u.a. local 71 pension plan · u. a. local 71 pension plan pension trust fund | january 2015 united...

TRANSCRIPT

U. A. Local 71 Pension PlanPension Trust Fund | January 2015

United Association of Journeymen and Apprentices of the Plumbing and Pipe Fitting Industry of the United States and Canada

i

Pension Plan

U.A. Local 71 Pension Plan January 2015BOARD OF TRUSTEESLabour IndependentPaul Dupont Michel PoirierBrent PayneMichael ReidRoland RoyLarry St. Germain

ACTUARYMorneau Shepell Ltd.

AUDITORBouris Wilson LLP

CONSULTANT AND ADMINISTRATOR

Mailing Address: Mailing Address: P.O. Box 3517, Station C 466 Tremblay Road Ottawa, ON K1Y 4H5 Ottawa, ON K1G 3R1 Telephone: 613-231-2266 Fax: 613-231-2345E-mail: [email protected]; or [email protected]: www.coughlin.ca

ii

INVESTMENT MANAGERSBrookfield Asset ManagementBTG Pactual Brazil Timberland Fund IBurgundy Asset Management Ltd.Canso Investment Counsel Ltd.CI Institutional Asset ManagementGlovista Investments LLCHillsdale Investment Management Inc.Jarislowsky Fraser Limited Investment CounselManulife Asset ManagementState Street Global Advisors Ltd.Trez Capital

OTHER PLACEMENTSLimited partnershipsPrivate mortgagesValleyview Lands LLP

iii

To all members of the U.A. Local 71 Pension PlanThe board of trustees is pleased to provide this updated booklet which is designed to provide answers to the most commonly asked questions about the pension plan.

We encourage you to read the booklet carefully to ensure that you understand the benefits you are entitled to receive under the pension plan. This booklet should be stored with your other important documents for future reference.

Any questions regarding the benefits, administration or application for pension benefits should be directed to your plan administrator.

Fraternally yours,

The board of trustees

iv

NotesIMPORTANTThis document contains important information concerning your pension plan and, therefore, should be kept in a safe place. This booklet supersedes and replaces all previously communicated material.

The purpose of this outline is to explain briefly the main features of this pension plan. This outline does not create or confer any contractual or other rights.

The trust agreement and plan document of the U.A. Local 71 Pension Trust Fund and Plan and any government regulations govern all rights and obligations of the plan.

REGISTRATION NUMBERSFinancial Services Commission of Ontario and Canada Revenue Agency registration number 0382481.

CHANGE OF ADDRESSIt is important to inform the plan administrator and the U.A. Local 71 of any address changes.

ERRORS OR OMISSIONSEvery effort has been made to ensure that this booklet is accurate and complete. Should errors, omissions or disputes occur, the terms of the policies issued to the U.A. Local 71 Pension Trust Fund and Plan will prevail.

v

Protecting your personal informationThe administrator of your group pension plan is Coughlin & Associates Ltd. At Coughlin, we recognize and respect every individual’s right to privacy. When personal information is provided to us, we establish a confidential file that is kept in the offices of Coughlin, or the offices of an organization authorized by Coughlin. We use the information to administer the group pension plan. We limit access to information in your file to Coughlin staff or persons authorized by Coughlin who require it to perform their duties, to persons to whom you have granted access, and to persons authorized by law.

Coughlin uses your Social Insurance Number for the purposes of government reporting, identification and administration of your pension plan. Coughlin may exchange your personal information with the following persons, organizations or parties: financial institutions; government agencies; insurance companies; employers or former employers; your local union; plan trustees; pension advisory committee members; actuaries and auditors. Coughlin may use the personal information on file to provide you with additional information regarding any benefits to which you are entitled.

You have the right to access or update any incorrect information by submitting a request in writing to:

The Privacy OfficerCoughlin & Associates Ltd.P.O. Box 3517, Station COttawa, ON K1Y 4H5

Table of contentsDefinitions ............................................................................................. 1 Define the role of: ............................................................................ 11

Summary of the provisions of the plan ................................................. 13 Purpose ........................................................................................... 13 Mission statement ........................................................................... 13 Effective date .................................................................................. 13 Eligibility ......................................................................................... 14 Enrolment ........................................................................................ 14 Beneficiary designation ................................................................... 14 Participation .................................................................................... 15 Contributions ................................................................................... 15 Vesting ............................................................................................ 17 Locking-in ....................................................................................... 17 Unlocking locked-in funds ............................................................... 18 Benefits on termination ................................................................... 19 Retirement dates ............................................................................. 21 Applying for your pension ................................................................ 24 Form of pension .............................................................................. 25 Amount of pension .......................................................................... 29 Past service credits ......................................................................... 34 Sample calculation .......................................................................... 35 Government programs ..................................................................... 38 Post-retirement contributions .......................................................... 38 Death benefits ................................................................................. 40 Credit splitting on divorce, annulment or separation ........................ 42 Subsequent spouse ......................................................................... 43 Spousal waivers .............................................................................. 43 Remarriage ...................................................................................... 44 Limitations on all payments ............................................................. 44 Restriction on entitlement ................................................................ 44 Assignment ..................................................................................... 44 Investments .................................................................................... 45 Rights to information ....................................................................... 46 Administration ................................................................................. 47

1

Pension Plan

DefinitionsAct

The Pension Benefits Act, RSO, 1990 of Ontario and the regulations thereunder, as amended.

Actuarial equivalent

A benefit of equal value computed upon an actuarial basis recommended by the actuary and approved by the board of trustees.

Actuary

A person who is a Fellow of the Canadian Institute of Actuaries or a firm employing such a person who is appointed actuary for the plan by the trustees.

Additional voluntary contributions

A contribution by the member to the pension fund beyond any amount that he/she is required to make. Such a contribution does not require any additional concurrent contributions by an employer.

Administrator

The person or persons that administer the pension plan as appointed by the trustees.

Annuity

A contract that provides an income for a specified period of time such as a number of years or for life.

Beneficiary

A person, or your estate, entitled under the terms of the plan to receive pre or post-retirement survivor benefits on your death. Under the Pension Benefits Act of Ontario, a spouse (legal or common-law) is automatically the beneficiary unless the appropriate waiver has been filed with the administrator either prior to your death or the commencement of the pension, as applicable.

2

U.A. Local 71

Board of trustees or trustees

The operation and administration of the pension plan shall be the responsibility of the board of trustees. The board of trustees shall be comprised of five trustees named by the union, including one independent trustee who is neither a significant shareholder, partner, proprietor nor an employee of a participating employer.

Canada Revenue Agency (CRA)

The Canada Revenue Agency enforces the provisions of the Income Tax Act.

Cessation of membership or termination in the plan

Cessation of membership or termination in the plan is defined as having ceased employment in the industry for any company under collective agreement with the U.A. Local 71, or for a participating company, for a continuous period of at least two years or more. Nevertheless, a disabled member who qualifies for Workplace Safety and Insurance Board (WSIB) benefits, weekly indemnity, or long-term disability benefits under the U.A. Local 71 Health and Welfare Trust Fund, or who is considered totally and permanently disabled as defined in this booklet, is considered active or employed during that time.

Collective agreement

Collective agreement shall mean any collective agreement between the Ontario Pipe Trades Council of the United Association of Journeymen and Apprentices of the Plumbing and Pipe Fitting Industry of the United States and Canada and the Mechanical Contractors Association of Ontario representing members of the U.A. Local 71. It also includes any modification or amendment of the agreement, by the terms of which the employer agrees to make contributions to the plan, which the board of trustees has agreed to accept.

3

Pension Plan

Commuted value

The commuted value calculation is used to determine the lump sum value of the deferred pension benefit. It is calculated in accordance with the “Standard of Practice for Determining Pension Commuted Values” published by the Canadian Institute of Actuaries effective April 1, 2009, or any successor recommendations adopted by the Canadian Institute of Actuaries. The assumptions and methods used in determining the commuted value must also be acceptable under the Income Tax Act. The commuted value varies with the age of the member and spouse, the amount of benefit accumulated, and the interest rate in effect at the time the calculation is performed.

Company or employer

Company or employer shall mean any of the participating employers accepted for participation in the pension plan by the board of trustees.

Consumer Price Index (CPI)

The Consumer Price Index for Canada (CANSIM V41690914) as published monthly in the Bank of Canada Review.

Continuous

In relation to employment, membership or service, continuous means without regard to periods of temporary suspension of employment, membership or service and without regard to periods of temporary layoff from employment not exceeding two consecutive years in duration. It includes any period to a maximum of one year for which an employee is in receipt of benefits under the Workplace Safety and Insurance Board benefits program.

