ubs investment summary, forecasts and sample portfolios€¦ · economic update global growth...

TRANSCRIPT

SPEAKER: George Boubouras, UBS

LOCATION: Melbourne

DATE: July 2012

ASX INVESTMENT TALKS

UBS Investment summary, forecasts and sample portfolios

DISCLAIMER: The views, opinions or recommendations of the presenters are solely their own and

do not in any way reflect the views, opinions, recommendations, of ASX Limited ABN 98 008 624 691

and its related bodies corporate (“ASX”). Information and material presented at the seminar is for

educational purposes only and does not constitute financial product advice. Investors should obtain

independent advice from an Australian financial services licensee before making investment decisions.

No responsibility is accepted by ASX for any loss or damage arising in any way (including due to

negligence) from anyone acting or refraining from acting as a result of this information or material.

© Copyright 2012 ASX Operations Pty Limited ABN 42 004 523 782. All rights reserved 2012.

UBS Investment summary, forecasts

and sample portfolios

- Cautious stance recommended for the

September quarter

July 2012

ASX Investment talks

George Boubouras

Head of Investment Strategy & Consulting

Email: [email protected]

ASX Investment talks George Boubouras provides us with a sense of perspective on the current status of domestic and global markets. George argues that whilst we should diversify across sectors and within sectors, the profile we choose for our investment portfolio depends on individual risk appetite. George presents a range of options for our investment portfolios and concludes by sharing some of UBS’s sample portfolios such as defensive and aggressive dividend optimisation.

2

3

Table of contents

SECTION 1 Investment Summary and Forecasts 2

SECTION 2 Market Macro & Risk Indicators 4

SECTION 3 Interest Rates & Credit 10

SECTION 4 Commodity Market & Australian Dollar 15

SECTION 5 Equity Market Indicators 21

SECTION 6 Domestic (& Global) Stock Picks, Bond & Hybrid Portfolios 30

SECTION 7 Portfolio Construction Themes 49

SECTION 8 Behavioural Finance Implications 56

SECTION 9 Summary 59

SECTION 1

Investment Summary

5

One Page Summary: Core theme for H2 2012 => cautiously

optimistic

Economic Update

Global growth forecasts revised lower to 2.8% (from 3.0%) for 2012 following softer data profile in recent months. No hard landing in China,

recent data consolidated following a softer phase. Significant capacity to stimulate further. Domestic demand and infrastructure to be a larger

driver of China activity going forward. Overall, composition of global growth will remain very uneven. Emerging economies will continue to be

large growth drivers. European progress is a positive in June. There is a blueprint but markets require more detail. ECB has capacity to

stimulate further. The US data profile slowing. Anticipate slower earnings growth in Q3 therefore additional stimulus required.

Asset Allocation Strategy

Our Core Model Portfolios for Conservative/Moderate/Aggressive risk profiles remain neutral both domestic & international equities vs strategic

benchmarks. Within our global equity allocation we remain overweight the US and Emerging Markets, underweight Europe, UK and Japan.

Neutral fixed income (underweight sovereign, short duration & strong focus on quality credit). Underweight A-REITs & Alternatives. Overweight

Cash remains. Defensives are doing what they should.

Equities

Neutral allocation to equities vs benchmarks with a focus on defensives and dividend strategy for conservative through to increased exposure

towards cyclicals for more aggressive risk appetite. Australian equities will benefit from further rate cuts. US earnings have grown more vs

expectations in recent quarters and are robust vs other developed markets. However recent run of softer data will imply a slower earnings growth

profile in H2 2012. While equity valuations remain discounted on most measures (1 year forward P/E, trailing PE, P/B, Earning Yield vs

Bond) there are ongoing macro risks. Investor confidence is set to remain challenged. Year-end ASX200 target 4450. Your risk appetite drives

your strategy.

Cash & Fixed Income

Cash rate futures now pricing in 2.75% by March 2013. Very stimulatory and below GFC levels. We expect 3.0%-3.25% to be low in current

cycle. Neutral tactical tilt for fixed income vs strategic benchmarks with a focus on quality investment grade corporate bonds. We prefer

shorter duration positions. For more aggressive investors, higher yielding emphasis is recommended (in local & non-AUD). Ranking in the

capital structure to reflect risk appetite. Further, some listed higher yielding hybrids offer attractive yields. A diversified approach always

recommended. UBS Composite Bond Index up 12.41% annually illustrating that fixed income is a defensive asset class.

Commodities & Australian Dollar

Ongoing weakness anticipated in the Sept quarter with higher volatility in broad commodity prices to persist. Energy price correction has been

aggressive. No catalyst for sharp rise in energy prices in July. Commodity currencies impacted with weaker commodity prices. AUD forecast

unchanged vs last month, 0.97, 1.00 and 1.05 for 3, 6 and 12-months respectively. Despite softer recent commodity profile the AUD has seen

some support via global investor demand for Australian government debt.

Please see important disclaimer and disclosures at the end of the document.

SECTION 3

Market Macro & Risk Indicators

7

Global growth revised higher vs late 2011 but marginally lower over past few months. The growth premia

from the emerging economies has been the core global growth driver of economic activity and therefore

earnings. Growth is uneven by region but now expanding at a slower pace.

Global growth pulse slowing. Expect slower earnings growth in Q3

(6.0)

(4.0)

(2.0)

0.0

2.0

4.0

6.0

8.0

10.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E

World Developed Economies Developing/Emerging Economies

Source: UBS

Forecasts

Global Grow th Composit ion. Developed vs Developing Economies Real GDP, Annual %. World growth compared to Developed and Developing Economies

8

Market volatility lower in late June as the full catastrophe was averted…

Investors with moderate risk profile balanced funds would have had a positive financial year performance.

Rule of thumb => investors should expect volatility is a normal event. Excessive volatility is not. Greek

elections, Spanish banking loans and EU Summit were all positive vs expectations. Hence volatility finished

the month lower. But it will rise again therefore understand your risk appetite…

0

10

20

30

40

50

60

70

80

90

Jan-90 Jan-92 Jan-94 Jan-96 Jan-98 Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12

M arket Volat ility (VIX) IndexImplied Volatility Index, daily data

Source: Bloomberg, CBOT, UBS WM

Asia Crisis

LTCM Global Balance Sheet Recession

Enron & WorldCom

default

Period of decreased volat ility as

leverage is increased

Credit Crunch

Global Bond &

Equity Bear M arket

Mexian Peso

Crisis

* Data as of 29 June 2012

Sovereign

Debt issues,

growth

concerns...

Japan

Tragedy

Market volatility

low

9

Terms of Trade since 1870 – supportive structurally… Australian Terms-of-Trade (ToT) simply reflects our report card vs the world over the long run. Australia is a

small, open economy that is effectively a net energy/soft commodity exporter. We are in the middle of a

super cycle of mining CAPEX investment – which looks set to continue – but there will be short term

volatility along the way. Therefore, investors need to be conditioned for short term volatile cycles.

60

70

80

90

100

110

120

130

140

150

160

170

180

190

200

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020

60

70

80

90

100

110

120

130

140

150

160

170

180

190

200

Average since 1870* Terms of trade*

Index: average 1870 to 2010 = 100

* Goods only pre 1959; Goods & services post 1959

Terms of Trade - Australia

Source: UBS

1920's soft

commodity boom

Wool boom - Korean War

Bulk, metals,

energy, precious

metals, soft

commodity

boom

10

Aussie household still not happy => recent rate cuts having limited impact…

A reading above 100 implies optimism, below 100 indicates pessimism. Rebound in the May Consumer

Sentiment Index following May rate cut did not occur. Clearly more rate cuts required…

60

70

80

90

100

110

120

130

140

Jul-78 Jul-80 Jul-82 Jul-84 Jul-86 Jul-88 Jul-90 Jul-92 Jul-94 Jul-96 Jul-98 Jul-00 Jul-02 Jul-04 Jul-06 Jul-08 Jul-10 Jul-12

Consumer Sentiment Index, Australia Index above 100 = optimistic

Source: Melbourne Institute, UBS Wealth Management

Last recession in Australia Weaker credit conditions reflects the

household is going through some challenges.

11

Cash rates falling but cash weightings for investors remain high

Cash weightings remain high vs long run historical Superannuation (outside of Life Offices). Australian

households are improving their balance sheet (lower debt levels, decreased consumption and saving more).

Most Super Funds have a large overweight to their Cash Benchmark. Most are looking for opportunity to go

overweight equities…

10%

15%

20%

25%

30%

Jun-88 Jun-90 Jun-92 Jun-94 Jun-96 Jun-98 Jun-00 Jun-02 Jun-04 Jun-06 Jun-08 Jun-10 Jun-12

long run average

Cash Weighting - Australian Superannuation Quarterly data*

Source: ABS, RBA, UBS WM * Data up to 31 March 2012 (June quarter 2012 estimate). Superannuation weightings outside of Life Offices.

