©ufs the boomer opportunity: tapping the expertise of the metlife mature market institute® barbara...

TRANSCRIPT

©UFS

The Boomer Opportunity: Tapping the Expertise of the MetLife Mature Market Institute®

Barbara HowardGerontology ConsultantMetLife Mature Market InstituteMay 2006

2

“I get the ‘boomer’ part but I don’t get the ‘baby’ part.”

3

MetLife’s comprehensive resource on aging, retirement, and long-term care for MetLife and its business partners.

•Research & Polls•Public Education & Policy•Facts, Stats, Information•Training & Education•Consultation

www.maturemarketinstitute.com

Mature Market Institute

4

Media Leadership

• The Mature Market Institute positioned to provide Thought Leadership for MetLife

• Sponsored Retirement Income IQ media event to dispel myths and misconceptions about annuities

• Sponsored Long-Term Care IQ media event to dispel myths and misconceptions about long-term care

• Expert resource to major media resulting in coverage in the Wall Street Journal, the New York Times, CNN, ABC World News Tonight, and USA Today.

5

Today’s Presentation

Demographic Profile

Life Stages and Behaviors

Retirement and Beyond

How the MMI can help you

6

7

Meanwhile, outside the park

Two Stones tickets please, Senior Discount

8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5 15 25 35 45 55 65 75 85 95 100+

Millions

Age

BabyBoomers

Baby BoomersAs of 2006

Source: MetLife Mature Market Institute AnalysisPopulation Projections ProgramUS Census Bureau, 2000