Corporate trust agreement

The agreement or contract entered into between the trustees and the financial institution appointed by the trustees to invest the fund established under this plan.

4

U.A. Local 71

Credited interest

Investment earnings (losses) credited on post-retirement contributions at rates determined by the trustees at the end of each plan year, having regard to the actual net rates earned by the fund on the basis of the audited financial statements.

For the purposes of determining the rate of credited interest to be credited on post-retirement contributions on an interim basis for refunds, death benefits and retirement benefits payable during the plan year, the administrator will determine the interim rate having regard to the actual net rates earned by the fund after allowing for applicable expenses and for all capital appreciation and depreciation whether realized or unrealized. When information or data is unavailable to determine the present monthly net rate, the administrator will refer to the most recent month(s) of the fiscal period whereby the information is available and project the year-to-date net return on a pro-rata basis to the end of the month prior to the settlement date.

Deferred pension benefit

A pension benefit other than an immediate pension benefit.

Defined benefit plan

A plan that defines the pension to be provided but not the total contributions.

Domestic contract

A domestic contract as defined in Part IV of the Family Law Act.

Employee

A person who is a member, or an employee, of the U.A. Local 71 and is employed on a regular, permanent, salaried or hourly-rated basis; or a person employed by a participating employer.

Employer

Any employer accepted by the board of trustees as a contributing or participating employer.

5

Pension Plan

Enrolment date

The date upon which your enrolment in the plan takes effect.

Financial Services Commission of Ontario (FSCO)

The Financial Services Commission of Ontario is the provincial regulator that enforces the terms of the Pension Benefits Act of Ontario.

Former member

An individual who has either terminated the employment that relates to the pension plan or has terminated membership in the pension plan and satisfies either of the following criteria:

(i) the individual is entitled to a deferred pension payable from the pension fund; or

(ii) he/she is entitled to receive any other payment from the pension fund.

Fund or trust fund

The fund established for purposes of the plan held in trust by the financial institution with whom the trustees have entered into an agreement for this purpose. The assets of the fund are managed by the board of trustees for the benefit of the beneficiaries of the trust.

Government regulations

The Pension Benefits Act of Ontario, the Income Tax Act, and any other provincial or federal legislation similar thereto.

Hourly worker

A member working on an hourly basis under the terms of the collective agreement.

Hybrid plan

A defined benefit plan that has certain attributes normally associated with a defined contribution or money purchase plan.

6

U.A. Local 71

Immediate pension benefit

A pension benefit that is to commence within one year of your entitlement to it.

Locked-in

The legislated conditions that limit the amount of cash refund a member can receive from the plan. Locking-in legislation requires that, under certain conditions, the refund must be used only to provide a pension benefit at retirement.

Locked-in retirement account (LIRA)

A non-commutable registered retirement savings plan as defined in the Income Tax Act.

Member

A person who has satisfied the conditions for membership in the plan and who has neither ceased membership in, nor retired from, the plan.

Money purchase plan

A type of defined contribution plan that is considered the reverse of a defined benefit plan. The cost in a money purchase plan is fixed and the pension benefit is variable. Contributions are accumulated with investment returns and used to purchase an annuity from an insurer or to provide a life income from a non-guaranteed vehicle.

Multi-employer pension plan

A pension plan established and maintained for employees of two or more employers who contributed, or on whose behalf contributions are made, to a pension fund by reason of agreement, statute or municipal by-law to provide a pension benefit that is determined by service with one or more of the employers. It does not include a pension plan where all the employers are affiliated within the meaning of the Business Corporations Act, 1982.

7

Pension Plan

Normal retirement date

The first day of the month coinciding with or next following the attainment of age 60.

Participant

Any member, former member, or retired member, as the context requires.

Participating employer

An employer that has been accepted by the board of trustees for participation in the U.A. Local 71 Pension Plan.

Pension

A monthly pension benefit that is in payment.

Pension benefit

A periodic amount to which under the terms of the plan, the member, member’s spouse, other beneficiary or estate may become entitled.

Pension Benefits Act

The Pension Benefits Act of Ontario and its regulations as amended from time to time, including any other applicable acts of a substantially similar nature adopted by any other province or by the government of Canada.

Plan

The U.A. Local 71 Pension Plan and Trust Fund and any of its amendments or supplements. For the purpose of the Income Tax Act, the pension plan is recognized as a hybrid specified multi-employer pension plan (SMEPP).

Plan year or fiscal year

The 12-month period commencing January 1st and ending December 31st each year.

8

U.A. Local 71

Prescribed

Prescribed by the regulation.

Reciprocal transfer agreement

An agreement related to two or more pension plans that provides for the transfer of money or credits for employment or both in respect of individual members.

Registered retirement savings arrangement

A registered retirement savings plan established in accordance with the Income Tax Act (Canada) or a registered income fund established in accordance with that Act.

Retire, retirement and retiring

Termination of employment with a participating employer or of membership in the U.A. Local 71 on or after the date the member is eligible for a pension benefit. It occurs on the date the member begins to receive an immediate pension, whether or not employment or membership in the local has terminated.

Retired member

An individual is a retired member of a pension plan if he/she has either terminated the employment that relates to the pension plan or has terminated membership in the pension plan and if one or more of the following criteria is also satisfied:

(i) the individual is receiving a pension payable from the pension fund;

(ii) he/she is entitled to begin to receive a pension from the pension fund by virtue of having reached the normal retirement date under the pension plan, even though he/she has not yet elected to receive the pension;

(iii) he/she has elected to receive an early retirement pension;

9

Pension Plan

(iv) he/she has elected, under the terms of the pension plan, to begin payment of a pension payable from the pension fund, whether or not receipt of the first payment of the pension is deferred until a later date.

Service

Continuous employment with a participating employer or continuous membership in the U.A. Local 71 subsequent to the effective date of the plan.

Specified multi-employer plan

A specified multi-employer plan (SMEP) is a multi-employer plan where employers participate under a collective bargaining agreement and there are either 15 or more participating employers or more than 10 per cent of the members work for more than one participating employer. Contributions are made pursuant to a negotiated formula as part of the union contract and do not fluctuate based on the financial experience of the plan.

Spouse

Two people who:

(i) are married to each other; or

(ii) are not married to each other and are living together in a conjugal relationship:

1. continuously for a period of not less than three years; or

2. in a relationship of some permanence if they are the natural or adoptive parents of a child, both as defined in the Family Law Act.

Superintendent

The Superintendent of Financial Services appointed under the Financial Commission of Ontario Act, 1997.

10

U.A. Local 71

Termination

In relation to employment, includes retirement and death.

Total and permanent disability

An individual, suffering from a physical or mental impairment that prevents an individual from engaging in any employment for which he/she is reasonably suited by education, training or experience and that can reasonably be expected to last for the remainder of the individual’s lifetime.

Trust agreement

The agreement that identifies the methods of receipt, investment and disbursement of funds of the plan and trust fund. It contains: provisions for investment powers of trustees; irrevocability and non-diversion of trust assets; payment of legal, trustee and other fees relative to the plan; exculpatory clauses pertaining to the liability of trustees; periodic reports to the employer or union by the trustees; records and accounts to be maintained by the trustees; conditions for removal, resignation or replacement of trustees; benefit payments under the plan; and the rights and duties of the trustees in case of amendment or termination of the plan.

Union

The United Association of Journeymen and Apprentices of the Plumbing and Pipe Fitting Industry of the United States and Canada, Local Union 71 with the geographic jurisdiction being the Regional Municipality of Ottawa Carleton, the Counties of Russell and Lanark, and the County of Renfrew, the City of Cornwall, the Counties of Stormont, Dundas, Glengarry and Prescott, and the Townships of Edwardsburg and Augusta in the County of Grenville; and that part of the County of Grenville east of Edward Street in the Town of Prescott.

Union member

A member in good standing of the U.A. Local 71 and, for contribution purposes, includes travel card members.

11

Pension Plan

Vesting or vested

Vesting refers to the degree to which you are entitled to the pension provided by the employer contributions. Vesting is immediate.

WSIB benefits

Workplace Safety and Insurance Board benefits.

Year of service

A year of service is defined as the accumulation of 1,000 hours in any given calendar year.

Year’s maximum pensionable earnings (YMPE)

Year’s maximum pensionable earnings (YMPE) shall have the meaning prescribed under the Canada Pension Plan (CPP).

Define the role of:Actuary

A person professionally trained in the technical and mathematical aspects of insurance, pensions and related fields. The actuary estimates how much money must be contributed to a pension fund each year to support the benefits that will become payable in the future.

