transforming adverse media screening a new paradigm

TRANSCRIPT

Transforming Adverse Media ScreeningA New Paradigm Powered by AI

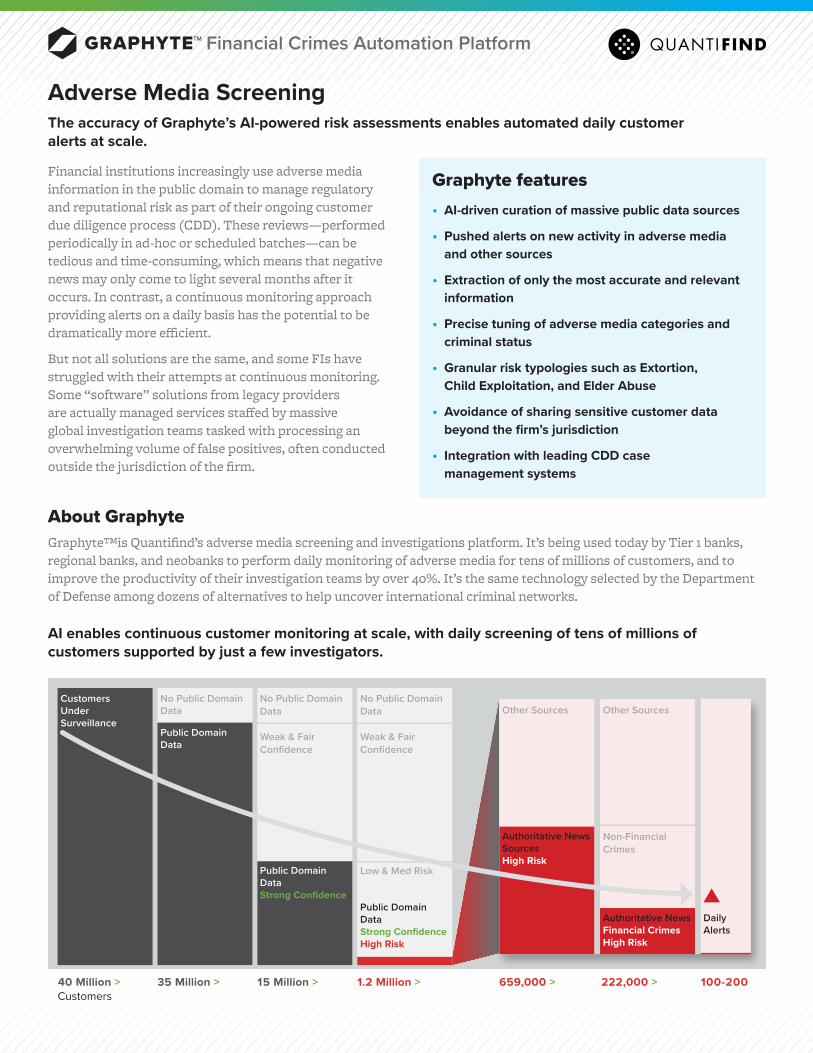

Adverse Media Screening The accuracy of Graphyte’s AI-powered risk assessments enables automated daily customer alerts at scale.

Financial Crimes Automation Platform™

Financial institutions increasingly use adverse media information in the public domain to manage regulatory and reputational risk as part of their ongoing customer due diligence process (CDD). These reviews—performed periodically in ad-hoc or scheduled batches—can be tedious and time-consuming, which means that negative news may only come to light several months after it occurs. In contrast, a continuous monitoring approach providing alerts on a daily basis has the potential to be dramatically more efficient.

But not all solutions are the same, and some FIs have struggled with their attempts at continuous monitoring. Some “software” solutions from legacy providers are actually managed services staffed by massive global investigation teams tasked with processing an overwhelming volume of false positives, often conducted outside the jurisdiction of the firm.

Customers40 Million > 15 Million > 1.2 Million > 659,000 > 222,000 > 100-20035 Million >

Public DomainData

Public DomainDataStrong Confidence

Public DomainDataStrong ConfidenceHigh Risk

No Public DomainData

No Public DomainData

Weak & Fair Confidence

No Public DomainData

Weak & Fair Confidence

Low & Med Risk

Authoritative NewsFinancial CrimesHigh Risk

Authoritative News SourcesHigh Risk

Other Sources Other Sources

Non-Financial Crimes

DailyAlerts

CustomersUnderSurveillance

AI enables continuous customer monitoring at scale, with daily screening of tens of millions of customers supported by just a few investigators.

About GraphyteGraphyte™is Quantifind’s adverse media screening and investigations platform. It’s being used today by Tier 1 banks, regional banks, and neobanks to perform daily monitoring of adverse media for tens of millions of customers, and to improve the productivity of their investigation teams by over 40%. It’s the same technology selected by the Department of Defense among dozens of alternatives to help uncover international criminal networks.

