triana - why does warren buffett make money

TRANSCRIPT

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 115

34

In a paper written last year a group of hedge fund profes-sionals and academics claimedto have ldquodiscoveredrdquo how f amedinvestor Warren Buffett makes

his money The outstanding returns expe-rienced by Berkshire Hathaway (Buffettrsquosfirm) can be explained by two main fac-tors (1) wise investments in underval-ued safe blue-chip securities and (2)extremely agreeable funding terms lead-

ing to economical leverage By punting ontemporarily cheap assets with lots of bor-rowed funds and by being able to bor row cheaply Buffett has been able to reachlegendary status among the investmentcommunity In the words of the paperrsquosauthors ldquoBuffett has developed a uniqueaccess to leverage that he has invested insafe high-quality cheap stocks and thesecharacteristics largely explain his i mpres-sive performancerdquo1

Here we focus on the funding side of the equation leaving the stock-picking prowess analysis to othe rs Where is Berk-shire getting that vast and affordablefunding f rom How is Buffett being ableto erect the wall of economical leveragethat makes his returns s o mouth water-ing Simply stated by being willing totake on a lot of risk For a fee of course

Berkshire sel ls insurance and rein-surance policies into the financial mar-kets It also sells der ivatives All of thosesales generate (for the most part upfront)premiums from those purchasing pro-

tection from Berkshire Those premi-ums can amount to a very large sumBuffett then invests that money an activ-ity that should lead to interesting returnsgiven his track record Given that a lotof the sold insurance policies and deriv-atives contracts may take a long whileif at all before Berkshire has to makeany loss payouts Buffett can make good

use of the premiumcollected for manymany years The hopeis that any eventualloss payment is bothlower than the pre-

m i u m i n i t i a l l y c o l -lected and long to come I f Berkshirebreaks even that is if the eventual insur-ance claims and derivatives payouts equalthe amount of premium received Berk-shire would have received the equiva-lent of zero-cost financing for all thatperiod of time (plus any returns obtainedfrom invest ing the premium s) WereBerkshire to actually enjoy underwrit-ing profits (payouts lower than the pre-miums) the company would have in

effect enjoyed negative cost fundingThis is what the paperrsquos authors meanwhen they state that Buffett enjoys thesignificant advantage of having uniqueaccess to steady cheap leverage In theSage of Omaharsquos very own words

If our premiums exceed the total of our expensesand e ve ntual losse s we re gis te r an unde r-writ ing prof i t that adds to the inve stme ntincome our float produces When such a profitis earned we enjoy the use of free money mdashand better yet get paid for holding it Thatrsquoslike your taking out a loan and having the bank

pay you interestrdquo

2

The difference between the premiumscollected and the loss payments made(i f any) is ca l led ldquof loat rdquo B erskhire rsquosprowess thus would be based on thetremendous amounts of float it can gen-erate According t o the pape rrsquos authors36 percent of Berk shirersquos liabilit ies comefrom insurance f loat on average Berk-shire does not seem to include deriva-tives-generated float under the overallinsurance float number so the fina l num-

ber may be even greater Exhibit 1 il lus-t r a t e s t h e e s t i m a t e d a n n u a l c o s t o f Berskhirersquos insurance float since 1976(22 percent on average 3 percentagepoints below the average Treasury Bill ratenotice how the company seems to havebeen getting better at it as of late)

And Berkshi rersquos float has been grow-i n g s p e c t a c u l a r l y t h r o u g h t h e y e a r s m a t c h i n g t h e c o m p a ny rsquos s p e c t a c u l a rgrowth If float was $39 million in 1970it had jumped to $16 billion by 1990 to

PABLO TRIANA is a professor at ESADE Business School and the author of The Number That Killed Us A Story of ModernBanking Flawed Mathematics and a Big Financial Crisis

P A B L O

T R I A NA

P R A C T I C A L

M A T T E R S

WHY DOES WARRENBUFFETT MAKE MONEY

CORPORATE FINANCE REVIEW NOVEMBERDECEMBER 2013

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 215

35PRACTICAL MATTERS NOVEMBERDECEMBER 2013 CORPORATE FINANCE REVIEW

$2787 bi l l ion a decade la ter and to$7312 billi on by 2012 (again these num-

bers may not include derivatives-gen-erated float only insurance-generatedfloat) Thatrsquos a lot of very cheap (evennegative cost) funding

Very few other insurers seem to beable to achieve those ty pes of outcomesWhile Berkshire has generated an under-w r i t i n g p r o f i t f o r t h e p a s t 1 0 y e a r sstraight competitors donrsquot appear to bea b l e t o b o a s t s i m i l a r l y r o s y r e s u l t s(reporting in fact underwriting lossesas a whole) Listen to Buffett explain it

Let me emphasize that cost-free float is not anoutcome to be expected for the [insurance]industry as a whole There is very litt le lsquoBerk-shire-qualityrsquo f loat existing in the insuranceworld In 37 of the 45 years ending in 2011 theindustr yrsquos premiums have been inadequate tocover claims plus expenses3

Berkshirersquos strategy has been lab eledas ldquobetting again st Bet ardquo after the famousinvestment risk measurement variableYou buy low risk ( ldquolow Betardquo) assets a nd

yo u sel l high r isk (ldquohigh B etardquo) ones

hoping that the former will do well whi le

the latter do b adly Insurance and rein-surance policies including on very exotic

underlyings are a way of making thatbet Derivatives are another While many would be expected to be familiar with Berk-shirersquos insurance forays they may be lessso with his derivatives trades In thisarticle we focus on this less-known leg of Warren Buffettrsquos search for float

Derivatives gamesBerkshire Hathaway began selli ng equity index put options and credit protection

through credit default obligations (creditdefault swaps and the like) in 2004 Atthe time Berkshire Hathaway already held a very substantial derivatives port-folio legacy of the acquisition of rein-surer General Re Berkshire had embarkedon a strategy to wind down the GeneralRe derivatives book which included a myr-iad of products and underlying assetsmore than 23000 contracts outstand-ing For instance as of December 312003 Berkshirersquos derivatives portfolio

included $11 billion in foreign currency

EXHIBIT 1 Buffettrsquos Cost of Leverage The Case of His Insurance Float

Fraction Averageof years with cost of funds

negative cost (truncated) Spread over benchmark rates

Fed Funds 1-Month 6-Month 10-year T-Bill Rate Libor Libor Bond

1976ndash1980 079 167 ndash459 ndash565 ndash576

1981ndash1985 020 1095 110 ndash027 ndash128

1986ndash1990 000 307 ndash356 ndash461 ndash480 ndash490 ndash530

1991ndash1995 060 221 ndash200 ndash224 ndash246 ndash271 ndash464

1996ndash2000 060 236 ndash270 ndash310 ndash333 ndash348 ndash356

2001ndash2005 060 129 ndash082 ndash096 ndash105 ndash119 ndash311

2006ndash2011 100 -400 -584 ndash606 ndash629 ndash659 ndash767

Full Sample 060 220 ndash309 ndash381 ndash369 ndash388 ndash480

In years when cost of funds is reported as ldquoless than zerordquo and no numerical value is available cost of

funds is set to zero

Data from Frazzini A Kabiller D and Pedersen LH Buffetts Alpha (May 3 2012) The data are hand-

collected from Buffetts comment in Berkshire Hathaways annual reports Rates are annulaized in percent

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 315

36 CORPORATE FINANCE REVIEW NOVEMBERDECEMBER 2013 PRACTICAL MATTERS

forwards $333 bil l ion in interest rateand currency swaps and $102 billion ininterest rate and currency options Thesecontracts (both long and short expo-sures) generated assets and liabilities insimilar amounts (about $15 billion each$10 billion if you allow for counterparty nettin g) A year later the legacy p ortfoliohad already been wound down signifi-cantly with swaps notional (including now credit products as well as interest rates-currency) just at $153 billion and inter-est rates-currency options just at $35billion By December 31 2005 with just740 contracts left outstanding the respec-tive numbers were $44 billion and $14billion (currency forwards remained ataround $13 billion in size) by Decem-

ber 2006 Berkshirersquos derivatives book

had become dominated by the equity index puts and credit default obligationspositions with interest rates-currency swaps at $10 billion interest rates-cur-rency options at $4 bill ion and foreigncurrency forwards at $1 billion By thebeginning of 200 8 the legacy portfoliohad been essentially liquidated and essen-tially a ll of B erkshirersquos derivatives bookconsisted of the equity puts and the creditobligations The unwinding had beencostly with losses of more than $400million by year-end 2005

The equity puts and credit defaul tobligations positions were built slowly at first and more intensely later on By

ye ar- end 2004 the not ion al size of theput contracts was around $4 bi l l ion

growing to $14 billion a year later and

EXHIBIT 2 The Evolution of the Notional Size of the Puts and the Credit Contracts

$

$

amp

amp

()

()

()

+

$

-

-

amp

-

()

-

$

amp

()

$

$

$

amp

$

()

$

$

$$

$$

amp

$$

()

$$

$

$

$

amp

$

()

$

$

$amp

$amp

amp

$amp

$amp ()+ - )ampamp)$ )0123 4025

678912 8lt0=2 gt=1ltABC5

$

amp

$

amp

()

()

()

+

()

amp

-

-

-

()

-

()

()

()

ampamp() + -amp( 012 (0345 6753839

675005lt4 =gtgtltA3

012 (0345 B =gtgtltA3

CAltA39DE70F0lt40G39

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 415

37PRACTICAL MATTERS NOVEMBERDECEMBER 2013 CORPORATE FINANCE REVIEW

to $21 billion by December 2006 Theposition reached its pinnacle notional sizeof $35ndash40 bil lion in late 2007 to early 2008and kept more or less constant at that levelfrom then on (save for a smallish unwind-ing several years later) Notional sizes

expressed in dollars take into accountcurrency exchange rates

The notional size of t he credit defaultobligations was $28 bil lion by year-end2005 $25 billion a year later and $46bil l ion in December 2007 Up to thatpoint Berkshire had sold protection only o n A m e r i c a n h i g h - y i e l d c o r p o r a t eindexes (about 100 names per contract)From 2008 the company not only sig-nificantly ramped up such act ivity butalso began to sel l protection on indi-

v i d u a l c o r p o r a t e n a m e s a n d o nstatemunicipal i t ies with the conse-quent drastic increase in total notionalamounts which reached a high of $30 bil-lion by year-end 2008 (sizes decreasedfrom that point due to a combination of contract expirations and cancellationsall the way to less than $10 billion by late 2013 essentially all exposures today come exclusively from the statemunic-ipalities contracts)