Administrator

The administrator is the board of trustees of the U.A. Local 71 Pension Plan and Trust Fund. The board of trustees can delegate the day-to-day administration to a third-party administrator responsible for the payment of benefits and the provision of other administrative services such as record keeping, accounting and communicating with plan members. The administration has been delegated to Coughlin & Associates Ltd.

12

U.A. Local 71

Auditors

The firm appointed by the board of trustees to conduct a systematic investigation of procedures or operations to assess conformity with prescribed criteria. The auditors certify the accuracy of the financial statements on an annual basis.

Board of trustees

The board of trustees makes the significant policy decisions that give the fund its direction. The board of trustees does not “run” the fund in an operational sense. It delegates the day-to-day administration to a professional administrator.

Consultant

The party appointed by the board of trustees responsible for advising on the general management of the fund, ensuring that the plan is in compliance with the government regulations, drafting of the plan’s policies, reviewing and maintaining contracts and providing any other services required by the trustees.

Custodian

The trust company that holds in custody and safekeeping the securities (i.e. stocks, bonds, certificates, etc.) and other assets of the trust.

Investment manager

A professional money manager appointed by the board of trustees to make the decisions relative to the asset mix and security selection of the fund’s portfolio. All transactions are executed by the custodian.

NOTE: In this plan, words denoting the masculine gender include the feminine gender, and the singular includes the plural, unless the context specifically provides otherwise.

13

Pension Plan

Summary of the provisions of the planPURPOSE

Q. What is the purpose of the pension plan?

A. The purpose of the pension plan is to provide retirement benefits to you on your retirement. As well, the plan provides benefits on the termination of your membership or your death prior to retirement. These are in addition to those benefits provided through the Canada/Quebec Pension Plan and Old Age Security. The plan may also provide benefits to your surviving spouse.

MISSION STATEMENT

Q. What is the plan’s mission statement?

A. The pension plan’s mission is to advance the financial benefit security of all plan members and beneficiaries by providing fully funded pension benefits for reasonable and stable contribution rates.

The plan will:

• provide efficient and effective investment management designed to achieve the highest possible return at an acceptable level of risk;

• create and maintain an environment that promotes the interests of plan members and beneficiaries;

• provide high quality, cost effective service to plan members and beneficiaries; and

• provide effective and efficient governance processes.

EFFECTIVE DATE

Q. When did the plan become effective?

A. The effective date of the plan is November 1, 1971. This booklet includes all revisions to January 1, 2015.

14

U.A. Local 71

ELIGIBILITY

Q. Who is eligible, AS AT the effective date of the plan?

A. Persons who were members in good standing of the U.A. Local 71 on November 1, 1971 were eligible to join the plan as of that date.

Q. Who is eligible, AFTER the effective date of the plan?

A. If you became a member of the U.A. Local 71 after November 1, 1971, you are eligible to join the plan on the first day of the month coincident with or next following the date of your employment.

Employees of the union, owners, contractors and their salaried workers are also eligible to join this plan, subject to approval by the board of trustees, effective on the first day of the month coincident with or next following the date of employment or on November 1, 1971, whichever is later.

ENROLMENT

Q. How do I enrol?

A. You must complete an enrolment form and submit it to the administrator. Forms are available from the union hall or the administrator’s office.

BENEFICIARY DESIGNATION

Q. How do I designate a beneficiary or submit a change of address, marital status or beneficiary?

A. The enrolment form is also used to notify the administrator of a change of personal information including a change to your address, marital status and/or beneficiary designation. Completing a form every time a change is required and submitting it to the administrator will ensure that your file is handled properly.

15

Pension Plan

PARTICIPATION

Q. Is participation in the plan mandatory?

A. Yes. As a condition of employment and as specified in the collective agreement, all eligible members must become members of the pension plan.

CONTRIBUTIONS

Q. How is the plan funded?

A. The plan is funded through employer contributions made at the hourly rate determined in your collective agreement. The contribution rate may change from time to time, as negotiated.

Q. Can I make voluntary contributions?

A. No. Following the introduction of Bill C-52 of the Income Tax Act on June 27, 1990, the practice of transferring funds from the health and welfare to the pension plan was discontinued. Members who made voluntary contributions prior to January 1, 1991, will have the option of purchasing additional amounts of pension at retirement or receiving a refund of these voluntary contributions with accumulated interest upon withdrawal from the plan, the industry or at death.

Q. How much interest is credited on my additional voluntary contributions?

A. Interest on additional voluntary contributions shall be calculated and credited at rates determined by the trustees at the end of each plan year, having regard to the actual net rates earned by the fund on the basis of the audited financial statements.

For the purpose of determining the interim rate of credited interest on additional voluntary contributions for refunds, death benefits and retirement benefits payable during the plan year, the administrator will estimate the interim rate having regard to the actual net rates earned by the fund after

16

U.A. Local 71

allowing for applicable expenses and for all capital appreciation and depreciation, whether realized or unrealized. When information or data is unavailable to determine the present monthly net rate, the administrator will refer to the most recent month(s) of the fiscal period whereby the information is available and project the year-to-date return on a pro-rata basis to the date of settlement.

Q. Will pension contributions continue to be made on my behalf while on maternity, parental or compassionate leave?

A. No. Benefits will not accrue while on maternity, parental or compassionate leave.

Q. Will pension contributions continue to be made on my behalf if I collect long-term disability benefits?

A. No. With the exception of the one-year extension while on WSIB, benefits will not accrue during the period of long-term disability.

Q. If I go on WSIB do I continue to accrue pension benefits?

A. Under Bill 162, if you are absent from work due to an occupational illness or injury, you are entitled to have benefits accrue for a maximum of one year. You must provide copies of the letter of approval from WSIB and copies of the WSIB pay stubs as proof of your eligibility. Your account will be credited with 144 hours for every full month you are in receipt of WSIB benefits to a maximum of 12 months. Partial months will be pro-rated.

Q. Will pension contributions continue to be made on my behalf after I retire?

A. If you return to work for a participating employer after the effective date of your retirement, the contributions made at the hourly rates determined in your collective agreement will be credited to the money purchase provision of the plan.

17

Pension Plan

Q. If I participate in the plan, how do I know how much I can contribute to my RRSP?

A. Since 1990, the Canada Revenue Agency (CRA) issues to each taxpayer a special notice of assessment indicating his/her RRSP contribution limit for the taxation year using his/her earnings and the pension adjustment for the previous year.

Q. What is the Pension Adjustment (PA)?

A. The CRA has introduced measures to equalize the amount each individual may contribute to his/her retirement savings in a given year, regardless of the type of plan under which he/she is covered. The PA is the amount by which your RRSP contribution limit is reduced in recognition of the value of benefit accruals under your pension plan. The higher the value placed on your accrued pension benefits each year, the lower your RRSP contribution room, and vice versa. Your PA is reported each year in Box 52 of your T4 statement.

Q. How is my PA calculated?

A. The PA is calculated in accordance with the terms of the Income Tax Act. Your plan qualifies as a specified multi-employer plan (SMEP). As such, the value of your PA is simply the contributions made to the plan in a given year.

VESTING

Q. Do employer contributions made on my behalf belong to me?

A. Employer contributions made on your behalf must be used to provide a monthly pension at retirement. Vesting is immediate.

LOCKING-IN

Q. When do my pension benefits become “locked-in” under the legislation?

A. All required contributions that have been made by the employer(s) as well as the accumulated pension credits become locked-in once you have been a member of the plan for two years.

18

U.A. Local 71

This means that on termination or retirement, you must accept a deferred or immediate annuity that provides a monthly pension for life. Neither the accumulated funds nor the value of your deferred pension can be withdrawn in a lump sum cash settlement unless:

(i) the amount of pension accrued is less than four per cent of the YMPE as defined yearly by the Canada Pension Plan/Quebec Pension Plan (CPP/QPP). In 2015, this is an amount of $178 of monthly benefit or less ($53,600 x 4% ÷ 12);

(ii) the commuted value of your deferred pension is less than 20 per cent of the YMPE in the year you terminate membership in the plan.

UNLOCKING LOCKED-IN FUNDS

Q. Is there any way for me to access the locked-in funds?

A. You may apply to unlock your pension funds if you suffer from an illness or physical disability that is likely to shorten your life expectancy to less than two years. Application must be made to the plan administrator.

The province of Ontario also allows members who are experiencing financial hardship to apply to their financial institution for consent to withdraw money from an Ontario locked-in retirement account (LIRA), life income fund (LIF) or locked-in retirement income fund (LRIF). It is important to note that this option is not available while your funds are in the U.A. Local 71 Pension Plan. You must first terminate your membership in the plan, transfer your account balance to an Ontario LIRA, LIF or LRIF, and then make application to the financial institution on the prescribed form (Form 6). For information regarding withdrawal for reasons of financial hardship, contact the FSCO directly at (416) 250-7250 or, toll-free, (800) 668-0128, extension 7250.

