM800 million which are ongoing. Although management has not elaborated on its margins, the group stated that its construction industry division will be kept busy at least for the new couple of years, with job glows coming in.

Another segment which cannot be missed is its utility segment. Although its performance in revenue received over the past five years has fluctuated, the utility division is expected to pro-duce steady earnings moving forward.

In 3Q16, the utility division contributed RM5.5 million to the top line, same as previous quarters, whereas profit before tax surged 60.3 percent to RM1.6 million, attributed to PT Dewata Ban-gun Tirta, a water supplier and water treatment services provider based in Indonesia.

In time to come, the utility segment is expect-ed to continue contributing steady earnings to Gadang before the construction of the 9 mega-watt mini-hydro power concession PT Ikhwan to be completed mid 2019. Upon full commission-ing, it is expected to contribute positively to the utility division.

Valuation: 2.1% Yield; Payout Ratio 20%; P/E Ratio 6.04

Gadang’s share price closed at RM2.37 on 20 July 2016, and with total dividends of five sen per share for FY15, it represents a dividend yield of 2.1 percent and payout ratio of 20 percent.

Although its dividend yield is nothing to shout about, and despite the fact that it has been on a 65 percent rally for the past year, we are op-timistic on its future earnings outlook. And at a price-to-earning (PE) ratio of 6.04, Gadang most certainly is at an undervalued position on track to achieve another good year for FY16.

35

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

BY: TAN JIA HUI

With the widespread of e-commerce today, people can purchase groceries, clothes or even vehicles with just a click of the mouse. Consumers are increasingly turning to making purchases online, given the convenience, variety and value.

While companies like Amazon and Alibaba are at the forefront, logistics and delivery services providers who have benefitted from the rise of e-commerce also play an important role in the value chain.

Here on the little red dot, national postal service provider Singapore Post (SingPost) is one of the first choices for investors when it comes to riding the e-commerce wave.

However, we cast our sights further this time round to across the causeway and see GD Express Carrier (GDEX) standing out as a good proxy to Malaysia’s e-commerce growth.

Below are three things that you need to know about this counter.

1. Net Profit Quadrupled from RM7 Million to RM28.3 Million Over 5 Years

GDEX is an express delivery and logistics solution provider that operates predominantly in Malaysia and Singapore.

The express delivery segment is the group’s largest revenue contributor, making up 95 percent of FY15 turnover.

The rising popularity of e-commerce, as well as the increasing trend of outsourcing of inter-company parcel deliveries has benefitted the company.

