ts.enkhbayar ceo [email protected] new delhi, india 2010.04.19 mongolian mortgage corporation...

Post on 22-Dec-2015

214 views

TRANSCRIPT

Ts.EnkhbayarCEO

New Delhi, India 2010.04.19

MONGOLIAN MORTGAGE CORPORATION M I K

Regional Symposium on Pro-Poor

Housing Finance in Asia and Pacific,

MORTGAGE MARKET DEVELOPMENT IN MONGOLIA

ISSUES AND CHALLENGES

Content • Housing finance system development

process• Mortgage market overview• Status of conditions on mortgage

market development • MIK performance , issues and

challenges

Housing finance system development overview

• Top down system• Financed by 100% state• Waiting list• Free housing delivery

Before 1990s Top down system

• Housing supply stopped• Housing law (1997)• State Housing policy

• HFS needs• Enabling environment

• Housing privatization • ADB project 3090• Some initiatives by private

sector

1990-2000 Transitional period

• Setting up mortgage legal environment

• Proper PMM infrastructure

• capital market development

• Capacity building, Institutional strengthening

• Warehousing • Liquidity facility• Issuance MIK bond• Phased development

approach

2008 …. Development

4

Housing Areas:

Ger area

Planning – not proper Water supply – kiosks (potable)Sewage – pit latrineHeating – stove using coal and woodElectricity – yesSocial infrastructure – not sufficientLand ownership –yesHousing finance – savings, assistance from relatives and friends, loans

Planning –proper , Water supply – central systemSewage – central systemHeating – central systemElectricity – central systemSocial infrastructure –sufficientApartment ownership –yesHousing finance – mortgage loans, savings

70%- population59%- UB80-90% provincial towns

Serviced apartment area

5

2009.12.31Mortgage market overview Market Core Indicators 2003 2004 2005 2006 2007 2008 2009

Total Debt Outstanding /mln.MNT/ 8,2 19 31 74,3 164,6 217 226 Total Debt Outstanding / Changes/ : 0% 132% 62% 141% 122% 8.3% 8.5%

Debt Outstanding/Borrower /mln MNT/ : 7,2 6,6 6,5 8,3 10,0 13 13.6

Number of Mortgage Borrowers 1,057 2,892 4,774 8,984 16,444 16 590 16 628

Market W.A.I.R /Ann , %/: 12.0% 14.5% 14.7% 17.8% 16% 18.7% 17.2%

Original W.A. LTV % : 83% 70% 75.% 76.% 68% 70% 78%

2003 2004 2005 2006 2007 I Quarter, 2008

8,199,617.

73

19,018,145

.68

30,839,715

.65

74,318,389

.54

164,625,90

1.96

205,857,09

0.12

Shareholders

MIК

Main Goal

Promotion and development of primary

and secondary mortgage markets by raising

medium to long term funds on domestic and foreign capital market

through a series of capital market tools to create and

ensure s smooth functioning of long-term

financing system to promote affordable home

ownership and urban development for

Mongolia’s people.

Established 06.09.2006

Mortgage market activity

LenderCommercial

Bank

loans Mortgage Bonds INVESTOR

(International,

Domestic )Funding Funding

Borrower

Loan

₮

SECONDARY MORTGAGE MARKET ( Raise fund through making a portfolio on similar housing

mortgage loans to sell it to the third party)Lender- Agency- Investor

Secondary Mortgage Market

Institution

2 major role i) market development driver I

i) Pioneering SMM

MONGOLIAN MORTGAGE CORPORATION

Shareholders

Board Members

Financial Committee

Operational Committee

Risk Committee

Legal & Audit Committee

CEO

Asset management and Securitization

Division(Asset management officer, Securitization officer)

Finance and Investment Division(Senior finance officer, Accountant, Assistant Accountant)

Risk Management Division

(Risk management officer)

Internal operation Division

(IT, Layer, Cooperation officer, Administration & HR officer)

8

Reason why we established MIK

– Increase the affordability of the housing loan – Stable structure for long term financing – Increase in housing mortgage market – Need for capital market development– Liquidity facility