As of year-end 2006 Berkshire had

sold 62 equity puts and credit defaultcontracts this number went up to 94 a

ye ar lat er and to 251 by ye ar- end 2008(down to 203 by year-end 2010 follow-ing the expiration of the first contractssome unwindings and the fact that nonew contracts were being writ ten) Thelast equity put contracts were sold inFebruary 2008 The last credit contractswere written in February 2009 (just onenew contract)

Exhibit 2 displays the evolution of the

notional size of the puts and the creditcontracts The equity index puts wereEuropean (can only be exercised at matu-rity) were struck at-the-money (thusaffording a very tasty premium for Berk-shire as these options are very close tohaving positive intrinsic value) werew r i t t e n o n f o u r i n t e r n a t i o n a l e q u i t y indexes (SampP 50 0 FTSE 100 Euro Stoxx 50 and Nikkei 225) and had the fol-lowing expiration dates between Sep-t e m b e r 2 0 1 9 a n d J a n u a r y 2 0 2 8 ( t h e

weighted average life of all put contracts

was approximately 75 years at Septem-ber 30 2013)

Originally 47 put contracts were soldgenerating $49 billi on upfront premiumThe maximum possible payment fromBerkshire on these contracts equals theputsrsquo notional s ize (currently around$32 bil l ion) but this would only takeplace at contract expiration and only if all the indexes reach a value of zero att h a t t i m e T h e l i k e l i h o o d o f t h a t i sseverely limited Were Berk shire forcedto make payments equal to $49 billionit would break even on the puts (plusany investment returns on the float) A25 percent drop in all the equity indexesby expiration date would yield a losspayout of around $8 billion at currentforeign exchange rates

I n Q2 2009 B erkshire agreed withcounterparties to amend six equity putcontracts reducing maturities by between35 and 9 5 years (br inging the tota lweighted average maturity of the puts port-folio from 13 to 12 years) Strike priceson those contracts were reduced between29 percent and 39 percent Finally theaggregate notional amount of three of thosecontracts increased by $160 m il l ionThese amendments were cost-free (nomoney changed hands) In Q4 2010 eightequity index put contracts ($43 billionnotional maturities between 2021 and2028) were terminated (at the instigationo f t h e c o u nt e r p a r t y ) t h e u n w i n d i n g required Berkshire to pay $425 millionfor a net gain of $222 million mdash as ithad originally received $647 million inpremium

All corporate credit default contracts(both high-y ield and investment grade)

expire in Q4 2013 a significant portionof high-yield contracts expired in Q42012 B erkshire is l iable for payoutswhenever a credit event takes p lace H igh-yie ld contract expirat ion datesranged from September 2009 to Decem-ber 2013 Individual corporate default con-tracts had f ive-year maturities and werereferenced to about 40 different namesBerkshire stopped selling individual cor-porate credit default contracts from 2009on as dealers began ask ing for stringent

collateral

BERKSHIRE

STOPPED

SELLING

INDIVIDUAL

CORPORATE

CREDIT DEFAULT

CONTRACTS

FROM 2009 ON

AS DEALERS

BEGAN ASKING

FOR STRINGENT

COLLATERAL

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 515

Premiums received upfront from thehigh-yield credit contracts totaled $34billion payouts on those contracts hadtotaled $26 billion by Q3 2013 Premi-ums from individual corporate creditdefault contracts are paid quarterly ($93million a year) Berkshire assumes that thefinal underwrit ing profit (premiums raisedminus payouts) from corporate creditcontracts will be around $1 billion whenthey expire by year-end 2013 having enjoyed on average annual $2 billion float

Statemunicipalities credit contractsexpire between 2019 and 2054 (about500 underlying debt issues) Any poten-tial loss payments cannot be settled untilexpiration We found no specific data on the amount of the (upfront) premi-ums received by Berkshire from selling this risk but we can make an informedapproximation At year-end 20 08 Berk-shire announced that the total premium

raised from selling the high-y ield defaultcontracts had been $34 billion A yearearlier the announced numb er had been$32 billi on This implies new premiumsof $02 billion in 2008 At the same timewe know that the individual corporatecontracts that were first sold in 2008implied annual premiums of $93 mil-lion That makes it $293 million in new p r e m i u m s f o r 2 0 0 8 S i n c e B e r k s h i r ereported in its 2008 annual report thatit had raised $633 million that year in new

premiums from credit default obliga-

tions we may be al lowed to concludethat the statemunicipalities contractswere sold for some $340 million ( only onecredit default contract was sold after2008 I donrsquot know which of the threeunderlying risk categories that last con-tract was referenced to) In August 2 012$825 billion of the statemunicipalitiesposition were terminated (apparentlyt h e o r i g i n a l c o u n t e r p a r t y h a d b e e nLehman B rothers and Lehm anrsquos l iq-uidators were eager to unwind the tradewhich was heavily in t heir favor thus thecontract cancellations may not neces-s a r i l y i m p l y a n e g a t i v e v i e w o f t h estatemunicipalities market on the partof Berkshire) I very roughly assume thatthe cost of this unwinding may have beenaround $475 million or the ldquoapproxi-materdquo size of the li abilities generated by these contracts at the time

Loss payout amounts on the credit

default obligations are subject to indi-vidual and aggregate limits (for instanceof around $5 billion in the case of the high-

y ield defau lt con tracts) and pay mentobligations are on a first-loss basis oron an aggregate-deductible basis

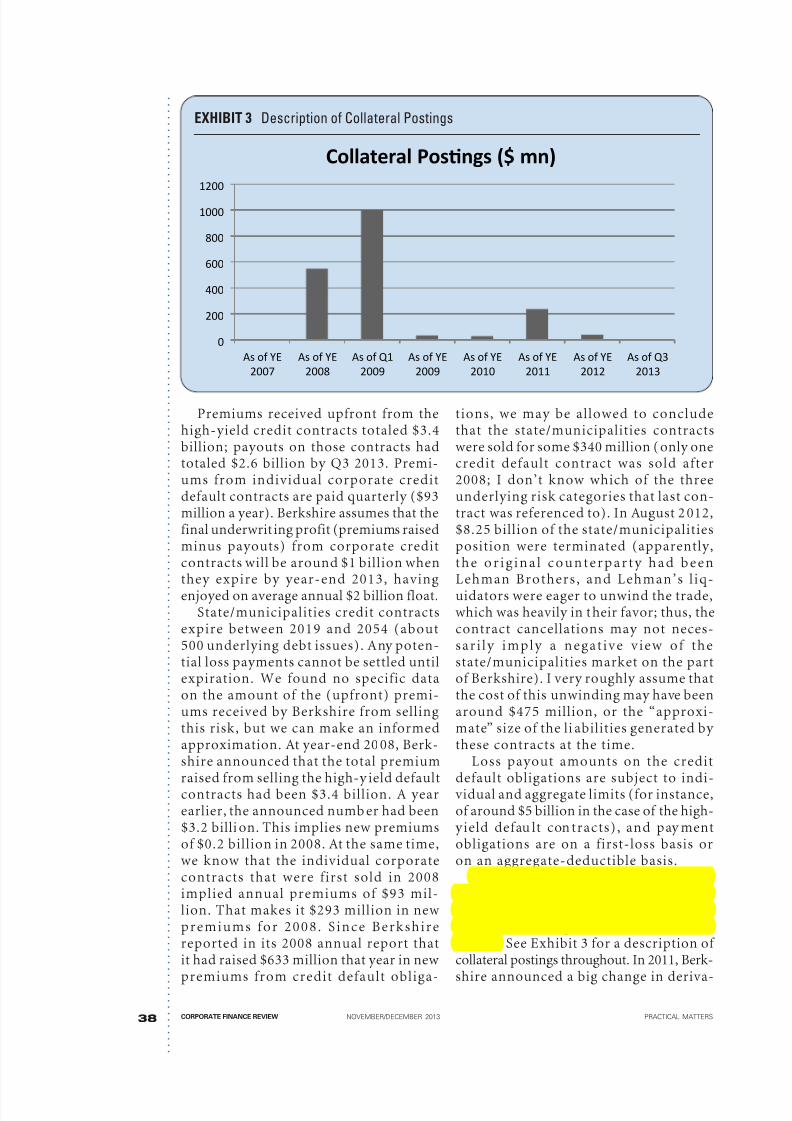

With limited exceptions Berkshire hasnot been required to post collateral How-ever were it to suffer a rating dow ngradeit would have to post an additional $11billion See Exhibit 3 for a description of collateral postings throughout In 2011 Berk-

shire announced a big change in deriva-

38 CORPORATE FINANCE REVIEW NOVEMBERDECEMBER 2013 PRACTICAL MATTERS

EXHIBIT 3 Description of Collateral Postings

$

amp

() + -

() + -

amp

() +

0

() + -

0

() + -

() + -

() + -

() + 1

1

$amp$ )+- 01

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 615

tives collateral requirementspolicies by the financial industr y making it now unac-ceptable for the company to enter intonew major derivatives contracts

Besides the attainment of a lot of extra float (some $7ndash8 bill ion for several years

some $6 billion for a lot of years) anotherkey reason for entering into these par-t i c u l a r d e r i v a t i v e s p o s i t i o n s w a s t h ebelief that they were vastly overpricedThat is Berkshire was being given thechance to collect much more money fromselling the risk than it should accord-ing to Berkshire If you look at the equity puts the premium at way over 10 per-cent of notional amount certain ly lookstasty (not surprising g iven the long matu-rities and the at-the-money strike) This

is how Buffett at year-end 2006 pre-emptively tried to address any queries hisshareholders may have about the factthat he had been se l l ing such a largederivatives por tfolio (whi ch as we knowwas only about to get even larger)

The answer is that derivat ives just like stocksa n d b o n d s a r e s o m e t i m e s w i l d l y m i s -pr ice dhellipThough we wil l e xpe r ie nce losse sfrom time to ti me we are likely to continue toearn mdash overall mdash significant profits from mis-priced derivatives4