19

Pension Plan

BENEFITS ON TERMINATION

Q. When can I terminate my membership in the plan?

A. Termination or cessation of membership in the plan is permitted once you have ceased employment for a participating employer and no contributions are due on your behalf for a continuous period of at least two years. You may not terminate your membership while you are deemed totally and permanently disabled as defined in this booklet, or while you are in receipt of Workplace Safety and Insurance Board (WSIB) benefits, weekly indemnity or long-term disability benefits under the U.A. Local 71 Health and Welfare Plan.

Q. What are my options on termination?

A. If your membership in the plan terminates while you are entitled to a deferred pension benefit, you may transfer the commuted value of the deferred pension benefit either:

(i) to the pension fund related to another pension plan registered under the Pension Benefits Act of Ontario, if the administrator of the other pension plan agrees to accept the payment; or

(ii) to a prescribed registered retirement savings plan (includes the LIRA, LIF and LRIF); or

(iii) to purchase a deferred life annuity or annuity that will not commence before the earliest date you would have been entitled to receive payment under the pension plan.

Q. If I terminate my membership in the plan, may I leave the pension benefit credit in the plan until retirement?

A. Yes. You may leave your accrued pension benefit in the plan until you are ready to retire as long as your pension payments commence by the end of the year you attain age 71.

20

U.A. Local 71

Q. How do I apply to transfer funds from the plan?

A. To apply to transfer funds, contact the plan administrator and complete the necessary form(s). The forms currently in use are:

(i) T2151 - Direct Transfer of a Single Amount under Subsection 147(19) or Section 147.3, supplied by the CRA;

(ii) Lock-In Agreement Concerning Transferred Pension Fund Proceeds making reference to the Pension Benefits Act of Ontario and Section 146 of the Income Tax Act.

Both forms are available from any financial institution offering registered retirement savings plans in Ontario, or from the plan administrator.

Q. What limits apply to transfers out of the plan?

A. If the amount of the commuted value of your deferred pension exceeds the amount prescribed under the Income tax Act, the portion that exceeds the prescribed amount will be paid as a lump sum and considered taxable income in the year of withdrawal.

Q. If I remain in the plumbing and pipefitting industry but transfer my union membership to another local or to the Commission de Construction du Québec (CCQ), can I transfer the pension benefit credit to that new local?

A. Yes. You may apply for a permanent transfer of the actuarial equivalent of your pension benefit to the new home local in accordance with the national reciprocal agreement. All future hours remitted to the U.A. Local 71 while you are working in its jurisdiction will be reciprocated to your new home local if you proceed with a permanent transfer. You may also apply for a temporary transfer of the hours you work in the Ottawa jurisdiction while your union membership is with another local or the CCQ.

21

Pension Plan

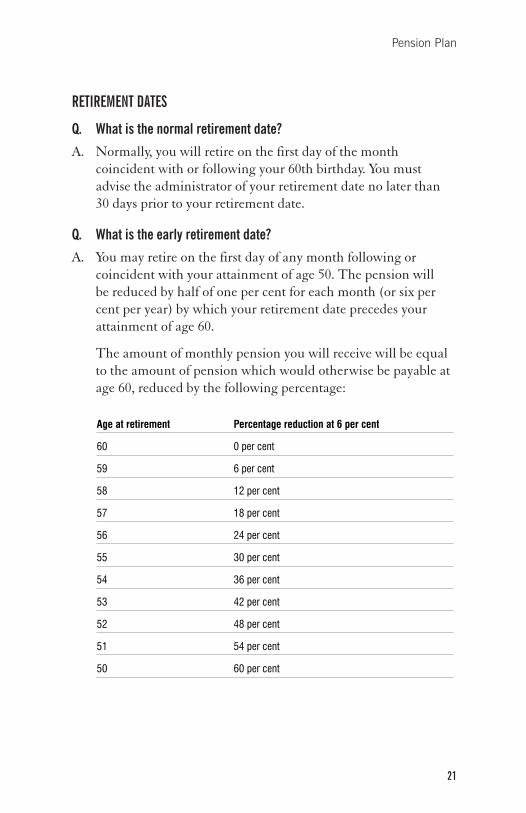

RETIREMENT DATES

Q. What is the normal retirement date?

A. Normally, you will retire on the first day of the month coincident with or following your 60th birthday. You must advise the administrator of your retirement date no later than 30 days prior to your retirement date.

Q. What is the early retirement date?

A. You may retire on the first day of any month following or coincident with your attainment of age 50. The pension will be reduced by half of one per cent for each month (or six per cent per year) by which your retirement date precedes your attainment of age 60.

The amount of monthly pension you will receive will be equal to the amount of pension which would otherwise be payable at age 60, reduced by the following percentage:

Age at retirement Percentage reduction at 6 per cent

60 0 per cent

59 6 per cent

58 12 per cent

57 18 per cent

56 24 per cent

55 30 per cent

54 36 per cent

53 42 per cent

52 48 per cent

51 54 per cent

50 60 per cent

22

U.A. Local 71

Q. What are my options if I become disabled prior to retirement?

A. If you are at least 45 years of age, have completed 10 years of service in the local including at least one current service pension year of credit, and have suffered from a total and permanent disability for a continuous period of not less than six months you may, subject to the approval of the board of trustees, collect a disability pension. To be considered totally and permanently disabled for the purposes of this plan, you must have medical evidence, certified by a qualified medical practitioner, confirming that a condition of total and permanent disability exists. The evidence must not be more than six months old at the time of your application. In addition, the trustees reserve the right to request proof of your application and qualification for WSIB, long-term disability and CPP/QPP disability benefits.

“Totally and permanently disabled” means suffering from a physical or mental impairment that prevents you from engaging in any employment for which you are suited by your education, training or experience and that can reasonably be expected to last for the remainder of your lifetime.

The amount of your disability pension will be equal to the amount of pension accrued to the date of your disability pension eligibility date, without reduction.

The trustees may require that you submit to a re-examination at any time prior to your normal retirement date in order to determine whether you continue to be disabled. If you are found to be no longer disabled or refuse to submit to such examination, your disability pension shall cease. In such case, you may qualify for early or normal retirement and be subject to the applicable terms.

Q. May I postpone my retirement date beyond age 60?

A. Yes, you may postpone your retirement date beyond age 60. The CRA requires that all pensions commence payment by the end of the year in which you attain age 71.

23

Pension Plan

In the event that you made application for your pension after your normal retirement date, your pension will not commence retroactively to your normal retirement date but will commence on the first day of the month following the month in which you last worked, or the first of the month in which the retirement application is received by the administrator, which ever is later. Payment will be made without any interest adjustment on the deferred payments. If you ceased employment and deferred your retirement beyond your normal retirement date, your pension benefit will be actuarially adjusted. Despite the actuarial adjustment, there is no real advantage to waiting to apply for your pension beyond age 60 if you have ceased employment. You must advise the administrator of your postponed retirement date no later than 30 days prior to that date.

Q. May I return to work once I begin to draw my pension?

A. Yes, you may return to work for a participating employer following your retirement from the plan. All post-retirement employer contributions received on your behalf to the end of the calendar year in which you attain age 71 will be credited to the money-purchase provision of the plan. You will be deemed to be a new member of the plan for the purpose of applying the locking-in and portability rules.

Q. How much interest is credited on my post retirement contributions?

A. Interest on post-retirement contributions are calculated and credited at rates determined by the trustees at the end of each plan year, based on the actual net rates earned by the fund as reported in the audited financial statements.

To determine the interim rate of credited interest on post-retirement contributions for refunds, death benefits and retirement benefits payable during the plan year, the administrator will estimate the interim rate based on the actual net rates earned by the fund after allowing for applicable expenses and for all capital appreciation and depreciation, whether realized or unrealized. When information or data

24

U.A. Local 71

is unavailable to determine the present monthly net rate, the administrator will refer to the most recent month(s) of the fiscal period whereby the information is available and project the year-to-date return on a pro-rata basis to the date of settlement.

APPLYING FOR YOUR PENSION

Q. How do I apply for my pension?

A. Once you have decided on a retirement date, notify the administrator at least one month in advance. He/she will send you the appropriate forms for completion and, at your request, will provide any and all information you may require concerning your selection of pension options.

Q. Can I make arrangements to discuss my retirement options with the administrator?

A. Yes, arrangements may be made by contacting the administrator and making an appointment. Spouses are encouraged to attend.

Q. Can I make arrangements to discuss my retirement options and other financial matters with a financial advisor?

A. Yes, the administrator has an individual financial consultant on staff who is available to assist you. There is no consultation fee. You may contact the administrator to arrange an appointment to discuss your retirement, financial planning, estate planning, investments, life insurance and other financial matters.

