transfer pricing issues in manufacturing industry · pdf fileindian pharma – big picture...

TRANSCRIPT

Transfer Pricing – Issues in Manufacturing Industry

Manufacturing sector in India

• Contribution of manufacturing sector in GDP is 15-17%

• Key products manufactured in India - Adhesive and films, tobacco products, chemicals, electronic, explosives, machineries and tools, plastic products, leather products, household, food, etc.

• ‘Make in India’ initiative taken by government of India to:

facilitate investment

foster innovation

enhance skill development

protect intellectual property

build best in class manufacturing infrastructure

turning labour intensive manufacturing industry to capital intensive

Slide 2

Functional, Asset and Risk Analysis (FAR) of manufacturing

Transfer Pricing Jigsaw

FAR analysis Selecting the tested party

Comparability

Analysis

Transfer

Pricing

Methods

Industry

Overview

Slide 4

TP Models

Manufacturers Distributors

Service Providers

Typical Business Models

Slide 6

Typical manufacturing models

Parameters Full Fledge

Manufacturer Licensed

Manufacturer Contract

Manufacturer

Toll Manufacturer

Produces on Own behalf Own behalf Principal Principal

Intellectual Property Owns the IP Licenses the IP Does not own Does not own

Materials Owns Owns Owns Does not own

Raw materials

Principal

Contract manufacturer

Production Schedule

Finished Goods

Production Schedule

Principal

Toll manufacturer

Raw materials

Finished Goods

Physical Flow

Legal Ownership

Information Flow

Slide 7

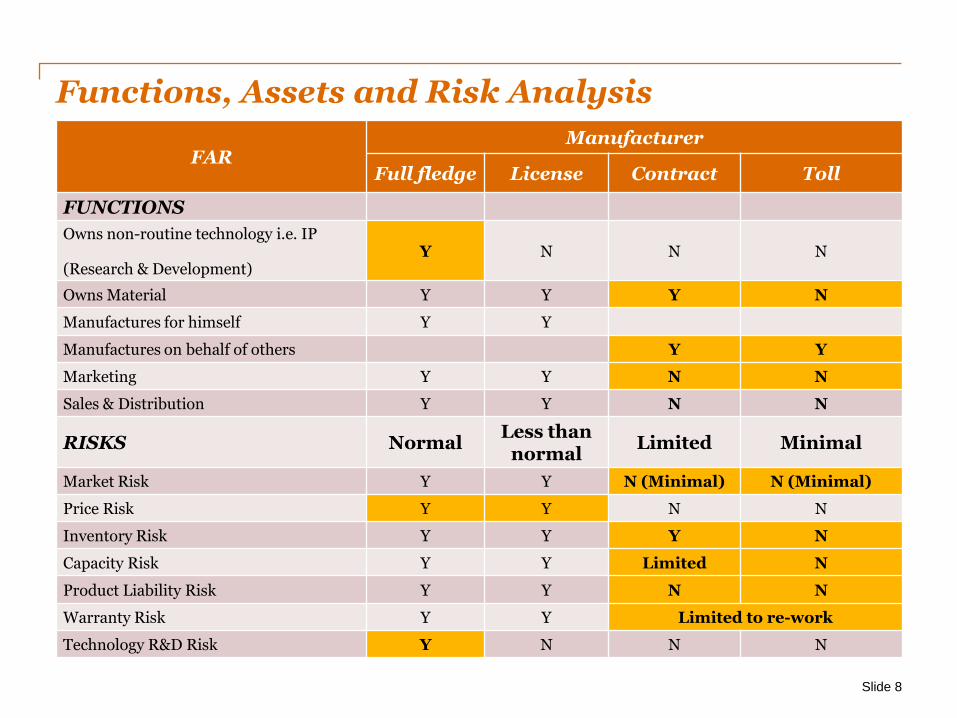

Functions, Assets and Risk Analysis

FAR Manufacturer

Full fledge License Contract Toll

FUNCTIONS

Owns non-routine technology i.e. IP

(Research & Development) Y N N N

Owns Material Y Y Y N

Manufactures for himself Y Y

Manufactures on behalf of others Y Y

Marketing Y Y N N

Sales & Distribution Y Y N N

RISKS Normal Less than

normal Limited Minimal

Market Risk Y Y N (Minimal) N (Minimal)

