tuesday 12 and wednesday 13 april, business design …€¦ · ufone ptml, senior manager finance...

TRANSCRIPT

Meetup Europe 2016

Tuesday 12 and Wednesday 13 April, Business Design Centre, London

Silver Sponsors: Exhibitors:Bronze sponsors:GOLD SPONSOR:

A unique networking opportunity with 200 leaders of the European telecom and broadcast tower industry

To discuss your participation, contact Annabelle on +44 7423 512588 or email [email protected]

Endorsed by:

Organised by:

The unique experience of a TowerXchange Meetup

< Europe market forecasts< Q&A with the CEOs< Round tables add insight< Structured introductions< Select your own agenda< Local market knowledge

< Market transformation< Next sale & leasebacks< BTS opportunities< Site upgrades< Energy opex reduction< Country specific round tables

Insights

Infrastructure focused

Personal development

Connections

Experience

Learning

< Network sharing JV leaders< Towerco CXOs< MNO tower strategists< Investors< Strategic advisors< Proven suppliers

< Networking< Selective audience< Curated exhibition< Relax and enjoy< Professionally hosted

< Telecom towers< Broadcast towers< Real estate< Decommissioning< Microcells and DAS< Monitoring< I&C and O&M

< Learn from 200+ peers, the leaders of the European tower industry< Align your role and strategy with the needs of the ecosystem

For more information visit www.towerxchange.com/meetups/meetup-europe

Day One | Tuesday 12 April

8:00 Coffee and registration

9.00 Opening presentation and TowerXchange analysisKieron Osmotherly, CEO, TowerXchangeLaura Dinnewell, Head of EMEA, TowerXchange

9:45 European towerco CXO panel – the big picture< Moderator: Kieron Osmotherly, CEO, TowerXchange< Scott Coates, CEO, Wireless Infrastructure Group< Frédéric Zimer, CEO, FPS Towers< Peter Owen Edmunds, Chairman, Russian Towers< Nicolas Ott, Managing Director, Telecoms, Arqiva

10:30 Broadcast assets & JV infracos in the telecoms mix< Moderator: Marco Cordoni, Senior Partner, Analysys Mason< Stefano Ciccotti, CEO, Rai Way< Malcolm Collins, CEO, CTIL< Nikos Babalis, CEO, Victus Networks

11:15 Coffee and networking

11:45 Roundtables session 1

12:45 Networking lunch

14:10 Roundtable session 2

15:10 Coffee and networking

15:40 Towerco investment, growth & exit strategies< Moderator: Gaurav Bath, Global Communications Group, Citi< Jack Colbourne, Partner, Arcus Infrastructure Partners

< Peter Egbertson, Director of Corporate Finance, Protelindo< Jack Dessay, Managing Director, Macquarie< Dany Rammal, Managing Director, EMEA, Providence Equity< Eric Crabtree, Chief Investment Officer, IFC< Vincent Policard, Director of Energy & Infrastructure, KKR

16:40 Improved monitoring, management and efficiency at cell sites< Senior Representative, Abloy< Senior Representative, Acsys< Senior Representative, Invendis< Senior Representative, Siterra, an Accruent Product< Senior Representative, Tarantula

17:00 End of day one and networking drinks

19:30 TowerXchange optional dinner

Day Two | Wednesday 13 April

8:30 Welcome coffee and breakfast hosted by FPS Towers

9:00 Keynote interview with Europe’s most acquisitive towerco< Interviewer: Enda Hardiman, Managing Partner, Hardiman Telecommunications< Interviewee: Tobias Martinez, CEO, Cellnex

9:20 Tower divestments, carve outs and M&A< Moderator: Alexandre Lucas, Executive Director, TMT Investment Banking, Goldman Sachs< Alexander Chub, President, Russian Towers< Colin Cunnigham, Managing Director, Cignal< Petr Slováček, CEO, CETIN< James MacLaurin, Director, Axiata

10:00 Energy management at European cell sites< Senior Representative, Heliocentris< Senior Representative, Medipower

10:20 Coffee and networking

10:50 Emerging European markets:< Moderator: Phil Cooper, Managing Director, EMEA, Digital Bridge< Temel Oktem, Head of Telecom, Media & Technology, Europe, Middle East and North Africa, IFC< Sergey Plissak, Commercial Director, Logycom Group< Sachit Ahuja, Vice President, Business Development, Tillman Global Holdings< Arthur Akopyan, Managing Director & Partner, UFG Asset Management< Zafer Ozbay, General Manager, UkrTower< Georgy Chumburidze, CEO, Vertical

11:30 Roundtable session 3

12:30 Networking lunch

13:40 Roundtable session 4

14:40 Coffee and networking

15:40 Small cells, DAS & heterogenous networks:< Moderator: Caroline Gabriel, Research Director & Co-Founder, Rethink Technology Research< Scott Coates, CEO, Wireless Infrastructure Group< Alexandre Mestre, International Business & Marketing Director, Cellnex< Nicolas Ott, Managing Director, Telecoms, Arqiva< Representative, Small Cell Forum

16:40 End of Meetup

TowerXchange Meetup Europe AgendaLondon | April 12-13, 2016

www.towerxchange.com/meetups/meetup-europe | TowerXchange Meetup Europe 2016, 12-13 April, London | 3

TowerXchange roundtables

| TowerXchange Meetup Europe, 12-13 April, London | www.towerxchange.com/meetups/meetup-europe4

Roundtable session 1: 11:45-12:45, 12 April

Country focus Russia< Alexander Chub, President, Russian Towers< Peter Owen Edmunds, Chairman, Russian Towers

Country Focus: Greece< Nikos Babalis, CEO, Victus Networks

Country Focus: France< Cedric Lepolard, CFO, FPS Towers

Decommissioning: Can it create value within an acceptable timescale?< David Bernal Cantero, Director of Business Development, Cellnex

European MNO consolidation: rumours, deals & drivers< Andrew Doyle, Managing Consultant, PA Consulting

Growing and scaling a towerco< Peter Egbertsen, Director of Corporate Finance, Protelindo

How to ensure a successful IPO< Julian Plumstead, Managing Director, Rothschild

Why is Europe different, how to be a successful towerco as markets mature?< Justin Speake, President, EuroTower

Strategic sourcing: what and how Europe’s tower owners buy to improve energy efficiency< Solange Karwera, Senior Category Manager, Network Site Infrastructure, Vodafone

Opportunities for towercos in small cells & DAS< Scott Coates, CEO, WIG

Roundtable session 2: 14:10-15:10, 12 April

Sourcing capital in Russia & the CIS< Arthur Akopyan, Managing Director & Partner, UFG Asset Management

Country Focus: Germany< Jonathan Dann, Managing Director, Telecom Research, RBC Capital Markets

Country Focus Ireland< Morag Pollock, GM, Towercom

What do you need to know about ground lease aggregation?< Bill Bates, International Business Development, SBA Communications

RAN sharing - threats and opportunities< Cedric Lepolard, CFO, FPS Towers< Pierre Cassier, Commercial Director, FPS Towers

Towerco valuations in Europe< Host TBC

TowerXchange roundtablesMaking the most of synergies between broadcast and telecoms< Nicolas Ott, Managing Director, Telecoms, Arqiva

Best practices in corporate governance and risk management for telecom infrastructure businesses< Belinda Fawcett, General Counsel, CTIL

Benchmarking tower efficiencies against best practice< Host TBC

Subcontractor performance management< Egor Bykov, Head of Strategy, Vertical

Roundtable session 3: 11:30-12:30, 13 April

Country focus Spain< Jorge Alberto Jimenez, President, Axion

Regional focus: CIS< Temel Oktem, Head of Telecom, Media & Technology, Europe, Middle East and North Africa, IFC

Country Focus: Poland< Darragh Stokes, Managing Partner, Hardiman Telecommunications

Regional Focus: Scandinavia< Henrik Kamstrup, Partner, KPR Consult

African market focus< Terry Rhodes, Co-founder & Director, Eaton Towers

How to carve out infrastructure assets from an MNO< Petr Slováček, CEO, CETIN

A comparison of neutral host DAS and multi-tenant small cell vendors and how to design a heterogeneous network attractive to multiple tenants< Representative, Small Cell Forum

Creating a tower value add to remain a core asset< Ronnie Horan, Infrastructure Manager, ESB Telecoms

TowerCo – Public equity, private equity or infrastructure opportunity?< Julian Plumstead, Managing Director, Rothschild

From tactical to strategic sourcing of deployment services< Ahmed Saeb, Principle Category Manager, Networks SCM Technology, Vodafone

Roundtable session 4: 13:40-14:40, 13 April

Country focus Italy< Carlo Ramella, Chairman, EI Towers

Country focus UK< Malcolm Collins, CEO, CTIL

Country Focus Turkey< Cihan Nazmi Biyikli, Executive Business Management and Strategy Consultant and former Chairman, Global Tower

Country Focus: Netherlands< Frank van Kuppeveld, Commercial Director, Novec< Randolf Nijsse, Open Tower Company

Country Focus: Czech Republic< Conor Plant, Managing Consultant, Hardiman Telecommunications

Change management: transitioning people and processes to meet the unique requirements of the commercial tower business< Ravi Kuppan, Founder and Director, Tarantula

Tower transaction deal structures & terms< Daniel Lee, Managing Director, Intrepid Advisory Partners

