trends in out sourcing in investment management industry prepared by rod homer & stewart copland...

TRANSCRIPT

Trends in Out Sourcing in

Investment Management Industry

Prepared by Rod Homer & Stewart Copland for

Securities & Investment Institute

2© Etheios Group Limited 2006

Your presenters today

• Rod Homer, Chief Executive

• Stewart Copland, Consulting Director

Seasoned practitioners

3© Etheios Group Limited 2006

Agenda

• Introductions• Overview of the Out Sourcing Market• Overview of Off Shore Scene• Major users of Out Source Services• The Indian Situation• South Africa, China et al• Predictions & Conclusions

4© Etheios Group Limited 2006

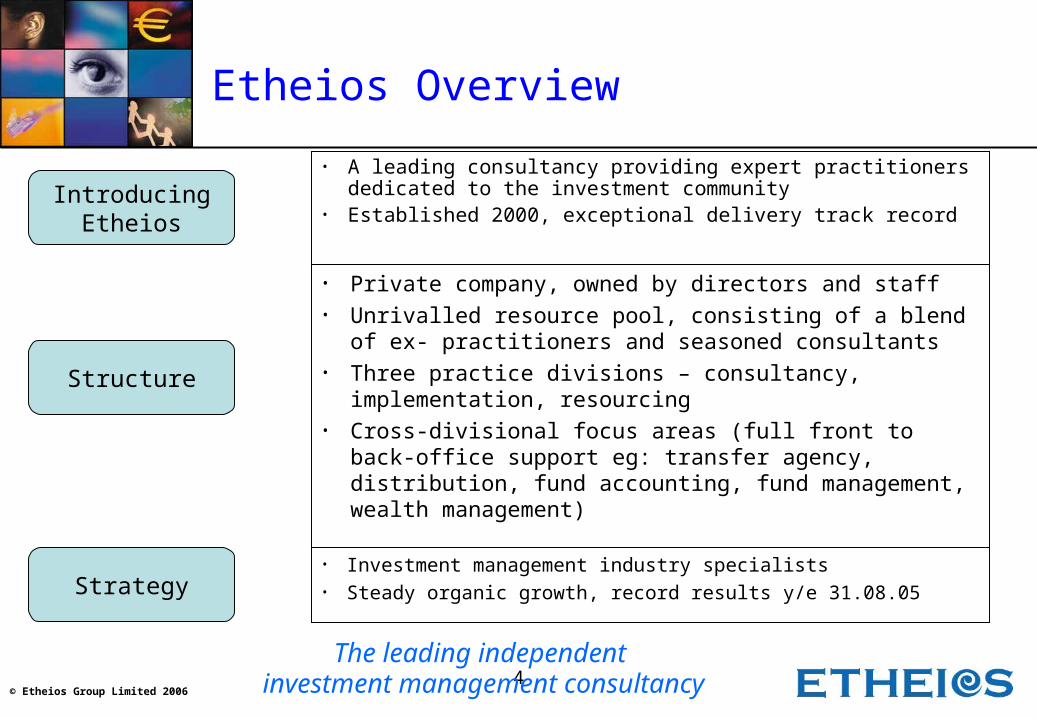

Etheios Overview

• A leading consultancy providing expert practitioners dedicated to the investment community

• Established 2000, exceptional delivery track recordIntroducing

Etheios

Structure

Strategy

• Private company, owned by directors and staff• Unrivalled resource pool, consisting of a blend of

ex- practitioners and seasoned consultants• Three practice divisions – consultancy,

implementation, resourcing • Cross-divisional focus areas (full front to back-office

support eg: transfer agency, distribution, fund accounting, fund management, wealth management)

• Investment management industry specialists• Steady organic growth, record results y/e 31.08.05

The leading independent investment management consultancy

5© Etheios Group Limited 2006

1st Generation Outsourcing New Breed Outsourcing

HR Outsourcing Payroll Benefits Administration Participant Recordkeeping

Funct

ion

al Sco

pe

Time

End-Client ReportingPaper StatementsWeb SolutionsPrivate Label

Accounting Separate Managed Accounts Vehicle Accounting Performance Measurement Composite Generation Post-Trade Compliance Risk Measurement

Investment Operations TPC Management Fail Management & Broker Claims Reconciliation Global Asset Servicing MIS Tax Reclaims

Trade Automation & Routing Message Transformation & Concentrator Trade Matching Trade Enrichment Data Management MIS

Fund Services Mutual Fund Accounting Mutual Fund Administration Master Trust/Master Custody Performance Measurement Transfer Agency

