u,me~'nlo assistance programme - world...

TRANSCRIPT

u,me~'nlo Assistance Programme

.. . C

.0 . f - -. -. f .. . - - E.

- - . . v.- - *No. U320 NA

. ... OF'wM |ec'

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

JOINT UNDP / WORLD BANKENERGY SECTOR MANAGEMENT ASSISTANCE PROGRAMME (ESMAP)

PURPOSE

The Joint UNDP/World Bank Energy Sector Management Assistance Programme (ESMAP) waslaunched in 1983 to complement the Energy Assessment Programme, established three yearsearlier. ESMAP's original purpose was to implement key recommendations of the EnergyAssessment reports and ensure that proposed investments in the energy sector represented the mostefficient use of scarce domestic and external resources. In 1990, an international Commissionaddressed ESMAP's role for the 1990s and, noting the vital role of adequate and affordable energyin economic growth, concluded that the Programme should intensify its efforts to assist developingcountries to manage their energy sectors more effectively. The Commission also recommendedthat ESMAP concentrate on making long-term efforts in a smaller number of countries. TheCommission's report was endorsed at ESMAP's November 1990 Annual Meeting and promptedan extensive reorganization and reorientation of the Programme. Today, ESMAP is conductingEnergy Assessments, performing preinvestment and prefeasibility work, and providing institutionaland policy advice in selected developing countries. Through these efforts, ESMAP aims to assistgovernments, donors, and potential investors in identifying, funding, and implementingeconomically and environmentally sound energy strategies.

GOVERNANCE AND OPERATIONS

ESMAP is governed by a Consultative Group (ESMAP CG), composed of representatives of theUNDP and World Bank, the governments and institutions providing financial support, andrepresentatives of the recipients of ESMAP's assistance. The ESMAP CG is chaired by the WorldBank's Vice President, Finance and Private Sector Development, and advised by a TechnicalAdvisory Group (TAG) of independent energy experts that reviews the Programme's strategicagenda, its work program, and other issues. ESMAP is staffed by a cadre of engineers, energyplanners and economists from the Industry and Energy Department of the World Bank. TheDirector of this Department is also the Manager of ESMAP, responsible for administering theProgramme.

FUNDING

ESMAP is a cooperative effort supported by the World Bank, UNDP and other United Nationsagencies, the European Community, Organization of American States (OAS), Latin AmericanEnergy Organization (OLADE), and countries including Australia, Belgium, Canada, Denmark,Germany, Finland, France, Iceland, Ireland, Italy, Japan, the Netherlands, New Zealand, Norway,Portugal, Sweden, Switzerland, the United Kingdom, and the United States.

FURTHER INFORMATION

For further information or copies of completed ESMAP reports, contact:

ESMAPc/o Industry and Energy Department

The World Bank1818 H Street N.W.

Washington, D.C. 20433U.S.A.

For Official Use

Report No. 11320-NAM

NAMIBIA

Issues and Options in the Energy Sector

March 1993

ESMAPc/o Industry and Energy DepartmentThe World Bank1818 H Street NWWashington D.C. 20433USA

ABSTRACT

Namibia is fortunate in that the energy sector is not a constraint on growth,as it is in so many developing countries. Indeed, through the exploitation of Namibia'shydroelectric and/or hydrocarbon resources for export, the sector may well become amajor engine of growth. At present, industry, commerce and the country's populationcenters are adequately supplied with commercial energy (electricity and petroleumproducts) at realistic prices. However, many households lack access to modem energysupplies and, especially in rural areas, still rely on wood and other traditional fuels.While fuelwood is increasingly difficult to come by in some areas, there are few signs ofresulting hardship, or that fuelwood cutting is contributing significantly to deforestation.

While the present strengths and resource potential of the energy sectorgive good grounds for optimism about its future development, much will depend on howeffectively the policy, investment and institutional issues that are the focus of this reportare addressed. Critical decisions will soon have to be made concerning the Epupahydroelectric project and the Kudu offshore gas field, as well as such issues as ruralelectrification and the least cost means of meeting future domestic power needs. Inaddition, the growing size and complexity of the sector will inevitably call for a moresystematic and sophisticated approach to regulation. On the petroleum side there is aneed to consider the possible dismantling of the present system of domestic priceregulation while, in the virtually unregulaed power sector, a whole new regulatory systemneeds to be devised and put in place. High priority also should be given to therestructuring of the institutionally fragmented and inefficient electricity distributionsystem.

Currency Equivalents

June, 1992

1 Rand = 0.36 US$1 US$ = 2.75 Rand

Abbreviations

MLGH Ministry of Local Governmentand Housing

MME Ministry of Mines and EnergyNISER Namibian Institute for Social and

Economic ResearchNAMCOR National Petroleum Corporation of

NamibiaR/Rc Rand/Rand centsRSA Republic of South AfricaSWAWEK South West Africa Water and

Electricity Corporation

Measurements

GWh gigawatt hourkg kilogramkan kilameterkW kilowattkWh kilowatt hoursMCF thousand cubic feetMJ megajouleMMBTU million British thermal unitsMMCFD million cubic feet per dayMW megawattTCF trillion cubic feettoe tons of oil equivalent

CONTENTS

EXECUTIVE SUIMMARY

I. INTRODUCTION 1

II. ENERGY AND THE ECONOMY 2The Economic Setting 2Energy Consumption 3

Im. HOUSEHOLD ENERGY 5Fuelwood 5Household Use of Conventional Fuels 9Small Scale Renewable Energy Sources 10Wood and Charcoal from Brush Clearing 13Rural Electrification 13

IV. MEETING NAMIBIA'S ENERGY NEEDS 17Power 17Petroleum Supply 28

V. EXPORT OPPORTUNITIES 34Epupa Hydropower Project 34Kudu Offshore Gas Field Development 36The Way Ahead 39Oil Exploration 40

VI. INSTITUTIONAL ISSUES 42Strengthening the MME 42Regulating the Power Sector 43Rationalizing Power Distribution 44Petroleum Product Pricing 45

ANNEX A 47Energy Balances, 1989-91ANNEX B 50Cost Comparison Of Short And Medium Term Power Supply OptionsANNEX C 54Epupa Hydropower Project

i

EXECUTIVE SUMMARY

1. Namibia is fortunate in that the energy sector is not a constraint on growth, as it is inso many developing countries. Indeed, through the exploitation of Namibia's hydro-electricand/or hydrocarbon resources for export, the sector may well become a major engine ofgrowth. At present, industry, commerce and the country's population centers are adequatelysupplied with commercial energy (electricity and petroleum products) at economic prices.However, many households sLill lack access to modem energy supplies and, especially inrural areas, still rely on wood and other traditional fuels, particularly for cooking.

2. Per capita energy use in 1991 amounted to 0.51 toe, which is well above that of mostSub-Saharan Africa. However, traditional fuelwood (non-commercial energy) plays a muchmore limited role in energy consumption (around 14%) in Namibia than in most othercountries on the continent. The predominance of commercial energy in the Namibianenergy balance reflects the importance of the energy-intensive mining industry in thecountry's economic structure as well as the relatively high incomes enjoyed in the modem,urban areas and the ready availability there of commercial energy at reasonable prices. Theincrease of energy consumption in the next few years is likely to parallel the modest growthrate foreseen for the economy and, thus, to arerage some 3.0-3.5% per annum.

3. While the energy sector today serves Namibia well, and much has beenaccomplished since independence, its future will depend in good measure on effectivelyaddressing the policy, investment and institutional issues that are the focus of this report.

Household Energy

Household Fuels

4. Fuelwood is the main energy source in rural areas, where it is frequentlysupplemented by dung and agricultural residues. Electricity is the main cooking fuel in theurban areas, where bottled gas and paraffin are also used to a limited extent. A householdenergy survey conducted in preparation for the assessment indicates that, while fuelwood isincreasingly difficult to come by in some areas, there are few signs of resulting hardshipand that energy in general does not take a disproportionate share of household budgets.

5. Widespread deforestation is clearly taking place in the north, where the bulk of therural population lives. However, the amounts of wood used in homestead construction aremany times greater than those used for fuelwood. Clearing for agriculture can also destroyconsiderably more forest than fuelwood cutting. Indeed, even if fuelwood consumptionwere to cease completely, deforestation would continue rapidly as a result of cutting treesfor homesteads and agricultural clearing. Any resolution of the deforestation problem willthus require a coordinated approach involving a wide variety of non-energy inputs andinitiatives.

6. The fact that the majority of families appear able to manage satisfactorily with theenergy resources freely available to them greatly limits the potential and the need forintervention in the rural fuelwood sector. Promoting tree growing for fuelwood is unlikelyto be successful. Investing time and effort in a woodlot is not an attractive option to afamily which can readily obtain brush wood, agricultural residues and animal dung assubstitutes if traditional supplies of fuelwood become scarce. Where fuelwood is purchased,there may, however, be some scope for the introduction of improved cooking stoves in orderto help families reduce the amount they spend on fuelwood. The mission recommends that

a preliminary assessment be made of the potential for introducing improved stoves in thenon-electrified urban areas as well as in the north.

7. Electricity is more or less universally available in the urban areas. It is the maincooking fuel for the great majority of families even in the lower income areas because it ismarkedly cheaper than fuelwood, paraffin, or bottled gas. The provision of electricity cantherefore bring significant savings to families who purchase their fuelwood.

