tuning in the rise of online video in latin america (4)

TRANSCRIPT

Festival of Media LatAm | 24 September 2012

Gian Fulgoni Executive Chairman and Co-founder, comScore

Tuning In:

The Rise of Online Video

in Latin America

1 Online Video Viewing in Latin America

2 What Can We Learn from the U.S.?

3 Some Thoughts for the Future

In 1996, 2/3 of world’s Internet population was in the US, yet today Asia Pacific is the largest region

with over 40% of online population.

Many emerging regions likely to bypass old modes, skipping dial-up to go straight to broadband,

making multimedia, video, and collaborative content immediately accessible.

Early adoption of mobile web in addition to PC web will likely be popular in many of these high-

growth areas.

Asia Pacific

Distribution of Worldwide Internet Audience

66%

13%

34%

87%

1996 2011

U.S. Internet Population vs. Rest of the World

Rest of the

World

U.S.

Source: comScore Media Metrix, Visitors Age 15+ Home/Work Location, Dec-2011

Asia Pacific, 41,3%

Europe, 26,4%

North America,

14,6%

Latin America,

9,0%

Middle East - Africa, 8,8%

The U.S. is No Longer the Center of the Online Universe

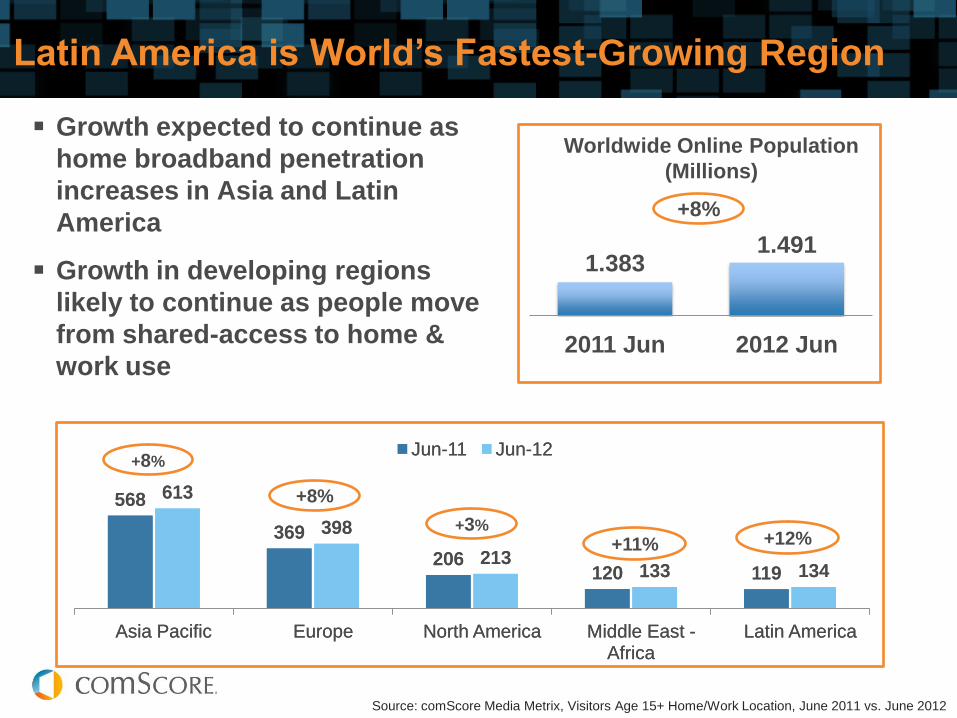

Latin America is World’s Fastest-Growing Region

568

369

206 120 119

613

398

213 133 134

Asia Pacific Europe North America Middle East - Africa

Latin America

Jun-11 Jun-12

Growth expected to continue as

home broadband penetration

increases in Asia and Latin

America

Growth in developing regions

likely to continue as people move

from shared-access to home &

work use

+8%

+8%

Worldwide Online Population

(Millions)

Source: comScore Media Metrix, Visitors Age 15+ Home/Work Location, June 2011 vs. June 2012

