traditional department stores need to establish a multi-business model

TRANSCRIPT

Sector Research | HK & China Consumer & Retail Sector

For ratings definitions and other important disclosures, refer to the Information Disclosures at the end of this report. 1

March 21, 2012

Online Retailing BUY

Traditional department stores need to establish a “multi-business model”

Investment highlights

Online retail market enjoyed impressive growth in the past few years.

Online retail sales in China surged by a CAGR of 97% in 2006-11 to RMB770

billion, and are expected to grow by 35% in 2012-15. For 2014, sales are

forecast to reach RMB2,000 billion, driven by development of the logistics

industry and online payment systems, as well as growing Internet usage.

The industry has three features: high concentration, standardised

products and regional difference. The top three online retailers in China

accounted for 75% of the overall market in 2011, of which taobao has over

50%, with total transaction volume of about RMB100 billion. Standardised

products, such as apparel, electronics and home appliances, are the main

products sold online. Online clothing sales totaled RMB204.9 billion in 2011,

and are expected to exceed RMB500 billion in 2014. Development of the

industry is concentrated in the southeast coastal regions, which has further

differentiated performance in these regions vs Midwest and Eastern China.

In the short term, online retailing poses challenges to traditional

retailers. Rapid growth of online sales of apparel, electronics and home

appliances will, to a large extent, drag down the sales of brick-and-mortar

department stores. To ride the competition and promote growth, traditional

players should focus on providing consumers with a comfortable shopping

environment and one-stop services, and transition to an “online + offline”

operating revenue model, which will give full play to their geographic

advantages and strengths in brand management.

Brand awareness plays a significant role in the development of virtual

stores. Online malls help brands to expand their distribution channels. To

enhance online sales, franchised stores will have to pay more attention to

brand promotion. Hence, more flagship stores and self-owned stores are also

expected to be set up as these can help promote the brand image to drive

online sales.

Exhibit 1: Valuation comparison

Tickers Company Last price (HK$)

Market cap (HK$ mn)

EPS (HK$) P/E (x) 2010A

Rating 2008A 2009A 2010A

1833.HK Intime Dep. Stores

10.28 19,000 0.237 0.296 0.461 20.8 Buy

0825.HK NWDs 5.39 8,300 0.32 0.34 0.51 9.7 Buy

3998.HK Bosideng 2.41 18,900 0.11 0.16 0.19 12 Buy

0210.HK Daphne 9.70 15,700 0.30 0.24 0.36 26.3 Buy

0738.HK Le’saunda 2.64 1,800 0.11 0.19 0.26 10.7 Buy

Source: Wind, Guosen Securities Economic Research Institute

Analyst

Season Sun +852-2899 8342 [email protected] SFC CE No.: ATO642

Sales Contact

Dan Weil Global Head of Institutional Sales and Trading Managing Director +852 2248 3588 [email protected]

Chris Berney Managing Director +852 2248 3568 [email protected]

Joe Chan Director +852 2248 3578 [email protected]

Cancy Kong Vice President +852 2248 3538 [email protected]

Jiafeng Li Vice President +852 2899 7281 [email protected]

Shunei Kin Vice President +852 2248 3536 [email protected]

Consumer & Retail Sector March 21, 2012 | HK & China

Guosen Securities (HK) Brokerage Co., Ltd.

2

1 China‟s online retail market is booming

Online purchases in China have surged at a 45% CAGR since 2005. Total transaction

volumes climbed to RMB6.8 trillion in 2011 (B2C and B2B), and are expected to grow

further by around 40% y-o-y in 2012.

Exhibit 2: Online shopping in China saw strong growth in the past few years

Source: China e-Commerce Market 2011-2015 Forecast and Analysis, Guosen

Securities (HK)

The percentage of online purchases as a share of traditional retailing has risen from 1%

in 2008 to 4% in 2011, and this is expected to reach 7-8% in 2014. In the case of Japan

and South Korea, where Internet shopping has become relatively developed, the

percentage has remained stable at around 10%. Given the short history and high

concentration of China’s online retailing to the mid-western region, we expect to see

rapid development in 2012-15, with a forecast 35% CAGR.