Boomers are getting older …

9

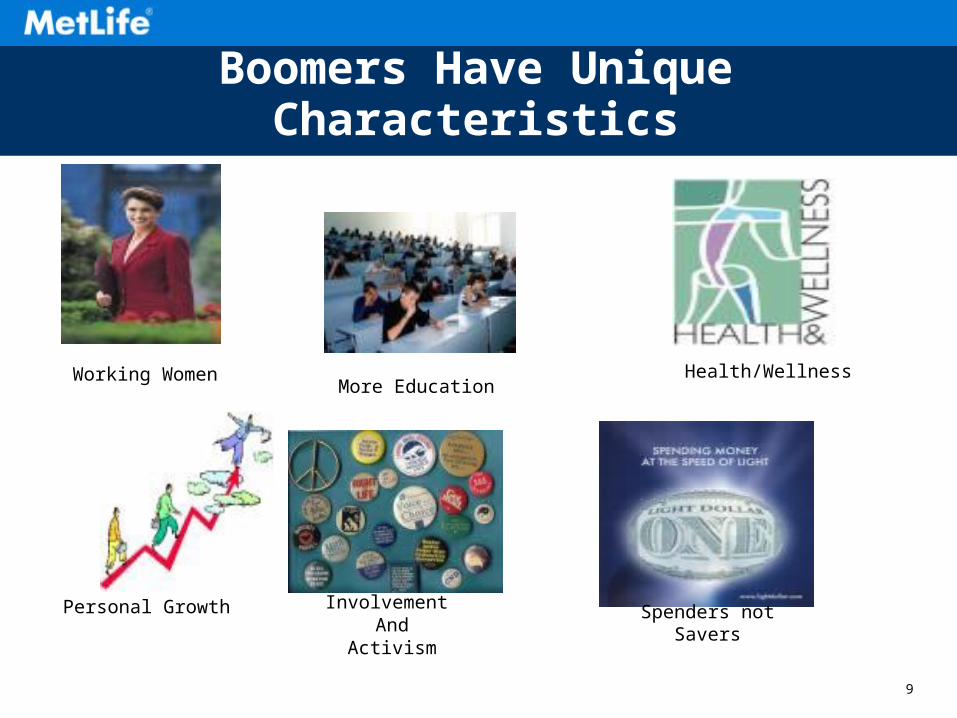

Boomers Have Unique Characteristics

Working WomenMore Education

Health/Wellness

Personal Growth Involvement And

ActivismSpenders not Savers

10

Boomer Formative Years

11

Longevity…The Greatest Risk

12

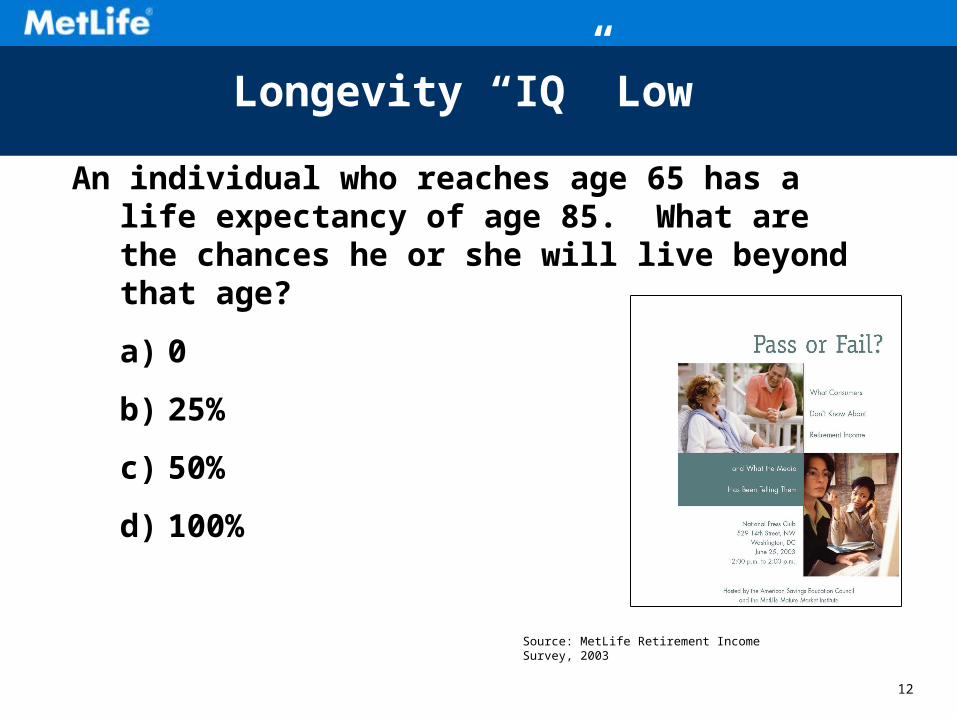

Longevity “IQ” Low

An individual who reaches age 65 has a life expectancy of age 85. What are the chances he or she will live beyond that age?

a) 0

b) 25%

c) 50%

d) 100%

Source: MetLife Retirement Income Survey, 2003

13

How do Boomers Feel about Retirement?

14

Boomers are Anxious About Retirement

• The number of boomers worried about retirement has almost doubled in four years.

• Younger boomers (41-49) are more likely to worry about retirement than older boomers (50-59) 39% vs. 30%

49%40%

19%

33%

LookForward toRetirement

Worry AboutRetirement

2001

2005

Source: The MetLife Survey of American Attitudes Toward Retirement: What’s Changed?, October 2005

