trends in government promotion of black entrepreneurship

TRANSCRIPT

TRENDS IN GOVERNMENT PROMOTIONOF BLACK ENTREPRENEURSHIP

By Timothy Bates

In 1968 the federal government established a new program, ProjectOWN, and expanded existing programs designed to foster the growthand development of the minority-owned business community.Government efforts stressed making long-term credit available tominority businessmen, and the expanded lending activities wererationalized by ambiguous references to "compensatory capitalism."In order to develop the minority resources seeking to find expressionin business, bankers and government lending agencies would have toaccept the principle of less stringent requirements for loans tominorities.' Always dominant in government attempts to financeminority enterprise, the Small Business Administration (SBA) ap-proved nearly 40,000 direct loans and bank loan guaranteesproviding over $1.1 billion to minority entrepreneurs in the six yearperiod ending June 30, 1973. 2

This study briefly examines SBA's overall minority businesslending effort and then describes changes over time in the numberand dollar volume of loans channeled to central city businessmenunder the auspices of the SBA's various loan programs. Loanrecipients have been disaggregated into three racial/ethnic groups—White, Black, and Other Minority. The evidence indicates thatgovernment loans to promote black capitalism have been decliningover the last four years. The SBA is promoting entrepreneurship forBlacks and other minority groups by (1) relying increasingly uponguaranteeing bank loans against default risk and (2) providingrelatively more loans to other minority groups and fewer loans toBlacks. When measured by either numbers of loan approvals or

176 The Review of Black Political Economy

relative emphasis on lending to whites and others, government effortsto promote minority business development, particularly blackenterprise, have stagnated.

BACKGROUND

6x6

Before 1964, racial, ethnic characteristics of SBA borrowers werenot recorded, but estimates from selected regional offices indicatedthat minority borrowers had received seven loans in Philadelphia andsix loans in Washington, D.C. in the ten years following the agency'sfounding in 1954. In January, 1964 an experimental program called6 x 6 was instituted to assist disadvantaged owners of very smallretail and service enterprises. While 6 x 6 was not specifically aprogram for minority group entrepreneurs, it was anticipated thatminorities would receive a large share of the loans granted. SBAoffered loan maturities extending to a maximum of six years andloan amount ceilings were $6,000—hence the 6 x 6 designation. Byearly 1965, 794 of these 6 x 6 loans had been approved and minoritybusinesses in five cities received 393. Average loan amount wasroughly $4,500. 3 The program was judged a success and provided thebasis for an expanded program which was authorized under Title IVof the Economic Opportunity Act. In 1965 the 6 x 6 program wasreplaced by the Economic Opportunity Loan (EOL) Program.

Economic Opportunity Loans

The early EOL program retained the philosophy of its predecessorbut the terms of lending became more generous—the loan maturitymaximum was extended to 15 years and loan amount ceilings wereincreased to $25,000. Loan eligibility was determined by theborrower's family income in relation to number of dependents. TheEOL program sought solely to assist persons living in poverty.

In 1966, amendments to Title IV broadened the program so thateligibility was expanded to include people with incomes above thepoverty level who "had been denied the opportunity to compete inbusiness on equal terms. "4 By July, 1968 there were 7,628 EOLloans approved, totalling over $80 million. Minorities received about40 percent (in terms of both number and dollar amount) of theseloans.' SBA had established an active program for lending toimpoverished businessmen but it did not really have a program

BLACK ENTREPRENEURSHIP 177

designed to foster the growth and development of the minority-owned business community.

Project OWN

In July, 1968 Howard Samuels was sworn in as Director of SBA,"and charged by the President with the responsibility of greatlyincreasing loans to minority businesses. " 6 Project OWN supportedthe creation and expansion of all lines of minority enterprise andshifted emphasis away from the poverty criteria upon which EOLloans had been based. Samuels emphasized the complementarynotions of "compensatory capitalism" and the under-representationof minorities as owners of businesses. Project OWN sought to narrowthe ownership gap (i.e., the gap between the proportion of minoritiesin the nation's population and the proportion of minority businessowners in the nation's population of business owners—roughly 17percent versus 4 percent)' by stimulating enormous increases inprivate sector lending to minority entrepreneurs. In addition toguaranteeing bank loans to minorities, SBA lending criteria wereeased in all agency financial assistance programs. SBA was nowfirmly committed to expanding the size and scope of the minority-owned business community and a large new source of loan funds,SBA guaranteed bank loans, had been effectively tapped. In fiscalyear 1969, though, EOLs still accounted for 67.0 percent of allloans to minorities and in fiscal year 1970 the EOL percentage roseslightly to 71.9.