Minimising costs in the strengthening of towers for additional operator equipment< Host TBC

Country Focus Romania< Temel Oktem, Head of Telecom, Media & Technology, Europe, Middle East and North Africa, IFC

How to monetise a JV infra-sharing firm< Tim Devine, Member of Management Group, PA Consulting

www.towerxchange.com/meetups/meetup-europe | TowerXchange Meetup Europe 2016, 12-13 April, London | 5

Vodafone Procurement Company, VP Global SCM Services

Towercos, Broadcast Towercos and JV InfracosAmerican Tower Germany, CEOArqiva, Product and Technology DirectorArqiva, Managing Director - Telecoms DivisionAxion, PresidentCellnex, CEOCellnex, International Business and Marketing DirectorCellnex, M&A Manager, Business Development DirectionCellnex, Corporate and Public Affairs DirectorCellnex, Deputy ManagerCETIN, CEOCignal, Managing DirectorCignal, ChairmanCTIL, CEOCTIL, Finance DirectorCTIL, General CounselDeutsche Funkturm, Head of Geodata ManagementDigita Oy, CEOEaton Towers, CEOEI Towers, ChairmanEI Towers, Director of Institutional AffairsEmiTel, CEOEmiTel, CFOEmiTel, Vice PresidentESB Telecoms Ltd, Infrastructure ManagerEuroTower, PresidentFPS Towers, COOFPS Towers, CFOFPS Towers, CEO

Latest attendee list for TowerXchange Meetup Europe 2016

Mobile Network OperatorsDeutsche Telekom, Vice PresidentDeutsche Telekom, VP M&ADialog Axiata, DirectorEE, Senior Property ManagerMegaFon, CTIOTalkTalk, Director of Small Cell TechnologyTelefonica, Head of Infrastructure EfficiencyTurkcell, Merger and Acquisition & Investor Relations Member at TuUfone PTML, Senior Manager FinanceVimpelcom, Chief Business Development & Portfolio OfficerVimpelcom, Group Director, Business DevelopmentVodafone Procurement Company, Head of Sales

FPS Towers, Commercial DirectorGrupo TorreSur, Chairman and Chief Executive OfficerHelios Towers Africa, Executive ChairmanHibernian Towers, Company DirectorHibernian Towers, Company DirectorIHS, Associate Communications DirectorIHS, Chief Commercial OfficerIHS Rwanda Ltd, NOC OperaterKonsing Group, CEOKonsing Group, CTOLink Development, CEOLogycom Group, Commercial DirectorMBNL, Managing DirectorMBNL, Finance DirectorNorkring AS, CEONOVEC, Commercial DirectorOpen Tower Company, General CounselOpen Tower Company, Managing PartnerProtelindo, DirectorProtelindo, Corporate FinanceRai Way, CEORai Way,, General DirectorRussian Towers, Co-FounderRussian Towers, PresidentRussian Towers, ChairmanSBA Communications, International Business DevelopmentShared Access, CEOShere Group Ltd, Managing DirectorShere Masten BV, General ManagerTDF, Group Deputy CEO/Group CFOTDF, Strategy & Development DirectorTeracom Boxer Group, VP Network Enterprise

| TowerXchange Meetup Europe, 12-13 April, London | www.towerxchange.com/meetups/meetup-europe6

Latest attendee list for TowerXchange Meetup Europe 2016Teracom Boxer Group, Head of Strategy & Business DevelopmentTowercom Ltd, Chief Executive OfficerTowercom Ltd, General ManagerTowercom Ltd, New Business Development ManagerUkrTower, General ManagerVertical, CEOVertical, Strategy DirectorVICTUS Networks, CEOWireless Infrastructure Group, CEOWireless Infrastructure Group, COOWireless Infrastructure Group, Director

Investors4M Investments, Principal7L Capital Partners, PartnerAlinda Capital Partners, Managing DirectorAlinda Capital Partners, DirectorAMP Capital Investors, Investment DirectorAMP Capital Investor, Investment ManagerAntin Infrastructure Partners, Managing PartnerAlinda Capital Partners, PartnerArcus Infrastructure Partners, Senior Investment DirectorCapital Group, PartnerCiti, Global Communications GroupCommunication Infrastructure Fund, Managing PartnerCredit Suisse, DirectorCredit Suisse, AnalystCrescent Park, AssociateDigital Bridge Holdings, Managing Director, EMEAGoldman Sachs, Executive Director

Goldman Sachs, Senior RepresentativeInternational Finance Corporation (IFC), Chief Investment OfficerInternational Finance Corporation (IFC), Head of Telecom, Media & Technology, EMEAKKR, Director, Energy & InfrastructureMacquarie, Managing Director, TMTMacquarie Infrastructure and Real Assets, Managing DirectorOch-Ziff, Managing DirectorProvidence Equity, Managing DirectorRBC Capital Markets, Managing DirectorRothschild, Managing DirectorTillman Global Holdings, VP Business DevelopmentUFG Asset Management, Managing Director, PartnerWood Creek, CEOWood Creek, Vice PresidentWood Creek, Managing Director

OtherAbloy Oy, Managing DirectorAbloy Oy, Business Development ManagerACSYS, COOACSYS, Business Development Director Global AccountsACSYS, Head of Marketing StrategyAnalysys Mason, PrincipalAnalysys Mason, Senior PartnerBladon Jets, CEOBladon Jets, VP Market DevelopmentCihan Nazmi Biyilki Education & Consultancy, Executive Business ManagementCoslight India Telecom Pvt Ltd, Director

Delmec Engineering Ltd, CTODelmec Engineering Ltd, CEODialight, Director SalesElectronic Control Systems, PresidentEnerSys EMEA, Director - Reserve Power EMEAEnerSys EMEA, VP Sales & Marketing - Reserve Power EMEAEricsson AB, Strategic Product Management Energy & EnclosureGSM Telecom ProductsHardiman Telecommunications, Managing PartnerHardiman Telecommunications, Managing ConsultantHeliocentris, VP Sales and MarketingIntrepid Advisory Partners, Managing DirectorInvendis, CTOInvendis, COOMedipower, CEOMedipower, Vice PresidentNorthStar, President, EMEANorthStar, Director, Solution EngineeringORION, Commercial ManagerPA Consulting, Managing ConsultantPA Consulting, Member of Management GroupRedflow, Sales Manager EuropeSiterra, An Accruent Product, SVP Telecom SalesStandard Advisory London Limited, Global Head Telecoms, Media and Technology, Head, Financial Sponsor CoverageTarantula, Founder & DirectorTarantula, Sales Director, EuropeVinson & Elkins, PartnerWillkie Farr & Gallagher, Partner

www.towerxchange.com/meetups/meetup-europe | TowerXchange Meetup Europe 2016, 12-13 April, London | 7

What is the TowerXchange Investors Club?

Held to complement the baseline market information shared during the TowerXchange Meetup roundtables, the TowerXchange Investor’s Club pre-arranges private one-to-one meetings between towercos and investors. These confidential meetings will give investors the opportunity to open dialogue with CXOs of Europe’s towercos and assess potential new investment opportunities in European telecoms infrastructure.

< How many towers do the company own?< How many have been bought versus built?< What capex on new build or tower strengthening is planned?< What is the current opex per tower?< Who are the major tenants?< What is the tenancy ratio?< Are the revenues from tenancies in local currency or euro / dollars?< What is the current shareholding of the company?< How much investment is the company looking for?< What is their proposed exit strategy?< Who is the management team and what experience do they have?

How can I get involved?

In order to participate in the first Investors Club you must be registered for the TowerXchange Meetup Europe. As a delegate you will be issued with a list of attending towercos and with whom our team will help you secure a number of meetings in our lounge area. If you would like to secure a large number of meetings, we advise that you book exclusive use of one of the on-site private meeting rooms. These are allocated on a strictly first come, first served basis - please contact Annabelle Mayhew [email protected] to enquire about availability.

Which towercos are already scheduled to attend?

We anticipate attendance from over 85% of Europe’s 67 towercos, broadcast companies and JV infracos. Companies already scheduled to attend include:

American Tower Germany, Arqiva, Axion, Cellnex, CETIN, Cignal, CTIL, Deutsche Funkturm, EI Towers, Emitel, ESB Telecoms, EuroTower, FPS Towers, Hibernian Towers, Konsing Group, Link Development, Logycom Group, Open Tower Company, Protelindo, Rai Way, Russian Towers, SBA Communications, Shared Access, Shere Group, TDF, Teracom Boxer Group, Teracom Denmark, Towercom, Vertical, Victus Networks, Wireless Infrastructure Group

What will I learn from the co-located roundtables?

The Investors Club has been designed to complement our TowerXchange Meetup roundtables and published research which provide the critical baseline data and insight into the dynamics of key markets on which to base investment decisions.

14 country or region specific roundtables will address such issues as:< How many towers are there in the market?< What ratio of towers are owned by towercos versus MNOs?< What are current and potential tenancy ratios?< How many independent towercos are there in the market?< Are new market entrants expected?< What network sharing agreements exist between MNOs?< What MNO consolidation is on the horizon?< What is the extent of LTE roll-out and how much growth potential is there?< What is the rate of growth of data usage?< What currency risk is there?

< What availability of local debt providers is there?< How does the initial yield compare to that in other markets?< What cash flow/ EBITDA multiples can be from transactions now versus future exits?