Exhibit 3: Online transaction volumes surged

Source: China e-Commerce Market 2011-2015 Forecast and Analysis, Guosen

Securities (HK)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

1

2

3

4

5

6

7

8

9

10

2006 2007 2008 2009 2010 2011 2012

RMB tr

E-commerce transaction volume (RMB tr,LHS)

Growth (RHS)

Proportion in GDP (RHS)

0%

20%

40%

60%

80%

100%

120%

140%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2006 2007 2008 2009 2010 2011 2012 2013

RMB bn

Online purchases (RMB bn, LHS)

Growth (RHS)

Proportion in total retail sales of consumer goods (RHS)

We forecast online retailing in the

Midwestern region will grow rapidly

by a 35% CAGR for 2012-15 given the

concentration of operators in the

region.

Consumer & Retail Sector March 21, 2012 | HK & China

Guosen Securities (HK) Brokerage Co., Ltd.

3

Exhibit 4: Major B2C business models

Category Key companies Features

Integrated online shopping cenre

taobao, Tee Mall, Bsnir.com, Grandview Mall

Comprehensive product range; round-the-clock service; adequate support services

(Currently, taobao occupies most of the market share of domestic online retail market)

Specialised Saivi.com.cn Specialised in selling branded sporting goods with quality guaranteed

Virtual merchant Amazon.com, Dangdang.com, Amazon.cn

Self-owned warehouses and brands

Vertical M18.com, Redbaby, 360buy, Ugou.cn Selected consumer group; offering full and professional services in specific fields

Manufacturer direct Giordano, BELLE Differentiated products and target consumers for online retail and traditional transactions

Source: Guosen Securities (HK)

2 Major driving forces

2.1 Fast growing logistics industry

Logistics is a pillar industry of the national economy; for 1-3Q2011, the coefficient of

logistics demand was 3.7, meaning that the production of one unit of GDP required

3.7 units of logistics service to support it (the number was 3 and 2.2 for the periods of

2005-10 and 2000-05, respectively), which reflects the growing importance of the

logistics industry to China’s economy. However, high logistics cost has resulted in

difficulties in promoting economic efficiency and national consumption. To cope with

this, the central government has released support policies for reducing logistics cost

and boosting the industry’s development. At the same time, many online retailers,

including 360buy, Redbaby, Amazon.cn and Newegg, have established their own

logistics centres in the southeast coastal regions, with the capital support of private

equity funds.

Exhibit 5: Policy incentives for logistics industry

Date of release Policy Purpose

Mar.2009 The plan for adjusting and accelerating the logistics industry To invigorate the industry and promote its structural adjustment

May.2009 The reply of the General Office of the State Council on issues concerning promoting the development of the service outsourcing industry

To promote development of the tertiary sector

Sep.2009 Opinions of the General Office of the State Council on providing financial support for promoting economic development

To offer more financial support to the industry

Mar.2011 Special plans on the development of trade and logistics To promote healthy development of the logistics industry

Jun.2011 State Council Executive meeting addressing promoting healthy development of the logistics industry

Alleviating the tax burden; providing support in respect of land use, logistics management system, to relevant companies

Aug.2011 Opinions of the General Office of the State Council on the policies and measures for promoting the sound development of the logistics industry

To provide guidelines regarding taxation, land policy, logistics management system and technologies

Nov.2011 Notice of the Ministry of Finance and the State Administration of Taxation on carrying out the pilot practice of levying value-added tax in lieu of business tax on the transportation industry and some modern service industries in Shanghai

To establish a more reasonable tax system

Jan.2012 The circular on the urban land use tax policy for bulk commodity storage facilities of logistics enterprises

To reduce the tax burden on logistics companies

Source: Government website, Guosen Securities (HK)

The government has issued various

policies to lower logistics costs and

to boost development of the industry.

Consumer & Retail Sector March 21, 2012 | HK & China

Guosen Securities (HK) Brokerage Co., Ltd.

4

Exhibit 6: Logistics demand and costs

Source: CPAG, Guosen Securities (HK)

2.2 Rapid development of online payment solutions

Development of various online payment solutions, especially electronic payment

methods, has greatly boosted online sales in China. Currently, more than 60% of online

purchases are settled via electronic means, while 29% is collected upon actual delivery

and the rest by postal remittance. Third-party payment and e-banking are the most

frequently used online payment methods, while the former, represented by Alipay and

Tenpay, was used to settle 65% of online payments in 2011.