15

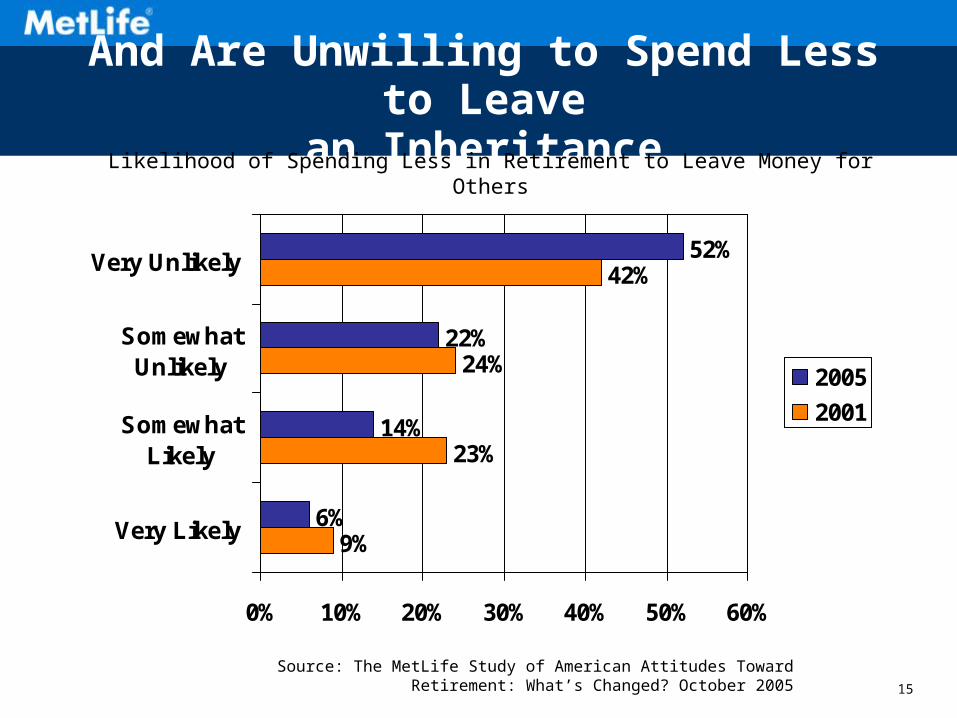

And Are Unwilling to Spend Less to Leave

an Inheritance

9%

23%

24%

42%

6%

14%

22%

52%

0% 10% 20% 30% 40% 50% 60%

Very Likely

SomewhatLikely

SomewhatUnlikely

Very Unlikely

2005

2001

Likelihood of Spending Less in Retirement to Leave Money for Others

Source: The MetLife Study of American Attitudes Toward Retirement: What’s Changed? October 2005

16

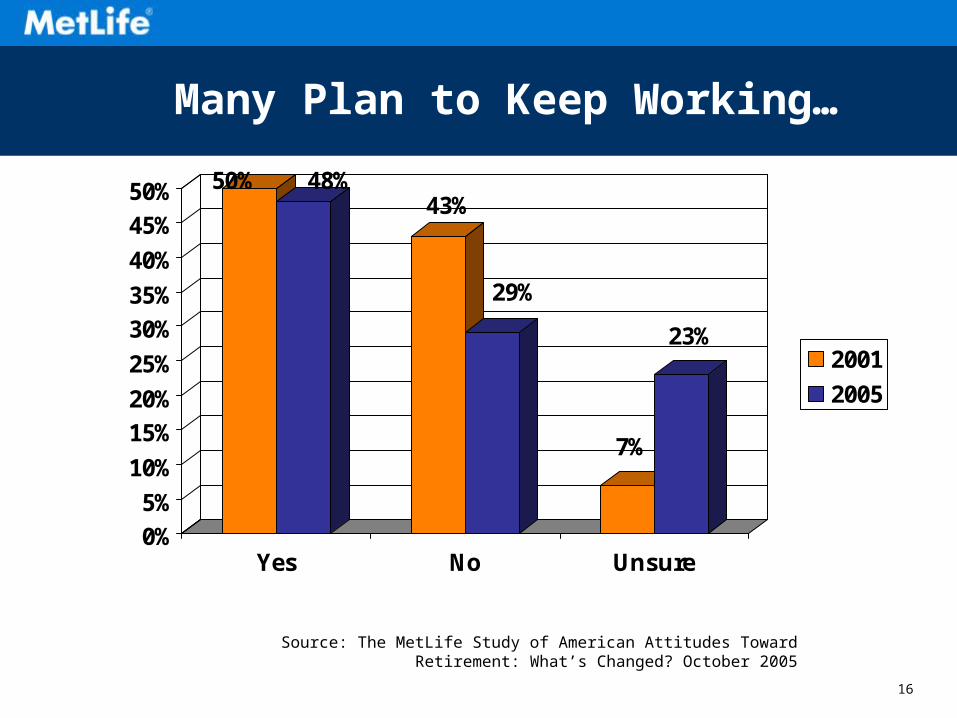

Many Plan to Keep Working…

50% 48%43%

29%

7%

23%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Yes No Unsure

2001

2005

Source: The MetLife Study of American Attitudes Toward Retirement: What’s Changed? October 2005