*Country/ regional roundtables: CIS, Czech Republic, France, Germany, Greece, Ireland, Italy, Netherlands, Poland, Russia, Scandinavia, Spain, Turkey and the UK

20+ strategic roundtables will centre on topics including: < Towerco valuations in Europe< Growing and scaling a towerco < Identifying new investment opportunities in European towercos< Tower transaction deal structures and terms< Towerco – Public equity, private equity or infrastructure opportunity?

Plus attend one of our operational roundtables to better understand key dynamics and performance metrics in the telecom tower industry and ensure that your investment is performing optimally.

TowerXchange Investors clubHeld at the TowerXchange Meetup Europe, 12-13 April 2016, Business Design Centre, London, UK

Registering your attendance at the TowerXchange Meetup Europe enables investors to request meetings with you. If you would like to pre-arrange a number of meetings with multiple investors, we advise that you pre-book one of the onsite meeting rooms - please contact Annabelle Mayhew [email protected] to enquire about availability

Are you a towerco interested in participating in the Investors’ Club?

Globally, TowerXchange are tracking 166 towercos and 109 investors with investments active in or a proven appetite for the tower asset class. Our research and series of eight by-invitation-only Meetups have become a valuable source of information for investors looking for new opportunities and in 2016 we are excited to launch the TowerXchange Investors Club. The first edition of the Investors Club will be held on day two of the TowerXchange Meetup Europe in London on 12-13 April.

| TowerXchange Meetup Europe, 12-13 April, London | www.towerxchange.com/meetups/meetup-europe8

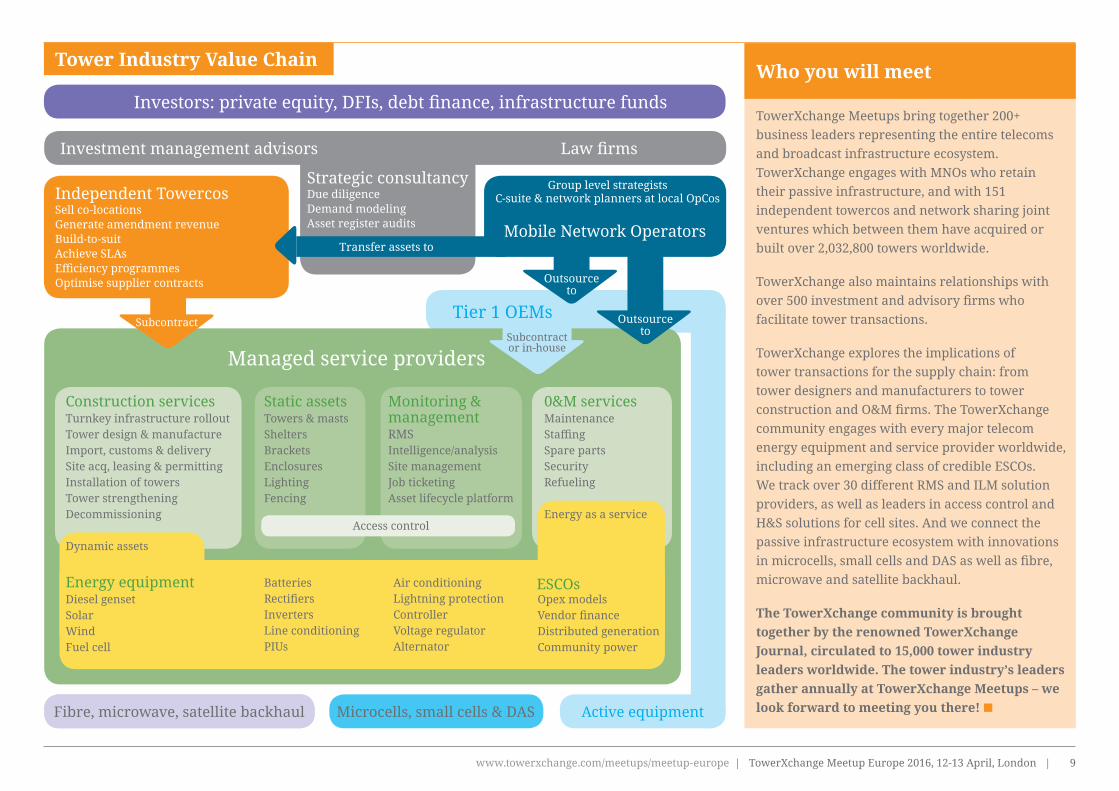

Tower Industry Value Chain

TowerXchange Meetups bring together 200+ business leaders representing the entire telecoms and broadcast infrastructure ecosystem. TowerXchange engages with MNOs who retain their passive infrastructure, and with 151 independent towercos and network sharing joint ventures which between them have acquired or built over 2,032,800 towers worldwide.

TowerXchange also maintains relationships with over 500 investment and advisory firms who facilitate tower transactions.

TowerXchange explores the implications of tower transactions for the supply chain: from tower designers and manufacturers to tower construction and O&M firms. The TowerXchange community engages with every major telecom energy equipment and service provider worldwide, including an emerging class of credible ESCOs. We track over 30 different RMS and ILM solution providers, as well as leaders in access control and H&S solutions for cell sites. And we connect the passive infrastructure ecosystem with innovations in microcells, small cells and DAS as well as fibre, microwave and satellite backhaul.

The TowerXchange community is brought together by the renowned TowerXchange Journal, circulated to 15,000 tower industry leaders worldwide. The tower industry’s leaders gather annually at TowerXchange Meetups – we look forward to meeting you there!

Who you will meet

Fibre, microwave, satellite backhaul Microcells, small cells & DAS Active equipment

Tier 1 OEMs

Mobile Network Operators

Investors: private equity, DFIs, debt finance, infrastructure funds

Law firms

Group level strategistsC-suite & network planners at local OpCos

Outsourceto

Strategic consultancyDue diligenceDemand modelingAsset register audits

Independent TowercosSell co-locationsGenerate amendment revenueBuild-to-suitAchieve SLAsEfficiency programmesOptimise supplier contracts

Transfer assets to

Construction servicesTurnkey infrastructure rollout Tower design & manufactureImport, customs & delivery Site acq, leasing & permitting Installation of towers Tower strengtheningDecommissioning

Dynamic assets

Energy equipmentDiesel gensetSolarWindFuel cell

BatteriesRectifiersInvertersLine conditioningPIUs

Air conditioning Lightning protectionControllerVoltage regulatorAlternator

Managed service providers

ESCOs

Static assetsTowers & mastsSheltersBracketsEnclosuresLightingFencing

0&M servicesMaintenanceStaffingSpare partsSecurityRefueling

Energy as a service

Monitoring & managementRMSIntelligence/analysisSite managementJob ticketingAsset lifecycle platform

Access control

Subcontract

Opex modelsVendor financeDistributed generationCommunity power

Subcontract or in-house

Outsourceto

Investment management advisors

www.towerxchange.com/meetups/meetup-europe | TowerXchange Meetup Europe 2016, 12-13 April, London | 9

80-90% of the leading towercos and MNOs attend

At other telecom events, a maximum of around 10-15% of the CXOs who lead tower strategy for MNOs and towercos are in attendance. At TowerXchange we regularly attract multiple senior representatives from 80-90% of the towercos active in any region, as well as the majority of MNOs. And thanks to our unique structured networking round tables, everyone has access to these decision makers.

Laser beam focus on towers

Another problem with other telecom events is that passive infrastructure is typically hidden away as an under-appreciated small part of a broader show. The huge audience of middle management, device and VAS influencers at other events dilutes access to the few tower decision makers present. In comparison, TowerXchange has been described as a “networking club for tower geeks” – everyone you meet at TowerXchange is focused on towers, and everyone you meet is a decision maker.

Proven over five past events attended by over 1,000 decision makers, TowerXchange Meetups are unique executive retreats for the most influential men and women in telecoms infrastructure. Held annually in Africa, Asia, CALA and Europe, we use small group round table breakouts to give participants unique access to the key stakeholders in the telecom tower industry in each country.

What is a Meetup?

Accelerate vendor selection

If you want to buy telecom tower structures and accessories, energy equipment, energy services, RMS, ILM, access control, H&S equipment, or if you want to contract with tower construction and O&M firms, then

Every TowerXchange expo has sold out

Curated expo of proven suppliers

| TowerXchange Meetup Europe, 12-13 April, London | www.towerxchange.com/meetups/meetup-europe10

the private expo at the TowerXchange Meetup provides a ‘who’s who’ of proven passive infrastructure equipment and service providers.

Identify opportunities for your business today…

TowerXchange introduces each Meetup with our proprietary research, defining the size of the tower market in each country, identifying who owns the towers today and predicting the future tower transaction pipeline. We also track network

consolidations, extensions and densification, and examine ownership of energy assets and the prospects for energy service providers.

…And opportunities for your business tomorrow

We use MNO and towerco CXO panel sessions to understand the future of the tower industry. What has been the progress of tower transactions and of portfolio integration? What future acquisitions are planned? How is capex being deployed? What are the

priorities of efficiency programmes? Are opex-sharing models being explored? Are microcells, small cells and DAS being rolled out?

Unique structured networking

TowerXchange’s renowned round table breakouts are led by an expert moderator, but everyone’s opinions and questions are welcomed. Each round table focuses on a specific country, financial or operational issue. You can attend three or four round tables at each Meetup. Register now to secure your choice of round table and tailor your agenda to meet your networking objectives!