Exhibit 7: Online payment systems are improving

Source: Roland Berger Report, Guosen Securities (HK)

2.3 Rapid growing number of online users

The number of online shoppers in China reached 46 million in 2007 and has grown at

around 50% per year since, reaching 161 million in 2010, which accounted for 35% of

total Internet users in China. The online shopping penetration rate in China (as a

percentage of overall Internet users) is expected to reach 45% in 2014, 30% more than

that in 2008.

0%

5%

10%

15%

20%

25%

No

n-f

err

ou

s m

eta

l

Paper-

ma

kin

g

Ele

ctr

o-m

ech

an

ics

Ph

arm

ace

utica

ls

Pe

tro

leu

m

pro

ce

ssin

g

Build

ing

m

ate

ria

ls

Ch

em

ica

ls

Na

tio

na

l a

ve

rag

e

Logistics cost as a % of product value

China Japan

0

0.5

1

1.5

2

2.5

3

3.5

4

1991-95 1996-2000 2001-05 2006-10 1-3Q11

Logistics demand

Coefficient of logistics demand

59%

29%

12%

Internet payment

Cash upon delivery

Postal remittance

65%

34%

1%

Third-party payment

E-banking

Mobile-phone payment

50%

8% 6%

6%

9%

21%

Alipay

China UnionPay online payment

ChinaPnR

99Bill

Others

TenPay

Consumer & Retail Sector March 21, 2012 | HK & China

Guosen Securities (HK) Brokerage Co., Ltd.

5

Exhibit 8: Growing number of online shoppers in China, driven by the expansion of

Internet coverage

Source: Winds, Guosen Securities (HK)

2.4 Rapid development of mobile Internet users

The number of mobile Internet users is expected to surpass traditional PC Internet users

by 2013. At present, over 70% of mobile Internet users are between the ages of 20 and

30 years old, while around 60% of female mobile Internet users have received a

bachelor’s degree or higher, with a monthly income of RMB1,000-3,000. As more and

more people are using their mobile phones to surf the web, we estimate online purchases

will further increase in the future

Exhibit 9: Expanding Internet usage is driving up online transactions

Source: China e-Commerce Market 2011-2015 Forecast and Analysis, Guosen Securities (HK)

3 Three features of China‟s online retailing

3.1 High concentration

China’s top three online retailers, namely, taobao, 360buy and Ebay accounted for 75%

of the overall market in 2011, of which taobao contributed 50%, reflecting a highly

0%

10%

20%

30%

40%

50%

60%

70%

0

50

100

150

200

250

300

350

400

450

500

2004 2005 2006 2007 2008 2009 2010

mn

Population of online shoppers in China (mn, LHS)

Population of Internet users (mn,LHS)

Growth of online shoppers (RHS)

Growth of Internet users (RHS)

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2007 2008 2009 2010 2011 2012 2013 2014 2015

Growth of Internet users

PC-Internet users Mobile Internet users

0

2

4

6

8

10

12

14

16

18

20

2009 2010 2011 2012 2013 2014

RMB tr

Online tranaction volume

China Japan US

Consumer & Retail Sector March 21, 2012 | HK & China

Guosen Securities (HK) Brokerage Co., Ltd.

6

concentrated industry. Both the profitability and employee numbers of online stores grew

significantly across the years. Based on the survey by Alibaba Group Research Centre,

as at June 2011, over 70% of online retailers recorded annual sales of RMB10 million

plus, while 17% of which achieved annual sales of RMB100 million plus (2010: 4%). As

the market concentration rate and specialisation level rise, more than 50% of online

retailers are now planning to establish and promote their own brands.

Exhibit 10: Online retailers are becoming more concentrated and specialised

Source: Alibaba Group’s research on the development of “China’s Top 100 Online Retailers in 2011”, Guosen Securities (HK)

3.2 Standardised products

The main products sold online are standardised and easy to deliver. Online sales of

clothing (apparel, headwear and footwear) contributed 26.5% of the total online sales in

China in 2011, while home appliances and consumer electronics made up 24.2%, and

cosmetics and books accounted for the rest. The online clothing market reached

RMB204.9 billion in sales in 2011, representing a 94.7% y-o-y increase. This number is

expected to surpass RMB500 billion in 2014.