17

To Keep Active and for Financial Reasons

42%

19%

17%

17%

69%

44%

30%

23%

0% 20% 40% 60% 80%

Want to KeepActive

Need Income

MaintainLifestyle

Want extras

2005

2001

Source: The MetLife Study of American Attitudes Toward Retirement: What’s Changed? October 2005

18

Aging and Disability

Disabilities over Age 65 Prevalence of Alzheimer’s Disease

Source: U.S. Dept. of Health & Human Services, July 2002

Source: Survey of Income and Program Participation, U.S.Census Bureau, March 2001

54.5%

37.6%

16.7%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

% With AnyDisability

% With SevereDisability

% Need Assistance

47%

19%

3%

0%5%

10%15%20%25%30%35%40%45%50%

65-74 75-84 85+

19

Perspectives on Caregiving and Long-Term Care

20

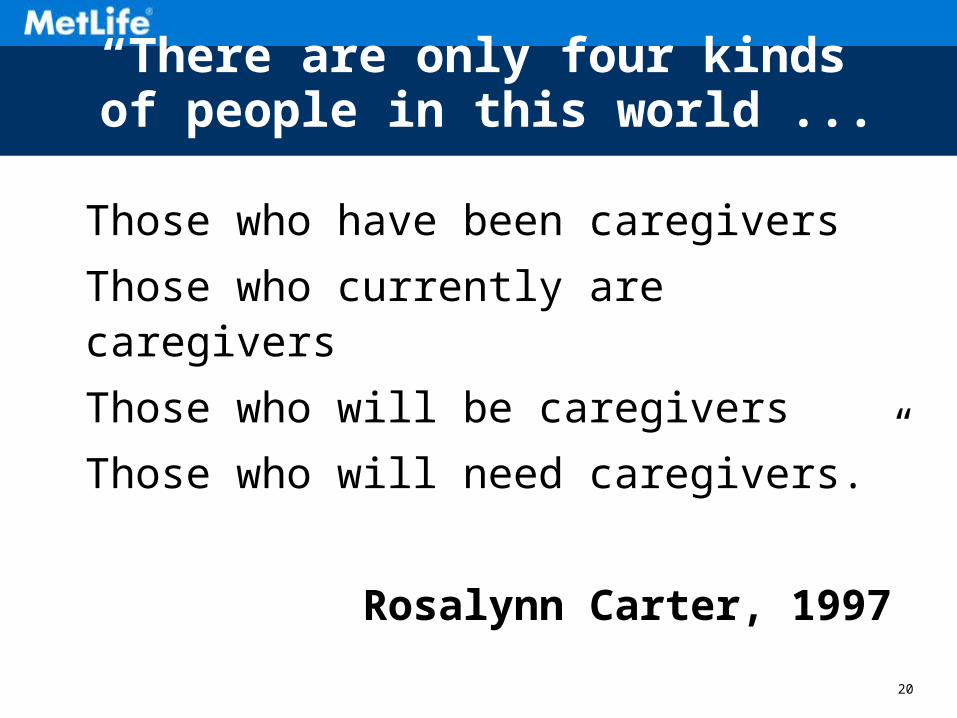

“There are only four kinds of people in this world ...

Those who have been caregivers

Those who currently are caregivers

Those who will be caregivers

Those who will need caregivers.”