Graphyte features• AI-driven curation of massive public data sources

• Pushed alerts on new activity in adverse media and other sources

• Extraction of only the most accurate and relevant information

• Precise tuning of adverse media categories and criminal status

• Granular risk typologies such as Extortion, Child Exploitation, and Elder Abuse

• Avoidance of sharing sensitive customer data beyond the firm’s jurisdiction

• Integration with leading CDD case management systems

Visit Quantifind’s website at www.quantifind.com or send us an email at [email protected] to learn more about how Graphyte’s unique AI technology and software-only approach make customer monitoring efficient and scalable.

Here are a few of the ways that Quantifind’s decade-plus of data science R&D and Fortune 50 deployments have changed the paradigm for adverse media screening:

The Old Way Graphyte™

Screening service combining software and analysts; prone to worker disruptions and requiring data sharing outside of jurisdictions.

100% subscription-based SaaS solution with end-to-end encryption.

Results with the wrong person or company identified 90% of the time.

AI-driven, high confidence entity resolution with 90% accuracy.

Human-curated lists of bad actors that quickly become outdated, in the model of PEP and sanctions screening.

Limitless risk assessments generated in real time using all available data, powered by full-text search against millions of articles.

Manually created, narrowly defined, static risk definitions that miss emergent threats.

Dynamic risk typologies that evolve with the threat space.

Google searches required to confirm hits and add context before decisioning; wasted time, inconsistent process, and non-secure methods.

Programmatic search performed anonymously and integrated with open source searches; review of only relevant results in a single purpose-built application.

Search machine-translated foreign-language sources for Anglicized names with English-only risk assessment.

Search foreign-language sources and assess risk in the native languages, using non-Roman character sets including Chinese.

Simple fuzzy matching algorithms and string distance metrics, unaware of cultural name variant conventions or name prevalence.

Name science quantifies expected name variants and name frequency within a specific country to assess the probability of a true match.

Graphyte uses a unique combination of external data sources, predictive risk typology models, and patented data management technologies to inform risk profiling and segmentation. The speed and accuracy achieved enable automation of ongoing continuous monitoring at scale. Results are summarized via Graphyte APIs and through the GraphyteSearch investigation application. Actionable information on individuals, organizations, and their relationships expands coverage to better manage reputational risk and fraud. Machine learning models and risk typologies optimize accuracy and relevancy ensuring that ongoing alerts are on target.

™

TRANSFORMING ADVERSE MEDIA SCREENING A New Paradigm Powered by AI

Arin Ray

This is an authorized reprint of a Celent report with the same title. The reprint was prepared for Quantifind, but the analysis has not been changed. For more information, please contact Celent at [email protected].

Transforming Adverse Media Screening

© CELENT

CONTENTS

Executive Summary .......................................................................................................... 3

Introduction ..................................................................................................................... 5

Adverse Media Screening Constrained by Legacy Technology ............................................ 6

Transforming Adverse Media Screening with AI ................................................................ 8

A New Screening Paradigm Powered by AI ...................................................................... 11

Considerations for Adoption ........................................................................................... 13

Path Forward ................................................................................................................. 16

Leveraging Celent’s Expertise.......................................................................................... 17 Support for Financial Institutions ......................................................................................................... 17 Support for Vendors.............................................................................................................................. 17

Related Celent Research ................................................................................................. 18

Transforming Adverse Media Screening Executive Summary

© CELENT 3

EXECUTIVE SUMMARY Combatting financial crime in the digital era will require financial institutions (FIs) to strengthen and widen their adverse media screening coverage while improving efficiency and effectiveness of the process. Artificial Intelligence (AI)-powered solutions have the potential to transform adverse media screening and enable more frequent, dynamic, and proactive monitoring of customer risk.

Critical money laundering-related information on a financial institution’s clients may be found in media sources. However, traditional technology used in adverse media screening is proving inefficient and ineffective in scanning a vast and rapidly expanding media universe, limiting its application to known high-risk actors. Financial institutions are turning to next generation technology to strengthen their adverse media screening process.

In the last five years, developments in next generation technology such as artificial intelligence and machine learning (ML) have advanced significantly, with noteworthy adoption in financial services including in anti-money laundering (AML) operations.

AI technology has the potential to transform adverse media screening. Specifically, Natural Language Processing (NLP) can greatly improve analysis of textual and unstructured data analysis and can bring about a paradigm change in adverse media screening.

• NLP techniques power intelligent analysis of textual information by goingbeyond keyword-based search and by identifying context, relevance, andrelationships embedded within news articles.