The portfolio selected by Berkshireto short had one highly intriguing char-acteris tic It was for the most part devoidof counterparty r isk Since premiumson the equity puts the high-yield cor-p o r a t e c r e d i t d e f a u l t s w a p s a n d t h estatemunicipalities credit default oblig-ations were received upfront Berkshirecould not b e ldquostiffedrdquo any money on th esecontracts Only in the case of the indi-vidual high- grade corporate credit defaulto b l i g a t i o n s w a s c o u n t e r p a r t y r i s k

involved as premiums were receivedquarterly but this position was just a small fraction of the total trade If Berk-shirersquos t rading counterpar ts went brokeor moved to a far away island the firmwould suffer almost no pain Given theintense focus on counterpart y risk afterthe financial cri sis this is no small feat

Berkshirersquos roller coasterHow did Buffettrsquos derivatives play evolve

Well itrsquos been qu ite a r ide thatrsquos for sure

Lots of ups and downs in gains and lossesGiven that Berkshire must account for thechanges in the market (fair) value of t hederivatives in its income statement thoseups and downs have impacted reportedearnings on a continuous bas is And

given that the value of derivatives mustbe accounted as either assets or liabili-ties on the balance sheet Berkshirersquoscapital ratios and perception of the firmas safe and sound (these derivatives hap-pened to be liabilities essentially all thetime since they mostly implied futurepotential obligations only from Berk-shire to its counterparties and not vi ceversa) could also be affected

Such chute-the-chute is the unavoid-able price to pay when one chooses to s ell

a lot of long-term and varied derivativesrisk However in this case two factorswere present that made it much morebearable than i t might have been forother firms First and crucially and aswe mentioned earl ier Berkshi re got away with very lig ht collateral terms at initi-ation of the contracts Many a firm hasb e e n s u n k b e c a u s e t h e m a r k e t w e n tagainst them increasing their liabilitiesand drastically enhancing margin require-ments until there was no more collat-

eral available to post up and liquidationwas the next sad step Thanks to thepreferential t reatment obtained Berkshirecould sell all that equit y currency andcredit r isk safe in the knowledge thatany potential future margin call wouldbe of a minimal size Collateral couldnot s ink Berkshire making the tradesmuch more attractive and probably evenpla in feas ible (B erkshire would quiteprobably not have sold the portfolio hadcollateral requirements been stringent)

Apparently the most Berkshire has hadto post during the life of the trade was$17 bil l ion at some point during theworst of the 2008 financial crisis Thisis money that still continues to producea return for Berkshire while it is being held as a guarantee

Second Warren Buffett doesnrsquot seemto care at all about interim earnings orbalance sheet volatility (the lack of strin-gent collateral requirements possibly plays a role here) repeatedly saying so

to his shareholders He firmly believes

39PRACTICAL MATTERS NOVEMBERDECEMBER 2013 CORPORATE FINANCE REVIEW

THE PORTFOLIO

SELECTED BY

BERKSHIRE TO

SHORT HAD

ONE HIGHLY

INTRIGUING

CHARACTERISTIC

IT WAS FOR

THE MOST

PART DEVOID OF

COUNTERPARTY

RISK

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 715

that the trades will in the end generatepositive float and thatrsquos what tr uly countsHey thatrsquos why they were put on in thefirst place free real money for the firmwho cares about some collateral-light unre-alized tu rbulence on the side Not War-

ren Buffett certainly

Our derivative posit ion will sometimes causelarge swings in reported earnings even though[we] might believe the intrinsic value of thesepositions has changed little [We] will not bebothered by these swings mdash even though they could easily amount to $1 billion or more ina quarter mdash and we hope [shareholders] wonrsquoteitherhellipIn our catastrophe insurance busi-ness we are always ready to trade increasedvolatility in reported earnings in the short runfor greater gains in net worth in the long runThis is our philosophy in derivatives as well5

The market value of B erskhirersquos deriv-atives portfolio would be impacted by several key variables In the case of theputs Berkshire would suffer setbacks if equity prices fell if equity volatility shotup if the dollar dropped in va lue versusthe yen euro or pound and if interestrates went down It would make gains if the opposite moves took place and also

just fro m t he p as sag e of time In the c as eof the credit default contracts Berskhirewould suffer losses if American corpo-

r a t e a n d s t a t e m u n i c i p a l i t i e s c r e d i tspreads shot up and (in the case of a few contracts) if the counterparty defaultedor looked close to defaulting

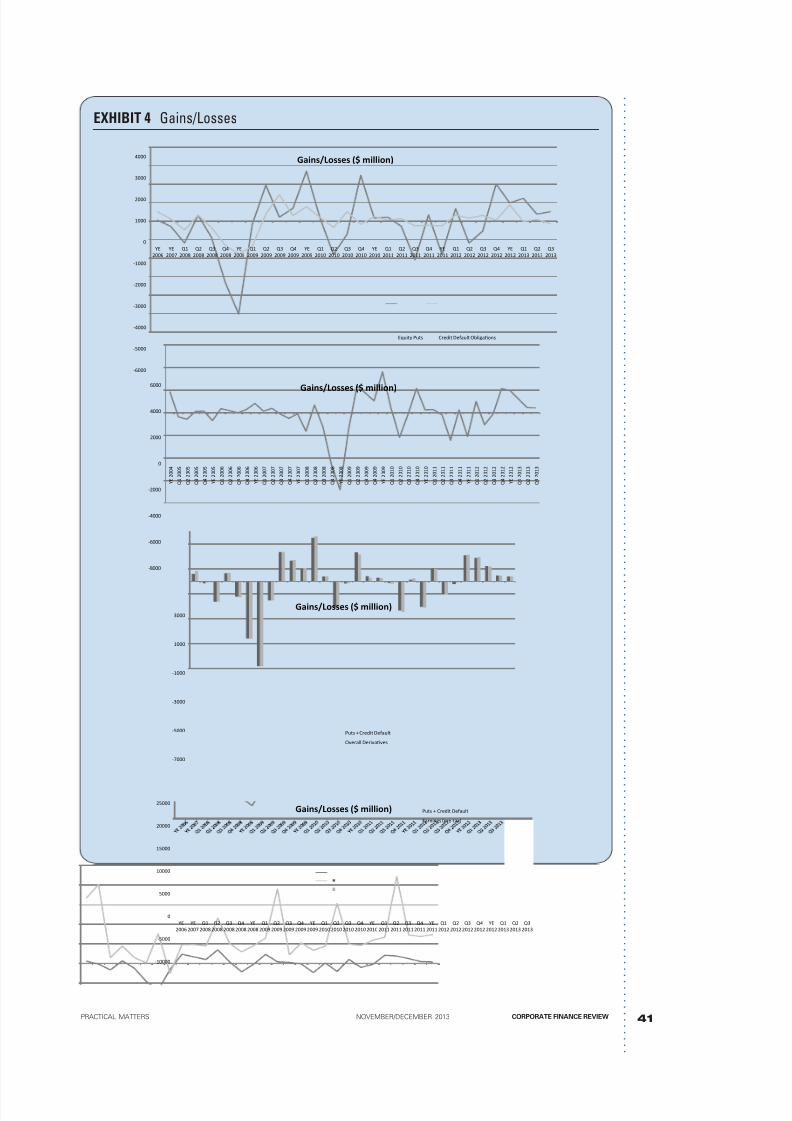

As these variables fluctuated signifi-cantly during the life of these contractsBerkshire experienced significant tur-bulence in mark-to-market derivativesgains and losses as well as on the port-foliorsquos liabilit ies And given that the port -folio was quite sizeable and that some of those gains and losses could be large

t h e t u r b u l e n c e s o m e t i m e s h a d a b i g impact on Berkshirersquos overall reportedearnings Exhibit 4 details t he evolutiono f t h e g a i n s l o s s e s l i a b i l i t i e s a n dnotional amounts The information comesfrom Berkshirersquos quarterly and annualreports and while thorough care hasbeen taken to collect the data accuratelys o m e e r r o r s o r o m i s s i o n s m a y b einevitable Detailed info on the puts andcredit contracts is only available on anannual basis from 2006 and on a quar-

terly basis from 2008

Letrsquos start w ith gains and losses (partof the companyrsquos income statement)While 2006 and 2007 were re lat ive ly placid (with the exception of Q4 2007)2 0 0 8 h a s b y f a r b e e n t h e w o r s t - p e r -forming year wit h a combined account-

ing setback of $6 8 billion Since by thattime unlike in previous years the putsand the credit contracts comprised essen-tially Berkshirersquos entire derivatives port -folio from that point on gains and losseson the former almost exactly matchedoverall derivatives gains and losses 2009was the best year ($36 billion gain ) inspite of a horrible Q 1 2010 saw a mod-est gain of $420 million notwithstand-i n g a $ 2 1 m i l l i o n l o s s i n Q 2 2 0 1 1was horrible mdash a $2 bill ion setback Mar-

kets rebounded in 2012 leading to a$19 billion gain So far 2013 has beengreat with a cumulative $2 billion gainSince 2008 the portfolio yielded gainsin excess of $1 billion on seven quar-ters and losses in excess of $1 billionalso on seven occasions Gains above$2 billion took place three times lossesabove $2 billion also three times

These gainslosses had on occasiona big impact on B erkshirersquos overall prof-its For instance Berkshire barely made

any money in Q4 2008 (just a t iny $140million in pretax earni ngs a 90 percentdecline with regards to the previous quar-ter) and the massive $45 billion deriv-atives loss surely had something to do withit The firmrsquos entire pretax earnings for2008 at just $75 billion were only 37percent of 2007rsquos figure the $68 bi llionderivatives debacle contributed might-ily to that sharp decline (ie withoutthe derivatives no such sharp declinein profitabilit y) To be fair derivatives

gains have also contributed to signif icantincreases in profits and even to the merepresence of such increase as in Q4 2010when overall earnings grew by less than$2 billion coincidental with a deriva-tives gain of $23 bil l ion or as in Q42 0 1 2 ( $ 8 0 0 m i l l i o n a n d $ 2 1 b i l l i o n respectively)

The derivatives portfolio could withminor exceptions represent only a lia-bility for B erkshire given that any pay-ments can only originate from the firm

