turkey’s pharmaceutical sector vision report 2023 vision. making turkey a global center for...

TRANSCRIPT

TURKEY’S PHARMACEUTICAL SECTOR

Vision

ReportStrategy Document

Turkey, a rising star in the region and the world, has ambitious socialand economic goals for 2023 - the 100th anniversary of the Republic.�

The pharmaceutical industry creates value through innovation.�By tappingits potential, the innovative pharmaceutical industry can lead the wayin helping Turkey achieve its 2023 goals.

AIFD is ready to do its part to help the Turkish population age healthfully,contribute to national economic growth, and strengthen Turkey’s globalcompetitiveness by promoting pharmaceutical innovation, R&D,�andcapital investment.

AIFD’s vision is to help create a pharmaceutical industry in Turkey thatcan manufacture higher value-added products, attract globally significantR&D investment, and use advanced technologies to export products ona exponentially greater scale, which will in turn help tip the foreigntrade balance in Turkey’s favor.

Now is the time that all interested parties - both domestic and internationalmust join together with common aims and commit ourselves to achievethese goals through dialogue and collaboration, so that together weshape an industry that will be “good medicine” in helping Turkey achieveits 2023 vision.

Making Turkey a Global Center forPharmaceutical R&D and Production

* The Pharmaceutical Industry: Good Medicine for Turkey!

‹laç gibigelecek!*

AIFD Members

Stakeholders WhoCommented onVision 2023 Report

4

6212

67

78

84

Table ofContents

Executive Summary

Vision 2023 andAction Plan

Key Success Indicators forVision 2023

2023 Scenarios

Map ofGoal Alignment with

Government Plans

ExecutiveSummary

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T03

C H A P T E R 1 • E X E C U T I V E S U M M A R Y 04

Executive Summary

As a result of aging populations, extended life spans, and socioeconomic changes aroundthe world, health services is one of the most important topics of the 21st century. As the averagelife expectancy increases, the risk of falling ill to chronic diseases and experiencing healthconcerns in the later stages of life also increases. When we consider these factors, innovativedrugs and new treatments, which can help prevent diseases and reduce treatment costs,become increasing important over time. Thus both developed and developing countries considerpharmaceutical research and development (R&D) aimed at the discovery of new treatmentsand the production of new drugs a priority area for investment and a strategic growth sector.

The Turkish Government aims to make Turkey one of the world’s top ten economies in healthservices by 2023 by increasing R&D expenditures to 3% of GDP and by increasing exportsto USD 500 billion. Moreover, according to the Turkish Ministry of Science, Industry, andTechnology (AIFD)’s Strategy Report, Turkey should become the Eurasian production basefor medium- and high-level technology products. Taking into account Turkey’s currentmacroeconomic conditions, political stability and increasing economic efficiency, AIFD considersthese R&D targets to be realistic.

Turkey’s “Health Care Transformation Program” that was implemented in 2004 marked amajor development in public access to health services and treatments. Physician consultationper capita increased five times from 1.7% in 1994 to 7.7% in 2011. The average life spanin Turkey also increased 24% in the last 30 years and has now reached 74 years. Innovativedrugs play an important role in increasing in life expectancy. Based on a study of conductedby Professor Lichtenberg of Columbia University and the National Bureau of Economic Research,innovative drugs accounted for 75% of the increase in life expectancy in the 30 countriessurveyed, including Turkey.

Thus if the Turkish government can implement the necessary structural changes and effectivelypromote innovation in the health care system, the pharmaceutical industry can be the drivingforce in helping to achieve the Turkish Government’s public health and economic targets.

However in order to achieve sustainable progress in health services, Turkey must also focuson improving its competitive position. Currently, Turkey lags behind other emerging pharmaceuticalcompanies, now referred to as “pharmerging” countries such as Brazil, Russia, India andChina, in global pharmaceutical investment.

According to the World Economic Forum’s Global Competition Index (2011-2012), Turkeyis ranked 59 out of 142 countries, and ranked 71 in the Innovation Capacity Index.

In the Global Competition Index, Brazil is ranked 31, Russia 38, India 35 and China 47.

While the Turkish pharmaceutical sector is ranked 16th in terms of market value, it is 36thin terms of the clinical research conducted and the volume of pharmaceutical exports.

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T05

Countries that invest in R&D, develop technology, and effectively convert this technologyinto products become more competitive. Innovative drugs create added value in thepharmaceutical industry and are key to a country’s economic advancement. While globalinvestment in innovative drug R&D is USD 120 billion each year, Turkey’s share is only USD60 million, representing only a 0.039% of global R&D. Currently, drug production is Turkeyis focused around low value-added products, with high value-added products being imported.Moreover, R&D aimed at developing new molecules (core research) has never been donein Turkey. As production of innovative drugs increases, the added value of the drugs producedwill also increase accordingly.

Turkey’s competitors in the health services sector made global pharmaceutical investmenta priority in the 1990s and were able to became net pharmaceutical exporters throughstrategic governmental planning. Turkey, which now boasts the strongest and most dynamiceconomy in the region, can become a formidable player in the pharmaceutical sector. Turkeyhas the necessary knowledge base, infrastructure, and geostrategic location to attract globalpharmaceutical R&D and could become a global player in the pharmaceutical industry. Thisreport suggests an exports-focused plan of action to develop Turkey’s pharmaceutical industryinto a global R&D and production center and regional shared service center location.

The main targets of this plan are:

Developing Basic and Clinical Research Competency and Services Exports: ImprovingTurkey’s R&D competency and increasing national and foreign direct investment; therebymaking Turkey’s pharmaceutical sector a leader in R&D

Developing Production Competency and Product Exports: Increasing the production capacityof specific high value-added product groups; thereby allowing Turkey to become aregional/global pharmaceutical powerhouse and net exporter

Making Turkey a Regional Management and Service Center location for the pharmaceuticalindustry

Prerequisites for this action plan are:

The formulation and implementation of a long-term policy to support innovation in the fieldof health sciences that makes R&D and value- added drug production the highest priority.Additionally, the government will provide grants that support innovation and implementregulations that protect international property rights (IPR).

ilaç gibigelecek!

C H A P T E R 1 • E X E C U T I V E S U M M A R Y 06

The implementation of a legal and administrative framework that counterbalances theconcerns of public health and the pharmaceutical sector, which should entail:

A current and realistic budget that can sustain pharmaceutical sector growth. Whilepatient access to health care and pharmaceutical drugs has increased significantlyin Turkey, the percentage of Turkey’s population with health insurance has alsoincreased rapidly. However, the budget allocation for public pharmaceuticalexpenditures has decreased since 2009, and pharmaceutical expenditures as apercentage of GDP has dropped to 1.11%. This number is considerably below theOECD average of 1.50%. These factors should be considered when determining thepharmaceutical budget for 2013 and beyond, as budget expenditures should matchthe growing healthcare needs of the country. The recommendation is to increasepharmaceutical expenditures as a percentage of GDP to 1.35%.

An improvement in patient access to pharmaceutical drugs to ensure that Turkishpatients can immediately benefit from innovative drugs once on the market. It isimperative that the government streamline the processes and procedures forpharmaceutical drugs entering the marketplace (via good manufacturing practices(GMP), timely registration, effective pricing, and reimbursements) to ensure thatpharmaceutical drugs become available to patients in a time-frame comparable toother developed countries. The increased speed to market will in turn, attract newinvestment in innovative R&D.

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T07

If the above is agreed upon with the cooperation and collaboration of all stakeholders, AIFDbelieves Turkey can achieve the following results by 2023:

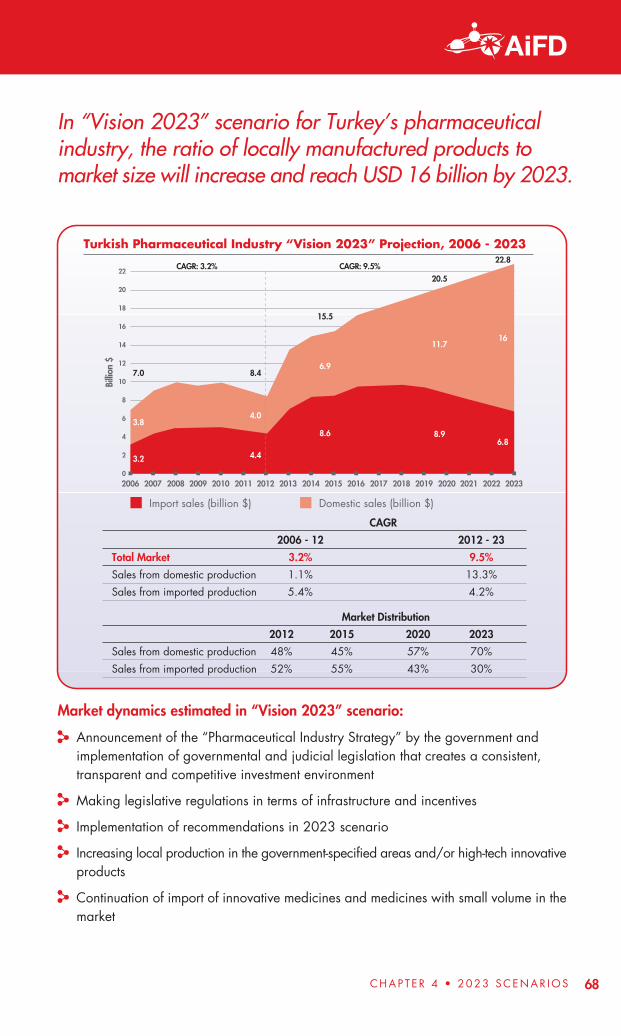

Achieve local pharmaceutical production of USD 23.3 billion through the production ofinnovative and technologically advanced products (as compared to local production ofUSD 5 billion in 2011)

Achieve pharmaceutical exports worth USD 7.3 billion and clinical trial services exportsworth USD 782 million - totaling USD 8.1 billion (as compared to total pharmaceuticalproduct and service exports of USD 587 million in 2011)

Become a net exporter of pharmaceutical drugs with an export surplus of more than USD1 billion (as compared to a 2011 foreign trade deficit of USD 4.1 billion)

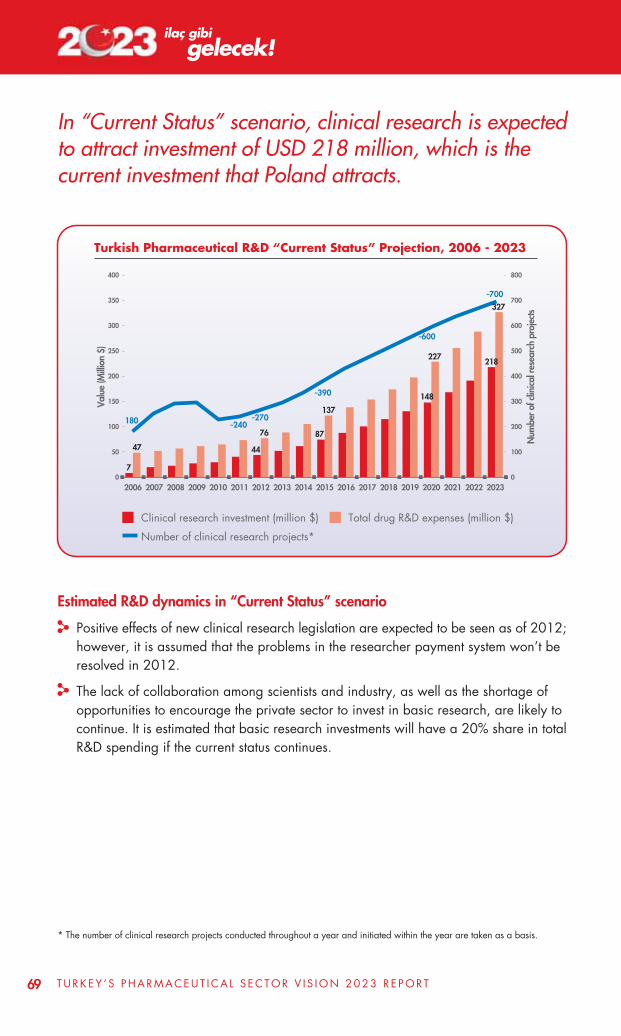

Achieve total R&D investment of USD 1.7 billion (R&D investment was USD 60 millionin 2010 ), with USD 1.1 billion of that investment derived from 3,600 clinical trials (ascompared to 240 clinical trials amounting to USD 40 million in 2011)

Become a regional Shared Service Center location for the pharmaceutical industry thatexports management services

The economic development plan outlined in the following “Turkey’s Pharmaceutical SectorVision 2023 Report”, will enable sustainable expansion and improvement in Turkey’s healthcare system while also achieving governmental targets.

ilaç gibigelecek!