Exhibit 11: Clothing is the major product sold online in China

Source: China e-Commerce Market 2011-2015 Forecast and Analysis, Guosen

Securities (HK)

0%

10%

20%

30%

40%

50%

60%

70%

2008 2009 2010 2011

<RMB1mn RMB1-10mn

RMB10-100mn >RMB100mn

e-commerce sales of China's top 100 online retailers

0%

10%

20%

30%

40%

50%

60%

2008 2009 2010 2011

Numbers of employees of China's top 100 online retailers

0-10 10-100 100-500

500-1000 >1000

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

0

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013 2014

RMB bn

Online transaction volume of clothing (RMB bn, LHS)

Growth (RHS)

Clothing sales' share in total online sales (RHS)

Online sales of clothing grew 94.7% in

2011 in China to RMB204.9 billion. We

forecast such sales will surpass

RMB500 billion in 2014.

Consumer & Retail Sector March 21, 2012 | HK & China

Guosen Securities (HK) Brokerage Co., Ltd.

7

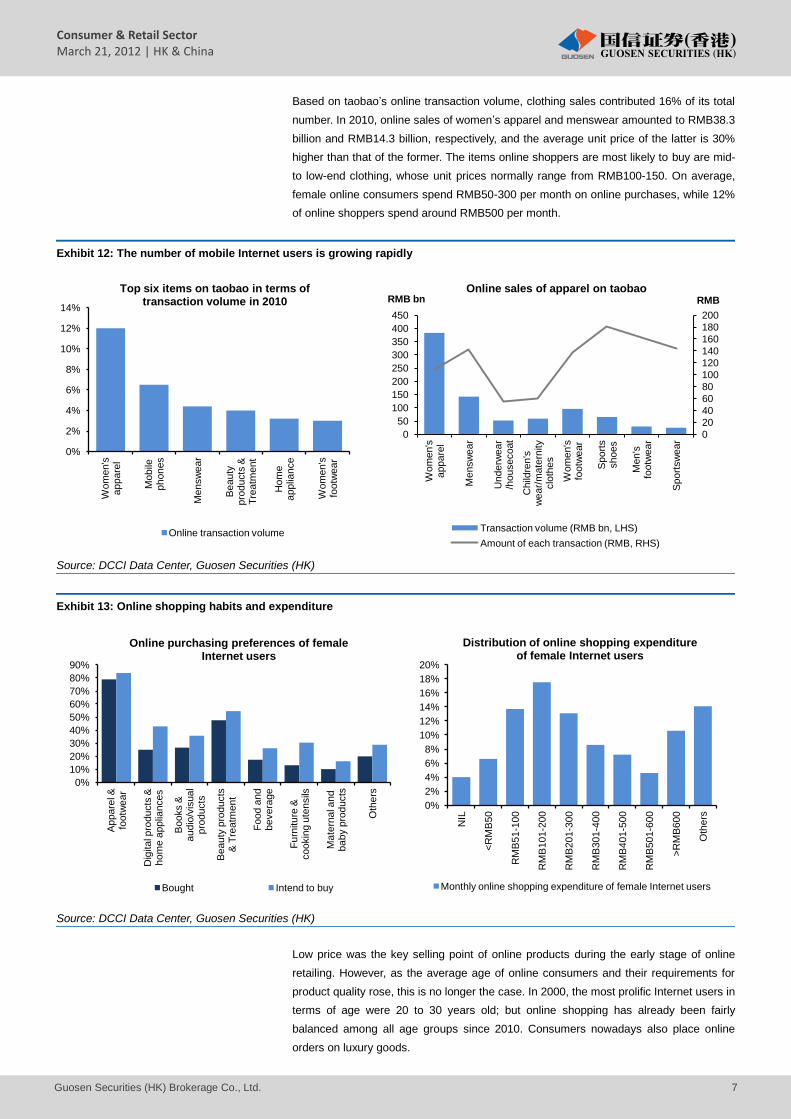

Based on taobao’s online transaction volume, clothing sales contributed 16% of its total

number. In 2010, online sales of women’s apparel and menswear amounted to RMB38.3

billion and RMB14.3 billion, respectively, and the average unit price of the latter is 30%

higher than that of the former. The items online shoppers are most likely to buy are mid-

to low-end clothing, whose unit prices normally range from RMB100-150. On average,

female online consumers spend RMB50-300 per month on online purchases, while 12%

of online shoppers spend around RMB500 per month.

