turning the page webinar - fhlbny

TRANSCRIPT

FHLBNY

FHLBNY

Presentation from the FHLBNY to:

© 2021 FEDERAL HOME LOAN BANK OF NEW YORK • 101 PARK AVENUE • NEW YORK, NY 10178 • WWW.FHLBNY.COM

Turning the Page: The U.S. and

Local Economic Outlook

Brian Jones, Vice President & Financial Economist, FHLBNY

February 11, 2021

FHLBNY

FHLBNY

Recent Data Continue to Eclipse Economists’ Expectations

Note: Shaded areas denote recessions. Sources: Citi Investment Research, Bureau of Labor Statistics, U.S. Commerce Department,

Federal Reserve System, Institute for Supply Management

93.495.0

96.7

105.8

106.3

116.7

103.5

118.8

70

80

90

100

110

120

130

70

80

90

100

110

120

130

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

Recent Performances of Key Economic Variables(Index February Cycle Peak = 100)

Nonfarm Payrolls Total Hours Worked Industrial ProductionControl Retail Sales Nondefense Capital Goods Shipments Ex Aircraft ISM ManufacturingISM Non-Manufacturing Building Permits

-150

-100

-50

0

50

100

150

200

250

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Citi U.S. Economic Surprise Index(end of month observations)

2

FHLBNY

FHLBNY

Consensus Projections Imply That Output Lost to the

Pandemic Will Be Recovered By Mid Year

Source: Bureau of Economic Analysis

3

2.3

1.3 2.2 2.5 2.3 1.7

2.9 3.93.8 2.7 2.1 1.3

2.9 1.5

2.6 2.4

-5.0

-31.4

33.4

4.0

2.3

4.1 4.9 3.8

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

35

2016 2017 2018 2019 2020 2021

Net Contributions to Real GDP Growth(quarterly percentage change at seasonally adjusted annual rate)

Consumer Spending Business Fixed Investment Residential Investment Inventories

Net Exports Government Outlays Real GDP

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Real Gross Domestic Product, Billions of Chained 2012 Dollars, Quarterly, Seasonally Adjusted Annual Rate