C H A P T E R 1 • E X E C U T I V E S U M M A R Y 08

Vision 2023 andAction Plan

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T11

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 12

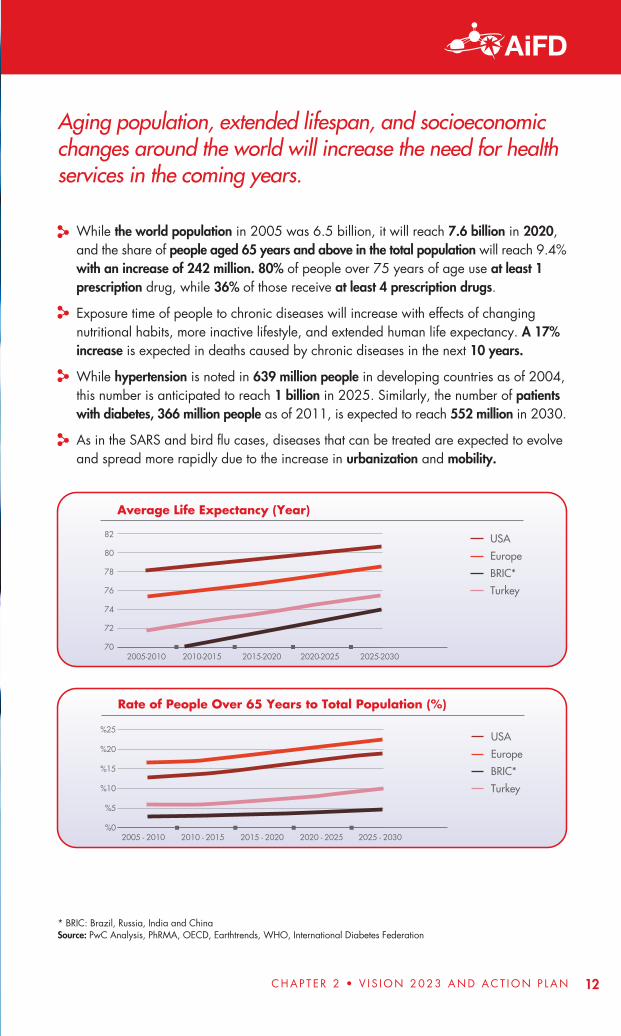

Aging population, extended lifespan, and socioeconomicchanges around the world will increase the need for healthservices in the coming years.

While the world population in 2005 was 6.5 billion, it will reach 7.6 billion in 2020,and the share of people aged 65 years and above in the total population will reach 9.4%with an increase of 242 million. 80% of people over 75 years of age use at least 1prescription drug, while 36% of those receive at least 4 prescription drugs.

Exposure time of people to chronic diseases will increase with effects of changingnutritional habits, more inactive lifestyle, and extended human life expectancy. A 17%increase is expected in deaths caused by chronic diseases in the next 10 years.

While hypertension is noted in 639 million people in developing countries as of 2004,this number is anticipated to reach 1 billion in 2025. Similarly, the number of patientswith diabetes, 366 million people as of 2011, is expected to reach 552 million in 2030.

As in the SARS and bird flu cases, diseases that can be treated are expected to evolveand spread more rapidly due to the increase in urbanization and mobility.

Rate of People Over 65 Years to Total Population (%)

2005 - 2010 2010 - 2015 2015 - 2020 2020 - 2025 2025 - 2030

USA

Europe

BRIC*

Turkey

%25

%20

%15

%10

%5

%0

* BRIC: Brazil, Russia, India and ChinaSource: PwC Analysis, PhRMA, OECD, Earthtrends, WHO, International Diabetes Federation

Average Life Expectancy (Year)

USA

Europe

BRIC*

Turkey

82

80

78

76

74

72

702005-2010 2010-2015 2015-2020 2020-2025 2025-2030

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T13

With the increase of need for health services, innovative drugs& treatments will gain importance in the pharmaceuticalindustry.

Source: PhRMA, PwC analysis

Contribution of new treatment methods and innovative drugs to public health willincrease.

The awareness of patients about the contribution of innovative drugs to public healthis increasing, which increases the demand for new treatment methods.

Effects of many chronic diseases have been brought under control by new drugs andtreatment methods developed so far:

From 1960 to the present, deaths due to heart attacks have decreased by 50% indeveloped countries.

From 1980 to today, life expectancy of cancer patients in USA has extended by83%, or approximately 3 years, with the effect of new drugs and treatments.

From 1995 until today, as the result of retroviral treatment, death rates due toHIV/AIDS have decreased by more than 75% in the USA.

The average life expectancy in the USA between 1900-2000 increased 66% andreached 78 (The contribution of innovative drugs to the improvement in life expectancywas observed to be by 40%).

Between 1982-2005, the frequency of disabilities arising from chronic diseases inthe USA decreased more than 25%.

Studies for developing new drugs and treatment methods will continue in parallel withchanging and increasing health demands:

Pharmaceutical companies will specialize in sophisticated fields such as biotechnology,oncology, etc.

As biotechnology develops, customized drug treatments will increase (Biotechnology-based innovative treatments cured 350 million patients so far).

The importance of preventive and protective treatment will increase. According tostudies by the World Health Organization, 80% of diabetes and heart diseases arepreventable.

ilaç gibigelecek!

Innovative drug investments will increase.

Convergence of medicine and technology will increase: Computer-aided drug design,customized drugs, genome projects and applications, etc.

For R&D studies of pharmaceutical companies, R&D collaborations with universitiesand small-scale R&D companies will increase.

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 14

Total R&D Expense for Global Pharmaceutical Industry

2002 2005 2010 2015

150

100

50

0

69

96127

144

Billio

n $

Innovative drugs support disease prevention, increase lifeexpectancy, reduce treatment expenses and enable patients

to live more productive, active and happier lives.

Source: EP Vantage, PwC analysis

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T15

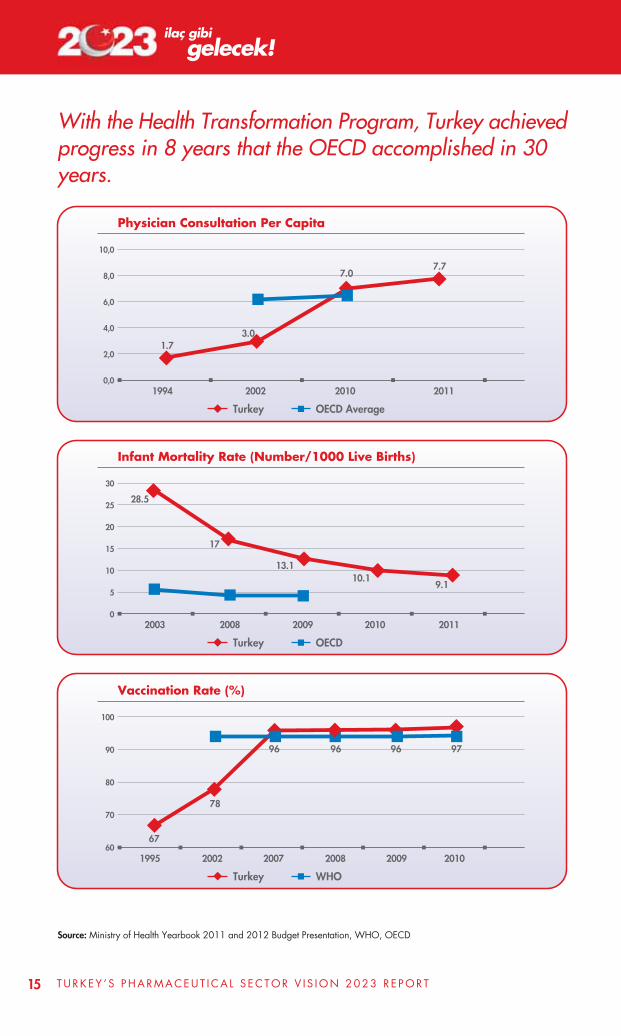

With the Health Transformation Program, Turkey achievedprogress in 8 years that the OECD accomplished in 30years.

Physician Consultation Per Capita

1994 2002 2010 2011

10,0

8,0

6,0

4,0

2,0

0,0

1.73.0

7.07.7

Turkey OECD Average

Source: Ministry of Health Yearbook 2011 and 2012 Budget Presentation, WHO, OECD

Infant Mortality Rate (Number/1000 Live Births)

2003 2008 2009 2011

30

25

20

15

10

5

0

Turkey OECD

2010

28.5

17

13.110.1

9.1

Vaccination Rate (%)

1995 2002 2007 2010

100

90

80

70

60

Turkey WHO

2008 2009

67

78

96 96 96 97

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 16

Among OECD countries, Turkey shows the most rapid increases with regard to averagelife expectancy statistics (according to OECD; 1960: 48.3; 2010: 74.3).

Thanks to the health transformation program, access to many treatment services anddrugs in Turkey has been led to a physician consultation per capita increasing 5 times,to 7.7 in 2011 from 1.7 in 1994.

All kinds of services can be freely offered nationwide through the family health practiceand other primary health institutions without requesting any social security certificates.

A vaccination rate greater than 95%, which is the average rate in high-income countries,was attained.

There was a significant decrease in mortality rates of mothers and children.

Continuation of this success will be possible by followingglobal trends in the healthcare sector and offering the innovative

drugs to patients at the same time they are offered to theworld.

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T17

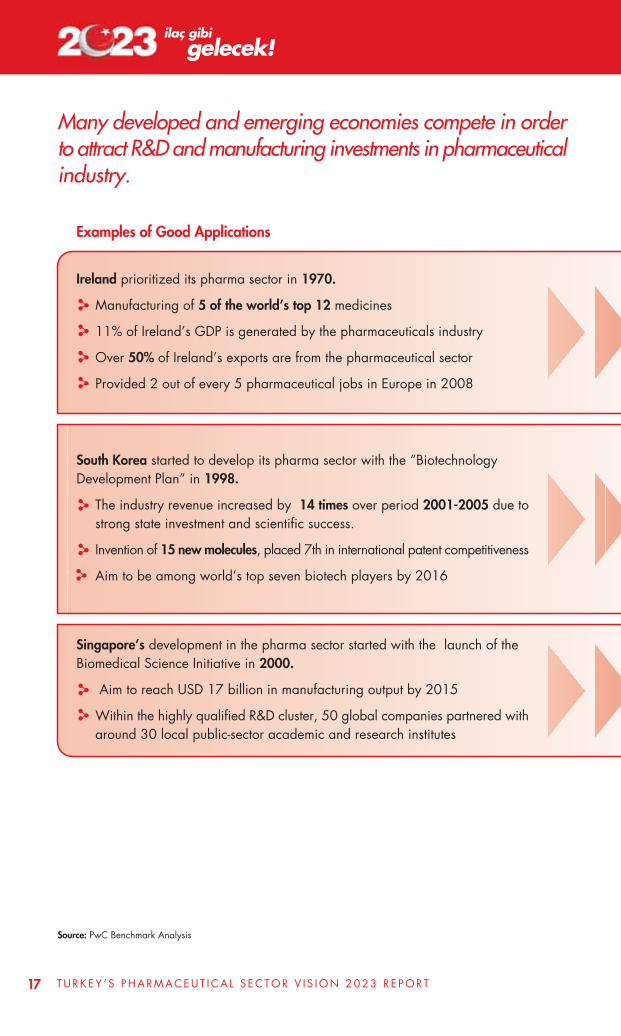

Many developed and emerging economies compete in orderto attract R&D and manufacturing investments in pharmaceuticalindustry.

