uncertainty - ucsb department of...

TRANSCRIPT

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Uncertainty

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Table of Contents

1 Choice Under UncertaintyBudget ConstraintPreferences

2 InsuranceChoice FrameworkExpected Utility Theory

3 Diversification & Risk Sharing

4 AIG

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

States of Nature and Contingent Plans

States of Nature:

“fire destroys house” (f) vs. “no fire” (nf)Probability of: fire = πf , no fire = πnf ; πf + πnf = 1Fire causes loss of $L

Contingent Plan:

A state-contingent consumption plan: consumptionlevel/bundle is different in each state (e.g. vacation only if nofire)Contracts may be state-contingent (e.g. insurer pays only ifthere is a fire)

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

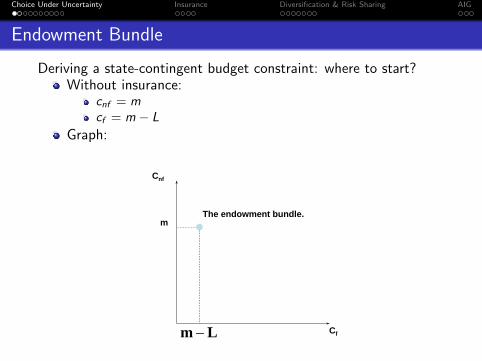

Endowment Bundle

Deriving a state-contingent budget constraint: where to start?Without insurance:

cnf = mcf = m − L

Graph:

Cnf

Cf

mThe endowment bundle.

m L−

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Budget Constraint

Buy $K of fire insurance at price p.

cnf = m − pKcf = m − L− pK + K = m − L + (1− p)KSolve for K , substitute:

cnf =m − pL

1− p− p

1− pcf

Cnf

Cf

mThe endowment bundle.

ppLm −m L−

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Preferences

We face a risky gamble

U(cf , cnf ) captures attitude towards uncertainty/risk

Risk averse vs. risk neutral

Consider our three favorite examples:

A Perfect SubstitutesB Cobb-DouglasC Perfect ComplementsD Not sureE Don’t have clicker yet

CLICKER VOTE: which reflects extreme risk aversion?

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Optimal Choice (Graph)

Some insurance (+ or -) is preferred

Cnf

Cf

m

optimal affordable plan

ppLm −m L−

Comparative statics:

risk aversion ↑=⇒ K?p ↑=⇒ K ↓L ↑=⇒ K?

What about algebraic solution? But first. . .

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Expected Utility

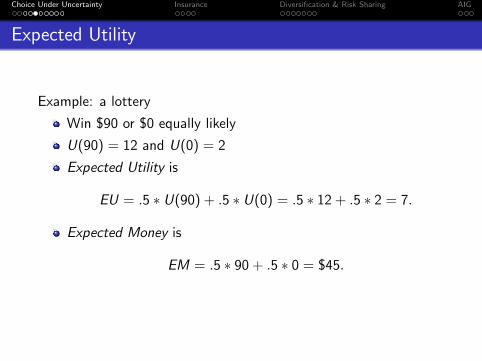

Example: a lottery

Win $90 or $0 equally likely

U(90) = 12 and U(0) = 2

Expected Utility is

EU = .5 ∗ U(90) + .5 ∗ U(0) = .5 ∗ 12 + .5 ∗ 2 = 7.

Expected Money is

EM = .5 ∗ 90 + .5 ∗ 0 = $45.

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

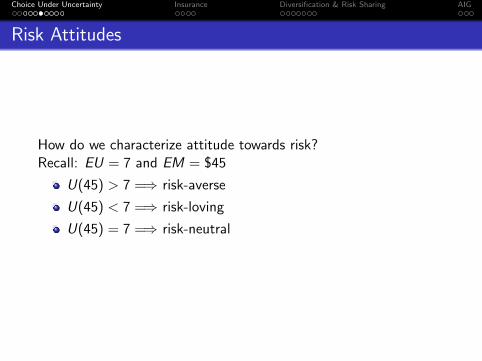

Risk Attitudes

How do we characterize attitude towards risk?Recall: EU = 7 and EM = $45

U(45) > 7 =⇒ risk-averse

U(45) < 7 =⇒ risk-loving

U(45) = 7 =⇒ risk-neutral

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Risk Attitudes

We typically assume diminishing marginal utility (DMU) of wealth.

Wealth$0 $90

2

12

$45

EU=7

So EU < U(EM). . .

this implies risk aversion!

