trends and patterns in top executive compensation

TRANSCRIPT

Lal Bahadur Shastri Institute of Management, Delhi

LBSIM Working Paper Series

LBSIM/WP/2020/19

Trends and Patterns in Top

Executive Compensation:

Evidence from India

Tarun Soni

August,2020

LBSIM Working Papers indicate research in progress by the author(s) and are brought out to elicit

ideas, comments, insights and to encourage debate. The views expressed in LBSIM Working Papers

are those of the author(s) and do not necessarily represent the views of the LBSIM nor its Board of

Governors.

WP/August2020/19

LBSIM Working Paper

Research Cell

Trends and Patterns in Top

Executive Compensation: Evidence

from India

Tarun Soni

Abstract

The study attempts to analyze the trends and patterns in executive compensation for 30

companies, which are among the largest listed companies on Bombay Stock Exchange over

the past 17 years. It tries to establish link between executive remuneration and firm

performance for the sample companies. The analysis portrays an increasing trend of

compensation to management especially after 2014. Further, the results of our empirical

analysis confirm positive relationship between executive compensation and certain firm

performance variables (Sales, long-term EPS and Dividends). However, our model also

indicates negative relationship between short-term EPS and executive compensation. For

corporate governance variables and executive compensation our model indicates inverse

relationship between executive compensation, board size and board meetings. Our findings

partially support the positive relationship between executive compensation and firm

performance and weak governance mechanism for our sample firms.

Keywords: Executive Compensation, Corporate Governance, Firm Performance, India

JEL Classification: G34, J33, G18, G38

Trends and Patterns in Top Executive

Compensation: Evidence from India

Introduction

The importance of good corporate governance practices has gained importance in the Indian

corporate sector especially in the past two decades. In the current business environment, good

corporate governance practices have been linked to superior returns to diverse stakeholders

thereby enhancing firm value in the long run.

An important indicator of good governance practices is the amount spent in terms of senior

and executive remuneration in comparison to firm performance. Huge expenditure on

remuneration of top executives can act as drainage of shareholders wealth especially when

remuneration is not linked to performance of organization thereby violating the general

principles of good governance.

Further, the issue of excessive executive compensation has been recognized by the G-20 and

the Financial Stability Forum as an important factor leading to the Global Financial Crisis in

developed countries. However, in comparison to the developed countries the scenario in India

is under better control due to imposition of certain maximum statutory limits prescribed by

the law. The concern arises from the fact that the pay scales of the top executives have seen a

steady rise over the years which has been proving to be disconcerting for market watchers

and regulators of the financial and corporate sector in India (Mukherjee and Majumdar 2010).

In the light of the same, an attempt has been made to analyze the trends and patterns in

executive compensation in India over the past 17 years. The research initially studies the

legal framework in terms of rules framed by companies act on the same issue and then studies

the trends and patterns over the years. Finally, it tries to establish link between firm

performance and executive remuneration for the sample companies.

The study thus tries to fill the vacuum upon the ongoing debate between top management and

other stakeholders on the issue of excessive executive compensation. The study will provide

inputs to policy researchers, academicians and shareholders on an important issue which has

not been studied in detail in Indian context.

The remainder of the paper is organized as follows. Section 2 presents a brief review of

existing laws which govern executive compensation in India. Section 3 describes the data

sources and the methodology adopted for estimation purposes. Section 4 presents the

empirical results. Finally, Section 5 provides a summary and concludes.

Executive Compensation and the Indian Companies Act 2013

The erstwhile Indian Companies Act 1956 contained provisions for managerial remuneration.

According to Section 198 of the Act the total compensation paid to top level management of

a public company or subsidiary private company, in a financial year, could not exceed eleven

percent of the net profits of the company. Further, it also barred payment of any

compensation to executives excluding the fees payable under Section 309(2) of the Act in the

case of inadequate profits or firm incurring severe losses. In addition, Section 309 imposed

restrictions on total compensation of all whole time/ managing directors should not exceed

ten percent of the net profits of the company in a financial year except with prior approval of

the Central Government. Further, Section 200 prohibited any company from paying

remuneration free of taxes to its executives.

Although the act had provisions to safeguard the interest of shareholders however the

framework was applicable only for public companies and its subsidiaries. This effectively

excluded private companies. In order to plug the loopholes of the Companies Act, 1956,

modifications were made and the new Companies Act, 2013 was introduced. The new act

has consolidated all provisions under a single provision of 197. Further, it has made

mandatory for all listed companies (Private and Public ltd Companies) to adhere to the new

guidelines of the act contained in Section 197 of the act.

As per the new guidelines every listed company has to constitute a nomination and

remuneration committee. This committee has to ensure the level and composition of

remuneration is reasonable and sufficient to attract, retain and motivate directors of the

quality required to run the company successfully. Further, the committee has to ensure that

remuneration paid is not higher than the provisions laid down in Companies Act 2013.

As per the provisions of Section 197 of the Companies Act, 2013, a public company having

sufficient profits can pay remuneration to its directors including Managing Directors and

Whole-time Directors, and its managers which shall not exceed 11% of the net profit.