Examples of Good Applications

Ireland prioritized its pharma sector in 1970.

Manufacturing of 5 of the world’s top 12 medicines

11% of Ireland’s GDP is generated by the pharmaceuticals industry

Over 50% of Ireland’s exports are from the pharmaceutical sector

Provided 2 out of every 5 pharmaceutical jobs in Europe in 2008

South Korea started to develop its pharma sector with the “BiotechnologyDevelopment Plan” in 1998.

The industry revenue increased by 14 times over period 2001-2005 due tostrong state investment and scientific success.

Invention of 15 new molecules, placed 7th in international patent competitiveness

Aim to be among world’s top seven biotech players by 2016

Singapore’s development in the pharma sector started with the launch of theBiomedical Science Initiative in 2000.

Aim to reach USD 17 billion in manufacturing output by 2015

Within the highly qualified R&D cluster, 50 global companies partnered witharound 30 local public-sector academic and research institutes

Source: PwC Benchmark Analysis

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 18

Source: PwC Benchmark Analysis

Many developed and emerging countries focused on the pharmasector over a decade ago and gained substantial investments, in

turn creating a competitive and net exporting industry. Turkey needsto develop and implement a government-initiated industry strategy

to compete with these countries.

Some Recent Investment & Export Facts

EUR 7 billion in investment in last decade

USD 31 billion in pharma export in 2010

Received 1/3 of total US investment in EU’s pharma industry

USD 550 million venture capital fund by Novartis available since 2007

USD 15 billion in FDI in 2010

USD 500 million investment in Biopolis cluster

USD 2 billion in investments in last four years, for 6 new plants

USD 4.4 billion in exports in 2010

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T19

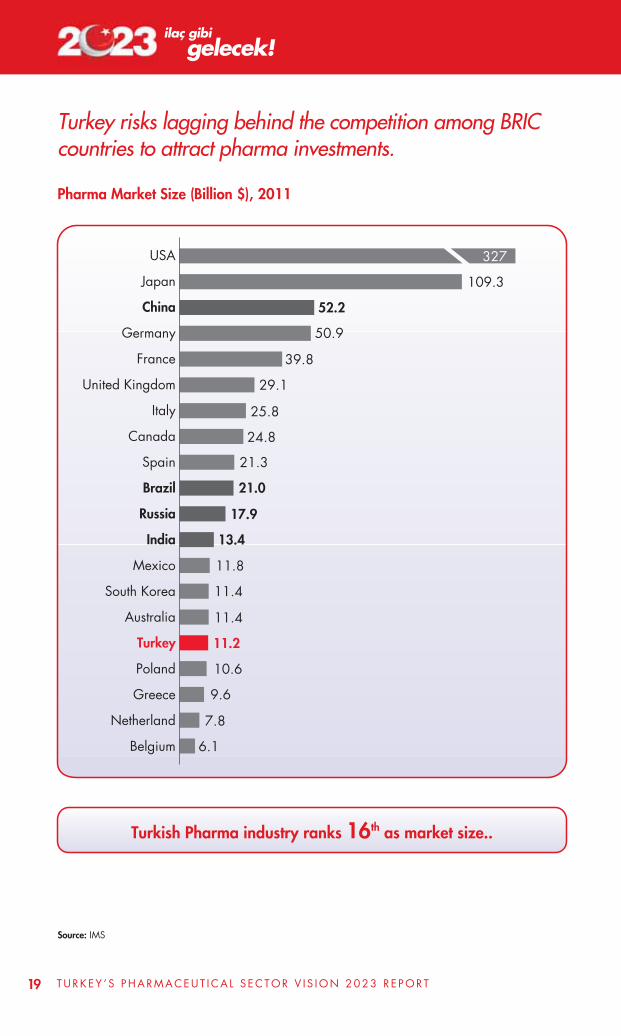

Turkey risks lagging behind the competition among BRICcountries to attract pharma investments.

Pharma Market Size (Billion $), 2011

Turkish Pharma industry ranks 16th as market size..

Source: IMS

USA

Japan

China

Germany

France

United Kingdom

Italy

Canada

Spain

Brazil

Russia

India

Mexico

South Korea

Australia

Turkey

Poland

Greece

Netherland

Belgium

327

109.3

52.2

50.9

39.8

29.1

25.8

24.8

21.3

21.0

17.9

13.4

11.8

11.4

11.4

11.2

10.6

9.6

7.8

6.1

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 20

Number of Clinical Trials (Number)*, 2011

..however ranks 36th in clinical trials..

* Only industry sponsored trials are taken into accountSource: clinicaltrials.gov

3,142

530

505384

341341

310

273

264225

195193

192

179

175

160157

70

USA

Germany

United Kingdom

Frace

Canada

Spain

Japan

Italy

Belgium

South Korea

Netherland

Poland

Australia

China

Russia

Sweden

Czech Rep.

Hungary

Austria

Israil

Denmark

Brazil

---

Turkey

778

514

332

183

148

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T21

Turkey is also behind in export volume and hence in theexport/import coverage rate.

Pharma Export (Billion $), 2011

Turkish pharma industry ranks 36th...

Source: UNCOMTRADE

Germany

Belgium

Switzerlang

USA

France

United Kingdom

Ireland

Netherland

Italy

Spain

---

India

---

China

---

Brazil

---

Turkey

64.7

49.7

45.2

40.8

33.5

32.9

31.2

27.9

16.4

11.2

7.0

4.5

1.3

0.6

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 22

Export / Import Coverage Rate (%), 2010

…and is very behind in terms of its export /import coverage rate.

Source: UNCOMTRADE

830%

457%

262%

144%143%

126%

99%88%

76%66%

62%

26%

21%13%

Ireland

India

Israil

Singapore

Switzerland

---

United Kingdom

Germany

France

Belgium

---

Netherland

Italy

Spain

USA

China

---

South Korea

---

Brazil

Turkey

462%

279%

134%

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T23

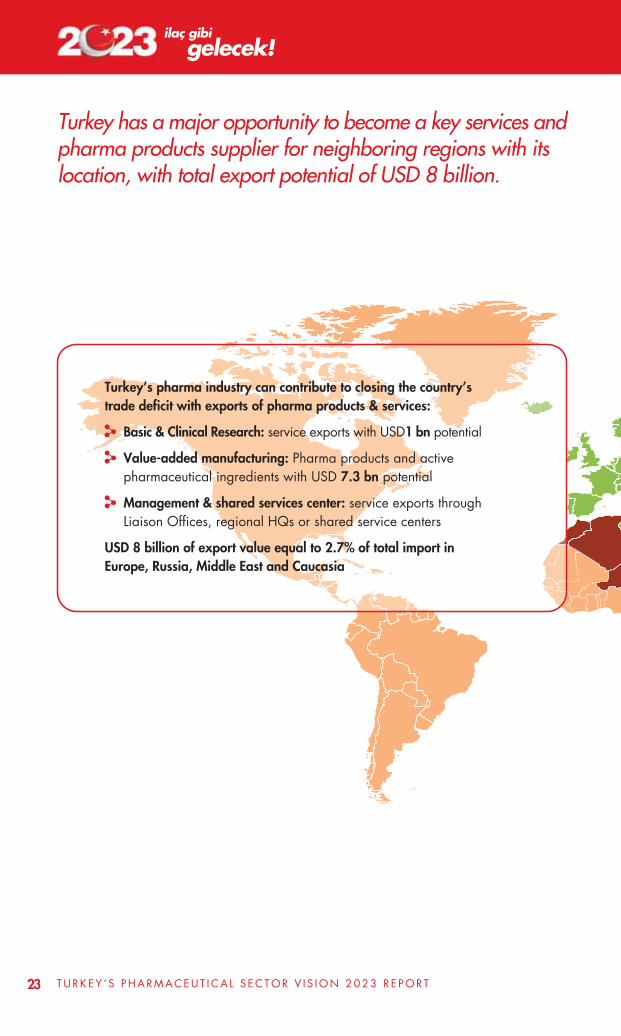

Turkey has a major opportunity to become a key services andpharma products supplier for neighboring regions with itslocation, with total export potential of USD 8 billion.

Turkey’s pharma industry can contribute to closing the country’strade deficit with exports of pharma products & services:

Basic & Clinical Research: service exports with USD1 bn potential

Value-added manufacturing: Pharma products and activepharmaceutical ingredients with USD 7.3 bn potential

Management & shared services center: service exports throughLiaison Offices, regional HQs or shared service centers

USD 8 billion of export value equal to 2.7% of total import inEurope, Russia, Middle East and Caucasia

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 24

EUROPEGDP USD 19.9 trillionPopulation 668 million

Pharma import USD 264 billion

RUSSIAN FEDERATIONGDP USD 1.8 trillion

Population 142 millionPharma import USD 11 billion

CENTRAL ASIA ANDCAUCASUS

GDP USD 0.4 trillionPopulation 82 million

Pharma import USD 2 billion

MIDDLE EAST AND NORTHAFRICA

GDP USD 3.3 trillionPopulation 647 million

Pharma import USD 14 billion

Source: Investment Support and Promotion Agency, UNCOMTRADE

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T25

Turkey’s pharmaceutical industry has enough infrastructureand potential to realize this vision and become a global player.

Strong features of Turkey’s pharmaceutical industrythat will support the targets in the “Vision 2023”.

The scope of social security services increased with successful healthcarereform, as did patient satisfaction, access to services, and industrial indicators.

Steady macroeconomic structureand rapid growth rates

Modern law system supported byeconomic and political stability

Turkish pharmaceutical industryranks 7th in Europe, 16th in the

world

Strong production facilityinfrastructure; 76% of drugsconsumed in Turkey on a box

basis and 49% on a value basisare locally produced

Industrial employment includesapproximately 25.000 people.

Over 300 industrially sponsoredor academic clinical trials are

conducted in 2011

Strong education capacity infundamental sciences, medicineand pharmaceutical departments

Number of specialist physiciansincreased from 18.000 to

31.000 since 2002

Competency in diagnosis andtreatment, and strong

development of healthcaretourism

Being regional center due tostrategic geographical location

and high possibility andadvantage of export to marketssuch as the Middle East, Eastern

Europe

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 26

Investments in health and pharmaceutical industries will improvepublic health and provide an economic benefit by increasingresearch, production, exports and employment.

Public Health Goals:

The main objective of the Ministry of Health in the 2010-2014 Strategy Document wasdefined as “Improving the health care level of our people”.

Supporting R&D studies within the scope of improving health services

Increasing the quality, effectiveness, and productivity of diagnostic and treatmentservices

Improving pharmaceutical and medical device services, and sustaining safe marketaccess

Making regulations that will encourage the development of new drugs to make progressin the field of pharmaceutical technology, and to carry out scientific studies incollaboration with the public, universities and private sector

Economic and Development Goals:

The long-term vision of the Turkish Industrial Strategy was specified as “To be the productionbase in Eurasia by producing medium - and high-level technology products”.

Strategic Targets:

Promote and strengthen the position of companies that can develop their competenciesand skills in a sustainable manner

Promote medium- and high-level technology industries in production and exports.

Switch from low technology industries to high value-added products

Industrial policies include:

Increasing the share of medium- and high-level technology industries in production andexports and developing a policy for industry clusters

The pharmaceutical industry is important for its potential tosupport the government’s public health and economic targets byincreasing R&D, innovation, employment, production and exports.

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T27

“Turkish Pharmaceutical Industry Vision” will provide economicand social benefits for our country and increase competitiveness.