To allow sufficient time for a proper consultation and thorough planning, it is recommended that you arrange to discuss your pre-retirement planning and investment strategies at least three to five years prior to your anticipated retirement date.

You should also visit your financial advisor six months prior to your effective date of retirement or when your financial, marital or employment situation changes.

25

Pension Plan

Q. Must I submit proof of age or marriage?

A. Yes. You are required to furnish proof of your date of birth before any pension payments are made to you. If you elect a type of pension that depends on the survivorship of your spouse, you are required to furnish proof of age of your spouse as well as a copy of the marriage certificate, if applicable, and a declaration of marital status.

FORM OF PENSION

Q. What is the normal form of pension?

A. The normal form of pension is a joint and last survivor annuity reducing to 60 per cent on the later of your death or the end of the five-year guarantee. This pension is payable for as long as you live. Should you predecease your spouse within the first five years, the payments will continue to your spouse at 100 per cent until the end of the guarantee period, at which time, they would reduce to 60 per cent and continue for your spouse’s lifetime. In the event that you and your spouse die within the guarantee period, the payments would continue to the designated beneficiary or estate until the end of the guarantee period.

RetirementDate

Member’s life line

Member dies$600 Monthly

Spouse’s life line

$1,000 Monthly 5 yrs 10 yrs 15 yrs

Member and Spouse die Benefit paid to end of 5th year

Spouse dies Payments stop

26

U.A. Local 71

The requirement or option to provide a joint and last survivor annuity does not apply where you and your spouse are living separate and apart on the date of your retirement.

Q. What other forms of pension are available?

A. The plan provides other optional forms of pension as follows:

LIFE ANNUITIES

1. Single life annuity with no guaranteed period

Under this form of payment, you will receive a monthly income for as long as you live. The monthly income will cease upon your death, which means no death benefits are payable to a spouse, beneficiary or estate. Since payments stop immediately after you die, this form of annuity may suit you if you are single and have no dependants.

2. Single life annuity with a minimum guaranteed period

Under this form of payment, you will receive a monthly income as long as you live. In addition, should you die before a specified number of payments have been made (usually 60, 120 or 180), the balance of the payments are continued to a named beneficiary or estate.

The amount of pension income you would receive under this option is less than the life annuity only option as there is a guarantee that payments will be made for a specified period.

Example:

If you choose a life annuity with a 10-year guarantee, you will receive a monthly payment as long as you live, with

RetirementDate

$1,000 Monthly

Member’s life linePayments terminate on member’s death

27

Pension Plan

the provision that if you die before receiving 120 monthly payments, your named beneficiary or estate will continue to receive the balance of your monthly payments until a total of 120 payments have been made. The present value of the remaining payments may be paid in a lump sum as an alternative to the continuation of monthly instalments. Once this provision has been met, no further payment will be made.

3. Joint and last survivor annuity

Under this form of payment, you will receive a monthly income as long as you live. Should you predecease the joint annuitant (your spouse), the payments will continue to your spouse at the chosen percentage for the spouse’s lifetime. When both you and your spouse are deceased, payments cease.

Your plan offers survivor benefits of 60 per cent or 100 per cent of the amount payable immediately prior to your death.

RetirementDate

$1,000 Monthly 5 yrs 10 yrs 15 yrs

Member’s life line

Member diesPayments continue to beneficiary until end of 10th year

RetirementDate

$1,000 Monthly

Member’s life line

Member dies Payments continue to spouse for life

$600 Monthly

Spouse’s life line

28

U.A. Local 71

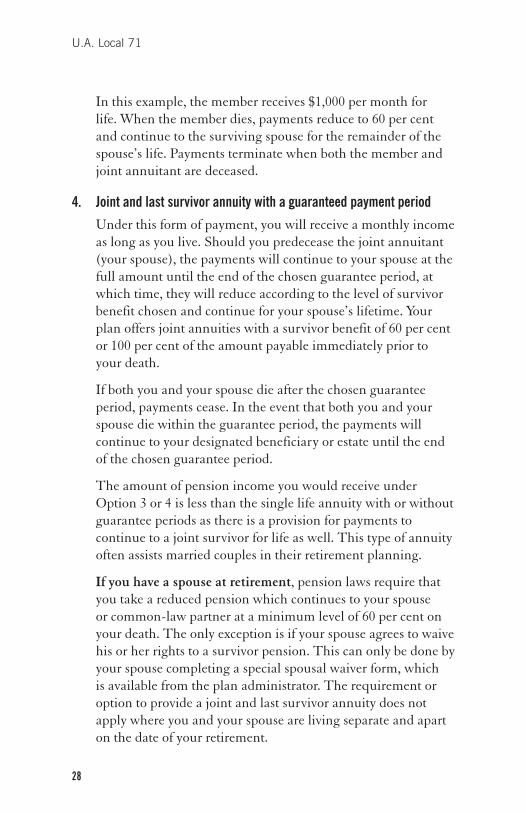

In this example, the member receives $1,000 per month for life. When the member dies, payments reduce to 60 per cent and continue to the surviving spouse for the remainder of the spouse’s life. Payments terminate when both the member and joint annuitant are deceased.

4. Joint and last survivor annuity with a guaranteed payment period

Under this form of payment, you will receive a monthly income as long as you live. Should you predecease the joint annuitant (your spouse), the payments will continue to your spouse at the full amount until the end of the chosen guarantee period, at which time, they will reduce according to the level of survivor benefit chosen and continue for your spouse’s lifetime. Your plan offers joint annuities with a survivor benefit of 60 per cent or 100 per cent of the amount payable immediately prior to your death.

If both you and your spouse die after the chosen guarantee period, payments cease. In the event that both you and your spouse die within the guarantee period, the payments will continue to your designated beneficiary or estate until the end of the chosen guarantee period.

The amount of pension income you would receive under Option 3 or 4 is less than the single life annuity with or without guarantee periods as there is a provision for payments to continue to a joint survivor for life as well. This type of annuity often assists married couples in their retirement planning.

If you have a spouse at retirement, pension laws require that you take a reduced pension which continues to your spouse or common-law partner at a minimum level of 60 per cent on your death. The only exception is if your spouse agrees to waive his or her rights to a survivor pension. This can only be done by your spouse completing a special spousal waiver form, which is available from the plan administrator. The requirement or option to provide a joint and last survivor annuity does not apply where you and your spouse are living separate and apart on the date of your retirement.

29

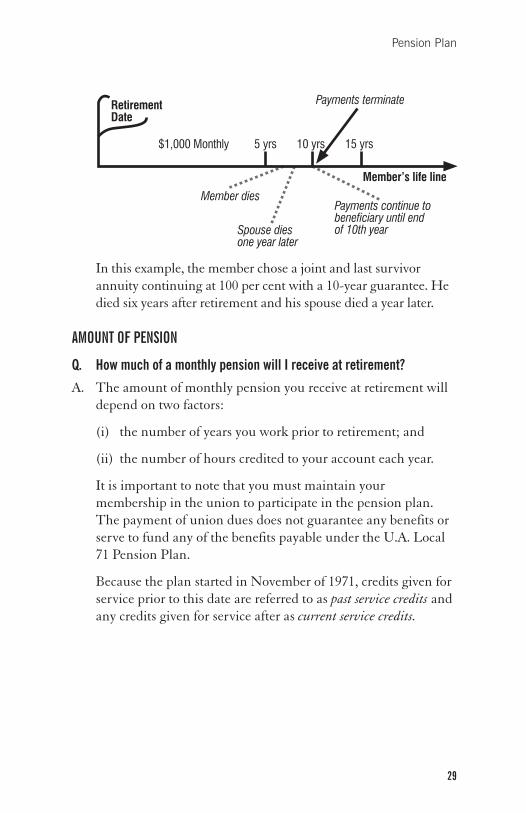

Pension Plan

In this example, the member chose a joint and last survivor annuity continuing at 100 per cent with a 10-year guarantee. He died six years after retirement and his spouse died a year later.

AMOUNT OF PENSION

Q. How much of a monthly pension will I receive at retirement?

A. The amount of monthly pension you receive at retirement will depend on two factors:

(i) the number of years you work prior to retirement; and

(ii) the number of hours credited to your account each year.

It is important to note that you must maintain your membership in the union to participate in the pension plan. The payment of union dues does not guarantee any benefits or serve to fund any of the benefits payable under the U.A. Local 71 Pension Plan.

Because the plan started in November of 1971, credits given for service prior to this date are referred to as past service credits and any credits given for service after as current service credits.