Price Risk Y Y N N

Inventory Risk Y Y Y N

Capacity Risk Y Y Limited N

Product Liability Risk Y Y N N

Warranty Risk Y Y Limited to re-work

Technology R&D Risk Y N N N

Slide 8

Compensation Structure – Manufacturing Models

Functions Typical Compensation model

Contract / Toll manufacturing operations

Full cost plus mark up (or)

Return for value added services plus appropriate return on capital investments in material and finished goods inventory

Routine manufacture / assembly activity with licensed technology from Group.

Risk free assured return in line with industry benchmarks

As a variant of the above with significant local marketing efforts

Receipt of compensation for marketing intangible in addition to the above

Full fledged manufacturer and contributing to the R&D effort of the Group

Profit Split Method (PSM) to determine the contribution towards routine functions and towards intangibles

Slide 9

Typical issues in Manufacturing Sector

Typical TP issues for Indian manufacturers

Slide 11

Payment of know-how royalty vs brand royalty (in

loss scenarios) Marketing intangibles

Comparability analysis for contract manufacturers

Risk adjustments – depreciation, capacity

utilisation, working capital and risk adjustments for

captive entities

Local vs export profits

Manufacture (Use of CUP over TNMM –

considerations for quality, shelf life etc.)

Hybrid models – segmental accounts and profitability

Location savings

Conversion of overseas contract manufacturers to toll manufacturers (Exit

charge and business restructuring implications)

1. Payment of know-how royalty vs brand royalty (in loss scenarios)

Slide 12

1. Payment of know-how royalty vs brand royalty (in loss scenarios)

Slide 13

IP Owner

India

ICO

Issues instrument • Licensed

manufacturing

• Distribution

• ICo is the Entrepreneur for the local market

• AE imports & exports, royalty payments and management fee could be challenged

• Losses would be borne by Indian company unless losses are a result of incorrect transfer price

1. Payment of know-how royalty vs brand royalty (in loss scenarios)

Slide 14

• Payment of royalty can be challenged aggressively in case of loss making companies

• Business and Commercial reasons for loss (capacity underutilization, start up / market penetration, competition / pricing pressures etc.)

• Company to substantiate benefits received –comprehensive documentation demonstrating business & commercial rationale

• Assess the royalty on the touchstone of third party scenario (risk and reward analysis)

• Projections, budgets / forecasts indicating profit potential

• Group Policy

2. Comparability analysis

Slide 15

2. Comparability analysis

Adjustment for differences in risks between comparables and tested party necessary to be included in the TP Study Report

Approach Full

Fledged Licensed Contract Toll

Comparable Set Manufacturing Set Services Set

Parameters for selection of comparable companies

Broad product comparability Keywords such as contract, custom, job work, processing, as per specifications / requirements, on behalf of

Absence of distribution facilities, sales personnel, marketing of products

No raw material content, only consumables (Notes to Accounts is key)

Ratios to be analysed Manuf. / Sales Manuf. / Sales R&D / Sales

R&D / Sales, Adv & Marketing / Sales, Royalty expense

RM / TC

Slide 16

3. Adjustment for Capacity Utilisation

Slide 17

3. Adjustment for Capacity Utilisation

• To account for differences in capacity utilization (fixed costs) between the tested party and the uncontrolled comparable transaction

• The low profitability of tested party may not always be attributable to pricing of international transaction

• One needs to consider effects of under-absorption of overheads due to under-utilisation of capacities

Slide 18

Need for adjustment for differences in capacity utilisation

3. Adjustment for Capacity Utilisation

Types of capacity utilization adjustment

• By hypothetically calculating sales/ revenue at optimum utilization level:

- Corresponding increase in variable cost

- Fixed cost assumed to be at same levels

Or

• By reducing fixed cost to the extent not utilized:

- Sales and variable cost remains unchanged

Slide 19

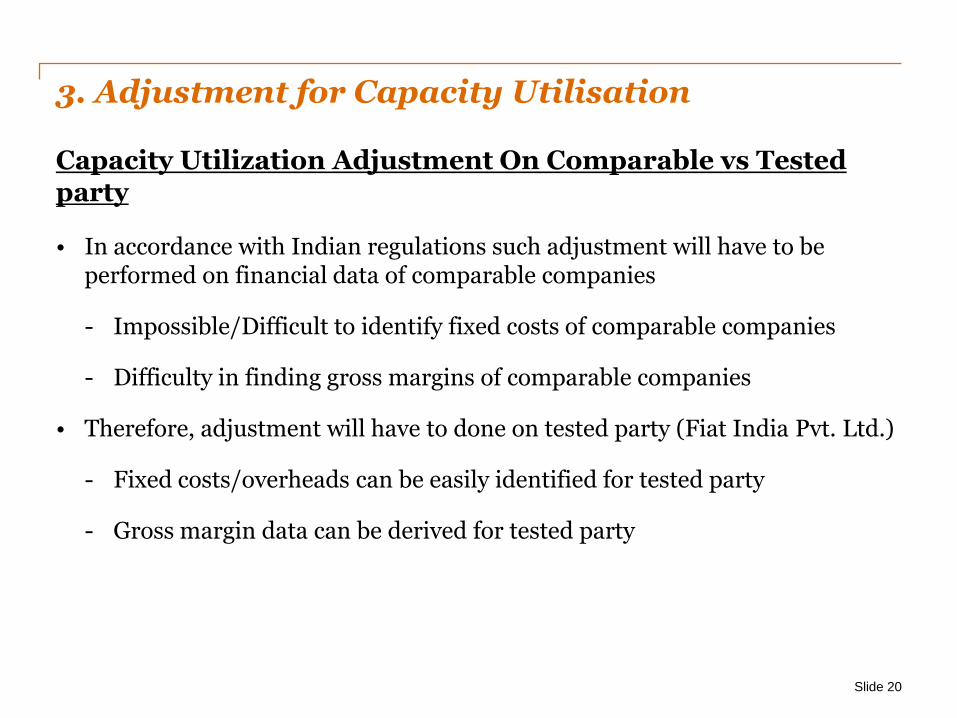

3. Adjustment for Capacity Utilisation

Capacity Utilization Adjustment On Comparable vs Tested party

• In accordance with Indian regulations such adjustment will have to be performed on financial data of comparable companies

- Impossible/Difficult to identify fixed costs of comparable companies

- Difficulty in finding gross margins of comparable companies

• Therefore, adjustment will have to done on tested party (Fiat India Pvt. Ltd.)