Renewable Energy

8. The Namibian renewable energy sector appears to be in an unusually strongposition. Photovoltaics and wind are well developed and filling the niches for which theyare presently suited both effectively and competitively. The private sector is active andcompetent; it should continue to play the major role in renewable energy development. Thisshould be facilitated by increased government support focused on data gathering anddissemination, the commissioning of studies and pilot projects and the establishment ofperformance and design standards.

Rural Electrrficadon

9. Rural electrification is an important element in the government's policy of redressingthe long neglect of the communal lands under the previous administration and directlyassisting Namibia's rural poor. As presently carried out, it mainly involves the provision ofgrid extensions to government facilities and other selected rural centers, most of which werepreviously supplied by isolated diesel generators. The largest rural electrification programat presently underway is in the northern province of Owamr.bo and is funded by NORAD.The transmission component of the program consisted of 530 km of high voltage line andassociated transformers and was completed in early 1992, almost a year ahead of scheduleand with a saving of more than 25% of the project budget. Progress on the local distributionsystem has, however, been slow.

10. It is unlikely that the Owambo project, and others like it, can be justified on stricteconomic grounds. Their primary justification must be social and political, which is entirelylegitimate but does not obviate the need to carefully evaluate such benefits. The direct socialbenefits may well be limited. Most of the government facilities already have electricity andtheir functioning will not be substantially altered although they will benefit from morereliable power supply and there will be substantial fuel cost savings. Internationalexperience generally indicates that the provision of grid electricity is unlikely, in itself, tobring about economic development which would otherwise not occur. Furthermore, thenumber of domestic connections is also likely to be low. Even if there is a high connectionrate in the electrified centers themselves, the number of households supplied will inevitablybe a small proportion of the total population of the region, which outside the few towns iswidely dispersed.

11. The undoubted need to address the needs of long-neglected rural people should beweighed against these uncertainties about the actual economic and social impact of presentrural electrification programs. The mission believes that sound decisions about furthermajor investments in Owambo-like rural electrification programs will only be possible whenimproved institutional arrangements for distribution are in place and when the economicviability and social benefits of the Owambo program can be better evaluated. As discussedbelow, Namibia's electricity distribution system needs to be restructured institutionally; inthis context, special attention should be paid to arrangements for rural electrificationincluding, perhaps, the creation of a special distribution agency for the north. While the

iii

administrative and population centers will remain a natural priority for grid connections,consideration of future rural electrification investments should address the question of howthe more dispersed rural population can also be provided with at least some of the benefitsof electrification. A study should be made of such options as small photovoltaic systemsfor lighting and radio; commercial battery charging systems using photovoltaics or smalldiesel generators; and local community management of small supply systems.

Meeting Namibia's Energy NeedsPower

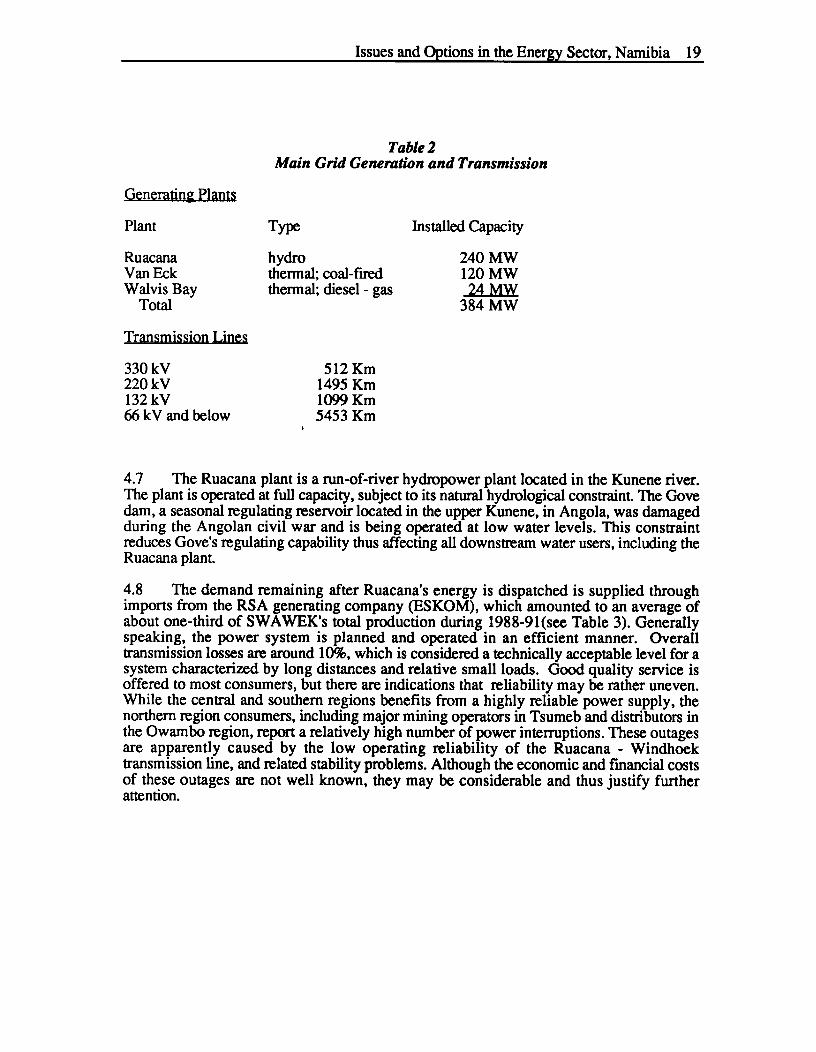

12. The power sector today presents a picture of good health. An extensive nationalgrid supplies urban and industrial consumers with ample supplies of power at tariffs which,while low by international standards, are more than adequate to keep the national powercompany financially flush. However, Namibia is heavily dependent on power imports fromthe RSA and, with demand beginning to press on capacity, it will soon have to faceimportant decisions, involving major investments, concerning how best to meet future needs.Other pending questions include revision of the tariff structure; the finances of the powercompany and their relationship to investment needs; whether to press ahead with large scalehydropower development for export to the RSA; and institutional refonm .

13. The operating institutions in the power sub-sector consist of a national generatingand transmission company and 46 municipal and local distribution agencies. The normativeinstitution is the Ministry of Mines and Energy (MME), which has broad regulatory andpolicy-making responsibility. The national power company, the South West African Waterand Electricity Company (SWAWEK), is responsible for generation and transmission ofpower in areas covered by the national grid. SWAWEK supplies the national gridprincipally from its Ruacana hydropower plant and with imports from the RSA. It can bereasonably assumed that the system's guaranteed capacity is effectively reduced to 260-300MW during the dry season, including the imports contribution but excluding the high costthermal reserve. Peak demand would tend to exceed this capacity by 1995/96, whenNamibia's dependency on energy imports would reach around 40% of total electricityconsumed. Even with demand growing more slowly than in the past, at about 3.5% perannum, additional generating and/or import capability would be required at that time.

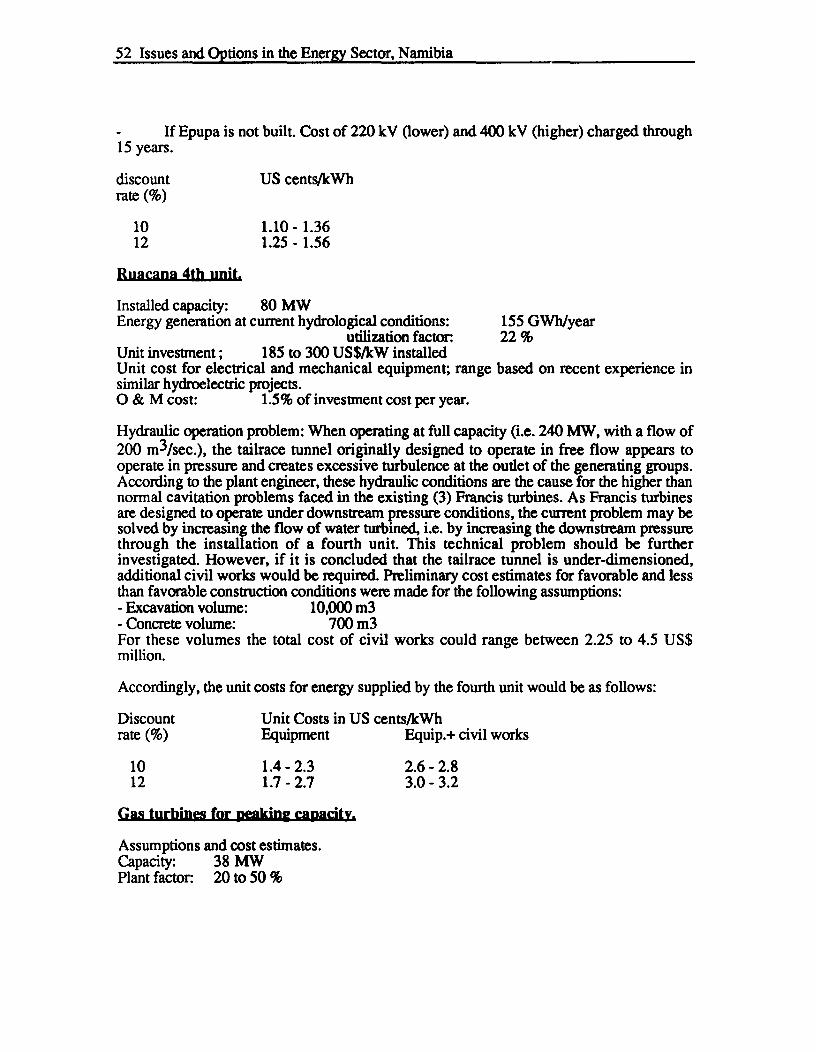

14. SWAWEK's plans for meeting Namibia's power needs in the short-medium termhave been focused mainly on an increase of imports. It has been planning to build anadditional 400kV line as soon as additional import capacity becomes necessary, assumingthat this line will be required in the early years of the next century to carry exports from theproposed Epupa hydropower project to the RSA. The mission's analysis indicates thatother options, although limited in scope, may be more attractive. They may make it possibleto defer major investments in transmission, which could be a great advantage so long as thefate of Epupa remains uncertain, as may well be the case for some time. It is thereforerecommended that these options be investigated further in the following order of priority:

--A peak/off-peak tariff for large consumers. This demand side option should begiven the highest priority because it could bring benefits equivalent to adding 10-20MW of capacity at very low cost.