FHLBNY

FHLBNY

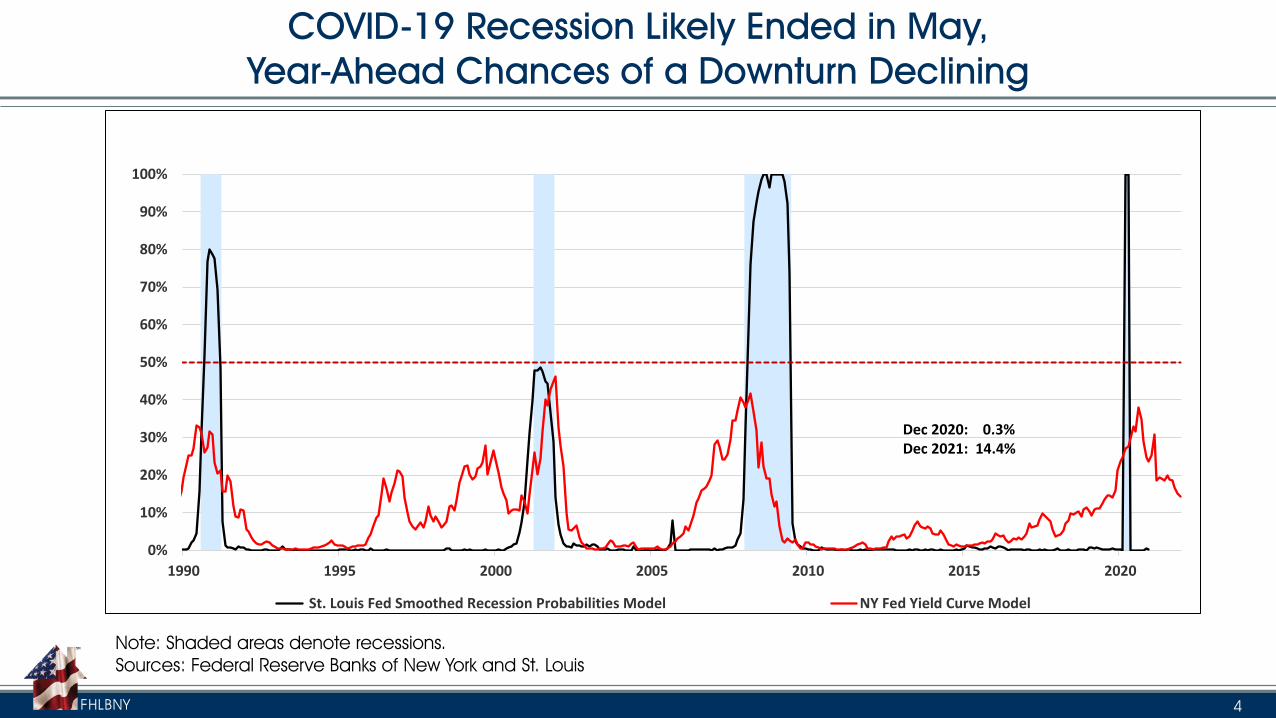

COVID-19 Recession Likely Ended in May,

Year-Ahead Chances of a Downturn Declining

Note: Shaded areas denote recessions.

Sources: Federal Reserve Banks of New York and St. Louis

4

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1990 1995 2000 2005 2010 2015 2020

St. Louis Fed Smoothed Recession Probabilities Model NY Fed Yield Curve Model

Dec 2020: 0.3%Dec 2021: 14.4%

FHLBNY

FHLBNY

Economy’s Near-Term Progress Will Depend on

Stemming Renewed COVID-19 Outbreak

Source: COVID Tracking Project

2%

4%

6%

8%

10%

12%

14%

16%

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2,200,000

2,400,000

U.S. COVID-19 Tests Results Per Day

Tests Conducted (scale left) 7-Day Moving Avg (scale left)Percent Positive (scale right) 7-Day Moving Avg (scale right)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21

Positive COVID-19 Test Results(7-Day Moving Averages)

New Jersey New York

5

FHLBNY

FHLBNY

And Progress in Distributing COVID-19 Vaccines

Source: Bloomberg

Doses Administered Daily Rate of Doses Administered % of Supply Used

1+ Dose 2 Doses

United States 44,413,509 10.2 3.1 1,528,618 70.6

FHLBNY District:

New York 2,513,387 9.7 3.2 76,921 73.3

New York City 1,032,158 9.3 3.0 29,784 69.9

New Jersey 1,096,789 9.6 2.7 37,172 74.1

Puerto Rico 321,965 7.4 2.4 21,783 51.0

Virgin Islands 10,064 6.9 2.6 479 46.8

% of Population Given

6

FHLBNY

FHLBNY

U.S. Railroad Traffic Well Off Pandemic Lows

7

Source: Calculated Risk

FHLBNY

FHLBNY

Resurgence in COVID-19 Infections Impacting Service-Sector Activity

Source: Calculated Risk

8

FHLBNY

FHLBNY

Office Occupancy Rising in Major Metro Areas,

But Still Well Below Pre-Pandemic Levels

Source: Kastle Systems

9

FHLBNY

FHLBNY

With Less Than 15% of Workers Back in the Office,

Subway Usage Well Below Normal

10

Source: Calculated Risk

Daily Turnstile Entries

FHLBNY

FHLBNY

Other Service-Producing Segments Continue to Struggle

Source: Calculated Risk

11

FHLBNY

FHLBNY

Labor Market Conditions Will Remain Challenging

for the Foreseeable Future

Note: Shaded areas denote recessions. Source: U.S. Department of Labor

12

1,000,000

4,000,000

7,000,000

10,000,000

13,000,000

16,000,000

19,000,000

22,000,000

25,000,000

28,000,000

100,000

1,100,000

2,100,000

3,100,000

4,100,000

5,100,000

6,100,000

7,100,000

2009 2011 2013 2015 2017 2019 2021

Initial Claims (scale left) Continuing Claims (scale right)