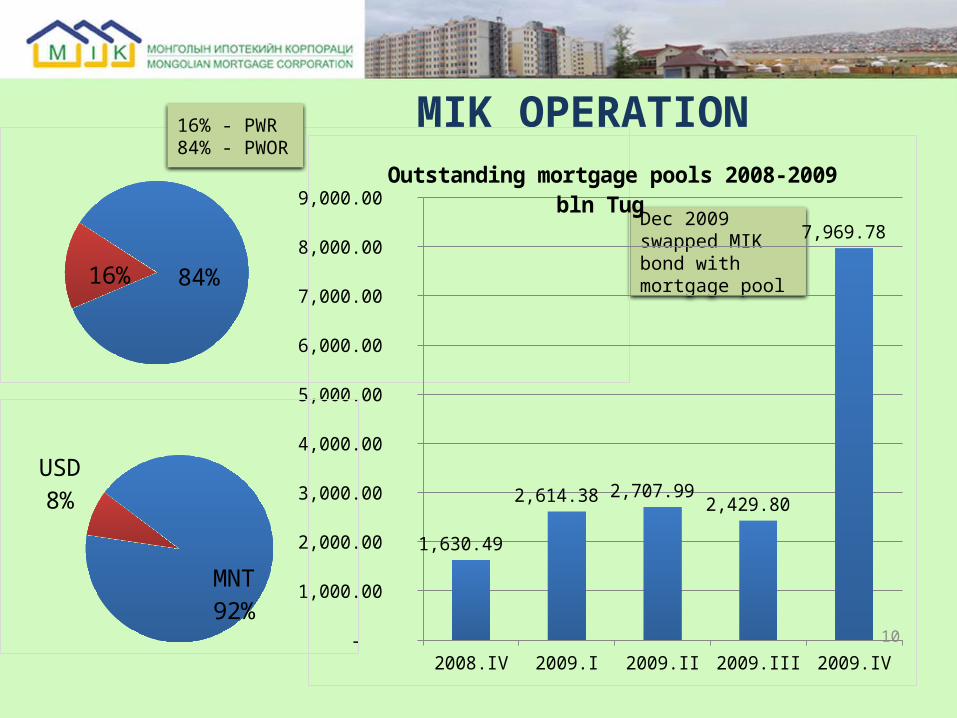

Dec 2009 swapped MIK bond with mortgage pool

МIK OPERATION

84%16%

10

2008.IV 2009.I 2009.II 2009.III 2009.IV -

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

7,000.00

8,000.00

9,000.00

1,630.49

2,614.38 2,707.99 2,429.80

7,969.78

Outstanding mortgage pools 2008-2009 bln Tug

MNT92%

USD8%

16% - PWR84% - PWOR

DEVELOPMENT PHASES

Diversification 2017-2020

Development period 2013-2016

Start up period (setting up solid foundation for mortgage market development)2007-2012

Phased Development Approach

Issues to be done for developing efficient mortgage market development

Legal environment

Mortgage lawMortgage securitySPV Pool registrationTax matterMIK legal status

Primary mortgage market i

nfrastructure

Standardization of mortgage loansProperty appraisal Mortgage database systemMortgage insuranceCredit bureauCapital market developmentRating Income verification system

Market environment

Political stabilityEconomic stabilityBalance on Supply and demand Creating domestic potential investor AffordabilityCapacity developmentInstitutional capacityCoordination and linkages of market playersQuality of collateral •Efficiency of Urban planning, land development, construction quality•Effective operation and maintenance

14

MIK ProgressSep 2006 • MIK established June 2007 • MOU signed with KfW, MOF, BOMNov. 2007 • First mortgage pool purchasedJune 2008

• MIK set up internal operational procedures

Oct. 2008• Mortgage standardization procedure

approvedMay 2009 • Mortgage toolkit with IFC TA projectJune 2009 • Mortgage law approvedJuly 2009 • Agreement with MOF-KfW

August 2009 • FRC shelf registration MIK BondSep. 2009

• UNESCAP-UNHABITAT- NHB workshop

Oct.2009 • first OTC transaction and procedureOct 2009 • First MIK bond issued and soldDec 2009 • KfW TA startedJan 2010 • MIK IT infrastructure

March 2010• Micro housing finance study project ,

IFCApril 2010 • ABS law has discussed by ParliamentApril 2010

• Domestic investor-insurance companies involved

April 2010• Mortgage guarantee program

initiated with FMO

15

learning• Play dual role

– Driven force of setting up Mortgage market development as well as capital market

• (laws, regulations, policy framework, financial infrastructure, capacity building, workshops, RTD, lobbying, etc)

– Acting as secondary mortgage institution

• Purchasing pools from banks, warehousing m issuing bonds and selling investors etc

• Institutional strengthening and capacity building

ISSUES AND CHALLENGES– Implementation of laws and regulations recently approved– Economic stability– Different Understanding of mortgage issues– Standardized and documented origination and servicing– Low affordability rate– Local rating agency– Inappropriate Professional appraisal– Title and Lien registration, enforcement– Balance sheet treatment with recourse based loan pools and bonds– Bankruptcy remote vehicles – Tax and accounting guidelines – IT infrastructure AM– Credit scoring – Mortgage insurance– Mortgage guarantee program

17

What is next?• Improve accessibility housing loans to LIHs

– Housing micro finance study,– Guarantee program with international orgs.

• ABS , SS laws and related regulations, by laws• Issue bonds to domestic and international

market• Expanding cooperation

– Network meeting in Mongolia APHFU– Intensive development of mining industry –coal

mining, copper mining, gold etc and

18

THANK YOU

Mongolian Mortgage Corporation LLC /MIK/

MIK Building , United Nations street-38Chingeltei district-4, 15160Ulaabaatar, Mongolia

www.mik.mn, [email protected] Tel: (976) 11-328267Fax (976) 11-313338