--Adding a Fourth Unit at Ruacana. Investigating the technical feasibility of thisoption should be accorded first priority on the supply side.

iv

--Gas turbines for peaking capacity. Although a relatively high cost solution, thiscould become a viable option if a time-of-use tariff is adopted.

15. These three options, as well as the plans for transmission for increasing importsfrom the RSA, should be the objects of a study aimed at defining a least-cost generation-transmission plan for meeting Namibia's power needs in the short and medium term.Indeed, such a study could mark the initiation of a much needed more systematic approachto power planning for optimizing sector investment decisions on the basis of a full range ofsupply and demand side options.

16. SWAWEK's costs are very low (0.053 R./kWh in 1991, i.e. less than 2 UScents/kWh), so that even with tariffs that are modest by international standards, income fromoperations substantially exceed operating expenditure. However, the tariff structure for bulksales and final consumers leaves much to be desired economically. It does not reflect thestructure of Namibia's hydro-thermal power supply costs which are strongly affected bypeak and off-peak hours and, probably more important, by the period of the year (i.e. wetand dry seasons). Since capital expenditures have been relatively low, SWAWEK has beengenerating a sizable cash surplus in recent years. The continued piling up of surpluses inSWAWEK's coffers would not be in the best interest either of the government, which facesserious budgetary problems, or of SWAWEK, which could discover that a cash cow's life isnot necessarily a happy one. Much will depend on the decisions to be taken about thepower sector investment program. If major new investments are to be made in the nearfuture, SWAWEK will need all the resources it can generate; if investment remains limited,SWAWEK's resources might be regarded as surplus to its requirements and a case couldbe made for having it fund rural electrification programs, and pay increased taxes and/ordividends to the government.

Petroleum Supply

17. There is as yet no indigenous source of petroleum in Namibia, and no refinery;hence, all products must be imported. The present system which relies on private firms toimport products and distribute them, but with the government closely controlling prices,profits and other aspects of their operation, has evolved from that used in the RSA. Itworks well in meeting the needs of the Namibian market; products of appropriate quality arereadily available throughout the country (except in some remote areas) at economicallyrealistic prices. Since independence, one of the government's major objectives has been thediversification of product supply away from complete dependence on the RSA, and in 1991the portion of Namibia's supplies coming from the RSA was reduced to about 65%. Thegovernment has, at least informally, decided not to press for further diversification of supplyat the present time. This decision seems wise since experience to date appears to indicatethat a significant increase in purchases from non-RSA sources might come only atappreciably higher cost in terms of price, security of supply and product quality.

18. While small in absolute size, Namibia's petroleum consumption per capita is high byAfrican standards. Given the already high consumption level, and tde modest prospects foreconomic growth in the near term, gasoline demand is forecast to grow at only 4% per year,and diesel at 2% per year. Six private companies are now active in the Namibian marketSince the prices of the major products are controlled, competition must be based on servicein lieu of price. This has put a premium on the expansion and modernization of thecompanies' network of service stations. As a result, the country is well served, but"overpumped" - -i.e., there has been over-investment in an excessive number of overlyelaborate service stations.

v

19. In June 1991, it was announced that the government had agreed to the constructionof a refinery proposed by private parties. Little is known about the proposal but theeconomic and financial viability of the project appears highly questionable because of itssmall size (15,000 b/d), a likely product mix that would not match the needs of theNamibian market and inland location. The risk to Namibia from the project appears to havebeen minimized by the requirement that it be constructed without public funds and operatedwithout public subsidy. Moreover, no implementation activity has been evident since theproject was announced and there is no indication of when, if ever, the sponsors intend toproceed with the project

Export Opportunities

Epupa Hydropower Project

20. The hydropower potential of the Kunene river, shared with Angola, constitutes oneof the main energy resources of Namibia. SWAWEK has identified a promising site for thedevelopment of a major hydro plant in the vicinity of the Epupa falls. Given Namibia'spresent generating and import capability, the capacity and energy to be supplied by theproject, particularly for its larger and costwise more attractive size (i.e. 450-500 MW) wouldnot be absorbed by Namibia's power market before the year 2010. Therefore, the project'seconomic viability in the medium term has been considered to rest heavily on its potentialfor exports to the RSA. However, the RSA currently has excess capacity of around 7,000MW and so will most probably not need additional capacity until early in the next century.ESKOM has indicated that it is interested, in principle, in purchasing power from Epupawhen it needs additional capacity but that Epupa would have to be competitive with low costcoal-fired generation in the RSA and with other potential sources in the region such as theKudu gas field and the Cahora Bassa plant in Mozanbique.

21. Until the results of the pre-feasibility study SWAWEK commissioned in 1992become available, there will be no basis for assessing the project other than SWAWEK'sown preliminary studies, which appear optimistic. Using capital costs based on Bankexperience indicates that energy from Epupa would cost 4.0-6.0 US cents/kWh, comparedto the 3.5 US cents/kWh resulting from SWAWEK's preliminary estimates. Although eventhe higher costs may appear attractive by international standards, they suggest that Epupawould have serious difficulty in competing in the RSA market. ESKOM estimates thatcoal fired generation there presently costs only about 2.0 US cents/kWh; the missionestimates the cost of new coal-fired plants to be about 3.0 US cents/kWh.

Kudu Offshore Gas Field Development

22. The evidence to hand suggests that this is a world-scale gas field, with characteristicsindicating that few problems should be encountered in its development and exploitation. Themost recent and thorough examination of the prospects for developing Kudu concludes thatgas can be delivered to shore at after tax prices in the range of $1.34 to $1.14 MCF(MMBTU) at flow rates of 275 and 1,000 MMCFD respectively. Prices in this rangewould compare favorably with those of other, similar gas fields and indicate that it should bepossible to develop Kudu commercially if a market can be found. The Namibian market isfar too small to absorb a meaningful quantity of gas and the likely economic returns onusing it to produce products for sale on world markets (i.e., as feedstock to produce urea ormethanol, or as a fuel for use in aluminum or iron refining) appear low. The government hasreportedly received a proposal from a major international oil company for the developmentof Kudu based on using the gas in a 1300MW combined cycle generating plant on theNamibian coast that would produce for the RSA grid. On the basis of international

vi

experience, a combined cycle plant burning gas priced in the range indicated in the studywould have costs of about $0.03-0.035/kWh (excluding transmission). This appears to bemarginally competitive with coal fired generation in the RSA. However, ESKOM isreportedly interested in purchasing gas, not power, and it is believed that negotiations havefocused on whether Kudu gas can be provided in the Cape at a price that would make itpossible for ESKOM to build a gas fired plant that would compete with coal.

23. Kudu may also have the potential economically to serve a large industrial market inthe Cape that should be ripe for conversion to gas delivered at the price it can offer. Also,since gas field development and production is a type of project eminently suitable for privatesector development and financing, Namibia could reap the very handsome benefits ofKudu's development without having to put public funds at risk or encumber its internationalcredit. To bring the prospects for Kudu into sharper focus, high priority should be given toexploring the feasibility of alternate development plans to include low cost fielddevelopment options, and to more detailed market studies for gas supply to Cape industrialusers. If the results are positive, it should be possible to develop a project that is attractive toprivate investors. A crucial component of such a project is likely to be a marketing strategythat focuses on getting Kudu's foot in the door by bringing gas to the Cape and offering itat the lowest possible price in order to quickly develop the market. Such a strategy wouldentail both risk and the deferral of returns. Namibia's petroleum legislation containsimportant elements of flexibility and the govemment may, given its interest in seeing thecommencement of development of its natural resources, wish to consider deferring its taxtake from the project to make it more attractive to investors.

Oil Exploraion

24. The discovery of oil would, needless to say, change the entire energy picture, andmuch else. One of the government's primary objectives in the sector has been to promotepetroleum exploration and, to this end, it moved rapidly after independence to strengthen thegeologic data base, enact an attractive contractual and fiscal framework and organizeinternational bidding for licenses. Results to date suggest that the promotion program isgoing extraordinarily well. Licenses for offshore exploration have been negotiated with fourconsortia of international oil companies, and NAMCOR, the state petroleum company,appears to have succeeded in obtaining minimum work commitments totaling some$110million, including the drilling of 8 wells. Based on international experience, efforts onthis scale should be sufficient to define the commercial potential of Namibia's hydrocarbonendowment. NAMCOR is presently planning to open a second promotion round in late1993-early 1994.