Operation Business Mainstream

In the 1968 presidential campaign, Richard Nixon stressedpromotion of "Black Capitalism" as the centerpiece of his civil rightsprogram. In practice, Nixon's black business development strategysimply meant a continuation of Project OWN (renamed OperationBusiness Mainstream) as far as SBA lending policies were concerned.Two changes implemented under Operation Business Mainstream,though, did facilitate the expansion of loans to high risk minorityborrowers. First, SBA loan approval procedures were simplified and ablanket guarantee arrangement was established which minimized thepaperwork involved in obtaining SBA guarantees for bank loans.Second, the proportion of equity financing required in a borrowingwas lowered for minorities, and rules prohibiting loans to finance achange in ownership of a business were relaxed.

178 The Review of Black Political Economy

TRENDS IN FINANCING MINORITY ENTERPRISE

Assistance for minority group entrepreneurs is sometimes equatedwith black business development or the promotion of "BlackCapitalism." This tends to obscure what has been occurring. To avoidpossible confusion, I will distinguish between Blacks and otherminority groups—i.e., Eskimos, Orientals, Indians, Puerto Ricans andSpanish Americans. A third group, white borrowers, will also beidentified in the following analysis.

The samples considered in this paper have been drawn from SBAtapes listing all loan approvals originated in the Washington, D.C.,Philadelphia, New York, Chicago, and Boston regional SBA offices.These tapes contain information about individual loans and guaran-tees approved between June, 1967 and June, 1973. Loans have beendropped from consideration if their businesses were not located inthe central city areas of the previously mentioned metropolitanregions. $ Nearly all of the minority business borrowers were locatedin central cities; the deletion of noncentral city firms simply removedmost of the white borrowers from the analysis tape.

In these five central cities, SBA approved over 7,300 loans toborrowers during the period under consideration. Time trends inrelative shares of loans received by the three racial/ethnic groups areparticularly revealing. In fiscal year 1968, Blacks and other minoritygroups received 251 and 46 loans, respectively; in 1973, Blacks andother minorities rceeived 740 and 357 loans. The major part of theincrease in loans to minority groups took place in fiscal year 1969when Howard Samuels implemented Project OWN. 9 Samuels vigor-ously promoted bank lending to Blacks and other minority groupsand he scrutinized regional SBA offices to insure that his policieswere being implemented at the local level.' 0

In the five cities under consideration, direct loans and loanguarantees to Blacks and other minority groups increased sharply infiscal year 1969; from 251 to 635 for Blacks; from 46 to 128 forother minorities; and from 255 to 362 for whites.

Under the Nixon Administration, Project OWN was renamedOperation Business Mainstream and the SBA established a blanketguarantee arrangement which simplified the process of obtainingSBA guarantees for bank loans. This simplification undoubtedlyencouraged increased bank participation in programs for lending toBlacks and other minority groups. Relative to fiscal year 1969, direct

BLACK ENTREPRENEURSHIP 179

SBA loans to Blacks in the 5 cities fell from 414 to 289 in fiscal year1970 while direct loans to other minority groups rose from 84 to124. During this same time period, SBA guaranteed bank loans toBlacks rose from 221 to 396 and guaranteed loans to other minoritygroup borrowers increased from 44 to 81. Table I shows that loansto Blacks leveled off in the 1970-1973 time period while loans toother minority groups increased rapidly and loans to whitesskyrocketed.

TABLE INumber of Approved SBA Direct and Guaranteed Loans

in Five Major Cities, by Race of Borrower 1970-73Race

OtherYear , Blacks Minorities Whites Total

1970 685 205 201 1,0911971 697 269 345 1,3111972 715 345 463 1,5231973 740 357 672 1,769Total 2,837 1,176 1,681 5,694% Increase1970-73 8.0 73.3 234.3 62.1

Banks were responsible for the entire increase in loans to Blacksduring this four-year period: SBA guaranteed bank loans increasedfrom 396 to 547 while SBA direct loans to Blacks declined from 289to 193. SBA direct loans to whites and other minorities increased193 9 percent and 7.3 percent respectively in this time period. Thecutback in SBA direct loans was sharpest in fiscal year 1973 and itaffected both Blacks and other minority groups (but not whiteborrowers).