Jobless Claims Remain Well Above Pre-Pandemic Levels

FHLBNY

FHLBNY

Roughly 11% of the Civilian Labor Force Receiving Assistance

13

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21

Unemployment Assistance Recipients Under Various Programs

Total Pandemic Unemployment Assistance Regular State Pandemic Emergency Unemployment Compensation Extended Benefits

Note: Shaded area denote recession. Source: U.S. Department of Labor

FHLBNY

FHLBNY

Nonfarm Payrolls Rose Modestly in January;

59.9% of Private Jobs Lost Have Been Recovered

Source: Bureau of Labor Statistics

49

6

-4 -3-10

9 10 14

-38-28

1

168

97

-7

-61

7

43

-75

-50

-25

0

25

50

75

100

January Changes in Nonfarm Payrolls(thousands, seasonally adjusted)

0

5,000

10,000

15,000

20,000

25,000

Still a Considerable Way to Go to Recover COVID-19 Job Losses(thousands, seasonally adjusted)

Jobs Lost (Mar 20-Apr 20) Jobs Recovered (May 20-Jan 21)

14

FHLBNY

FHLBNY

Hiring Breadth Gauges Retreated Across the Board in January

Note: Shaded areas denote recessions. Source: Bureau of Labor Statistics

0

10

20

30

40

50

60

70

80

90

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

Diffusion Indexes of Nonfarm Payrolls(% increase plus one half those unchanged)

One Month Three Months Six Months

15

FHLBNY

FHLBNY

Unemployment Measures Remained Elevated at Beginning of New Year

Note: Shaded areas denote recessions. Source: Bureau of Labor Statistics

2

4

6

8

10

12

14

16

18

20

22

24

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

Unemployment Rates(percent)

Conventional Unemployment Rate (U-3)

Plus marginally attached workers & those on part time for eco reasons (U-6)

NAIRU (Non-Accelerating Inflation Rate of Unemployment)

16

FHLBNY

FHLBNY

Core Consumer Inflation Gauges Likely Will

Remain Below Fed Target Until the Spring

Notes: Light blue shaded areas denote recessions. Pink shaded area denotes projections. Sources: Bureau of Labor Statistics and FHLBNY

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

Core Consumer Price Index Core PCE Chain Price Index Federal Reserve Target

%

Core Consumer Inflations Measures(percentage change from year ago)

17

FHLBNY

FHLBNY

Financial Conditions Have Returned to Pre-Pandemic Levels

Note: Shaded areas denote recessions. Source: Bloomberg

-10

-8

-6

-4

-2

0

2

Bloomberg U.S. Financial Conditions Index

Std Dev

18

24-Mar-20 10-Feb-21 Change

US Financial Conditions -6.34 0.80 7.13

Money Market Spreads:

TED Spread 127.05 16.98 -110.07

Libor/OIS Spread 112.05 13.11 -98.94

Com Paper/T-Bill Spread 205.64 9.20 -196.44

Bond Market Spreads:

Baa/10-Yr Treasury Spread 456.37 98.71 -357.66

High-Yield/10-Yr Treas Spread 11.00 3.28 -7.72

Muni/10-Yr Spread 235.89 -44.14 -280.03

Swaption Volatility Index 118.27 63.78 -54.49

Equity Market:

S&P 500 2447.33 3903.24 1455.91

VIX S&P Volatility Index 61.67 22.68 -38.99

FHLBNY

FHLBNY

Fed Officials Expect No Change in Fed Funds

Target Range Over Next Three Years

19

Percent Percent

3.375 3.375

3.25 l 3.25

3.125 3.125

3 l ll ll ll 3

2.875 ll 2.875

2.75 ll l l l 2.75

2.625 ll 2.625

2.5 llllllll llllllll llllllll llllllll 2.5

2.375 lll llll l l l l 2.375

2.25 ll lll lll lll 2.25

2.125 lllll lll 2.125

2 l l l l 2

1.875 llll lllll 1.875

1.75 1.75

1.625 lllll l 1.625

1.5 1.5

1.375 l 1.375

1.25 1.25

1.125 l l 1.125

1 1

0.875 0.875

0.75 0.75

0.625 l l l 0.625

0.5 0.5

0.375 l l ll lll 0.375

0.25 0.25

0.125 lllllllllllllllll lllllllllllllllll lllllllllllllllll lllllllllllllll llllllllllllllll llllllllllllllll lllllllllllll llllllllllll 0.1250 0