It will ensure DEVELOPMENT

Becoming a global supplier of products by meeting a great portion of the requirementsof the Local Market through local production, and by producing specific products inTurkey

Decreasing the current account deficit by increasing pharmaceutical exports, andbecoming a global supplier for important products

Improving pharmaceutical R&D and production competencies, to enable new localmolecule invention and long-term interest by international pharmaceutical companies

Becoming a regional management center in the pharmaceutical sector, and developingother industries that are associated with pharmaceutical production

Supporting small and medium-sized enterprises and integrating them into thepharmaceutical supply chain through clustering

Expanding Turkey’s financial sector by introducing new venture capital into Turkey

It will provide SOCIAL benefits

Ensure the most effective treatment of diseases with the introduction of more innovativedrugs to the market

Discover new molecules and increase domestic patents with the development of R&D

Increase the number of researchers working in life sciences

Gain scientific knowledge and experience participating in global R&D networks

Increase employment in the pharmaceutical industry (currently 25,000)

Increase indirect employment in the pharmaceutical sector’s supply chain

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 28

It will increase COMPETITIVENESS

Increase the global competitiveness of Turkey by developing and producing advancedtechnology products through the discovery of new molecules and an increase in numberof patents

Shift the competitiveness of Turkey from cost advantage to innovation competency bymerging the knowledge of academia with industry

Increase investment by making Turkey a regional management center and creating aninvestment environment suitable for production and R&D

Ensure that domestic pharmaceutical companies gain the regional and global prominencein R&D and production competency

Increase the global competitiveness of universities with effective industrial collaborationand greater funding

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T29

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 30

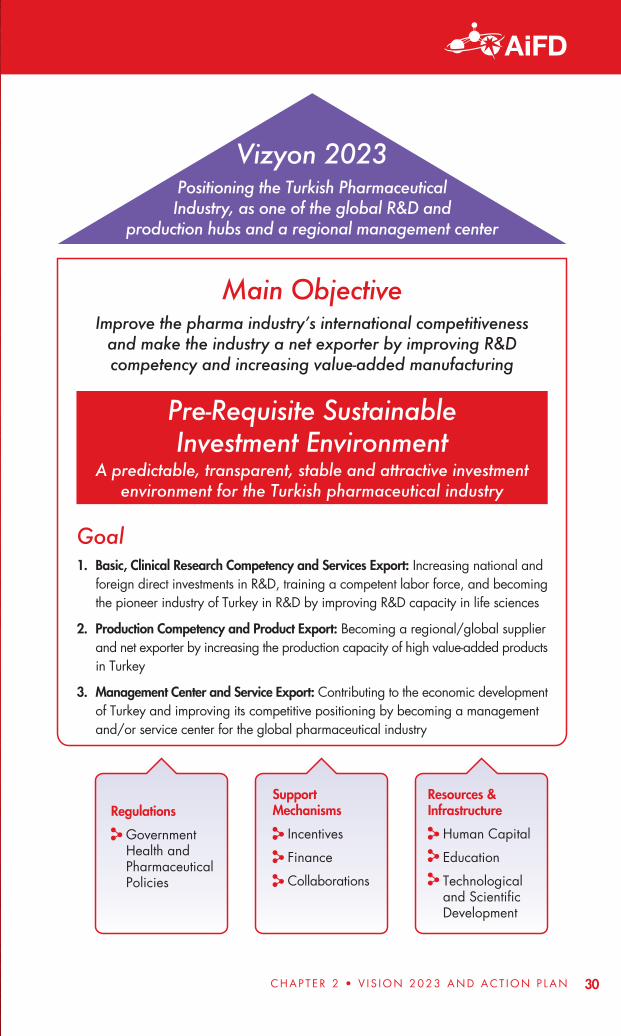

Improve the pharma industry’s international competitivenessand make the industry a net exporter by improving R&Dcompetency and increasing value-added manufacturing

Main Objective

Pre-Requisite SustainableInvestment Environment

Goal1. Basic, Clinical Research Competency and Services Export: Increasing national and

foreign direct investments in R&D, training a competent labor force, and becomingthe pioneer industry of Turkey in R&D by improving R&D capacity in life sciences

2. Production Competency and Product Export: Becoming a regional/global supplierand net exporter by increasing the production capacity of high value-added productsin Turkey

3. Management Center and Service Export: Contributing to the economic developmentof Turkey and improving its competitive positioning by becoming a managementand/or service center for the global pharmaceutical industry

SupportMechanisms

Incentives

Finance

Collaborations

Resources &Infrastructure

Human Capital

Education

Technologicaland ScientificDevelopment

Regulations

GovernmentHealth andPharmaceuticalPolicies

A predictable, transparent, stable and attractive investmentenvironment for the Turkish pharmaceutical industry

Positioning the Turkish PharmaceuticalIndustry, as one of the global R&D and

production hubs and a regional management center

Vizyon 2023

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T31

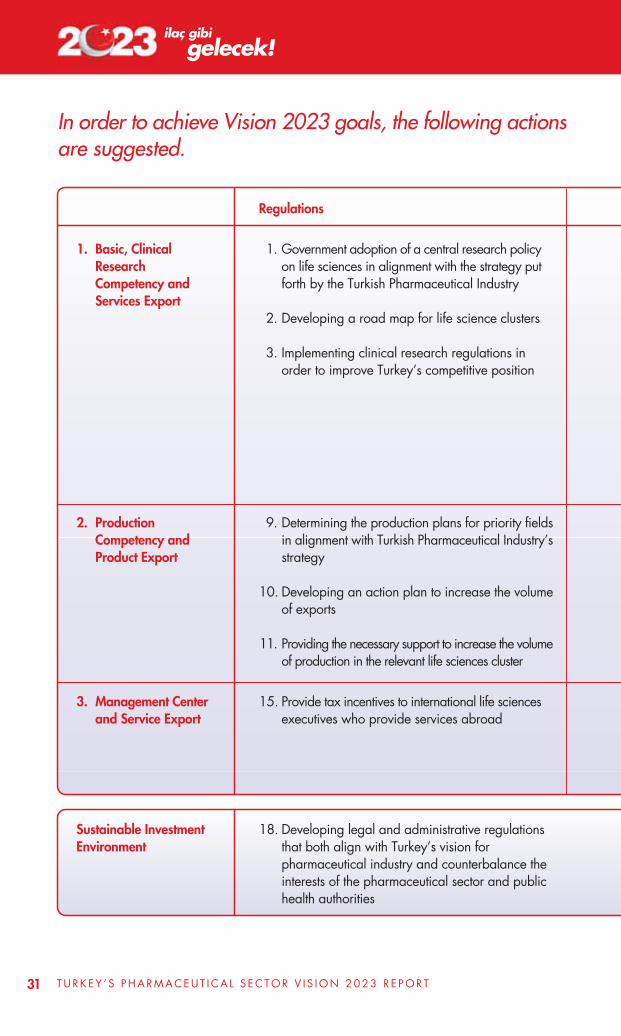

In order to achieve Vision 2023 goals, the following actionsare suggested.

1. Basic, ClinicalResearchCompetency andServices Export

2. ProductionCompetency andProduct Export

3. Management Centerand Service Export

Sustainable InvestmentEnvironment

Regulations

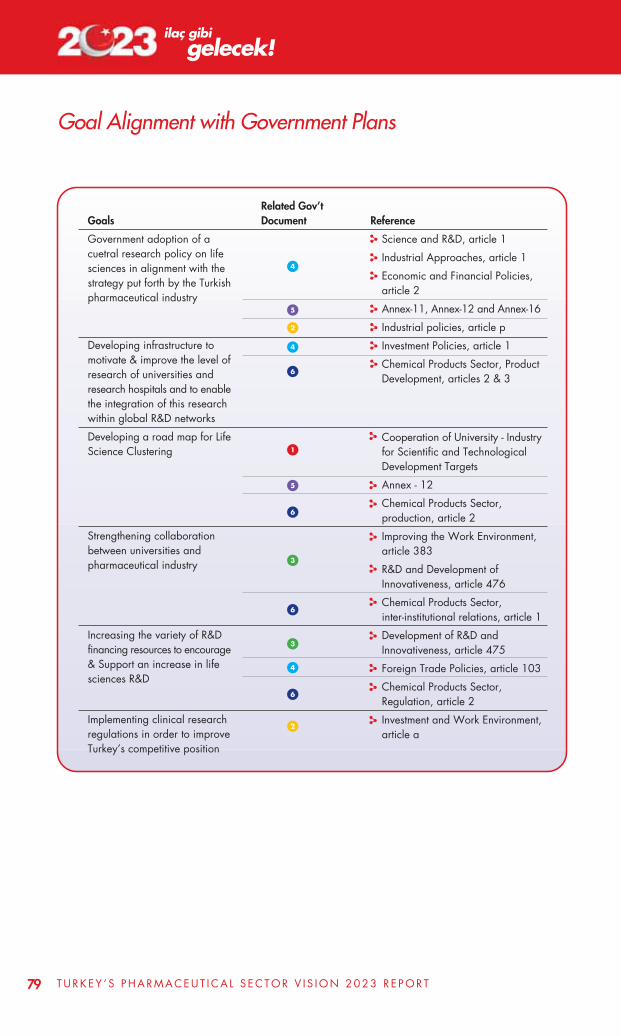

1. Government adoption of a central research policyon life sciences in alignment with the strategy putforth by the Turkish Pharmaceutical Industry

2. Developing a road map for life science clusters

3. Implementing clinical research regulations inorder to improve Turkey’s competitive position

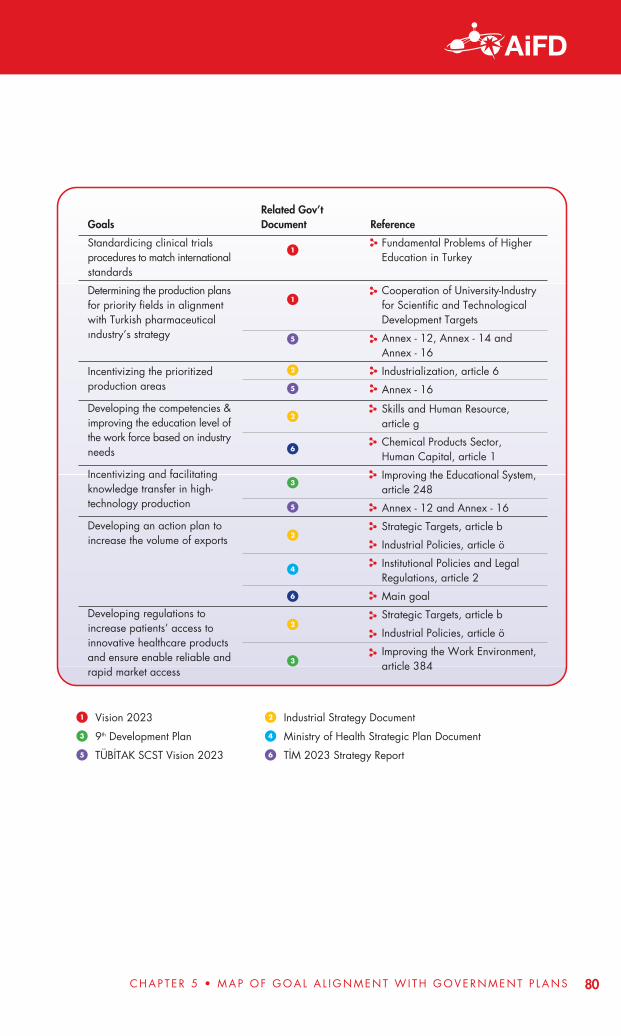

9. Determining the production plans for priority fieldsin alignment with Turkish Pharmaceutical Industry’sstrategy

10. Developing an action plan to increase the volumeof exports

11. Providing the necessary support to increase the volumeof production in the relevant life sciences cluster

15. Provide tax incentives to international life sciencesexecutives who provide services abroad

18. Developing legal and administrative regulationsthat both align with Turkey’s vision forpharmaceutical industry and counterbalance theinterests of the pharmaceutical sector and publichealth authorities