Wherein a company in which there is one Managing Director; Whole-time Director or

manager the remuneration to be payable shall not exceed 5% of net profits and where there

are more than one of such Directors remuneration payable shall not exceed 11 % of the net

profit. A company with inadequate profit may pay to its managing director or whole-time

director in according to Schedule V (Part II) of the Companies act 2013. Further, such

compensation can be increased upto 200% if shareholders have given their approval through

a special resolution.

The Companies Act 2013 adds a requirement that the companies should give a detailed

explanation of any pay increases. Further, it has to publish the ratio of median pay of top

management and pay of all employees in their annual reports.

Thus it may be concluded, that compared to the erstwhile Companies act 1956, the new

regulations have made way for a more clear and less complicated policy on executive

remuneration which requires Indian listed companies to be more transparent in reporting their

executive remuneration policies. At the same time, new provisions aim at empowering

shareholders especially in case the company is unable to earn adequate profits. Further, some

initiatives have also been taken to link executive remuneration with organizational

performance. In the same line, the study tries to capture the past trends of executive

compensation and tries to empirically establish a linkage with the firm performance variables

after controlling for corporate governance variables of these organizations. The next section

discusses literature followed by the empirical methods followed by findings and conclusion.

Literature Review

The research on the issue of executive compensation stems from agency theory, which deals

with how top executive compensation policies should be designed to minimize agency cost.

A brief review of the relevant research has been reported in this paper.

Jensen and Murphy (1990) have studied performance pay and top-management incentives for

over a large sample of 2,000 CEOs and found positive and statistically significant

relationship among the two variables however they also note that the coefficients are small

and have declined over the years.

Hubbard and Palia (1993) examine CEO compensation in the banking industry on a sample

of 147 banks and found higher levels of pay in those markets where interstate banking was

permitted. They also report increase in CEO turnover in less regulated markets.

Main et al. (1996) found a higher degree of relationship among top management

compensation and firm performance than suggested by previous studies. They found that the

relation between executive pay and firm performance became more significant when

executive options were included in executive compensation.

On the contrary, Core et al. (1999) report inverse relationship between board characteristics

and ownership structure with subsequent firm operating and stock return performance.

Further, they also report positive relationship between larger boards in terms of both cash

compensation and total compensation. Furthermore, they also found inverse relationship with

CEO pay and firm governance structures.

In the same line, Brick et al. (2006) found evidence for excessive remuneration that was not

linked to the performance of the firm. They consider unobserved firm complexity (omitted

variables), and/or to excess compensation of directors and managers as reasons for the higher

levels of pay.

Dong and Ozkan (2008) have studied the impact of institutional ownership influencing top

management compensation for firms in context of UK. The study found institutional

investors, did not had any bearing on the director pay levels and pay–performance

relationship.

Frydman and Jenter (2010) also report a significant rise in top management remuneration

from the 1970s to the early 2000s. Further, they also attribute managerial power and

competitive market forces as important determinants of CEO pay for the sample firms.

Guest (2010) study the relationship between governance structures and executive

compensation and concluded that higher proportion of independent directors in the

company’s board negatively influences the executive pay rise. They also report positive

relationship between board size and executive remuneration in context of U.K.

Ozkan (2011) studied the relationship between cash (salary and bonus) and equity-based

(stock options and long-term incentives) components of executive compensation and reported

a significant positive relationship between firm performance and CEO compensation

Further, Alonso and Aperte (2011) study board composition and equity linked compensation

in European context. The study found presence of higher percentage of independent directors

on the board negatively impacts direct compensation and positively impacts bonus or equity

link compensation.

Ntim et al. (2015) have examined the relationship between executive remuneration and firm

performance using a three-stage least squares (3SLS) simultaneous equation framework and

found improved executive compensation and performance relationship in case of 3SLS

model.

Studies in the Indian context

The literature on executive remuneration and firm performance linkages in the Indian context

is quite limited. Ramaswamy et al. (2000) studied CEO remuneration of top 150 companies

listed on the Bombay Stock Exchange and reported negative relationship among executive

compensation and ownership levels in family-controlled companies during 1992-1993. The

recent studies include:

Ghosh (2006) using panel data approach of 5 years (1997-2002) studied a sample of 462

Indian manufacturing firms and found firms return on assets taken as proxy of firm

performance had a positive and marginally significant influence on CEO compensation.

Chakrabarti et al., 2011 studied companies listed on the Bombay Stock Exchange for seven

years (2004–2010) and reported positive association between CEO remuneration and firm

size (measured by market capitalisation, assets, and sales) and the proportion of promoter

holding.

Aggarwal and Ghosh (2015) have explored the impact of directors’ compensation on the

firm’s value. The study found that the performance indicators (from investors perspective)

indicated no significant relation of the increase in the firm’s performance with the increase in

directors’ remuneration. But, from the accounting viewpoint, there exists a positive

correlation between the two. The authors conclude that the directors’ compensation has a

positive effect to the intrinsic value, but has no effect on the extrinsic value of the firm.

Raithatha and Komera (2016) have examined the relationship between executive

compensation and firm performance among Indian firms by employing the system

generalized methods of moments (GMM) estimator and could not find evidence of pay–

performance relationship among the sample firms.