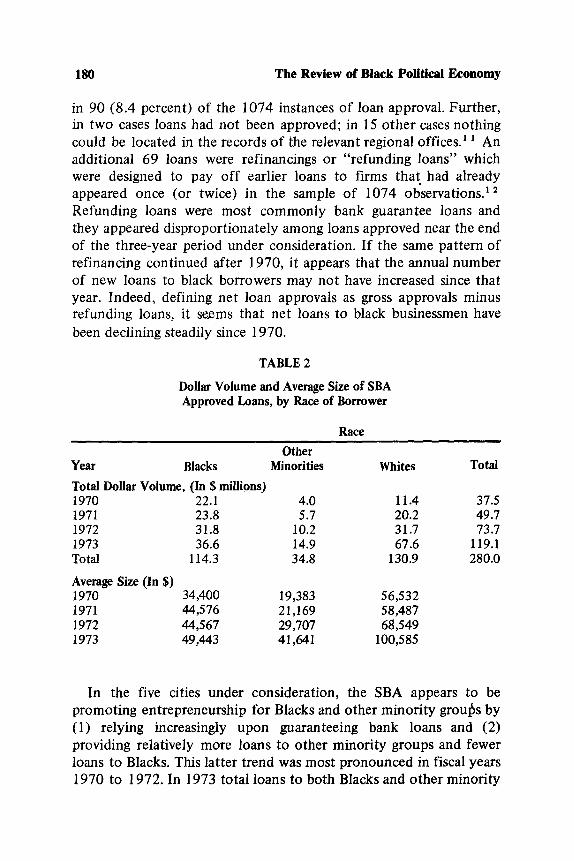

Data reported in Table 1 are gross loan approvals; they seriouslyoverstate the number of net new loans actually received byborrowers. For a three-city subsample of loan approvals to Blacks inBoston, New York, and Chicago, I tried to estimate the amount ofthis overstatement. Other magnetic tapes from the SBA's Office of Re-cords indicate that 1074 loans to black borrowers had been approvedbetween June, 1967 and June, 1970 in these three cities.By visiting the regional SBA offices in Boston, New York, andChicago and by individually examining the loan files of these 1074borrowers, I found that the loan proceeds had never been disbursed

180 The Review of Black Political Economy

in 90 (8.4 percent) of the 1074 instances of loan approval. Further,in two cases loans had not been approved; in 15 other cases nothingcould be located in the records of the relevant regional offices." Anadditional 69 loans were refinancings or "refunding loans" whichwere designed to pay off earlier loans to firms that had alreadyappeared once (or twice) in the sample of 1074 observations.' 2

Refunding loans were most commonly bank guarantee loans andthey appeared disproportionately among loans approved near the endof the three-year period under consideration. If the same pattern ofrefinancing continued after 1970, it appears that the annual numberof new loans to black borrowers may not have increased since thatyear. Indeed, defining net loan approvals as gross approvals minusrefunding loans, it seems that net loans to black businessmen havebeen declining steadily since 1970.

TABLE 2

Dollar Volume and Average Size of SBAApproved Loans, by Race of Borrower

Race

OtherYear Blacks Minorities Whites Total

Total Dollar Volume, (In $ millions)1970 22.1 4.0 11.4 37.51971 23.8 5.7 20.2 49.71972 31.8 10.2 31.7 73.71973 36.6 14.9 67.6 119.1Total 114.3 34.8 130.9 280.0

Average Size (In $)1970 34,400 19,383 56,5321971 44,576 21,169 58,4871972 44,567 29,707 68,5491973 49,443 41,641 100,585

In the five cities under consideration, the SBA appears to bepromoting entrepreneurship for Blacks and other minority grouts by(1) relying increasingly upon guaranteeing bank loans and (2)providing relatively more loans to other minority groups and fewerloans to Blacks. This latter trend was most pronounced in fiscal years1970 to 1972. In 1973 total loans to both Blacks and other minority

BLACK ENTREPRENEURSHIP 181

groups had leveled off in number. Quite clearly, the SBA isaggressively expanding the flow of loans to central city businessesowned by whites. This is true for both SBA direct loans and bankguarantee loans; if the dollar amount rather than number of loanapprovals is examined, this trend is much more pronounced becauseloans to whites are typically larger than loans to Blacks and otherminority groups (see Table 2). Although guaranteed bank loans bearmuch higher interest rate charges than SBA direct loans, bank loansmay be advantageous because they are typically larger in dollaramount.