Unique round table breakouts

Suresh Sidhu’s insightful keynote address

www.towerxchange.com/meetups/meetup-europe | TowerXchange Meetup Europe 2016, 12-13 April, London | 11

(Chairman) Daniel Lee Managing DirectorIntrepid Advisory Partners

Akhil GuptaChairmanBharti Infratel

Michel FaivreDirecteur Programme Partaged’Infrastructure AMEAOrange

Terry RhodesActing CEOEaton Towers

Marc GanziPresident, Digital Bridge &Mexico Tower Partners

Arun KapurExecutive ChairmanIrrawaddy Green Towers

James Maclaurinformerly CEOedotco

Areef KassamDirector of InfrastructureGSMA Mobile for Development

Ayman Al AdlDirector - TMTStandard Chartered Bank

Dagan KasavanaCEOPhoenix Tower International

Malcolm CollinsChief ExecutiveCTIL

Chuck GreenExecutive ChairmanHelios Towers Africa

Suresh SidhuCEOedotco

Hal HessEVP, International Operations andPresident, EMEA and Latin AmericaAmerican Tower

Nobel TanihahaPresident DirectorPT SOLUSI TUNAS PRATAMA (STP)

Umang DasChief MentorViom Networks

Maria ScottiCEOTorrecom

David MeganckFounder and COOAcsys

Gary StauntonCEOLikusasa Group

Tilak Raj DuaDirector GeneralTAIPA

Nina TriantisManaging Director, Global, Head of Telecoms & MediaStandard Bank

Peter Owen EdmundsCo-founder and ChairmanRussian Towers

Kurt BagwellPresident InternationalSBA Communications

Jim EisensteinChairman & CEOGrupo TorreSur

Riana DonaldsonManager: International Network Operations SupportVodacom

Bimal DayalCOOIndus Towers

Inder BajajCEOHTN Towers

Tunde TitilayoVice ChairmanSWAP International

Thorsten SchaeferCEOazeti Networks

Jeffrey EldredgePartnerVinson & Elkins

Enda HardimanManaging PartnerHardiman Telecommunications Ltd.

Adeel BajwaSenior GM of Legal Affairs and ContractsWarid Telecom

Scott CoatesCEOWireless Infrastructure Group

With special thanks to the TowerXchange “Inner Circle”About TowerXchange

TowerXchange is your independent community for operators, towercos, investors and suppliers interested in EMEA, CALA and Asian towers. We’re a community of practitioners formed to promote and accelerate infrastructure sharing. TowerXchange don’t build, operate or invest in towers; we’re a neutral community host and commentator on telecoms infrastructure.

The TowerXchange Journal is free to qualifying recipients. We also provide webinars and regular meetups. TowerXchange monetizes this community through hosting annual Meetups and the sale of advertising, without compromising editorial integrity.

TowerXchange was founded by Kieron Osmotherly, a TMT community host and events organizer with 16 years’ experience, and is governed with the support and advice of the TowerXchange “Inner Circle” – an informal network of advisors

Our informal network of advisers:

© 2015 Site Seven Media Ltd. All rights reserved. Neither the whole nor any substantial part of this publication may be re-produced, stored in a retrieval system, or transmitted by any means without the prior permission of Site Seven Media Ltd. Short extracts may be quoted if TowerXchange is cited as the source. TowerXchange is a trading name of Site Seven Media Ltd, registered in the UK. Company number 8293930.

| TowerXchange Meetup Europe, 12-13 April, London | www.towerxchange.com/meetups/meetup-europe12

TowerXchange’s analysis of the independent tower market in Europe

The past couple of months have seen big news in the European market indicating a major shift is underway in attitudes toward tower ownership. Of Europe’s 600,000 towers (including Russia and the CIS), currently 29% sit in the hands of independent towercos, operator-captive towercos and JV infracos but with the recent pipeline of activity, TowerXchange expect this to increase to

35% in 2016 with the figure having the potential to exceed 40% in the next two years if momentum continues apace. If such forecasts came to pass, towercos would have the same level of penetration in Europe as they currently do in Sub-Saharan Africa, where four towercos rapidly rolled up the most investible assets ostensibly over a five year period.

The most recent European news come from Spanish giant, Telefónica. After months of speculation surrounding a potential divestment of towers, January saw the carve out of their 11,500 Spanish sites into a newly formed infrastructure business – Wireless Towers. Whilst still unclear whether this will lead to an IPO or sale (although a two stage approach involving both seems likely) – the move will either result in the introduction of significant sized operator-owned competitor, or will provide a highly attractive acquisition for either a European or an international towerco to achieve scale rapidly. Speculation is already mounting that Telefónica’s Wireless Towers footprint could be extended to absorb their German and remaining CALA towers, although the MNO has not confirmed this.

In Russia, the sale of Vimpelcom’s 10,400 towers is well underway, with three shortlisted bidders – Russian Towers, Vertical and the Russian Direct Investment Fund in the running for the portfolio. The deal is expected to close in Q1-2 2016, marking Russia’s first major tower transaction. Following the completion of the sale it is widely expected that Vimpelcom will then turn their attention to potential divestitures across their CIS markets, in a bid to further reduce their current debt.

Keeping our focus on the east, Russia’s MTS and Megafon are also rumoured to be re-evaluating their tower strategies – with Megafon looking into a potential carve out with a view to IPO. In Turkey it has recently been reported that Turkcell have re-opened discussions with bankers regarding a

Top ten independent towercos in Europe by telecom site count (excludes infracos)

Deutsch

e

Funkturm Celln

exTDF

CETINIn

wit

Arqiv

a

Global

Tower FPS

TowersEI

Towers Rai

Way

Wire

less

Infr

astru

cture

Group

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0

27,000

15,127

6,966 5,300

11,519 10,5507,870

11,500

Source: TowerXchange

2,618 2,300 2,300

www.towerxchange.com/meetups/meetup-europe | TowerXchange Meetup Europe 2016, 12-13 April, London | 13

Russia85,000

Germany63,754

UK53,000

Italy47,517

Spain45,052

potential tower sale, and in Poland, Orange are also rumoured to be looking into a tower sale.

The other major piece of news is the imminent closure of the sale of a 45% stake in Telecom Italia’s infrastructure unit – Inwit. Following a successful IPO of 40% of the business in 2015, the sale of the 45% stake is expected to close mid-March. Three offers have been received – from American Tower (AMT), EI Towers and Cellnex in conjunction with infrastructure fund F2i (the latter consortium reportedly being the front runner). EI Towers favors acquiring a smaller stake – it remains to be seen whether the AMT or Cellnex bid would trigger the acquisition of the whole company.

TowerXchange are currently tracking 67 towercos, broadcast companies and JV infracos with tower portfolios in Europe. With the exception of Cellnex (active in Spain and Italy), Wireless Infrastructure Group (with assets in the UK, Ireland and the Netherlands), Shere Group (with towers in the UK and Netherlands) and Britannia/Hibernian (with assets in both the UK and Ireland), all other companies have a presence in just one country.

Major tower transactions on the cards represent an opportunity for Europe’s towercos to expand into new geographies and also represent an opportunity for major international players to gain a footprint in Europe: #3 and #4 US towercos SBA Communications and Digital Bridge both have an appetite for European towers, for example. What’s more, such transactions are leading to the creation of new domestic towercos. In such a fragmented

market, with independent tower ownership in the hands of a number of mid-sized companies and with investors having a growing appetite to invest in European tower infrastructure, it often seems that there is more capital seeking tower opportunities than there are opportunities. A domestic player with local expertise together with the backing of a financial investor and the presence of a strong management team could be well placed to make a significant play in upcoming transactions. TowerXchange are tracking a lot of towercos, infrastructure funds and PE firms

with an appetite for smaller portfolios, from BTS startups to 100-2,000 towers. But the question remains: does anyone have the appetite and digestive capacity to compete with Cellnex for Europe’s largest sale and leasebacks?

Moving away from macro-structures, an increasing number of European towercos are tapping opportunities in the small cell and DAS markets. With European MNOs accustomed to infrastructure sharing, and urban infill to meet growing data demand sitting as a top priority,

Estimated tower and rooftop counts for selected markets in Europe

Source: TowerXchange

France45,000

Czech Republic12,336

Nether-lands:15,204

Ireland4,000

| TowerXchange Meetup Europe, 12-13 April, London | www.towerxchange.com/meetups/meetup-europe14

European tower deals since 2008

Year Country Seller Buyer Tower countCost per tower € Deal structureDeal value €

Source: TowerXchange

there exists significant potential for a third party infrastructure provider to deliver more cost effective, neutral host heterogeneous networks. The uptake of venue-DAS is growing significantly and a number of city-wide outdoor small cell projects are being rolled out, with observers believing that 2016/2017 will be the time when small cells and DAS start to achieve scale. Cellnex and Wireless Infrastructure Group offer exclusive

interviews on this topic in our small cells special feature later in this edition.

Further focus for Europe’s towercos resides in decommissioning as the impact of MNO consolidation (such as that of 3’s acquisition of O2 in Ireland and the proposed merger of 3 and O2 in the UK) starts to filter through to their infrastructure

At such a pivotal time for the European tower industry, TowerXchange is excited to be launching the first TowerXchange Meetup Europe in London, taking place on 12-13 April.

For further detail on the European tower market, checkout TowerXchange’s Who’s Who in European towers.