Dec '19 Jun '20 Sep '20 Dec' 20 Dec '19 Jun '20 Sep '20 Dec' 20 Sep '20 Dec' 20 Dec ' 19 Jun '20 Sep '20 Dec' 20

2021 2022 2023 Longer Run

Source: Federal Reserve Board

FHLBNY

FHLBNY

Policymakers Revised Forecasts at December FOMC Meeting

Source: Federal Reserve Board

2.0 1.9 1.8 1.9

-6.5

5.0

3.5

1.8

-3.7

4.03.0

2.51.9

-2.4

4.23.2

2.41.8

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

2020 2021 2022 2023 Longer Run

Real GDP Growth(percentage change Q4/Q4)

Dec-19 Jun-20 Sep-20 Dec-20

3.5 3.6 3.7

9.3

6.5

5.5

4.1

7.6

5.5

4.64.0

6.7

5.0

4.23.7

2.0

4.0

6.0

8.0

10.0

2020 2021 2022 2023 Longer Run

Unemployment Rate(average level in Q4 of inciated year)

Dec-19 Jun-20 Sep-20 Dec-20

1.92.0 2.0

0.8

1.61.7

1.2

1.71.8

2.0

1.81.9

2.0

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2020 2021 2022 2023 Longer Run

PCE Inflation(percentage change Q4/Q4)

Dec-19 Jun-20 Sep-20 Dec-20

1.92.0 2.0

1.0

1.5

1.7

1.5

1.71.8

2.0

1.4

1.81.9

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2020 2021 2022 2023

Core PCE Inflation(percentage change Q4/Q4)