RetirementDate

$1,000 Monthly 5 yrs 10 yrs 15 yrs

Member’s life line

Member diesPayments continue to beneficiary until end of 10th yearSpouse dies

one year later

Payments terminate

30

U.A. Local 71

HISTORICAL PENSION CREDIT TABLE (Entitlement to benefit improvements is subject to eligibility criteria)

Period Original Credits 1st 2nd

Monthly credit for minimum of 1,500 hours

1971/11/01 to 1972/12/31 $4.0000 $8.0000 $10.0000

1973/01/01 to 1973/12/31 $4.0000 $8.0000 $10.0000

1974/01/01 to 1974/12/31 $4.0000 $8.0000 $10.0000

PLUS Monthly credit for minimum of 1,800 hours

1975/01/01 to 1975/12/31 $6.0000 $12.0000 $15.0000

1976/01/01 to 1976/12/31 $6.0000 $12.0000 $15.0000

1977/01/01 to 1977/12/31 $6.0000 $12.0000 $15.0000

OR Monthly credit per 100 hours if <1,800 hours

1975/01/01 to 1975/12/31 $0.3330 $0.6660 $0.8333

1976/01/01 to 1976/12/31 $0.3330 $0.6660 $0.8333

1977/01/01 to 1977/12/31 $0.3330 $0.6660 $0.8333

PLUS Rate per 100 hours

1978/01/01 to 1978/12/31 $0.5000 $1.0000 $1.2500

1979/01/01 to 1979/12/31 $0.5000 $1.0000 $1.2500

1980/01/01 to 1980/12/31 $1.0000 $2.0000 $2.5000

1981/01/01 to 1981/12/31 $1.0000 $2.0000 $2.5000

1982/01/01 to 1982/12/31 $1.0000 $2.0000 $2.5000

1983/01/01 to 1983/12/31 $1.0000 $2.0000 $2.5000

1984/01/01 to 1984/12/31 $1.0000 $2.0000 $2.5000

1985/01/01 to 1985/12/31 $2.2500

1986/01/01 to 1986/12/31 $2.2500

1987/01/01 to 1987/12/31 $2.2500

1988/01/01 to 1988/12/31 $2.2500

1989/01/01 to 1989/12/31 $2.2500

1990/01/01 to 1990/12/31 $2.2500

31

Pension Plan

Pension credit following benefit improvement

3rd 4th 5th 6th 7th 8th

Monthly credit for minimum of 1,500 hours

$10.0000 $10.8000 $10.8000 $11.8800 $13.6600 $15.0260

$10.0000 $10.8000 $10.8000 $11.8800 $13.6600 $15.0260

$10.0000 $10.8000 $10.8000 $11.8800 $13.6600 $15.0260

Monthly credit for minimum of 1,800 hours

$15.0000 $16.2000 $16.2000 $17.8200 $20.4900 $22.5390

$15.0000 $16.2000 $16.2000 $17.8200 $20.4900 $22.5390

$15.0000 $16.2000 $16.2000 $17.8200 $20.4900 $22.5390

Monthly credit per 100 hours if <1,800 hours

$0.8333 $0.9000 $0.9000 $0.9900 $1.1385 $1.2524

$0.8333 $0.9000 $0.9000 $0.9900 $1.1385 $1.2524

$0.8333 $0.9000 $0.9000 $0.9900 $1.1385 $1.2524

Rate per 100 hours

$1.2500 $1.3500 $1.3500 $1.4850 $1.7078 $1.8786

$1.2500 $1.3500 $1.3500 $1.4850 $1.7078 $1.8786

$2.5000 $2.7000 $2.7000 $2.9700 $3.4155 $3.7571

$2.5000 $2.7000 $2.7000 $2.9700 $3.4155 $3.7571

$2.5000 $2.7000 $2.7000 $2.9700 $3.4155 $3.7571

$2.5000 $2.7000 $2.7000 $2.9700 $3.4155 $3.7571

$2.5000 $2.7000 $2.7000 $2.9700 $3.4155 $3.7571

$2.5000 $2.7000 $2.7000 $2.9700 $3.4155 $3.7571

$2.6000 $2.8100 $2.8100 $3.0910 $3.5547 $3.9102

$2.7000 $2.9200 $2.9200 $3.2120 $3.6940 $4.0634

$2.8000 $3.0200 $3.3200 $3.6520 $4.2000 $4.6200

$2.9000 $3.1300 $3.4400 $3.7840 $4.3516 $4.7868

$3.0000 $3.2400 $3.5600 $3.9160 $4.5034 $4.9537

32

U.A. Local 71

HISTORICAL PENSION CREDIT TABLE(Entitlement to benefit improvements is subject to eligibility criteria)

Period Original Credits 1st 2nd

1991/01/01 to 1991/12/31 $3.2500

1992/01/01 to 1992/12/31 $3.2500

1993/01/01 to 1993/12/31 $3.8350

1994/01/01 to 1994/12/31 $4.0630

1995/01/01 to 1995/12/31 $5.1100

1996/01/01 to 1996/12/31 $5.1100

1997/01/01 to 1997/12/31 $5.1100

1998/01/01 to 1998/12/31 $5.1100

1999/01/01 to 1999/12/31 $5.7500

2000/01/01 to 2000/12/31 $5.7500

2001/01/01 to 2001/12/31 $5.7500

2002/01/01 to 2002/12/31 $5.7500

2003/01/01 to present $6.3250

33

Pension Plan

Pension credit following benefit improvement

3rd 4th 5th 6th 7th 8th

$3.6700 $4.0400 $4.4440 $5.1106 $5.6217

$3.8400 $4.2200 $4.6420 $5.3383 $5.8721

$4.2700 $4.6970 $5.4015 $5.9417

$4.8800 $5.3680 $6.1732 $6.7905

$5.6210 $6.4642 $7.1106

$5.8765 $6.4642

$5.8765 $6.4642

$5.8765 $6.4642

$6.3250

$6.3250

$6.3250

$6.3250

The amount of these pension credits in dollars of monthly pension is subject to change. Such a change may result from a new negotiated collective agreement or the fund’s investment earnings. The above table illustrates the results of eight retroactive benefit improvements that allocated any surplus that accumulated in the fund back to its active or retired members. You must meet the eligibility criteria to qualify for each of the benefit improvements illustrated above.

34

U.A. Local 71

PAST SERVICE CREDITSThe plan has been designed to provide pension credits to those who were members prior to the effective date of the plan, namely November 1, 1971. A past service pension credit of $4.00 of monthly pension for each full year of membership prior to November 1, 1971, has been credited to those eligible up to a maximum of ten years or $40.00 of monthly past service pension. Past service pension credits have since been increased.

The following table illustrates the amounts of past service credits for which you may be eligible:

Pension credits Pension credits Original pension following latest Initiation date in years credits in dollars $ benefit improvement $

Before 1961/11/01 10 40.00 54.65

1961/11/01 to 1962/10/31 9 36.00 49.18

1962/11/01 to 1963/10/31 8 32.00 43.71

1963/11/01 to 1964/10/31 7 28.00 38.26

1964/11/01 to 1965/10/31 6 24.00 32.79

1965/11/01 to 1966/10/31 5 20.00 27.32

1966/11/01 to 1967/10/31 4 16.00 21.86

1967/11/01 to 1968/10/31 3 12.00 16.39

1968/11/01 to 1969/10/31 2 8.00 10.93

1969/11/01 to 1970/10/31 1 4.00 5.47

After 1970/11/01 0 0.00 0.00

To be eligible for the past service credits, a member must have accumulated at least 300 contribution hours in the first year of the plan.

35

Pension Plan

SAMPLE CALCULATIONMember’s date of birth 1959/01/04

Member’s date of entry 1978/08/31

Normal retirement date 2019/02/01

Spouse’s date of birth 1961/06/29

Actual retirement date 2014/08/01

Assume member worked 1,500 hours every year from 1978 to 2013 and worked 1,000 hours in 2014.

Current service credits Rate per 100 hours Annual credit $ Total credits $

1978/01/01 to 1979/12/31 1.8786 28.18 56.36

1980/01/01 to 1985/12/31 3.7571 56.36 338.16

1986/01/01 to 1986/12/31 3.9102 58.65 58.65

1987/01/01 to 1987/12/31 4.0634 60.95 60.95

1988/01/01 to 1988/12/31 4.6200 69.30 69.30

1989/01/01 to 1989/12/31 4.7868 71.80 71.80

1990/01/01 to 1990/12/31 4.9537 74.31 74.31

1991/01/01 to 1991/12/31 5.6217 84.33 84.33

1992/01/01 to 1992/12/31 5.8721 88.08 88.08

1993/01/01 to 1993/12/31 5.9417 89.13 89.13

1994/01/01 to 1994/12/31 6.7905 101.86 101.86

1995/01/01 to 1995/12/31 7.1106 106.66 106.66

1996/01/01 to 1998/12/31 6.4642 96.96 290.88

1999/01/01 to 2013/12/31 6.3250 94.88 1,423.20

2014/01/01 to 2014/07/31 6.3250 94.88 63.25

36

U.A. Local 71

Current service credits = $2,958.13 Total monthly pension = $2,958.13

Based on joint and last survivor annuity, reducing to 60 per cent, with five-year guarantee.

