uncertainty is the “new normal” deloitte m&a index m&a · uncertainty is the “new...

TRANSCRIPT

Uncertainty is the “new normal”Deloitte M&A IndexOutlook for 2017 M&A

Uncertainty is the “new normal” 01

Slowdown in global trade is mirrored by growth of the digital economy 04

Economy of expectations 05

Contents

"Once uncertainties subside, M&A tends to pick up rapidly."

Uncertainty is the “new normal”

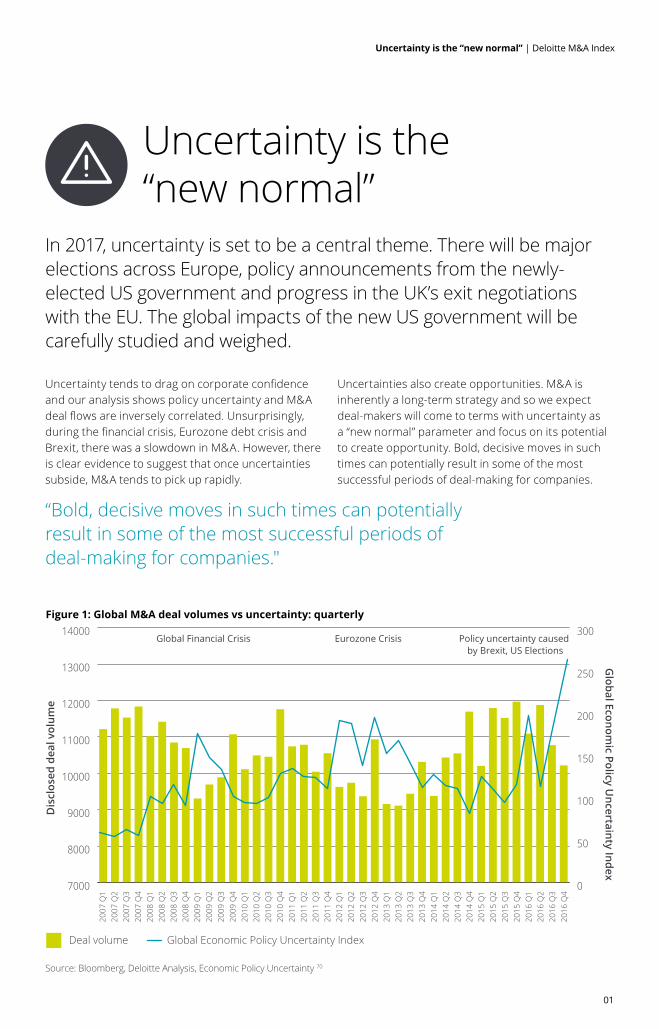

In 2017, uncertainty is set to be a central theme. There will be major elections across Europe, policy announcements from the newly-elected US government and progress in the UK’s exit negotiations with the EU. The global impacts of the new US government will be carefully studied and weighed.

“Bold, decisive moves in such times can potentially result in some of the most successful periods of deal-making for companies."

Deal volume Global Economic Policy Uncertainty Index

Global Financial Crisis Eurozone Crisis Policy uncertainty caused by Brexit, US Elections

Global Econom

ic Policy Uncertainty Index

Dis

clos

ed d

eal v

olum

e

7000

8000

9000

10000

11000

12000

13000

14000

0

50

100

150

200

250

300Figure 1: Global M&A deal volumes vs uncertainty: quarterly

2007

Q1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

Source: Bloomberg, Deloitte Analysis, Economic Policy Uncertainty 70

Uncertainty tends to drag on corporate confidence and our analysis shows policy uncertainty and M&A deal flows are inversely correlated. Unsurprisingly, during the financial crisis, Eurozone debt crisis and Brexit, there was a slowdown in M&A. However, there is clear evidence to suggest that once uncertainties subside, M&A tends to pick up rapidly.

