uk protection - realising our potential - the … · go to slide master to edit / delete footer uk...

TRANSCRIPT

GO TO SLIDE MASTER TO EDIT / DELETE FOOTER

UK PROTECTION - REALISING OUR POTENTIAL

BRAVE IN A WORLD OF RISK

David Howell, CEO Pacific Life Re

Protection Review Conference; 15th July 2015

AGENDA

2

• UK Protection Market – global perspective

• Challenges, trends and opportunities

• Lessons from other markets

• Immediate priorities

GLOBAL PERSPECTIVEHow does the UK market compare?

3Which are the worlds biggest Protection markets?

UK PROTECTION MARKETBetter than you might think!

4

Probable “facts”

• UK 2nd largest individual protection market after US

• Australia largest for group protection and overall

market penetration

UK PROTECTION MARKETParticularly strong on consumer focus

5

UK Protection market – a world leader in:

• Competitive consumer prices

• Independent financial advice regime

• Protection of consumer interests

GO TO SLIDE MASTER TO EDIT / DELETE FOOTER

SO WHY ARE WE SO DEPRESSED?Challenges to healthy growth….

6

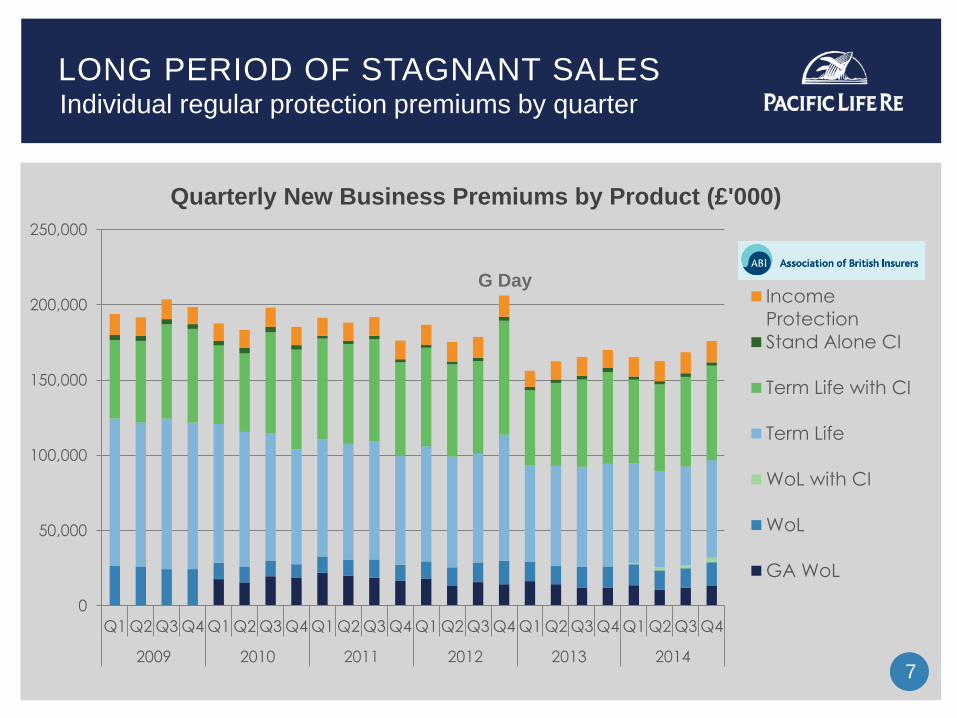

LONG PERIOD OF STAGNANT SALESIndividual regular protection premiums by quarter

7

0

50,000

100,000

150,000

200,000

250,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2009 2010 2011 2012 2013 2014

Quarterly New Business Premiums by Product (£'000)

Income

Protection

Stand Alone CI

Term Life with CI

Term Life

WoL with CI

WoL

GA WoL

G Day

WHAT’S DRIVING SALES TRENDS?Distribution mix

8

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1 Q2 Q3 Q4

2009 2010 2011 2012 2013 2014

Share of Regular New Protection Premiums

Pure Direct (Non Int. pre 2013)

Non Adv. - Intro / 3rd Party

Restriced - Single Tied

Restricted - Multi Tied

Restricted - WoM

Independent (IFA / WoM pre 2013)

Bank

WE NEED TO HELP ADVISERSSource of 70% of our business…

9

14%

41%

2%

5%

7%

9%

6%

8%

8%

2014 ABI Individual Life New Regular Premiums by Channel

Independent Advice Mortgage

Independent Advice Other

Restricted Advice - WoM All

Restricted Advice - Multi Tied Mortgage

Restricted Advice - Multi Tied Other

…make it easier for IFA’s to sell:

• Stable & proportionate regulation

• Improved tools to support advice

• Better conversion rates

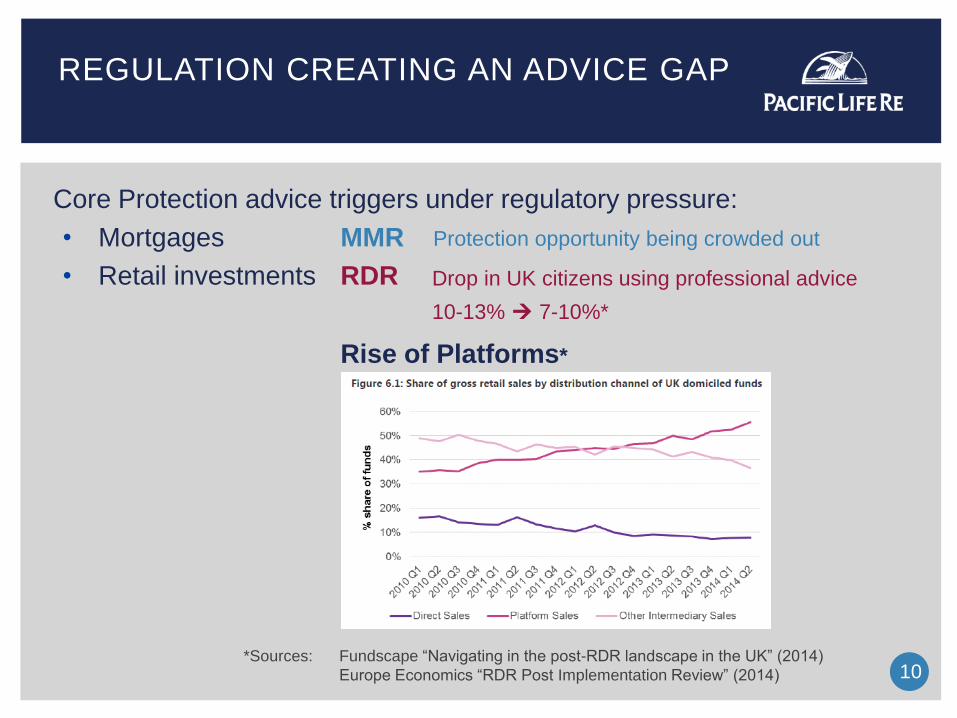

REGULATION CREATING AN ADVICE GAP

10

Core Protection advice triggers under regulatory pressure:

• Mortgages MMR

• Retail investments RDR

Rise of Platforms*

Drop in UK citizens using professional advice

10-13% 7-10%*

*Sources: Fundscape “Navigating in the post-RDR landscape in the UK” (2014)

Europe Economics “RDR Post Implementation Review” (2014)

Protection opportunity being crowded out

UK PROTECTION MARKET“D2C” channels are underdeveloped…

11

14%

41%

2%

5%

7%

9%

6%

8%

8%

2014 ABI Individual Life New Regular Premiums by Channel

Restricted Advice - Single Tied Mortgage

Restricted Advice - Single Tied Other

Non-advised - Introduced/3rd Party All

Non-advised - Pure Direct All

…establish new markets:

• Bank direct

• Auto-enrolment/worksite

• Creditor & general insurance

Substantial growth potential

UK LEADING WAY ON E-COMMERCE

12

UK in the vanguard

• High propensity to

buy on line

• Mobile digital

beginning to

dominate

*Sources: We Are Social

GlobalWebIndex

AUTO-ENROLMENT HAS BARELY STARTED

13

0

50,000

100,000

150,000

200,000

250,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2014/15 2015/16 2016/17 2017/18

tPR staging forecastsNumber of employer PAYE schemes by financial year

Medium employers50-249 people

Small & micro employersfewer than 50 people

New employers

Good progress to date*:

• Large employer staging

essentially complete

• Covers nearly 11,000

employers with over 15

million employees

• Over 3 million employees

auto-enrolled so far

More to come…

• DWP estimates of ultimate

impact of reforms: 8-9 million

extra employees saving

*Source: tPR 30 March 2014 data

Opportunity to provide easy access to protection cover

GO TO SLIDE MASTER TO EDIT / DELETE FOOTER

CAN WE LEARN FROM OTHER MARKETS?

14

LESSONS FROM AROUND THE WORLDAustralia

15

• Superannuation linked group protection cover was a great success

from 1980s through early 2000s

• Very high penetration means little anti-selection risk

• But lack of advice meant low customer understanding which

eventually ended in disaster

• Group market now correcting and likely to stabilise

• Retail (individual) segment may also grow from low base

LESSONS FROM AROUND THE WORLDUnited States

16

• Mainly a “preferred life” market supported by “invasive” underwriting

• Low penetration below high net worth / healthy segments

• Very different consumer regulation regime

• Much higher IP penetration than UK

LESSONS FROM AROUND THE WORLDAsia

17

• Seen as high growth potential

• Generally much more prolific in product innovation

• Direct sales have achieved high penetration in some markets

• Very different consumer regulation regimes

GO TO SLIDE MASTER TO EDIT / DELETE FOOTER

18

IMMEDIATE PRIORITIES

19

1. Help advisors sell

• Better tools & a regulatory reprieve!

2. Increased focus on D2C

• Capitalise on Auto Enrolment

• Simpler products clearly served-up that are “safe to buy”

3. Be realistic!

• Ours is a successful market with plenty of strengths to build on…

• … so please let’s stop beating ourselves up!

UK PROTECTION

Immediate priorities