trends in action: responsibility in financial services - white paper

DESCRIPTION

The financial crisis has left the society concerned about the long-term future of the financial system. Consumers now want to see banks making commitment to financial sustainability and demand ethical and socially responsible practices. In this white paper, we examine some of the industry’s efforts towards introducing sustainable practices. This white paper is part of our monthly ‘Trends in Action’ series, providing insight into key consumer trends in the financial services industry.TRANSCRIPT

White paper

December 2012

.

2

Hannah Williams Senior Analyst Retail Banking

Since joining Datamonitor in 2010 I have specialized in

Consumer Insight and Retail Banking. Working as a

Senior Analyst in the financial team I have authored

reports on a wide range of topics, including social media,

the financial services sector in 2020, customer satisfaction

and loyalty, and fee-based advice.

Pivotal to our insight is our global consumer survey and I devote a lot of my time both to creating the survey and to querying the data. I have also played a key role in the development of the Financial Customer Intelligence framework – our global consumer trend framework.

If you have questions about the research, data, and findings within this document you can put your questions directly to the analysts. Simply email your questions to [email protected]. To find out more about Datamonitor Financial contact us at: email [email protected] phone +44 20 7551 9437 Visit our website: www.datamonitorfinancial.com Or follow us on Twitter: @DatamonitorFS

DISCLAIMER

While every care is taken to ensure the accuracy of the information contained in this material, the facts, estimates, and opinions

stated are based on information and sources which, while we believe them to be reliable, are not guaranteed. In particular, it

should not be relied upon as the sole source of reference in relation to the subject matter. No liability can be accepted by

Datamonitor, its directors, or employees for any loss occasioned to any person or entity acting or failing to act as a result of

anything contained in or omitted from the content of this material, or our conclusions as stated. The findings are Datamonitor's

current opinions; they are subject to change without notice. Datamonitor has no obligation to update or amend the research or to

let anyone know if our opinions change materially.

3

The Financial Customer Intelligence framework presents eight mega-trends that

help us to understand the needs, preferences, and demands of consumers. It is

vital to understand the attitudes and behaviors of consumers in order to design

products and services that align with these demands.

Source: Datamonitor. Marketing Strategies for Rebranding Financial Services (2012)

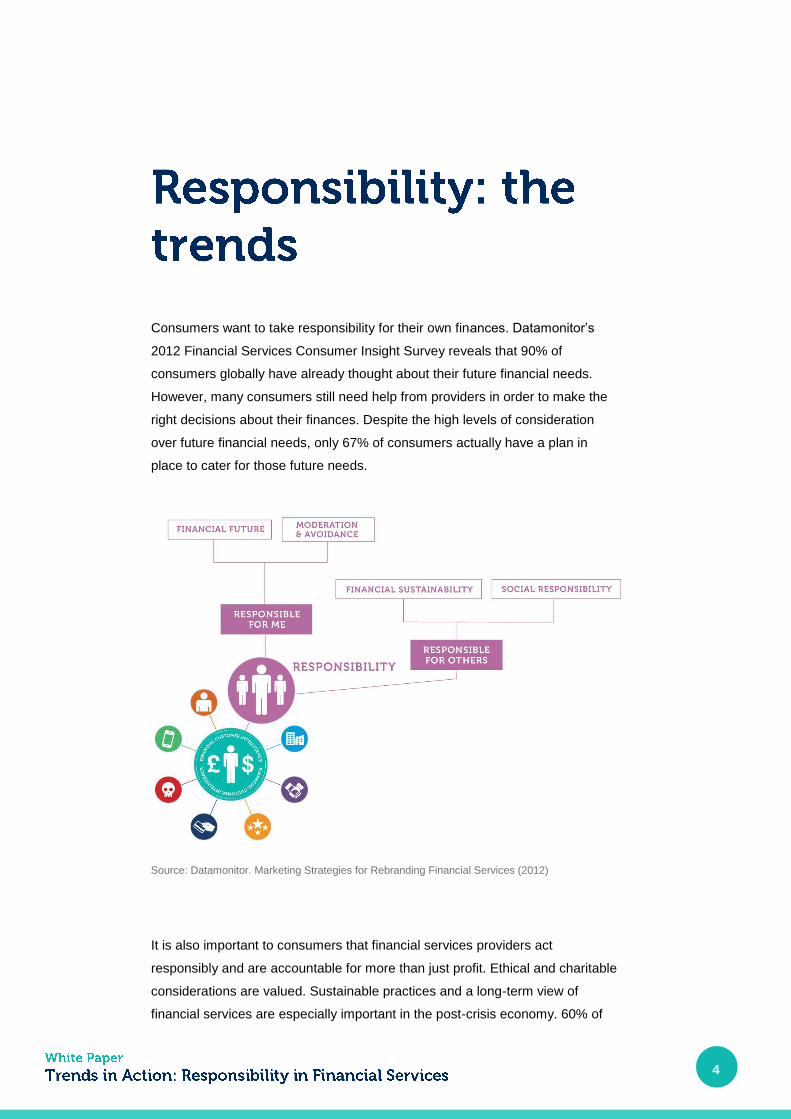

This document will focus on the Responsibility mega-trend. Responsibility is

one of the eight mega-trends that Datamonitor has identified as being a

significant driver of consumer behavior in relation to the purchase and use of

financial services and products.