In fiscal year 1973, for example, the mean direct and guaranteedloan amounts for black borrowers were $25,425 and $58,617,respectively, in the five cities. Annual interest rates on direct loansranged from 5.5 percent to 6.75 percent in 1973 while forguaranteed loans, "the interest rate is set by the bank," 1 3 typically2 or 3 percentage points above the prime interest rate. That is,guaranteed bank loans bore interest rates of 10 to 12 percent for theperiod in question.' a

The SBA has recently been accused of switching emphasis fromBlacks to Spanish Americans. " ... the change was made to attractSpanish voters after Republicans concluded that it was futile to goafter the Black vote." 1 ' Evidence presented here weakly supportsthis assertion but further suggests that changing priorities favorwhites over both Blacks and Spanish-speaking persons (the otherminorities category is predominantly Spanish American and PuertoRican for the five cities under consideration).

TABLE 3Percentage of SBA Direct and Guarantee Bank Loans

Received by Minority Borrowers' 6

1970-72

Year % of Loans % of Dollar Volume

1970 41 231971 36 191972 32 16

Sparse evidence provides a rough overview of SBA's nationallending activities and further reinforces the notion that governmentresources are being oriented increasingly toward financing white

182 The Review of Black Political Economy

rather than black and other minority group entrepreneurs (see Table3).

When measured by either numbers of loan approvals or relativeemphasis on lending to whites and others, it appears that governmentefforts to promote minority business development, particularly blackenterprise, have stagnated. As the SBA has shifted from grantingdirect loans to guaranteeing bank loans, minority group borrowershave clearly been burdened with much higher loan interest paymentobligations. Are these developments consistent with SBA's policyobjective of narrowing the ownership gap (the number of minoritygroup entrepreneurs relative to the number of white entre-preneurs)?' ' What actual standards does the SBA rely upon tomeasure the success of its minority lending programs?

Peat, Marwick, Mitchell, and Co., in their 1971 consultantevaluation of the SBA, stated that "SBA relied exclusively on thenumber of loans being made to measure the success of itsprograms.... "' $ A recent report by the General Accounting Officeconcludes that "SBA has measured the success of Operation BusinessMainstream primarily by the annual increase in the number anddollar amount of loans made rather than by the number of successfulminority businesses established.... We found no evidence that SBAhad presented information to the Coipgress on the number ofsuccessful minority enterprises or that SBA had established any goalsin terms of success or failure rates of businesses with SBA loans." '9

Increases in the number and dollar amount of loans is a rather crudesuccess measure for the minority enterprise lending effort. Numberand size of loans granted may have little relationship to the numberof firms successfully created and expanded, the number of jobscreated by SBA induced investment, or other sensible lendingobjectives. However, if the policies of SBA are internally monitoredby the criteria discussed above, then the information summarized inTables 1, 2, and 3 of this article is an accurate measure of SBA'sdedication to financing minority enterprise. This evidence suggeststhat SBA has been de-emphasizing loans to minorities since fiscalyear 1970; in terms of numbers of loans or loan size, annual increasesin SBA lending activity have clearly benefited whites relative tominority borrowers. The data presented in Table 3, though, indicatethat lending policy has been consistent with the SBA's goal ofnarrowing the ownership gap. Minorities account for four to fivepercent of America's entrepreneurs but they received 16 to 23

BLACK ENTREPRENEURSHIP 183

percent of the dollar volume and 32 to 41 percent of the totalnumber of loans approved by the SBA in fiscal years 1970 through1972. These numbers suggest that the SBA is increasing both therelative number of minority group entrepreneurs and the absolutedifference between the number of white and minority groupentrepreneurs. 2 ° If present trends in actual SBA loan approvalspersist, however, increases in the proportion of minorities (especiallyBlacks) in the nation's population of business owners will beminimal.