• By assessing the context, they can flag the type of adverse activity and mapthem with AML typologies. For each search result, AI systems can providescores that enable ranking of search results according to their relevance andriskiness.

• FIs can then devote their scarce resources to the riskiest and most relevantresults while routing less risky ones to junior analysts or suppressing or auto-closing them.

AI-driven solutions enable expanding scale and breadth of coverage exponentially by analyzing a myriad of sources, including those in foreign languages. This automation-driven approach removes human biases and errors and improves investigation consistency. It also ensures auditability because an software systems can provide and record the rationale for its suggestions.

FIs have started exploring the application of AI in adverse media. We have come across impressive outcomes reported by early adopters, such as reduction in case investigation time by over 75%, accelerating corporate client onboarding time to 2 days from 2 weeks, and improving coverage of AML program.

Transforming Adverse Media Screening Executive Summary

© CELENT 4

AI-powered adverse media screening has the potential to go above and beyond efficiency improvements.

• A natural extension of AI application will be to automatically link and analyze entities across adverse media as well as other screening sources such as sanction lists, watchlists, company registries, beneficiary information, and other sources.

o This can enable FIs to take a more integrated and holistic approach in screening.

• Another critical edge that AI-powered solutions can offer is through conducting more frequent screening and client monitoring.

o This will enable FIs to undertake a more proactive and dynamic approach to customer risk monitoring, and empower them to conduct continuous monitoring of clients so that whenever there is adverse media on a client, the systems will trigger an alert prompting immediate reassessment of customer risk.

o Ongoing screening of customer activity will also reveal trends and patterns about evolution of risk for different customer segments that can further inform risk assessment methodology and help in calibrating risk scoring systems.

For smooth implementation and maximum benefit realization, FIs must pay attention to critical issues such as data management, system integration, model governance, and resourcing.

AI is not meant to replace human analysts and their judgments, and humans will still be in charge of decision making while working with AI-based systems. But AI-powered tools can and will augment human analysts by reducing their operational burden in adverse media screening and helping them with advanced insights.

Transforming Adverse Media Screening Introduction

© CELENT 5

INTRODUCTION

Critical money laundering-related information on a financial institution’s clients may be found in media sources. However, traditional technology used in adverse media screening is proving inefficient and ineffective in scanning a vast and rapidly expanding media universe—limiting its application to only known high-risk actors. Combatting financial crime in the digital era will require FIs to strengthen and widen their adverse media screening coverage while improving efficiency and effectiveness of the process.

The key focus of FIs’ AML monitoring activities rely on two pillars: • Watchlist screening, where FIs screen customer names and biographical information against governmental and other lists. • Transaction monitoring, where FIs monitor transactional patterns of their customers.

Adverse media screening has been used sporadically in AML monitoring. While it is recommended by regulators, it is not always mandatory, and legacy technology used for adverse media screening is inefficient and costly. Therefore, FIs generally limit the use of adverse media for due diligence during KYC and periodic refresh on their higher risk clients, and for conducting enhanced due diligence in watchlist screening and transaction monitoring.

Adverse media screening can play a more critical role in AML because regulators increasingly want FIs to scrutinize their clients’ sources of funds and their involvement in different types of financial crime-related activities as well as connections with financial criminals. They also want banks to identify their clients’ involvement in not only the core offenses of money laundering but also on predicate offenses such as human trafficking, corruption, fraud, counterfeiting of currency or products, extortion, and so on.

Today’s rapidly expanding media and open source intelligence sources can contain critical information on a client’s potential engagement in financial crime that may not be covered by watchlist screening, transaction monitoring, and basic adverse media coverage. Financial institutions therefore need to strengthen and widen their coverage of adverse media screening while improving efficiency and effectiveness of the process.

What is Adverse Media?

Adverse media or negative news is any unfavorable information about an individual’s or entity’s potential involvement in financial crime-related activities.

Negative news may be found in several sources. • It could be “traditional” news

outlets like newspapers or broadcast news.

• Negative news can also be found in nontraditional media such as blogs, web posts, social media, and other forums.

Adverse media analysis can play an important role in AML, but traditional technology used to monitor a vast and exponentially growing universe of adverse media sources is proving inefficient and ineffective.

Transforming Adverse Media Screening Adverse Media Screening Constrained by Legacy Technology

© CELENT 6

ADVERSE MEDIA SCREENING CONSTRAINED BY LEGACY TECHNOLOGY

Traditional keyword-based technology used in adverse media screening results in suboptimal outcomes because they are inefficient and ineffective in dealing with growing volumes and complexities in AML.