+8%

+3%

+11% +12%

568

369

206 120 119

613

398

213 133 134

Asia Pacific Europe North America Middle East - Africa

Latin America

Jun-11 Jun-12

1.383 1.491

2011 Jun 2012 Jun

Focus: Latin America

July 2010 Penetration Data V0910

Latin America

Argentina

Brazil

Chile

Mexico

Growth in Video Viewing in 2011

Total Videos Viewed (000) Dec-2011

Percent Growth vs. Dec. 2010

BRAZIL 4.7 Billion +74%

MEXICO 3.0 Billion +80%

ARGENTINA 1.5 Billion +75%

CHILE 1.0 Billion +91%

Online Video’s Blockbuster Year Videos Viewed Grew by Double Digits Across LatAm Region

1

Source: comScore Video Metrix, July-2012

MEXICO

Videos

(Millions)

Share of

Videos

Google Sites 2,164 62%

VEVO 219 6%

Viacom Digital 54 2%

CHILE

Videos

(Millions)

Share of

Videos

Google Sites 927 80%

VEVO 58 5%

Viacom Digital 17 2%

BRAZIL

Videos

(Millions)

Share of

Videos

Google Sites 4,435 75%

Globo 359 6%

VEVO 193 3%

ARGENTINA

Videos

(Millions)

Share of

Videos

Google Sites 988 63%

VEVO 65 3%

Facebook.com 22 1%

Driven by YouTube, Google Sites Account for

More than 60% of Videos Viewed in LatAm

Video Consumption in LatAm skews younger … with under 34

age segment accounting for almost 60% of videos viewed

15-24 25-34 35-44 45-54 55+

28% 30%

21%

14%

8%

Source: comScore Video Metrix, July-2012

% Composition of Video Time Spent

Reach of online video is slightly greater in the LatAm

region than Worldwide

82%

92%

81%

96%

85%

84%

Mexico

Chile

Brazil

Argentina

USA

Worldwide

Monthly Online Video Reach / Web Population

Source: comScore Video Metrix, July-2012

Room for growth in video consumption in LatAm

151,2

168,6

139,2

120,0

245,9

169,5

Mexico

Chile

Brazil

Argentina

USA

Worldwide

Videos per Viewer

Source: comScore Video Metrix, July-2012

Room for growth in video engagement in LatAm

13,63

12,45

11,61

11,32

22,05

19,40

Mexico

Chile

Brazil

Argentina

USA

Worldwide

Monthly Hours per Viewer

Source: comScore Video Metrix, July-2012

While growing rapidly in LatAm,

time spent watching online video

equivalent to only a percentage point

or two of the time spent watching TV

What Can We Learn from the U.S.?

SOURCE: IAB for Internet Advertising Revenue and KANTAR for Total Mediaedia

Measurement

$31.7 Billion U.S. Online

Ad Spending in 2011

+22% vs. year ago

IAB says U.S. online ad spend is now larger than newspapers,

magazines and radio, and equivalent to 46% of TV

10X Faster

Growth

Than

All Media

TV Online Video

44.581

1.338

44.334

2.321

US Monthly Total Hours (millions) Spent Watching TV vs. Online Video

Monthly Total Hours (millions) in Q4 2010

Monthly Total Hours (millions) in Q4 2011

In the U.S, time spent watching traditional TV is essentially flat while

online video is growing strongly

SOURCE: TV: Nielsen Cross Platform Report – Q4 2011. Online Video: comScore Video Metrix