Investor caution

persists - cash

weighting remains

above average

SECTION 4

Interest Rates & Credit

13

Futures market now pricing in 2.80% by year end…

The 30 day interbank cash rate futures forward curve is higher in yield over past month. The Dec 2012 rate

has moved from 2.25% to 2.80%. Therefore implies 2.75% by year end in now the market target, still under

GFC lows. Target remains ambitious. We are still targeting a 3.0%-3.25% Cash Rate as a low in current

cycle...

0

1

2

3

4

5

6

7

8

9

10

Jun-92 Jun-94 Jun-96 Jun-98 Jun-00 Jun-02 Jun-04 Jun-06 Jun-08 Jun-10 Jun-12

30 day Cash Futures Official RBA Cash Rate

Source: ASX, Bloomberg, UBS WM

Off icial RBA Cash Rate and Implied Cash Futures Curve %, Monthly Data

Futures market now pricing in 2.75%

cash rate by year end

Cash

Rate

Futures

Curve*

* Cash rate futures curve as of 29 June 2012

Actual

14

Bonds are a defensive asset class with low correlation to equities. Chart shows rolling 12-month returns. It

clearly illustrates bonds out-performing in the GFC & in 2011. The 1-year return for the bond index is now

12.4%. Expected return for a diversified bond portfolio is 6.0-6.5% p.a. on average through a cycle…

Bonds belong in all portfolios => the classic traditional defensive asset class…

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Jun-92 Jun-94 Jun-96 Jun-98 Jun-00 Jun-02 Jun-04 Jun-06 Jun-08 Jun-10 Jun-12

Expected return Rolling 12-month return, %

UBS Composite Bond Index Rolling 12-month returns Monthlty Data

Bonds out-performed in

the GFC. It is a defensive

asset class

Source: UBS WM

Bonds are

defensive

15

Australian credit spreads improve

The Australian Markit iTraxx Index shows 25 equally weighted CDS spreads for Australian investment grade

companies. Core corporate balance sheet remains sound vs pre-GFC but global macro risks dominate. The

worst of the European Credit Crunch (in 2011) looks to be behind us but there are challenges ahead. Focus

on quality debt and the ranking in the capital structure should reflect your risk appetite.

0

50

100

150

200

250

300

350

400

450

500

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

Australian Credit Spreads - M arkit iTraxx Index Daily Data, Basis Points

Source: Bloomberg, Markit iTraxx, ASX, USB WM * Daily data as of 2 July 2012

2011 European

Credit Crunch behind

us?

The GFC was

unforgiving

16

US long bond yields to remain low for now…

Decoupling re bonds & equities. The US long bond at 1.55% with inflation around 2.0% implies negative real

10-year bond yields. Earnings yields looks more compelling vs bond yields…

0

2

4

6

8

10

12

14

16

18

Jan-19 Jan-26 Jan-33 Jan-40 Jan-47 Jan-54 Jan-61 Jan-68 Jan-75 Jan-82 Jan-89 Jan-96 Jan-03 Jan-10

US 10 Year Bond Yield Monthly Data, Jan 1919 through to present (%)

Source: Bloomberg, Global Financial Data Inc, UBS WM

LR mthly average Jan 1919 through to present: 5.08%

* Data as of 30 June 2012

Inflation Era

SECTION 5

Commodity Markets & the Australian Dollar

18

Commodity cycle weakness to continue in Q3…

Australia is a small open economy, a net energy/commodity, food exporter. In the shorter term weaker

commodity prices to continue but some consolidation in the Sept quarter. Longer term the structural cycle (ie

ToT) positive for global commodity currencies (AUD, NZD, BZL, NOK, ZAR..)…

0

20

40

60

80

100

120

140

160

Jun-86 Jun-88 Jun-90 Jun-92 Jun-94 Jun-96 Jun-98 Jun-00 Jun-02 Jun-04 Jun-06 Jun-08 Jun-10 Jun-12

RBA Commodity Prices (All Items )

Source: RBA Bulletin, UBS Wealth Management

RBA Commodity Index - All Items, SDR Terms

Emerging world contributing increasingly to

global growth (nearly 10 years now) underpins

commodity prices. Prices remain well above

past 30 year average

Long Run Average

19

AUD holding up as global investors buy Aussie bonds…

Commodities structurally well supported (but volatile), higher relative Aussie cash rates, AAA rated status of

Australia remain supportive for AUD. Any further spike in market volatility & signs of US recovery will be a

negative for AUD. Negative real yields in the US supportive for commodities therefore underpin commodity

currencies over the longer term but volatility (& weaker commodity prices) in shorter term…

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

Jun-86 Jun-88 Jun-90 Jun-92 Jun-94 Jun-96 Jun-98 Jun-00 Jun-02 Jun-04 Jun-06 Jun-08 Jun-10 Jun-12

120

160

200

240

280

320

360

400

440

480

AUD, LHS CRB Index, RHS

AUD & Commodity Prices (CRB* ) AUD CRB Index

Source: Bloomberg, RBA Bulletin, UBS WM

* Commodity Research Bureau (CRB) Index includes Grains, Soft

Commodities, Energy, Industrials, Precious Metals & Livestock

20

Gold prices consolidated June. There was some price

recovery as markets considered possibility of QE3.

Forecast remains bearish in the next 3 months but more

bullish on a 12-month outlook. Higher gold supply in

March quarter 2012 which was in line with market

expectations. Catalyst in July for a spike in prices will

be further central bank intervention or prospect of

further QE in September quarter (not our core view).

Gold: still remain bearish 3-months & bullish 12-months

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Jun-06 Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 May-

Gold - Spot 55-Day MA 200-Day MA

Gold Price USD/Ounce, Daily Data

Source: Bloomberg, UBS WM * Data to 30 June 2012

Gold Price and Forecast (USD/Ounce)

Spot* 1,558

3-Month Futures Contract* 1,560

3-Month Forecast Bearish 1,520

12-Month Forecast Bullish 1,820

Source: UBS WMR, Bloomberg. * 30 June 2012

21

Weaker energy prices on growth concerns, will continue in July…

Weaker demand, higher supply combined

with rising inventories => lower short-term

trading ranges for the Sept quarter. In

general global growth needs to be revised

higher as a catalyst for energy prices to

move higher. WTI is heading towards the

$70-$80 USD/BBL band with Brent remaining

around the US$10-15 premium.

Forecast for Brent is $80-$99 USD/BBL for 3-

month trading range. 12-month forecast $110

USD/BBL.

0

25

50

75

100

125

150

Jun-00 Jun-01 Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

Oil Spot Price - West Texas Intermediate (WTI) USD/Barrel. Weekly Data

Source: Bloomberg, UBS WM

Ideal oil price range as identified by

OPEC's largest producer

* Data up to 30 June 2012

0

2

4

6

8

10

12

14

16

Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Natural Gas - NYM EX Futures Contract 10,000m Thermal Units (mmBtu). Weekly Data

Source: Bloomberg, UBS WM

Natural gas accounts for almost a

quarter of US energy consumption

Higher US inventories

+ LNG alternative

options not enough to

drive a strong rebound

despite recent

production cuts

* Data up to 30 June 2012

0

100

200

300

400

500

600

700

800

Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Energy 3-M onth Forw ard Commodity Index Index. Jan 1996 = 100. Weekly Data

Source: Bloomberg

* Bloomberg 3-Month Forward

Global Energy Index

* Data up to 30 June 2012

22

No major catalyst for bulk prices to accelerate in short term…

Iron ore spot prices not as cyclical (or as volatile) as base metals. China 5 year plan will be more sustainable

pro-growth outlook. Demand for bulk commodities remains structurally strong, but shorter term more

volatile. Further, iron ore does not only come from the Pilbara region. The marginal CAPEX dollar for bulks

can (& is) going elsewhere. Ultimately, Australia will always be a price taker re commodity exports…

0

25

50

75

100

125

150

175

200

225

Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12

Source: Bloomberg, The Steel Index (TSI), UBS WM

Iron Ore Prices - China Import Fines 62% Fe spot USD/metric tonne, Tianjin port. Daily data

Price index is volume weighted average of transaction spot

* Data up to 30 June 2012

SECTION 6

Equity Market Indicators

24

US valuations not expensive

Simple US equity market multiples show valuations not very demanding vs. historical benchmarks. US

earnings recovery has been strong year-to-date but anticipate slower earnings growth in H2 2012. Limited

multiple expansion in current cycle. Current market correction challenging investor confidence. On balance,

reward for risk remains compelling over the cycle…

8.0

10.7

13.3

16.0

18.7

21.3

24.0

26.7

Jun-94 Jun-96 Jun-98 Jun-00 Jun-02 Jun-04 Jun-06 Jun-08 Jun-10 Jun-12

5-year average

Long run average

Market valuations - forward P/E

Source: Bloomberg, IBES, UBS WM

US Equity Valuat ions: S&P 500 1 Year Forward P/E. I/B/E/S. End-month Data

recent 5-year

average

25

S&P 500 Earnings Yield vs Credit Yield – Mind the Gap

The correlation between the S&P 500 earnings yield & corporate (Baa) bond index historically high until GFC.

Current Baa index yield suggests P/E should be greater than 16.0x – not the current 12.2x. Earnings

momentum will slow in 2012 vs 2011 but gap “should” converge further by year-end (non linear of course).