Asset Processing & Servicing Global Custody Clearance Cash Management Securities Lending Income Collection & Corporate Actions

Outsourcing evolution

Source: The Bank of New York

6© Etheios Group Limited 2006

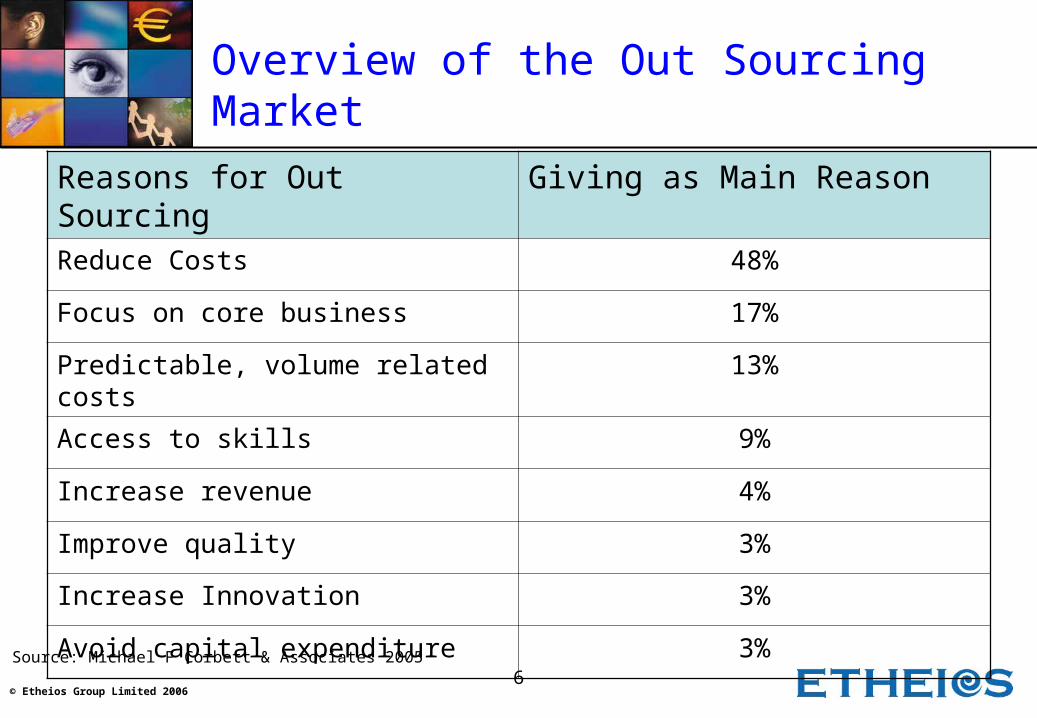

Overview of the Out Sourcing Market

Reasons for Out Sourcing Giving as Main Reason

Reduce Costs 48%

Focus on core business 17%

Predictable, volume related costs 13%

Access to skills 9%

Increase revenue 4%

Improve quality 3%

Increase Innovation 3%

Avoid capital expenditure 3%

Source: Michael F Corbett & Associates 2005

7© Etheios Group Limited 2006

Where did it all go wrong?

Schroders cancels outsourcing deal1 July 2005

Outsourcing savings are unrealistic - Cost savings actually average just 15 per cent, study finds13 April 2006

New study shows that the benefits of IT outsourcing are real1 May 2006

JPMorgan Chase cancels IBM outsourcing contract15 September 2004

F&C fails to agree terms with Mellon1 November 2005

8© Etheios Group Limited 2006

Reasons given for not Out Sourcing

The most common reasons for retaining services in house after considering out sourcing are:

• Loss of control – Dependency on supplier when introducing new products or services

may constrain speed to market– Less flexibility to allocate resources to new projects– Competing for prioritisation for new developments and project

resources• Security

– Unauthorised release of data– Business continuity plans

• Regulatory– Less stringent local regimes– Incompatibility with latest EU directives

9© Etheios Group Limited 2006

Benefits of Out Sourcing

IBM examined 56 out source contracts and reported that significant benefits were achieved:

• 11.8% higher earnings growth than the sector median• 9.9% reduction in expenses compared with sector median• 8.6% increase in RoA • swing of 16.1% from their pre-out source position of 7.5% lower

than median.