Despite the widespread usage of technology solutions, adverse media screening suffers from efficiency and effectiveness challenges. The traditional approach to adverse media screening technology is based on basic keyword-based search augmented by Boolean search queries such as “and” and “or” functions (e.g., find results for “John Smith” and “money laundering”). This crude approach generates numerous alerts, an overwhelming share of which are false positives. The alert investigation process is heavily manual and labor intensive and therefore highly inefficient. As a result, the current approach to adverse media screening suffers from many challenges as highlighted in Figure 1 and discussed below.

Figure 1: Traditional Adverse Media Screening Technology Creates Many Challenges

Source: Celent

Difficult to scale with growing

volumes

Redundant search results

Large false positives and case backlogs

Inability to categorize and

prioritize results

Poor coverage beyond English, Latin languages

Manual error, inconsistent

investigations

Difficult to assess relevance and

context

Inability to identify exact

targets

Challenges

Transforming Adverse Media Screening Adverse Media Screening Constrained by Legacy Technology

© CELENT 7

Inexact search results: Keyword-based search of names produces irrelevant search results because of the prevalence of common names and surnames. Consequently, such searches produce results of individuals with same name as an FI’s customers but who are not related to the actual person or entity being searched. Analysts must then manually evaluate about fitness of the results, which is a drag on efficiency.

Redundant search results: The same news item is often covered by multiple media sources. Traditional adverse media solutions pick up many of them as relevant search results, which analysts must manually filter, group, or discard depending upon their relevance to the specific investigation.

Irrelevant search results: The keyword-based approach cannot assess the context of a media article, so it cannot distinguish between “John Smith criminal” and “John Smith criminal defense lawyer.” This is even more challenging because of the complexities involved in AML. Even with a proper adverse media result on John Smith’s crime, traditional systems cannot distinguish whether it is a money laundering-related crime or other general type of adverse news which may not be relevant from a money laundering perspective. These add to the false positive volumes and operational inefficiencies.

Inability to prioritize results: Because of their inability to assess context, traditional solutions cannot rate or rank the accuracy, relevance, and risk of search results in relation to an FI’s specific investigation objectives. As a result, even high-risk adverse media information can be buried among the irrelevant and redundant search results, making it challenging for analysts to sift through the noise.

False positives and case backlogs: The result of all these shortcomings is that the traditional systems generate a large number of false positives, disposing of which requires significant manual efforts and results in steady build-up of case backlogs.

Manual error and bias prone: Overreliance on manual efforts makes the process prone to errors and biases because different analysts think, interpret, and work on cases differently. Flooded with voluminous false positives, they may also miss out on true risky events. Because of the heavy reliance on manual processing, adverse media screening suffers from inconsistent investigation and auditability challenges.

Limited coverage: Traditional solutions, because of their reliance on rudimentary technology, cover limited news sources—mostly mainstream international and leading local sources in English or Latin languages. They often leave out local media sources, foreign language sources, and may not support new media sources such as social media, blogs, and other open source intelligence sources. This can create gaps and deficiencies in coverage of adverse media programs.

Limited scale: Because of these challenges, FIs do not conduct negative news screening more frequently or widely on all customers because the operational costs can become prohibitively high. Sometimes FIs outsource false positive remediation to low-cost locations, which does not necessarily address the efficiency or effectiveness challenges.

Transforming Adverse Media Screening Transforming Adverse Media Screening with AI

© CELENT 8

TRANSFORMING ADVERSE MEDIA SCREENING WITH AI

AI-powered adverse media screening solutions can sift through the noise and extract risk-relevant information, reduce false positives, and highlight the most relevant search results and rank them in accordance of their risk. Early adopters report significant improvements in efficiency and coverage by their application.

The traditional technology solutions for adverse media screening were developed in the early 2000s when financial services technology was much simpler and rudimentary across the board. They are not well suited to tackle the challenges of the digital era where exponentially growing media volumes and source types, as well as complexities of the content, are exposing the limitations of the legacy solutions.

In the last five years, developments in next generation technology such as artificial intelligence and machine learning have advanced significantly, with noteworthy adoption in financial services including in AML. Celent has discussed about AI and its application in AML along with impressive adoption stories in our research, which are mentioned in the Related Research Section at the end of this report.

AI technology has the potential to transform adverse media screening. A specific AI technique called Natural Language Processing (NLP) can greatly improve analysis of textual and unstructured data analysis and can bring about a paradigm change in adverse media screening.

AI and NLP Techniques are Poised to Transform Adverse Media Screening

Artificial Intelligence (AI)

Machine Learning (ML)

Natural Language Processing

(NLP)

The science of training computers to perform tasks mimicking human reasoning.

A subset of AI that automatically learns and improves from experience without being explicitly programmed.

A subset of AI that automatically analyzes large amounts of natural language data and accurately extracts and categorizes information and insights from documents containing unstructured data.