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

Baa Index Yield S&P 500 Earnings Yield

Source: Bloomberg, Moodys, IBES, UBS WM

S&P 500 Earnings Yield vs Credit Yield (Baa)End-month Data

Mind the Gap - Correlation between earning yield

& credit yield has remained high over time. Recent

years the breakdown in relationship an

opportunity to accumulate risk. Current credit

spreads indicate a "higher" multiple vs current.

The Gap remains wide!

26

US equities earnings yield remains attractive vs long bonds

US Equity earnings yield vs bond yield remains attractive. Quality large cap defensives that offer sustainable

dividends look relatively attractive vs long bonds. However, long bonds look set to remain expensive for now

as global stimulus is expected to continue. Equity investors will continue to focus on a dividend strategy…

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

Jun-92 Jun-94 Jun-96 Jun-98 Jun-00 Jun-02 Jun-04 Jun-06 Jun-08 Jun-10 Jun-12

US Bond Yield - Earnings Yield Ratio

Equit ies less attract ive

Equit ies more attract ive

Source: Bloomberg, Datastream, IBES, UBS WM

+/- 1 std dev from rolling 3yr mean

IBES 1 Year Forw ard P/E

Bonds expensive vs earning yields

27

Aust equity market valuations remain compelling

Multiple shows Australian equity valuations cheap on a 12-month forward estimate. Australian market offers

value. Dividend strategy has delivered. Recent rates cuts a positive for earnings in second half 2012…

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

Jun-94 Jun-96 Jun-98 Jun-00 Jun-02 Jun-04 Jun-06 Jun-08 Jun-10 Jun-12

5-year average

Long run average

Market valuations - forward P/E

Source: Bloomberg, IBES, UBS WM

ASX 200 12 M onth Forw ard P/E Ratio 1 Year Forward P/E. I/B/E/S. End-month Data

28

Earnings yield remains attractive vs bond yields…

Australian Bond Yield vs. Earnings Yield (BY/EY) ratio suggests that the forward earnings yield remains

attractive vs bond yields. Bonds yields however look set to remain low in the coming months. Further,

discount rate falling. Supportive for equities, particularly income focused stocks initially…

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Jun-92 Jun-94 Jun-96 Jun-98 Jun-00 Jun-02 Jun-04 Jun-06 Jun-08 Jun-10 Jun-12

Australian Bond Yield - Earnings Yield Ratio

Equit ies less attract ive

Equit ies more attract ive

Source: Bloomberg, Datastream, IBES, UBS WM

+/- 1 std dev from rolling 3yr mean

1 Year Forw ard P/E

As bond yields fall Aussie Equities remain cheap vs bonds

29

Australian equity market dividend yield compelling vs cash

Lower cash rate => quality dividends become more compelling. Dividend yield becoming more attractive vs

cash rates in 2012. Franking a key contributor for the local market. Investors should target a 6.0-7.0% (before

franking) yield for a large cap income equity portfolio…

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

Dividend Yield Grossed-up Dividend Yield RBA Cash Rate

ASX 200 Dividend Yield & Cash Rate %, Monthly Data

Source: Bloomberg, IRESS, RBA Bulletin, UBS WM

Mind the Gap. Cash rate

below the dividend &

looks set to remain so for

some time

30

Australian equity market dividend yield vs bond yields

Lower bond rates => quality dividends become more compelling. Dividend yield remains compelling vs bond

yields. Franking a key contributor for the local market. Investors should target a 6.0-7.0% (before franking)

yield for a large cap income equity portfolio. Focus on a quality dividend targeting equity portfolio…

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

Dividend Yield Grossed-up Dividend Yield 10 Year Bond Yield

ASX 200 Dividend Yield & Bond Yield %, Monthly Data

Source: Bloomberg, IRESS, RBA Bulletin, UBS Wealth Management

long bond yields look

set to remain lower in

the short run

31

Australian equity market performance over the long run

Year-to-date total return marginally positive (up 2.86% as of 30 June). The dividend has been a large

contributor. Australian equity market averages a negative annual return once every 3.4 years in the past 50

years. Annual expected returns going forward for domestic equities are around 10.0%. This does not include

franking. Can you handle negative returns through your lifecycle? If not => diversify…

-60%

-40%

-20%

0%

20%

40%

60%

80%

1958 1964 1970 1976 1982 1988 1994 2000 2006 2012

All Ordinaries Accumulat ion Index - Annual Performance

Source: Bloomberg, Datastream, RBA Bulletin, UBS WM Australia * Accumulation data. 2012 reading is data as of 30 June (YTD%)

Long-run average

More rate cuts

required to drive

market higher

SECTION 7.1

Sample equity portfolios & metrics

33

Australian Core Equity Portfolio

Aims of the Australian Core Equity Portfolio

For investors looking for a balanced, blue-chip core Australian portfolio, UBS WM offers the Australian Core Equity Portfolio. This

Portfolio gives the starting investments for every Australian portfolio.

When determining companies to add to the Australian Core Equity Portfolio, some of the metrics we consider include :

Potential for long term outperformance, and a history of stable growth and income distribution

A beta close to the market beta

Generally, the company should have a large market capitalisation, and companies on should be part of the ASX 50 index

The company must carry either a Buy or Neutral rating from UBS IB

The Australian Core Equity Portfolio

Source: UBS, Iress. Prices as at 29 June 2012.

Code Company Sector Market

Price UBS Rating

UBS Price

Target

Upside

/Downside P/E 12e Yield 12e %

Franking %

12e

Grossed

Up Yield

12e %

Market

Cap ($m)

AMP AMP Financials 3.85 Neutral 4.15 7.8% 12.1 6.36 0 6.36 10,990

BHP BHP Billiton Limited Materials 31.45 Buy 47.00 49.4% 9.7 3.39 100 4.84 167,408

CBA Commonwealth Bank Financials 53.10 Buy 53.50 0.8% 12.2 6.14 100 8.77 83,966

NAB National Australia Bank Financials 23.54 Neutral 24.50 4.1% 9.4 7.73 100 11.05 52,713

ORG Origin Energy Energy 12.20 Buy 17.00 39.3% 14.9 4.10 100 5.85 13,251

RIO Rio Tinto Limited Materials 56.50 Buy 103.00 82.3% 8.3 2.90 100 4.15 104,422

TCL Transurban Group Industrials 5.69 Buy 6.25 9.8% 50.9 5.18 24 5.58 8,049

TLS Telstra Corporation Limited Telecoms 3.69 Buy 4.00 8.4% 12.8 7.59 100 10.84 45,915

WOW Woolworths Limited Consumer Staples 26.80 Buy 28.00 4.5% 15.0 4.66 100 6.66 32,935

WPL Woodside Petroleum Limited Energy 31.02 Buy 43.05 38.8% 13.4 3.73 100 5.33 24,992

Average Yield: 5.18 6.94

34

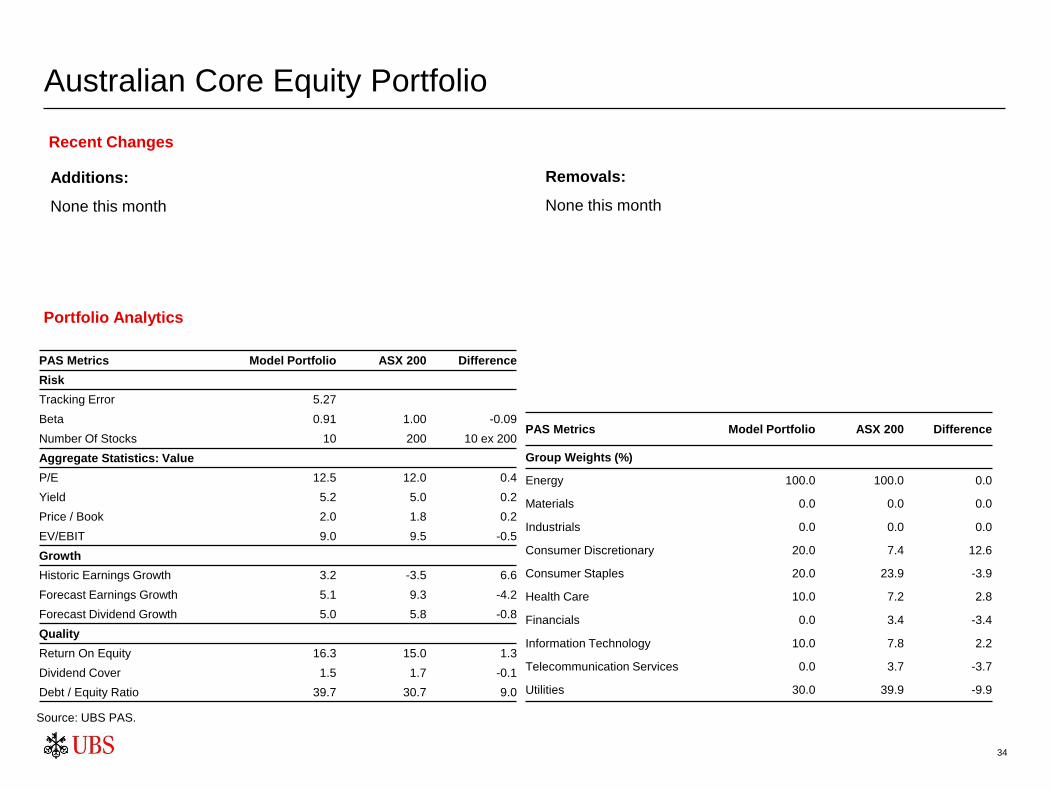

Australian Core Equity Portfolio

Additions:

None this month

Portfolio Analytics

Removals:

None this month

Recent Changes

Source: UBS PAS.