4

Consumers want to take responsibility for their own finances. Datamonitor’s

2012 Financial Services Consumer Insight Survey reveals that 90% of

consumers globally have already thought about their future financial needs.

However, many consumers still need help from providers in order to make the

right decisions about their finances. Despite the high levels of consideration

over future financial needs, only 67% of consumers actually have a plan in

place to cater for those future needs.

Source: Datamonitor. Marketing Strategies for Rebranding Financial Services (2012)

It is also important to consumers that financial services providers act

responsibly and are accountable for more than just profit. Ethical and charitable

considerations are valued. Sustainable practices and a long-term view of

financial services are especially important in the post-crisis economy. 60% of

5

consumers worldwide believe that their bank has a strong commitment to a

charitable and ethical strategy.

Datamonitor's Financial Customer Intelligence framework summarizes the two

trends within the Responsibility mega-trend as Responsible For Me and

Responsible For Others. This white paper will use current case studies to

illustrate how each of the sub-trends (Moderation and Avoidance, Financial

Future, Financial Sustainability, and Social Responsibility) is now impacting on

the financial services industry.

Consumers need to keep their finances under control on a day-to-day basis,

monitoring their financial statements and levels of debt. In order to prevent

avoidance behaviors such as ignoring debt, consumers need providers to

facilitate the checking of finances.

The ImpulseSave service in the US allows consumers to set savings goals and

transfer money towards these when they resist the urge to spend. “Impulse

saving” is seen as the opposite of making an impulse purchase; rather than

making an unnecessary purchase consumers are encouraged to save the

money they would have spent. The service allows consumers to physically

transfer the money into a savings account, ensuring that the resisted purchase

is converted into an actual saving for the consumer. Impulse savings can be

made through an iPhone app or by SMS.

Source: OrSaveIt (2012)

6

The ImpulseSave idea is being built upon by OrSaveIt, which is due to launch in

the UK imminently. This service will also offer an app through which customers

can instantly save the money that they have resisted spending. While the full

details are as yet unknown, this app will also help consumers to control their

everyday finances and see tangible rewards from doing so.

Credit Sesame is a tool that allows consumers to monitor all their debt,

including their mortgage, credit cards, and personal loans, in one place. The

service combines an individual’s credit score and financial profile along with

available products and market changes, to produce personalized

recommendations that would help that individual to save money. “Debt

optimization” is a key selling point of Credit Sesame; the tool helps customers to

restructure their debt so that it is cheaper over the life of the debt.

Source: Credit Sesame (2012)

Credit Sesame was one of the FinnovateFall 2012 “Best of Show Winners.” The

service has clear benefits for consumers who want to keep track of their debt

7

and to reduce this as quickly as is possible. The personalized recommendations

save consumers time, and they can also be applied for through the site. “What

if” modeling helps customers to see what would happen if factors such as their

credit score changed. This helps consumers to take more responsibility for their

debt, while helping them to make better informed decisions.

Consumers want to take responsibility for their long-term financial future. Help

with planning and choosing appropriate products is important to consumers.

The LearnVest website in the US combines more traditional personal financial

management (PFM) functionality with the addition of tailored financial planning.

The site allows consumers to make contact with a Certified

Financial Planner to build a five-year plan or investment

portfolio. While this planning service carries a cost to

the consumer, it provides a convenient channel for

consumers to make contact with an expert who can

help them with their finances. The imagery and many

of the topics covered on the site highlight its target

audience – women – whom the site aims to “empower”

to take control of their finances.

In addition to the PFM tools and financial planning options, the site provides

context on news stories and how these may affect customers’ finances, as well

as a series of “bootcamps” to help customers take control their financial

situation. Overall this site helps consumers who may otherwise struggle to find

access to financial planning to create a plan for their financial future. The

emphasis on the importance of having a financial plan in place demonstrates

how the provider is aiming to educate its target audience.

Consumers want providers to take a long-term view of financial services.

Responsible lending and ensuring sustainable practices appeal to consumers.

8

In October 2012, Barclays announced that it would end all commission-based

sales targets for frontline staff, instead paying bonuses based solely on

customer satisfaction ratings. Branch and call center staff will be affected by this

change of focus of their bonus scheme. Team, rather than

individual, performance will be assessed by looking at

customer satisfaction ratings across a branch or

area.