Institutional Issues

25. While the present strengths and resource potential of the energy sector give goodgrounds for optimism about its future development, much will depend on the effectivenessof policy-making and administration in the sector. As is inevitable in so new a nation, a greatdeal needs to be done to strengthen policy analysis and decision making capabilities, tobuild an appropriate the legal and regulatory framework, to rationalize the institutionalstructure, and to enhance the professional and technical capacities of those working in thesector. The outstanding institutional issues that appear most pressing to the mission arediscussed below. The MME is well aware of the importance of these issues and intends to26. give high priority to addressing them in 1993 and later years.

vii

Strengthening the MME

26. While still a fledgling institution, the MME has done much to strengthen itsorganizational structure and to bolster its staff. To date, it has played L much moreimportant role in petroleum than in power, where practical and historical considerations havelimited its role as regards both policy and regulation. Legal and institutional changes, suchas those discussed below, can contribute much to strengthening the ministry's hand inpower regulation. To enhance its role in policy-making, the MME will need to equip itselfwith more comprehensive, current and systematic data on all aspects of the sector andincrease its analytical capabilities, especially on the economic and financial side. For bothpurposes, it will need to further upgrade its staff, not so much quantitatively as qualitatively.The MME is working closely with NORAD and other donor agencies on training programsand other technical assistance that will help it meet these needs.

Regulating the Power sector

27. A number of factors have limited the MME's effectiveness in the power sector. Asa well established, technically proficient and financially strong institution with forcefulleadership, SWAWEK has naturally tended to have a major, even dominant, voice in policy-making. In addition, the lack of a regulatory framework for generation and transmission,and the fact that other government agencies have primary responsibility for distribution,have limited the MME's role in power regulation. The MME reviews tariff changesproposed by SWAWEK, but since there are no publicly established criteria, and the MME'sanalytical resources are limited, it is not surprising that SWAWEK's proposals seeminvariably to be approved. The challenge facing the government is to establish a frameworkunder which it can provide policy direction and regulatory oversight in a meaningful fashionwhile enabling SWAWEK to continue functioning efficiently and on a financially sound,commercial basis. As regards tariffs, the government might be well advised to give firstconsideration to a simple rate of return based approach to the overall level of tariffs, and toestablishing a time of day tariff structure that differentiates between peak and off-peaksupply costs.

Rationaliing Power Distribution

28. The involvement of three sets of institutions --the municipalities, the Ministry ofLocal Government and Housing (MLGH), and the Peri-Urban Development Board-- inelectricity distribution in a country with as small a population as Namibia's has resulted inan atomization of responsibility and a variety of diseconomies and inequities. Even the bestequipped of the three, the municipalities, vary widely in competence and the service they canoffer and none of the distributing institutions runs its system as a financially responsiblecommercial enterprise. The MLGH, which is responsible for distribution in rural areas,incurs a significant loss on its operations as a result of the very high level of unpaid bills(arrears) owed by its customers and high technical losses in its distribution systems.Distribution is, therefore, a major weak point in Namibia's power system and one thaturgently requires attention, particularly in view of the growing importance of householdconsumption in the system. The objective should be to restructure the system with a view to(i) putting the operation of the system on a commercial, preferably private basis insofar aspossible (ii) centralizing operations so as to obtain greater economies of scale and toequalize service while (iii) maintaining and enhancing local responsibility. A thoroughstudy of the distribution system and the options for its rationalization is recommended.

vii

Petrokum Product Pricing

29. The prices of the major petroleum products (petrol, diesel and kerosene) arecontrolled by the government under a system essentially similar to that in the RSA. Pricesare reasonable and the system works smoothly; it is quite transparent and there appear to beno inherent conflicts of interest. Nevertheless, prices are almost certainly higher than theywould be if the market were competitive, and price control seems a hangover from pre-independence times with little or no economic benefits today. In the absence of pricecontrols, with margins no longer assured, it is likely that one or more of the less efficientdistribution companies will withdraw from the market. It is generally agreed that sixcompanies are too many for Namibia's small market and that only three or four wouldremain after deregulation. This should be sufficient to maintain competition. It is thereforerecommended that the government move to phase out price controls

L. INTRODUCTION

1.1 Namibia is fortunate in that the energy sector is not a constraint on growth, as it is inso many developing countries. Indeed, thrugh the exploitation of Namibia's hydro-electricand/or hydrocarbon resources for export, the sector may well become a major engine ofgrowth. At present, industry, commerce and the country's population centers are adequatelysupplied with commercial energy (electricity and petroleum products) at economic prices.However, many households still lack access to modern energy supplies and, especially inrural areas, still rely on wood and other traditional fuels, particularly for cooking. Ahousehold energy survey conducted in preparation for the assessment indicates that, whilefuelwood is increasingly difficult to come by in some areas, there are few signs of resultinghardship and that energy in general does not take a disproportionate share of householdbudgets.

1.2 That Namibia's energy sector works so well owes much to the fact that the sector'smajor public and private institutions operate on commercial principles and that energy pricesare sufficient to ensure the financial soundness of the operating agencies, to provide fundsfor investment and, in most cases, to send the "right" economic signals to producers andconsumers. While maintaining this essential framework, Namibia needs to pursue four keyobjectives in further developing its energy sector.

* increasing access to modem energy supplies for households,

* ensuring that commercial energy supplies expand to meet the growing needs of theeconomy,

e developing its export potential, and

* strengthening the institutional structure of the sector in order to facilitate moreeffective policy-making and implementation.

1.3 This report presents the findings and recommendations concerning issues in theseareas of a mission that visited Namibia in June-July, 1992. The mission was led by Mr.Richard S. Dosik (consultant) and included Mr. Thomas O'Connor, Oil and Gas Specialist;Mr. Enrique Crousillat, Power Specialist, Mr. Gerald Foley (consultant), Household EnergySpecialist; and Mr. Amadou Cisse, Energy Economist. While the energy sector todayserves Namibia well, and much has been accomplished since independence, its future willdepend in good measure on effectively addressing the policy, investment and institutionalissues that are the focus of this report. The mission's recommendations are generally limitedin scope and quite tentative in nature, reflecting both the limited information available to it insome areas, as well as the mission's feeling that, in the case of the Namibian energy sector, itwould best to be guided by the adage "If it ain't broke, don't fix it.".

2 Issues and Options in the Energy Sector, Namibia

I. ENERGY AND THE ECONOMY

The Economic Setting

2.1 Namibia's energy sector reflects the sharp (even for Africa) contrast between themodem/commercial and ruraVtraditional sectors of the economy. Looking at just themodem sector, Namibia appears much like a prosperous middle income country; it has anestimated GNP per capita of nearly $1200 and much physical infrastructure (in transportand telecommunications, as well as energy) of which an industrial country would be proud.However, the majority of Namibia's approximately 1.5 million people has an income perhead of about $85 per year and lives under primitive conditions without adequate housing,water or health or education services. Mining (chiefly for diamonds, uranium and copper)is the mainstay of the modem economy, accounting for some three-quarters of exportearnings, four-tenths of public revenue, and nearly one-third of GDP. Agriculture is,however, the major source of employment, supporting some 70% of the population. Itscontribution to GDP and exports (about 12% in both cases) comes mainly from the largecommercial cattle and sheep ranches that occupy the arid southern two-thirds of the country,whereas the bulk of the rural population is engaged in subsistence farming in the somewhatless arid north.

2.2 Namibia's dependence on primary production, which all told accounts for nearly45% of GDP, makes its economy subject to significant fluctuations resulting frominternational market conditions, the weather and other external forces. The mining industrygenerally calls the tune and the depressed state of the minerals markets had much to do withthe sluggish growth of the Namibian economy during most of the 1980s. Stabilizinginfluences on Namibia's economy come from the secondary (21% of GDP) and tertiarysectors (35% of GDP). Government expenditures on goods and services, including thegrowing civil service (19% of GDP) are particularly important in smoothing the otherwiseerratic impact of the primary sector. The role played by government expenditures can beexpected to grow, in part because Namibia's membership in the Common Monetary Area(CMA) with the RSA effectively takes monetary policy out of the government's hands andmakes fiscal policy the default policy tool. In addition, the government's concern withreducing the inequality in income distribution seems bound to increase its role in theeconomy.

2.3 Since the 1960s, when the GDP growth rate was some 9.0%, there has been littleforward momentum in the economy. Growth was weak in the 1970s and the 1980s was aperiod of fluctuation between boomlets and busts, with net growth of only about 1% overdecade. However, a modest revival of growth appears to have taken place in 1990 and 1991,when GDP rose by 3. 1% and 5.1%, respectively. In 1991, diamond production jumped byalmost 56% and gold extraction increased by around 16%, although the rest of the country'smining output (uranium, copper, lead, zinc, silver) declined by 20%. The fishing industry,which is expected to become a significant growth pole in the primary sector, also had a goodyear in 1991, when the catch grew by no less than 84%! However, one or even two goodyears do not a growth trend make, especially since one-time factors in the form of theopening of a new diamond mine and the extension of Namibia's territorial waters had much

Issues and Options in the Energy Sector, Namibia 3

to do with the economy's improved performance in 1991. All told, the growth rate willprobably average 3-4% over the next few years.