Transforming Adverse Media Screening Transforming Adverse Media Screening with AI

© CELENT 9

AI in Action in Adverse Media Screening NLP techniques power intelligent analysis of textual information by going beyond keyword-based search to identify context, relevance, and relationships embedded within news articles.

• It uses identifiers such as name, address, biographical information, and IDs to match with relevant information in news articles.

o By using techniques such as entity recognition, parts-of-speech tagging, sentiment analysis, and pattern-based matching, it can not only perform word matching but also identify relationships between the identifiers and other textual information to establish the context, relationship, and relevance of the articles.

o By assessing the context, NLP can flag the types of adverse activity and map them with AML typologies such as fraud, sanctions, corruption, bribery, terrorist financing, cybercrime, drug trafficking, and so on.

• For each search result, AI systems can provide relevancy ratings that reflect the confidence level of the match. Similarly, they can provide risk scores that reflect the riskiness of each hit from an AML perspective.

o This enables ranking of search results according to their risk and relevance, as well as easy discarding of irrelevant or redundant results.

o The systems can be configurable and tuneable in accordance with an FI’s risk appetite and policies.

o FIs can then devote their scarce resources on the riskiest and most relevant results while routing less risky ones to junior analysts.

• At the investigation stage, AI systems can highlight the most relevant sections of an article so that analysts can quickly skim through them without wasting time on less relevant portions.

o Similarly, most relevant sections can be automatically extracted and annotated for preparing case reports, further enhancing investigation efficiency.

• This automation-driven approach removes human biases and errors and improves investigation consistency. It also ensures auditability as systems can provide and record the rationale for suggestions.

• Automation enables expanding scale and breadth of coverage exponentially.

o Machines can scan across the open web, deep web, and other information sources—covering recently published articles and linking them with historical records.

Transforming Adverse Media Screening Transforming Adverse Media Screening with AI

© CELENT 10

o They can include established mainstream media sources as well as lesser known sources such as those from local media, corporate registries, and so on.

• NLP techniques also support multilingual searches, including searches in native languages, that overcome the language barrier. Machine translation can make it easier for analysis to synthesize articles in foreign languages.

• This intelligent automation-driven approach enables more frequent screening and expansion pf coverage to include a larger segment or the whole of an FI’s client base.

• AI systems can learn on an ongoing basis based on investigation feedback and continually improve their performance.

Figure 2: Transforming Adverse Media Screening with AI

Source: Celent

Financial institutions have started exploring the application of AI in adverse media. We have come across impressive outcomes reported by early adopters.

• For a financial institution, NLP-driven automation reduced case investigation time by over 75%, and processing time was brought down from multiple hours to 20-40 minutes.

• Especially when applied at KYC onboarding, this can have a positive impact on customer experience and onboarding time; one bank reported reduction in corporate client onboarding time from two weeks to two days.

• This AI-driven approach also allowed the bank to scan all entities involved in a corporate hierarchy and all beneficial owners associated with those entities across regions, which further improved the coverage of their AML program.

Transforming Adverse Media Screening A New Screening Paradigm Powered by AI

© CELENT 11

A NEW SCREENING PARADIGM POWERED BY AI

Beyond improving efficiency and effectiveness of current adverse media screening programs, AI-powered solutions can open new horizons in customer screening. They can enable connecting adverse media screening with other screening processes and make it more dynamic and continuous—enabling FIs to take a more holistic, proactive, and risk-based approach in customer screening.

AI-powered adverse media screening has the potential to bring about a paradigm change in how FIs conduct AML screening.

Improve Efficiency and Effectiveness with AI The first lever of transformation is AI’s ability to vastly improve the efficiency and effectiveness of current programs. Such solutions drive automated and contextual analysis of unstructured data that can reduce inefficiencies and improve the scale and breadth of coverage manifold. Eliminating the need to manually evaluate volumes of content saves valuable time and reduces the possibility of introducing human bias and errors. NLP-driven analysis combined with AI-driven risk scoring can reduce false positives significantly, which further improves efficiency and resource utilization. Automated search increases depth, breadth, and frequency of monitoring, strengthening regulatory compliance.

Connect Adverse Media with Other Screening Processes AI-powered adverse media screening has the potential to go above and beyond just efficiency improvements. A natural extension of AI application would be to automatically link and analyze entities across adverse media as well as other screening sources such as sanction lists, watchlists, company registries, UBO information, and other sources containing financial crime-related information.

Along with developments in AI, we are witnessing maturation of graph technology and network analytics. Marrying AI with graph technology can power automated linkages with unstructured data, whereby the disparate screening components—from watchlist screening, payments, and adverse media screening—can all be integrated, enabling FIs to take a more holistic approach in screening.