Dec-19 Jun-20 Sep-20 Dec-20

20

FHLBNY

FHLBNY

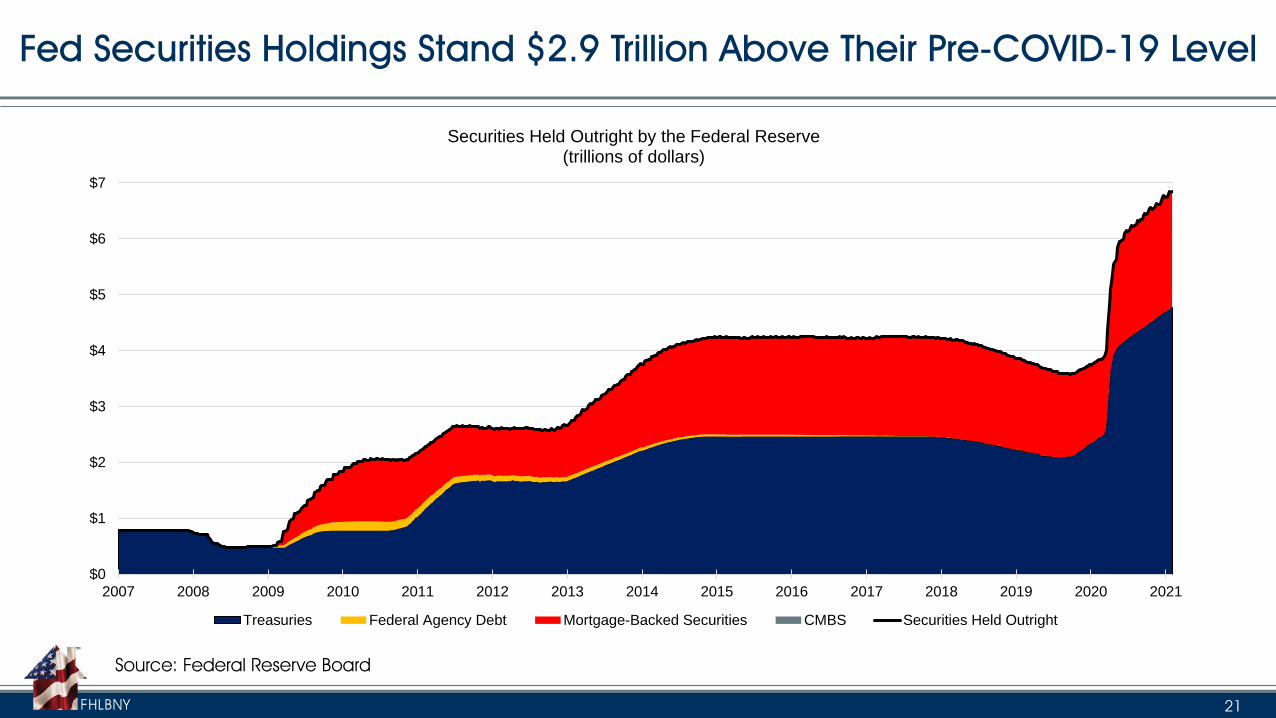

Fed Securities Holdings Stand $2.9 Trillion Above Their Pre-COVID-19 Level

Source: Federal Reserve Board

21

$0

$1

$2

$3

$4

$5

$6

$7

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Securities Held Outright by the Federal Reserve(trillions of dollars)

Treasuries Federal Agency Debt Mortgage-Backed Securities CMBS Securities Held Outright

FHLBNY

FHLBNY

Massive Federal Deficits in the Wake of the COVID-19 Outbreak

Will Require Record Treasury Debt Issuance

22

FHLBNY

FHLBNY

Consensus Projections Call for Steady Rise in

Treasury Rates Through Spring of 2022

Sources: Bloomberg, Blue Chip Consensus

0.13

0.04 0.05 0.07 0.11

0.46

1.13

1.93

0.10.2 0.2

0.3

0.4

0.8

1.5

2.2

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

Fed Funds 3-Month 6-Month 1-Year 2-Year 5-Year 10-Year 30-Year

2/10/2021 2Q21 3Q21 4Q21 1Q22 2Q22

23

FHLBNY

FHLBNY

NY Factory Activity Rose Modestly in January;

Firms More Hopeful About the Future

Note: Shaded areas denote recessions. Sources: Federal Reserve Bank of New York, FHLBNY estimates

10

20

30

40

50

60

70

80

Empire State Manufacturing Survey(diffusion indexes, 50 = no change from prior month)

Composite New Orders Employment

25

30

35

40

45

50

55

60

65

70

Empire State Manufacturing Composite Indexes(diffusion indexes, 50 = no change from prior month)

Present Future

24

FHLBNY

FHLBNY

Local Service-Producing Activity Weakened,

Yet Firms More Optimistic About the Future

Note: Shaded areas denote recession. Sources: Federal Reserve Bank of New York, FHLBNY estimates

0

10

20

30

40

50

60

70

80

90

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

New York Fed Business Leaders Survey(diffusion indexes, 50 = no change from prior month)

Business Activity Business Climate Employment Wages

0

10

20

30

40

50

60

70

80

New York Fed Business Leaders Survey(diffusion indexes, 50 = no change from prior month)

Future Business Activity Future Business Climate

25

FHLBNY

FHLBNY

Small Business in the FHLBNY District Have

Suffered More Than Others Amidst Healthcare Crisis

Source: U.S. Census Bureau

26

43.9%

17.8%

29.0% 30.1%

24.1%

32.8%

5.2%

29.9%

13.7%

20.7% 22.2%

14.0%

26.5%

52.5%

30.1%

60.7%64.9%

44.0%

0%

10%

20%

30%

40%

50%

60%

70%

Firms Experiencing a Large Negative Impact From COVID-19 By Industry

Average 30.7%

30.7%

44.3%

18.7%

5.0%

1.4%

35.9%

42.6%

12.2%

7.0%

2.4%

40.3% 40.8%

12.8%

4.5%1.7%

28.6%

51.4%

16.7%

0.0% 0.0%0%

10%

20%

30%

40%

50%

60%

Large Negative Impact Moderate Negative Impact Little or No Effect Moderate Positive Impact Large Positive Impact

Overall, how has business been effected by the COVID-19 pandemic?