2.4 Namibia's balance of payments appears quite strong. The boost to exports resultingfrom the aforementioned windfall gains in the diamond and fishing industries helped to cutthe trade deficit by more than 50% in 1991 and this, together with higher transfer paymentsand service earnings, resulted in a substantial surplus on current account. Inflation in 1991was held to the 1990 level of about 12%, but there were disquieting developments in thelatter part of the year when the monthly rate of increase in the price indices, which had beendeclining, reportedly began to move up. This turn-around was attributed mainly to risingconsumer demand resulting from an expansion of consumer credit coupled with inflationarywage settlements.

Energy Consumption

2.5 Per capita energy use in 1991 amounted to 0.51 toe, which is well above that of mostSub-Saharan Africa. However, traditional fuelwood (non-commercial energy) plays amuch more limited role in energy consumption (around 14%) in Namibia than in most othercountries on the continent. 1 The predominance of commercial energy in the Namibianenergy balance reflects the importance of the energy-intensive mining industry in thecountry's economic structure as well as the relatively high incomes enjoyed in the modern,urban areas and the ready availability there of commercial energy at reasonable prices.

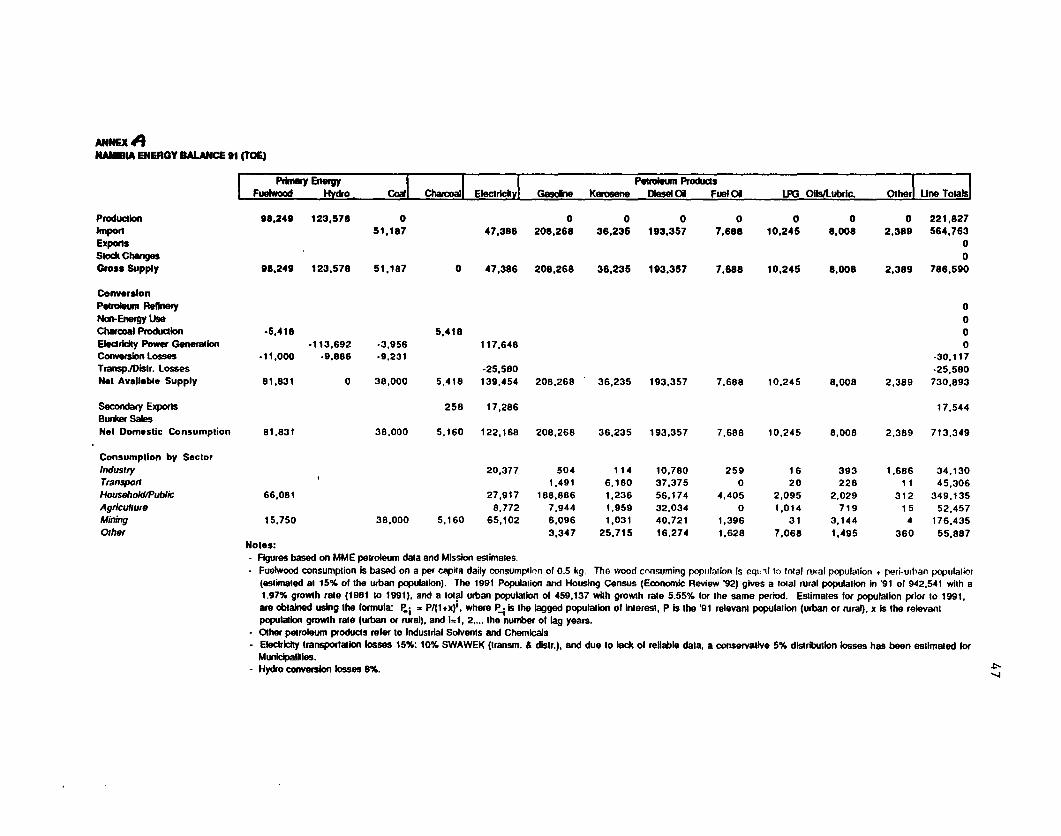

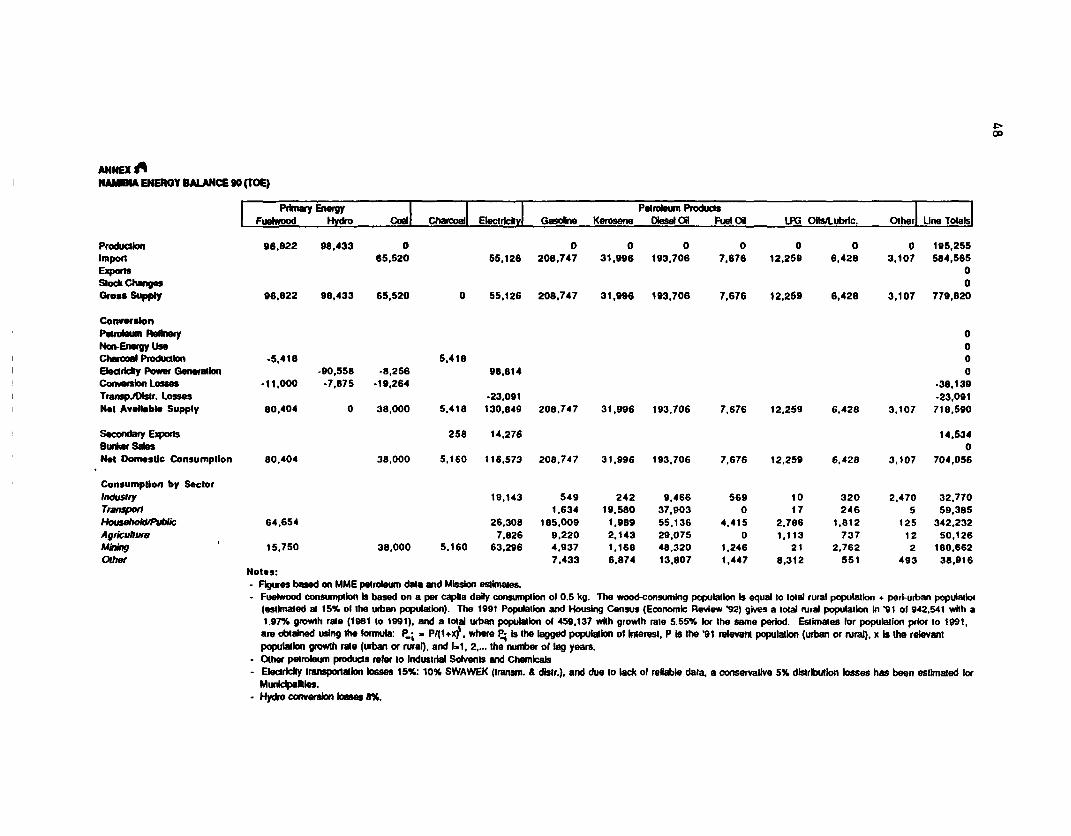

2.6 As the summary balance below shows, petroleum products account for the largestshare of energy use (over 65%), followed by electricity (around 17%). Annex A containsdetailed energy balances for 1989-91.

Final Energy Consumption, 1989-91 (TOE)

1989 1992 191Oil Products 563,132 463,919 466,190Electricity 111,091 116,573 122,168Fuelwood 70,013 80,404 81,831Coal 43,160 43,160 43,160Total 796,396 704,056 713,349Per Capita 0.603 0.517 0.509Consumption per SectorIndustry 34,752 32,770 34,130Transport 71,617 59,385 45,306Household/Public 394,316 342,232 349,135Agriculture 50,947 50,26 52,457Mining 199,098 180,662 176,435

45,666 38,916 55,887

1 Data onffuelwood consumption are sparse and must be regarded with caution.

4 Issues and Options in the Energy Sector, Namibia

2.7 After dropping off sharply in 1990, in the wake of the departure of the RSA and UNforces at the time of independence, energy consumption recovered modestly last year whenit grew by some 1.55%2 The increase of energy consumption in the next few years islikely to parallel the modest growth rate foreseen for the economy and, thus, to averagesome 3.0-3.5% per annum. With a continuing decline in Uranium production at theRossing mine and the impending closure of the Tsumeb copper mine offsetting the impactof the planned new operations, the demand for electricity in the mining sector is, at best,likely to remain flat. However, demand from the municipalities, the government and forrurl electrification can be expected to continue to expand rapidly and to largely account foran overall growth in electricity consumption of around 3.5% per annum. The demand forpetroleum products is projected to grow somewhat more slowly, at about 3.0% per annum,with new requirements coming only from the fishing industry. In the fuelwood sector,demand is likely to grow only modestly, if at all, since the impact of population growth islikely to be mostly offset by a continuing switch to electricity and other modern fuels forcooking.

2 The continued sharp decline in consumption in the transport sector in 1991 was mainly theresult of a further sharp reduction in jet fuel sales as the last of the major UN operations wounddown.

Issues and Options in the Energy Sector, Namibia 5

III. HOUSEHOLD ENERGY

3.1 Fuelwood is the main rural energy source in Namibia and is frequentlysupplemented by dung and agricultural residues. Electricity is the main cooking fuel in theurban areas. Bottled gas and paraffin are also used to a limited extent.