- Fixed costs/overheads can be easily identified for tested party

- Gross margin data can be derived for tested party

Slide 20

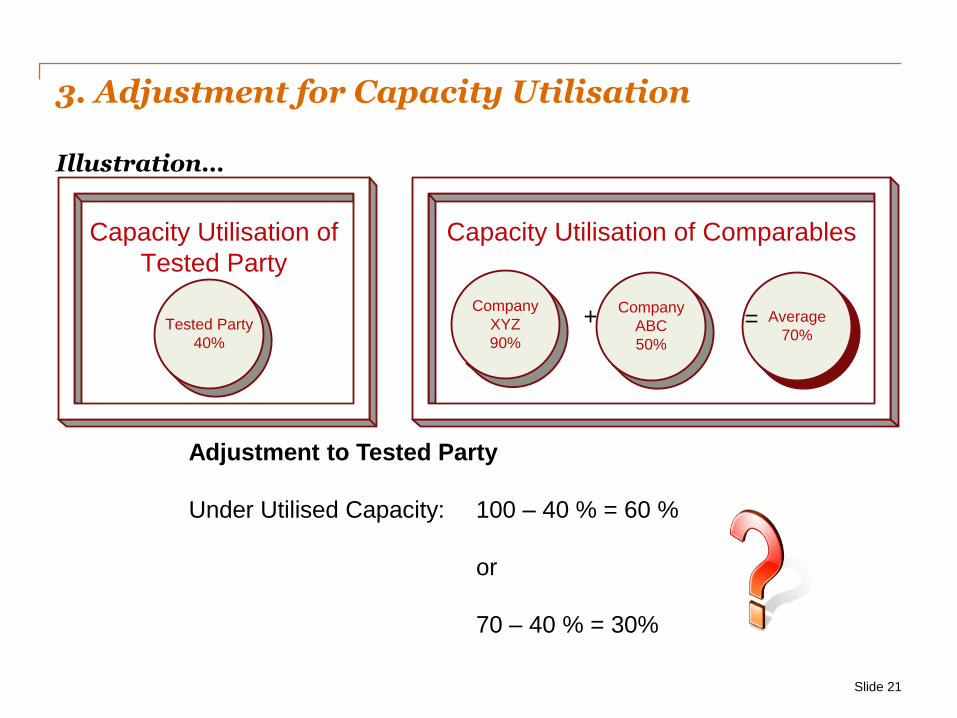

3. Adjustment for Capacity Utilisation Illustration…

Capacity Utilisation of ComparablesCapacity Utilisation of

Tested Party

Tested Party

40%

Company

XYZ

90%

Company

ABC

50%

Average

70%

Slide 21

Adjustment to Tested Party

Under Utilised Capacity: 100 – 40 % = 60 %

or

70 – 40 % = 30%

+ =

3. Adjustment for Capacity Utilisation Illustration…

Slide 22

1Underutilised capacity = 40/70*100=57% (approx)

Particulars Actual Data

Variable Cost Fixed Cost Adjusted

Fixed Cost

Adjusted Financial

Data

A B C = B x 57%1 D = A + C

Sales 1000 1000

Operating Expenses

Material 600 600 - - 600.00

Salary 100 25 75 42.75 67.75

Depreciation 200 - 200 114.00 114.00

Other Expenses 100 50 50 28.50 78.50

Total Cost 1000 860.25

Operating Profit 0 139.75

OP / Sales 0% 13.98%

3. Adjustment for Capacity Utilisation

• Document basis and method of calculation of underutilized capacity

- business reason for under utilization of capacity

- rationale for setting up excess capacity

- business plans, capacity utilisation data and profitability for future years

Slide 23

3. Adjustment for Capacity Utilisation

Fiat India • Assessee was under utilized due to low sales/production volume

• Made several adjustments on account of depreciation and other fixed overhead

• Tribunal ruled in favor stating that the Assessee had sufficiently explained and demonstrated (with relevant facts/figures/supporting evidence) that there were material differences

Brintons Carpets Asia Pvt. Ltd.

• Adjustment on account of labour unrest carried out • Tribunal ruled in favor by allowing economic adjustment

which was restricted to fixed cost/ overhead • Ruling supported adjustment to tested party

Slide 24

Legal Precedence

4. Location savings

Slide 25

4. Location Savings

• Location savings is generally defined as the net cost savings realized by a party in a high cost location through outsourcing a certain activity to a low cost location

• In addition, Location specific benefits/advantages such as proximity to local market, regulations also increase profitability

• Net Location savings + Location specific benefits = Location specific advantages (LSAs)

• Location rent is the incremental profit derived from the exploitation of the LSAs

Slide 26

GAP Ruling

• Generally, the advantage of location savings is passed on to the end customer via a competitive sales strategy

• The arm’s length principle requires benchmarking to be done with comparables in the jurisdiction of the tested party and the location savings, if any would be reflected in the profitability earned by comparables.

• No separate/additional allocation is called for location savings

4. Location Savings

Slide 27

Watson Pharma Ruling

• The taxpayer as well as AEs operated in a perfectly competitive market, and the taxpayer did not have exclusive / unique access to factors leading to location-specific advantages and therefore there was no super profit arising

• Where local market comparables were available and used, specific adjustment for location savings was not required. Any benefit/ advantage to the AE was irrelevant if the profit level indicator of the taxpayer was within the range of comparables.

• The India chapter of the United Nations Transfer Pricing Manual (which, among other issues, also discusses location savings) represented a view of the Indian tax

administration and was not binding on appellate authorities.