After reviewing the available literature, it is quite clear that a majority of the work is carried

out in developed countries. In context of India, executive remuneration of public limited

companies was heavily regulated by government till 2002 which makes it interesting to see

the trends after the deregulation. Further, the research on relationship between executive

compensation and firm performance has given mixed results. Many researchers over the

years have confirmed positive relationship at the same time numerous studies could not

establish strength of this relationship which they attribute to other factors of the organization

which could influence executive compensation or firm performance. In the same line, the

paper attempts to fill the vacuum by studying the past trends of executive compensation in

India and also tries to establish its linkages with firm performance after controlling for other

firm characteristics like firm size, governance variables etc.

3. Data and methods

3.1 Data

The study c a n be broadly divided into two parts: first part of the study empirically

examines the pattern of growth in executive compensation over the last 17 years for 30 major

listed companies included in BSE SENSEX. It studies the past trends and patterns using

yearly data of executive compensation paid at managerial level from 2002 till 2019. In the

second part it studies the relationship between executive compensation, corporate governance

and firm performance variables. The data of executive compensation and firm performance

measures was extracted from Prowess1database. Finally, panel data approach was followed to

empirically investigate the relationship between executive compensation variable, corporate

governance variables and various firm performance variables.

The alternative executive compensation, firm performance and corporate governance

measures are described in Table 1. As we examine the relationship between pay and

performance, we consider consolidated executive compensation and its components as the

proxy for pay. We consider both accounting measures as well as market performance

measures to represent firm performance, we use return on asset (ROA), Profit before Interest and

Taxes (PBIT) as the accounting based measures of firm performance. Further, annual stock return

(RET) and enterprise value are considered as the market based measures of firm performance.

Further, we consider firm specific variables such as size, leverage, and risk as they could influence the

pay–performance relationship. The description of the variables is provided in Table 1.

The PROWESS database is similar to Compustat database of US firms. It is increasingly employed for getting

firm-level analysis of Indian industry and contains information on around 25,000 companies, either listed on

stock exchanges or the major unlisted companies.

Table 1 Description of Variables used in the analysis

S.No Variable Full Form Definition

Panel A: Executive Compensation

1. EXCOMP Total Executive Remuneration

Total Compensation paid to senior executives in an

accounting year.

2. Salary

Salary Component of Total

Remuneration Salary paid to senior executives in an accounting year.

3.

Bonus/Commissi

on

Component of Bonus/Commission

received Bonus paid to senior executives in an accounting year.

4. Perquisites Component of Perquisites received

Perquisites paid to senior executives in an accounting

year.

Panel B: Corporate Governance Measures

5. IM Independent Members on the Board Number of Independent Members on the board.

6. BS Board Size Total number of members on Board.

Panel C: Firm Performance variables

7. EV Enterprise Value

Market capitalization plus debt, minority interest and

preferred shares, minus total cash and cash equivalents.

8. TR

Total Shareholders Returns/Annual

stock return

The financial gain that results from a change in the

stock's price plus any dividends paid by the company

9.

ROA

Ratio of earnings before interest and

taxes to total assets Net profit divided by total assets

10. PBDITA

Profit before dividend, interest and

tax Natural log of Profit before dividend, interest and tax

Panel D: Control variables

11. SALES Net Sales Natural log of Sales

12.

T_EXPENSES Total expenditure

Natural log of all expenditure incurred by a firm in an

accounting year.

13.

DE Debt to Equity Ratio

14. BETA Measure of Market Risk

It refers to company’s beta calculated considering BSE

Sensex as the market index

3.2 Econometric Methods

Before proceeding to our analysis, study uses Levin et al. (2002) and Lm et al.(2003) unit

root test (hereafter referred to as LLC and IPS test, respectively) to examine the order of

integration of all variables in a panel framework. Further, we test whether there are two-way

causal links between executive pay and firm performance by conducting Dumitrescu and

Hurlin (2012) heterogeneous panel non-causality tests. We explore the short-run dynamic

bivariate panel causality among the variables by using a model that supports the presence of

heterogeneity across the cross-sections. A simple approach is proposed by Dumitrescu and

Hurlin (2012) for testing the null hypothesis of homogeneous non-causality against the

alternative hypothesis of heterogeneous non-causality. This test has to be applied on

stationary data series using the fixed coefficients in a vector autoregressive (VAR)

framework. The significance of this test is that it allows for having dissimilar log structures

and also heterogeneous unrestricted coefficients across the cross-sections under both

hypotheses. Under the null hypothesis, no causality in any cross-section is tested against the

alternative hypothesis of causality at least for few cross-sections. The Wald statistics for

testing Granger non-causality are computed for each of the cross-sections separately. Then,

the panel test value is acquired by taking the cross-sectional average of individual Wald

statistics. Dumitrescu and Hurlin (2012) argue that this panel test value converges to a normal

distribution under the homogeneous non-causality hypothesis when T goes to infinity first,

and then N also goes to infinity.

We then estimate long run relationship among the variables to calculate pay-performance

sensitivities and elasticities as denoted by Eq. (1) using panel fixed effects (FE) estimators.

The FE estimator effectively controls the sample firms’ unobservable fixed effects. The

model to be tested different components of executive compensation as dependent variable

and board size, number of independent directors in the board, firm performance measures and

control variables as independent variables.