Linkages can be established across retail and corporate client bases; for example, the screening solution can start with a corporate entity and conduct adverse media screening of that entity as well as its beneficial owners. Similarly, it can start with a retail client and screen if they are connected to a dubious corporate; or connected to

Transforming Adverse Media Screening A New Screening Paradigm Powered by AI

© CELENT 12

a corporate whose beneficial owners may be suspects from an AML perspective. With growing scrutiny from regulators on sanctions through ultimate beneficial owners, this approach could open new horizons in the whole screening process beyond adverse media.

Move Toward Dynamic and Continuous Risk Monitoring Another critical edge that AI-powered solutions can offer is through conducting more frequent screening and client monitoring. Historically, FIs have done periodic risk refreshes of their client base typically once or twice a year for high-risk clients and once every three or five years for low-risk clients. But customer risk can change quickly, and low-risk customers can become high risk at any time.

The ability to screen all clients automatically and efficiently—free of worrying about voluminous false positives and case backlogs—will allow FIs to conduct screening more frequently and widely; for example, monthly for all clients and even more frequently for high-risk clients. When a newsworthy article is published about a customer, the adverse media screening process will trigger an alert notifying the FI to undertake further due diligence. This will enable FIs to undertake a more proactive and dynamic approach to customer risk monitoring.

This dynamic adverse media screening approach could potentially be combined with transactional data monitoring to form a complete view of customer risk. Ongoing screening of customer activity will also reveal trends and patterns about the evolution of customer risk for different customer segments that can further inform risk assessment methodology and help in calibrating risk scoring systems.

Transforming Adverse Media Screening Considerations for Adoption

© CELENT 13

CONSIDERATIONS FOR ADOPTION

For operationalizing AI-powered adverse media screening solutions, FIs must pay attention to critical issues such as data management, system integration, model governance, and resourcing.

FIs are at an early stage of AI and ML application in AML in general and adverse media in particular. For smooth implementation and maximum benefit realization, they must streamline their practices in data management, system integration, model governance, and resourcing.

Data Management Data is the fuel driving analytics. Data quality, transformation, and governance issues will be critical in their adoption, because the full benefit of AI solutions can only be realized with complete and quality information. The traditional approach to data storage, querying, and computing, which relied heavily on relational databases, may not be suitable for meeting the exponential scalability needs of AI in a cost-effective way.

Customer data is the essential ingredient in adverse media screening, and augmenting customer names with additional secondary information can help improve search accuracy and reduce false positives. Therefore, managing customer data effectively across the organization and efficiently enriching them with additional information will be critical in deriving maximum benefits of AI.

Another challenge is data privacy and data sovereignty issues, and limitations around banks’ ability to share data due to regulations (e.g., GDPR). For comprehensive analysis, banks need aggregate data cutting across business lines and geographies, yet regulations can prevent them from sharing within or between institutions.

Model Governance Model governance, auditability, and explainability of models and decisions will be critical in operationalizing AI solutions. How AI algorithms assign relevance scores, risk scores, and false positive likelihoods needs to be explainable, documentable, and auditable, because regulators demand AML programs to have strict controls, transparency, auditability, and documentation. This concern has led some banks to hold back on experimenting with AI, but this is changing. A recent joint statement from several supervisory agencies in the US including FINCEN, FDIC, and OCC has laid out their thinking on this issue.

Transforming Adverse Media Screening Considerations for Adoption

© CELENT 14

Some banks are experimenting with artificial intelligence and digital identity technologies applicable to their BSA/AML compliance programs. These innovations and technologies can strengthen BSA/AML compliance approaches, as well as enhance transaction monitoring systems. The Agencies welcome these types of innovative approaches to further efforts to protect the financial system against illicit financial activity.

To this end, the Agencies are exploring additional methods to encourage innovation, including through FinCEN’s Bank Secrecy Act Advisory Group.

Joint Statement from several supervisory agencies in the US1

Some consider this statement to be revolutionary and a catalyst that could expedite adoption of AI and ML solutions in AML. Regulators in other regions are also becoming more involved in promoting use of next-generation technology in AML. Solution providers and banks are working closely with regulators in this regard, sharing results and learnings from their pilots and PoCs, which are helping to enhance understanding of the issues and challenges involved, thereby informing all participants how to tackle regulatory issues without impeding innovation.

System Integration Integration of AI-powered adverse media solution with up and downstream systems such as KYC, screening engines, and case management tools will be needed to drive maximum efficiency improvements. Adverse media systems will require easy ingestion tools from screening or KYC systems as well as easy exportability of results to case management solutions. It is unlikely many banks will have dedicated case management tools just for adverse media; they will instead likely incorporate adverse media results as one of many components in their due diligence process. Similarly, moving to continuous monitoring will require them to easily access customer data and trigger alerts to risk rating systems when adverse news on customers is found.