Rosalynn Carter, 1997

21

Women are working

More divorces

Fewer or no children

Geographic separation

Care recipients living longer

Family Structures Have Changed

22

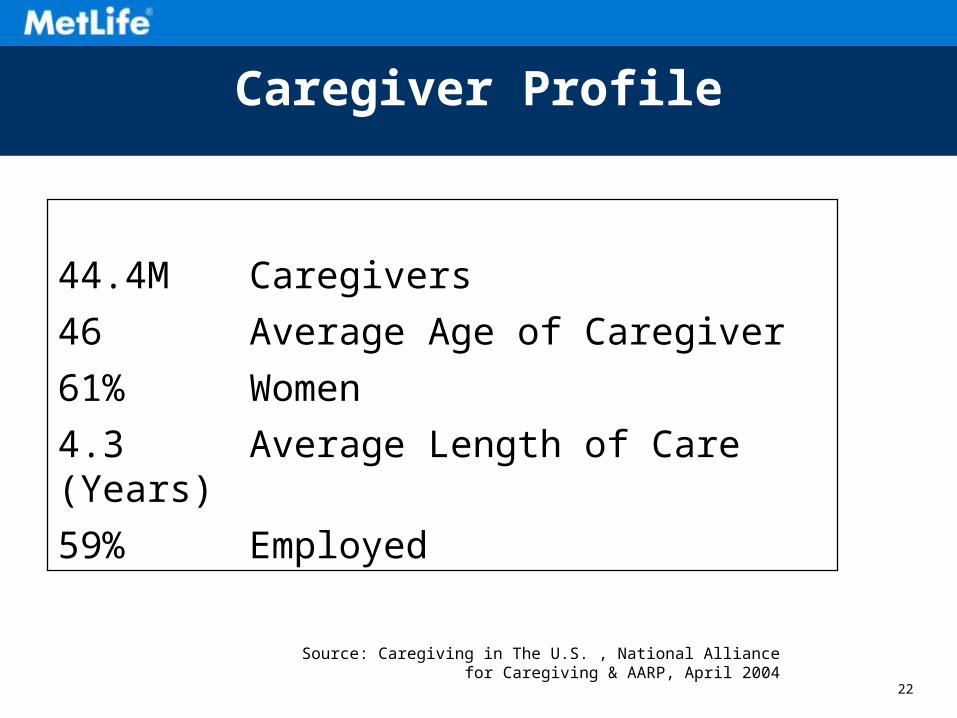

44.4M Caregivers

46 Average Age of Caregiver

61% Women

4.3 Average Length of Care (Years)

59% Employed

Source: Caregiving in The U.S. , National Alliance for Caregiving & AARP, April 2004

Caregiver Profile

23

•Annual Market Survey of Nursing Home, Home Care, and Assisted Living Costs

•Covers 87 major markets

Source: The MetLife Market Survey of Nursing Home & Home Care Costs, 2005, The MetLife Market Survey of Assisted Living Costs, 2005

24

2005 Major Findings•National average for a private room in a nursing home

•$203/day or $74,095 annually

•National average for a semi-private room in a nursing home•$176/day or $64,240 annually

•National average for a private room in an assisted Living facility

•$2,905/month or $34,860 annually

•Average hourly rate for Home Health Aid•$19/hour

•Average hourly rate for Homemaker/companion•$17/hour

Source: The MetLife Market Survey of Nursing Home & Home Care Costs, 2005, The MetLife Market Survey of Assisted Living Costs, 2005