(and not from its counterparties) Only

40 CORPORATE FINANCE REVIEW NOVEMBERDECEMBER 2013 PRACTICAL MATTERS

BERKSHIRE

EXPERIENCED

SIGNIFICANT

TURBULENCE

IN MARK-TO-

MARKET

DERIVATIVES

GAINS AND

LOSSES AS

WELL AS ON THE

PORTFOLIOrsquoS

LIABILITIES

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 815

41PRACTICAL MATTERS NOVEMBERDECEMBER 2013 CORPORATE FINANCE REVIEW

EXHIBIT 4 GainsLosses

amp

(

)

)

(

amp

+

(

+

(

-)

(

-(

(

-

(

-amp

(

+

(

-)

(

-(

(

-

(

-amp

(

+

(

-)

()

-(

()

-

()

-amp

()

+

()

-)

())

-(

())

-

())

-amp

())

+

())

-)

()(

-(

()(

-

()(

-amp

()(

+

()(

-)

()

-(

()

-

()

$amp() + -($

+01234 5136 78923 9lt=1gt3 gt2A=BCD6

amp

amp

( ) amp

+

-

amp

( )

+

-

amp

( )

+

-

amp

( )

+

-

amp

( )

+

-

amp

( )

+ +

+

- +

amp +

( ) +

+ + +

+ +

- + +

amp + +

( ) + +

+ +

+

- +

amp +

( ) +

+ + -

+ -

- + -

$amp() + -($

amp

amp

$amp() + -($

()+ -01 234)5

67455 217487+

amp

amp

(

amp)

(

amp

+

amp

+amp

amp

+-

amp

+

amp

(

amp

+

amp

+amp

amp

+-

amp

+

amp

(

amp

+

amp

+amp

amp

+-

amp

+

amp

(

amp

+

amp

+amp

amp

+-

amp

+

amp

(

amp

+

ampamp

+amp

ampamp

+-

ampamp

+

ampamp

(

ampamp

+

amp-

+amp

amp-

+-

amp-

$amp() + -($ 0123 4 567892 7lt1=2

(lt6gt9gt3 A672ltBC

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 915

in the case of the individual corporatecredit default contracts did Berkshireface counterparty r isk as the premiumswere paid quarterly rather than entirely upfront This explains that in some peri-o d s ( i n m a n y a c t u a l l y ) B e r k s h i r e

recorded those high-grade corporatepositions as assets and not l iabil itiesThe expected value of the premiums tob e r e c e i v e d b y B e r k s h i r e w a s s i m p l y higher than the expected value of any default payments to be made by Berkshire

B e r k s h i r e rsquo s d e r i v a t i v e s l i a b i l i t i e s(recorded on the right hand side of thebalance sheet) change for three reasonschanges in the fair value of the deriva-tive (ie gains or losses) new premi-ums collected and new payouts made

When no new premiums or new payoutshave taken place the change in deriva-tives liabilities will be equal to the gains(leading to a decrease in liabilities) orlosses (leading to an increase in liabili-t i e s ) i n c u r r e d b y t h e p o s i t i o n F o rinstance year-end 2008 credit defaultcontract liabilit ies increased by $23 bil-lion with respec t to year-end 2007 Thiswas explained by pretax fair value lossesof $18 bil lion $633 million in new pre-miums and $152 mill ion of loss pay-

m e n t s P r o g r e s s i v e l y e s s e n t i a l l y a l lchanges in derivatives l iabil ities wereexplained by mark-to-market gains orlosses on the puts and credit contractsportfolio as no more premium money wasbeing raised and as new l arge loss pay-ments vanished

As can be seen in Exhibit 5 equity puts liabilities only reached $10 billiona couple of times having been between$6 billion and $8 bill ion for most of thet i m e C r e d i t d e f a u l t l i a b i l i t i e s o n l y

reached $4 billion a couple of times hav-ing been less than $2 billion most of thetime As the corporate credit contractsbegan to expire as investment-gradeexposures turned into net assets (froml a t e 2 0 0 9 o n ) a n d a s h a l f o f t h estatemunicipalities exposure was liq-uidated credit default liabilities naturally nosedived As of Q3 2013 Berkshirersquoscredit liabilities stand at just $470 mil-lion Thatrsquos how much it wou ld cost War-ren Buffett to buy back the contracts and

liquidate the exposure once and for all

Was it worth it

ldquoWe are delighted that we hold th e deriv-atives contracts that we dordquo declaredWarren Buffett in h is 2009 letter to share-holders6 Coming as they did soon afterthe financial cri sis which had led to big losses amid the worst performance everexperienced by the por tfolio these wordsare doubly reassuring as to Berkshirersquosenthusiastic and staunch commitmentto the trade The firm was looki ng for onething substantial and long-lasting floatAs long as col lected prem ium s (bothupfront and quarterly) kept above any pay-ments derived from the derivatives posi-tion Berkshire would be h appy That theoutcome was going to be favorable seemsto have never been in serious doubt In

the 2007 letter Buffett stated ldquoI believethat on premium revenues alone thesecontracts wi ll prove profitable leaving aside what we can earn on t he large sumswe holdrdquo 7 A year later he reiteratedldquoOur expectat ionhellipis that we wi l l dobetter than break even and that the sub-stantial investment income we earnhellipwil lbe f rosting on t he cakerdquo8 As for longevitywell the equity puts and the statemunic-ipal i t ies credit defaul t swaps maturebetween 10 and 45 years after premium

has been collected with no loss paymentby Berkshire taking place if at al l untilthose far away expiration dates

B y y e a r - e n d 2 0 1 1 B e r k s h i r e w a salready dancing the v ictory lap at leastwhen it came to one of the (sizable) com-ponents of the trade

O u r i n s u r a n c e - l i k e d e r i v a t i v e s c o n t r a c t s whereby we pay if various issues included inhigh-yield bond indexes default are coming to a closehellipWe are almost certain to realizea final lsquounderwriting profitrsquo on this portfoliobecause the premiums we received were $34billion and our future losses are apt to beminorhellipThis successful result during a t imeof great credit stress underscores the impor-tance of obtaining a premium that is com-mensurate with the risk9

There was also l itt le doubt that theequity puts play wil l prove handsomely profitable as expressed in the 2012 mis-sive to shareholders

Though itrsquos no sure thing [we] believe it likely that the final liability wil l be considerably lessthan the amount we currently carry on our

books ($75 bil lion) In the meantime we can

42 CORPORATE FINANCE REVIEW NOVEMBERDECEMBER 2013 PRACTICAL MATTERS

BERKSHIRErsquoS

DERIVATIVES

LIABILITIES

(RECORDED ON

THE RIGHT HAND

SIDE OF THE

BALANCE SHEET)

CHANGE FOR

THREE REASONS

CHANGES IN THE

FAIR VALUE OF

THE DERIVATIVE

(IE GAINS OR

LOSSES) NEW

PREMIUMS

COLLECTED

AND NEW

PAYOUTS MADE

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 1015

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 1115

any loss payout and there seem to be noindications of counterparty default on

the quarter ly premium payments Those$93 million annua l fees (plus any upfrontfee) appear to have been entirely freemoney for five long years

The statemunicipalities default con-tracts canrsquot generate a loss payout untiltheir maturity (far far in the future)and while Berkshire had to make goodon $85 billion of t he position the amountpaid to the counterparty is not known(a very rough and almost certainly inex-act approximation may be in t he neigh-

borhood of $400 million) In any caseit canrsquot have been a prohibitive amountgiven that at the time of the unwindingthe total mark-to-market liability on theentire $16 billion port folio was around$950 million Assuming that Berkshireraised around $340 million through thesale of these contracts (as per our cal-culation in the prior secti on) this par-ticular t rade may have been unprofitable

Exhibit 7 provides a description of the evolution of Berkshirersquos derivatives

float (again drawi ng on the companyrsquos

quarterly and annual reports and on ouranalysis for the cost of the s tatemunic-

ipalities portfolio unwinding in 2012this being the only relevant number seem-ingly not having been publicly disclosed)We see that the b enefits have been prett y substant ial so far And the news get e venbetter when we take into account thatbarring any desperate request by a coun-terparty to unwind a trade (togetherwith Berkshirersquos acquiescence to do soand incur the cost of buying back theexposure) no further loss payouts canhappen before expiration of the only two

remaining positions the equity puts andthe statemunicipalities credit defaultobligations that mature in the pleasantly distant 2019ndash2054 period

Another way to analyze the perfor-mance of the trade is by comparing thefloat obtained with the accounting lia-bilities generated In other words com-pare premiums minus payouts with t hemarket cost of liquidating the exposuresHad Berkshire had or wanted to termi-nate the puts and the credit default con-

tracts would the raised premiums (minus

44 CORPORATE FINANCE REVIEW NOVEMBERDECEMBER 2013 PRACTICAL MATTERS

EXHIBIT 6 Buffettrsquos Performance

PublicUS stocks Overall

Berkshire (from Private stock market

Hathaway 13F filings) Holdings performance

Sample 1976ndash2011 1980ndash2011 1984ndash2011 1976ndash2011

Beta 068 077 028 100

Average excess return 1900 1180 960 610

Total volatility 2480 1720 2230 1580

Idiosyncratic volatility 2240 1200 2180 000

Sharpe ration 076 069 043 039

Information ratio 066 056 036 000

Leverage 164 100 100 100

Sub period excess returns

1976ndash1980 4210 3140 7801981ndash1985 2860 2090 1850 430

1986ndash1990 1730 1250 970 540

1991ndash1995 2970 1880 2290 1200

1996ndash2000 1490 1200 880 1180

2001ndash2005 320 220 170 160

2006ndash2011 330 300 230 070

Data from Frazzini A Kabiller D and Pedersen LH Buffetts Alpha (May 3 2012)

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 1215

any loss payments) have been able tocope or would the final t ally have beenway in excess of that Well the evidenceis somewhat mixed unless we assumethat the float led to pretty interesting investment ret urns Exhibi t 8 shows whyWhile the float from the credit contractswould have been in general enough to covertheir liabilit ies that from the puts would

by itself have been widely incapable of doing soFinally we can look at the s ize of t hose