10© Etheios Group Limited 2006

Benefits of Out Sourcing

Size Front Office Middle/Back Office

IT

Small – AUM €11bn

6.0 bp 3.7 1.9

Medium – AUM €44bn

5.3 5.0 2.6

Large –AUM €102bn

3.9 2.4 1.4

Source: McKinsey 2003

Typical costs for in-house operations and support

11© Etheios Group Limited 2006

Benefits of Out Sourcing

Size Front Office Middle/Back Office

IT

Small – AUM €11bn

6.0 bp – 18%

3.7 – 35% 1.9 – 26%

Medium – AUM €44bn

5.3 – 8% 5.0 – 52% 2.6 – 46%

Large –AUM €102bn

3.9 – 8% 2.4 – 52% 1.4 – 46%

Source: McKinsey 003

Typical savings from out sourcing operations and support

12© Etheios Group Limited 2006

The UK Market - Trends

• Continuing pressure on fund managers’ margins and increasing public awareness of costs.

• Consolidation of product providers has not met predictions and may have some way to go.

• Increased penetration by volume providers.• Extended penetration of outsourcing to middle

office.• Niche suppliers making inroads. • Structured products threat.• New entrants to 3rd Party Administration.

13© Etheios Group Limited 2006

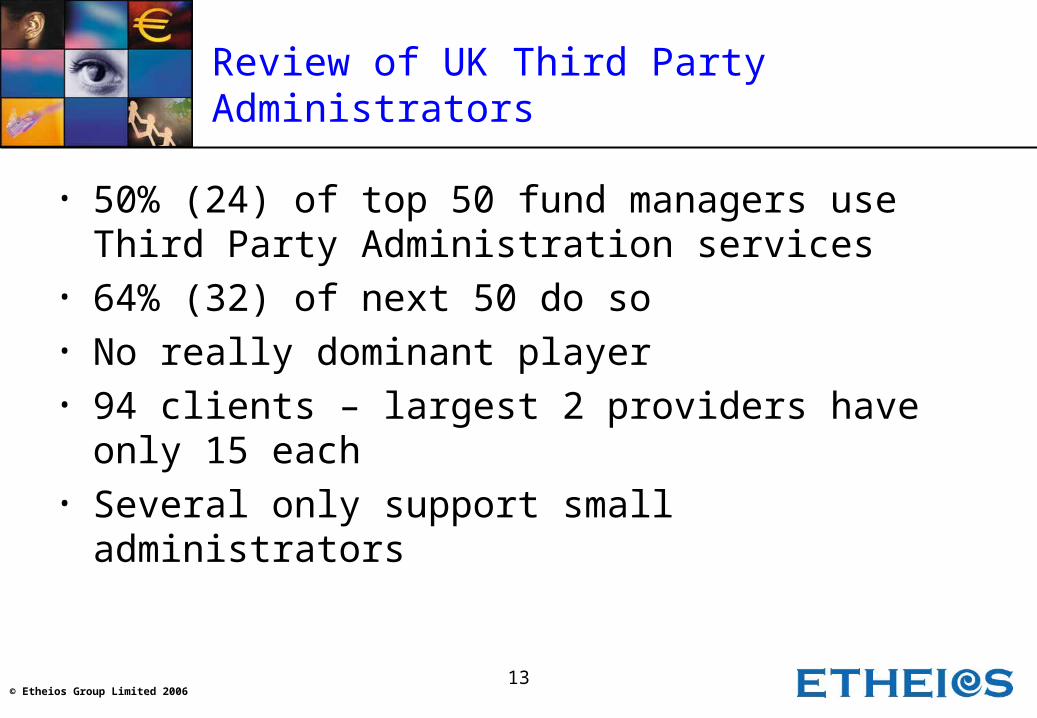

Review of UK Third Party Administrators

• 50% (24) of top 50 fund managers use Third Party Administration services

• 64% (32) of next 50 do so• No really dominant player• 94 clients – largest 2 providers have only 15