Exhibit 12: The number of mobile Internet users is growing rapidly

Source: DCCI Data Center, Guosen Securities (HK)

Exhibit 13: Online shopping habits and expenditure

Source: DCCI Data Center, Guosen Securities (HK)

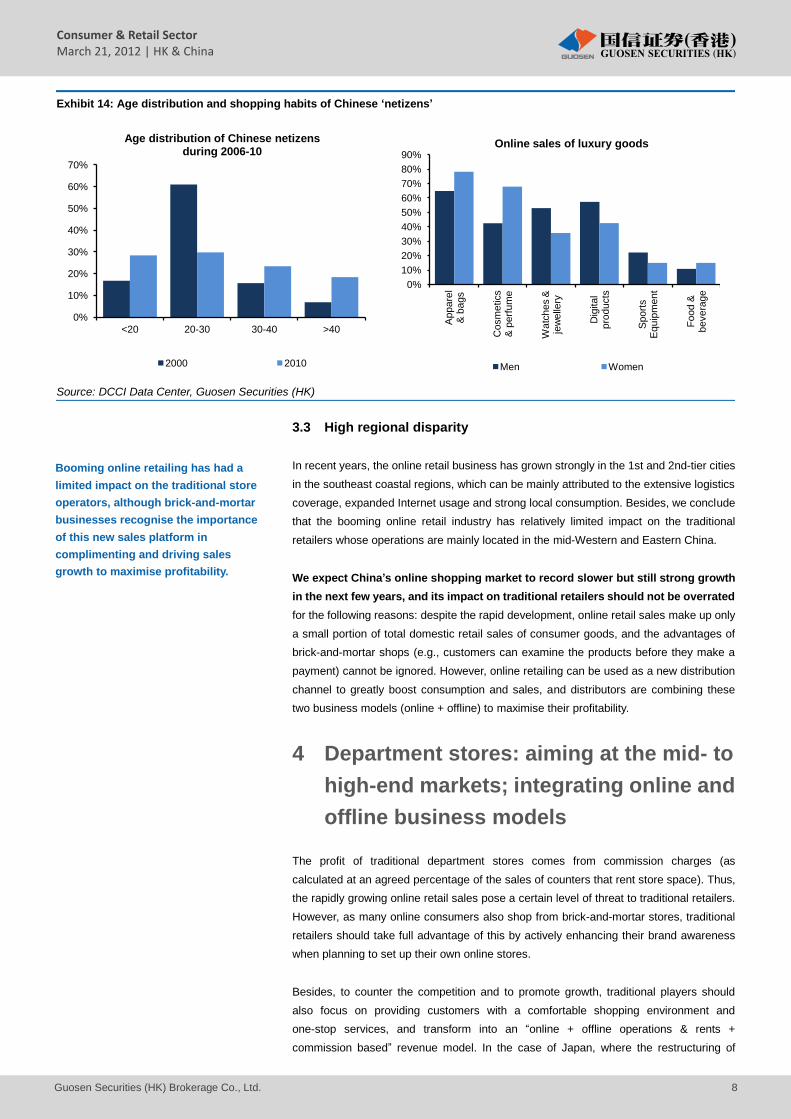

Low price was the key selling point of online products during the early stage of online

retailing. However, as the average age of online consumers and their requirements for

product quality rose, this is no longer the case. In 2000, the most prolific Internet users in

terms of age were 20 to 30 years old; but online shopping has already been fairly

balanced among all age groups since 2010. Consumers nowadays also place online

orders on luxury goods.

0%

2%

4%

6%

8%

10%

12%

14%

Wo

me

n's

appare

l

Mo

bile

phones

Me

nsw

ea

r

Be

au

ty

pro

du

cts

&

Tre

atm

en

t

Ho

me

applia

nce

Wo

me

n's

fo

otw

ea

r

Top six items on taobao in terms of transaction volume in 2010

Online transaction volume

0

20

40

60

80

100

120

140

160

180

200

0

50

100

150

200

250

300

350

400

450

Wo

me

n's

appare

l

Me

nsw

ea

r

Un

de

rwe

ar

/ho

use

co

at

Ch

ildre

n's

w

ea

r/m

ate

rnity

clo

the

s

Wo

me

n's

fo

otw

ea

r

Sp

ort

s

sh

oe

s

Me

n's

fo

otw

ea

r

Sp

ort

sw

ea

r

RMB RMB bn Online sales of apparel on taobao

Transaction volume (RMB bn, LHS)