National New Jersey New York Puerto Rico

FHLBNY

FHLBNY

FHLBNY District Added Jobs Over May-December Span,

But Payrolls Remain Well Below Pre-Pandemic Levels

Note: Shaded areas denote recessions. Source: Bureau of Labor Statistics

12,000

12,500

13,000

13,500

14,000

14,500

15,000

15,500

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

FHLBNY Nonfarm Payrolls(thousands, seasonally adjusted)

New York New Jersey Puerto Rico Virgin Islands FHLB-NY DistrictJobs Lost (March-April), thous -1,944.9 -831.3 -119.6 -2.7 -2,898.5Jobs Recovered (May-December) 886.6 479.4 46.4 0.2 1,412.6

% Recovered 45.6% 57.7% 38.8% 7.4% 48.7%

-1000

-800

-600

-400

-200

0

200

400

600

Private Payroll Changes By Industry in the FHLBNY District

March-April May-December

Thous

43.8%

76.1%

61.0% 54.0%

71.1%

57.6%12.1%

33.9%40.4%

38.2%

44.4%

27

FHLBNY

FHLBNY

FHLBNY District Has a Considerable Way to Go to

Recoup COVID-19 Job Losses

Source: Bureau of Labor Statistics

Jobs Lost (thous) Jobs Recovered (thous) Percent

United States -22,160 12,321 55.6%

FHLBNY District -2,899 1,413 48.7%

New York State -1,944.9 886.6 45.6%

Albany-Schenectady-Troy, NY -74.9 29.3 39.1%

Binghamton, NY -14.2 7.6 53.5%

Buffalo-Cheektowaga-Niagara Falls, NY -111.7 66.3 59.4%

Dutchess County-Putnam County, NY Metropolitan Division -26.0 11.2 43.1%

Elmira, NY -4.6 2.2 47.8%

Glens Falls, NY -10.5 5.8 55.2%

I thaca, NY -9.7 7.3 75.3%

Kingston, NY -9.6 6.4 66.7%

Nassau County-Suffolk County, NY Metropolitan Division -296.4 187.5 63.3%

New York-Jersey City-White Plains, NY-NJ Metropolitan Division -1,478.2 683.0 46.2%

New York-Newark-Jersey City, NY-NJ-PA -2,036.2 986.7 48.5%

Rochester, NY -100.0 43.1 43.1%

Syracuse, NY -59.9 25.4 42.4%

Utica-Rome, NY -19.6 9.3 47.4%

Watertown-Fort Drum, NY -7.3 3.3 45.2%

New York City, NY -944.1 360.9 38.2%

Orange-Rockland-Westchester, NY -149.7 85.3 57.0%

Jobs Lost (thous) Jobs Recovered (thous) Percent

New Jersey -831.3 479.4 57.7%

Atlantic City-Hammonton, NJ -44.5 25.3 56.9%

Camden, NJ Metropolitan Division -89.7 54.4 60.6%

Newark, NJ-PA Metropolitan Division -225.8 105.4 46.7%

Ocean City, NJ -11.1 9.1 82.0%

Trenton, NJ -38.1 22.5 59.1%

Vineland-Bridgeton, NJ -8.3 4.2 50.6%

Bergen-Hudson-Passaic, NJ -185.5 108.8 58.7%

Middlesex-Monmouth-Ocean, NJ -195.1 128.0 65.6%

Puerto Rico -119.6 46.4 38.8%

Aguadilla-Isabela -7.9 4.0 50.6%

Arecibo -4.9 3.7 75.5%

Guayama -1.6 0.9 56.3%

Mayaguez -3.9 0.6 15.4%

Ponce -10.2 5.3 52.0%

San German -2.7 1.7 63.0%

San Juan-Carolina-Caguas -91.8 24.5 26.7%

Virgin Islands -2.7 0.2 7.4%

28

FHLBNY

FHLBNY

District Jobless Rates Have Generally Moved Lower,

But Remain Well Above National Average

Note: Shaded areas denote recessions. Source: Bureau of Labor Statistics

2

4

6

8

10

12

14

16

18

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Unemployment Rates(percent)