each• Several only support small administrators

14© Etheios Group Limited 2006

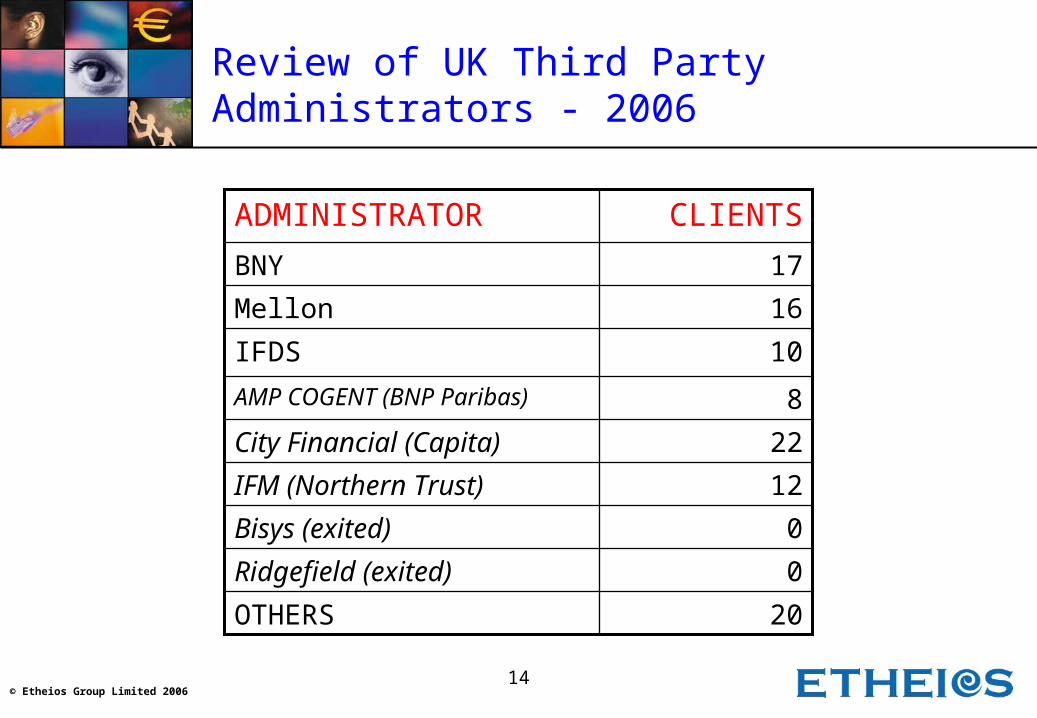

Review of UK Third Party Administrators - 2006

0Bisys (exited)

12IFM (Northern Trust)

22City Financial (Capita)

8AMP COGENT (BNP Paribas)

0Ridgefield (exited)

20OTHERS

10IFDS

16Mellon

17BNY

CLIENTSADMINISTRATOR

15© Etheios Group Limited 2006

• Continued consolidation• Established Continental operators have

expressed interest in bringing their services to the UK market

• Service providers are not immune from world economics

UK TPA trends

16© Etheios Group Limited 2006

Overview of European Market

• Growth in funds under management forecast to exceed 10% p.a. in all European markets and average 14%

• Banks still dominate distribution

• On-line distribution growing rapidly

• Considerable potential for further changes in distribution and 3rd party product providers

17© Etheios Group Limited 2006

Where to Out Source

High

LowHigh

Off-shore – a foreign location with low cost base and access to skills supported by technology providing equal or improved quality of service at lower cost.

Near-shore – nearby location with common/similar language, culture and business environment provides convenience of access to compensate for lower cost savings.

On-shore – same country as client with mix of in-house and external service provision. Low risk but minimal cost savings. Used to gain access to improved process, technology or to solve an internal problem.

18© Etheios Group Limited 2006

Off Shore Locations

Country IT BPO

Brazil $200m

Canada $8.2bn $5.5bn

China $700m $300m

Czech Republic

$60m $40m

Hungary $50m $25m

India £12.2bn $5,2bn

Ireland $2.2bn

Malaysia $120m $40m

Mexico $100m $200m

Philippines $330m $800m

Poland $110m $70m

Romania $30m $25m

Russia $550m $25m

South Africa $220m

Source: neoIT 2005

19© Etheios Group Limited 2006

Some Major user of Off Shore Services

20© Etheios Group Limited 2006

The Indian Situation

• Largest supplier world-wide of both ITO and BPO with exports worth over $17bn in 2005

• Impressive facilities• Substantial investment• Highly competent management• Keen and enthusiastic staff• High quality work• Productivity can be improved• Capacity for growth

21© Etheios Group Limited 2006

Comparison of Strengths

Source: neoIT of San Ramon California who produce an index of attractiveness of the major out source centres using the under mentioned factors.