Amount of each transaction (RMB, RHS)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Appare

l &

foo

twe

ar

Dig

ita

l pro

du

cts

&

ho

me

ap

plia

nce

s

Bo

oks &

a

ud

io/v

isua

l p

rod

ucts

Be

au

ty p

rod

ucts

&

Tre

atm

en

t

Fo

od

an

d

be

ve

rag

e

Fu

rnitu

re &

co

okin

g u

ten

sils

Ma

tern

al a

nd

b

ab

y p

rod

ucts

Oth

ers

Online purchasing preferences of female Internet users

Bought Intend to buy

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

NIL

<R

MB

50

RM

B5

1-1

00

RM

B1

01-2

00

RM

B2

01-3

00

RM

B3

01-4

00

RM

B4

01-5

00

RM

B5

01-6

00

>R

MB

60

0

Oth

ers

Distribution of online shopping expenditure of female Internet users

Monthly online shopping expenditure of female Internet users

Consumer & Retail Sector March 21, 2012 | HK & China

Guosen Securities (HK) Brokerage Co., Ltd.

8

Exhibit 14: Age distribution and shopping habits of Chinese „netizens‟

Source: DCCI Data Center, Guosen Securities (HK)

3.3 High regional disparity

In recent years, the online retail business has grown strongly in the 1st and 2nd-tier cities

in the southeast coastal regions, which can be mainly attributed to the extensive logistics

coverage, expanded Internet usage and strong local consumption. Besides, we conclude

that the booming online retail industry has relatively limited impact on the traditional

retailers whose operations are mainly located in the mid-Western and Eastern China.

We expect China‟s online shopping market to record slower but still strong growth

in the next few years, and its impact on traditional retailers should not be overrated

for the following reasons: despite the rapid development, online retail sales make up only

a small portion of total domestic retail sales of consumer goods, and the advantages of

brick-and-mortar shops (e.g., customers can examine the products before they make a

payment) cannot be ignored. However, online retailing can be used as a new distribution

channel to greatly boost consumption and sales, and distributors are combining these

two business models (online + offline) to maximise their profitability.

4 Department stores: aiming at the mid- to

high-end markets; integrating online and

offline business models

The profit of traditional department stores comes from commission charges (as

calculated at an agreed percentage of the sales of counters that rent store space). Thus,

the rapidly growing online retail sales pose a certain level of threat to traditional retailers.

However, as many online consumers also shop from brick-and-mortar stores, traditional

retailers should take full advantage of this by actively enhancing their brand awareness

when planning to set up their own online stores.

Besides, to counter the competition and to promote growth, traditional players should

also focus on providing customers with a comfortable shopping environment and

one-stop services, and transform into an “online + offline operations & rents +

commission based” revenue model. In the case of Japan, where the restructuring of

0%

10%

20%

30%

40%

50%

60%

70%

<20 20-30 30-40 >40

Age distribution of Chinese netizens during 2006-10

2000 2010

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Ap

pa

rel

& b

ag

s

Co

sm

etics

& p

erf

um

e

Wa

tch

es &

je

we

llery

Dig

ita

l p

rod

ucts

Sp

ort

s

Eq

uip

me

nt

Fo

od

&

be

ve

rag

e

Online sales of luxury goods

Men Women

Booming online retailing has had a

limited impact on the traditional store

operators, although brick-and-mortar

businesses recognise the importance

of this new sales platform in

complimenting and driving sales

growth to maximise profitability.

Consumer & Retail Sector March 21, 2012 | HK & China

Guosen Securities (HK) Brokerage Co., Ltd.

9

traditional retailing has already been completed, department stores are now focusing on

providing different products (such as well-cooked food and semi-finished products) and a

comfortable shopping environment to meet consumers’ leisure requirements, while in

China, department stores normally organise promotional campaigns to boost

consumption.