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 32

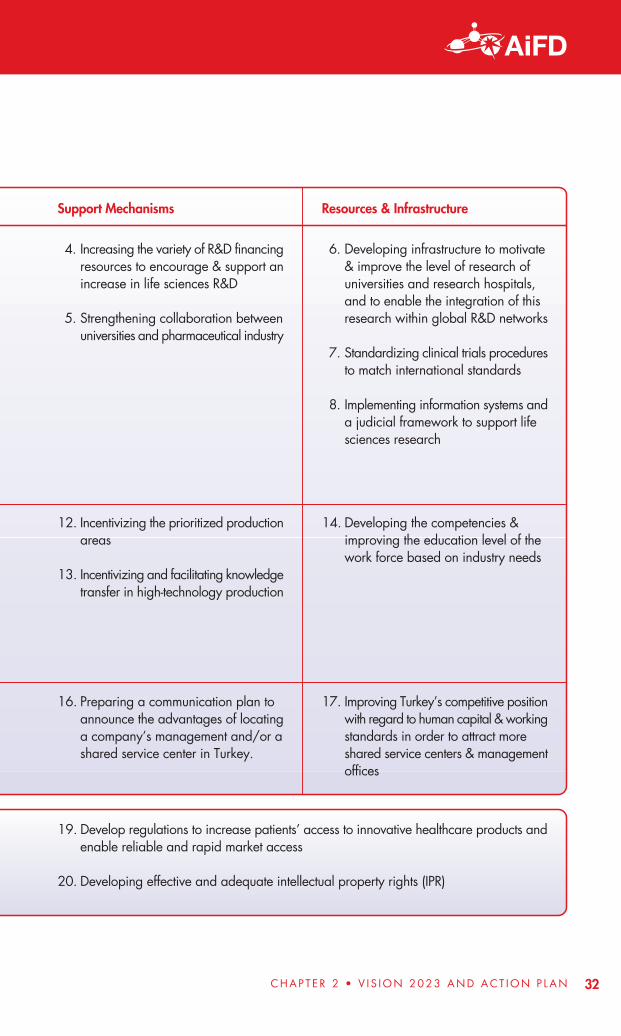

Support Mechanisms Resources & Infrastructure

4. Increasing the variety of R&D financingresources to encourage & support anincrease in life sciences R&D

5. Strengthening collaboration betweenuniversities and pharmaceutical industry

6. Developing infrastructure to motivate& improve the level of research ofuniversities and research hospitals,and to enable the integration of thisresearch within global R&D networks

7. Standardizing clinical trials proceduresto match international standards

8. Implementing information systems anda judicial framework to support lifesciences research

12. Incentivizing the prioritized productionareas

13. Incentivizing and facilitating knowledgetransfer in high-technology production

14. Developing the competencies &improving the education level of thework force based on industry needs

16. Preparing a communication plan toannounce the advantages of locatinga company’s management and/or ashared service center in Turkey.

17. Improving Turkey’s competitive positionwith regard to human capital & workingstandards in order to attract moreshared service centers & managementoffices

19. Develop regulations to increase patients’ access to innovative healthcare products andenable reliable and rapid market access

20. Developing effective and adequate intellectual property rights (IPR)

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T33

Action PlanBasic and Clinical Research

Regulations

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

1.1. Including life sciences in “Prioritized Areas”by the decision of the Supreme Council forScience and Technology (SCST)(TÜB‹TAK has identified energy, food,automotive, information and communicationtechnology and machinery manufacturingtechnologies as prioritized areas for R&Dsupport in accordance with National Science,Technology and Innovation Strategy (NSTIS)2011-2016 Document.)

SCST, MoH,MoSIT, MoD,STRCoT, CoHE,

NGO, SI

Implementationof the regulation

Actions Rel. Stakeholder Follow-up Ind. Duration

1. Government adoption of a central research policy on life sciences in alignment with thestrategy put forth by the Turkish Pharmaceutical Industry

A Strategic Plan for Life Sciences that focuses on R&D has been recently launched in the UK.

The government in China has developed a strategic plan for science and technology with theaim of becoming an “R&D hub” in 2006 and defined specific goals for life sciences.

2012

- 20

13

1.2. Determining essential life science researchfields for Turkey based on consideration oftrends related to pharmeceutical researchglobally and synchronizing with government’shealthcare policies

MoH, MoSIT,MoD, Univ, PS,

SI

Prioritization ofR&D goalsdedicated to atleast 3 fieldsrelated with tothe pharmasector

2012

1.3. Updating of education, financing andincentive mechanisms to support the BasicResearch Policy

MoH, MoD,MoSIT, CoHE, Univ, STRCoT,MoNE, NGO

Implementationof the regulation

2013

-20

15

1.4. Establishment of an organization to coordinateefforts, management and financing for thefield of life medical sciences in Turkey

MoH, STRCoT,MoSIT, MoD,MoF, MoE, UoT

Preparation ofregulations

2013

-20

14

ilaç gibigelecek!

Action PlanBasic and Clinical Research

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 34

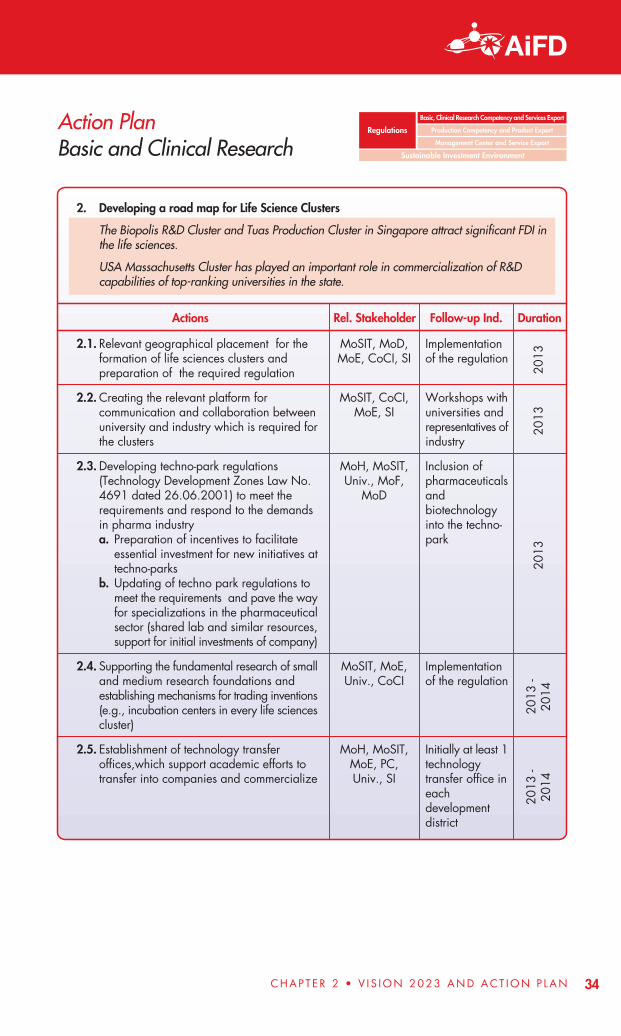

2.1. Relevant geographical placement for theformation of life sciences clusters andpreparation of the required regulation

MoSIT, MoD,MoE, CoCI, SI

Implementationof the regulation

Actions Rel. Stakeholder Follow-up Ind. Duration

2. Developing a road map for Life Science Clusters

The Biopolis R&D Cluster and Tuas Production Cluster in Singapore attract significant FDI inthe life sciences.

USA Massachusetts Cluster has played an important role in commercialization of R&Dcapabilities of top-ranking universities in the state.

2013

2.2. Creating the relevant platform forcommunication and collaboration betweenuniversity and industry which is required forthe clusters

MoSIT, CoCI,MoE, SI

Workshops withuniversities andrepresentatives ofindustry

2013

2.3. Developing techno-park regulations(Technology Development Zones Law No.4691 dated 26.06.2001) to meet therequirements and respond to the demandsin pharma industrya. Preparation of incentives to facilitate

essential investment for new initiatives attechno-parks

b. Updating of techno park regulations tomeet the requirements and pave the wayfor specializations in the pharmaceuticalsector (shared lab and similar resources,support for initial investments of company)

MoH, MoSIT,Univ., MoF,

MoD

Inclusion ofpharmaceuticalsandbiotechnologyinto the techno-park

2013

2.4. Supporting the fundamental research of smalland medium research foundations andestablishing mechanisms for trading inventions(e.g., incubation centers in every life sciencescluster)

MoSIT, MoE,Univ., CoCI

Implementationof the regulation

2013

-20

14

2.5. Establishment of technology transferoffices,which support academic efforts totransfer into companies and commercialize

MoH, MoSIT,MoE, PC,Univ., SI

Initially at least 1technologytransfer office ineachdevelopmentdistrict

2013

-20

14

Regulations

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T35

Action PlanBasic and Clinical Research

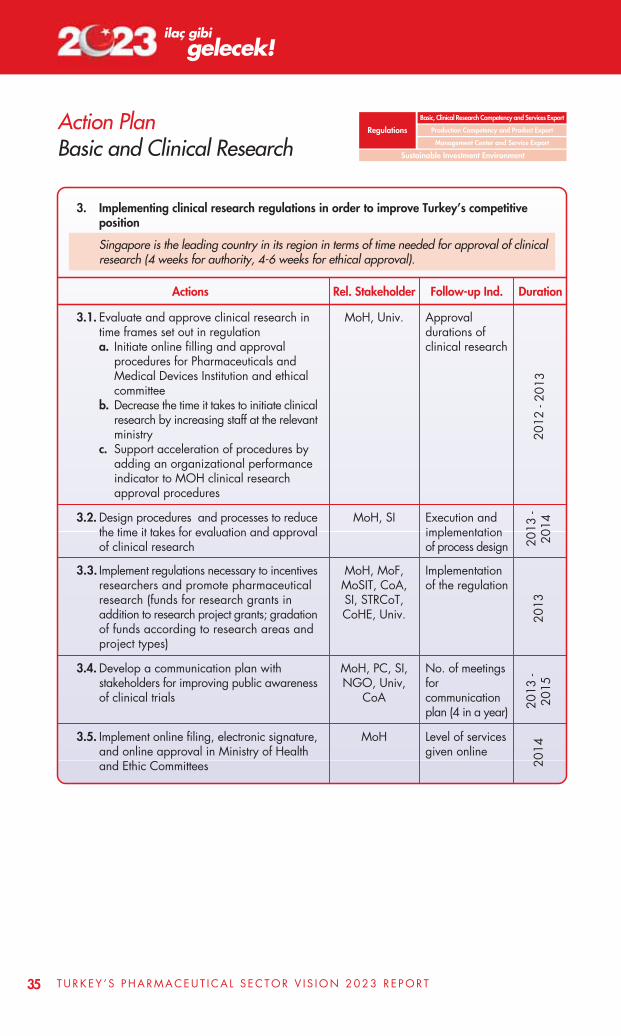

3. Implementing clinical research regulations in order to improve Turkey’s competitiveposition

Singapore is the leading country in its region in terms of time needed for approval of clinicalresearch (4 weeks for authority, 4-6 weeks for ethical approval).

3.1. Evaluate and approve clinical research intime frames set out in regulationa. Initiate online filling and approval

procedures for Pharmaceuticals andMedical Devices Institution and ethicalcommittee

b. Decrease the time it takes to initiate clinicalresearch by increasing staff at the relevantministry

c. Support acceleration of procedures byadding an organizational performanceindicator to MOH clinical researchapproval procedures

MoH, Univ. Approvaldurations ofclinical research

Actions Rel. Stakeholder Follow-up Ind. Duration

2012

- 20

13

3.2. Design procedures and processes to reducethe time it takes for evaluation and approvalof clinical research

MoH, SI Execution andimplementationof process design 20

13 -

2014

3.3. Implement regulations necessary to incentivesresearchers and promote pharmaceuticalresearch (funds for research grants inaddition to research project grants; gradationof funds according to research areas andproject types)

MoH, MoF,MoSIT, CoA,SI, STRCoT,CoHE, Univ.