Factor Weight Sub FactorsFinancial Benefit 30 Labour costs

Cost advantage – operating and capital expenditure

Service Maturity 25 Process maturity and competence of suppliers

Industry size and growth

Security and IP protection

People 25 Labour pool and skill level

Language proficiency

HR

Education system

Infrastructure 5 ICT and physical infrastructure

Catalyst 15 Government support and geo-political environment

Physical and time zone displacement

Cultural compatibility

22© Etheios Group Limited 2006

Off Shore Attractiveness Index - ITO

Location 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0 1.1 1.2 1.3 1.4 1.5 1.6 1.7 1.8 1.9 2.0 2.1 2.2 2.3 2.4 2.5 2.6 2.7 2.8 2.9 3.0 3.1 3.2 3.3 3.4 3.5 3.6 3.7 3.8 3.9 4.0 4.1 4.2 4.3

IndiaCanadaChinaPolandIreland CzechRussiaMalaysia 0.2

MexicoHungaryPhilippinesRomaniaBrazil 0.1

South Africa

Financial Benefit Service Maturity People Infrastructure Catalyst

0.470.18

0.16

0.58

0.66

0.53

0.61

0.69

0.54

0.44

0.59

0.16

0.16

0.16

0.6

0.52

0.56

0.52

0.450.35

0.48

0.18

0.25

0.19

0.18

0.24

0.18

0.15

0.38

0.43

0.37

0.35

0.62

0.52

1.03

0.79

0.61

0.54

0.60

0.48

0.49

0.39

1.15

0.69

0.73

0.45

0.94

1.16

0.83

0.57

0.69

0.61

0.46

0.42

0.39

1.06

1.27

1.33

1.29

1.30

1.12

0.62

0.72

1.30

1.24

1.38

1.30

1.30

23© Etheios Group Limited 2006

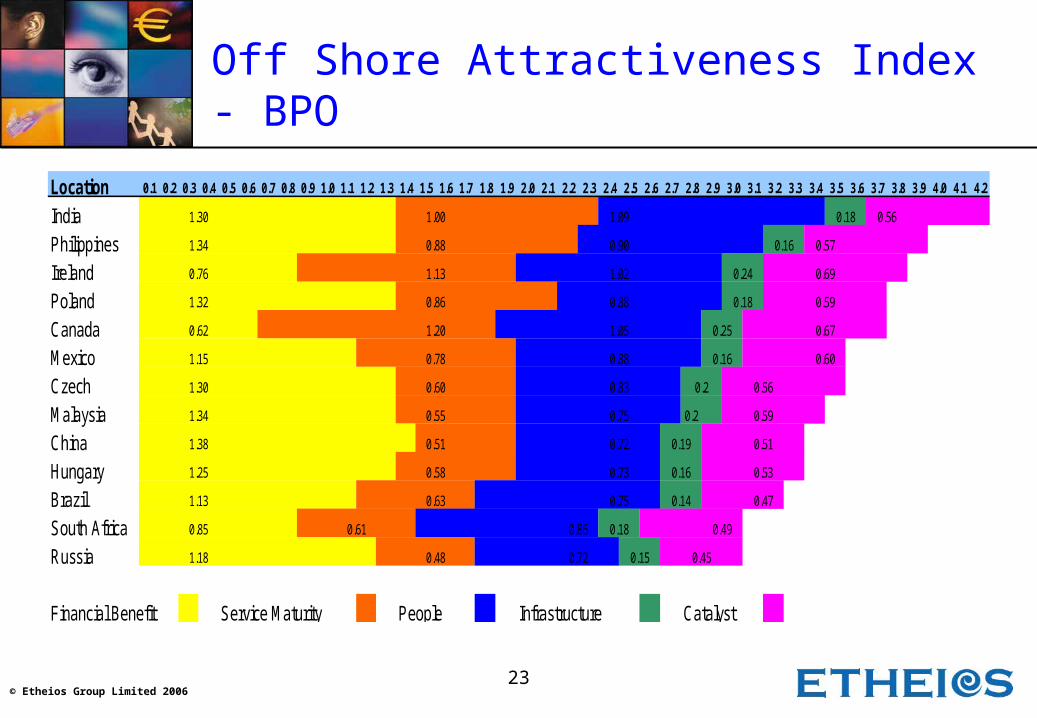

Off Shore Attractiveness Index - BPO

Location 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0 1.1 1.2 1.3 1.4 1.5 1.6 1.7 1.8 1.9 2.0 2.1 2.2 2.3 2.4 2.5 2.6 2.7 2.8 2.9 3.0 3.1 3.2 3.3 3.4 3.5 3.6 3.7 3.8 3.9 4.0 4.1 4.2