𝑬𝑿𝑬𝑪 = 𝜶𝟏 + 𝜷𝟏𝑰𝑴𝒕 + 𝜷𝟐𝑩𝑺 + 𝜷𝟑𝑭𝑷𝟏 𝒕 + 𝜷𝟒𝑺𝑨𝑳𝑬𝑺𝒕 + 𝜷𝟓𝑫𝒆𝒃𝒕/

𝑬𝒒𝒖𝒊𝒕𝒚 𝒕+𝜷𝟔𝑩𝒆𝒕𝒂 𝒕 + 𝒆𝒕 Equation 1

4. Results and Discussion

In this section, we discuss the results of our data analysis. Figure 1 presents the trends of total

executive compensation paid to executives for these sample firms over the years. We can

clearly see an increasing trend of salaries paid to higher management especially after 2012.

For period ranging from 2002 till 2012, we could observe a steady growth in executive

compensation followed by a steep growth especially after 2013 till 2016. The figure also

depicts a dip in compensation in the last three years.

Figure 2 represents the growth in average salary paid to executives. We can clearly see the

peaks in the data indicating revision of salary packages every second year. Further, the graph

also indicates a steady rise in salary after 2015 for these companies.

Figure 1 Total Executive Compensation paid to

the sample companies

Figure 2 The growth in Executive Compensation paid

to the sample companies

Figure 4 Components of Executive Remuneration (Aggregate) for last 17 years.

Figure 3 The ratio of Total Executive Compensation and PAT.

Figure 3 presents the ratio of total executive compensation to profit after tax. It also indicates

that the executive compensation rose steeply after 2014 and the ratio which was stable at 10

0

200

400

600

800

1000

1200

1400

1600

200220042006200820102012201420162018

Total Executive Compensation (Rs. Crore)

Total Executive Compensation (Rs. Crore)

1.92

50.0646.77

13.8316.07

28.74

10.44

19.67

3.861.87

22.75

13.22

67.11

21.46

-11.13

3.63

-16.69

-40.00

-20.00

0.00

20.00

40.00

60.00

80.00

2002 2004 2006 2008 2010 2012 2014 2016 2018

Growth in Executive Compensation

Change in Exec. Compensation

10.77

7.97

10.8311.2511.0010.2310.58

11.0811.64

10.56

9.23

10.3610.70

16.50

19.74

17.5217.23

12.20

0.00

5.00

10.00

15.00

20.00

25.00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

RATIO OF TEC/PAT

Salary29%

Directors sitting fees

1%

Contribution to PF

1%

Bonus/Commission45%

Perquisites12%

Retirement benefits

4%

Stock Options

Amt7% Other

Remuneration

1%

Components of Executive Remuneration (Aggregate)

percent for almost 12 years almost doubled within a time frame of 2 years after 2014. In line

to our observations from the previous figures, it also indicates a drop in the ratio calculated

after 2016. Figure 4 represents the different components of executive compensation. The

percentages have been calculated by adding the amount received in each category for the last

17 years. Three main components i.e. Bonus, Salary and Perquisites emerge as most

important constituents of executive compensation.

Table 2 presents the details of highest executive remuneration being paid along with exact

amount being disclosed in the annual statements. The highest package for our sample

companies has been received by Vineet Nayyar in 2016 while acting as Vice Chairperson of

Tech Mahindra Ltd. More interestingly, the top ten remuneration packages have been

dominated by two companies (Tech Mahindra Ltd. And Larsen & Toubro Ltd.) from the

sample of 30 companies.

Table 2 A Snapshot of Highest Executive Compensation paid from 2002 till 2019

Rank Company Name Year

Director Name Designation

Total Remuneration (Rs. Crores)

1 Tech Mahindra Ltd. 2016

VINEET NAYYAR Vice Chairperson 181.786

2 Tech Mahindra Ltd. 2015

C P GURNANI

Managing Director & Chief Executive Officer 165.570

3 Tech Mahindra Ltd. 2017

C P GURNANI

Managing Director & Chief Executive Officer 150.707

4 Tech Mahindra Ltd. 2018

C P GURNANI

Managing Director & Chief Executive Officer 146.192

5 Larsen & Toubro Ltd. 2018 A M NAIK Chairperson 139.783

6 Tech Mahindra Ltd. 2015

VINEET NAYYAR Executive Vice Chairperson 119.911

7 Hero Motocorp Ltd. 2019

PAWAN MUNJAL

Chairperson, Managing Director & Chief Executive Officer 80.410

8 Larsen & Toubro Ltd. 2017 A M NAIK Executive Chairperson 78.910

9 Hero Motocorp Ltd. 2018

PAWAN MUNJAL

Chairperson, Managing Director & Chief Executive Officer 75.440

10 Larsen & Toubro Ltd. 2016 A M NAIK Executive Chairperson 66.140

Proceeding further in the direction of understanding the changes in patterns of different

components of executive remuneration, we study the year wise composition of the

remuneration paid to executives of our sample firm for the last five years. As a benchmark

for comparison past seventeen years average figures of the sample companies were also

calculated in Table 3. It is quite evident that there has been significant shift in how executives

have been paid remuneration in the last five years. The salary component has witnessed a

significant increase and at the same time the proportion of bonus/commissions and

perquisites have declined substantially. Also, remuneration in the form of stock options have

also gained importance in the recent years.