126,866

93,941

446,226

90,016

100,400

193,501

287,356

250,000

90,000

114,973

Portfolio acquisition

Asset Transfer

Portfolio acquisition

SLB with 10% equity

Company acquisition

SLB

SLB with 15% equity

SLB

SLB

SLB

SLB

SLB

SLB

17,000,000

693,000,000

94,600,000

385,000,000

185,000,000

393,000,000

75,000,000

115,000,000

45,000,000

2,002,600,000

113

7700

134

7377

212

4277

2166

2031

261

460

500

500

101

25,832

2015

2015

2015

2015

2015

2014

2012

2012

2012

2012

2012

2010

2008

Cignal

Deutsche Telecom/ Omega Towers

EI Towers

Cellnex

Cellnex

Cellnex

FPS Towers

American Tower

Protelindo

Shere Group

Cellnex

Open Tower Company

Open Tower Company

Totals / average

Coillte

Telefonica

Tecnorad

Wind (Vimpelcom)

TowerCo

Telefonica/Yoigo

Bougyes Telecom

KPN

KPN

KPN

Telefonica

KPN

KPN

Ireland

Germany

Italy

Italy

Italy

Spain

France

Germany

Netherlands

Netherlands

Spain

Netherlands

Netherlands

www.towerxchange.com/meetups/meetup-europe | TowerXchange Meetup Europe 2016, 12-13 April, London | 15

European tower activity - the headlines

Azerbaijan: Infraco Azerconnect active in the country.

CIS: Logycom forms first independent towerco in Kazakhstan, with an order to build just under 100 towers. Meanwhile, Vimpelcom’s towers could come to market across several CIS states.

Czech Republic: CETIN, infrastructure business carved out of O2 has 5,300 towers and 750 micro sites. Also in infrasharing venture with T-Mobile.

Denmark: Infrasharing mandated by the state - TT-Network formed by Telia and Telenor. MNO divestments expected in 2-4 years.

Finland: Digita sold to First State Investments in 2012.

France: Towerco FPS active after acquiring towers from Bougyes Telecom and 20,000 rooftop sites from Loxel. TDF lead the market, ITAS TIM and Towercast also active. Free Mobile’s entry disrupting the market, SFR-Numericable forced into merger; Bouygues Telecom looking to exit? Could more towers become available for sale and leaseback?

Germany: Towercos Deutsche Funkturm and American Tower active in the market, ATC’s towers bought from KPN. Potential for carve out and sale/IPO of Telefonica’s 10-12,000 towers.

Greece: Infraco VICTUS Networks run by Vodafone Greece and Wind Hellas. Initial rumors of potential sale and leasebacks emerging.

Hungary: Antenna Hungaria acquired by the state from TDF in 2014.

Ireland: Towercom, ESB Telecoms, WIG, Hibernian, Cellcom and Highpoint active. Together with three state-owned entities, they own 40% of Ireland’s 4,000 towers. 3’s acquisition of O2 disrupted network sharing agreements and is leading to consolidation. Coillte sold 298 sites including 113 towers to InfraVia Capital Partners creating new towerco Cignal.

Italy: 45% stake in Inwit being sold following an IPO of 40% of the business. Cellnex/F2i, American Tower and EI Towers in the running. EI Towers acquisition of fellow broadcast towerco Rai Way initially halted. EI Towers continue to roll-up smaller towercos. Cellnex closed landmark sale and leaseback with Wind in 2015.

Latvia: Bite Group brought towers to market in 2013 but no agreement reached.

Netherlands: Protelindo, Shere Group and Open Tower Company acquired a total of 1,322 towers from KPN. Rumours that T-Mobile may be looking to sell its business.

Poland: Emitel (towerco) and NetWorkS! (infraco) active in the market. Rumours surrounding a potential tower sale by Orange.

Portugal: Portugal Telecom sold to Altice – tower sale rumour has gone quiet.

Romania: Orange and Vodafone sharing networks since 2013.

Russia: 10,400 Vimpelcom towers up for sale and rumoured divestments from MTS and Megafon. Active towercos include Russian Towers, Vertical, Link Development and Service Telecom.

Serbia: Managed service provider Konsing Group owns a portfolio of 47 sites.

Spain: Telefonica carved out 11,500 towers into new infrastructure business, Wireless Towers, with a view to sell or IPO. Towerco Cellnex active after acquiring towers from Telefonica/Yoigo. Axion towers rumoured to be on the market.

Sweden: Several infracos including Net4Mobility, 3GiS and SUNAB

Turkey: Turkcell’s Global Tower manages over 16,000 sites including 7,870 macro towers. Turkcell in talks with bankers regarding a potential tower sale.

UK: Towercos active in the market include Arqiva, WIG and Shere Group, MBNL and CTIL sizable infracos. Sale of O2 to Hutchison still under review; implications for joint venture infracos unclear.

Ukraine: Towerco UKRTower active in the market.

| TowerXchange Meetup Europe, 12-13 April, London | www.towerxchange.com/meetups/meetup-europe16

123456

European heatmap

TowerXchange research has not revealed any infracos or

towercos to date

Towercos or infracos active in the market. No recent

transactions have taken place and none rumoured to take

place soon

Towercos or infracos active in the market. No current

transactions taking place but an attempted tower sale has

taken place in the last 3 years or there are unconfirmed

rumours of a deal in this market.

Towercos or infracos active in the market. Rumours of deals

confirmed in the market.

Towercos or infracos active in the market. Deals of significant

size have taken place in the last 5 years.

Towercos or infracos active in the market. Deals have taken

place in the last year and more imminent deals rumoured

Legend

Note: For the purposes of our European coverage, ‘Towerco’ describes an independent company which owns and operates passive infrastructure for commercial profit. ‘Infraco’ incorporates MNO joint venture organisations and carve outs which serve more than one entity or market their towers commercially

Source: TowerXchange

www.towerxchange.com/meetups/meetup-europe | TowerXchange Meetup Europe 2016, 12-13 April, London | 17

Who owns Europe’stelecom towers?Smart capital seeks investible European tower builders – and tower consolidators

A breakdown of the European telecom tower industry by tower ownership TowerXchange have been studying the emerging European tower industry for almost a year now, and so far we have identified 41 telecom and broadcast towercos in Europe, including ten joint venture infracos, three operator-led towercos and 28 independent towercos. In total these 41 companies own or operate 166,494 towers; 29% of Europe’s ~600,000 towers. The remaining 433,500+ assets remain operator-captive. We breakdown the ownership of Europe’s towers in figure one. From this simple analysis, you can see that the European tower market is far from fully penetrated. Why? Two of the three primary motivations for tower divestitures in other markets are less prevalent in Europe: many of Europe’s MNOs don’t have the same need to raise capital as MNOs do in emerging markets, nor are they motivated to outsource the expansion of their tower networks to specialist third parties during periods of intense growth. However, the third motivation, the stabilisation of opex by outsourcing or divesting non-core assets and activities remains a motivation. Meanwhile the European tower market introduces a new motivation; the consolidation and decommissioning of overlapping tower networks; creating value by reducing operating costs (primarily land lease costs) and creating value by adding more tenants to remaining towers. This new decommissioning function means business models and balance

Read this article to learn:< How many towers are there in Europe and who owns them?

< Contrasting infrasharing JVs, operator-led and independent towercos

< The drivers for European MNOs to divest towers

< The need for more European tower builders (and tower consolidators)

TowerXchange have spoken to dozens of private equity, institutional and strategic investors keen to put capital to work within the emerging European telecom tower market. So what are your investment options in Europe? Investors in listed entities Cellnex and Inwit have to date enjoyed buoyant valuations – but that opens only passive investments restricted to date to Southern Europe. TowerXchange have identified 28 independent towercos in Europe, and many are highly investible, but most are well capitalised and few are seeking new equity partners. How about Europe’s ten joint venture infrastructure sharing companies? Not easy: few if any currently solicit third party investment. The starting point for many PE firms’ investment in towers are build to suit towercos who permit, build, own and operate towers in response to MNO search rings – but TowerXchange have found few such firms in Europe. A gap in the market perhaps…

Keywords: 3GIS, Alticom, American Tower, Antenna Hungaria, Arqiva, Axion, Azerconnect, Bankability, Build-to-Suit, CTIL, Cellnex, Colite, Decommissioning, Deutsche Funkturm, Digita, EI Networks, ESB Telecos, Emitel, Estonia, Europe, FPS Towers, Falck, Global Tower, HIGHPOINT (obelisk), Hi3G, Hibernian/Britannia Towers, ITAS TIM, Infrastructure Sharing, Inwit, JV Infraco, Link Development, MBNL, Market Overview, Mosaic, NetWorkS!, Open Tower Company, Operator-Led JV, Protelindo, Research, Russian Towers, Sale & Leaseback, Sheere Group, Sunab, TDF, TT-Network, TowerXchange Research, Towercast, Towercom, Towercos, VICTUS Networks, Who’s Who, Wireless Infrastructure Group, České Radiokomunikace

By Kieron Osmotherly, CEO, TowerXchange

| TowerXchange Meetup Europe, 12-13 April, London | www.towerxchange.com/meetups/meetup-europe18

Figure two: Who’s who in European JV infracos and operator-led towercos

MNO captive (433,506)JV infracos (58,500)Operator-led towercos (46,389)Independent towercos (61,605)

Figure one: A breakdown of the ownership of Europe’s ~600,000 telecom cell sites

Defining ‘towercos’ and ‘infracos’ We define a towerco as a business whose raison d’etre is to construct, consolidate AND co-locate telecom towers – with or without a hybrid business model also including broadcast towers, IoT, heterogeneous and public safety network hosting. Note that there is a sub-category within this segment: independent towercos that are majority owned by parties other than MNOs, and operator captive towercos where most or all of the equity is retained by an MNO. There are three operator captive towercos in Europe: Deutsche Funkturm, Global Tower in Turkey and the Ukraine, and Inwit (which remains 60% owned by Telecom Italia).