Refocusing the payment of staff incentives in this

way demonstrates that Barclays has realized the

potential damage of commission-based sales.

These can lead to mis-selling and the pushing of

inappropriate products. An emphasis instead on customer

perceptions of the service that they have received should ensure that staff act in

the best interests of the customer. This in turn will help to improve sustainability,

with consumers purchasing the products that they need and that are best suited

to their circumstances.

The US community bank PremierWest Bank launched an online “Financial

Answer Center” in October 2012. This service provides customers with access

to a host of financial questions, as well as offering “Quick Guides” on specific

financial issues. The service also puts customers in touch with a local bank

representative with expertise in a particular area if they want to discuss

something further with their bank.

PremierWest Bank’s education platform demonstrates a commitment to helping

consumers to make sensible decisions over their finances. It also differentiates

the bank’s proposition from its competitors by going one step further to highlight

its approach to financial responsibility. While it is very hard for providers to

demonstrate attributes such as responsible lending, taking steps to educate

customers and offering additional help when needed will provide an idea of

financial responsibility.

9

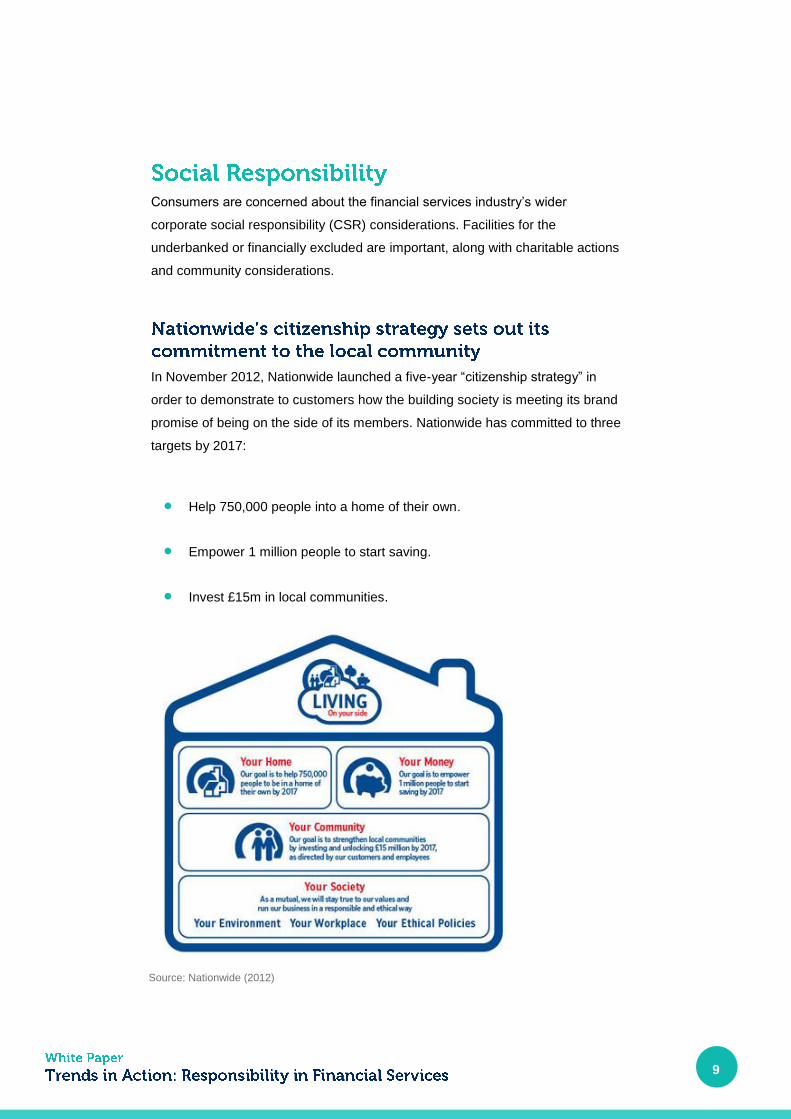

Consumers are concerned about the financial services industry’s wider

corporate social responsibility (CSR) considerations. Facilities for the

underbanked or financially excluded are important, along with charitable actions

and community considerations.

In November 2012, Nationwide launched a five-year “citizenship strategy” in

order to demonstrate to customers how the building society is meeting its brand

promise of being on the side of its members. Nationwide has committed to three

targets by 2017:

Help 750,000 people into a home of their own.

Empower 1 million people to start saving.

Invest £15m in local communities.

Source: Nationwide (2012)

10

The setting out of clear and measurable objectives adds credibility to

Nationwide’s new strategy. The three goals that the building society has set are

focused on its customers and the communities in which it operates, highlighting

a commitment to being socially responsible. The high level of transparency

utilized by Nationwide in promoting this citizenship strategy is important so that

consumers can see what the building society is doing and track its progress.