Table 3 Component wise segregation of Executive Compensation paid from 2015 till 2019

Year Salary Bonus/ Commission Perquisites

Retirement Benefits Stock Options

Other Remuneration

2015 24% 38% 33% 1% 1% 3%

2016 29% 36% 9% 4% 19% 2%

2017 32% 32% 8% 5% 19% 6%

2018 35% 26% 10% 8% 16% 6%

2019 46% 33% 7% 2% 8% 4%

17 years Average 29% 45% 12% 4% 7% 3%

Other includes directors sitting fees and contribution to provident fund

In the next step we test the correlation among the variables of our study. The results are

reported in Table 4. The findings indicate that four different variables of executive

compensation display positive correlations with all of the variables except total return (TR)

and beta. These findings give preliminary evidence that executive compensation have

considerable positive correlations with firm performance variables, supporting that higher

firm performance may lead to higher executive compensation. However, correlations have the

ability to quantify only contemporaneous relationships between variables without reflecting

the time dimension. In addition, correlation do not provide evidence of the direction of

causation. For these reasons, causality tests are needed as well as estimations on pay and

performance sensitivities and elasticities. In particular, the calculation of pay-> performance

elasticities enables us to differentiate the reward from the motivational effect, which has been

necessarily neglected in previou

Table 3 Unconditional correlations.

TOTAL EXPENSES ROA EVALUE PBDITA TR BETA BS IM

Total

Remuneration 0.33*** 0.15*** 0.33*** 0.21*** 0.00 -0.10** 0.29*** 0.35***

Bonus/

Commission 0.25*** 0.32*** 0.34*** 0.03 -0.01 -0.02 0.25*** 0.18***

Salary 0.39*** 0.15*** 0.35*** 0.26*** 0.04 -0.04

0.28***

0.26***

Perquisites 0.27*** 0.17*** 0.34*** 0.17*** -0.08* 0.03 0.16*** 0.21***

Other 0.40*** 0.10*** 0.36*** 0.36*** -0.01 -0.14*** 0.19*** 0.23***

Panel unit root results

Table 5 presents the results of LLC and IPS unit root tests for the level and first differenced

series of the all variables used in the study. Results indicate that null hypothesis of a unit root

is rejected for LLC and IPS tests at level for all the variables except beta. However, after

taking the first difference of variable beta, both tests reject the null hypothesis at 1 per cent

significance level. Thus, we conclude that all the series except beta are stationary and

integrated of order zero, i.e. I(0). Thus cointegration tests and long-run relationships between

the variables are not applicable to our data.

Table 5 Panel unit root test results

Test Variables

LLC Test IPS Test

Inference At Level At 1st difference At Level At 1st difference

Log Total Remuneration -7.51* -18.41* -2.13** -14.72* I(O)

Log of Bonus/Commission

-31.65* -49.53* -13.43* -23.77* I(O)

Log of Perquisites -7.62* -12.75* -6.58* -14.73* I(O)

Log of Total Expenses -8.55* -7.54* -1.26*** -7.06* I(O)

Log of ROA -10.46* -17.69* -7.78* -16.78* I(O)

Log of Sales -9.17* -29.47* -6.21* -10.52* I(O)

Log of EV -11.43* -25.82* -7.52* -19.61* I(O)

Log of TR -19.30* -23.50* -15.70* -24.13* I(O)

Log of Total Assets -12.16* -32.85* -5.88* -14.91* I(O)

Log of PBDITA -4.50* -13.81* -0.05 -12.12* I(O)

DE 59.67 -1625.86* -8.04* -286.75* I(O)

Beta -0.61 -13.64* 1.58 -10.93* I(1)

Log of IM -4.07* -21.48* -4.30* -18.45* I(O)

Log of BS -4.19* -15.76* -4.53* -14.60* I(O)

* significant at 1% ,** significant at 5%,*** significant at 10%,

Heterogeneous panel non-causality test

The results from the causality tests summarised in Table 6 reveal the existence of significant

two-way causality between executive pay and all four performance measures, suggesting that

executive pay and performance mutually affect each other. It is straightforward to interpret

the causation from performance to pay, as found in some prior studies (Firth et al., 2006;

Kato & Long, 2006), as reward is performance based.

However, the significant reverse causation running from pay to performance, which is shown

with one lag, indicates that there is also feedback from pay to performance, thus supporting

Hypothesis 2. This interplay between executive pay and performance constitutes a distinctive

feature of quoted companies in China that is difficult to detect in the USA and UK, owing to

the existence of long-term financial incentives in executive pay.

Table 6 Results of Heterogeneous panel causality results.

Null Hypothesis: W-Stat. Zbar-Stat. Prob.

EVALUE does not homogeneously cause TOTAL_REMUNERATION 7.285 8.653 0.00

TOTAL_REMUNERATION does not homogeneously cause EVALUE 71.808 123.984 0.00

PBDITA does not homogeneously cause TOTAL_REMUNERATION 10.706 14.767 0.00

TOTAL_REMUNERATION does not homogeneously cause PBDITA 14.949 22.352 0.00

TR does not homogeneously cause TOTAL_REMUNERATION 2.402 -0.184 0.85

TOTAL_REMUNERATION does not homogeneously cause TR 2.339 -0.283 0.776

ROA does not homogeneously cause TOTAL_REMUNERATION 4.609 3.713 0.000

TOTAL_REMUNERATION does not homogeneously cause ROA 24.139 37.520 0.000

PBDITA does not homogeneously cause TOTAL_REMUNERATION 10.706 14.767 0.000

TOTAL_REMUNERATION does not homogeneously cause PBDITA 14.949 22.352 0.000

Panel Least Square- FE

Finally, we test our formulated model by employing panel least square method where

executive compensation is taken as dependent variable and firm performance variables,

corporate governance variables and control variables are taken as independent variables. The

model has been explained in equation 1. From specifications 1 to 4, in Table 7 considers total

remuneration as dependent variable and in case of specifications 5-8 which considers salary

as independent variable. Similarly, Table 8 presents the results of linkage between the

amount of bonus/commission and perquisites with firm performance variables.