5. Marketing Intangibles

Slide 28

5. Marketing Intangibles

• Advertising and promotional activities - Focus area of TP authorities in India

• Promotional spends considered a service to the parent

• Possible adjustment scenarios:

Slide 29

Prices of imported goods Imputed as cost reimbursement

Disallowance of excessive

marketing spend

Disallowance / reduction of

brand royalty paid

5. Marketing Intangibles

• In relation to the AMP issue faced by manufacturing entities, the Delhi high court in case of Maruti Suzuki has seen the concerned issue in new light:

- Once the ‘Bright line test’ had been negated, there was no basis on which it could be said that there was an international transaction;

- It is essential to show the existence of an ‘agreement’, an ‘understanding’, an ‘agreement’ or ‘action’ in concert between the Indian company and the AE as regards to AMP spend for brand promotion; and

- Any incidental benefit to the AE on account of AMP expenses incurred by the taxpayers should not lead to an automatic interference of a service being rendered by the taxpayer of the AE; and

- The said manufacture’s ruling is in line with the fundamentals of ‘TP international guidelines including the OECD TP guidelines’

Slide 30

Key issues

Key Clauses in a contract

Key Clauses in a contract / toll manufacturing scenario

• Compensation clause

- True up / true down

• Minimum commitment

• Idle capacity costs

• Product liability risk

• Early termination

setting up of asset with no alternative use

asset capable of alternative use

• Termination after initial period

• Inventory on termination

• Right to subcontract

Slide 32

Industry Specific issues

Pharmaceutical Sector

Slide 34

Indian Pharma – Big picture

• Highly regulated – from innovation till sale

• Trend towards new drug discovery

- In-house research (Generic as well as branded)

- Collaboration

• Overseas acquisitions

• Hub for Pharma Manufacturing (‘CRAMS’)

- Low cost

- Easier process

- Infrastructure – Good Manufacturing Practice

• FDI in pharma – Greenfield / Brownfield

Slide 35

• Licensed manufacturer vs. value added distributor

• Import of APIs vs. local procurement

Inbound models

Slide 36

Sale of formulations

Principal Co API Manufacturer (Legal owner of IP)

Indian Sub Co

(Secondary Manufacturer)

Imports of

original

APIs

Indian Customer

India

Outside India

Distribution

Principal Co (Legal owner of IP)

Distributor

Imports of

branded

finished goods

Indian Customer

India

Outside India

• Routine vs. super distributor

• Return for local value addition

• Basket of product approach - product launch/ start-up issue

• Product wise profitability analysis

• Various Distribution models – Consistency TP models

• Bill to Ship to model using Marketing Companies

Outbound models

Sale of formulations Distributor / MSS

IP Owner – Manufacturer

Exports of

original

APIs

Foreign Customer

India

Outside India

Legal owner of IP & Distribution

Contract Manufacturing /

Contract Research Companies

(Flag ship Group Co)

Cost plus

markup India

Outside India

• Low-Risk / Low Return models for Indian Flag ship companies scrutinized by tax authorities

• FA related challenges

Sale of formulations Foreign

Customer

Slide 50

Principal Co API Manufacturer (Legal owner of IP)

Indian Sub Co (Secondary

Manufacturer)

Imports of

original APIs

Indian Customer

Sale of formulations

Issue: • Comparison of import price of

branded APIs with price of generic APIs (Serdia Ruling)

• Customs database (TIPS)

India

Outside India

Slide 38

Import of API

Import of API - Key points

• Adjustments in view of quality, purity etc. and their quantification

• Relevance of SVB Order

Serdia Fulford

CUP most appropriate method for import of API transaction

Before applying CUP it is important to understand characterization of the entity importing API

Comparison of import price of off-patented API with generic API

Comparison with generic API not sustained, product accompanied with IP rights will fetch premium price

Is CUP the right method

after ruling in case of

Fulford India Limited

Slide 39

Issue: • Product-wise profitability analysis • New product launches (initial

losses)

ABC Inc. (Legal owner of IP)

DEF (Distributor)