Europe also has a number of joint venture infracos, typically carved out of two or more MNOs, whose raison d’etre is to manage, supplement and consolidate those assets, but who don’t market the sites for co-location as proactively as an independent towerco. Typically the tower assets remain on the partner MNOs’ balance sheets, but there are instances of this business model where the passive infrastructure has been transferred to the infraco (e.g. CTIL in the UK). A simple who’s who of European towercos is presented in figures two and three TowerXchange include in our analysis of “JV infracos” only infrastructure sharing deals which

were consolidated into joint venture newcos. Note that there have been several other infrastructure sharing deals in Europe where the assets apparently remained under the ownership and management of the MNOs concerned:

< Austria (T-Mobile+ Hutchison 3G)< Belgium (Orange+KPN)< Czech Republic (Telefonica+T-Mobile)< Finland (TeliaSonera+DNA)< France (SFR+Bouygues)< Iceland (Vodafone+Nova)< The Netherlands (Tele2+T-Mobile)< Romania (Orange+Vodafone)< Russia (Vimpelcom+MTS)

GermanyUKUKSpainPolandTurkeyDenmarkUkraineSwedenSwedeAzerbaijanIrelandSwedenRomaniaSwedenGreece

Deutsche FunkturmCTILMBNLWireless Towers (Telxius)NetworkS!Global TowersTT NetworkUKR TowerHi3G3GISAzerconnectMosaicNet4MobilityOvidiuSunabVICTUS

27,00018,00018,00011,50010,0007,8702,500370125 Undisclosed Undisclosed UndisclosedUndisclosedUndisclosedUndisclosedUndisclosed

Operator-led towercoJV InfracoJV InfracoOperator-led towercoJV InfracoOperator-led towercoJV InfracoOperator-led towercoJV InfracoJV InfracoJV InfracoJV InfracoJV InfracoJV InfracoJV InfracoJV Infraco

Countries Est site count* Business model

71%

10%

9% 10%

*We understand Deutsche Funkturm has around 8,500 GBTs, with the rest rooftops

www.towerxchange.com/meetups/meetup-europe | TowerXchange Meetup Europe 2016, 12-13 April, London | 19

Countries Est site count* Business model

Figure three: Who’s who in European independent towercos sheets in the European tower market will differ substantially from the ‘old growth’ tower industry in markets like the U.S. and India. Time for European MNOs to cash out Another new motivation for European MNOs to divest towers is the relative favorable relative multiple arbitrage between MNO and towerco valuations. This has never been more pronounced than when called to attention by the valuations secured by the recent successful IPOs of Cellnex and Inwit. Whether MNO’s towers sit on their balance sheet, on the balance sheet of a captive towerco or a joint venture infraco, the potential valuation of European towers at IPO, or indeed to a strategic buyer, may be at an all time high. Is it time for European MNOs to cash in their chips whilst they’re ahead in the game of passive infrastructure? Indeed, is this a game European MNOs want to be playing any more when they could take their metaphorical winnings to the spectrum auction or customer experience improvement tables? At TowerXchange, we tend to think that four tower transactions of scale (2,000+ towers) being sold and leased back is indicative that a tower market has achieved ‘launch velocity’. That benchmark was achieved with Cellnex’s acquisition of 7,377 towers from Wind Italy, following Cellnex’s previous acquisitions from Telefónica and Yoigo in Spain in 2014, FPS’s acquisition of 2,166 towers from Bougyes Telecom in France and American Tower’s acquisition of a portfolio of 2,031 towers in Germany – the latter two deals being announced in 2012.

Deutsche FunkturmCellnexInwitArqivaTDFCETIN EI TowersRai WayFPS TowerAmerican Tower GermanyWireless Infrastructure GroupRussian TowersVerticalShere GroupCeske RadiokomunikaceOpen Tower CompanyAxionITAS TIMTowercomESB TelecomsEmitelLink DevelopmentProtelindo2rnCignalLogycomBritannia / HibernianHighpoint (Obelisk)Konsing GroupÖsterreichischer RundfunkCellcomAlticomService TelecomEuroTowerAntenna HungariaDigeaDigitaETBLeviraMedia BroadcastNorkring Norkring BelgieOIVRadiocomRTPShared AccessSwisscom Teracom Boxer GroupTowercast

GermanySpain, ItalyItalyUKFranceCzech RepublicItalyItalyFranceGermanyUK, Ireland, NetherlandsRussiaRussiaUk, NetherlandsCzech RepublicNetherlandsSpainFranceIrelandIrelandPolandRussiaNetherlandsIrelandIrelandKazakhstanUK, IrelandIrelandSerbiaAustriaIrelandNetherlandsRussia-HungariaGreeceFinlandSerbiaEstoniaGermanyNorwayBelgiumCroatiaRomaniaPortugalUKSwitzerlandSweden, DenmarkFrance

27,00015,37711,51910,5006,9665,3002,3002,3002,0512,031 2,0001,7001,60096080068458042040037737730026015011310070504740403310UndisclosedUndisclosedUndisclosedUndisclosedUndisclosedUndisclosedUndisclosedUndisclosedUndisclosedUndisclosedUndisclosedUndisclosedUndisclosedUndisclosedUndisclosed

Operator-led towercoIndependent towercoIndependent towercoBroadcast towercoBroadcast towercoIndependent towercoBroadcast towercoBroadcast towercoIndependent towercoIndependent towercoIndependent towercoIndependent towercoIndependent towerco Independent towercoBroadcast towercoIndependent towercoBroadcast towercoIndependent towercoIndependent towercoIndependent towercoBroadcast towercoIndependent towercoIndependent towercoBroadcast towercoIndependent towercoIndependent towercoIndependent towercoIndependent towercoIndependent towercoBroadcast towercoIndependent towercoBroadcast towercoIndependent towercoIndependent towercoBroadcast towercoBroadcast towercoBroadcast towerco Broadcast towercoBroadcast towercoBroadcast towercoBroadcast towercoBroadcast towercoBroadcast towercoBroadcast towercoBroadcast towercoIndependent towercoBroadcast towerco Broadcast towerco Broadcast towerco

| TowerXchange Meetup Europe, 12-13 April, London | www.towerxchange.com/meetups/meetup-europe20

With a further 1,822 towers acquired in five smaller sale and leasebacks in the Netherlands (KPN to Protelindo, Shere Group and Open Tower Company) and Spain (the first phase of Telefónica to Cellnex), the blue touch-paper has been lit for tower sale and leasebacks in Europe. The inauguration of Cellnex, already highly acquisitive when fully owned by Abertis, has created another prospective counterpart for tower divestitures in a market that had previously been stymied by U.S. towercos’ reluctance to close the gap to European MNOs’ valuation of their towers. Equipped with an acquisition warchest from a successful IPO, Cellnex’s investors have bought into a consolidation narrative that will extend the towerco’s acquisition spree. So while U.S. strategic investors may have preferred to deploy their capital elsewhere whilst Europe stood still, the pipeline of tower transactions is flowing now – whether American Tower, SBA Communications or even Crown Castle is interested to tap the European tower transaction pipeline remains to be seen. Tower builders and tower consolidators needed The European tower market, like any tower market, is not just about large scale sale and leasebacks. There are some great tower builders in Europe. Some are pure builders, some blend small to medium sized acquisitions into the business model. There are some very solid, investible platforms in Europe – in fact, most are very happy with their capital structure, thank you very much, and looking

Five critical considerations to maximise towerco valuations on exit – by Nicholas Van Slyck, a skilled entrepreneur whose Costa Rican towerco was sold to SBA Communications in 2010. Nicholas is now GM – Costa Rica at SBA

Paper Assets Permits Rates Growth

PAPER - Get the paperwork done right: it’s really important to have strong ground leases and good tenant agreements in place, especially if you plan on eventually selling the business.

ASSETS - Don’t cut corners on the construction: I have seen quite a few entrepreneurs opting for cheap solutions when it came to building sites. But in the long run, this strategy won’t pay off. Building robust, multi-carrier towers with plenty of capacity will position your business on the right track to be acquired at a fair price. If a buyer has to reinforce your towers, this will have a negative impact on your ROI.

PERMITS - Ensure your permits are in place: some towercos start building sites without the necessary permits in an attempt to speed up the process. But permits create immense value for

your portfolio and, especially in a place like Costa Rica where sometimes as many as eight or nine permits are needed, you’d better get things right from day one.

RATES - Negotiate the right rental rates with tenants: I have seen some small towercos agreeing very low lease rates in an effort to gain business but again, this strategy won’t pay off and will affect the payout on exit. Aim for good, fair market rates with all your tenants.