United States FHLBNY District NAIRU New Jersey New York Puerto Rico

Pandemic Peak Dec ChangeUnited States: 14.7% 6.7% -8.0%

FHLBNY: 15.2% 8.1% -7.1%New York: 15.9% 8.2% -7.7%New Jersey: 16.8% 7.6% -9.2%Puerto Rico: 9.0% 9.1% 0.1%

29

FHLBNY

FHLBNY

Income Inequality Rising Across U.S. and Majority of FHLBNY District

30

46.7

46.3

49.8

48.2 48.1

51.4

43

44

45

46

47

48

49

50

51

52

United States New Jersey New York

2006-2010 2014-2018

Note: The Gini Index is a summary measure of income inequality. A value of 0 indicates perfect equality while a value of 1 (or 100)

indicates perfect inequality. Source: Population Research Bureau

FHLBNY

FHLBNY

Record Low Mortgage Rates Are Boosting

Home-Purchase Mortgage Applications

Note: Shaded areas denote recessions. Sources: Mortgage Bankers Association

100

150

200

250

300

350

400

450

500

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

Home-Purchase Mortgage Applications

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

2014 2015 2016 2017 2018 2019 2020 2021

Mortgage Interest Rates

5-Yr ARM 15-Yr Fixed 30-Yr Fixed

31

FHLBNY

FHLBNY

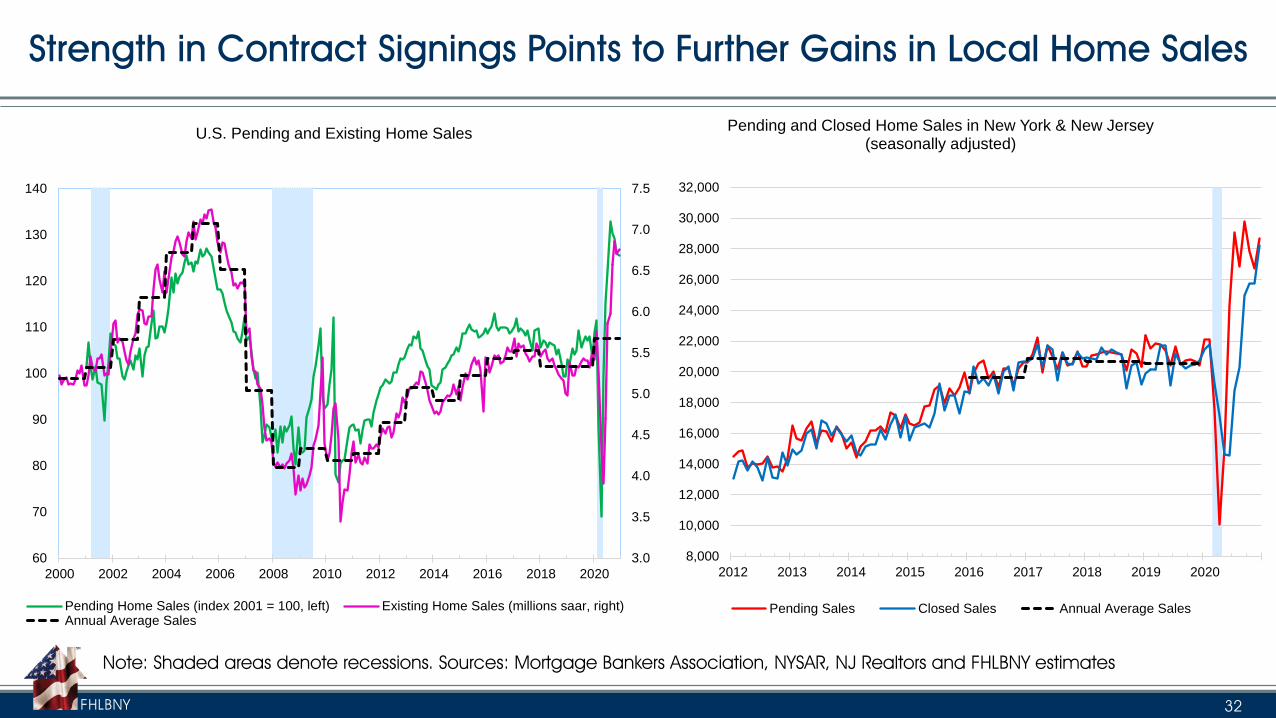

Strength in Contract Signings Points to Further Gains in Local Home Sales

Note: Shaded areas denote recessions. Sources: Mortgage Bankers Association, NYSAR, NJ Realtors and FHLBNY estimates