PAS Metrics Model Portfolio ASX 200 Difference

Risk

Tracking Error 5.27

Beta 0.91 1.00 -0.09

Number Of Stocks 10 200 10 ex 200

Aggregate Statistics: Value

P/E 12.5 12.0 0.4

Yield 5.2 5.0 0.2

Price / Book 2.0 1.8 0.2

EV/EBIT 9.0 9.5 -0.5

Growth

Historic Earnings Growth 3.2 -3.5 6.6

Forecast Earnings Growth 5.1 9.3 -4.2

Forecast Dividend Growth 5.0 5.8 -0.8

Quality

Return On Equity 16.3 15.0 1.3

Dividend Cover 1.5 1.7 -0.1

Debt / Equity Ratio 39.7 30.7 9.0

PAS Metrics Model Portfolio ASX 200 Difference

Group Weights (%)

Energy 100.0 100.0 0.0

Materials 0.0 0.0 0.0

Industrials 0.0 0.0 0.0

Consumer Discretionary 20.0 7.4 12.6

Consumer Staples 20.0 23.9 -3.9

Health Care 10.0 7.2 2.8

Financials 0.0 3.4 -3.4

Information Technology 10.0 7.8 2.2

Telecommunication Services 0.0 3.7 -3.7

Utilities 30.0 39.9 -9.9

35

Australian Core Equity Defensive Portfolio

Aims of the Core Equity Defensive Portfolio

For conservative equity investors, or investors looking for more defensive equity holdings, UBS WM offers the Core Equity Defensive

Portfolio. The aim is to encourage investors to look at companies with defensive cash flows to be adequately represented in portfolios.

When determining companies to add to the Core Equity Defensive Portfolio, some of the metrics we consider include :

Quality dividends through a cycle. The dividend target of the Core Equity Defensive Portfolio is higher than the Core

Equity Portfolio

The portfolio is intended to be less volatile vs the broader equity market, so the aim is for a lower than market beta value

The company must carry either a Buy or Neutral rating from UBS IB

Generally, the company should have a large market capitalisation, and companies should be part of the ASX 100 index

The Core Equity Defensive Portfolio

Source: UBS, Iress. Prices as at 29 June 2012.

Code Company Sector Market

Price UBS Rating

UBS Price

Target

Upside

/Downside P/E 12e Yield 12e %

Franking %

12e

Grossed Up

Yield 12e %

Market

Cap ($m)

AGK AGL Energy Limited Utilities 14.77 Buy 16.20 9.7% 14.7 4.06 100 5.80 8,061

CBA Commonwealth Bank Financials 53.10 Buy 53.50 0.8% 12.2 6.14 100 8.77 83,966

CCL Coca-Cola Amatil Limited Consumer Staples 13.38 Neutral 12.45 -7.0% 17.7 4.25 100 6.07 9,935

NAB National Australia Bank Financials 23.54 Neutral 24.50 4.1% 9.4 7.73 100 11.05 52,713

NCM Newcrest Mining Limited Materials 22.61 Neutral 30.00 32.7% 15.5 1.11 0 1.11 17,297

TAH Tabcorp Holdings Limited Consumer Discretionary 2.93 Buy 3.50 19.5% 5.9 8.53 100 12.19 2,016

TCL Transurban Group Industrials 5.69 Buy 6.25 9.8% 50.9 5.18 24 5.58 8,049

TLS Telstra Corporation Limited Telecoms 3.69 Buy 4.00 8.4% 12.8 7.59 100 10.84 45,915

WES Wesfarmers Limited Consumer Staples 29.90 Neutral 31.40 5.0% 16.3 5.45 100 7.79 34,849

WOW Woolworths Limited Consumer Staples 26.80 Buy 28.00 4.5% 15.0 4.66 100 6.66 32,935

Average Yield: 5.47 7.59

36

Australian Core Equity Defensive Portfolio

Removals:

ANZ – Since the initiation of the portfolio on 22 August 2011, ANZ

has returned 15.34% versus the ASX 200 Accum return of 2.93%.

In light of the UBS IB Sell recommendation at current price levels,

we have decided to take profit in ANZ.

Portfolio Analytics

CSL – Since the initiation of the portfolio on 22 August 2011, CSL

has returned 34.20% versus the ASX 200 Accum return of

2.93%.

In the current market climate, we have decided to lock in this

profit. We continue to believe that CSL is a quality defensive

position for portfolios.

Recent Changes

Source: UBS PAS.

PAS Metrics Model Portfolio ASX 200 Difference

Risk

Tracking Error 6.77

Beta 0.74 1.00 -0.26

Number Of Stocks 10 200 10 ex 200

Aggregate Statistics: Value

P/E 13.1 12.0 1.1

Yield 5.8 5.0 0.7

Price / Book 1.9 1.8 0.1

EV/EBIT 10.6 9.5 1.2

Growth

Historic Earnings Growth -0.4 -3.5 3.1

Forecast Earnings Growth -0.5 9.3 -9.8

Forecast Dividend Growth 0.9 5.8 -4.9

Quality

Return On Equity 14.5 15.0 -0.5

Dividend Cover 1.3 1.7 -0.3

Debt / Equity Ratio 40.2 30.7 9.5

PAS Metrics Model Portfolio ASX 200 Difference

Group Weights (%)

Energy 100.0 100.0 0.0

Materials 0.0 0.0 0.0

Industrials 0.0 0.0 0.0

Consumer Discretionary 0.0 7.4 -7.4

Consumer Staples 10.0 23.9 -13.9

Health Care 10.0 7.2 2.8

Financials 10.0 3.4 6.6

Information Technology 30.0 7.8 22.2

Telecommunication Services 0.0 3.7 -3.7

Utilities 20.0 39.9 -19.9

37

Australian Core Equity Income Portfolio

Aims of the Core Equity Income Portfolio

For equity investors looking to maximise the income from investments, UBS WM offers the Core Equity Income Portfolio. The target of

this portfolio is to provide a yield significantly in excess of the benchmark, without necessarily being exposed to greater levels of risk and

earnings uncertainty.

When determining companies to add to the Core Equity Income Portfolio, some of the metrics we consider include:

• A dividend yield above that average yield of the ASX 200, and above the 10 year bond yield

• A lower than market beta value

• A dividend coverage ratio above 1.00

• Generally, the company should have a market capitalisation of over $500 million

The Core Equity Income Portfolio

Source: UBS, Iress. Prices as at 29 June 2012.

Code Company Sector Market

Price UBS Rating

UBS Price

Target

Upside

/Downside P/E 12e Yield 12e %

Franking %

12e

Grossed Up

Yield 12e %

Market

Cap ($m)

AMP AMP Financials 3.85 Neutral 4.15 7.8% 12.1 6.36 0 6.36 10,990

CBA Commonwealth Bank Financials 53.10 Buy 53.50 0.8% 12.2 6.14 100 8.77 83,966

CCL Coca-Cola Amatil Limited Consumer Staples 13.38 Neutral 12.45 -7.0% 17.7 4.25 100 6.07 9,935

DUE Diversified Utility & Energy Utilities 1.84 Neutral 1.82 -1.1% 11.7 8.70 0 8.70 2,070

NAB National Australia Bank Financials 23.54 Neutral 24.50 4.1% 9.4 7.73 100 11.05 52,713

TAH Tabcorp Holdings Limited Consumer Discretionary 2.93 Buy 3.50 19.5% 5.9 8.53 100 12.19 2,016

TLS Telstra Corporation Limited Telecoms 3.69 Buy 4.00 8.4% 12.8 7.59 100 10.84 45,915

TTS Tatts Group Limited Consumer Discretionary 2.62 Neutral 2.50 -4.6% 11.4 8.02 100 11.45 3,513

WBC Westpac Banking Corporation Financials 21.13 Neutral 23.00 8.8% 10.6 7.86 100 11.22 64,531

WES Wesfarmers Limited Consumer Staples 29.90 Neutral 31.40 5.0% 16.3 5.45 100 7.79 34,849

WRT Westfield Retail Trust Financials 2.85 Buy 2.90 1.8% 15.2 6.59 0 6.59 8,704

Average Yield: 7.02 9.18

38

Australian Core Equity Income Portfolio

Additions:

CCL - CCL is the Australasian anchor bottler in the Coca-Cola

system, with Australia contributing approximately 68% of group

earnings.