3 Things To Know About GD Express Carrier – Proxy To Malaysia’s E-Commerce Growth

GDEX

0078

-0.58%

GD EXPRESS CARRIER-0.58%

KLCI-2.63%

36

CONTENT PAGE

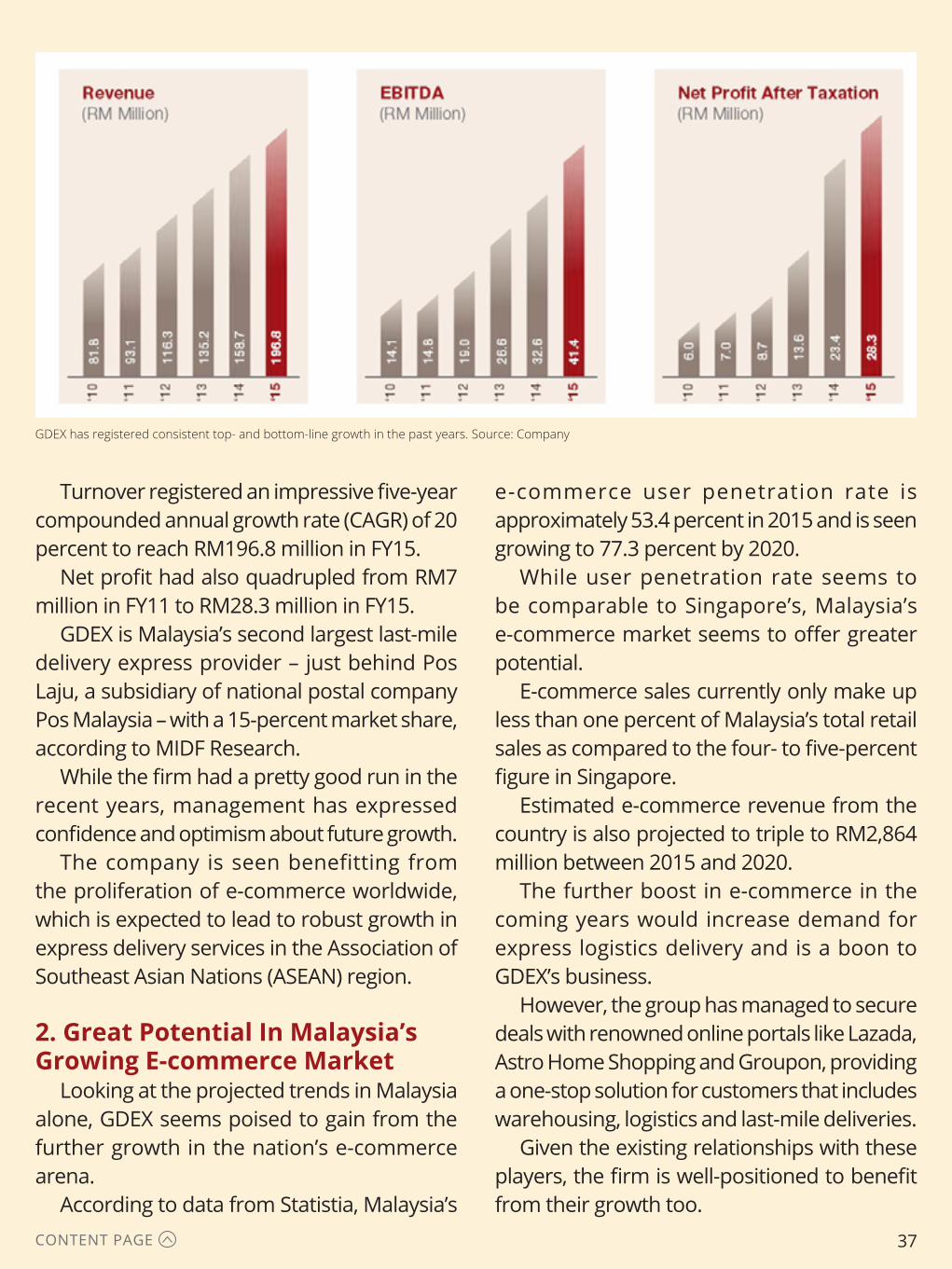

Turnover registered an impressive five-year compounded annual growth rate (CAGR) of 20 percent to reach RM196.8 million in FY15.

Net profit had also quadrupled from RM7 million in FY11 to RM28.3 million in FY15.

GDEX is Malaysia’s second largest last-mile delivery express provider – just behind Pos Laju, a subsidiary of national postal company Pos Malaysia – with a 15-percent market share, according to MIDF Research.

While the firm had a pretty good run in the recent years, management has expressed confidence and optimism about future growth.

The company is seen benefitting from the proliferation of e-commerce worldwide, which is expected to lead to robust growth in express delivery services in the Association of Southeast Asian Nations (ASEAN) region.

2. Great Potential In Malaysia’s Growing E-commerce Market

Looking at the projected trends in Malaysia alone, GDEX seems poised to gain from the further growth in the nation’s e-commerce arena.

According to data from Statistia, Malaysia’s

e-commerce user penetration rate is approximately 53.4 percent in 2015 and is seen growing to 77.3 percent by 2020.

While user penetration rate seems to be comparable to Singapore’s, Malaysia’s e-commerce market seems to offer greater potential.

E-commerce sales currently only make up less than one percent of Malaysia’s total retail sales as compared to the four- to five-percent figure in Singapore.

Estimated e-commerce revenue from the country is also projected to triple to RM2,864 million between 2015 and 2020.

The further boost in e-commerce in the coming years would increase demand for express logistics delivery and is a boon to GDEX’s business.

However, the group has managed to secure deals with renowned online portals like Lazada, Astro Home Shopping and Groupon, providing a one-stop solution for customers that includes warehousing, logistics and last-mile deliveries.

Given the existing relationships with these players, the firm is well-positioned to benefit from their growth too.

GDEX has registered consistent top- and bottom-line growth in the past years. Source: Company

37

CONTENT PAGE

3. Strategic Partnerships With Other Industry Players

Over the years, the company has established partnerships with other international courier players including UPS, FedEx, SingPost, SF Express and TNT.

These tie-ups are beneficial to the firm as apart from providing last-mile delivery services for its partners, the firm also benefits from leveraging on them to provide international delivery services for its own clients.

Notably, SingPost has been one of the largest shareholders of GDEX since 2011 and currently holds an 11.2 percent stake in the latter (after a recent sale of part of its stake).

At the start of 2016, Yamato Holdings – Japan’s top parcel delivery company – took a direct stake in the group, buying up a total 22.8 percent stake in GDEX.

The two parties will have a tie-up on their line haul businesses between major centres to further improve efficiencies and also collaborate to leverage on the opportunities in the growing ASEAN region.

Yamato’s entry as a shareholder is a boost to GDEX’s status as it can be seen as validation of the group’s service level and ability to integrate with other players to extract possible synergies.

ValuationGiven the expectations that growth would

be high at GDEX in the next few years as it rides on the burgeoning e-commerce market in Malaysia and other ASEAN countries, the firm’s stock valuations are rather lofty at the moment.

Based on the close price of RM1.53 as at 27 May, the company’s shares are trading at a trailing twelve-month price-to-earnings ratio (P/E) of 62.2 times, even after share price corrected 15 percent from a high of RM1.80.

In comparison, the group’s Malaysia-listed peer Pos Malaysia trades at 22.6 times P/E while Singapore-listed SingPost has a P/E of 14.6 times.

It is worth pointing out though that Yamato’s acquisition of GDEX shares in early 2016 works out to approximately RM1.68 per share at an even higher valuation of close to 68.3 times P/E.

However, from the former’s perspective, the purchase could be part of a strategic move to gain access to the region and hence the willingness to pay a higher price.

For the average investors though, while GDEX serves as a good proxy to Malaysia’s and the region’s growing e-commerce market, expectations of growth are high as reflected by the share price, something investors have to consider carefully before jumping on the bandwagon.

38

Stock Short Name:

Code:

YTD Return (as at 3 Nov):

Year-To-Date Gains

In 2015, we saw the gaming sector revealing a string of disappointments in results releases.

However, with players have got various expansion plans that will only contribute to earnings in the next few years, will we see optimism in the sea of gloominess for the sector?

Genting Berhad (Genting) saw its share price tumbling from a high of RM9.30 a share on 9 April 2015 to a low of RM6.60 per share on 24 August 2015. This represented a 29 percent fall in less than 6 months.

As of 19 January 2016, Genting seems to be trading in a consolidation region, with prices trading within a contained band between RM7 to RM7.50.

Inconsistent Earnings From Overseas Operations’ Drag