25

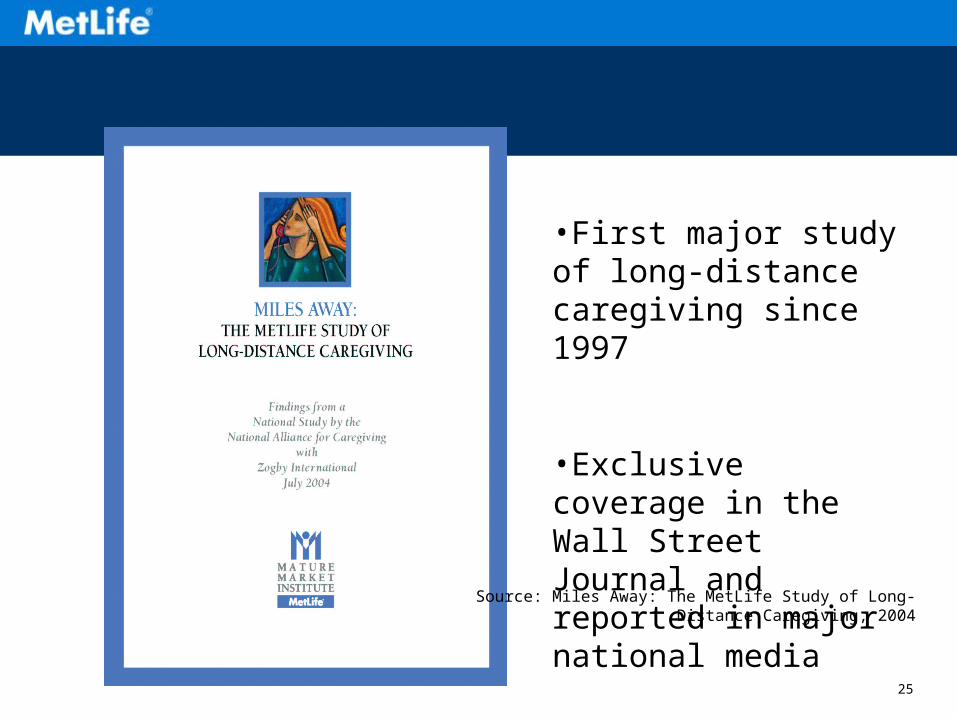

•First major study of long-distance caregiving since 1997

•Exclusive coverage in the Wall Street Journal and reported in major national media

Source: Miles Away: The MetLife Study of Long-Distance Caregiving, 2004

26

Miles AwayMajor Findings

•Caregivers live an average of 450 miles from care recipient and spend $392 monthly on travel and out-of-pocket expenses

•80% work either full or part-time

•44% rearrange work schedules

•36% miss days of work

•12% took a leave of absenceSource: Miles Away: The MetLife Study of Long-Distance Caregiving, 2004

27

Sons at WorkBalancing Employment and Eldercare

• Men are just as likely as women to be the primary caregiver

• Women perform more personal tasks than men

• Both men and women have little knowledge about company-sponsored programs

Source: The MetLife Study of Sons at Work, 2003

28

Study of Employed Caregivers: Does LTCI Make a Difference?

Employed caregivers of elders with LTCI are nearly twice as likely to stay in the workforce and have fewer social stresses

Source: The MetLife Study of Employed Caregivers: Does Long Term Care Insurance Make a Difference, 2001