Last month, we added CCL to the Core Defensive Portfolio. We are

now adding to the Core Income Portfolio, as even at current

historical high share prices, CCL delivers a yield of 8.41% (fully

franked). Portfolio Analytics

Removals:

None this month

Recent Changes

Source: UBS PAS.

PAS Metrics Model

Portfolio ASX 200 Difference

Risk

Tracking Error 6.31

Beta 0.85 1.00 -0.15

Number Of Stocks 11 200 11 ex 200

Aggregate Statistics: Value

P/E 12.4 12.0 0.3

Yield 7.0 5.0 1.9

Price / Book 1.5 1.8 -0.3

EV/EBIT 9.3 9.5 -0.1

Growth

Historic Earnings Growth -1.9 -3.5 1.5

Forecast Earnings Growth -7.5 9.3 -16.8

Forecast Dividend Growth -3.5 5.8 -9.3

Quality

Return On Equity 12.2 15.0 -2.8

Dividend Cover 1.2 1.7 -0.5

Debt / Equity Ratio 124.7 30.7 94.0

PAS Metrics Model Portfolio ASX 200 Difference

Group Weights (%)

Energy 100.0 100.0 0.0

Materials 0.0 0.0 0.0

Industrials 0.0 0.0 0.0

Consumer Discretionary 0.0 7.4 -7.4

Consumer Staples 0.0 23.9 -23.9

Health Care 0.0 7.2 -7.2

Financials 18.2 3.4 14.8

Information Technology 18.2 7.8 10.3

Telecommunication Services 0.0 3.7 -3.7

Utilities 45.5 39.9 5.5

SECTION 7.2

Sample International Equity Satellite Portfolio Themes

40

International Equity Satellite Portfolio

Aims of the International Equity Satellite Portfolio

For equity investors looking to add direct Global equities to portfolios, UBS WM offers the International Equity Satellite Portfolio. The

target of this portfolio is to provide a Satellite portfolio of mega-cap, International companies with solid future growth prospects. The

holdings are determined in consultation with Specialists in both Australia and APAC.

When determining companies to add to the International Equity Satellite Portfolio, some of the metrics we consider include:

• A focus on sector representation that is not adequately represented on the Australian market, e.g. Information

Technology, Global Industrials and Telecommunications.

• Companies with a globally recognised business line that provide an opportunity to participate in earnings upside.

• Any company that becomes part of the Portfolio must be included in the Global Top Pick List, the UBS IB Key Calls List,

or the WMR Top 25 Stock List. If the company is subsequently removed from all of these lists, it is also automatically

removed from the Portfolio.

International Equity Satellite Portfolio

Source: UBS, Iress. Prices as at 29 June 2012.

Code Company Base Currency Market Price UBS Rating UBS Price

Target Price Upside P/E 12e Yield 12e %

Market

Cap ($B USD)

DE Deere and Co USD 80.87 Buy 115.00 42.2% 9.7 2.03 30.9

CSX CSX Corporation USD 22.36 Buy 29.00 29.7% 12.8 2.37 22.3

EBAY EBay Inc USD 42.01 Buy 45.00 7.1% 17.8 0.00 52.2

GE General Electric Company USD 20.84 Buy 23.00 10.4% 13.4 3.26 196.3

GOOG Google Inc USD 580.07 Buy 825.00 42.2% 13.1 0.00 201.0

KO Coca Cola Company USD 78.19 Neutral 77.00 -1.5% 19.0 2.74 176.1

NESN NESTLE N CHF 56.55 Buy 58.00 2.6% 17.4 3.63 174.0

NOVN NOVARTIS N CHF 52.90 Buy 60.00 13.4% 9.7 4.54 143.1

Average Yield: 2.32

SECTION 7.3

Sample Australian Listed Property

42

Australian Listed Property Portfolio

Aims of the Australian Listed Property Portfolio

For equity investors looking to add listed property exposure to portfolios, UBS WM offers the Australian Listed Property Portfolio.

Overall, the focus of the portfolio is to include core names with a large market capitalisation, comparatively low volatility with solid pricing

power within their market and a solid earnings stream in 2012.

When determining companies to add to the Australian Listed Property Portfolio, some of the metrics we consider include:

A history of paying quality distributions

The company must carry either a Buy or Neutral rating from UBS IB

Generally, the company should have a large market capitalisation

Generally, the company should have an Interest Cover ratio above the average for the sector

Australian Listed Property Portfolio

Source: UBS, Iress. Prices as at 29 June 2012.

Code Company Market Price UBS Rating UBS Price

Target

Upside

/Downside P/E 12e Yield 12e %

Market

Cap ($m)

CFX CFS Retail Property Trust 1.94 Neutral 1.95 0.5% 14.8 6.75 5,509

GMG Goodman Group 3.67 Buy 3.85 4.9% 11.9 5.06 5,687

GPT GPT Group 3.29 Neutral 3.42 4.0% 14.0 5.62 5,953

WDC Westfield Group 9.50 Neutral 9.50 0.0% 14.3 5.21 21,935

WRT Westfield Retail Trust 2.85 Buy 2.90 1.8% 15.2 6.59 8,704

Average Yield: 5.85

SECTION 7.4

Sample Australian Fixed Income & Hybrids

44

Government Bond Portfolio

Aims of the Government Bond Portfolio

The Government Bond Portfolio provides a regular income with minimal credit risk and capital preservation. The bonds pay semi

annual coupons, offer a range of maturities from 1 to 12 years, are highly liquid and can be traded in minimum parcel sizes of $5,000 and

in $1,000 increments.

When determining bonds to add to the Government Bond Portfolio, some of the metrics we consider include:

The Government Bond Portfolio

• The number of securities varies between 6 and 12 in

order to give a representative spread of the curve.

• Client suitability – the Portfolio is suitable as a starting

point for all fixed income clients but is specifically

designed with the risk-averse investor in mind. It is a

―AAA‖ portfolio.

• The duration of the chosen bonds varies according to the

current duration strategy.

• Duration management relies more on the weightings applied to

particular bonds rather than using all the securities available

across the curve from the benchmark index.

Source: UBS, Iress. Prices as at 29 June 2012.

Issuer Coupon Rate

%

Call/Maturity

Date

Duration

(Years)

Running Yield

%

Yield to

Call/Maturity %

Face Value

$AUD

Gross Price

$AUD

Consideration

$AUD

Portfolio

Weight

CGL 6.50 15-May-13 0.84 6.25 2.87 145,000 103.96 150,735 15%

CGL 6.25 15-Jun-14 1.84 5.81 2.46 235,000 107.50 252,623 25%

CGL 6.25 15-Apr-15 2.55 5.60 2.39 180,000 111.69 201,040 20%

CGL 6.00 15-Feb-17 4.01 5.11 2.50 85,000 117.47 99,851 10%

CGL 5.25 15-Mar-19 5.66 4.49 2.73 130,000 116.89 151,962 15%

CGL 4.50 15-Apr-20 6.57 4.00 2.84 90,000 112.53 101,280 10%

CGL 5.75 15-May-21 7.12 4.69 2.93 40,000 122.63 49,052 5%

Total 3.36 5.33 2.66 905,000 1,006,543 100%

Index duration: 4.23

Active duration: -0.88

45

Semi Government Bond Portfolio

Aims of the Semi Government Bond Portfolio

The Semi Government Bond Portfolio provides a regular income with minimal credit risk and capital preservation. The bonds are

issued by all Australian States and Territories, pay semi annual coupons and offer a range of maturities from 1 to 23 years. They are

highly liquid and can be traded in minimum parcel sizes of $5,000 and in $1,000 increments.

When determining bonds to add to the Semi Government Bond Portfolio, some of the metrics we consider include:

The Semi Government Bond Portfolio

• The number of securities varies between 6 and 12 in

order to give a representative spread of the curve.

• Client suitability – the Portfolio is suitable as a starting

point for all fixed income clients but is specifically

designed with the risk-averse investor in mind. It is

representative of the UBS Semi-Government benchmark

index.

• The duration of the chosen bonds varies according to the

current duration strategy.

• Duration management relies more on the weightings applied to

particular bonds rather than using all the securities available

across the curve from the benchmark index.

• Lower coupons are usually selected in order to prevent

investors having to pay any significant premiums

Source: UBS, Iress. Prices as at 29 June 2012.

Issuer Coupon Rate

%

Call/Maturity

Date

Duration

(Years)

Running Yield

%

Yield to

Call/Maturity %

Face Value

$AUD

Gross Price

$AUD

Consideration

$AUD

Portfolio

Weight

QTC 6.00 21-Aug-13 1.07 5.70 3.16 45,000 105.34 47,402 5%

TCV 4.75 15-Oct-14 2.14 4.54 3.07 95,000 104.71 99,473 10%

QTC 6.00 21-Oct-15 2.97 5.51 3.52 185,000 108.87 201,400 20%

TCV 5.75 15-Nov-16 3.85 5.22 3.41 225,000 110.20 247,952 25%

WATC 8.00 15-Jul-17 4.12 6.43 3.50 200,000 124.36 248,720 25%

QTC 6.00 21-Feb-18 4.71 5.36 4.04 135,000 111.99 151,184 15%

Total 3.57 5.56 3.56 885,000 996,131 100%

Index duration: 4.46

Active duration: -0.89

46

Corporate Fixed Rate Bond Portfolio

Aims of the Corporate Fixed Rate Bond Portfolio

The Corporate Fixed Rate Bond Portfolio consists of the best value fixed rate bonds from the current available corporate issues. The

chosen bonds have had their liquidity confirmed and can be traded in minimum parcel sizes of $500,000. We look to ensure that the

portfolio is diversified across all the sectors of the issuers.