Early retirement on August 1, 2014Pensionable service as illustrated above

Reduction: 6 per cent per year

Your age Reduced monthly pension

59.0 $2,958.13 x 94% = $2,780.65

58.0 $2,958.13 x 88% = $2,603.16

57.0 $2,958.13 x 82% = $2,425.67

56.0 $2,958.13 x 76% = $2,248.18

55.5 $2,958.13 x 73% = $2,159.44

Please note: If you retire early, the early retirement penalty will apply as long as the pension is payable. The unreduced amount will not be reinstated upon attaining age 60 or 65.

The following table illustrates the normal and optional forms of pension available to you and your spouse, if applicable, based on a retirement age of 60, a monthly pension of $2,958.13, and certain actuarial assumptions:

37

Pension Plan

SAMP

LE C

ALCU

LATIO

NFo

rm o

f pen

sion

M

onth

ly p

ensi

on $

Sp

ouse

’s m

onth

ly p

ensi

on $

Life

gtd

. 5 y

ears

3,

251.

36

Life

gtd

. 10

year

s 3,

200.

17

Life

gtd

. 15

year

s 3,

121.

96

Join

t and

60

per c

ent s

urvi

vor

2,96

3.63

1,

778.

18

Join

t and

60

per c

ent s

urvi

vor g

td. 5

yea

rs

2,95

8.13

1,

774.

88

Join

t and

60

per c

ent s

urvi

vor g

td. 1

0 ye

ars

2,94

0.12

1,

764.

07

Join

t and

60

per c

ent s

urvi

vor g

td. 1

5 ye

ars

2,91

0.03

1,

746.

02

Join

t and

100

per

cen

t sur

vivo

r 2,

790.

33

2,79

0.33

Join

t and

100

per

cen

t sur

vivo

r gtd

. 5 y

ears

2,

790.

36

2,79

0.36

Join

t and

100

per

cen

t sur

vivo

r gtd

. 10

year

s 2,

789.

03

2,78

9.03

Join

t and

100

per

cen

t sur

vivo

r gtd

. 15

year

s 2,

784.

04

2,78

4.04

The

abo

ve a

mou

nts a

re fo

r illu

stra

tion

purp

oses

onl

y ba

sed

on fa

ctor

s app

licab

le a

t the

tim

e of

cal

cula

tion.

T

he a

mou

nts a

re a

lso

subj

ect t

o an

nual

par

tial i

ndex

atio

n ad

just

men

ts. T

he sp

ouse

’s pe

nsio

n is

onl

y pa

yabl

e on

you

r dea

th.

38

U.A. Local 71

Q. Are my pension benefits indexed?

A. No. Since January 1, 2014, indexation adjustments are no longer applicable.

Q. Does this pension affect my entitlement to CPP or OAS benefits?

A. No. The pension you earn with the U.A. Local 71 Pension Plan is payable in addition to the Canada or Quebec Pension Plans (CPP/QPP) and Old Age Security (OAS).

GOVERNMENT PROGRAMSAs of January 2015, the maximum benefits available at age 65 are:

(i) Canada Pension Plan (CPP) ($1,065.00/month); or

(ii) Quebec Pension Plan (QPP) ($1,065.00/month); and

(iii) Old Age Security (OAS) ($563.74/month).

You may begin to receive the Canada Pension Plan or Quebec Pension Plan (CPP/QPP) benefits as early as age 60 or as late as age 70. The benefit amount will be reduced (if taken prior to age 65) or increased (if taken after age 65) by a monthly adjustment factor. Please refer to www.servicecanada.gc.ca for additional details.

If your net income exceeds $71,592, you must repay part or all of the Old Age Security (OAS) pension amount. The full OAS is eliminated when your net income is $115,716 or above.

POST-RETIREMENT CONTRIBUTIONS

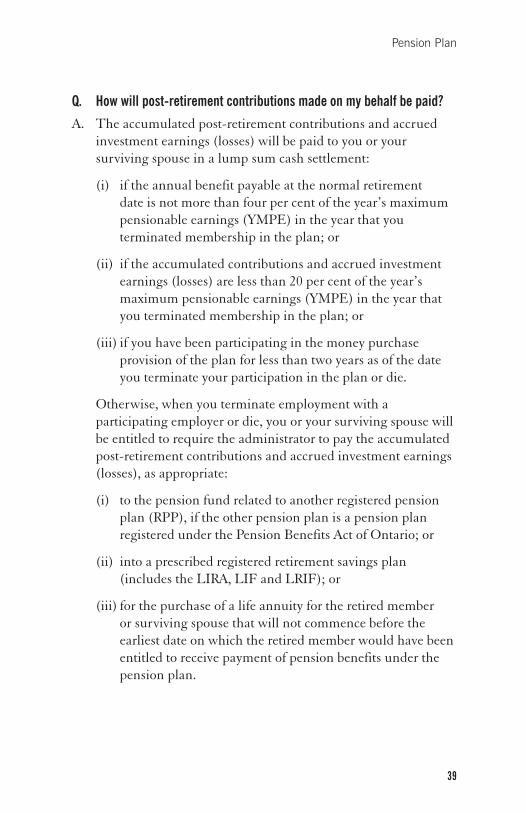

Q. When will post-retirement contributions made on my behalf be paid to me?

A. The post-retirement contributions credited to the money purchase provision of the plan will be determined at the date you return to retired member status. They will be based upon the total of the post-retirement contributions made on your behalf together with the net investment earnings (losses) accrued to the end of the month prior to the date of settlement.

39

Pension Plan

Q. How will post-retirement contributions made on my behalf be paid?

A. The accumulated post-retirement contributions and accrued investment earnings (losses) will be paid to you or your surviving spouse in a lump sum cash settlement:

(i) if the annual benefit payable at the normal retirement date is not more than four per cent of the year’s maximum pensionable earnings (YMPE) in the year that you terminated membership in the plan; or

(ii) if the accumulated contributions and accrued investment earnings (losses) are less than 20 per cent of the year’s maximum pensionable earnings (YMPE) in the year that you terminated membership in the plan; or

(iii) if you have been participating in the money purchase provision of the plan for less than two years as of the date you terminate your participation in the plan or die.

Otherwise, when you terminate employment with a participating employer or die, you or your surviving spouse will be entitled to require the administrator to pay the accumulated post-retirement contributions and accrued investment earnings (losses), as appropriate:

(i) to the pension fund related to another registered pension plan (RPP), if the other pension plan is a pension plan registered under the Pension Benefits Act of Ontario; or

(ii) into a prescribed registered retirement savings plan (includes the LIRA, LIF and LRIF); or

(iii) for the purchase of a life annuity for the retired member or surviving spouse that will not commence before the earliest date on which the retired member would have been entitled to receive payment of pension benefits under the pension plan.

40

U.A. Local 71

DEATH BENEFITS

From defined benefit plan

Q. What happens to the pension credits that I have accumulated if I die before retirement?

A. When you die before the commencement of your pension and have a surviving spouse at the time, your spouse is entitled:

(i) to receive a lump sum payment equal to the commuted value of the deferred pension; or

(ii) to purchase an immediate or deferred pension, the commuted value of which is at least equal to the commuted value of the deferred pension. The benefit must begin no later than one year following your death and the end of the calendar year in which your surviving spouse attains 71 years of age; or

(iii) to purchase a registered retirement income fund (RRIF) or registered retirement savings plan (RRSP) that meets the requirements under the Income Tax Act; or

(iv) to transfer the commuted value to the pension fund related to another pension plan registered under the Pension Benefits Act of Ontario, provided the administrator of the other pension plan agrees to accept the payment.

From money purchase provision

Q. What happens to the post-retirement contributions made on my behalf if I die?

A. Any post-retirement contributions made on your behalf and deposited to the money purchase provision of the plan shall be paid to your spouse on your death. Your surviving spouse is entitled to require the administrator to pay the accumulated post-retirement contributions with accrued investment earnings (losses):

41

Pension Plan

(i) in a lump sum payment; or

(ii) into a registered retirement savings arrangement; or

(iii) to purchase an immediate or deferred pension.