Uncertainties also create opportunities. M&A is inherently a long-term strategy and so we expect deal-makers will come to terms with uncertainty as a “new normal” parameter and focus on its potential to create opportunity. Bold, decisive moves in such times can potentially result in some of the most successful periods of deal-making for companies.

01

Uncertainty is the “new normal” | Deloitte M&A Index

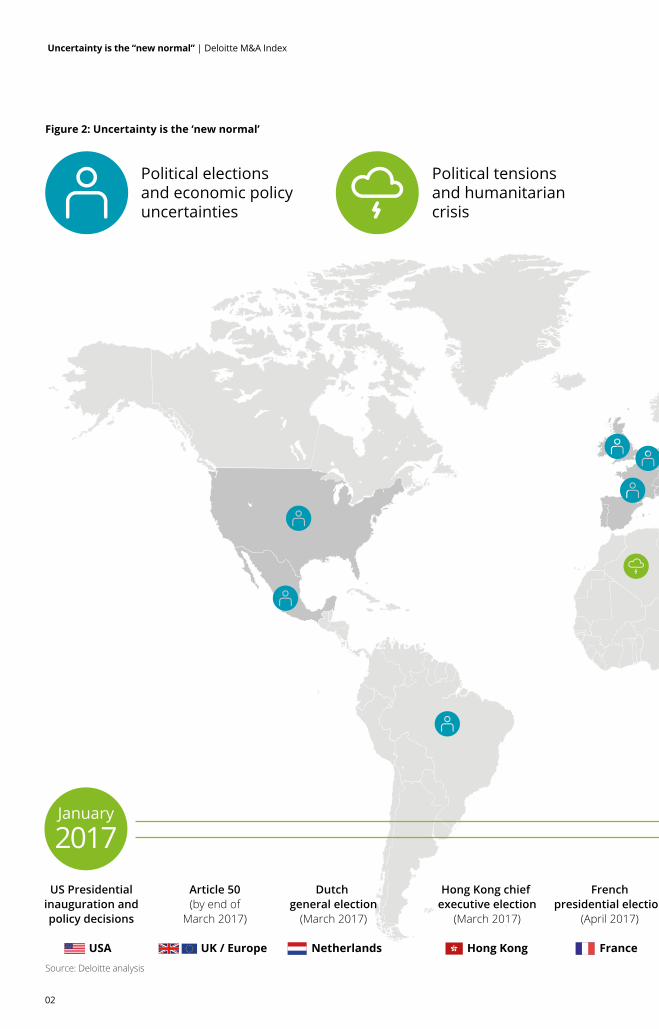

Political elections and economic policy uncertainties

Political tensions and humanitarian crisis

January

2017 May

2018US Presidential

inauguration andpolicy decisions

USA

Article 50(by end of

March 2017)

UK / Europe

Dutch general election

(March 2017)

Netherlands

Hong Kong chief executive election

(March 2017)

Hong Kong

Frenchpresidential election

(April 2017)

France

German federal election

(Oct 2017)

Germany

South Korean presidential election

(Dec 2017)

South Korea

Hungarian parliamentary election

(before Spring 2018)

Hungary

Italiangeneral election(before May 2018)

Italy

Figure 2: Uncertainty is the ‘new normal’

Figure 2: YTD (3Q) comparisons

Source: Deloitte analysis

02

Uncertainty is the “new normal” | Deloitte M&A Index

Political elections and economic policy uncertainties

Political tensions and humanitarian crisis

January

2017 May

2018US Presidential

inauguration andpolicy decisions

USA

Article 50(by end of

March 2017)

UK / Europe

Dutch general election

(March 2017)

Netherlands

Hong Kong chief executive election

(March 2017)

Hong Kong

Frenchpresidential election

(April 2017)

France

German federal election

(Oct 2017)

Germany

South Korean presidential election

(Dec 2017)

South Korea

Hungarian parliamentary election

(before Spring 2018)

Hungary

Italiangeneral election(before May 2018)