When determining bonds to add to the Corporate Fixed Rate Bond Portfolio, some of the metrics we consider include:

The Corporate Fixed Rate Bond Portfolio

• The bond must exist on the Universe of Approved

issuers.

• The duration of the chosen bonds varies according to the

current duration strategy. Our current core duration

recommendation is a shorter than benchmark position.

• Client suitability – the Portfolio is suitable as a starting point for

all fixed income clients.

• The bond must have at least $3m of the issue currently

available to meet liquidity requirements.

Source: UBS, Iress. Prices as at 29 June 2012.

Issuer Coupon Rate

%

Call/Maturity

Date

Duration

(Years)

Running Yield

%

Yield to

Call/Maturity %

Face Value

$AUD

Gross Price

$AUD

Consideration

$AUD

Portfolio

Weight

NAB SUB 7.25 21-Dec-12 0.46 7.15 4.58 500,000 101.46 507,310 10%

UBSAGAU 6.25 26-Aug-13 1.08 6.00 4.46 500,000 104.18 520,905 10%

CBA# 6.25 10-Sep-13 1.12 5.96 3.73 500,000 104.86 524,305 10%

WESFARMERS 8.25 11-Sep-14 1.96 7.48 4.50 500,000 110.30 551,475 10%

GECAPITAL 7.00 8-Oct-15 2.88 6.42 4.55 500,000 109.02 545,100 10%

WOOLWORTHS 6.75 22-Mar-16 3.24 6.13 4.31 500,000 110.19 550,970 10%

ING 7.00 22-Mar-16 3.19 6.66 6.06 500,000 105.05 525,245 10%

WESTF RET 7.00 18-Oct-16 3.66 6.45 5.15 500,000 108.51 542,565 10%

CB CBA 5.75 25-Jan-17 3.91 5.32 4.37 500,000 108.18 540,905 10%

CB WESTPAC 5.75 6-Feb-17 3.94 5.32 4.37 500,000 108.02 540,080 10%

Total 2.56 6.29 4.69 5,000,000 5,348,860 100%

47

Corporate Floating Rate Note Portfolio

Aims of the Corporate Floating Rate Note Portfolio

The Corporate Floating Rate Note Portfolio consists of the best value FRNs from the current available corporate issues. The chosen

bonds have had their liquidity confirmed and can be traded in minimum parcel sizes of $500,000. We look to ensure that the portfolio is

diversified across all the sectors of the issuers.

When determining bonds to add to the Corporate Floating Rate Note Portfolio, some of the metrics we consider include:

The Corporate Floating Rate Note Portfolio

• The bond must exist on the Universe of Approved

issuers.

• The duration of the chosen bonds varies according to the

current duration strategy. Our current core duration

recommendation is a shorter than benchmark position.

• Client suitability – the Portfolio is suitable as a starting point for

all fixed income clients.

• The bond must have at least $3m of the issue currently

available to meet liquidity requirements.

Source: UBS, Iress. Prices as at 29 June 2012.

Issuer Coupon

Margin bps

Call/Maturity

Date

Duration

(Years)

Running

Yield %

Yield to

Call/Maturity

%

Face Value

$AUD

Gross Price

$AUD

Consideration

$AUD

Trading

Margin %

Next Coupon

Date

Portfolio

Weight

NAB SUB 26 21-Dec-12 0.22 3.81 4.75 500,000 99.64 498,180 1.30 21-Sep-12 10%

BKQLD 150 6-Jun-13 0.18 4.90 4.96 500,000 100.11 500,550 1.75 6-Sep-12 10%

UBSAGAU 148 26-Aug-13 0.15 4.98 4.45 500,000 100.69 503,445 1.30 27-Aug-12 10%

GECAPITAL 110 18-Feb-14 0.13 4.69 4.02 500,000 100.92 504,610 0.90 20-Aug-12 10%

WESTPAC 110 18-Aug-14 0.13 4.69 4.00 500,000 101.08 505,375 0.87 20-Aug-12 10%

HSBC 115 6-Mar-15 0.18 4.54 4.32 500,000 100.36 501,795 1.13 6-Sep-12 10%

ANZ 135 26-Oct-15 0.06 5.40 4.55 500,000 101.43 507,150 1.23 26-Jul-12 10%

WESTPAC 110 9-Nov-15 0.10 4.80 4.63 500,000 100.28 501,410 1.25 9-Aug-12 10%

AMP SUB 250 26-Mar-16 -0.02 6.92 6.35 500,000 100.01 500,050 2.85 26-Jun-12 10%

CB WESTPAC 165 6-Feb-17 0.10 5.29 4.44 500,000 103.27 516,360 1.07 7-Aug-12 10%

Total 0.12 5.00 4.64 5,000,000 5,038,925 1.20 100%

48

Conservative Hybrid Portfolio

Aims of the Conservative Hybrid Portfolio

The Conservative Hybrid Portfolio focuses on issuers with investment grade ratings that display minimum volatility in normal market

conditions. The issuer must be a financial institution and be highly liquid relative to other hybrid securities listed on the ASX. We

recommend no more than a 10% weighting to listed subordinated hybrids within the fixed income asset class for conservative

investors.

When determining companies to add to the Conservative Hybrid Portfolio, some of the metrics we consider include:

The Conservative Hybrid Portfolio

• S&P security rating of investment grade (BBB- and above)

• Minimum Issue size of $500m

• Included in the top fifteen hybrid securities by monthly turn

over

• The hybrid must have limited extension risk, based on

market expectations and UBS analysis

• The issuer must have a strong, stable cash flow and

balance sheet, and must be listed on the ASX 200

Source: UBS, Iress. Prices as at 29 June 2012.

ASX Code Security - Franking Dividend Rate First call/reset

date

Yield to call /

reset

Trading

Margin over

BBSW

Running

Yield

Duration

(Years)

Call Date

(years)

Market

Price Weight

ANZHA ANZ Sub Notes - Unfranked BBSW + 2.75% 20-Jun-17 6.24% 2.65% 6.23% 0.18 4.98 $100.65 10.0%

ANZPA ANZ CPS2 - Franked BBSW + 3.10% 15-Dec-16 6.89% 3.39% 6.77% 0.15 4.47 $99.25 10.0%

ANZPC ANZ CPS3 - Franked BBSW + 3.10% 01-Sep-17 7.52% 3.92% 7.81% 0.11 5.18 $98.99 10.0%

CBAHA CBA Retail Bond - Unfranked BBSW + 1.05% 24-Dec-15 5.18% 1.84% 5.39% 0.00 3.49 $98.78 10.0%

CBAPA CBA PERLS V - Franked BBSW + 3.40% 31-Oct-14 6.34% 3.10% 7.37% 0.04 2.34 $203.99 10.0%

CNGHA Colonial Group Sub Notes - Unfranked BBSW + 3.25% 31-Mar-17 6.95% 3.40% 7.65% -0.05 4.76 $99.50 10.0%

IAGPC IAG CPS - Franked BBSW + 4.00% 01-May-17 8.36% 4.79% 8.22% 0.29 4.84 $98.10 10.0%

SBKPB Suncorp-Metway CPS - Franked BBSW + 3.20% 14-Jun-13 8.88% 5.66% 6.90% 0.15 0.96 $98.15 10.0%

TAHHA Tabcorp Bonds - Unfranked BBSW + 4.25% 01-May-14 5.94% 2.72% 7.81% 0.08 1.84 $103.80 10.0%

WOWHC WOW Notes II - Unfranked BBSW + 3.25% 24-Nov-16 5.99% 2.50% 6.53% 0.10 4.41 $103.60 10.0%

Total 6.79% 3.31% 7.07% 0.11 3.73 100.0%

49

Moderate Hybrid Portfolio

Aims of the Moderate Hybrid Portfolio

The Moderate Hybrid Portfolio focuses on issuers with investment grade ratings that may display some volatility. The issuer must be a

recognised, regular user of debt and/or hybrid markets, and the issue must be moderately liquid, relative to other hybrid securities listed

on the ASX. We recommend no more than a 20% weighting to listed subordinated hybrids within the fixed income asset class for

moderate investors.

When determining companies to add to the Moderate Hybrid Portfolio, some of the metrics we consider include:

• S&P security rating of investment grade (BBB- and above)

• Minimum Issue size of $250m

• Included in top twenty hybrid securities by monthly turn over

• The issuer must have a strong, stable cash flow and balance sheet

The Moderate Hybrid Portfolio

Source: UBS, Iress. Prices as at 29 June 2012.