Implementationof the regulation

2013

3.4. Develop a communication plan withstakeholders for improving public awarenessof clinical trials

MoH, PC, SI,NGO, Univ,

CoA

No. of meetingsforcommunicationplan (4 in a year) 20

13 -

2015

3.5. Implement online filing, electronic signature,and online approval in Ministry of Healthand Ethic Committees

MoH Level of servicesgiven online

2014

Regulations

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 36

Action PlanBasic and Clinical Research

4. Increasing the variety of R&D financing resources to encourage & support an increase inlife sciences R&D

In Massachusetts, USA, along with USD 1 billion of various state funds, researchers andresearch companies receive support by 30 venture capital funds, amounting to USD 1.1 billion.

In Ireland, postgraduate research programs with R&D projects, R&D infrastructure, education,and advisory services are supported by investment improvement agency funds. USD 1.2 billionof investment has been made in postgraduate programs in order to increase research capacitysince 1998.

4.1. Promote and provide institutional support toensure that Turkish pharma researchenterprises can benefit from internationalcapital funds

ISPAT, PC, SI,MoE, MoSIT

No. of seminars-meetings/year

Actions Rel. Stakeholder Follow-up Ind. Duration

2013

4.2. Establish a Turkish Government venture capitalfund to support basic research by small andmedium research organizations

MoSIT, UoT,MoE, SMEDO

Establishment ofventure capitalfund 20

13 -

2014

4.3. Develop new incentive programs/and reviseexisting R&D support programs in TÜB‹TAK,TTGV and programs like SAN-TEZ inaccordance with the R&D objectives ofpharma industry and update theseperiodicallya. To determine the grant amounts, periods

and assessment criteria according to thespecific properties of basic and appliedsciences

b. Generating an innovation-based supportmechanism by transparently evaluatingresearch projects and researchersaccording to determined success criteria

MoSIT,STRCoT, MoF

Follow-up ofsupportedprojects and tehiroverall successrate

2013

SuppertMechanisms

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T37

4. Increasing the variety of R&D financing resources to encourage & support an increase inlife sciences R&D (continued)

Actions Rel. Stakeholder Follow-up Ind. Duration

4.4. Develop regulations that allow clinical andtranslational research to benefit fromincentives under the R&D lawa. Remove the requirement in article 6. 1.d.

of the R&D regulation numbered 5746(Regulation of Implementation and Auditon the support of R&D activities, publishedon the Official Gazette dated 31.07.2008, numbered 26953) which mandates thata minimum of two clinical trials (amongclinical phases I-III) are obliged to beconducted in Turkey in order to benefitfrom incentives.

b. Revise the requirement in article 4.1.band 15.1.a that an R&D center mustemploy at least 50 full-time R&D employeesso as to decrease the requirement for full-time employment and reduce constraintsfor pharma basic and clinical research.(If a clinical trial is conducted in thepharmaceutical company’s own laboratoryor R&D center by personnel employed bythe pharmaceutical company, incentivescannot be utilized at present)

MoSIT, MoH,MoF, MoE, SI

Amendment ofrelevantlegislation

The number ofclinical trials thatutilize incentives

2013

Action PlanBasic and Clinical Research

SuppertMechanisms

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

ilaç gibigelecek!

Action PlanBasic and Clinical Research

5. Strengthening collaboration between universities and pharmaceutical industry

The life sciences ability management and biotechnology program aims to train thenecessary workforce for the life sciences areas in industry and academia in Massachusetts,USA.

5.1. Create and support platforms to facilitatecooperation between university and industrya. Initiate large scale and multi-stakeholder

(university, public, private sector) researchprograms through TÜB‹TAK and relevantinstitutions, similar to the Inovita LifeSciences and Technologies IstanbulCooperation Platform

MoSIT, MoE,STRCoT, Univ,SI, PC, CoCI

Increase innumber ofcooperations inlife sciences

Actions Rel. Stakeholder Follow-up Ind. Duration

2012

-20

15

5.2. Develop legislation that will allow researchersto work both in techno-parks and in privatesector R&D centers with similar benefits

MoH, CoHE,Univ, SI

Amendment ofrelevantlegislation 20

13

5.3 Develop legislation that will allow researchersto work in every research center and enablesustainable finance and management ofresearch centersa. Improve legislation related to employment

of full-time employees/technicians inresearch centers

b. Provide governmental financial supportuntil stronger relations with industry areformed

c. Improve legislation to increase the portionallocated to researchers in researchfunding

MoH, MoSIT,MoD, CoHE,

MoLSS,STRCoT, MoF,

Univ, SI

Full-timepersonnel rate inresearch centers

Rate of non-public income tototal income inresearch centers 20

13

5.4. Facilitate private sector guidance and supportof academic stuff to increase participationof researchers in international researchnetworks of pharmaceutical companies andinstitutionsa. Increase participation in clinical research

studies conducted on internationalplatforms

Univ, PC, SI,CoCI

Number ofGlobal Basic andClinical studies inTurkey thatresearchersparticipate in

2012

- 20

15

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 38

SuppertMechanisms

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T39

Action PlanBasic and Clinical Research

6. Developing infrastructure to motivate & improve the level of research of universities and research hospitals, and to enable the integration of this research within globalR&D networks

TGNA, CoHE,MoF, MoH,

Univ., ERH, SI

Enforcement ofrelevantlegislation

Ratio of netsalary of doctorsto total clinicalresearch budget

6.4. Implement regulations that encourage greaterremuneration of academic staff working inbasic and clinical research

MoH, CoHE,Univ.

Enforcement ofrelevantlegislation

6.5. Develop working hour regulations that allowacademics to conduct research for product& service development

Actions Rel. Stakeholder Follow-up Ind. Duration

6.1. Develop a road map aimed at integratinga qualified labor force in Turkey into globalR&D studiesa. Assess research capabilities & interests

of Turkish scientists & Turkish expatriatesscientists, and implement mechanism forcontinuous monitoring

b. Organize workshops aimed atdeveloping or enhancing collaborationwith Turkish scientists in successful R&Dcenters around the world

SI, PC, NGO,MoSIT, CoHE,

Univ.

Taking inventoryof scientists andintegration ofthem into adatabase.

Number ofworkshopsorganized

2012

-201

4

MoH, CoHE,Univ, MoSIT, SI

Number ofdepartmentsestablished

6.2. Establish bachelors, masters and doctorateprograms in biomedical and clinicalengineering which will be necessary toincrease R&D and domestic pharmaceuticalproductiona. Enhance interdisciplinary programs for

increasing academic capacity in Turkishuniversities in necessary areas

2013

- 20

15

CoHE, MoSIT,Univ., NGO,

SI, PC

Number ofacademicsappointed

6.3. Improve ability of academic staff to transferknowledge, have simultaneous appointmentswithin the country and abroad, and supportcollaboration and global integration 20

12 -

2014

2012

2013

Resources &Infrastructure

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 40

Action PlanBasic and Clinical Research

7. Standardizing clinical trials procedures to match international standards

Actions Rel. Stakeholder Follow-up Ind. Duration

7.1. Provide necessary training of stakeholdersso that clinical studies can be conducted ina rapid, ethical and effective way.a. Ethical Committee and Ministry of Health

audit committee's take necessary trainingregarding process

b. Investigators are provided necessarytechnical education related to clinicalstudies

c. In undergraduate study, add technicaleducation about Clinical Research to thesyllabus

MoH, SI, PC,MoHE, MoNE,

Univ.

Number ofpeople to whomeducationtraining isprovidedthroughout theyear

2012

- 20

13

MoH, TAA, TSI Ratio of certifiedinstitutions

7.2. Audit all stakeholders conducting clinicaltrials and research to assure they are meetingnecessary Good Clinical Practice (GCP),Good Laboratory Practice (GLP) criterion 20

13 -

2014

MoH, Univ.,ERH, CoHE,

PC

Amount ofresearch perclinic center

7.3. Improve clinical studies infrastructure atuniversities and hospitals, and increasecapacity for clinical studies 20

13 -

2014

Resources &Infrastructure

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T41

8. Implementing information systems and a judicial framework to support life sciencesresearch

England aims to establish a Clinical Research Web Access wherein clinical researchinformation is published by the National Health Service (NHS) which has made it centerof innovation.

Actions Rel. Stakeholder Follow-up Ind. Duration

8.1. Standardize and integrate current datasystems (family health practices andhospitals)

MoH, SSI Integrationpercentage ofcurrent systems 20

13

8.2. Develop legislation in order to omit personalidentifiers and to sort anonymous data intoprioritized categories (age/geographicarea/illness, etc)

MoH, SSI Preparing relatedregulations

2013

-20

14

8.3. Create a legal framework for usage of thisdata (terms of use, duration, authorizationmechanisms and responsibility for criminalsanctions)

MoH, SSI, MoJ,MoSIT

Preparing relatedregulations

2013

-20

148.4. Activate “Saglik.net” (health.net) system MoH, SSI Percentage of

health.net systemthat is working 20

13 -

2014

8.5. Create a voluntary database based on data-processing infrastructure that researchersdoing clinical research can benefit from;transform database into a transparentapplication that volunteers can use

MoH, Univ.,ERH, SI, SSI,

NGO

Preparingnecessaryregulations

The ratio of datarecorded

2013

-20

16

Action PlanBasic and Clinical Research

Resources &Infrastructure

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 42

Action PlanProduction and Export

9. Determining the production plans for priority fields in alignment with Turkish PharmaceuticalIndustry’s strategy

Actions Rel. Stakeholder Follow-up Ind. Duration

9.1. Map out an Inventory of Turkishpharmaceutical industry (facilities, productioncapacity and usage rate, actual production,production range, production structure,technological level, etc.)

MoH, MoSIT,MoE, MoD, PC,

SI, UCCT

Carrying out adetailedinventory ofpharmaceuticalindustry

2012

MoE, MoH,MoSIT

Enact incentivepackage

9.2. Implement the regulation of the IncentivePackage declared in April 2012

(The new incentive system became effective20 June 2012 by the Notification on StateAid for Investments Decree and Applicationof the Decree. Only the criteria for strategicinvestments were defined. The relatedcommission was held responsible forselecting strategic investments. None theless, some biotechnological products, bloodproducts and oncology products are defined as prioritized investment areas in the StateAid for Investments Decree no:2012/3305, Article 17.1.e, issued 19.06.2012)

2012

MoH, MoSIT,MoE, MoD, PC

Publish of theaction plan

Determine ofother prioritizedproduction areasconsiderednecessary

9.3. Include the government’s prioritizedproduction areas (oncology, biotechnology,blood products) that were announced bythe Incentive Package in April 2012 to theTurkish Pharmaceutical Industry Strategyand, if necessary, determine other prioritizedareas and develop an action planaccordingly. In June 2012, some biotechproducts, blood products and oncologyproducts were defined as prioritizedinvestment areas (the State Aid forInvestments Decree no:2012/3305 , Article17.1.e, issued 19.06.2012

2012

Regulations

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T43

Action PlanProduction and Export

SB, EB No. of countrieswith which mutualrecognitionagreements aresigned

10.2. Apply to the Pharmaceutical InspectionConcention & Pharmaceutical InspectionCooperation Scheme (PIC/S), and enterinto mutual recognition agreements withcountries that are target export markets

BSTB, SB, SGK Implementation ofregulation

10.3. Apply pricing conditions compatible withglobal pharmaceutical pricing

MoH, SSI Implementation ofregulation

10.4. Develop market access regulations that alignwith global market access conditions

10. Developing an action plan to increase the volume of exports

Actions Rel. Stakeholder Follow-up Ind. Duration

10.1. Having determined potential export markets,develop of action plans to improve exportsto these countries (bilateral licensingagreements)

BSTB, EB,YDTA, T‹M,DE‹K, ‹SF

At least 5 prioritycountriesidentified 20

1320

13 -

2014

2013

2013

10.6. Develop action plan to improve the ecosystemso as to create a competitive environment vis-a-vis other emerging markets that will attractmanufacturing investments by which Turkeybecomes the global supplier for selectedproduct lines

MoH, MoSIT,MoE, TEA, PC,

SI

Implementation ofaction plan andregulation

MoSIT, MoE Determination ofat least 5 rawmaterials givenglobalconsumptionlevels

10.7. Determine of competitive advantages in termsof raw materials, auxiliary materials andpackage production; complete feasibilitystudies

10.5. Remove licensing obligations for exportproduction purposes

MoH, MoSIT Implementation ofregulation 20

1220

12 -

2013

2013

Regulations

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 44

11. Providing the necessary support to increase the volume of production in the relevant lifesciences cluster

Biomedical intervention was established in Singapore in 2000 in order to create a biomedicalscheme within the government’s improvement plan for the biomedical industry. It was carriedout by the Research, Innovation and Intervention High Commission and will improve theclustering process in 3 stages: 2000-2005 improvement of infrastructure and collaboration;2006-2010 improvement of R&D sustainability; 2011-2015 creation of economic outputand contribution to growth.