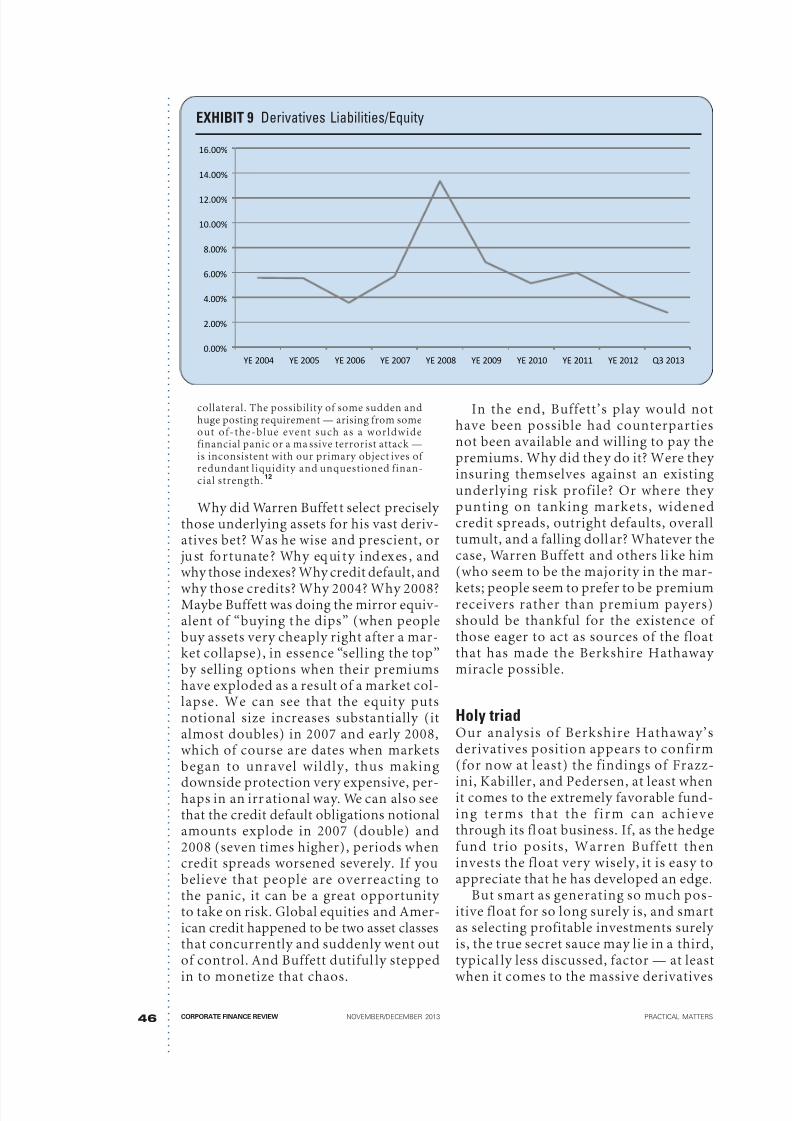

l i a b i l i t i e s w i t h r e g a r d t o B e r k s h i r e rsquosequity capital In other words if thosemark-to-market losses grew too largewould the companyrsquos solvency b e at stakeExhibit 9 provides some guidance I tdoesnrsquot look as if the portfolio gravely threatened Berkshire

Lack of strict collateral requirementswas key for the trade to work and p erform

B erkshire would otherwise not have

entered into the t rades Buffett has referredto derivatives coll ateral as a ldquolethal t hreatrdquothat can sink companies While it is tru ethat by avoiding stringent margin rulesBerkshire agreed to collect less premi-ums on the sold contracts than wouldotherwise have been the case Buffettdeclared at the end of 2010 ldquoThatleftus feeling comfortable during the finan-

cial crisis allowing us in those days to com-mit to some advantageous purchasesForegoing some additional derivativespremiums proved to be well worth itrdquo 11

A year later Buffett made clear t hat as a consequence of the new post-cr isis much-more-demanding industry policies oncollateral his firm would not be entering into new positions

Though our existing contracts have very minorcollateral requirements the rules have changedfor new positionshellip We shun contracts of a ny

type that could require the instant posting of

45PRACTICAL MATTERS NOVEMBERDECEMBER 2013 CORPORATE FINANCE REVIEW

EXHIBIT 8 Liabilities Versus Float ($ Million)

$

amp

() () amp () + () () ()

)-0 1-2 3456782

98 lt8=4-6 3456782

)-0 1-2 gt64

9lt gt64

EXHIBIT 7 The Evolution of Berkshirersquos Derivatives Float

Equity Puts($ mn) Premiums CDS Premiums Cumulative Put Payouts CDS Payouts Float

Up to YE 2007 4500 3200 7700 0 472 7228Up to YE 2008 4900 3833 8733 0 542 8191

Up to YE 2009 4900 3926 8826 0 2442 6384

Up to YE 2010 4900 4019 8919 425 2442 6052

Up to YE 2011 4900 4112 9012 425 2528 6059

Up to YE 2012 4900 4205 9105 425 3005 5676

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 1315

collateral The possibility of some sudden andhuge posting requirement mdash arising from someout of-the -blue e ve nt such as a wor ldwidefinancial panic or a ma ssive terrorist attack mdashis inconsistent with our primary object ives of redundant liquidity and unquestioned finan-cial strength12

Why did Warren Buffet t select precisely those underlying assets for his vast deriv-atives bet Was he wise and prescient or

ju st fo rtunate Why eq ui ty ind ex es andwhy those indexes Why credit default and

why those credits Why 2004 Why 2008Maybe Buffett was doing the mirror equiv-alent of ldquobuying t he dipsrdquo (when peoplebuy assets very cheaply right after a mar-ket collapse) in essence ldquoselling the toprdquoby selling options when their premiumshave exploded as a result of a market col-lapse We can see that the equity putsnotional size increases substantially (italmost doubles) in 2007 and early 2008which of course are dates when marketsbegan to unravel wildly thus making

downside protection very expensive per-haps in an irr ational way We can also seethat the credit default obligations notionalamounts explode in 2007 (double) and2008 (seven times higher) periods whencredit spreads worsened severely If youbelieve that people are overreacting tothe panic it can be a great opportunity to take on risk Global equities and Amer-ican credit happened to be two asset classesthat concurrently and suddenly went outof control And Buffett dutiful ly stepped

in to monetize that chaos

In the end Buffettrsquos play would nothave been possible had counterpartiesnot been available and willing to pay thepremiums Why did the y do it Were they insuring themselves against an existing underlying risk profile Or where they punting on tanking markets widenedcredit spreads outright defaults overalltumult and a falling doll ar Whatever thecase Warren Buffett and others li ke him(who seem to be the majority in the mar-

kets people seem to prefer to be premiumreceivers rather than premium payers)should be thankful for the existence of those eager to act as sources of the floatthat has made the Berkshire Hathaway miracle possible

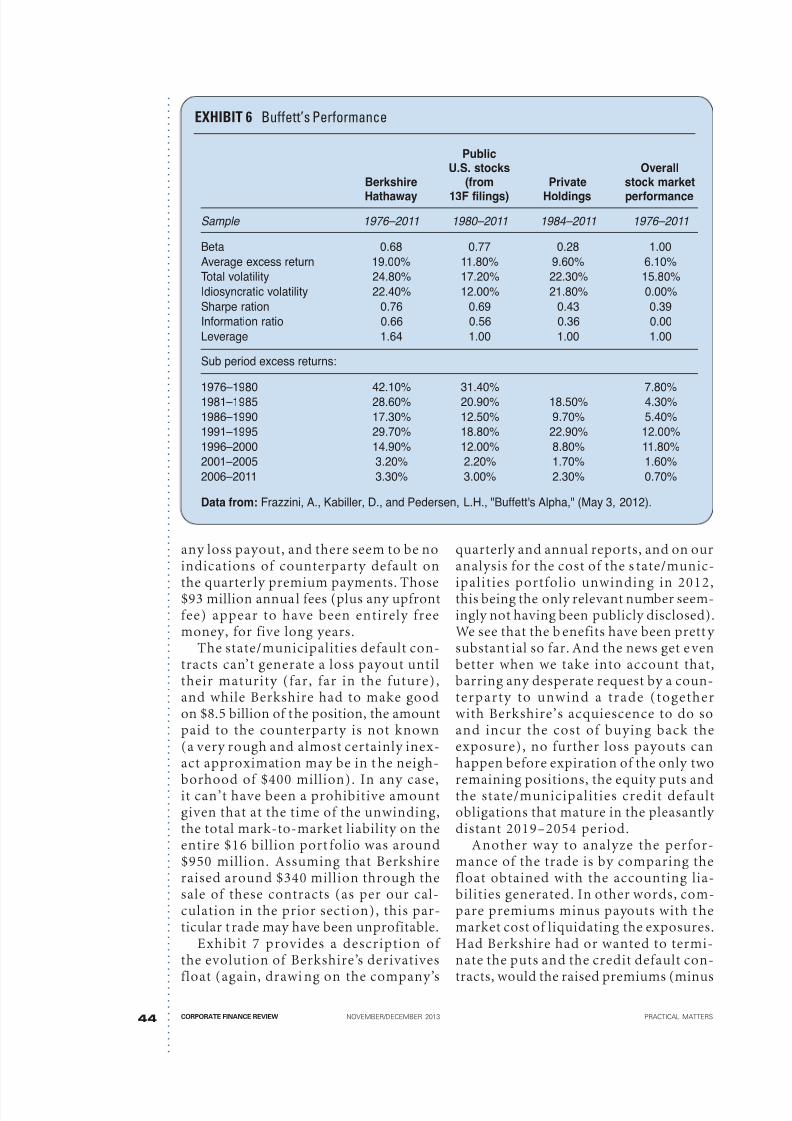

Holy triadOur analysis of Berkshire Hathawayrsquosderivatives position appears to confirm(for now at least) the findings of Frazz-

ini Kabiller and Pedersen at least whenit comes to the extremely favorable fund-i n g t e r m s t h a t t h e f i r m c a n a c h i e v ethrough its fl oat business If as the hedgefund trio posits Warren Buffett theninvests the float very wisely it is easy toappreciate that he has developed an edge

But smart as generating so much pos-itive float for so long surely is and smartas selecting profitable investments surely is the true secret sauce may lie in a thirdtypical ly less discussed factor mdash at least

when it comes to the massive derivatives

46 CORPORATE FINANCE REVIEW NOVEMBERDECEMBER 2013 PRACTICAL MATTERS

EXHIBIT 9 Derivatives LiabilitiesEquity

amp

(

)