ASX Code Security - Franking Dividend Rate First call/reset

date

Yield to call /

reset

Trading

Margin over

BBSW

Running

Yield

Duration

(Years)

Call Date

(years)

Market

Price Weight

AGKHA AGL Notes - Unfranked BBSW + 3.80% 08-Jun-19 7.66% 3.91% 7.39% 0.15 6.95 $99.92 10.0%

ANZHA ANZ Sub Notes - Unfranked BBSW + 2.75% 20-Jun-17 6.24% 2.65% 6.23% 0.18 4.98 $100.65 10.0%

ANZPC ANZ CPS3 - Franked BBSW + 3.10% 01-Sep-17 7.52% 3.92% 7.81% 0.11 5.18 $98.99 10.0%

CBAHA CBA Retail Bond - Unfranked BBSW + 1.05% 24-Dec-15 5.18% 1.84% 5.39% 0.00 3.49 $98.78 10.0%

IAGPC IAG CPS - Franked BBSW + 4.00% 01-May-17 8.36% 4.79% 8.22% 0.29 4.84 $98.10 10.0%

ORGHA Origin Notes - Unfranked BBSW + 4.00% 22-Dec-16 7.57% 4.07% 7.55% 0.19 4.48 $99.99 10.0%

SBKPB Suncorp-Metway CPS - Franked BBSW + 3.20% 14-Jun-13 8.88% 5.66% 6.90% 0.15 0.96 $98.15 10.0%

TAHHA Tabcorp Bonds - Unfranked BBSW + 4.25% 01-May-14 5.94% 2.72% 7.81% 0.08 1.84 $103.80 10.0%

WCTPA Westpac TPS - Franked BBSW + 1.00% 30-Jun-16 8.27% 4.85% 6.00% -0.07 4.01 $87.75 10.0%

WOWHC WOW Notes II - Unfranked BBSW + 3.25% 24-Nov-16 5.99% 2.50% 6.53% 0.10 4.41 $103.60 10.0%

Total 7.16% 3.63% 6.98% 0.12 2.05 100.0%

50

Aggressive Hybrid Portfolio

Aims of the Aggressive Hybrid Portfolio

The Aggressive Hybrid Portfolio focuses on issuers which may provide significant capital upside from opportunities that may arise, for

reasons including, but not limited to, speculation regarding time to maturity, earnings outlook of the underlying issuer, market and

economic conditions. We recommend no more than a 25% weighting to listed subordinated hybrids within the fixed income asset class

for aggressive investors.

When determining companies to add to the Aggressive Hybrid Portfolio, some of the metrics we consider include:

• No rating of the issuer or issue is required

• Minimum Issue size of $100m

• Liquidity available to facilitate entry

• Displays a yield to call date significantly higher than the average weighted yield of the major bank convertible hybrids

The Aggressive Hybrid Portfolio

Source: UBS, Iress. Prices as at 29 June 2012.

ASX Code Security - Franking Dividend Rate First call/reset

date

Yield to call /

reset

Trading

Margin over

BBSW

Running

Yield

Duration

(Years)

Call Date

(years)

Market

Price Weight

AAZPB Australand ASSETS - Unfranked BBSW + 4.80% Perp 9.79% 5.85% 10.15% -0.02 - $89.00 8.3%

AGKHA AGL Notes - Unfranked BBSW + 3.80% 08-Jun-19 7.66% 3.91% 7.39% 0.15 6.95 $99.92 8.3%

IAGPC IAG CPS - Franked BBSW + 4.00% 01-May-17 8.36% 4.79% 8.22% 0.29 4.84 $98.10 8.3%

HLNG Healthscope Notes - Unfranked 11.25% Fixed 17-Jun-16 10.68% 7.26% 11.01% 3.97 3.97 $102.50 8.3%

NFNG Nufarm Step-up Securities - Unfranked BBSW + 3.90% Perp 10.78% 6.84% 11.13% 0.25 - $74.60 8.3%

MQCPA Macquarie Group CPS - Unfranked 11.10% Fixed 30-Jun-13 3.96% 0.77% 10.83% 1.00 1.00 $102.50 8.3%

ORGHA Origin Notes - Unfranked BBSW + 4.00% 22-Dec-16 7.57% 4.07% 7.55% 0.19 4.48 $99.99 8.3%

SBKPB Suncorp-Metway CPS - Franked BBSW + 3.20% 14-Jun-13 8.88% 5.66% 6.90% 0.15 0.96 $98.15 8.3%

SVWPA Seven Telys 4 - Franked BBSW + 4.75% Perp 11.23% 7.29% 10.34% 0.36 - $77.99 8.3%

TAHHB Tabcorp Subordinated Notes - Unfranked BBSW + 4.00% 22-Mar-17 8.23% 4.68% 7.73% 0.19 4.73 $97.60 8.3%

WCTPA Westpac TPS - Franked BBSW + 1.00% 30-Jun-16 8.27% 4.85% 6.00% -0.07 4.01 $87.75 8.3%

WOWHC WOW Notes II - Unfranked BBSW + 3.25% 24-Nov-16 5.99% 2.50% 6.53% 0.10 4.41 $103.60 8.3%

Total 7.95% 4.42% 8.65% 0.55 1.63 100.0%

SECTION 8

Strategic Asset Allocation (SAA)

Tactical Asset Allocation (TAA)

Reference Portfolios – risk metrics and expected returns. Sample only

52 52

The importance of Strategic Asset Allocation

Strategic Asset Allocation:

The appropriate mix of asset classes based on long-term market assumptions (10+ years) given an

investor's objectives and risk tolerance. The optimal portfolio depends on the preferences and the risk

profile of the investor.

Sub-

optimal

portfolio

Optimal

portfolio

Efficient frontier

line

Risk

Re

turn

Strategic Asset Allocation of an initial and optimized

portfolio.

The efficient frontier line represents the portfolios

with the lowest risk for each given return level.

These portfolios are called "efficient" portfolios.

Equity

Bonds

Real Estate

Cash

Sub-optimal

portfolio

Optimal

portfolio

Equity

Bonds

Commodities

Real Estate

Cash

Hedge Funds

Private Equity

Please refer to the disclaimer at the end of this presentation

For illustrative purposes only

The most important

decision, in the long

term, is the Strategic

Asset Allocation ...

… as it accounts for

up to 90% of asset

returns

53

Comparison of Sample Portfolios reflecting different risk appetites

Generated by QIS

3

2

1

5.3%

5.8%

6.3%

6.8%

7.3%

7.8%

8.3%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0%

Annualised Est imated Risk %

An

nu

alise

d E

stim

ate

d R

etu

rn %

1 = Conservative 2 = Moderate 3 = Aggressive

Risk p.a Return p.a

1 4.8% 6.3%

2 7.5% 6.9%

3 9.6% 7.4%

Portfolio forward-looking estimated risk and return scatter

Data as of 31/05/2012

For illustrative purposes only. Markets are subject to change and returns may vary. See explanation under "Ex-Ante Estimates" at the end of this document. Please note that this page

is always to be read in conjunction with the risk information and explanations of terms appended to this presentation.

54

Comparison of Portfolios

Generated by QIS

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

Re

turn

Conservat ive 9.7% 24.9%10.9%23.7%-7.8% 19.0%10.6% 21.1% 15.7% 4.2% 14.7% 8.7% 0.0% 1.1% 11.3% 10.4% 9.0% 2.6% -8.1% 3.3% 1.0% 2.6% 5.6%

M oderate 2.0% 26.5% 9.2% 27.4%-8.2%19.2% 9.9% 23.4%17.8% 8.6% 12.3% 8.3% -6.6% 2.3% 14.4% 14.5% 13.2% 3.8% -20.7 9.2% -0.4%-3.2% 5.2%

Aggressive -3.3%29.1% 6.9% 30.1% -8.2%19.7% 10.1% 23.1%18.3% 11.3% 8.9% 6.4% -10.8%4.9% 16.9% 17.7% 15.8% 5.8% -27.5%15.0% -0.3% -5.7% 4.6%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999200

02001

200

2

200

3

200

42005

200

62007

200

8

200

92010 2011 2012

Simulated historic annual returns

The chart shows the

performance of the chosen

asset allocations in each

calendar year.

Data as of 31/05/2012. Time horizon: 29/12/1989 - 31/05/2012

For illustrative purposes only. Markets are subject to change and returns may vary. See explanation under "Simulated Historical Performance" at the end of this document. Please

note that this page is always to be read in conjunction with the risk information and explanations of terms appended to this presentation.

55

Comparison of Portfolios

Generated by QIS

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

Re

turn

Conservat ive -2.7% -7.1% 1.7% 1.7% -0.4% 9.2% 1.3% -0.1% -1.5% -4.6% -5.7% 7.3%

M oderate -7.1% -7.3% -0.6% -1.0% -3.1% 6.0% -0.6% -5.6% -4.8% -8.5% -18.0% 0.7%

Aggressive -10.1% -7.7% -1.9% -3.4% -5.2% 2.1% -2.6% -9.7% -6.9% -11.0% -25.7% -3.3%

1st Gulf

War '90

Fed Hike

'94

Tequila

Crisis

'94/95

Asia Crisis

'97

Russian

Crisis '98

Tech

Bubble

'00/01

Sept 11 '01

Corp.