Imports of branded

finished goods

Indian Customer Distribution to customers

India

Outside India

Slide 40

Import of Finished Goods

Import of Finished Goods – Key points

• Routine v/s marketer distributor

• Low operating margins – product launch/ start-up issue

• Harmonization with Custom positions

• Value addition at India: Reward

• Aggregation

• Basket of products

Slide 41

Exports to AEs

India

Outside India

Export of goods for

resale

Issue: • Comparison of sales to AEs

with third party (domestic/ export) sales

• Tested Party selection

Third Party Sale of

goods

ABC India

XYZ Inc. JKL GmbH

Slide 42

Exports to AEs – Key Points

• Generally non-comparable transactions – functional, risk and market differences

• Robust FAR analysis and characterizing operations of AEs

• Evaluate whether AEs can be selected as tested party

Slide 43

Contract Manufacturing

Slide 44

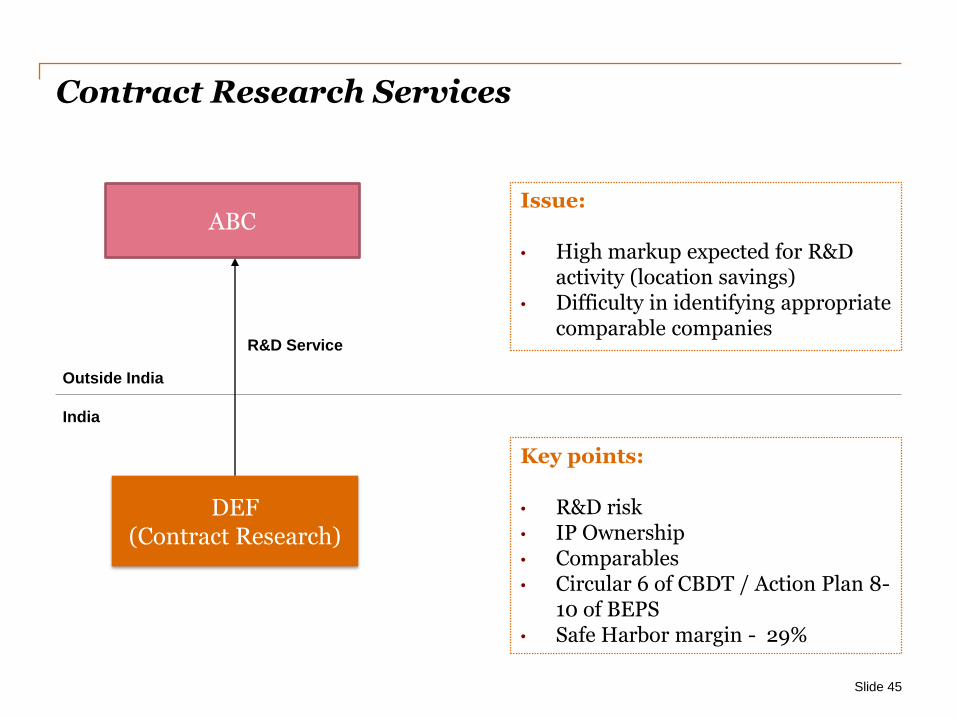

India

DEF (Contract

Manufacturing

ABC

Sale of goods

Outside India

Issue: • High markup expected for Contract

Manufacturing activity (location savings)

• Difficulty in identifying appropriate comparable companies

Key points: • Agreement • Prior purchase orders / Volume

Commitment • Operating cost definition, ROA • Capacity Utilisation • Early termination • Comparables

Issue: • High markup expected for R&D

activity (location savings) • Difficulty in identifying appropriate

comparable companies

Key points: • R&D risk • IP Ownership • Comparables • Circular 6 of CBDT / Action Plan 8-

10 of BEPS • Safe Harbor margin - 29%

Slide 45

India

DEF (Contract Research)

ABC

R&D Service

Outside India

Contract Research Services

ABC India Indian CRO/

Hospitals

Facilitation

Issue: • Treatment of third party costs as

pass-through denied • Comparison with full fledged

Contract Research Organizations (CROs) for determination of mark-ups by Revenue authorities

India

Outside India

Clinical trial facilitation

service

Slide 46

ABC Inc.

Clinical Trials Facilitation Services

Clinical Trials Facilitation Services – Key points

• Key points:

- Agreement

- Comparables

- Support services v/s clinical trials

- Robust FAR

Slide 47

Thank You!

Questions ???