)

)amp

)

+ amp + + + - + ( + + ) + )) + ) 0 )0

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 1415

portfolio analyzed in this paper Simply stated Berkshire appears to have enjoyedtremendous and perhaps unique advan-tages when it came to selling the deriv-atives from which the float (and thus theedgersquos foundat ion) comes Without those

advantages in place the whole thing may not have been possible to begin withAnd the true key is that those advan-tages may be reserved for Buffett andmaybe just a handful of other peopleE n j o y i n g t h o s e a d v a n t a g e s i n o t h e rwords can lead to vast competit ive ben-efits

Those three key factors that may nothave been available to all market play-ers are (1) very soft collateral require-ments (2) utter disregard for quarterly

earnings volatility and (3) the ability to find buyers of sizable and often het-erodox contracts Other players may havefaced much more s tr ingent col la tera lrequirements Other players may caremuch more about continuous earningsturbulence Other players may not beable to sell such contracts Buffett is ver y clear about it If he had to f ace ldquonormalrdquocollateral ru les he would not have enteredinto the trades Did he get preferentialtreatment because of who he is Likely

Buffett was willing to sell contracts forless premium just to avoid col la tera lposting since raising premium is all thatmatters his concerns about collateralare obvious With standard collateralrules $40ndash50 billion would have beenat instant risk (and could suddenly sinkmany a firm) Many other investors wouldnot have been able to sell a simi lar deriv-atives portfolio for fear of those expo-sures or for utter lack of resources Thatis a float-generating trade that is pos-

sible and desirable for Buffett to makebecomes impossible and undesirable formany or most others Only Buffett wouldget to enjoy the float and thus the tremen-dous investment edge

The contracts Berksh ire sold were notall ortho dox Buffett placed as much as$40 bil l ion of very long dated at-the-money equity risk Buffett collected $4b i l l i o n o f h i g h - r i s k c r e d i t p r e m i u mupfront when quarterly payments tendto be the norm Some credit contracts had

10ndash45 year maturities with five years

being the norm Loss payouts on severalcontracts can only take place at matu-rity with whenever a credit event ta kesplace being the norm These unorthodox contracts were apparently wildly over-pr iced a f fording B uffett lots of f loat

from the get-go Could anybody enterinto such trades (i e be able to findwill ing buyers) or do you need to beWarren Buffett

As for quarterly earnings volatilitynot everyone may be able or willing tobe so sangui necomplacent Buffett enjoysgod-like stature with his shareholdersand has built a career on long-term focusldquoTemporaryrdquo setbacks including very large ones may thus not t urn them i ntoferocious critics Not everyone may be

shielded from cri ticism i n such a way Of course this is directly linked to the col-lateral issue If you donrsquot face hard col-lateral penalties you can afford to notcare about earnings turbulence

Legend or bustNaturally Buffett could have borrowedlike anybody else and then invested themoney But he want s to bui ld an e dge Itrsquoshard to become a legendary investor if

yo u do what eve r yo ne can do The floatgives him that edge Of course the activ-ities that lead to the generation of f loatcontain the seeds of risk s that may mate-rialize into costs way above those of a sim-ple loan But Berkshire and our analysisseems to confirm this has been master-ful at achieving underwriting profits andthus negative cost funding Float does-nrsquot have to be paid back doesnrsquot imply payment of i nterest and is not debt HadBerkshire in 2004 borrowed $6 billion

(approximately the average annual pos-itive float from the derivatives trade)for 15 years at say 5 percent annualinterest it would have been $105 bil-lion out of pocket by the loanrsquos maturity date So far itrsquos only lost $3 billion onthe derivatives position and barring some surprise no extra cash disburse-ments will take place until 2019hellipif at allThatrsquos a $75 bi llion surplus So the big lesson from Berkshire Hathaway may bethat you must take chances if you want

to a superior investor983150

47PRACTICAL MATTERS NOVEMBERDECEMBER 2013 CORPORATE FINANCE REVIEW

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 1515

NOTES1Frazzini A Kabil ler D and Pedersen LH ldquoBuf-fettrsquos Alphardquo (May 3 2012) (whit e paper )

2Berkshi re Hathaway Inc rsquos annual repo rt (2012) 7Avai lable at httpwwwberkshirehathawaycom 2012ar2012arpdf

3Ibid p 8

4

Berkshire Hathaway Incrsquos sharehold er letter (20 06)17 Available at httpwwwberkshi rehathawaycom letters2006ltrpdf

5Berkshire Hathaway Inc press release (May 2 2008)Avai lable at httpwwwberkshirehathawaycom newsmay0208pdf

6Berkshire Hathaway Incrsquos sharehold er letter (20 09)15 Available a t httpwwwberkshirehat hawaycom letters2009ltrpdf

7Berkshire Hathaway Incrsquos sharehold er letter (20 07)

16 Available at httpwwwberkshirehat hawaycom

letters2007ltrpdf8Berkshire Hathaway Incrsquos sharehold er letter (20 08)

18 Available at httpwwwberkshirehat hawaycom

letters2008ltrpdf9Berkshire Ha thaway Incrsquos share holder l etter (2011)

17 Available at httpwwwberksh irehath awaycom

letters2011ltrpdf10

Berkshire Hat haway Incrsquos shareholder letter (2012)

16 Available at httpwwwberkshirehat hawaycom

letters2012ltrpdf11

Berkshir e Hathaway Incrsquos annual re port (2010) 20

Avai lable at httpwwwberkshirehathawaycom

2010ar2010arpdf12

Op cit note 9

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 215

35PRACTICAL MATTERS NOVEMBERDECEMBER 2013 CORPORATE FINANCE REVIEW

$2787 bi l l ion a decade la ter and to$7312 billi on by 2012 (again these num-

bers may not include derivatives-gen-erated float only insurance-generatedfloat) Thatrsquos a lot of very cheap (evennegative cost) funding

Very few other insurers seem to beable to achieve those ty pes of outcomesWhile Berkshire has generated an under-w r i t i n g p r o f i t f o r t h e p a s t 1 0 y e a r sstraight competitors donrsquot appear to bea b l e t o b o a s t s i m i l a r l y r o s y r e s u l t s(reporting in fact underwriting lossesas a whole) Listen to Buffett explain it

Let me emphasize that cost-free float is not anoutcome to be expected for the [insurance]industry as a whole There is very litt le lsquoBerk-shire-qualityrsquo f loat existing in the insuranceworld In 37 of the 45 years ending in 2011 theindustr yrsquos premiums have been inadequate tocover claims plus expenses3

Berkshirersquos strategy has been lab eledas ldquobetting again st Bet ardquo after the famousinvestment risk measurement variableYou buy low risk ( ldquolow Betardquo) assets a nd

yo u sel l high r isk (ldquohigh B etardquo) ones

hoping that the former will do well whi le

the latter do b adly Insurance and rein-surance policies including on very exotic

underlyings are a way of making thatbet Derivatives are another While many would be expected to be familiar with Berk-shirersquos insurance forays they may be lessso with his derivatives trades In thisarticle we focus on this less-known leg of Warren Buffettrsquos search for float

Derivatives gamesBerkshire Hathaway began selli ng equity index put options and credit protection

through credit default obligations (creditdefault swaps and the like) in 2004 Atthe time Berkshire Hathaway already held a very substantial derivatives port-folio legacy of the acquisition of rein-surer General Re Berkshire had embarkedon a strategy to wind down the GeneralRe derivatives book which included a myr-iad of products and underlying assetsmore than 23000 contracts outstand-ing For instance as of December 312003 Berkshirersquos derivatives portfolio

included $11 billion in foreign currency

EXHIBIT 1 Buffettrsquos Cost of Leverage The Case of His Insurance Float

Fraction Averageof years with cost of funds

negative cost (truncated) Spread over benchmark rates

Fed Funds 1-Month 6-Month 10-year T-Bill Rate Libor Libor Bond

1976ndash1980 079 167 ndash459 ndash565 ndash576

1981ndash1985 020 1095 110 ndash027 ndash128

1986ndash1990 000 307 ndash356 ndash461 ndash480 ndash490 ndash530

1991ndash1995 060 221 ndash200 ndash224 ndash246 ndash271 ndash464

1996ndash2000 060 236 ndash270 ndash310 ndash333 ndash348 ndash356

2001ndash2005 060 129 ndash082 ndash096 ndash105 ndash119 ndash311

2006ndash2011 100 -400 -584 ndash606 ndash629 ndash659 ndash767

Full Sample 060 220 ndash309 ndash381 ndash369 ndash388 ndash480

In years when cost of funds is reported as ldquoless than zerordquo and no numerical value is available cost of

funds is set to zero

Data from Frazzini A Kabiller D and Pedersen LH Buffetts Alpha (May 3 2012) The data are hand-

collected from Buffetts comment in Berkshire Hathaways annual reports Rates are annulaized in percent

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 315

36 CORPORATE FINANCE REVIEW NOVEMBERDECEMBER 2013 PRACTICAL MATTERS

forwards $333 bil l ion in interest rateand currency swaps and $102 billion ininterest rate and currency options Thesecontracts (both long and short expo-sures) generated assets and liabilities insimilar amounts (about $15 billion each$10 billion if you allow for counterparty nettin g) A year later the legacy p ortfoliohad already been wound down signifi-cantly with swaps notional (including now credit products as well as interest rates-currency) just at $153 billion and inter-est rates-currency options just at $35billion By December 31 2005 with just740 contracts left outstanding the respec-tive numbers were $44 billion and $14billion (currency forwards remained ataround $13 billion in size) by Decem-

ber 2006 Berkshirersquos derivatives book

had become dominated by the equity index puts and credit default obligationspositions with interest rates-currency swaps at $10 billion interest rates-cur-rency options at $4 bill ion and foreigncurrency forwards at $1 billion By thebeginning of 200 8 the legacy portfoliohad been essentially liquidated and essen-tially a ll of B erkshirersquos derivatives bookconsisted of the equity puts and the creditobligations The unwinding had beencostly with losses of more than $400million by year-end 2005

The equity puts and credit defaul tobligations positions were built slowly at first and more intensely later on By

ye ar- end 2004 the not ion al size of theput contracts was around $4 bi l l ion

growing to $14 billion a year later and

EXHIBIT 2 The Evolution of the Notional Size of the Puts and the Credit Contracts