29

30

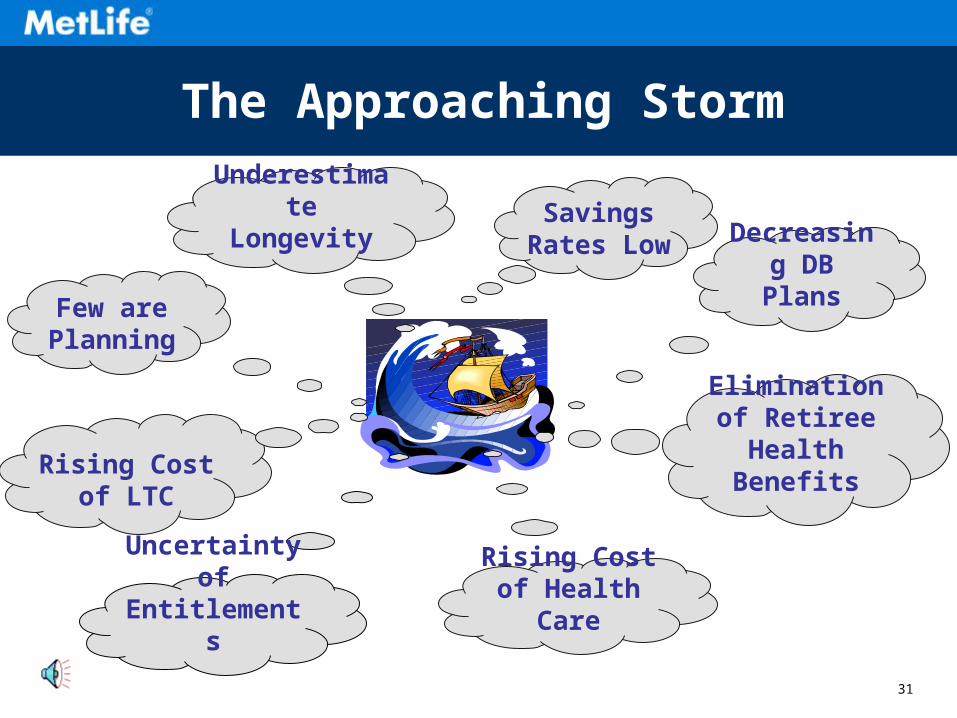

Retirement Looming on The Horizon

31

Savings Rates Low

Decreasing DB Plans

Elimination of Retiree Health

Benefits

Rising Cost of Health Care

Rising Cost of LTC

Few are Planning

Underestimate Longevity

The Approaching Storm

Uncertainty of Entitlements

32

Less than $25K

$25K - $49,999

$50K - $99,999

$100K - $249,999

$250K+

Retirement ReadinessBad News Savings Rates are Low

All

Workers

53

12

12

11

12

Ages

25-34

73

11

7

4

5

Ages

35-44

49

14

16

12

9

Ages

45-54

43

14

12

14

16

Ages

55+

43

8

12

11

26

L0408JHEC(0807)MLIC-LDAll figures are percentages. Source: EBRI, The 2006 Retirement Confidence Survey

33

Workers with Pension Coverage By Type Of Plan

0

10

20

30

40

50

60

Traditional DefinedBenefit Plan Only

Defined Contribution-401(k)-Only

Both

1981 1991 2001Source: U.S.Department of Labor (2002) and authors estimates based on Board of Governors, Survey of Consumer Finances (2001). From EBRI Issue Brief, January 2005

34

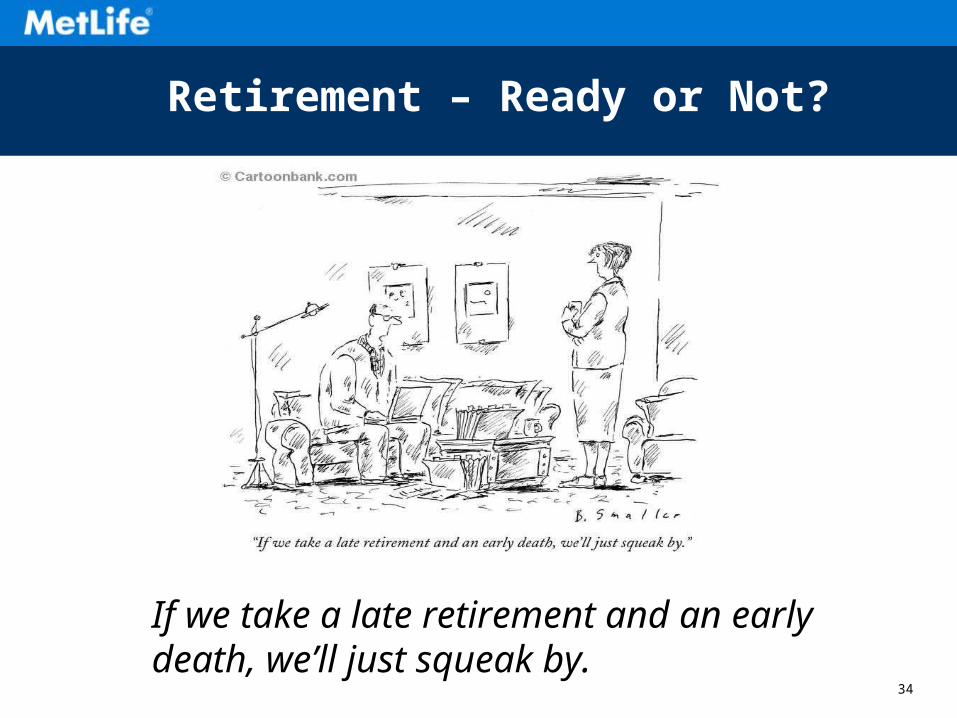

Retirement – Ready or Not?