GROWTH - Lease up: a good tower professional needs to keep an eye towards acquiring a second, a third and even a fourth tenant if possible. That’s where the real value is. If your plan is to build single tenant towers in rural areas with limited lease up potential, you might want to re-think your business model

www.towerxchange.com/meetups/meetup-europe | TowerXchange Meetup Europe 2016, 12-13 April, London | 21

portfolio is assembled purely by building to suit, or as a product of a decent scale decommissioning opportunity where the towerco retains the consolidated towers, European towers are becoming a safer bet. European MNOs: it’s time to cash in your tower chips. European tower builders: it’s time to put your chips on the table, the towerco business is now be a safe bet in Europe

and small cells as infill and capacity as subscribers demand more and more data, and sooner or later migrate to 4G.

There is no shortage of tower building and tower decommissioning wisdom in Europe – some of the world’s most renowned turnkey infrastructure firms come out of Europe. But there hasn’t been the same appetite to move up the value chain from building towers for MNOs to building towers, retaining those assets and leasing them to MNOs. One reason for this lack of appetite is a lack of realised towerco exits; all I can say in response to that is that any towerco will be not be short of prospective counterparts to realise their exit strategy provided they build a portfolio of several hundred to a few thousand robust tower assets in unique locations, with structural capacity for multiple tenants, and demonstrate the market potential to lease up those towers. Whether the

“ “Whether the portfolio is assembled purely by building to suit, or as a product of a decent scale decommissioning opportunity where the towerco retains the consolidated towers, European towers are becoming a safer bet

We will be hosting our inaugural TowerXchange Meetup Europe on 12-13 April 2016 in London. If you are a stakeholder in European towers, or if you’d like to be a stakeholder in European towers, and have an interest in joining our speaker panel, then email me at [email protected].

for more assets of a similar ilk to buy. Indeed, TowerXchange has spoken to dozens of private equity firms, infrastructure funds and strategic investors with an appetite to invest in or acquire small to medium sized European towercos. There is more capital with appetite for European tower builders (and tower consolidators) than there are investable platforms. Consider this; there are maybe 10-12 bona fide build to suit (BTS) towercos serving a European tower market of ~600,000 towers. There are a similar number serving a Brazilian tower market which is one twelfth that size. Wireless Estimator tracks 100 U.S. BTS towercos serving a market a quarter of the size of Europe. Why so few towercos in Europe? One explanation I’ve heard is that Europe’s tower market is saturated – it’s a consolidation game not a growth game. Well, it isn’t saturated and it isn’t just a consolidation game. In general, Europe’s tower networks are more mature than some other continents; for example there are an average of 1,673 SIMs per tower in Europe compared to 2,597 in MENA, 4,670 in CALA and 4,717 in SSA. However, Europe has considerably less tenants per tower than the U.S. and Indian markets where tenancy ratios are close to two, and where there are 2,352 and 2,091 SIMs per tower respectively, albeit obviously around half that number per BTS. There is some consolidation to be undertaken in Europe – decommissioning represents a great opportunity for tower entrepreneurs in itself – but in every market there is a need for new towers, rooftops, microcells, DAS

| TowerXchange Meetup Europe, 12-13 April, London | www.towerxchange.com/meetups/meetup-europe22

TowerXchange’s who’s who in European towersTowerXchange presents an A-Z of 122 MNOs, towercos, investors and advisors who could be key stakeholders in the emerging European tower industry

2rn: Irish broadcast towerco with around 150 towers, some of which are used by telecom clients. 3GIS: Operates a shared network between Telenor and 3 (Hi3G) in Sweden. Abertis Telecom: See Cellnex. Alinda Capital Partners: Acquired 100% equity in Polish broadcast towerco Emitel in 2013. Emitel has diversified into telecom co-location. Alinda are believed to have appetite for more investments in the tower industry. Altice: French billionaire Patrick Drahl’s Altice acquired French #2 MNO Numericable-SFR from Vivendi in 2014 and has been trying to merge this entity with third ranked MNO Bouygues Telecom, a transaction which may shake loose more of one or both entity’s towers. Altice also acquired Portugal Telecom in June 2015, and has been similarly acquisitive in the Americas. Altice is relatively highly leveraged and has advocated efficiencies that have not to date explicitly extended to divesting towers, but it seems plausible that either monetising network assets or divesting towers to reduce competitive concerns might be a plausible extension of their current strategies. Alticom: Dutch towerco with 24 towers and 9 masts primarily at high altitudes (by Dutch standards!) primarily used by broadcast tenants but also by telecom operators for microwave links. Services include provision of power and cooling.

Read this article to learn:< Who’s who of 41 towercos and joint venture infrastructure sharing firms in Europe

< Maps showing the footprints of Europe’s leading MNOs and commentaries on their history and

appetite to share towers

< An introduction to some of the most credible current and prospective investors into European towers

< An introduction to the TMT advisory firms with experience of tower transactions

The European telecom tower market may be opening up to the independent towerco business model. Held in stasis for many years whilst Europe’s MNOs didn’t need cash and towercos weren’t prepared to meet their valuations, successful new towerco ventures like Cellnex, Inwit and CETIN are galvanising the tower transaction pipeline and rekindling interest in Europe’s existing telecom and broadcast towercos.

Keywords: TowerXchange Research, Who’s Who, MNOs, Towercos, Investors, Europe, 2rn, 3GIS, Abertis Telecom, Alinda Capital Partners, Altice, Alticom, America Movil, American Tower, Analysys Mason, Antenna Hungaria, Antin, Arcus, Arqiva, Ashmore, Axion Azerconnect, Berkshire Partners, Blackstone, Bouygues Telecom, Britannia Towers, Brookfield, BuyIn, Capital Group, CEE Equity Partners, Cellnex, České Radiokomunikace, Česká Telekomunikační Infrastruktura, CETIN, Cignal, Citi, Communication Infrastructure Partners, Crown Castle, CTIL, Deutsche Funkturm, Digea, Digita, Digital Bridge, ECS, EE, EI Towers, Emitel, ESB Telecoms, ESN Group, ETB, European Wireless Infrastructure Association, EWIA, EuroTower, EY, F2i, FMO, FPS Towers, Galata, Global Tower, Goldman Sachs, Hardiman Telecommunications, Hibernian Towers, Highpoint, Hutchison, InfraVia, ING, IFC, Intrepid Advisory Partners, Inwit, ITAS TIM, J.P. Morgan, KPN, KPR Consult, Levira, Link Development, Logycom Group, Macquarie, MBNL, Media Broadcast, MegaFon, MOSAIC, Mott MacDonald, MTS, Net4Mobility, NetShare, NetWorkS!, Norkring, Obelisk, OIV, Open Tower Company, Orange, ORS, Portugal Telecom, PPF, Protelindo, Providence Equity, Quippo, Radicom, Rai Way, Rothschild, RTRS, Russian Towers, SBA Communications, Service Telecom, Shere Group, SUNAB, Swisscom, T-Mobile, TAP Advisors, TDF, Tele2, Tele2 Russia, Telefónica, Telemont, Telenor, Telekom Austria, TeliaSonera, Teracom, Three, Threefold, TOWERCAST, Towercom, TT-Network, Turkcell, UFG Asset Management, UkrTower, Vertical, VICTUS Networks, Vimpelcom, Vodafone, Vodafone Procurement, Wind, Wireless Infrastructure Group

www.towerxchange.com/meetups/meetup-europe | TowerXchange Meetup Europe 2016, 12-13 April, London | 23

America Movil: See Telekom Austria. American Tower: The world’s largest independent commercial towerco, American Tower need no introduction within this publication. Present in Europe to date only in Germany, where the company owns and operates a network of 2,031 sites, the majority acquired in 2012 for €393mn from KPN. “We liked the opportunity in Germany because of the size and economic stability of the market, the absence of other independent towercos, and an attractive valuation that allowed the portfolio to yield over 8% on day one,” said Hal Hess, President of EMEA and Latin America for American Tower in a August 2015 TowerXchange interview. “The acquisition made economic sense for us despite the

acquisition of E-Plus by Telefónica – we knew this was a likely scenario, so when we structured the transaction we made adjustments to be able to meet our objectives. Our German business continues to perform above the expectations we set out in our acquisition business case.” “We are very interested in further transaction opportunities in Germany, provided of course they meet our investment criteria,” continued Hess. “We feel it may make sense for an independent towerco to be involved in the consolidation and rationalisation of the other national tower portfolios.” Analysys Mason: Marco Cordoni and his team at Analysys Mason are among the ‘go-to-guys’ for tower market analysis and due diligence on a global basis, and Europe is no exception. Antenna Hungaria: Hungary’s recently re-Nationalised broadcast towerco also sells co-locations to and provides installation and maintenance services to telecom clients. Antin Infrastructure Partners: One of the first movers in the European telecom tower asset class, Antin are investors in FPS Towers which owns over 2,000 towers and the rights to 15,000 rooftops in France, and Axion the leading broadcast towerco in Andalucía, Spain. Antin has appetite for further European tower investments. Arcus Infrastructure Partners: Arcus has been an active investor in European towers for over