The use of API and cloud technology can help in this regard. API supports easy integration and interoperability with data sources and up and downstream systems. Cloud offers flexibility and scalability for optimal utilization of infrastructure and computing power needed to run AI algorithms in bursts. Cloud adoption has been steadily growing in financial services, and we have started seeing its application in

1Joint Statement on Innovative Efforts to Combat Money Laundering and Terrorist Financing. December 2018.

Transforming Adverse Media Screening Considerations for Adoption

© CELENT 15

compliance functions as well. This growing usage could accelerate interconnectivity in the ecosystem, starting from FIs’ internal systems through to vendor solutions, data sources, and open source information.

Expertise and Sourcing Finding resources with expertise in both AML and AI and machine learning is another challenge. It is not easy to train and retain staff with expertise across technology, regulations, investigations, and language skills. While some large banks have the resources to invest in data scientists and machine learning experts, many banks do not, and they expect technology companies to make analytics easy to use and consumable by business users.

Evolution of the Solution Provider Landscape Most banks are therefore looking for external help for operationalizing AI and ML in AML, because they feel this approach can accelerate time to benefit and minimize costs and risks. Some banks prefer working with their existing AML solution providers or seeking help from incumbent industry solution providers. Others are working with industry newcomers such as fintech and regtech start-ups. This is driving rapid evolution of AI and ML solution providers in the industry, and FIs have several choices to procure adverse media screening solutions, as shown in Figure 3.

Figure 3: The Landscape of Adverse Media Solution Providers is Diverse and Rapidly Evolving

Source: Celent Illustrative examples, not exhaustive

Transforming Adverse Media Screening Path Forward

© CELENT 16

PATH FORWARD

Next generation technology opens new horizons in adverse media screening and empowers FIs to move away from manual or keyword-based searches and adopt automation and intelligence-driven approaches. This adoption is already underway; with growing maturity of users and solution providers, we expect it to intensify.

With early adoption of this new technology and tools, banks, solution providers, and regulators are undergoing an educational journey regarding how to strike the right balance between promoting innovation and ensuring adequacy of model governance requirements. We expect industry dialogue, sharing of results and findings from pilots and use cases, and similar engagements to continue—which should ease regulatory concerns, accelerate adoption, and further promote innovation.

AI is not meant to replace human analysts and their judgments, and humans will still be in charge of decision making while working with AI-based systems. But AI-powered tools can and will augment human analysts by reducing their operational burden in adverse media screening and helping them with advanced insights.

While AI technologies can support wider, deeper, and more frequent screening automatically, FIs need to judiciously choose an optimal number of data sources, client segments, and screening frequency to ensure they strike the right balance between resource utilization (including infrastructure and human resources) and compliance effectiveness. Taking a risk-based approach—which regulators have been promoting for some time—would be prudent in this regard because it will ensure FIs are optimizing their resources in accordance with their risk profile and risk appetite.

Transforming Adverse Media Screening Leveraging Celent’s Expertise

© CELENT 17

LEVERAGING CELENT’S EXPERTISE

If you found this report valuable, you might consider engaging with Celent for custom analysis and research. Our collective experience and the knowledge we gained while working on this report can help you streamline the creation, refinement, or execution of your strategies.

Support for Financial Institutions Typical projects we support include:

Vendor short listing and selection. We perform discovery specific to you and your business to better understand your unique needs. We then create and administer a custom RFI to selected vendors to assist you in making rapid and accurate vendor choices.

Business practice evaluations. We spend time evaluating your business processes and requirements. Based on our knowledge of the market, we identify potential process or technology constraints and provide clear insights that will help you implement industry best practices.

IT and business strategy creation. We collect perspectives from your executive team, your front line business and IT staff, and your customers. We then analyze your current position, institutional capabilities, and technology against your goals. If necessary, we help you reformulate your technology and business plans to address short-term and long-term needs.

Support for Vendors We provide services that help you refine your product and service offerings. Examples include:

Product and service strategy evaluation. We help you assess your market position in terms of functionality, technology, and services. Our strategy workshops will help you target the right customers and map your offerings to their needs.

Market messaging and collateral review. Based on our extensive experience with your potential clients, we assess your marketing and sales materials—including your website and any collateral.