The results from the panel fixed effect show that out of the four performance measures

considered in our first model only enterprise value is statistically significant (i.e., total

executive compensation is regressed on different performance measures). Similarly, when

salary component is regressed on other firm performance variables, we also get similar

results. The other three variables. This positive association between executive pay and

performance again indicates that an increase in firm performance will result in a rise in

executive reward.

The variable for firm size has a positive sign and is statistically significant. This result

corroborates previous studies around the world, which have found that there is a positive link

between firm size and executive pay (Kato & Long, 2006; Tosi et al.,2000). At the same

time, the variables for the board size is statistically significant. This may reflect the formation

and function of these boards in the formation and function of these boards in the Indian

context, as discussed above in "The executive pay literature".

Again, the size of the board of directors has great impact on executive compensation,

indicating that board size does play a significant role on executive remuneration.

For control variables such as sample firms’ leverage and market risk report the significant

negative and positive influence on their executive compensation respectively. From

specifications 1 and 5, it is evident that executive compensation is positively influenced by

the firm’s contemporaneous performance

We find significant pay–performance relationship among the larger sample firms, and the

pay–performance relationship seems to be absent among the smaller sample firms

suggesting limited evidence for executive pay affecting firm performance.

Table 7 Results of panel least square (FE)

Variable 1 2 3 4 5 6 7 8

Total Remuneration Salary

EVALUE 0.276*** 0.267***

TR -0.8 0.036

PBDITA -0.14 0.13

ROA -0.55 0.19

TOTAL_EXPENSES/sales

-0.11 -0.02 -0.18 -0.17 -0.395 -

0.511** -

0.54** -0.53**

IM 0.62 0.47 0.75 0.76 -0.488 -0.704 -0.38 -0.39

LBS 2.704*** 2.75** 2.88** 2.88** 4.068*** 4.186**

* 4.32**

* 4.31***

BETA -0.98*** -

0.78** -

0.90** -0.88** -0.77 -0.74 -0.77 -0.79

DE 0.145** 0.16** 0.19** 0.18** -0.039 -0.035 -0.02 -0.02

C 3.896** 4.19** 4.92**

* 4.73*** 2.559

4.455***

3.61** 3.91**

R2 0.512 0.465 0.495 0.496 0.438 0.412 0.43 0.43

Table 8 Results of panel least square (FE)

Variable 1 2 3 4 5 6 7 8

Bonus_ Commission Perquisites

EVALUE -0.01

0.261*

TR -0.025 -0.07

PBDITA 0.579* 0.640*

ROA 1.48* 1.69*

Sales -

1.014***

-

0.996***

-

1.212*** -1.22***

-

0.743** -0.79**

-

1.066*** -1.093***

IM 0.086 0.225 0.095 0.15 0.379 0.31 0.5 0.438

LBS 2.551 2.474 2.581 2.56 0.627 0.88 0.905 0.891

BETA -0.433 -0.375 -0.366 -0.41 -0.426 -0.47 -0.362 -0.473

DE 0.153 0.145 0.131 0.17 0.074 0.09 0.071 0.112

C 6.097*** 5.999*** 4.458** 5.57*** 5.062** 6.45*** 4.677* 5.977*

R2 0.595 0.595 0.598 0.601 0.448 0.434 0.448 0.448

Conclusion

The study tried to analyze the trends and patterns in executive compensation in India over the

past 17 years. The research initially presented the past trends of executive remuneration and

then investigated its relationship between firm performance variables and the corporate

governance variables. The study involves an in-depth analysis for the emerging market, India.

It examines 30 companies, which are among the largest listed companies on Bombay stock

exchange.

The results of initial analysis found substantial increase in executive compensation over the

past five years especially in case of Hero Moto Corp, L&T and Reliance Industries. Further,

we found significant differences in executive compensation as compared to other firms with

similar profitability. The pay difference can be logically attributed to low compensation by

peer group or excessive remuneration by these companies. Additionally, increase in

compensation with the simultaneous decline in earnings puts the management of certain

companies under suspicion of taking decision in self-interest and ignoring shareholders’

interests.

Further, our final results confirm positive relationship in case of Sales, Dividend and Long

term EPS. However, contradictory results arrive when we examine the relationship with

respect to Return on Net worth (RONW) and Profit after Tax (PAT).

In case of our results from the empirical model, out of the three corporate governance

variables i.e. Board Size (BS), Board Meetings (BM) & Number of Independent Members

(IM) only number of board meetings have a significant influence on executive compensation.