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

60

70

80

90

100

110

120

130

140

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

U.S. Pending and Existing Home Sales

Pending Home Sales (index 2001 = 100, left) Existing Home Sales (millions saar, right)Annual Average Sales

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

32,000

2012 2013 2014 2015 2016 2017 2018 2019 2020

Pending and Closed Home Sales in New York & New Jersey(seasonally adjusted)

Pending Sales Closed Sales Annual Average Sales

32

FHLBNY

FHLBNY

Historically Low Homes on the Market Will

Continue to Support Local Median Prices

Note: Shaded areas denote recession. Sources: NYSAR, NJ Realtors and FHLBNY estimates

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2012 2013 2014 2015 2016 2017 2018 2019 2020

Homes Available for Sale(seasonally adjusted)

NY & NJ New York New Jersey

$200,000

$225,000

$250,000

$275,000

$300,000

$325,000

$350,000

$375,000

$400,000

2012 2013 2014 2015 2016 2017 2018 2019 2020

Median Selling Prices (seasonally adjusted)

NY & NJ New York New Jersey

33

FHLBNY

FHLBNY

Mortgage Delinquencies Dipped in November;

Forbearances Edging Lower

34

Note: Shaded areas denote recessions Source: Mortgage Bankers Association

3.9%

2.0%

0.3%

1.0%

0.4%

6.1%

1.4%

0.6%0.8%

3.3%

0.3%

5.9%

3.1%

0%

1%

2%

3%

4%

5%

6%

7%

30+ Days PastDue

30-59 Days PastDue

60-89 Days PastDue

90-119 DaysPast Due

120+ Days PastDue

In Foreclosure

Mortgage Delinquency Rates

Nov-19 Oct-20 Nov-20

FHLBNY

FHLBNY

Commercial Segment Drove Nonresidential

Building Projects Higher at Beginning of 2021

35

Note: Shaded areas denote recessions. Source: Dodge Data & Analytics

40

60

80

100

120

140

160

180

200

220

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Dodge Momentum Index(2000 = 100, seasonally adjusted)

Dodge Momentum Index Commercial Building Planning Index Institutional Building Planning Index

FHLBNY

FHLBNY

Risks to Commercial Real Estate Will Remain High

In contrast to the residential sector, commercial real estate likely will face significant headwinds in the future:

▪ $10,000 cap on state and local tax deductions in the Tax Cuts and Jobs Act of 2018 put the New York City

metropolitan area at a competitive disadvantage as people and then businesses moved to lower tax

states.

▪ The City’s population growth, which turned negative for the first time in 2017, suffered accelerated declines

over the past two years, falling from a peak of 8.47 million in 2016 to 8.34 million in 2019.

▪ Financial problems at co-working firms – the largest consumers of office space during the past several years

– have further reduced demand.

▪ In addition, the ability to operate successfully from a remote posture in the wake of the COVID-19

pandemic has prompted many companies to question the need for physical office space.

▪ Finally, new competitive construction will weigh on existing properties, resulting in a rise in vacancy rates.

36

FHLBNY

FHLBNY

101 PARK AVENUE • NEW YORK, NY 10178 • WWW.FHLBNY.COM

Advancing Housing and Community Growth

The information provided by the Federal Home Loan Bank of New York (FHLBNY) in this communication is set forth for informational purposes only. The information should not be construed as an opinion,

recommendation or solicitation regarding the use of any financial strategy and/or the purchase or sale of any financial instrument. All customers are advised to conduct their own independent due diligence

before making any financial decisions. Please note that the past performance of any FHLBNY service or product should not be viewed as a guarantee of future results. Also, the information presented here and/or

the services or products provided by the FHLBNY may change at any time without notice.

Brian M. Jones

FHLBNY, Financial Economist

Office: (212) 441- 6802; Mobile (914) 351-8994