$

$

amp

amp

()

()

()

+

$

-

-

amp

-

()

-

$

amp

()

$

$

$

amp

$

()

$

$

$$

$$

amp

$$

()

$$

$

$

$

amp

$

()

$

$

$amp

$amp

amp

$amp

$amp ()+ - )ampamp)$ )0123 4025

678912 8lt0=2 gt=1ltABC5

$

amp

$

amp

()

()

()

+

()

amp

-

-

-

()

-

()

()

()

ampamp() + -amp( 012 (0345 6753839

675005lt4 =gtgtltA3

012 (0345 B =gtgtltA3

CAltA39DE70F0lt40G39

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 415

37PRACTICAL MATTERS NOVEMBERDECEMBER 2013 CORPORATE FINANCE REVIEW

to $21 billion by December 2006 Theposition reached its pinnacle notional sizeof $35ndash40 bil lion in late 2007 to early 2008and kept more or less constant at that levelfrom then on (save for a smallish unwind-ing several years later) Notional sizes

expressed in dollars take into accountcurrency exchange rates

The notional size of t he credit defaultobligations was $28 bil lion by year-end2005 $25 billion a year later and $46bil l ion in December 2007 Up to thatpoint Berkshire had sold protection only o n A m e r i c a n h i g h - y i e l d c o r p o r a t eindexes (about 100 names per contract)From 2008 the company not only sig-nificantly ramped up such act ivity butalso began to sel l protection on indi-

v i d u a l c o r p o r a t e n a m e s a n d o nstatemunicipal i t ies with the conse-quent drastic increase in total notionalamounts which reached a high of $30 bil-lion by year-end 2008 (sizes decreasedfrom that point due to a combination of contract expirations and cancellationsall the way to less than $10 billion by late 2013 essentially all exposures today come exclusively from the statemunic-ipalities contracts)

As of year-end 2006 Berkshire had

sold 62 equity puts and credit defaultcontracts this number went up to 94 a

ye ar lat er and to 251 by ye ar- end 2008(down to 203 by year-end 2010 follow-ing the expiration of the first contractssome unwindings and the fact that nonew contracts were being writ ten) Thelast equity put contracts were sold inFebruary 2008 The last credit contractswere written in February 2009 (just onenew contract)

Exhibit 2 displays the evolution of the

notional size of the puts and the creditcontracts The equity index puts wereEuropean (can only be exercised at matu-rity) were struck at-the-money (thusaffording a very tasty premium for Berk-shire as these options are very close tohaving positive intrinsic value) werew r i t t e n o n f o u r i n t e r n a t i o n a l e q u i t y indexes (SampP 50 0 FTSE 100 Euro Stoxx 50 and Nikkei 225) and had the fol-lowing expiration dates between Sep-t e m b e r 2 0 1 9 a n d J a n u a r y 2 0 2 8 ( t h e

weighted average life of all put contracts

was approximately 75 years at Septem-ber 30 2013)

Originally 47 put contracts were soldgenerating $49 billi on upfront premiumThe maximum possible payment fromBerkshire on these contracts equals theputsrsquo notional s ize (currently around$32 bil l ion) but this would only takeplace at contract expiration and only if all the indexes reach a value of zero att h a t t i m e T h e l i k e l i h o o d o f t h a t i sseverely limited Were Berk shire forcedto make payments equal to $49 billionit would break even on the puts (plusany investment returns on the float) A25 percent drop in all the equity indexesby expiration date would yield a losspayout of around $8 billion at currentforeign exchange rates

I n Q2 2009 B erkshire agreed withcounterparties to amend six equity putcontracts reducing maturities by between35 and 9 5 years (br inging the tota lweighted average maturity of the puts port-folio from 13 to 12 years) Strike priceson those contracts were reduced between29 percent and 39 percent Finally theaggregate notional amount of three of thosecontracts increased by $160 m il l ionThese amendments were cost-free (nomoney changed hands) In Q4 2010 eightequity index put contracts ($43 billionnotional maturities between 2021 and2028) were terminated (at the instigationo f t h e c o u nt e r p a r t y ) t h e u n w i n d i n g required Berkshire to pay $425 millionfor a net gain of $222 million mdash as ithad originally received $647 million inpremium

All corporate credit default contracts(both high-y ield and investment grade)

expire in Q4 2013 a significant portionof high-yield contracts expired in Q42012 B erkshire is l iable for payoutswhenever a credit event takes p lace H igh-yie ld contract expirat ion datesranged from September 2009 to Decem-ber 2013 Individual corporate default con-tracts had f ive-year maturities and werereferenced to about 40 different namesBerkshire stopped selling individual cor-porate credit default contracts from 2009on as dealers began ask ing for stringent

collateral

BERKSHIRE

STOPPED

SELLING

INDIVIDUAL

CORPORATE

CREDIT DEFAULT

CONTRACTS

FROM 2009 ON

AS DEALERS

BEGAN ASKING

FOR STRINGENT

COLLATERAL

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 515

Premiums received upfront from thehigh-yield credit contracts totaled $34billion payouts on those contracts hadtotaled $26 billion by Q3 2013 Premi-ums from individual corporate creditdefault contracts are paid quarterly ($93million a year) Berkshire assumes that thefinal underwrit ing profit (premiums raisedminus payouts) from corporate creditcontracts will be around $1 billion whenthey expire by year-end 2013 having enjoyed on average annual $2 billion float

Statemunicipalities credit contractsexpire between 2019 and 2054 (about500 underlying debt issues) Any poten-tial loss payments cannot be settled untilexpiration We found no specific data on the amount of the (upfront) premi-ums received by Berkshire from selling this risk but we can make an informedapproximation At year-end 20 08 Berk-shire announced that the total premium

raised from selling the high-y ield defaultcontracts had been $34 billion A yearearlier the announced numb er had been$32 billi on This implies new premiumsof $02 billion in 2008 At the same timewe know that the individual corporatecontracts that were first sold in 2008implied annual premiums of $93 mil-lion That makes it $293 million in new p r e m i u m s f o r 2 0 0 8 S i n c e B e r k s h i r ereported in its 2008 annual report thatit had raised $633 million that year in new

premiums from credit default obliga-

tions we may be al lowed to concludethat the statemunicipalities contractswere sold for some $340 million ( only onecredit default contract was sold after2008 I donrsquot know which of the threeunderlying risk categories that last con-tract was referenced to) In August 2 012$825 billion of the statemunicipalitiesposition were terminated (apparentlyt h e o r i g i n a l c o u n t e r p a r t y h a d b e e nLehman B rothers and Lehm anrsquos l iq-uidators were eager to unwind the tradewhich was heavily in t heir favor thus thecontract cancellations may not neces-s a r i l y i m p l y a n e g a t i v e v i e w o f t h estatemunicipalities market on the partof Berkshire) I very roughly assume thatthe cost of this unwinding may have beenaround $475 million or the ldquoapproxi-materdquo size of the li abilities generated by these contracts at the time

Loss payout amounts on the credit

default obligations are subject to indi-vidual and aggregate limits (for instanceof around $5 billion in the case of the high-

y ield defau lt con tracts) and pay mentobligations are on a first-loss basis oron an aggregate-deductible basis

With limited exceptions Berkshire hasnot been required to post collateral How-ever were it to suffer a rating dow ngradeit would have to post an additional $11billion See Exhibit 3 for a description of collateral postings throughout In 2011 Berk-

shire announced a big change in deriva-

38 CORPORATE FINANCE REVIEW NOVEMBERDECEMBER 2013 PRACTICAL MATTERS

EXHIBIT 3 Description of Collateral Postings

$

amp

() + -

() + -

amp

() +

0

() + -

0

() + -

() + -

() + -

() + 1

1

$amp$ )+- 01

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 615

tives collateral requirementspolicies by the financial industr y making it now unac-ceptable for the company to enter intonew major derivatives contracts

Besides the attainment of a lot of extra float (some $7ndash8 bill ion for several years

some $6 billion for a lot of years) anotherkey reason for entering into these par-t i c u l a r d e r i v a t i v e s p o s i t i o n s w a s t h ebelief that they were vastly overpricedThat is Berkshire was being given thechance to collect much more money fromselling the risk than it should accord-ing to Berkshire If you look at the equity puts the premium at way over 10 per-cent of notional amount certain ly lookstasty (not surprising g iven the long matu-rities and the at-the-money strike) This

is how Buffett at year-end 2006 pre-emptively tried to address any queries hisshareholders may have about the factthat he had been se l l ing such a largederivatives por tfolio (whi ch as we knowwas only about to get even larger)

The answer is that derivat ives just like stocksa n d b o n d s a r e s o m e t i m e s w i l d l y m i s -pr ice dhellipThough we wil l e xpe r ie nce losse sfrom time to ti me we are likely to continue toearn mdash overall mdash significant profits from mis-priced derivatives4

The portfolio selected by Berkshireto short had one highly intriguing char-acteris tic It was for the most part devoidof counterparty r isk Since premiumson the equity puts the high-yield cor-p o r a t e c r e d i t d e f a u l t s w a p s a n d t h estatemunicipalities credit default oblig-ations were received upfront Berkshirecould not b e ldquostiffedrdquo any money on th esecontracts Only in the case of the indi-vidual high- grade corporate credit defaulto b l i g a t i o n s w a s c o u n t e r p a r t y r i s k

involved as premiums were receivedquarterly but this position was just a small fraction of the total trade If Berk-shirersquos t rading counterpar ts went brokeor moved to a far away island the firmwould suffer almost no pain Given theintense focus on counterpart y risk afterthe financial cri sis this is no small feat

Berkshirersquos roller coasterHow did Buffettrsquos derivatives play evolve

Well itrsquos been qu ite a r ide thatrsquos for sure

Lots of ups and downs in gains and lossesGiven that Berkshire must account for thechanges in the market (fair) value of t hederivatives in its income statement thoseups and downs have impacted reportedearnings on a continuous bas is And

given that the value of derivatives mustbe accounted as either assets or liabili-ties on the balance sheet Berkshirersquoscapital ratios and perception of the firmas safe and sound (these derivatives hap-pened to be liabilities essentially all thetime since they mostly implied futurepotential obligations only from Berk-shire to its counterparties and not vi ceversa) could also be affected