Transforming Adverse Media Screening Related Celent Research

© CELENT 18

RELATED CELENT RESEARCH

Innovation in Risk: A Snapshot Through the Lens of Model Risk Manager 2021 April 2021

Model Risk Manager 2021 Award Winners: 8 Separate Case Studies March 2021

Transforming Sanctions Screening: Improving Performance with Advanced Technology February 2021

IT and Operational Spending on Fraud: 2021 Edition February 2021

IT and Operational Spending in AML-KYC: 2020 Edition November 2020

Top Technology Trends in KYC-AML: Transforming AML Operations in the Digital Era November 2020

Public Cloud Adoption in Risk and Compliance: 7 Key Considerations for CIOs and Key Stakeholders September 2020

Managing Digital Transformation Risk in Financial Services September 2020

Know Your Customer Systems: 2020 xCelent Awards, Powered by VendorMatch June 2020

Rethinking Data for a New Era in AML June 2020

Risk and Compliance in the Wake of COVID-19: Strengthening Risk Postures with Digital Toolkits June 2020

COPYRIGHT NOTICE Copyright 2021 Celent, a division of Oliver Wyman, Inc., which is a wholly owned subsidiary of Marsh & McLennan Companies [NYSE: MMC]. All rights reserved. This report may not be reproduced, copied or redistributed, in whole or in part, in any form or by any means, without the written permission of Celent, a division of Oliver Wyman (“Celent”) and Celent accepts no liability whatsoever for the actions of third parties in this respect. Celent and any third party content providers whose content is included in this report are the sole copyright owners of the content in this report. Any third party content in this report has been included by Celent with the permission of the relevant content owner. Any use of this report by any third party is strictly prohibited without a license expressly granted by Celent. Any use of third party content included in this report is strictly prohibited without the express permission of the relevant content owner This report is not intended for general circulation, nor is it to be used, reproduced, copied, quoted or distributed by third parties for any purpose other than those that may be set forth herein without the prior written permission of Celent. Neither all nor any part of the contents of this report, or any opinions expressed herein, shall be disseminated to the public through advertising media, public relations, news media, sales media, mail, direct transmittal, or any other public means of communications, without the prior written consent of Celent. Any violation of Celent’s rights in this report will be enforced to the fullest extent of the law, including the pursuit of monetary damages and injunctive relief in the event of any breach of the foregoing restrictions.

This report is not a substitute for tailored professional advice on how a specific financial institution should execute its strategy. This report is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accountants, tax, legal or financial advisers. Celent has made every effort to use reliable, up-to-date and comprehensive information and analysis, but all information is provided without warranty of any kind, express or implied. Information furnished by others, upon which all or portions of this report are based, is believed to be reliable but has not been verified, and no warranty is given as to the accuracy of such information. Public information and industry and statistical data, are from sources we deem to be reliable; however, we make no representation as to the accuracy or completeness of such information and have accepted the information without further verification.

Celent disclaims any responsibility to update the information or conclusions in this report. Celent accepts no liability for any loss arising from any action taken or refrained from as a result of information contained in this report or any reports or sources of information referred to herein, or for any consequential, special or similar damages even if advised of the possibility of such damages.

There are no third party beneficiaries with respect to this report, and we accept no liability to any third party. The opinions expressed herein are valid only for the purpose stated herein and as of the date of this report.

No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this report to reflect changes, events or conditions, which occur subsequent to the date hereof.

Americas EMEA Asia-Pacific

USA 99 High Street, 32nd Floor Boston, MA 02110-2320 +1.617.262.3120

Switzerland Tessinerplatz 5 Zurich 8027 +41.44.5533.333

Japan Midtown Tower 16F 9-7-1, Akasaka Minato-ku, Tokyo 107-6216 +81.3.3500.4960

USA 1166 Avenue of the Americas New York, NY 10036 +1.212.345.3960

France 1 Rue Euler Paris 75008 +33 1 45 02 30 00

Hong Kong Unit 04, 9th Floor Central Plaza 18 Harbour Road Wanchai +852 2301 7500

USA Four Embarcadero Center Suite 1100 San Francisco, CA 94111 +1.415.743.7960

Italy Galleria San Babila 4B Milan 20122 +39.02.305.771

Singapore 138 Market Street #07-01 CapitaGreen Singapore 048946 +65 6510 9700

Brazil Av. Dr. Chucri Zaidan, 920 Market Place Tower l - 4° Andar Sao Paulo SP 04583-905 +55 11 5501 1100

United Kingdom 55 Baker Street London W1U 8EW +44.20.7333.8333

For more information please contact [email protected] or:

Arin Ray [email protected]

About Quantifind

Quantifind was founded in 2009 upon pioneering work building machine learning technology to discover meaningful patterns across large, disparate, unstructured datasets. Quantifind’s Graphyte platform is differentiated by its risk assessment accuracy and speed, achieved through best-in-class name science, AI-driven entity resolution, dynamic risk typologies, and patented in-memory data storage and search techniques. The platform embodies over a decade of R&D and large-scale deployments with government agencies and Fortune 50 companies.

©2021 Quantifind

Financial Crimes Automation Platform™

Visit Quantifind’s website at www.quantifind.com or send us an email at [email protected] to learn more about how Graphyte’s unique AI technology and software-only approach make customer monitoring efficient and scalable.