The “Superstorm” that hit New York and the northeastern US at the end of

October 2012 caused widespread destruction to the area. Chase, which is

based in New York, was one of the first banks to announce that it would offer

disaster relief, pledging up to $5bn of support for small businesses and $5m in

charitable relief. On a more practical level, Chase sponsored food trucks to

deliver hot meals to people in areas affected by the storm. The bank also

waived fees for customers affected by the storm.

This ad hoc demonstration of community support shows customers that their

bank truly is interested in being socially responsible, beyond pre-planned CSR

efforts. Banks are integral to the daily lives of consumers and

in a crisis, providers need to demonstrate that they

understand this. Support for the local community may

not be in response to such a large-scale event; in the

UK, for example, banks have the opportunity to assist

communities dealing with flooding and to help

customers in need.

11

Personal responsibility and corporate responsibility are important to the modern

consumer. The global financial crisis made abundantly clear the potentially

damaging effects of individuals and providers not acting responsibly.

Consumers want to do more to ensure the security of their financial futures.

They also want to see providers making the same commitment to financial

sustainability. This paper has identified several examples of tools that aid

consumers in taking more responsibility for their finances, as well as initiatives

from providers to highlight their efforts towards introducing sustainable

practices.

Datamonitor's Financial Customer Intelligence framework offers a useful means

of identifying the different factors that providers need to be aware of when trying

to help consumers take responsibility for their finances, as well as demonstrate

their own commitment to financial responsibility.

The financial crisis and previous cycles of boom and bust have left consumers

concerned about the long-term future of the financial system as a whole.

Consumers therefore want to see that providers are taking into account the

long-term viability of financial services when making decisions. Responsible

lending and borrowing are important to consumers.

There is also concern over the wider ethical and social considerations of

financial services providers. Consumers want their providers to uphold the

same values as they themselves hold. Activities such as sponsorship of events

12

or teams, the support of charities, and community events all help to

demonstrate to consumers that a provider is aiming to be socially responsible.

Consumers need to “keep on top of” their finances in order to ensure that their

spending or levels of debt are under control. However, it is very easy for

consumers to ignore their finances or spend in excess of their budget. Providers

should help those consumers who need assistance to monitor their finances.

Providers should consider tools and services that will provide additional support

to those consumers who need it.

The long-term future of their finances is of vital importance to consumers. They

want to take ownership of processes such as retirement planning to ensure that

they have the financial future that they want. This does not mean that they will

not need help from their financial services providers to do this effectively;

planning for retirement or choosing life cover are not always simple processes.

Providers must therefore offer consumers the advice or tools that they need in

order to understand their position and what planning needs to be done.

Providers must get involved in the communities in which they

operate – This shows consumers that the provider is aware of its wider

responsibilities.

Help consumers to plan their finances – Consumers want to be

responsible for their own finances but are not always able to plan without

guidance.

Offer sustainable and ethical products and services – Consumers

demand that their financial services providers align with their own beliefs

around sustainability and ethicality.

Encourage consumers to be responsible for their finances – Helping

consumers to engage with their finances will help to avoid problems with

debt or low savings in the future.

13

Be transparent about practices to secure financial sustainability –

Consumers want to know that providers are designing strategies to

safeguard their sustainability in the long term.

14

Access this report through your Knowledge Center, or order from the

Datamonitor Research Store for instant access.

Knowledge Center subscriber >>

Research Store >>

Knowledge Center subscriber >>

Research Store >>

Trends in Action: Trust in Financial Services >>

Trends in Action: Digital Lifestyles in Financial Services >>

Trends in Action: Convenience in Financial Services >>

Trends in Action: Individualism in Financial Services >>

At Datamonitor Financial, we deliver intelligence-led insight and data on

financial services markets, competitors, and consumers. Our robust forecasting

methodologies, proprietary databases, and the experience and knowledge of

our in-house analysts help clients to make better strategic decisions in the

areas of Retail Banking, Cards & Payments, Savings & Investments, Private

Wealth Management, Life & Pensions, and General Insurance. Our research on

cards and payments covers competitor developments, consumer attitudes,

market forecasts, and technology developments, highlighting current and future

trends. The Global Payment Card Analyzer, our proprietary online tool, includes

market size, consumer, and competitor data for 60 countries.

If you have questions about the research, data and findings within this document you can put your questions directly to the analysts. Simply email your questions to [email protected]. To find out more about Datamonitor Financial contact us at:

email [email protected]

phone +44 20 7551 9437

visit our website: www.datamonitorfinancial.com

Or follow us on Twitter: @DatamonitorFS

Datamonitor is owned and operated by Informa plc ("Informa"), the registered office of which is Mortimer House,

37–41 Mortimer Street, London, W1T 3JH. Registered in England and Wales Number 3099067.