Italy

Figure 2: Uncertainty is the ‘new normal’ “Uncertainty is an uncomfortable position. But certainty is an absurd one.” Voltaire

03

Uncertainty is the “new normal” | Deloitte M&A Index

UK Industrial Products M&A Survey and Outlook | May you live in interesting times

Slowdown in global trade is mirrored by growth of the digital economy

Uncertainty is the “new normal” | Deloitte M&A Index

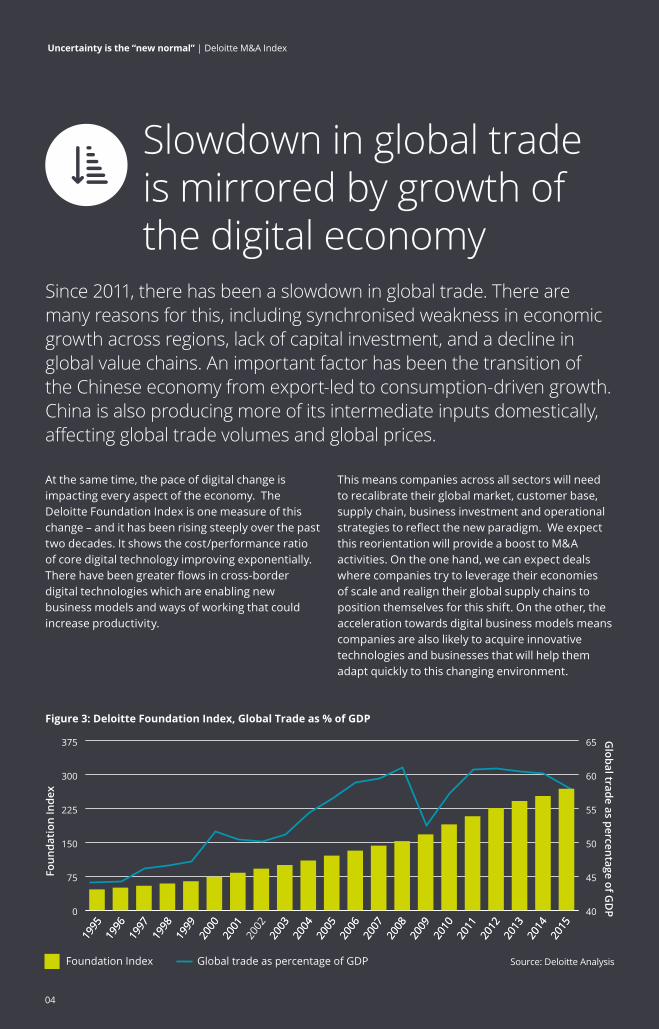

Since 2011, there has been a slowdown in global trade. There are many reasons for this, including synchronised weakness in economic growth across regions, lack of capital investment, and a decline in global value chains. An important factor has been the transition of the Chinese economy from export-led to consumption-driven growth. China is also producing more of its intermediate inputs domestically, affecting global trade volumes and global prices.

At the same time, the pace of digital change is impacting every aspect of the economy. The Deloitte Foundation Index is one measure of this change – and it has been rising steeply over the past two decades. It shows the cost/performance ratio of core digital technology improving exponentially. There have been greater flows in cross-border digital technologies which are enabling new business models and ways of working that could increase productivity.

This means companies across all sectors will need to recalibrate their global market, customer base, supply chain, business investment and operational strategies to reflect the new paradigm. We expect this reorientation will provide a boost to M&A activities. On the one hand, we can expect deals where companies try to leverage their economies of scale and realign their global supply chains to position themselves for this shift. On the other, the acceleration towards digital business models means companies are also likely to acquire innovative technologies and businesses that will help them adapt quickly to this changing environment.