3.2 A survey of household energy consumption was carried out for ESMAP by theNamibian Institute for Social and Economic Research (NISER)3. The study focused onOwambo, which accounts for about 70% of the rural population, and on the large townshipof Katutura outside Windhoek4. Table 1 shows the breakdown of household cookingenergy consumption for Owambo and Katutura.

Table I

FUEL OWAMBO KATUTURA

Fuelwood 90 11.7Ag. residues, dung 7.5Electricity 1 84.5Bottled gas 1.5 2.8Paraffin -

Fuelwood

The Owambo region

3.3 Fuelwood consumption is concentrated in the Owambo region of northern Namibiawhich, with a population of about 600,000, is the most densely inhabited region of thecountry. The density is nevertheless low in absolute terms. In Owambo as a whole it isonly about 12 persons per square kilometer though it is higher towards the center where thewater supplies are most plentiful.

3.4 Owambo is crossed by a large number of seasonal rivers draining in a deltaformation, known as the Cuvelai system, towards the Etosha Pan. Rainfall increasestowards the north east but over most of Owambo is 400-500 mm per year. The naturalvegetation varies from grassland to tree savanna depending on rainfall.

3.5 Central Owambo is the main area of crop cultivation in the country. Farms aresmall, with a typical cultivated area of two to three hectares. Drought is common and themain subsistence crop is millet (muhango). Fruit trees are grown but there is no significanttree planting for other purposes.

3.6 The ground water in most of the area is highly saline but people are able to obtainfresh water from shallow hand dug wells. These tap into an aquifer fed by the Cuvelai

3 "Household Energy Consumption, Distribution and Marketing Survey of the Owambo Region ofNorthern Namibia and Katutura, Windhoek" , 1992 .

4 Further information on family fuel consumption is available in the NISER report: "Socio-economic study of the OndangwalOshakati nexus area." Research Report No 8, Feb 1992.

6 Issues and Options in the Energy Sector, Namibia

system but isolated from the lower saline ground water by a hard calcareous layer.Pipelines from the Kunene river provide supplies to the main population centers as well asstock watering points.

3.7 Land is held under traditional tenure rules administered by local chiefs. Individualsare allocated a holding for life but are not allowed to pass it on within the family. Outsidethe cultivated fields the land is open to everyone for grazing and tree cutting.

The household energy study

3.8 The NISER study divided Owambo into four ecological zones: grassland, palm-tree,savanna, and woodland; and the peri-urban OshakatiVOndangwa area. The sample consistedof 200 families, all within a 100 km radius of Oshakati. The average household size was8.13 persons. The average annual family expenditure was estimated to be R3,514.

3.9 The survey showed that fuelwood was the main cooking fuel of 90% of families.Dung and agricultural residues were widely used as supplementary fuels but were theprincipal fuels of 7.5% of families. Fuelwood use varied in accordance with its availability;in the grassland area, 75% of families used other fuels occasionally or all the time whereasin the woodland areas only fuelwood was used. The great majority of families (94%) usingfuelwood collected it from their surroundings. On average, collection was every four daysand took about 90 minutes. A small number of families (6%) were found to purchase someor all of their fuelwood.

3.10 The quantities of fuelwood used were calculated by asking households how longsample bundles would last. This gave an average daily consumption per head of 0.50 kg forthe rural areas, varying from 0.31 kg in the grassland area up to 0.56 kg for the woodlandareas. These figures appear low in comparison with other African countries5 though thefact that they show a plausible pattern of variation between ecological zones adds to theircredibility. But depending, as they do, on subjective estimations, they must be subject toconsiderable reservation.

3.11 The survey of the Ondangwa/Oshakati nexus found that fuelwood consumptionfalls off within the peri-urban area with 56% of households relying on it as their maincooking fuel. About 70% of these purchased their supplies. The mean annual householdexpenditure was R9,754 and the mean annual expenditure on fuelwood was R750, or about7.7% of total expenditure.

Fuelwood consumption in Katutura

3.12 Katutura is a township established in 1968 on the edge of Windhoek. It has apopulation of around 90,000. Dwelling plots are officially designated and the majorityhave water, electricity and sanitation. About 90% of the houses are of brick or block withiron roofs and about 50% are privately owned. In the past few years an increasing numberof squatter settlements have been established around Katutura. The dwellings are ofmakeshift construction and do not have electricity.

5 Figures of over 2 kglhead/day have been found in Tanzania, south Sudan, Kenya and theGambia, though 0.8-1.0 kglhead per day is more typical of the drier areas in these countries.Figures from Mali give 0.7-0.9 kglhead/day for the arid areas and 1.7-2.4 kglhead/day for thehigher rainfall areas.

Issues and Options in the Energy Sector, Namibia 7

3.13 In the NISER survey, a total of 103 families were interviewed. The average familysize was 6.37. The average annual family expenditure was estimated to be R10,699. Justunder 15% of families use fuelwood most or all of the time. The estimated consumptionwas 0.64 kg per head per day. The average annual expenditure on fuelwood per family wasR740, about 7% of total expenditure.

3.14 Large amounts of wood are available within the open lands and commercial farmsimmediately around and within a few tens of kilometers of Windhoek. A proportion of thesupplies to Katutura are collected, or stolen, from these areas. There are also sales fromcommercial farms to fuelwood dealers. Reports that fuelwood is transported to Windhoekfrom Owambo are almost certainly exaggerated. Wood prices are based on the bundle sizerather than the weight and unit prices vary greatly, ranging from RO.40 cents per kg toR1.20 per kg.

Fuelwood consumption in other rural areas

3.15 Fuelwood is also used in the communal areas to the south, east and northeast of thecountry. In general, population densities are extremely low - less than one person persquare kilometer in Kaokaland, Keetmanshoop, and Hereroland East and about five personsper square kilometer in East Caprivi. In such areas, the available wood, or other burnablebiomass, is generally likely to be adequate for local people's needs.

3.16 The mission was, however, informed by the MME that there are some fuelwoodshortages in parts of Keetmanshoop and Marienthal though no details were available. It isrecommended that a rapid appraisal be made of the position in these areas to establishwhether a more detailed investigation of the problems and available options should be made.

Overall household consumption offuelwood

3.17 Bearing the reservations about the consumption figures in mind, and assuming atotal of 1.1 million consumers, total household consumption of fuelwood is around230,000 tons per year. This is equivalent to about 80,000 tons of oil equivalent.

Fuelwood consumption and the natural environment

3.18 Widespread deforestation is clearly taking place in Owambo. Records from the1950s show that many communities were separated from each other by tracts of forest. Inthe more heavily populated areas, this forest has now vanished. Around the towns andalong the livestock routes by the main roads, not only trees but the whole vegetation coverhas disappeared.

3.19 One of the largest uses of wood is construction of traditional homesteads. Theseconsist of a series of huts and compounds, separated by fences and surrounded by a highstockade. The total length of stockade may be 300 meters or more, made up of logs 2-3meters long and 6-9 cm in diameter. In addition, there may be up to 1.5 km of fencingmade of smaller poles and sticks around the cultivated fields and stock pens.Measurements made in 1990 of a typical homestead near Oshigambo found about 100cubic meters of wood had been used. Traditionally, homesteads have tended to be movedevery five or six years, with most of the poles being replaced in the process.

8 Issues and Options in the Energy Sector, Namibia

3.20 The wood for homesteads is taken from the nearby forests if suitable trees still exist.In areas where the larger trees have been cut, families use a cart or hire or borrow a pick-uptruck to obtain the wood from further away. Otherwise, alternative construction methods areused, with fences being made of thorn brush or bound bundles of millet stalks.

3.21 The amounts of wood used in homestead construction are many times greater thanthose used for fuelwood. Using the NISER survey figure of 0.5 kg per head per day, atypical family uses about 1500 kg per year or about 2 cubic meters. The construction of theOshigambo homestead above is equivalent to 50 years supply of fuelwood for such afamily.

3.22 Clearing for agriculture can also destroy considerably more forest than fuelwoodcutting. The wood "consumption" of a family clearing 3 hectares of intact woodland everyfive years is about 15 tons or 21 cubic meters per year, ten times its fuelwood consumption.

3.23 Attempts to slow deforestation through energy initiatives are thus unlikely to haveany significant effect. Indeed, even if fuelwood consumption were to cease completely,deforestation would continue rapidly as a result of cutting trees for homesteads andagricultural clearing. Any resolution of the deforestation problem will require a coordinatedapproach involving a wide variety of non-energy inputs and initiatives.

Recommendadons

3.24 The fact that the majority of families appear able to manage satisfactorily with theenergy resources freely available to them greatly limits the potential and the need forintervention in the rural fuelwood sector.

3.25 Promoting tree growing for fuelwood is unlikely to be successful. There is notradition of cultivating indigenous trees for fuel and exotic species such as eucalyptus,leucaena or others tend to require watering and considerable care over at least the first twoyears6. Investing time and effort in a woodlot is not an attractive option to a family whichcan readily obtain brush wood, agricultural residues and animal dung as substitutes iftraditional supplies of fuelwood become scarce.

3.26 Where fuelwood is purchased, there may, however, be some scope for theintroduction of improved cooking stoves. These, it should be noted, will not have anysignificant effect on deforestation but can help families reduce the amount they spend onfuelwood. A number of attempts have already been made to introduce such stoves but theeffect has been slight The mission recommends that a preliminary assessment be made ofthe potential for introducing improved stoves in the non-electrified parts of Katutura as wellas Oshakati and Ondangwa. This assessment should be carried out, in collaboration withthe MME, by one of the well-established international stove organizations with a provenrecord of field success.