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

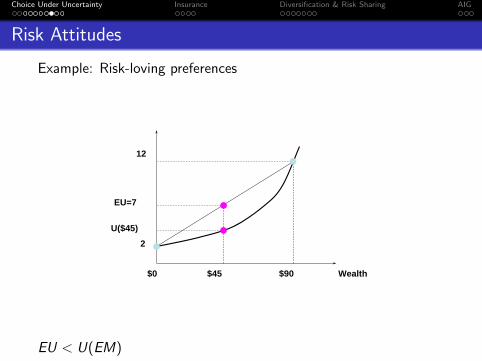

Risk Attitudes

Example: Risk-loving preferences

Wealth$0 $90

12

2

EU=7

$45

U($45)

EU < U(EM)

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Risk Attitudes

Example: Risk-neutral preferences

Wealth$0 $90

12

2

$45

U($45)=EU=7

EU = U(EM)

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Optimal Choice (Algebra)

Calculating the MRS

EU = πf U(cf ) + πnf U(cnf )

Indifference curve =⇒ constant EU

Differentiate:

dEU = 0 = πf MU(cf )dcf + πnf MU(cnf )dcnf

MRS = dcnf

dcf= − πf MU(cf )

πnf MU(cnf )

Solution satisfies

p

1− p=

πf MU(cf )

πnf MU(cnf ).

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Competitive Insurance

Free entry =⇒ zero expected economic profit

So pK − πf K − (1− πf )0 = (p − πf )K = 0.

=⇒ p = πf

Insurance is fair

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Competitive Insurance

With fair insurance, rational choice satisfies

πf

πnf=

πf

1− πf=

p

1− p=

πf MU(cf )

πnf MU(cnf ).

In other words, MU(cf ) = MU(cnf )

Risk-aversion =⇒ cf = cnf

Full insurance!

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

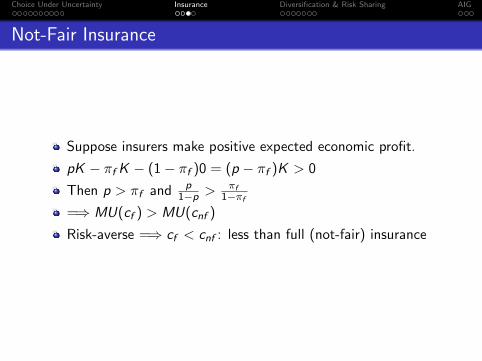

Not-Fair Insurance

Suppose insurers make positive expected economic profit.

pK − πf K − (1− πf )0 = (p − πf )K > 0

Then p > πf and p1−p >

πf1−πf

=⇒ MU(cf ) > MU(cnf )

Risk-averse =⇒ cf < cnf : less than full (not-fair) insurance

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Demand for Insurance: EU Perspective

Certainty Equivalent = dollar amount you would need to havewith certainty to make you indifferent to the gambleU(CE ) = EUEM − CE = willingness to pay for full-insurance (length of redline)

Wealth$0 $90

2

12

$45

EU=7=U(CE)

CE

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Proposed Gamble

I flip a fair coin. Heads: I pay you $120; tails: you pay me $100.Any takers?

CLICKER VOTE:

A Accept

B No thank you!

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Proposed Gamble: II

What if I offered this same gamble at the beginning of every lecture(and you had to tell me today what you would choose each time)?

CLICKER VOTE:

A Accept every time

B Reject every time

C Some combination

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Analysis

Why is the same gamble more attractive when it is repeated?

Each gamble has positive expected value

Each coin toss is independent

Law of Large Numbers: expected money from compoundgamble = N times the EM = a big positive number

Portfolio of gambles is diverse, so very little chance of net loss

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Diversification

Example:

Two firms, A and B. Shares cost $10

With prob = .5, ΠA = 100 and ΠB = 20

With prob = .5, ΠA = 20 and ΠB = 100

You have $100 to invest. How?

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Diversification

Example:

Buy only firm A’s stock?

$100/10 = 10 shares

Earn $1000 w/ prob .5 and $200 w/ prob .5

Expected earning: $500 + $100 = $600

Same for buying only B

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Diversification

Example:

Buy 5 shares of each firm?

Earn $600 for sure

Diversification has maintained expected earnings whilelowering risk

Typically there’s a tradeoff between earnings and risk

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

Recap

What are rational responses to risk?

Buying insurance

A diverse portfolio of contingent consumption goods (assets)

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

AIG: WTF?

How does this help us understand what big insurance/financialcompanies like AIG are supposed to do?

You buy insurance in response to risk

Insurance company gets your premium, but now faces risk ofhaving to pay claim

To the extent that claims are independent, this is ok for thembecause they have a diverse portfolio of risks

Same w/ home lenders: they get your mortgage payments,but lose if you default

To diversify risk, lenders wad mortgages together into bundles,then sell them (in pieces) as relatively safe (diversified)securities

Thus, our risk and insurance courses through the veins of thefinancial system

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

AIG: WTF?

So what can and did go wrong?

Diversification works if risks are independent, but not ifcorrelated.

My proposed gamble: imagine if I decided outcome w/ onecoin-toss at the end of the quarter. Taker?

Risk of house burning down: Seattle vs. SoCal

Wildfires, earthquakes, hurricanes can wipe out entirecities/regions at once

Natural disasters are disasters for insurers

Insurers know this: there is an enormous re-insurance industry

Choice Under Uncertainty Insurance Diversification & Risk Sharing AIG

AIG: WTF?

So what can and did go wrong?

Lenders/financiers were not prepared for the collapse of thehousing bubble

Housing crisis =⇒ financial crisis =⇒ credit crisis =⇒ baaadrecession