-0.6%

+74%

Video now equals 5% of total time

spent watching TV

$1.8 Billion U.S. Online Video Ad Spending in 2011

IAB says U.S. online video ad spending is surging

Equivalent

to 6% of all

online ad

spending

+40% vs. year ago

SOURCE: IAB for Online and Various for Total Media dia

Measurement 2011

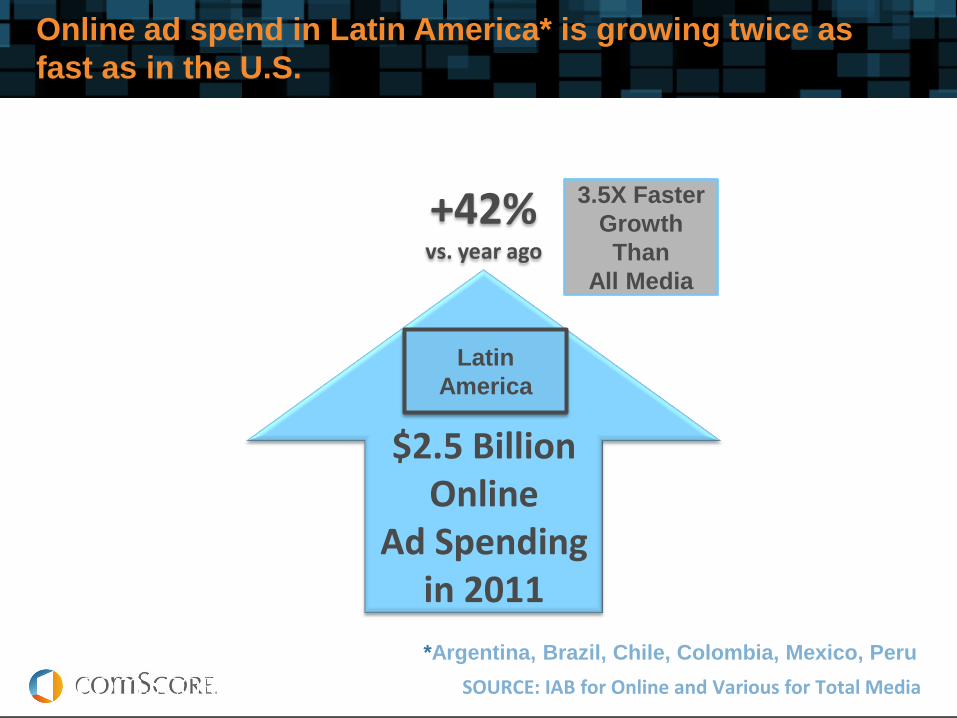

Online ad spend in Latin America* is growing twice as

fast as in the U.S.

3.5X Faster

Growth

Than

All Media

$2.5 Billion Online

Ad Spending in 2011

+42% vs. year ago

Latin

America

*Argentina, Brazil, Chile, Colombia, Mexico, Peru

Online video allows convenient viewing of TV content and

is an incremental audience – it’s not about avoiding ads

Recent comScore study sought to answer: why do viewers choose to watch

TV content online?

– NOT out of ad-avoidance

– Main factor is convenience and time-shifting

7%

13%

25%

38%

57%

71%

Don’t subscribe to cable/don't have a TV

Prefer the online experience

Like to see past episodes

Less ads

Convenience

Missed episode on TV

Online viewers of TV programs are open to more ads – at least 6.5 minutes

per TV hour

0,0

20,0

40,0

60,0

80,0

100,0

1 min 2 min 3 min 4 min 5 min 6 min 7 min 8 min 9 min 10 min 11 min 12 min 13 min 14 min 15 min

Negligible Minimal Long Enough Too Long

Base sizes:

Total=640

Optimal length of commercials for an hour of TV viewed online

*Respondents were asked questions on a sliding scale from ‘how much advertising is so

negligible that it would not interfere at all’, through to ‘how much advertising is too long and

would interfere completely with the viewing experience’?

A CBS Perspective on TV and Video Advertising from 2009

CBS: Online video ads can demand a premium price because

of heightened consumer attention and more precise targeting

CBS: Even with lower ad loads than TV but a premium price, video

ads can have same value as TV ads

The Limitation of TV: Brands Trying to Reach their Target with

TV Alone Hit A Plateau of Diminishing Returns

85,1 87,9

67,8 74,1

0

10

20

30

40

50

60

70

80

90

100

0 2.500 5.000 7.500 10.000 12.500 15.000

Cost ($000)

Total Reach

Effective Reach

Total Reach and Effective Reach for a TV

Campaign as a Function of Cost

Typically 30%+ of Target Audience is not Effectively reached

Adding Branding Advertising to TV With Online Video Builds

Reach and Effective Reach

Media Plan GRPs Total Reach Effective

Reach

TV Only 1,000 85% 68%

TV + Video Combination

TV (90%) 900 84% 66%

Online Video (10%) 500 64% 44%

TV + Online Video 1,400 90% 84%

TV Only vs.

90% TV + 10% Online Video 400 5% 16%

Impact of a 90/10 Allocation

Source: comScore simulation using

single source TV and Internet data

1 Online video viewing in LatAm is surging

2 Lessons from U.S.

Online video viewing of TV content incremental to TV

Consumers will accept online video ad loads of 10%+

Premium pricing possible for video ads

3 Online video advertising can add effective reach to a TV

campaign –especially among younger age segments

Summary Thoughts