6 A total of about 100 hectares of eucalyptus plantations have been established at various timesover the past 20-30 years. Growth and survival have been relatively poor. There is, forexample, a poorly growing 45 ha plantation established in the 1970s beside the main road atOnankali to the north of Tsumeb.

Issues and Options in the Energy Sector, Namibia 9

Household Use of Conventonal Fuels

3.27 Electricity is more or less universally available in the urban areas. It is the maincooking fuel for the great majority of families even in the lower income areas. In Katutura,the NISER survey found it was the main cooking fuel of 84.5% of households. It is alsoused for lighting, TV and other household uses.

3.28 Appliances are readily available and relatively affordable in relation to averagehousehold incomes. A two plate cooker, for example, is about Rl3. The NISER surveyfound that average annual consumption per household was 3,841 kWh. The average outlayon electricity was R944, about 9% of family expenditure.

3.29 In the Oshakati/Ondangwa nexus, where electricity is confined to a smallproportion of households, bottled gas is the most popular cooking fuel next to fuelwood. Itis used as the main cooking fuel by almost 30% of families. In Katutura, it is used by about10% of families.

3.30 The NISER survey found that paraffin was used by 52.5% of Owambo families forlighting. A small proportion of households (6%) also used it for cooking. The averageannual consumption was 67.5 liters per family. The price was in the range R1.67 - 1.94 perliter and average family expenditure was Ri 13 per year.

3.31 Candles are the other main lighting source in the rural areas. Dry cell batteries arewidely used for radios and torches. Car batteries are used for lights, radios and other lowvoltage appliances and are recharged in vehicles or service stations where a fee is charged.

Prices and supplies

3.32 Domestic fuel prices, except for electricity, tend to vary widely even within the samelocality. Fuelwood, however, even at the low end of the retail price range, is considerablymore expensive than conventional fuels, especially electricity, for cooking as can be seen inTable 2.

Table 2

Fuel Unit price Price/MJ Efficiency Price/end-Rcents % use MJ

Fuelwood 3.33 Rc/kg 3.34 3.35 3.36Paraffin 3.37 R/ltr 3.38 3.39 3.40Electricity 3.41 Rc/kWh 3.42 3.43 3.44Botded gas 3.45 R/kg 3.46 3.47 3.48

3.33 Electricity's marked price advantage goes far to account for its popularity as acooking fuel wherever it is available. The provision of electricity can therefore bringsignificant savings to families who purchase their fuelwood. The impact on the pooresturban families, however, is generally less since they tend to collect rather than purchase theirfuelwood. This is also true of the great majority of families in the rural areas.

10 Issues and Options in the Energy Sector, Namibia

3.34 There do not appear to be any significant problems in the supply of conventionalfuels. In areas where a demand exists, there is every indication that the distribution andmarket systems already in place are able to meet it satisfactorily as well as supply any likelyfuture increases.

Small Scale Renewable Energy Sources

Solar energy

3.35 Namibia has around 3300 hours of sunshine per year, one of the highest figures inthe world. Insolation levels reach 8 kWh per square meter per day and even in the rainyseason there are normally 4-5 hours of bright sunlight.

3.36 The main user of photovoltaic systems is the Department of Posts and Telegraphswhich has installed a total of about 180kW for use in relay stations and other remoteapplications. The Department calculates that the savings in comparison with diesel enablethe capital costs of a typical installation to be amortized in 14-26 months.

3.37 The Ministry of Wildlife, Conservation and Tourism has installed a total of 18photovoltaic pump systems for game water holes in Etosha National Park with a totalcapacity of about 25 kW. A further 33 installations are planned. The NamibianBroadcasting Company is also a major user.

3.38 A number of photovoltaic systems have been installed for lighting and pumping atschools, clinics and other government facilities and such applications are under increasinglyactive consideration. Sales in the commercial farming areas for farm and householdapplications are also rising. Studies by NISER and the Department of Water Affairs intothe potential for wider application of photovoltaics are to be carried out later in 1992.

3.39 Despite the abundance of solar energy, solar water heaters are little used. The mainreason is that the majority of potential consumers are connected to the SWAWEKelectricity supply system. The low level of tariffs makes solar water heating at aroundR4000 per installation an unattractive option. There would appear, however, to beopportunities for the installation of heaters in government facilities not served by gridelectricity. In some cases diesel generated electricity is apparently being used for waterheating. This deserves to be investigated.

3.40 The private sector is active in the supply and installation of photovoltaic systems.Most of the components are imported but the design, assembly and testing of systems iswell within the capacity of local companies.

3.41 The market appears to be competitive, with at least three active local companies andothers based in South Africa willing to tender for work. Government projects are generallybased on performance specifications and are subject to competitive bidding. There is a highlevel of awareness of the need for testing of designs and vulnerable components and of theimportance of adequate repair and maintenance.

3.42 The following are sample retail prices for a number of systems. They do notinclude installation or Government sales tax.

Issues and Options in the Energy Sector, Namibia 11

Siemens (Namibia?20 Wp lighting kit for 2 lights R835.0055 Wp 3 light kit 2,225.0055 Wp 6 light kit 2,743.00

Solar Age (Namibia)11 Wp lighting kit for 1 light 900.003 Wp rechargeable portable lamp 550.0060 Wp panel, 4 lights, 12V B+W TV 3,200.002x60 Wp panels + inverter 7,000.00

3.43 These prices appear rather high by international standards, but are comparable withZimbabwe, for example, where a significant local photovoltaic supply industry alreadyexists.

Wind power

3.44 Wind power is well established and is the main source of energy for water pumpingin the commercial farm area. It is estimated that there may be 30,000 or more functioningwindmills in the country, many of which have been working for decades.

3.45 The potential use of wind pumps in the communal lands has yet to be explored indepth though it is likely to be less than in the commercial farm areas because of the lessfavorable wind regimes. The possibility that combined wind and photovoltaic installationsmight be able to replace some of the smaller diesel generators presently being maintained bythe Department of Works has been suggested by the Research Section of the MME. Underthis scheme, pumping would be provided by the windmill and electricity by the photovoltaicsystem. The possibility deserves more detailed investigation.

3.46 Apart from the use of a small number of wind chargers for batteries, wind power isnot used for electricity generation. This is likely to remain the case as wind speeds aregenerally below the figure of 4 meters per second at which electric power generationbecomes a potentially attractive option.

3.47 The exception is the coastal area where wind speeds are high and relatively constant.A proposal has been made to investigate the possibility of establishing a wind farm tosupply the grid at Luderitz and is reported to be under sympathetic consideration by anumber of donor agencies. Although the technical potential for such a project may exist,there is no reason to suppose it would be able to compete with SWAWEK's very low costs.

Biogas

3.48 Although biogas has attracted some interest in Namibia, its potential role is minor.The shortage of water is a key limitation. The free range grazing of cattle also makes itdifficult and time consuming to collect the dung required for the digester. In general, theexpense and complexity of constructing and managing digesters coupled with theirrelatively low and unpredictable energy yields make them unattractive options in most ruralNamibian applications.

12 Issues and Options in the Energy Sector, Namibia

Renewable energy recommendations

3.49 The Namibian renewable energy sector appears to be in an unusually strongposition. Photovoltaics and wind are well developed and filling the niches for which theyare presently suited both effectively and competitively. The private sector is active andcompetent; it should continue to play the major role in renewable energy development.

3.50 This should be facilitated by increased government support. Within the MME,renewable energy sources are handled by the Research Section in the Electricity Division ofthe Directorate of Energy. The Section presently has a staff of two with the position ofhead unfilled. The mission feels that its present role could usefully be extended to includethe following:

3.51 Assembly and publication of meteorological data on wind and insolation. Thereare gaps in the available infornation, especially in the communal lands. It would be usefulfor renewable energy designers to have comprehensive and reliable data. This task wouldrequire liaison with the Meteorological Office and renewable energy suppliers anddesigners.

3.52 Assembly of data on renewable energy experience. This would primarily be basedon experience within the government sector but would incorporate available data from theprivate sector. It would provide a publicly accessible data bank, helping researchers avoidduplication and enabling them to build upon the results of previous work. The Sectioncould also act as a clearing house for small scale donor-funded projects in the renewablesarea

3.53 Conmissioning studies and pilot projects. The Section could identify gaps in theexisting knowledge and commission studies or pilot projects to obtain the necessaryinformation.

3.54 Raising awareness of renewable energy sources anong government decisionmakers. Awareness of the potential and limitations of renewable energy sources is stilllimited among many government decision makers. The Section could help raise the level ofawareness by providing general information and carrying out case studies of particularapplcations.

3.55 Setting performance and design standards for renewable energy equipment.Performance and design standards are necessary to protect consumers. The standardsshould be based upon those already accepted elsewhere, adapted where necessary forNamibian conditions. The standards should be set in conjunction with private sectorsuppliers, the Department of Trade and Industry and relevant professional and academicorganizations.