Exhibit 15: Clothing is the principal product of the online retail industry

Comparison between major B2C business models

Pros Cons

Direct-sales Comprehensive product range Short supply; high logistics cost

Trading platform provider Competitive pricing Lack of logistics management expertise

Manufacturer Competitive pricing; ample supply of goods

Limited product offerings; high logistics costs

Online retailer Extensive product range; ample supply of goods

Lack of technical support of operating virtual stores

Source: China e-Commerce Market 2011-2015 Forecast and Analysis, Guosen

Securities (HK)

Customer traffic is the most crucial growth driver for traditional retailers. In recent years,

many department stores in China have started to associate themselves with the

construction of HOPSCA (retail complexes that have a hotel, offices, parks, a shopping

mall, clubs and apartments), such as Hexi G-City and Intime’s HOPSCA project, and

started to expand themselves into large shopping centres. But the development pace is

slow, mainly because the construction of shopping centres require a large amount of

capital, strong land-purchasing power and the capacity to operate self-owned properties.

As such, this will slow the pace of development of department store operators and put

them at a disadvantage in comparison to property developers when constructing

HOPSCA.

According to our analysis, traditional department stores can carry out the

transformation via two approaches:

4.1 Plan A: To combine department stores with HOPSCA complexes

Successful cases are Wangda Plaza, Van’s Department Store and Intime Ningbo Wanda.

These stores have formed beneficial partnerships with each other, and fully utilised their

advantages to established long-term partnerships with renowned brand names. Besides,

leveraging on their financial strength, they also managed to locate their stores in

favourable places, where high flow of customer traffic and complete ancillary facilities

(such as high-grade office buildings, squares and commercial real estate) are available.

Consumer & Retail Sector March 21, 2012 | HK & China

Guosen Securities (HK) Brokerage Co., Ltd.

10

Exhibit 16: Integrated urban development projects

HOPSCA projects (these complexes normally include a hotel, offices, a park, a shopping mall, clubs and apartments)

Company Project Date of operation Location Construction area of

each building

Golden Eagle Retail Group Hexi G-City Jun 2014 Hexi, Xin Jiang Dong 0.9mn sm2

Better Life HOPSCA project

Wanda Xiamen Huli Wanda Plaza 02 Sep 2011 Xiamen

Wangfujing Dept Store Jihualu Foshan

China Poly Group Dongping New City Foshan 1.0mn sm2

China Poly Group Desheng CBD Foshan 1.0mn sm2

COFCO Dayuecheng Shopping Center Dec 2011 Tianjin

Wanda Hedong Wanda project 2010 ianjin

NWDs Wantai*Yancheng-HK New World Department Store

Source: Guosen Securities (HK)

4.2 Plan B: To continue to conduct offline operations while

establishing their own online stores

We have made some bold assumptions to integrate different business models: firstly, we

classified the existing brands into two categories: “competitive brands” refer to those that

are highly popular with a large custom base (e.g. “Chow Tai Fook” and “Chow Sang Sang”

for jewellery, and “ONLY”, “Orchirly” and “IT” for casual wear), and “distinguishable

brands” are those with less consumer awareness. Products with “competitive brands”

can be sold via third-party online stores (e.g. taobao and 360buy), department stores, or

self-owned flagship stores where their brand images can be fully presented. As for the

products with “distinguishable brands”, retailers can adopt the “online sales +

commission-based” business model, i.e. to offer brand names with concessionary rents

for the brick-and-mortar stores, and charge commissions for selling their products

through online retail sites.

5 Physical specialty shops: focus on

promoting brand awareness and

expanding sales channels

As for traditional retailers with brick-and-mortar stores, online retailing can be used as an

additional sales channel to promote brand awareness. Manufacturers can set up their

own Internet platform to sell products. The function of offline franchise stores will be

shifted to presenting brands, and more effort will be exerted into establishing self-owned

stores to promote brand awareness.

B2C players adopt one of two different approaches to solve their logistics issue: the

platform approach and the self-build approach. Under the first approach, which is

adopted by taobao, logistics services are largely provided by third-party partners, while

under the latter, which is adopted by Suning and Intime, B2Cs are exposed to all the

elements in the logistics chain. Many retailers preferred the platform approach in the

previous years, mainly because the online retail business was quite new to them, and it

would cost a lot to establish their own logistics platform. However, given the scalability of

the self-build approach, which allows the B2C players to drive volume growth and

increase business scale quickly, it will be adopted by more retailers in the future. We

Consumer & Retail Sector March 21, 2012 | HK & China

Guosen Securities (HK) Brokerage Co., Ltd.