If we take a late retirement and an early death, we’ll just squeak by.

35

Progress Toward Retirement Savings Goals

3%

24%

23%

22%

19%

9%

Already achievedgoals

On track for reachinggoals

Somewhat behind

Significantly behind

Haven't started

Don't have goals

Employee Perceptions of Progress Toward Retirement Savings Goals

Source: MetLife Employee Benefit Trends Study - 2004

36

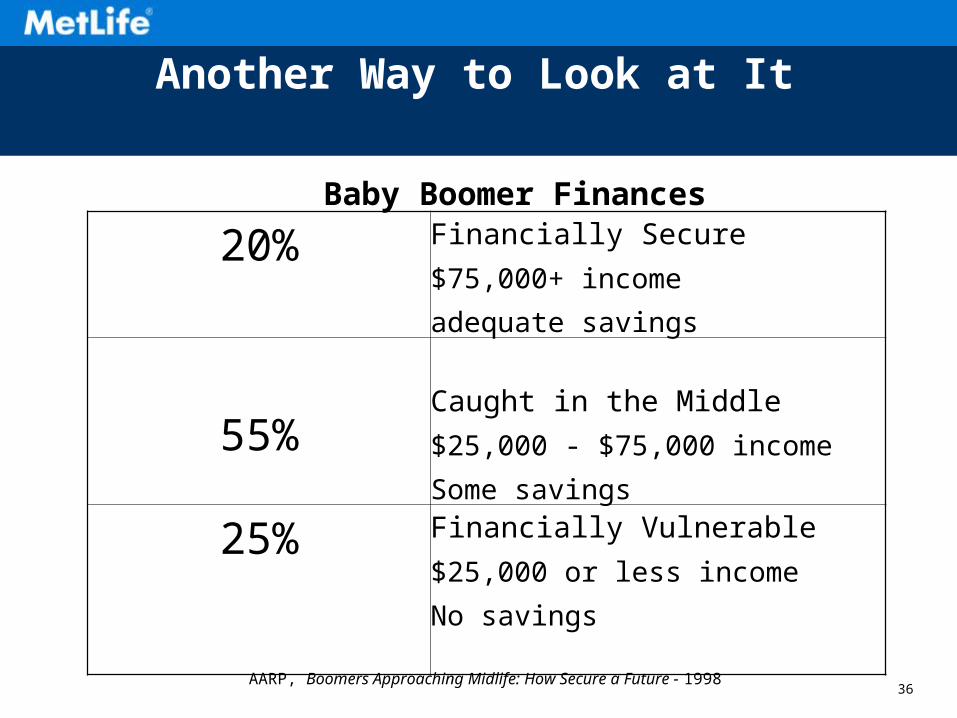

Another Way to Look at It

Source: AARP, Boomers Approaching Midlife: How Secure a Future:, 1998

20% Financially Secure

$75,000+ income

adequate savings

55%Caught in the Middle

$25,000 - $75,000 income

Some savings

25% Financially Vulnerable

$25,000 or less income

No savings

AARP, Boomers Approaching Midlife: How Secure a Future - 1998

Baby Boomer Finances

37

Glass Half Empty….Or Half Full

38

Boomer Window of Opportunity

Not yet retired

Better educated

Healthier

Interested in second careers

Not as concerned with leaving an inheritance

Assets in homes

Open to advice and assistance

39

Longevity Basics First

Income for life

Provide for spouse/dependents

Long-term care protection

Health care coverage

Legacy

40

The New Face of Aging

41

Barbara HowardMetLife Mature Market Institute

57 Greens Farms RoadWestport, CT 06880

(203) 454-5392Website

www.maturemarketinstitute.com

Metropolitan Life Insurance Company, New York, NYL06019SOI(exp0108)MLIC-LD