11.1. Develop the necessary regulations to ensurethe investments in the cluster benefit from theincentives in the Incentive Package launchedApril 2012 (According to the new incentivesystem that became effective by the State Aidfor Investments Decision no:2012/3305issued in 19.06.2012 and the Notificationon State Aid for Investments and Applicationof the Decree no:2012/1 issued in20.06.2012, large scale investments inOrganized Industrial Zones (OIZ) andinvestments covered under regional incentivescould benefit from incentives for less developedregions in which they are located. (Regionsare divided into 6 classes based on level ofdevelopment.)

TGNA, MoH,MoSIT, MoE

Implementation ofregulation

(the decree lawon State Aid forInvestments andApplication of theDecree numbered28239, No:2012/1 issued in20 June 2012)

Actions Rel. Stakeholder Follow-up Ind. Duration

2012

Action PlanProduction and Export

Regulations

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T45

Action PlanProduction and Export

12. Incentivizing the prioritized production areas

Actions Rel. Stakeholder Follow-up Ind. Duration

12.1. Ensure incentives for prioritized productionfields (oncology, biotechnology, bloodproducts, etc.) identified by incentive systemannounced in April 2012 are used byinvestors• The State Aid for Investments Decree

no:2012/3305 issued in 19.06.2012in Official Gazette numbered 28328.

• The Notification on State Aid forInvestments and Application of theDecree no:2012/1 issued in20.06.2012 in Official Gazettenumbered 28329. By these law andnotification the design of the legalinfrastructure regarding the new incentivesystem has been completed

ISPAT, PC,MoH, MoSIT

Number ofapplications forbenefitingincentives

Value ofincentives whichcompanies utilizePositive/Negative respond rateof applications 20

12 -

2013

MoLSS, MoF Average time toobtain temporaryemploymentpermits

13.2. In high technology production, granttemporary employment permits for foreignexperts

13. Incentivizing and facilitating knowledge transfer in high-technology production

13.1. Develop incentives and financingadvantages for high-technology investmentswithin the Incentive Package announcedto public in April 2012 and/or in the TurkishPharmaceutical Industry Strategy preparedby MoSIT (In the new incentive system thatis based on the State Aid for InvestmentsDecree no:2012/3305 issued in19.06.2012 and the Notification on StateAid for Investments and Application of theDecree no:2012/1 , 4 types of incentivemechanism were defined; however theinvestment for high technology is notspecified.)

MoSIT, MoE,MoH, MoF,

MoCT

Regulation ofrelevantlegislation

2012

2015

SuppertMechanisms

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 46

Action PlanProduction and Export

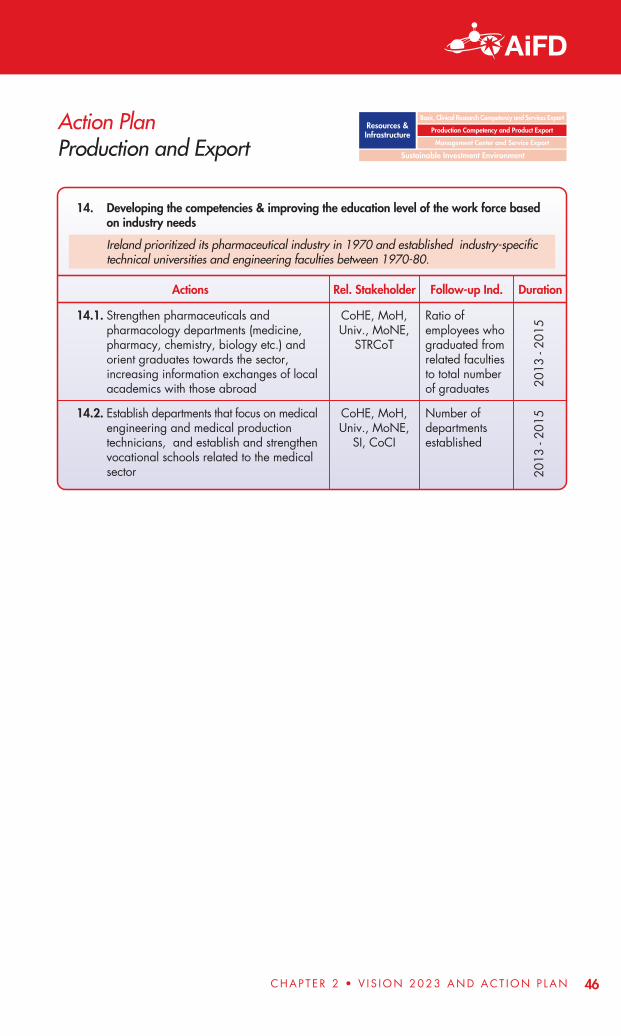

14. Developing the competencies & improving the education level of the work force basedon industry needs

Ireland prioritized its pharmaceutical industry in 1970 and established industry-specifictechnical universities and engineering faculties between 1970-80.

14.1. Strengthen pharmaceuticals andpharmacology departments (medicine,pharmacy, chemistry, biology etc.) andorient graduates towards the sector,increasing information exchanges of localacademics with those abroad

CoHE, MoH,Univ., MoNE,

STRCoT

Ratio ofemployees whograduated fromrelated facultiesto total numberof graduates

Actions Rel. Stakeholder Follow-up Ind. Duration

2013

- 20

15

14.2. Establish departments that focus on medicalengineering and medical productiontechnicians, and establish and strengthenvocational schools related to the medicalsector

CoHE, MoH,Univ., MoNE,

SI, CoCI

Number ofdepartmentsestablished

2013

- 20

15

Resources &Infrastructure

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T47

Action PlanManagement Center

15. Provide tax incentives to international life sciences executives who provide services abroad

Actions Rel. Stakeholder Follow-up Ind. Duration

15.1. Eliminate tax disadvantages of internationalexecutives/qualified white-collar workforcewho work as experts in free-trade zonesand R&D centers:For the foreign-owned companies,coordination and management of affiliationsand business units in Europe, Asia and theMiddle East are allowed to function inTurkey as a Regional Management Centerby the Amendment of the ImplementationRegulation of Foreign Direct Investment Lawissued on 3.7.2012 in Official Gazettenumbered 28342,. In this context , wagesof employees in a Regional ManagementCenter in Turkey will not be subject toincome tax and exempted from stamp taxin accordance with income tax legislation.Tax disadvantages for white-collaremployees have been eliminated by thislegislation. However a similar legislationshould be implemented for R&D personnel

MoLSS, MoF,MoE

Implementationof regulation

Taxdisadvantageseliminated forwhite-collarpersonnel by theAmendment oftheImplementationRegulation ofForeign DirectInvestment Lawissued on3.7.2012;similar revision isstill needed forR&D personnel

2013

Regulations

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 48

Action PlanManagement Center

16. Execute a publicity campaign to highlight the advantages of locating a managementand/or a shared services center in Turkey

Actions Rel. Stakeholder Follow-up Ind. Duration

16.1. Participate in domestic and internationalplatforms to explain the advantages toinvestors about why their managementand/or shared services center should belocated in Turkey

ISPAT, PC Number ofrelated meeting/ seminars

2013

- 20

14

SuppertMechanisms

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T49

Action PlanManagement Center

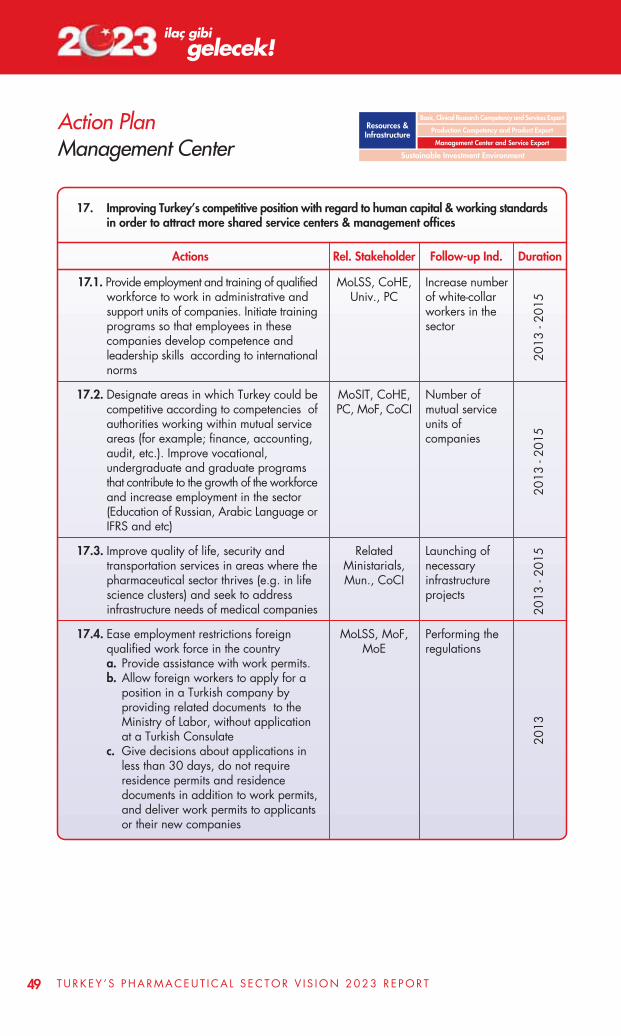

17. Improving Turkey’s competitive position with regard to human capital & working standardsin order to attract more shared service centers & management offices

Actions Rel. Stakeholder Follow-up Ind. Duration

17.1. Provide employment and training of qualifiedworkforce to work in administrative andsupport units of companies. Initiate trainingprograms so that employees in thesecompanies develop competence andleadership skills according to internationalnorms

MoLSS, CoHE,Univ., PC

Increase numberof white-collarworkers in thesector

2013

- 20

15

MoSIT, CoHE,PC, MoF, CoCI

Number ofmutual serviceunits ofcompanies

17.2. Designate areas in which Turkey could becompetitive according to competencies ofauthorities working within mutual serviceareas (for example; finance, accounting,audit, etc.). Improve vocational,undergraduate and graduate programsthat contribute to the growth of the workforceand increase employment in the sector(Education of Russian, Arabic Language orIFRS and etc)

2013

- 20

15Related

Ministarials,Mun., CoCI

Launching ofnecessaryinfrastructureprojects

17.3. Improve quality of life, security andtransportation services in areas where thepharmaceutical sector thrives (e.g. in lifescience clusters) and seek to addressinfrastructure needs of medical companies 20

13 -

2015

MoLSS, MoF,MoE

Performing theregulations

17.4. Ease employment restrictions foreignqualified work force in the countrya. Provide assistance with work permits.b. Allow foreign workers to apply for a

position in a Turkish company byproviding related documents to theMinistry of Labor, without applicationat a Turkish Consulate

c. Give decisions about applications inless than 30 days, do not requireresidence permits and residencedocuments in addition to work permits,and deliver work permits to applicantsor their new companies

2013

Resources &Infrastructure

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 50

Aciton PlanSustainable Investment Environment

18. Developing legal and administrative regulations that both align with Turkey’s visionfor pharmaceutical industry and counterbalance the interests of the pharmaceuticalsector and public health authorities

Actions Rel. Stakeholder Follow-up Ind. Duration

18.1. Provide necessary regulations that arecompatible with international standards,mindful of the investor, transparent andpredictable ( New Turkish CommercialCode which has come into effect as of 1July 2012 is a good example oftransparency)

RelatedMinistries.