Such chute-the-chute is the unavoid-able price to pay when one chooses to s ell

a lot of long-term and varied derivativesrisk However in this case two factorswere present that made it much morebearable than i t might have been forother firms First and crucially and aswe mentioned earl ier Berkshi re got away with very lig ht collateral terms at initi-ation of the contracts Many a firm hasb e e n s u n k b e c a u s e t h e m a r k e t w e n tagainst them increasing their liabilitiesand drastically enhancing margin require-ments until there was no more collat-

eral available to post up and liquidationwas the next sad step Thanks to thepreferential t reatment obtained Berkshirecould sell all that equit y currency andcredit r isk safe in the knowledge thatany potential future margin call wouldbe of a minimal size Collateral couldnot s ink Berkshire making the tradesmuch more attractive and probably evenpla in feas ible (B erkshire would quiteprobably not have sold the portfolio hadcollateral requirements been stringent)

Apparently the most Berkshire has hadto post during the life of the trade was$17 bil l ion at some point during theworst of the 2008 financial crisis Thisis money that still continues to producea return for Berkshire while it is being held as a guarantee

Second Warren Buffett doesnrsquot seemto care at all about interim earnings orbalance sheet volatility (the lack of strin-gent collateral requirements possibly plays a role here) repeatedly saying so

to his shareholders He firmly believes

39PRACTICAL MATTERS NOVEMBERDECEMBER 2013 CORPORATE FINANCE REVIEW

THE PORTFOLIO

SELECTED BY

BERKSHIRE TO

SHORT HAD

ONE HIGHLY

INTRIGUING

CHARACTERISTIC

IT WAS FOR

THE MOST

PART DEVOID OF

COUNTERPARTY

RISK

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 715

that the trades will in the end generatepositive float and thatrsquos what tr uly countsHey thatrsquos why they were put on in thefirst place free real money for the firmwho cares about some collateral-light unre-alized tu rbulence on the side Not War-

ren Buffett certainly

Our derivative posit ion will sometimes causelarge swings in reported earnings even though[we] might believe the intrinsic value of thesepositions has changed little [We] will not bebothered by these swings mdash even though they could easily amount to $1 billion or more ina quarter mdash and we hope [shareholders] wonrsquoteitherhellipIn our catastrophe insurance busi-ness we are always ready to trade increasedvolatility in reported earnings in the short runfor greater gains in net worth in the long runThis is our philosophy in derivatives as well5

The market value of B erskhirersquos deriv-atives portfolio would be impacted by several key variables In the case of theputs Berkshire would suffer setbacks if equity prices fell if equity volatility shotup if the dollar dropped in va lue versusthe yen euro or pound and if interestrates went down It would make gains if the opposite moves took place and also

just fro m t he p as sag e of time In the c as eof the credit default contracts Berskhirewould suffer losses if American corpo-

r a t e a n d s t a t e m u n i c i p a l i t i e s c r e d i tspreads shot up and (in the case of a few contracts) if the counterparty defaultedor looked close to defaulting

As these variables fluctuated signifi-cantly during the life of these contractsBerkshire experienced significant tur-bulence in mark-to-market derivativesgains and losses as well as on the port-foliorsquos liabilit ies And given that the port -folio was quite sizeable and that some of those gains and losses could be large

t h e t u r b u l e n c e s o m e t i m e s h a d a b i g impact on Berkshirersquos overall reportedearnings Exhibit 4 details t he evolutiono f t h e g a i n s l o s s e s l i a b i l i t i e s a n dnotional amounts The information comesfrom Berkshirersquos quarterly and annualreports and while thorough care hasbeen taken to collect the data accuratelys o m e e r r o r s o r o m i s s i o n s m a y b einevitable Detailed info on the puts andcredit contracts is only available on anannual basis from 2006 and on a quar-

terly basis from 2008

Letrsquos start w ith gains and losses (partof the companyrsquos income statement)While 2006 and 2007 were re lat ive ly placid (with the exception of Q4 2007)2 0 0 8 h a s b y f a r b e e n t h e w o r s t - p e r -forming year wit h a combined account-

ing setback of $6 8 billion Since by thattime unlike in previous years the putsand the credit contracts comprised essen-tially Berkshirersquos entire derivatives port -folio from that point on gains and losseson the former almost exactly matchedoverall derivatives gains and losses 2009was the best year ($36 billion gain ) inspite of a horrible Q 1 2010 saw a mod-est gain of $420 million notwithstand-i n g a $ 2 1 m i l l i o n l o s s i n Q 2 2 0 1 1was horrible mdash a $2 bill ion setback Mar-

kets rebounded in 2012 leading to a$19 billion gain So far 2013 has beengreat with a cumulative $2 billion gainSince 2008 the portfolio yielded gainsin excess of $1 billion on seven quar-ters and losses in excess of $1 billionalso on seven occasions Gains above$2 billion took place three times lossesabove $2 billion also three times

These gainslosses had on occasiona big impact on B erkshirersquos overall prof-its For instance Berkshire barely made

any money in Q4 2008 (just a t iny $140million in pretax earni ngs a 90 percentdecline with regards to the previous quar-ter) and the massive $45 billion deriv-atives loss surely had something to do withit The firmrsquos entire pretax earnings for2008 at just $75 billion were only 37percent of 2007rsquos figure the $68 bi llionderivatives debacle contributed might-ily to that sharp decline (ie withoutthe derivatives no such sharp declinein profitabilit y) To be fair derivatives

gains have also contributed to signif icantincreases in profits and even to the merepresence of such increase as in Q4 2010when overall earnings grew by less than$2 billion coincidental with a deriva-tives gain of $23 bil l ion or as in Q42 0 1 2 ( $ 8 0 0 m i l l i o n a n d $ 2 1 b i l l i o n respectively)

The derivatives portfolio could withminor exceptions represent only a lia-bility for B erkshire given that any pay-ments can only originate from the firm

(and not from its counterparties) Only

40 CORPORATE FINANCE REVIEW NOVEMBERDECEMBER 2013 PRACTICAL MATTERS

BERKSHIRE

EXPERIENCED

SIGNIFICANT

TURBULENCE

IN MARK-TO-

MARKET

DERIVATIVES

GAINS AND

LOSSES AS

WELL AS ON THE

PORTFOLIOrsquoS

LIABILITIES

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 815

41PRACTICAL MATTERS NOVEMBERDECEMBER 2013 CORPORATE FINANCE REVIEW

EXHIBIT 4 GainsLosses

amp

(

)

)

(

amp

+

(

+

(

-)

(

-(

(

-

(

-amp

(

+

(

-)

(

-(

(

-

(

-amp

(

+

(

-)

()

-(

()

-

()

-amp

()

+

()

-)

())

-(

())

-

())

-amp

())

+

())

-)

()(

-(

()(

-

()(

-amp

()(

+

()(

-)

()

-(

()

-

()

$amp() + -($

+01234 5136 78923 9lt=1gt3 gt2A=BCD6

amp

amp

( ) amp

+

-

amp

( )

+

-

amp

( )

+

-

amp

( )

+

-

amp

( )

+

-

amp

( )

+ +

+

- +

amp +

( ) +

+ + +

+ +

- + +

amp + +

( ) + +

+ +

+

- +

amp +

( ) +

+ + -

+ -

- + -

$amp() + -($

amp

amp

$amp() + -($

()+ -01 234)5

67455 217487+

amp

amp

(

amp)

(

amp

+

amp

+amp

amp

+-

amp

+

amp

(

amp

+

amp

+amp

amp

+-

amp

+

amp

(

amp

+

amp

+amp

amp

+-

amp

+

amp

(

amp

+

amp

+amp

amp

+-

amp

+

amp

(

amp

+

ampamp

+amp

ampamp

+-

ampamp

+

ampamp

(

ampamp

+

amp-

+amp

amp-

+-

amp-

$amp() + -($ 0123 4 567892 7lt1=2

(lt6gt9gt3 A672ltBC

8112019 Triana - Why Does Warren Buffett Make Money

httpslidepdfcomreaderfulltriana-why-does-warren-buffett-make-money 915

in the case of the individual corporatecredit default contracts did Berkshireface counterparty r isk as the premiumswere paid quarterly rather than entirely upfront This explains that in some peri-o d s ( i n m a n y a c t u a l l y ) B e r k s h i r e

recorded those high-grade corporatepositions as assets and not l iabil itiesThe expected value of the premiums tob e r e c e i v e d b y B e r k s h i r e w a s s i m p l y higher than the expected value of any default payments to be made by Berkshire

B e r k s h i r e rsquo s d e r i v a t i v e s l i a b i l i t i e s(recorded on the right hand side of thebalance sheet) change for three reasonschanges in the fair value of the deriva-tive (ie gains or losses) new premi-ums collected and new payouts made

When no new premiums or new payoutshave taken place the change in deriva-tives liabilities will be equal to the gains(leading to a decrease in liabilities) orlosses (leading to an increase in liabili-t i e s ) i n c u r r e d b y t h e p o s i t i o n F o rinstance year-end 2008 credit defaultcontract liabilit ies increased by $23 bil-lion with respec t to year-end 2007 Thiswas explained by pretax fair value lossesof $18 bil lion $633 million in new pre-miums and $152 mill ion of loss pay-

m e n t s P r o g r e s s i v e l y e s s e n t i a l l y a l lchanges in derivatives l iabil ities wereexplained by mark-to-market gains orlosses on the puts and credit contractsportfolio as no more premium money wasbeing raised and as new l arge loss pay-ments vanished

As can be seen in Exhibit 5 equity puts liabilities only reached $10 billiona couple of times having been between$6 billion and $8 bill ion for most of thet i m e C r e d i t d e f a u l t l i a b i l i t i e s o n l y

reached $4 billion a couple of times hav-ing been less than $2 billion most of thetime As the corporate credit contractsbegan to expire as investment-gradeexposures turned into net assets (froml a t e 2 0 0 9 o n ) a n d a s h a l f o f t h estatemunicipalities exposure was liq-uidated credit default liabilities naturally nosedived As of Q3 2013 Berkshirersquoscredit liabilities stand at just $470 mil-lion Thatrsquos how much it wou ld cost War-ren Buffett to buy back the contracts and

liquidate the exposure once and for all

Was it worth it