These provisions do not apply if you and your spouse are living separate and apart at the date of your death, or if your spouse signed a waiver of pre-retirement death benefit prior to your demise.

Where no surviving spouse exists, or where you and your spouse are living separate and apart, your designated beneficiary or estate will receive the commuted value in a lump sum cash settlement.

Q. How long does my spouse have to decide on his/her options after my death?

A. The law requires a surviving spouse to notify the administrator and make a decision on the necessary forms within 90 days from the date of death. Otherwise, he/she will be deemed to have elected to receive an immediate pension.

Q. If I am married, can I designate a beneficiary other than my spouse?

A. Yes, you may designate a beneficiary other than your spouse. However, to do so, your spouse must complete a spousal waiver where the spouse gives up all rights to a benefit on your death. These forms are available at the administrator’s office and must be filed with the administrator prior to the death of the member. You will be required to have the waiver notarized at your expense or witnessed by a pension administrator. Your spouse will also be required to provide photo identification.

Q. What happens to my pension if I die after retirement?

A. If you die after you begin receiving a monthly pension, the amount of any further benefit will be determined by the form of pension you chose at retirement.

42

U.A. Local 71

Upon your death, the plan may pay the commuted value of the joint and last survivor benefit to the joint annuitant if, at the date of your death:

(i) the annual benefit payable is not more than four per cent of the YMPE; or

(ii) the commuted value of the benefit is less than 20 per cent of the YMPE.

Your surviving spouse may require the administrator to pay the commuted value into a registered retirement savings arrangement by delivering a direction to the administrator within the prescribed period.

Q. Is the death benefit taxable?

A. Yes, the death benefit is taxable. If your surviving spouse wishes to defer the taxation, he/she may transfer the commuted value to a registered retirement savings plan. This option is not available to a beneficiary other than the surviving spouse.

CREDIT SPLITTING ON DIVORCE, ANNULMENT OR SEPARATION

Q. Is my spouse entitled to any portion of my pension on marriage breakdown?

A. Yes, under the Family Law Act of Ontario, your spouse is entitled to a maximum of 50 per cent of the pension credits that you accumulated during your relationship. The pension plan administrator shall request such information as is required to calculate and pay the pension or pension benefit. Such information may include the sections of the court order, separation agreement or other document addressing the division of property on breakdown of a spousal relationship.

Former spouses of plan members may receive an immediate payment of their share of the pension assets, either as a lump sum transfer or a division of monthly pension payments. In any case, the pension credits assigned to your spouse continue to be subject to the lock-in provisions.

43

Pension Plan

Q. How is the value of my spouse’s share determined?

A. The valuation of pension assets will be calculated by the plan administrator, in accordance with formulas set out in the new family law regulations made under the Pension Benefits Act.

The parties must apply directly to the plan administrator to get the valuation of pension assets, using the prescribed application for family law value forms.

The plan administrator may charge a fee to provide the calculations.

SUBSEQUENT SPOUSEIn the event you remarry, your subsequent spouse has no entitlement to the benefits assigned to a former spouse.

SPOUSAL WAIVERSPension legislation protects the rights of your spouse. It is important for you to realize that your spouse or common-law partner is entitled to different types of pension benefits at different times during your membership in the plan. For example, although your spouse may agree to waive his/her entitlement to a pre-retirement death benefit, this does not affect his/her entitlement to pension benefits on marriage breakdown, or on your death after retirement.

There are basically three triggering events:

(i) legal separation or divorce;

(ii) retirement; and

(iii) death.

Three distinct waivers are required. On legal separation or divorce, your former spouse is entitled to a maximum of 50 per cent of the assets accumulated during the relationship. On retirement, you must select a form of pension which will provide a survivor pension of at least 60 per cent of the amount payable prior to your death. On death prior to retirement, your surviving spouse is entitled to 100 per cent of the assets in your account, less any assets which were previously assigned to a former spouse or common-law partner.

44

U.A. Local 71

All waivers must be notarized at your expense or witnessed by a pension administrator. Photo identification of your spouse will also be required.

Please contact the plan administrator for assistance with any of these issues.

REMARRIAGEIf the spouse of a deceased former member or retired member is receiving a pension under the pension plan, he/she is still entitled to receive a pension under the pension plan, despite becoming the spouse of another person.

LIMITATIONS ON ALL PAYMENTSThe entitlements under this plan are subject to the prescribed limitations in respect of the transfer of funds from pension funds. If the amount of the commuted value of the deferred pension is greater than the amount prescribed under the Income Tax Act, the administrator shall pay the portion that exceeds the prescribed amount as a lump sum, less applicable taxes, to the person entitled to the benefit.

RESTRICTION ON ENTITLEMENTAn entitlement to a benefit under this plan is subject to any rights to or interest in the benefit set out in an order made under Part I (Family Property) of the Family Law Act, a family arbitration award or a domestic contract.

ASSIGNMENT

Q. Can I use my pension benefits as collateral to borrow money? Can my pension benefits be seized on bankruptcy?

A. No. The law prohibits the assignment of any pension benefits except in the case of marriage breakdown. This provision is for your protection and is intended to ensure that you will receive a pension when you retire.

45

Pension Plan

INVESTMENTS

Q. Where are the funds being invested?

A. As of January 2015, the assets of the fund are managed by 11 investment management firms. Each manager has its own mandate as follows:

Investment manager Mandate Per cent of assets

Brookfield Asset Management US commercial mortgages 3.50 per cent

BTG Pactual Brazil Timberland Fund I Timberland fund 3.50 per cent

Burgundy Asset Management Ltd. Special equity 28.87 per cent

Canso Investment Counsel Ltd. Fixed income 9.27 per cent

CI Institutional Asset Management Canadian equity 5.05 per cent

Glovista Investments LLC. Emerging markets equity 4.52 per cent

Hillsdale Investment Management Inc. Canadian equity 4.40 per cent

Jarislowsky Fraser Limited Investment Counsel Special equity 8.75 per cent

Manulife Asset Management Asian equity 3.00 per cent

State Street Global Advisors Ltd. Currency hedging Overlay

Trez Capital Mortgage fund 5.00 per cent

Other Placements:

Limited partnerships Variable rate mortgages 12.76 per cent

Private mortgages Private mortgages 1.07 per cent

Private equity Private equity 5.31 per cent

Valleyview Lands LLP Domestic real estate 5.00 per cent

The asset mix, performance objectives, and manager mandates are outlined in a statement of investment policies and procedures (SIP&P) and reviewed regularly.

46

U.A. Local 71

RIGHTS TO INFORMATION

Q. How will I know how much pension I have accumulated?

A. Each year, the administrator will forward to your home address a pension statement outlining the amount of pension, the retirement dates, the name of your beneficiary, etc. It is important that the information on this statement be accurate. If this is not the case, the administrator should be notified immediately.

Q. Once an amendment to the plan has been made, will I be notified?

A. Yes, once a plan amendment has been registered with the FSCO, the administrator has 60 days to notify in writing all members affected by the amendment.

Q. When a new member enrols in the plan, what information is provided?

A. Each member is entitled to receive a booklet outlining the general provisions of the plan. He/she is also entitled to inspect the registered documents with the FSCO on written request.

Q. What other sources of information am I entitled to receive?

A. On termination, retirement or death, you or your surviving spouse shall receive a written statement of your entitlements and options.

Once a year, you are also entitled to inspect or copy all documents that support or relate to the plan and its operation. You must file a written request with the administrator to review or obtain a copy of the documents. The administrator is entitled to charge a reasonable amount ($0.25 per page for each paper copy and $5 for each request for one or more records provided by electronic means) for any copies that are provided. The documents that you may review or copy include but are not limited to:

(i) pension plan documents and all amendments;

47

Pension Plan

(ii) previous versions of plan documents and amendments;

(iii) documents that set out the plan sponsor’s responsibilities to the pension plan;

(iv) documents appointing a plan or fund administrator;

(v) copies of all documents required to be filed with the FSCO (i.e. annual information returns, audited financial statements, trust agreement and amendments);

(vi) copy of statement of investment policies and procedures; and/or

(vii) copies of all correspondence between the administrator and the FSCO staff, except for correspondence respecting individual plan members.

Q. Who should be contacted for more information?

A. The administrator, Coughlin & Associates Ltd., should be contacted for information regarding the plan.

ADMINISTRATION

Q. Who administers the plan?

A. The board of trustees of the U.A. Local 71 Pension Plan is responsible for its administration. The daily administration is handled by Coughlin & Associates Ltd., a third-party administrator.

Q. Can the plan be changed or discontinued?

A. The board of trustees can change the plan provided:

(i) the change does not contravene any provisions of the applicable collective agreements and trust agreement;