Further, the inverse relationship with two governance variables (Board Size and Board

Meetings) and executive compensation was established indicating larger and active boards

exercise more control on paying excessive compensation to its executives. Furthermore,

positive relationship reported between independent members on the board and executive

remuneration could be linked to lack of decision making powers with Independent directors

on the board or due to cross board phenomena as highlighted by various studies done in

Indian context(Arora and Sharma,2015).

The positive relationship reported among executive compensation and firm performance

measures is in line with past studies (Chakrabarti et al., 2011; Ghosh, 2006; Ozkan, 2011).

However, our results contradict if we compare our established relationship of governance

variables and executive remuneration highlighting the need to strengthen governance

mechanism in Indian scenario (Guest, 2010; Alonso and Aperte, 2011).

Finally, future research could encompass a larger sample of companies. Also, a comparison

could be done for public sector and private sector companies. The present study is done by

ignoring components which are indirectly related to executive compensation (stock holdings)

therefore not only the cash compensation but the total compensation should be considered for

such investigations. Similarly, there has been debate on the other factors which influence

managerial remuneration like managerial skills, market forces etc. for example few people

may demand extraordinary remuneration because of their leadership skills which have to be

modeled in while examining managerial remuneration and firm performance linkages.

References

Aggarwal, R, and Ghosh, A. (2015) ‘Director’s remuneration and correlation on firm’s

performance: A study from the Indian corporate’, International Journal of Law and

Management, Vol. 57 No.5, pp.373-399

Alonso, P. and Aperte, L.A., (2011) ‘CEO Remuneration and Board Composition as

Alternative Instruments of Corporate Governance’, Working Paper, University of Valladolid

Boschen, J.F and Smith, K.J., (1995) ‘You can pay me now and you can pay me later: The

dynamic response of executive remuneration to firm performance’, Journal of Business, Vol.

68, No. 4 , pp. 577-608

Brick, I.E., Oded, P. and John, K., (2006) ‘CEO remuneration, director remuneration, and

firm performance: Evidence of cronyism?’, Journal of Corporate Finance, Vol. 12 No.3,

pp.403-423

Chakrabarti, R., Subramanian, K., Yadav, P. K., & Yadav, Y. (2012). 21 Executive

compensation in India. Research handbook on executive pay, 435.

Chakrabarti, R., Subramanian, K., Yadav, P.K. and Yadav, Y. (2011) ‘Executive

compensation’, in Thomas, R and Hill, J. (Eds.): Handbook on Executive Compensation,

Edgar Elgar, Gloucestershire, UK, pp.435–465

Dong, M. and Aydin, O., ‘Institutional investors and director pay: An empirical study of UK

companies’, Journal of Multinational Financial Management, Vol.18 No.1, pp.16-29

Doucouliagos, H., Graham, M. and Haman, J., (2012) ‘Dynamics and convergence in chief

executive officer pay’, Available at

SSRN: https://ssrn.com/abstract=2033535 or http://dx.doi.org/10.2139/ssrn.2033535

Dumitrescu, E. I., & Hurlin, C. (2012). Testing for Granger non-causality in heterogeneous

panels. Economic modelling, Vol. 29, No.4, pp.1450-1460.

Firth, M., Fung, P.M. and Rui, O.M., (2007). How ownership and corporate governance

influence chief executive pay in China's listed firms. Journal of Business Research, Vol. 60

No.7, pp.776-785

Frydman, C. and Dirk, J., (2010) ‘CEO remuneration’, National Bureau of Economic

Research, No. w16585

Ghosh, A. (2006) ‘Determination of executive compensation in emerging economies:

evidence from India’, Journal of Emerging Markets Finance and Trade, Vol. 42, No. 3,

pp.66–90.

Ghosh, A., (2003) ‘Board structure, executive remuneration and firm performance in

emerging economies: Evidence from India’, Indira Gandhi Institute of Development

Research, Working Paper, 91-9819090266.

Guest, P. M. (2010). Board structure and executive pay: evidence from the UK. Cambridge

Journal of Economics, Vol. 34 No. 6, pp. 1075-1096.

Hubbard, R.G. and Darius, P., (1995) ‘Executive pay and performance evidence from the US

banking industry’, Journal of Financial Economics, Vol. 39 No.1, pp.105-130

Jaiswall, S. S. K., & Bhattacharyya, A. K. (2016). Corporate governance and CEO

compensation in Indian firms. Journal of Contemporary Accounting & Economics, Vol.12,

No. 2, pp. 159-175.

Jensen, M.C. and Kevin J.M., (1990) ‘Performance pay and top-management

incentives’, Journal of Political Economy, Vol. 98 No. 2, pp. 225-264.