40

45

50

55

60

65

1995

1996

1997

1998

1999

2000

2001

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Figure 3: Deloitte Foundation Index, Global Trade as % of GDP

Global trade as percentage of G

DP

Foun

dati

on In

dex

Foundation Index Global trade as percentage of GDP

0

75

150

225

300

375

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Source: Deloitte Analysis

04

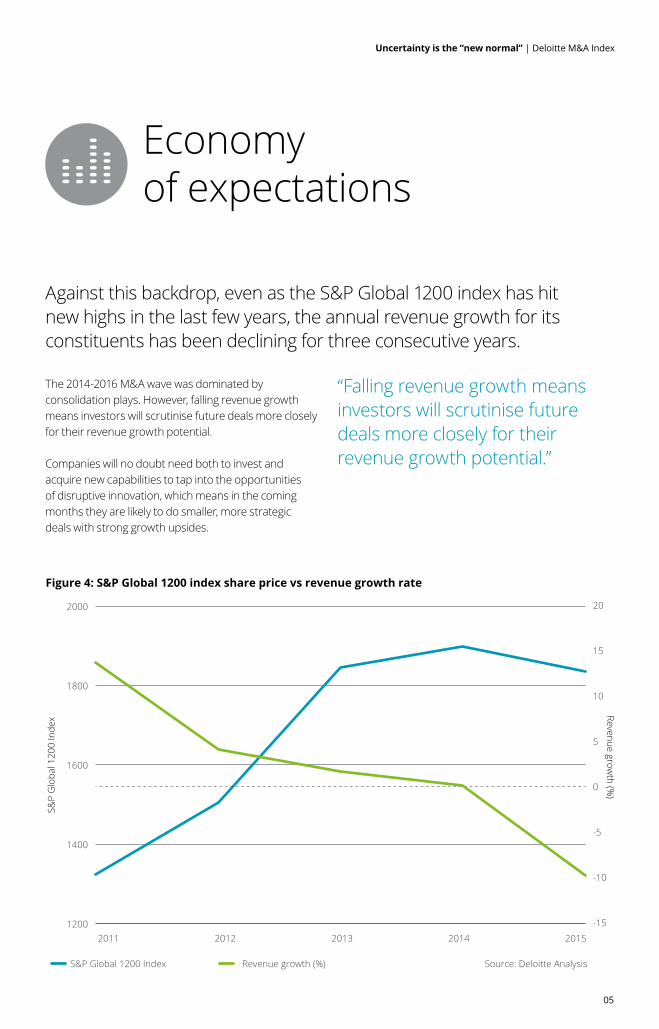

Against this backdrop, even as the S&P Global 1200 index has hit new highs in the last few years, the annual revenue growth for its constituents has been declining for three consecutive years.

Economy of expectations

The 2014-2016 M&A wave was dominated by consolidation plays. However, falling revenue growth means investors will scrutinise future deals more closely for their revenue growth potential.

Companies will no doubt need both to invest and acquire new capabilities to tap into the opportunities of disruptive innovation, which means in the coming months they are likely to do smaller, more strategic deals with strong growth upsides.

“Falling revenue growth means investors will scrutinise future deals more closely for their revenue growth potential.”

1200

1400

1600

1800

2000

2011 2012 2013 2014

S&P Global 1200 Index

2015

Revenue growth (%) Source: Deloitte Analysis

Revenue growth (%

)

Figure 4: S&P Global 1200 index share price vs revenue growth rate

-15

-10

-5

0

5

10

20

15

S&P

Glo

bal 1

200

Inde

x

05

Uncertainty is the “new normal” | Deloitte M&A Index

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Deloitte LLP is the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

© 2017 Deloitte LLP. All rights reserved.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street Square, London EC4A 3BZ, United Kingdom. Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198.

Designed and produced by The Creative Studio at Deloitte, London. J10516

Iain Macmillan Managing Director – Global M&A Services

+44 (0)20 7007 2975 [email protected]

Sriram Prakash Global Lead, M&A Insights

+44 (0) 20 7303 3155 [email protected]

Contacts