11

believe more and more traditional players are beginning to tap into the e-business arena,

to remove the restrictions of their geographical locations and complement their offline

sales efforts.

Exhibit 17: Growth of different online business models

Source: Guosen Securities (HK)

Risk factors

1. The rapid development of China’s online retail industry is currently largely funded by

private equity investment. Thus, insufficient funds would severely affect the

performance and the pace of the industry’s development. In addition, intense price

competition between retailers has caused losses among online players, which has

created uncertainty to their future development.

2. The transition from traditional department stores to shopping plazas needs to be

supported by enormous investments, and requires strong project implementation

skills and operational expertise. Establishing self-owned online stores also require

large capital investments, and no successful cases have been recorded yet.

3. Brand names that have experienced rapid development through franchisees are

now suffering losses, and may not be able to meet the financial requirements of

setting up self-owned stores. Besides, operating self-owned stores require expertise

in terms of managing inventories and the supply of new products.

-20%

0%

20%

40%

60%

80%

100%

120%

2009 2010 2011 2012 2013 2014

Growth of the usage of platform approach among B2Cs

Growth of the usage of self-build approach among B2Cs

Growth of C2C segment's share

Consumer & Retail Sector March 21, 2012 | HK & China

Guosen Securities (HK) Brokerage Co., Ltd.

12

Information Disclosures

Stock ratings, sector ratings and related definitions

Stock Ratings:

Buy: A return potential of 10 % or more relative to overall market within 6 – 12 months.

Neutral: A return potential ranging from -10% to 10% relative to overall market within 6 – 12 months.

Sell: A negative return of 10% or more relative to overall market within 6 –12 months.

Sector Ratings:

Buy: The sector will outperform the overall market by 10% or higher within 6 –12 months.

Neutral: The sector performance will range from -10% to 10% relative to overall market within 6 –12 months.

Sell: The sector will underperform the overall market by 10% or lower within 6 – 12 months.

Interest disclosure statement

The analyst is licensed by the Hong Kong Securities and Futures Commission. Neither the analyst nor his/her associates serves as an

officer of the listed companies covered in this report and has no financial interests in the companies.

Guosen Securities (HK) Brokerage Co., Ltd. and its associated companies (collectively “Guosen Securities (HK)”) has no disclosable

financial interests (including securities holding) or make a market in the securities in respect of the listed companies. Guosen Securities

(HK) has no investment banking relationship within the past 12 months, to the listed companies. Guosen Securities (HK) has no

individual employed by the listed companies.

Disclaimers

The prices of securities may fluctuate up or down. It may become valueless. It is as likely that losses will be incurred rather than profit

made as a result of buying and selling securities.

The content of this report does not represent a recommendation of Guosen Securities (HK) and does not constitute any buying/selling or

dealing agreement in relation to the securities mentioned. Guosen Securities (HK) may be seeking or will seek investment banking or

other business (such as placing agent, lead manager, sponsor, underwriter or proprietary trading in such securities) with the listed

companies. Individuals of Guosen Securities (HK) may have personal investment interests in the listed companies.

This report is based on information available to the public that we consider reliable, however, the authenticity, accuracy or completeness

of such information is not guaranteed by Guosen Securities (HK). This report does not take into account the particular investment

objectives, financial situation or needs of individual clients and does not constitute a personal investment recommendation to anyone.

Clients are wholly responsible for any investment decision based on this report. Clients are advised to consider whether any advice or

recommendation contained in this report is suitable for their particular circumstances. This report is not intended to be an offer to buy or

sell or a solicitation of an offer to buy or sell the securities mentioned.

This report (including any information attached) is issued by Guosen Securities (HK) Brokerage Co., Ltd, a member of Guosen Securities

Co., Ltd. Some parts of the report may have been originally published in Chinese, within the People’s Republic of China, by Guosen

Securities Co., Ltd. That material has been reviewed, translated and, where applicable, adapted by Guosen Securities (HK) Brokerage

Co., Ltd. This report is for distribution only to clients of Guosen Securities (HK). Without Guosen Securities (HK)’s written authorization,

any form of quotation, reproduction or transmission to third parties is prohibited, or may be subject to legal action. Such information and

opinions contained therein are subject to change and may be amended without any notification.