IndiaPhilippinesIreland PolandCanadaMexicoCzechMalaysia 0.2

ChinaHungaryBrazilSouth AfricaRussia

Financial Benefit Service Maturity People Infrastructure Catalyst

0.88 0.60

0.90 0.57

1.34

0.18

1.32 0.86 0.88 0.18 0.59

1.02

1.25

1.34

1.30

1.15

0.62

0.76

1.30

1.18

1.38

0.85

1.20

1.13

0.60

0.78

0.58

0.88

1.13 0.63

1.00

0.51

0.48

0.55

0.83

0.72

0.75

0.73

0.75

1.09

1.05

0.72

0.61

0.14 0.47

0.86

0.25

0.19

0.24

0.2

0.15

0.51

0.59

0.16

0.16

0.53

0.490.18

0.16

0.56

0.67

0.69

0.56

0.45

24© Etheios Group Limited 2006

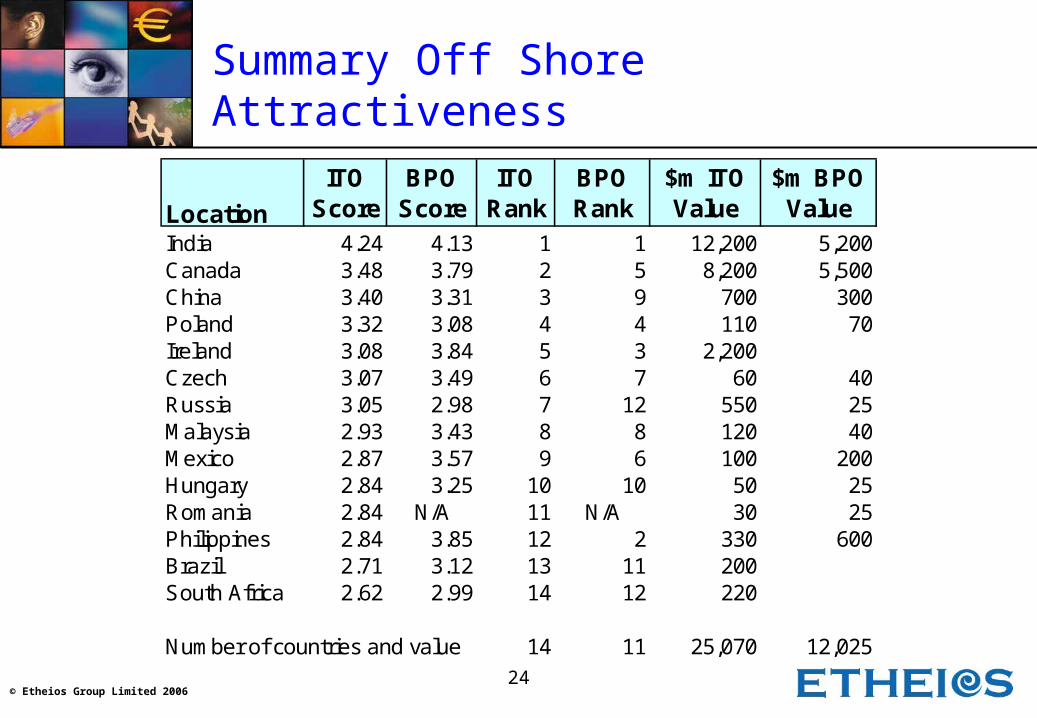

Summary Off Shore Attractiveness

Location

ITO Score

BPO Score

ITO Rank

BPO Rank

$m ITO Value

$m BPO Value

India 4.24 4.13 1 1 12,200 5,200Canada 3.48 3.79 2 5 8,200 5,500China 3.40 3.31 3 9 700 300Poland 3.32 3.08 4 4 110 70Ireland 3.08 3.84 5 3 2,200Czech 3.07 3.49 6 7 60 40Russia 3.05 2.98 7 12 550 25Malaysia 2.93 3.43 8 8 120 40Mexico 2.87 3.57 9 6 100 200Hungary 2.84 3.25 10 10 50 25Romania 2.84 N/A 11 N/A 30 25Philippines 2.84 3.85 12 2 330 600Brazil 2.71 3.12 13 11 200South Africa 2.62 2.99 14 12 220

Number of countries and value 14 11 25,070 12,025

25© Etheios Group Limited 2006

Predictions & Conclusions

1. Companies will continue develop strategies which focus on what they do best.

2. Customer contact will remain of crucial importance for financial institutions.

3. Core financial products will become less complex but exotic products will continue to be developed for niche markets.

4. The pace of technology advance will not slacken.

5. Focus on costs will continue.

26© Etheios Group Limited 2006

Questions & Discussion