Scandals

'02

2nd Gulf

War '03

Sub Prime

'08

Credit

Crunch

'08/09

Euro Zone

Crisis

'11/12

1st Gulf War '90

Fed Hike '94

Tequila Crisis '94/95

Asia Crisis '97

Russian Crisis '98

Tech Bubble '00/01

Sept 11 '01

Corp. Scandals '02

2nd Gulf War '03

Sub Prime '08

Credit Crunch '08/09

Euro Zone Crisis '11/12

7/1990-9/1990

1/1994-5/1994

10/1994-2/1995

7/1997-10/1997

7/1998-9/1998

8/2000-3/2001

8/2001-9/2001

5/2002-9/2002

11/2002-3/2003

10/2007-1/2008

5/2008-2/2009

4/2011-5/2012

Simulated historic stress tests

The chart shows the impact

(gains and losses) of different

financial crises on the value of

the asset allocations.

Impact is shown in percentage

decrease in value.

Data as of 31/05/2012. Time horizon: 29/12/1989 - 31/05/2012

For illustrative purposes only. Markets are subject to change and returns may vary. See explanation under "Simulated Historical Performance" at the end of this document. Please

note that this page is always to be read in conjunction with the risk information and explanations of terms appended to this presentation.

56

Moderate

Generated by QIS

10.0%

15.0%

50.0%

20.0%

5.0%

Liquidit y

Bonds

Equit ies

HF&PE

Real estate

Asset Class

4.1%2.1%

31.8%

2.0%

60.0%

AUD

JPY

USD

GBP

EUR

Currency

LIQUIDITY 5.0%

JPM Cash Index AUD 3M 5.0%

BONDS 20.0%

Barclays Global Aggregate 5.0%

JPM GBI Australia 15.0%

EQUITIES 50.0%

MSCI Japan 2.0%

MSCI EMU 4.1%

MSCI United Kingdom 2.1%

MSCI Australia 30.0%

MSCI Emerging Markets 2.2%

MSCI USA 9.6%

HEDGE FUNDS & PRIVATE EQUITY 15.0%

HFRX Global Hedge Fund USD 15.0%

REAL ESTATE 10.0%

GPR General Australia 10.0%

Asset allocation (AUD)

Data as of 31/05/2012

For illustrative purposes only. Markets are subject to change and returns may vary. The above asset classes, asset allocation and investment instruments are indicative only and can

be changed at any time at UBS' discretion. Please note that this page is always to be read in conjunction with the risk information and explanations of terms appended to this

presentation.

57

Moderate

Generated by QIS

0

100

200

300

400

500

600

700

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

AU

D

1st Gulf War '90 Fed Hike '94 Tequila Crisis '94/95

Asia Crisis '97 Russian Crisis '98 Tech Bubble '00/01

Sept 11 '01 Corp. Scandals '02 2nd Gulf War '03

Sub Prime '08 Credit Crunch '08/09 Euro Zone Crisis '11/12

History

1st Gulf War '90

Fed Hike '94

Tequila Crisis '94/95

Asia Crisis '97

Russian Crisis '98

Tech Bubble '00/01

Sept 11 '01

Corp. Scandals '02

2nd Gulf War '03

Sub Prime '08

Credit Crunch '08/09

Euro Zone Crisis '11/12

7/1990-9/1990

1/1994-5/1994

10/1994-2/1995

7/1997-10/1997

7/1998-9/1998

8/2000-3/2001

8/2001-9/2001

5/2002-9/2002

11/2002-3/2003

10/2007-1/2008

5/2008-2/2009

4/2011-5/2012

Simulated historical stress test

The chart shows the simulated

historical performance of the portfolio.

The time periods of the historical

financial crises are highlighted, to show

the impact of each crisis on the

portfolio.

Data as of 31/05/2012. Time horizon: 29/12/1989 - 31/05/2012

For illustrative purposes only. Markets are subject to change and returns may vary. See explanation under "Simulated Historical Performance" at the end of this document. Please

note that this page is always to be read in conjunction with the risk information and explanations of terms appended to this presentation.

SECTION 8

Behavioural Implications for Investors

59

Behavioral Finance – 7 Traps for Investors

Selective Perception: Ignoring information that contradicts our opinion

Herd Instinct: Doing what everybody else is doing

Overconfidence: Trading too much

Loss Aversion: Selling winners too soon and losers too late

Ignoring Lessons from the Past: "This time it is different"

Home Bias: Investing only in what we know

Lack of Diversification: Too concentrated portfolios

60

Remember: stay in the game—it never ever pays to panic

Maximum Financial Risk

Maximum Financial Opportunity Optimism

Optimism

Euphoria

Panic

Despondence

Hope Fear

Source: UBS

Behavioural Finance tells us emotions get in the way of wealth accumulation. What is getting in the way of

your wealth accumulation plan?

SECTION 9

Summary

62

Summary – Europe delivered. More challenges persist globally…

Defensives did what they are supposed to do for the financial year. Investor caution is set to

remain in the Sept quarter. Therefore cash weightings expected to remain high vs historical.

RBA Implied Cash Futures now pricing in 2.75% by year-end. We expect 3.0%-3.25% as the low.

Europe delivered in June and worst case scenario avoided. Key EU blueprint a positive. Europe

moving towards a common monetary & fiscal union which now will include an independent

European banking regulator.

Global PMI Surveys (ie. ISM Survey) are mixed by region but the US conditions remain

expansionary. Other developed economies remain subdued.

US earnings have delivered year-to-date. Equities have only reflected the growth in earnings, but

no multiple expansion. Investors remain cautious despite solid corporate balance sheet.

Equity valuations still remain discounted vs long-run historical benchmarks. This will continue.

Sept quarter earnings growth pulse to slow.

10.8x P/E vs 14.5x long run remains a very large discount. 12.0x looks a reasonable outcome

over the next year. Year end target for ASX200 4,450.

Domestic Tactical Asset Allocation: Large overweight Cash remains. Neutral Equities (we prefer

Aust, US & EM. Remain underweight Europe, UK and Japan). Neutral Fixed Income (short

duration remains, preference for quality corporate bonds), underweight A-REITs & Alternatives.

Your portfolio asset allocation must reflect your risk profile

63

64

Contact information

George Boubouras

Executive Director

Head of Investment Strategy & Consulting

Tel: +61 (3) 9242 6747

Mobile: +61 (0) 411 285 577

E-mail: [email protected]

Important: This document has been prepared by UBS Wealth Management Australia Limited ABN 50 005 311937, holder of AFSL 231127, which is a subsidiary of UBS AG (together, "UBS").

This document contains general information and general advice only and does not constitute personal financial product advice. As such, the material does not take into account the personal

investment objectives, financial situation, tax position or particular needs of any specific recipient. Prior to any investment decision, we recommend that you seek personal investment advice

from your Client Advisor, based on your personal situation and consider the relevant offer document (including the product disclosure statement) before making any investment decision.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete

statement or summary of the securities, markets or developments referred to in the materials. It should not be regarded by recipients as a substitute for the exercise of their own judgement. Any

opinions expressed in this material are subject to change without notice and may differ or be contrary to opinions expressed by other business areas or divisions of UBS as a result of using

different assumptions and criteria. UBS, its directors, officers and employees' or clients may have or have had interests or long or short positions in the securities or other financial instruments

referred to herein and may at any time make purchases and/or sales in them as principal or agent. UBS may act or have acted as market-maker in the securities or other financial instruments

discussed in this material. Furthermore, UBS may have or have had a relationship with or may provide or has provided investment banking, capital markets and/or other financial services to the

relevant companies. Neither UBS nor any of its affiliates, nor any of UBS' or any of its affiliates, directors, employees or agents accepts any liability for any loss or damage arising out of the use

of all or any part of this material.

Options, derivative products and futures are not suitable for all investors, and trading in these instruments is considered risky. Past performance is not necessarily indicative of future results.

Foreign currency rates of exchange may adversely affect the value, price or income of any security or related instrument mentioned in this document. Before making an investment decision, you

should consider whether the information is appropriate in light of your particular investment needs, objectives and financial circumstances, and seek your own legal, regulatory, tax, financial and

accounting advice.

This material is for distribution only under such circumstances as may be permitted by applicable law. To the extent that UBS has sourced any material in this document from a third party, UBS

accepts no liability for the accuracy, currency or completeness of that material. All information is correct at the time of publication only and is subject to change without notice. UBS Wealth

Management Australia Limited, Registered Office: Level 16, Chifley Tower, 2 Chifley Square, Sydney NSW 2000.

© UBS 2012. All rights reserved. UBS specifically prohibits the redistribution of this material and accepts no liability whatsoever for the actions of third parties in this respect.

• Take a short online course

• Subscribe to the Investor Update e-newsletter

• Play the ASX Sharemarket Game

• Watch another ASX Investment talks presentation

KEEP LEARNING

VISIT www.asx.com.au/education