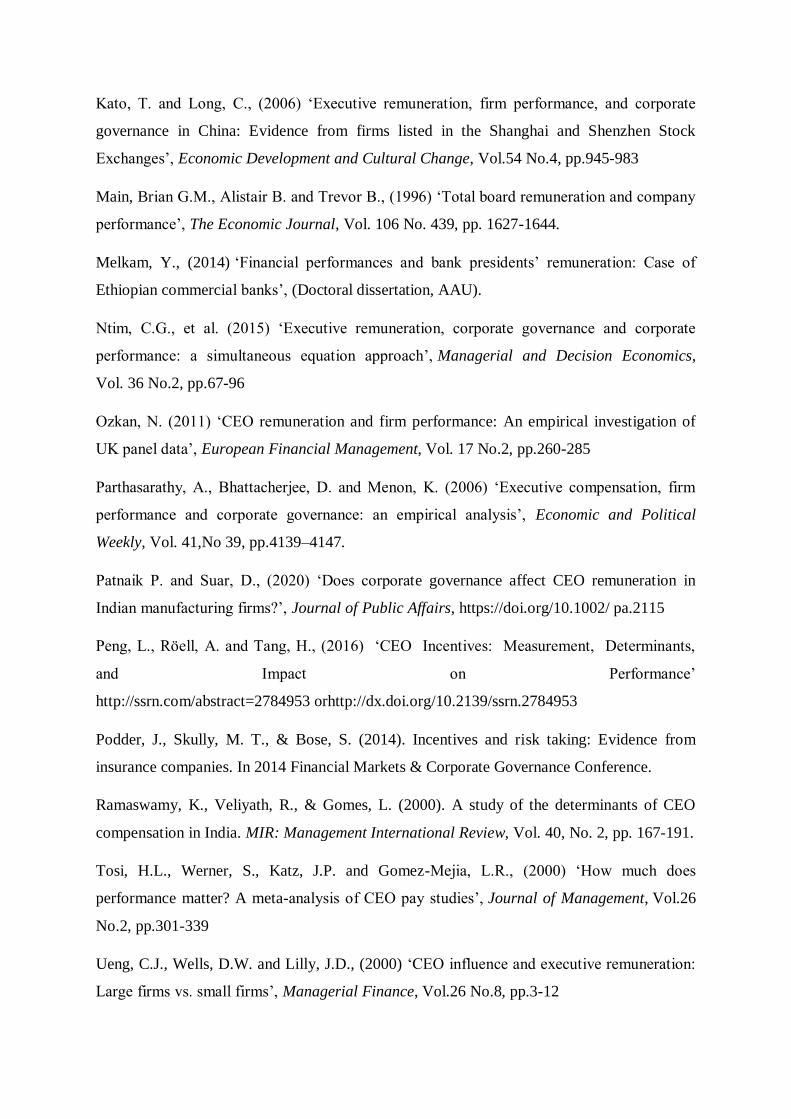

Kato, T. and Long, C., (2006) ‘Executive remuneration, firm performance, and corporate

governance in China: Evidence from firms listed in the Shanghai and Shenzhen Stock

Exchanges’, Economic Development and Cultural Change, Vol.54 No.4, pp.945-983

Main, Brian G.M., Alistair B. and Trevor B., (1996) ‘Total board remuneration and company

performance’, The Economic Journal, Vol. 106 No. 439, pp. 1627-1644.

Melkam, Y., (2014) ‘Financial performances and bank presidents’ remuneration: Case of

Ethiopian commercial banks’, (Doctoral dissertation, AAU).

Ntim, C.G., et al. (2015) ‘Executive remuneration, corporate governance and corporate

performance: a simultaneous equation approach’, Managerial and Decision Economics,

Vol. 36 No.2, pp.67-96

Ozkan, N. (2011) ‘CEO remuneration and firm performance: An empirical investigation of

UK panel data’, European Financial Management, Vol. 17 No.2, pp.260-285

Parthasarathy, A., Bhattacherjee, D. and Menon, K. (2006) ‘Executive compensation, firm

performance and corporate governance: an empirical analysis’, Economic and Political

Weekly, Vol. 41,No 39, pp.4139–4147.

Patnaik P. and Suar, D., (2020) ‘Does corporate governance affect CEO remuneration in

Indian manufacturing firms?’, Journal of Public Affairs, https://doi.org/10.1002/ pa.2115

Peng, L., Röell, A. and Tang, H., (2016) ‘CEO Incentives: Measurement, Determinants,

and Impact on Performance’

http://ssrn.com/abstract=2784953 orhttp://dx.doi.org/10.2139/ssrn.2784953

Podder, J., Skully, M. T., & Bose, S. (2014). Incentives and risk taking: Evidence from

insurance companies. In 2014 Financial Markets & Corporate Governance Conference.

Ramaswamy, K., Veliyath, R., & Gomes, L. (2000). A study of the determinants of CEO

compensation in India. MIR: Management International Review, Vol. 40, No. 2, pp. 167-191.

Tosi, H.L., Werner, S., Katz, J.P. and Gomez-Mejia, L.R., (2000) ‘How much does

performance matter? A meta-analysis of CEO pay studies’, Journal of Management, Vol.26

No.2, pp.301-339

Ueng, C.J., Wells, D.W. and Lilly, J.D., (2000) ‘CEO influence and executive remuneration:

Large firms vs. small firms’, Managerial Finance, Vol.26 No.8, pp.3-12

Van Essen, M., Heugens, P. P., Otten, J., & van Oosterhout, J. H. (2012). An institution-

based view of executive compensation: A multilevel meta-analytic test. Journal of

International Business Studies, Vol.43, No. 4, pp. 396-423.

Zhou, X., (2000) ‘CEO pay, firm size, and corporate performance: evidence from

Canada’, Canadian Journal of Economics, Vol.33 No.1, pp.213-251

LAL BAHADUR SHASTRI INSTITUTE OF MANAGEMENT, DELHI

PLOT NO. 11/7, SECTOR-11, DWARKA, NEW DELHI-110075

Ph.: 011-25307700, www.lbsim.ac.in