NOTES

1. The philosophy of compensatory capitalism is put forth in HowardSamuels, "Compensatory Capitalism," Black Economic Development, eds., G.Douglas Pugh and William F. Haddad (Englewood Cliffs, New Jersey: Prentice-Hall, 1969), pp. 60-73.

2. Loan figures for fiscal years 1969 through 1973 are taken from, LimitedSuccess of Federally Financed Minority Businesses in Three Cities, ComptrollerGeneral of the United States (Washington, D.C., 1973), p. 17. Fiscal year 1968loan figures come from, "Evaluation of the Minority Enterprise Program," SmallBusiness Administration, 1970 (mimeo), p. 4.

3. "Evaluation of Minority Enterprise Program, Attachment I: A BriefHistory of SBA Minority Entrepreneurship Programs," Small Business Admin-istration, 1970 (mimeo), p. 2.

4. Ibid., p. 3.5. Ibid., p. 4.6. "Compensatory Capitalism," p. 71.7. Limited Success, p. 5.8. Central city areas analyzed in this study were defined to include those

counties which were dominated by the city under consideration. For New YorkCity, Washington, D.C., and Philadelphia, city boundaries coincide exactly withthe boundaries of the central counties. For Chicago and Boston, the centralcounties used to define the central city area, Cook County and Suffolk Countyrespectively, encompass the entire cities and small parts of the surroundingmetropolitan areas.

9. Project OWN and "compensatory capitalism" are discussed in more detailin Timothy Bates, "An Econometric Analysis of Lending to Black Business-men," The Review of Economics and Statistics, LV, 3 (August 1973), p. 273.

10. Howard Samuels, "How to Even the Odds," The Saturday Reviéw, LII,34 (August 23, 1969), p. 26. The New York SBA director, Charles Kreiger, wastransferred to Washington in late 1968 because Samuels felt that he lacked theability to implement SBA's programs for promoting minority entrepreneurship.With the change of administration in January 1969, Samuels was forced out ofthe SBA directorship and Kreiger was restored to his New York post. Accordingto one source, Kreiger summarized the problems of minority businessmen bystating that Blacks just don't know how to handle money. For a detaileddiscussion of Kreiger's conflict with Samuels and his opinions of minority

184 The Review of Black Political Economy

entrepreneurs, see Arthur Blaustein and Geoffrey Faux, The Star-SpangledHustle (New York: Doubleday, 1972), pp. 187-93.

11. For a detailed analysis of the selection and the editing of this 1074observation sample, see Timothy Bates, " "The Potential of Black Capitalism,"Public Policy, XXI, I (Winter 1973), pp. 147-48.

12. Ibid., p. 147.13. SBA: What It Is... What It Does (Washington, D.C., Small Business

Administration, 1973), P. 4.14. Available information does not permit safe generalizations of the relative

merits of large, high cost versus small, low cost loans. Empirical evidencesuggests that injections of loan funds would yield rates of return between 14.4percent and 23.0 percent before payment of interest charges. These are marginalrates of return, though, and they may decline as loan size increases. These ratesof return are estimated in Chapter 3 of Timothy Bates, Black Capitalism: AQuantitative Analysis (New York: Praeger, 1973), pp. 55-62.

15. Paul Delaney, "Aid to Minority Businesses: A Lever for Nixon in '72,"New York Times (November 18, 1973), p. 70.

16. "The SBA and Black Business," Black Enterprise (October 1972), p. 50.17. SBA official Dr. Wilfred J. Garvin discusses attempts to measure progress

and performance in SBA minority lending programs; see W.J. Garvin, "The SmallBusiness Capital Gap: The Special Case of Minority Enterprise," Journal ofFinance (May 1971), pp. 451-57.

18. Limited Success, p. 70.19. Ibid., pp. 68-69.20. The extent to which SBA programs are increasing the relative number of

minority group entrepreneurs is less than the gross figures on loan approvalssuggest; failure rates for minorities are much higher than failure rates for whiteborrowers. See Bates, Black Capitalism, pp. 99-100.