11 years with the predecessor of what is now UK and Dutch towerco Shere Group. More recently Arcus manages their own and other consortium members’ investments in TDF, France’s largest towerco with 9,950 sites. Arcus has an interest in further opportunities in European towers which may or may not be addressed through their existing platforms, depending on scale and geo. Arqiva: The largest independent towerco in the UK with around 10,550 active towers with a tenancy ratio around 2.5 and a portfolio of 16,500 in total, of which less than 1,000 are pure broadcast sites. Acquired by a Macquarie-led consortium in 2005, into which was rollup up the NTL Broadcast and National Grid Wireless assets. Arqiva has over 2,000 employees and has deep I&C and O&M competencies and resources spanning broadcast and telecom. Arqiva is currently restructuring debt which could result in a change of strategic direction for the company. Ashmore: Another investment firm with an appetite for telecom towers. Axion: Operates 586 broadcast towers with some telecom co-location in Spain, 70% of which are in Andalucía. Owners Antin Infrastructure are believed to be seeking to sell some or all of their stake. Azerconnect: Infrasharing business in Azerbaijan. Berkshire Partners: Berkshire backed Crown Castle during their successful foray into European

Altice

Altice (France, Portugal)

Altice

| TowerXchange Meetup Europe, 12-13 April, London | www.towerxchange.com/meetups/meetup-europe24

towers in the late nineties, and currently has active investments in Protelindo (largest towerco in Indonesia with a small footprint in the Netherlands), Torres Unidas (Andean region of CALA) and Tower Development Corporation in the US and Puerto Rico. Blackstone: Another serial towerco investor currently working with Phoenix Tower International in CALA with at least one other investment in the asset class imminent, none of which is in Europe leaving a vacancy in their stable! Bouygues Telecom: Bouygues Telecom was one of Europe’s first MNOs to sell towers to an independent towerco, selling 2,166 of their estimated 17,000 towers to Antin’s FPS Towers in 2012 for €185mn. Acquisition overtures from Altice, which already owns Numericable-SFR, could result in the divestment of more towers. Britannia Towers / Hibernian Towers: Privately owned towerco with 60 towers in the UK under the Britannia brand, 60 towers in Ireland under Hibernian and a further 20 towers in Northern Ireland under Ulstercom.

Broadcast Networks Europe: Association of 18 broadcast companies operating in 21 European countries whose remit includes ensuring the economic competitiveness of Europe’s broadcast networks, optimising platform developments and representing the industry with regards to policy developments and regulatory intervention.

Brookfield Infrastructure Partners: Participated in the consortium which acquired equity in TDF in 2014 and known to have an appetite for further opportunities in European towers. BuyIn: A 50/50 procurement joint venture between Deutsche Telekom and Orange with an annual budget of €28bn across network technology and other telecom equipment categories. Capital Group: Another investor keen on the telecom tower asset class, Capital Group has or had capital at work in Russian Towers as well as Eaton Towers in Africa. CEE Equity Partners: Investor exploring opportunities in CEE towers. Cellnex Telecom: Catalysts for the opening of the European tower market, Cellnex (formerly Abertis Telecom) have to date deployed over €1.2bn rolling up a portfolio of 15,140 telecom and broadcast towers across Spain and Italy. To put that into context, the sum represents more than half the total capital spent on European towers in the last five years. Flush with capital and confidence from their successful IPO, Cellnex has a €multi-billion acquisition warchest. Although Cellnex dominates the European deal table, it still has plenty of room for growth in its existing markets: towercos own just 18% of towers in Spain and 48% of Italy’s towers. Telecom Italia’s Inwit could be Cellnex’s next acquisition target. “Our model (in Europe) is not based on the idea of

getting three or four tenants on a tower, it’s based around the idea you can dismantle the tenants on an existing tower and transfer them to new sites,” said David Bernal Cantero, BDM at Cellnex in a recent TowerXchange interview. “Our plan in Europe is diversification,” continued Bernal Cantero. “Germany is an attractive market at the moment, reducing the number of operators from four to three will shake things up. The UK is also interesting but it’s a very competitive market with strong incumbent towercos. France is a strong market with some MNO transactions in the pipeline which might drive some changes in the market. We see some good short term opportunities in Europe, not only in the countries mentioned above but also in other European countries.” České Radiokomunikace: With 1,000 access points across the Czech Republic, České Radiokomunikace provides structures and services to broadcast and telecom clients. Owned by Macquarie. Česká Telekomunikační Infrastruktura (CETIN): When PPF acquired O2 Czech Republic from Telefónica in January 2014, they immediately set about separating the retail assets from the infrastructure, in the latter case creating CETIN which was briefly listed on the Prague stock exchange prior to a squeeze out of minority shareholders putting PPF as sole shareholders. CETIN owns 20,000,000 km of metallic cable pairs, 38,000km of fibre and 5,300 outdoor base stations plus 750 micro base stations, providing 99.6% population coverage. With O2 having set up a

www.towerxchange.com/meetups/meetup-europe | TowerXchange Meetup Europe 2016, 12-13 April, London | 25

network sharing agreement with T-Mobile prior to the carve out, CETIN have taken over O2’s role in managing the RAN sharing with T-Mobile Cignal: Owns 115 towers developed for Hutch in Ireland, plus the ground leases under a just under 300 other operator towers. Recently sold to InfraVia prior to which it was known as Coillte. Citi: One of the world’s leading tower transaction advisory groups can be found within the TMT team at Citi. Communication Infrastructure Partners: Owners of Open Tower Company, which acquired 601 towers from KPN in the Netherlands in two tranches in 2008 and 2010 for an undisclosed sum. Current tower count: 684. Crown Castle: Publicly listed U.S. towerco Crown Castle had a profitable foray into European towers between 1997 and 2003, acquiring a £75mn revenue tower business from the BBC and transforming it into a £233mn revenue tower business with a tenancy ratio of 2.9 by 2003, selling it to National Grid Wireless for £1.1bn (just over US$2bn). While Crown Castle has largely retrenched from their international strategy to deploy capital domestically diversifying into small cells and fibre, TowerXchange would not rule out the U.S. giant returning to Europe. CTIL: Joint venture between Vodafone and O2 (Telefónica) in the UK with around 18,000 sites. Predecessor Cornerstone established the passive

infrastructure sharing business, the new CTIL business now has around a £1bn of passive assets on its balance sheet whilst also leading the Beacon active infrastructure sharing project, again between Vodafone and O2. Status of the JV remains unclear if the O2-Three merger is approved.

Deutsche Funkturm (DFMG): Towerco carved out of Deutsche Telekom in 2002. Their parent company remains their lead client representing around a third of DFMG’s tenancies. Operates 26,000 sites, of which around half are rooftops. Deutsche Telekom has twice been rumored to be on the brink of divesting DFMG, but to date the assets are retained on their balance sheet. Digea: Greek broadcast towerco. Digita: Broadcast towerco from Finland. Digital Bridge: Serial tower entrepreneurs Mark Ganzi and Ben Jenkins are building another empire having sold their last venture, GTP, to American Tower for US$4.8bn. Digital Bridge is an investment vehicle through which stakes are invested in towercos around the world. Digital Bridge recently appointed Phil Cooper as Managing Director EMEA, having previously kicked the tyres on the opportunity to invest in TDF. We expect Digital Bridge to have an active investment / platform in Europe by Q2 2016. ECS: Polish tower builder with an appetite to move up the value chain.

EE: UK MNO joint venture between T-Mobile and Orange currently subject to a proposed acquisition by BT which could destabilise the country’s JV infrastructure sharing companies – in this case particularly MBNL. EI Towers: Broadcast towerco with a progressive management team and an appetite to diversify into telecoms – a strategy they are well under way in executing having acquired 700 telecom towers from various small independent towercos in Italy. Telecom now represents 8.9% of EI Towers’ revenues. EI Towers more recently made headlines for their aggressive but ultimately justifiable persuit of an acquisition of Italy’s other broadcast towerco Rai Way – the combination of the two entities could create tremendous efficiencies given the estimated 60% overlap in their networks. Emitel: Polish broadcast towerco diversifying into telecoms. Own 300-400 sites. Acquired by Alinda Capital Partners. ESB Telecoms: Subsidiary of Irish National power company ESB Networks developed to operate telecom sites. Most of their sites, which total around 400, are in substations. ESN Group: Russian oil and gas, energy, engineering and infrastructure giant founded by Grigory Berezkin. Had been interested to bid for Vimpelcom’s Russian towers when the process started and stopped in the past – interest in the current process unknown.

| TowerXchange Meetup Europe, 12-13 April, London | www.towerxchange.com/meetups/meetup-europe26

ETB: Serbian broadcast towerco. European Wireless Infrastructure Association (EWIA): Trade association for independent towercos in Europe whose members included (at time of press): American Tower Germany, Arqiva, Axion, Cellnex, EI Towers, FPS Towers, Open Tower Company, PCIA, Protelindo Towers BV, Towercom and Wireless Infrastructure Group, whose CEO Scott Coates chairs the EWIA. EuroTower: Aspiring towerco for Europe with big vision and a willingness to evolve the business model to meet the needs of European MNOs. Yet to close their first deal. EY: TMT strategy and corporate finance advisory team with extensive experience of advising on tower transactions. F2i: One of the largest infrastructure funds in Europe, and owns a majority stake in Metroweb, which operates a fibre network in Milan and Lombardy. F2i was rumored to have bid for Wind’s towers ultimately acquired by Cellnex, and has been again linked with a bid for Inwit, possibly coming in as partners of Cellnex. FMO: Dutch development bank 51% government owned, 49% by commercial banks and financial institutions. Have invested in African towercos, not yet in Europe, where Eastern Europe is a better fit than the West given their developing market remit. FPS Towers: FPS was formed in 2012 by Antin