Speed ofupdatingregulation

2013

RelatedMinistries.

Speed ofupdatingregulation

18.2. Develop legislation in a way that it doesnot allow for broad interpretation, is clearand based on objective and measurablecriteria

2013

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

Aciton PlanSustainable Investment Environment

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T51

19.2. Until the mutual recognition is secured:a. Review GMP and registration

applications concurrentlyb. Ensure transparency in GMP processes

and share these with stakeholders, agreeon criteria and timetables

c. Increase number of GMP audit staff atMinistry of Health

d. Implement risk-based audit approach toGMP audits• Allow for non facility-based GMP

audits, independent of the productitself

• Allow for paper documentation inplace of physical audits in clearlydefined cases

MoH Implementing theregulation

2013

19. Develop regulations to increase patients’ access to innovative healthcare products andenable reliable and rapid market access

In Ireland, reimbursement decisions for new products are based on the Ireland Health TechnologyAssessment Guide. This guide is prepared according to a collective agreement of the HealthHigh Commission and Ireland Medicine and Health Institution (Reimbursement decisions for“existing products” are made in 60 days or less and “for new products” max. 90 days).

In Ireland, there are 3 types of registration procedures; there is a different procedure forinnovative medicines. Sales permission is given to European Medicine Agency (EMA) licensedproducts.

In Singapore, drug pricing is left to market forces in the private sector, but in the public sectordrugs are divided into two categories: ‘standard’ and ‘non-standard’. Standard drugs aresubsidized by the government.

Actions Rel. Stakeholder Follow-up Ind. Duration

19.1. Develop a regulatory framework that allowsfor fast introduction of new and innovativeproducts into the marketa. Exclude innovative medicines from

budgetary control actionb. Use current exchange rates when setting

pharmaceutical prices

MoH, SSI Implementing theregulation

2013

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

ilaç gibigelecek!

Aciton PlanSustainable Investment Environment

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 52

19. Develop regulations to increase patients’ access to innovative healthcare products andenable reliable and rapid market access (continued)

19.4. Improve reimbursement and pricingimplementation in accordance with legalduration and legislationa. Develop and implement of regulations

regarding pricing, reference pricing andfixed exchange rate application

b. Define & implement criteria related toinputs/outputs on reimbursement listsand make them transparent

c. Implement the current legislation byholding regular meetings of thereimbursement commission (three timesa year) and preparing annual actionplans

SSI Application ofchange inexchange ratesfrequency ofcommissionmeetings;implementingcurrencychanges;placing relatedregulations inrelatedannouncements

2013

Actions Rel. Stakeholder Follow-up Ind. Duration

19.3. Accelerate registration of applicationsa. Allow clinical benefits to be sufficient

criteria for the registration processb. Allow for an accelerated registration

process according to the EU and EMAcriteria

MoH Finalization ofregistrationapplicationswithin 210 days,which is an ABcriteria

2013

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T53

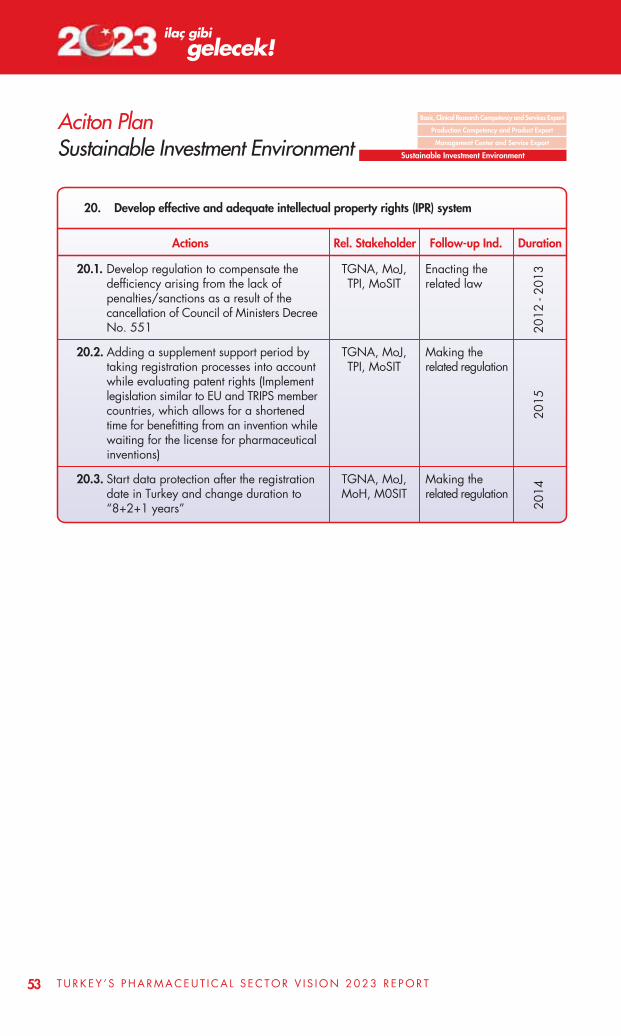

TGNA, MoJ,TPI, MoSIT

Enacting therelated law

20.1. Develop regulation to compensate thedefficiency arising from the lack ofpenalties/sanctions as a result of thecancellation of Council of Ministers DecreeNo. 551 20

12 -

2013

Actions Rel. Stakeholder Follow-up Ind. Duration

20. Develop effective and adequate intellectual property rights (IPR) system

TGNA, MoJ,TPI, MoSIT

Making therelated regulation

20.2. Adding a supplement support period bytaking registration processes into accountwhile evaluating patent rights (Implementlegislation similar to EU and TRIPS membercountries, which allows for a shortenedtime for benefitting from an invention whilewaiting for the license for pharmaceuticalinventions)

2015

TGNA, MoJ,MoH, M0SIT

Making therelated regulation

20.3. Start data protection after the registrationdate in Turkey and change duration to“8+2+1 years” 20

14

Aciton PlanSustainable Investment Environment

Basic, Clinical Research Competency and Services Export

Production Competency and Product Export

Management Center and Service Export

Sustainable Investment Environment

ilaç gibigelecek!

Abbrevations for stakeholders mentioned in the ActionPlan section

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 54

CoA

CoCI

CoHE

MoNE

ERH

FERB

ISPAT

MoCT

MoD

MoE

MoF

MoH

MoJ

MoLSS

MoSIT

Mun.

NGO

PC

SCST

SI

SMEDO

SSI

STRCOT

TAA

TEA

TGNA

TPI

TSI

UCCT

Univ

UoT

Abbrevation

Courf of Accounts

Chamber of Commerce and Industry

Commission of Higher Education

Ministry of National Education

Education and Research Hospitals

Foreign Economic Relations Board

Investment Support and Promotion Agency

Ministry of Customs and Trade

Ministry of Development

Ministry of Economy

Ministry of Finance

Ministry of Health

Ministry of Justice

Ministry of Labour and Social Security

Ministry of Science, Industry and Technology

Municipalities

Non Govermental Organizations

Pharma Companies

Supreme Council for Science and Technology

Sector Institutions (AIFD, IEIS, TISD)

Small and Medium Enterprises Development Organization

Social Security Institution

Scientific and Technological Research Council of Turkey

Turkish Accreditation Agency

Turkish Exporters Assembly

Turkish Grand National Assembly

Turkish Patent Institution

Turkish Standards Institutions

Union of Chambers and Commodity Exchanges of Turkey

Universities

Undersecretariat of Treasury

Description

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T55

Actions proposed for Turkish Pharmaceutical Industry haveyielded results in other countries.

The South Korean Government started restructuring its pharma sector via the BiotechnologyDevelopment Plan in 1994.

Key actions that improved R&D competency

Improved the regulatory and legal infrastructure

Restructured national biotech initiatives in order to support innovation and research

Expanded infrastructure for upgrading R&D

Achieved globalization of bio-industries

Basic, Clinical Research Competency and Service Export

Development through 1st plan

Establishment of KoreanBiotechnology ResearchInstitute in 1985

Biotech venture boomwith 500 enterprises

Government’sinvestment in biotechworth $5.5 bn since1994

9 bio-venture centerssupporting venturecapitals

1st FrameworkPlan forBiotechnologyDevelopment(1998 - 2007)

Target for 2016

Vision 2016

Rank 7th among allcountries for number ofscience technologypapers published

Rank 7th among allcountries forcompetitiveness inpatented technology

17,300 R&D manpowerwith post-graduatedegree

Industialized marketvalue: ~USD 66 bn

Status in 2006

Ranked 12th among allcountries for number ofscience technologypapers published.

2nd FrameworkPlan (2007-2016)

Ranked 15th among allcountries forcompetitiveness inpatented technology

9,500 R&D manpowerwith post-graduatedegree

15 new moleculeinventions since 1999

ilaç gibigelecek!

C H A P T E R 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 56

Ireland identified its pharma sector as a priority for FDIand improved investment environment for production.

Source: PwC Benchmark Analysis

Key success factors of the pharma sector

5 of the world’s top 12 medicines are manufactured in Ireland.

Pharmaceutical industry in Ireland created 2 out of every 5 pharmaceutical jobs whichcame to Europe in 2008.

11% of Ireland’s GDP is generated by the pharmaceutical industry.

Pharma exports worth EUR 31 bn in 2010 and sector generates over 50% of Ireland’stotal exports.

Production Competency and Product Export

In 1970, the InvestmentDevelopment Agency (IDA)

identified the pharma industry asa priority for foreign investment.

Between 1970-80, 9 technicaluniversities, research centers, andengineering faculties were founded

for targeted industries.

In 2000, the “Science FoundationIreland” was founded.

In 2006, the Science, Technologyand Inovation Strategy for 2006 -

2013 was launched by thegovernment with promises to invest

EUR 3.8 bn.

Incentives

LABOR

Social securitycontributions arelowest in EU(10.75%)

Easy access toskilled labor

TAX

12.5% CorporateTax Rate

25% R&D taxcredit

Intellectualproperty tax write-offs

T U R K E Y ’ S P H A R M A C E U T I C A L S E C T O R V I S I O N 2 0 2 3 R E P O R T57

Massachusetts, USA became management center forpharma companies by providing financing sources and aqualified workforce.

Key Facts

Industry

240 pharma & biotech companies: of 83 are listed

Funding

30 Venture Capital Firms: USD1.1 bn VC investmentfor biotech in 2010,24% of all US biotech VC investment, available inMassachusetts,NIH funding

University / Medical Center

16 medical centers and 5 of the top eight NIH funded hospitals: Harvard, Uni. of MA,Boston, MIT, Tufts)5,997 research facilities covering thousands of square feet

Talent Base

More than 85,000 high-tech research employees and more than 340,000 medicalemployeesLife Sciences Talent Initiative and Biotech Program: Study conducted to developcollaborative statewide strategy between business, government and higher educationto ensure that the state's talent needs in life sciences are met.

Regulatory Environment

In 1980, Massachusetts Biotechnology Council (MBC) was formed.MA Life Sciences Initiative: Designed to administer the state's 10-year, USD1 bn lifesciences initiative to support the cluster through job growth, economic development.State governors also promoted MA as a location for biotech expansion at all biotechtrade shows and conferences.State supported shared services to achieve cost efficiency.

Management Center And Service Export

Availability ofFunding

AdvancedUniversity andMedical Center

Presence

IndustyPresence

MA Cluster

Regulatory andBusiness

Environment

Availability ofSignigicentTalent Base

Source: PwC Benchmark Analysis

ilaç gibigelecek!

S E C T I O N 2 • V I S I O N 2 0 2 3 A N D A C T I O N P L A N 58

Sustainable Investment Environment

In China, approval processes were sped up under the name “Green Channel” forensuring the rapid introduction of innovative products to the market.