Issues and Options in the Energy Sector, Namibia 13

Wood and Charcoalfrom Brush Clearing

Charcoal making

3.56 Farmers also use brush wood for charcoal making. The charcoal is made in mildsteel vertical retorts 10-15 meters high built by farmers themselves to a local design. Theyoperate on a semi-continuous process and have a production of about 35-40 tons per monthof good quality charcoal. The yield is about one ton of charcoal per five tons of wood.The bulk of the charcoal is sold to the TCL mine at Tsumeb for ore smelting. Consumptionis about 500 tons per month and the mine pays R180 per ton.

3.57 A South African company is at present exploring the possibility of investing in asophisticated Lambiotte-type retort at a reputed cost of R36 million. This would have anannual output of about 16,000 tons of charcoal of sufficiently high quality to meet EuropeanCommunity import standards and would require a guaranteed supply of 80,000 tons ofwood per year. The resource availability and possible contractual arrangements forobtaining supplies from farmers are being examined.

3.58 Such a project, if it can be established, would bring a variety of benefits: increasedlocal employment, encouragement to farmers in their brush clearing, and export earnings.The investment decis3.54 Some 8-10 million hectares of grazing land are seriouslyaffected by brush encroachment in the center and north of the commercial farm areas. As aresult, the grazing area is reduced by up to 50%, with some places becoming completelyimpassable for livestock.

3.59 Clearing the brush from the encroached land is an extremely labor-intensive anddifficult operation but yields about 6 tons of wood per hectare. Wood production costs arein the range R45-65 per ton. The TCL mine at Tsumeb has provided a market of about3000 tons per month at a price of R65 per ton, though there have been serious problems inloading the fuel into the existing coal-fired boilers. While scarcely profitable in its ownright, the opportunity to sell the wood helps offset the heavy costs of brush clearing forfarmers.

3.60 The run down of Tsumeb mine has considerably reduced the market for boiler fuelbut similar quantities will be required when the new Kombat mine about 90 km fromTsumeb comes into production. Management of the mine is determined to resolve theloading problem so that local wood supplies can be used.ions must be left to the private sector, but the many potential benefits from the project makeit important that its implementation be encouragedi and facilitated as much as possible.

Rural Electrification

3.61 Rural electrification is an important element in the government's social and politicalpolicies aimed at redressing the long neglect of the communal lands under the previousadministration and directly assisting Namibia's rural poor. As presently carried out, itmainly involves the provision of grid extensions to selected rural centers, most of whichwere previously supplied by isolated diesel generators.

14 Issues and Options in the Energy Sector, Namibia

Rural electification policy

3.62 SWAWEK, according to its annual report, carries out rural electrification "whereverit is possible to do so and whenever funds are available". In practice, this appears to meanproviding rural electricity supplies wherever this meets normal commercial criteria. Whennon-commercial projects are carried out at the government's request, SWAWEK expects thecapital costs to be covered by a grant.

3.63 Priority is given to centers with existing government facilities such as schools,hospitals, police stations, clinics or administrative offices. The majority of these alreadyhave an electricity supply from isolated diesel sets provided and maintained by theDepartment of Works. These vary in capacity from units of 10-20 kW used to supplysmall schools and clinics through to 250 kW units for larger schools and hospitals. TheDepartment is responsible for a total of 450 units many of which are in poor condition. Theaverage estimated cost of the electricity supplied is RO.66 per kWh.

3.64 In carrying out rural electrification programs, SWAWEK acts only as a bulkelectricity supplier. The construction and management of the local distribution system is theresponsibility of the Ministry of Local Government and Housing (MLGH) and is generallycarried out with technical support from a consulting fimn. The MLGH purchases electricityfrom SWAWEK at RO.048/kWh and is responsible for setting its own retail tariffs. Theseare generally in the range RO.15-0.20/kWh and are heavily subsidized in the case ofsupplies from isolated diesel sets.

3.65 As rural electrification proceeds in the northern part of the country, the burden onthe MLGH is increasing. One of the options being considered as an alternative tostrengthening the MLGH capacities in the construction and management of localdistribution systems is the establishment of an autonomous electricity distribution authorityfor northern Narnibia.

3.66 The largest rural electrification program at present under way is in Owambo and isfunded by NORAD. Preliminary designs have been drawn up for further programs inKavango and Caprivi but no commitment of donor funds has yet been made for eitherprogram. In Kavango, certain distribution lines are already being built to supply centersalong the Okavango river west of Rundu. This work is funded by the government and isbeing undertaken without foreign assistance.

Owambo rural electrification program

3.67 An outline program for the electrification of 29 centers in Owambo was drawn upby the government in 1990. This was presented to NORAD which, following a study byconsultants, agreed to provide NK48.5 (about $8.Omillion) to fund the transmissionfacilities to be constructed by SWAWEK.

3.68 The SWAWEK component of the program consisted of 530 km of high voltage lineand associated transformers and was completed in early 1992, almost a year ahead ofschedule and with a saving of more than 25% of the project budget. Progress on the localdistribution system has, however, been slow with five centers completed by mid-May 1992and a further three half-completed. Arrangements are being made to transfer some of thesavings from the SWAWEK component to the MLGH to speed up the work on thedistribution systems.

Issues and Options in the Energy Sector, Namibia 15

3.69 As part of the program, two important innovations are being introduced. The first isa "Redi-board" incorporating a light and three socket outlets, from which extension cordscan be safely run to appliances and other rooms, making it unnecessary to hard-wire ahome. Domestic consumers are given an electronic pre-payment meter with which they payin advance for the electricity they use. They do this by purchasing from machines, locatedin local shops or other facilities, electronically coded cards available in sums ranging from afew Rand to a hundred or more. When inserted in their home meter these cards enable theconsumer to use the amount of electricity purchased. A display on the meter shows theamount of electricity available and indicates the rate of consumption.

3.70 No connection fees are charged, the cost of the connection and the meter being builtinto the retail tariff of R.0.20/kWh. The pre-payment meter also prevents consumers fromusing more electricity than they can afford at any time, while helping them to economize onelectricity costs by showing them visually how quickly they are using what they paid for.For the distributor, these meters have the advantage of eliminating meter reading, billing andcollection costs, and the problem of unpaid bills. They are being successfully used in theRSA, from which they are imported.

Rural electri:ficadon overview

3.71 The NORAD economic analysis of the Owambo program assumed a high growth inelectricity demand in all the centers. The benefits were calculated on the basis that, in theabsence of the program, the projected energy demand would be met 60% by dieselgenerated electricity at RO.70/kWh and 40% by bottled gas at R0.05/MJ (RI 10/kg). Underthese conditions and a 5% discount rate the project had a positive NPV over 20 years butnot with an 8% and 10% discount rate.

3.72 SWAWEK, however, is of the view that the NORAD demand forecasts areunrealistically high. But it also observes "..if a grant is received, the returns should be ableto cover the maintenance and direct operating costs as well as the generating and distributioncost of electricity. There should also be some money left over for a contribution towardsdepreciation and replacement."

3.73 The mission inclines towards the SWAWEK view of the demand forecast and feelsit is unlikely that the project, and others like it, can be justified on strict economic grounds.The primary justification for such projects will therefore tend to be social and political. Thisis entirely legitimate, particularly in view of the fact that the capital costs are clearlyidentified and separately funded (largely by foreign grants), but it leaves questions aboutwhether the expected social benefits are being realized.

3.74 The direct social benefits are, in fact, likely to be limited. The government facilities,in general, already have electricity and their functioning will not be substantially altered.However, they will benefit from more reliable power supply and the government will reapsubstantial fuel cost savings. Intemational experience generally indicates that the provisionof grid electricity is unlikely, in itself, to bring about economic development which wouldotherwise not occur. Furthermore, the number of domestic connections is also likely to below. Even if there is a high connection rate in the electrified centers themselves, the numberof households supplied will inevitably be a small proportion of the total population of theregion, which outside the few towns is widely dispersed.

16 Issues and Options in the Energy Sector, Namibia

Looking to thefuture

3.75 The future course of rural electrification is dependent in good measure on (i) thedevelopment of improved institutional arrangements to ensure that the construction andsubsequent management and expansion of rural distribution systems are effectively handledand (ii) whether the benefits of electrical service actually come to reach a substantial portionof the rural population. At present, there is considerable uncertainty on both scores. Tospeed completion of the Owambo project, the MME has taken over responsibility forconnecting consumers from the MLGH as a temporary measure. A more permanent fix ofthe institutional arrangements for power distribution is being planned but will depend, interalia, on the direction taken by the presently planned reform of local and municipalgovernment, which is still unclear. It is also still far too early to assess the rate at whichconsumers will be connected and the load will actually grow in Owambo.

3.76 The undoubted need to address the needs of long-neglected rural people should beweighed against these uncertainties about the actual economic and social impact of presentrural electrification programs. The mission believes that sound decisions about furthermajor investments in Owambo-like rural electrification programs will only be possible whenimproved institutional arrangements for distribution are in place and when the economicviability and social benefits of the Owambo program can be better evaluated.

3.77 While the administrative and population centers will remain a natural priority forgrid connections, to extend the social impact of rural electrification consideration of futureinvestments should address the question of how the more dispersed rural population that isnot within reach of the grid can also be provided with at least some of the benefits ofelectrification. It is unlikely that there is any uniform "solution" and that a multipleapproach will be the most effective. Among the initiatives which could usefully beconsidered are the promotion of:

* small photovoltaic systems for household lighting and radio;

* commercial battery charging systems using photovoltaics or small dieselgenerators;

* local community management of small supply systems.