tr 2013/5 - the impact on smsf pensions

TRANSCRIPT

WEBINAR:

TR 2013/5: WHEN A PENSION

COMMENCES AND CEASES

THE IMPACT ON

SMSF PENSIONS

Aaron Dunn

The SMSF Academy

© The SMSF Academy 2013

• Attendees are muted for the session

• Presentation slides & tax ruling can be accessed from the materials tab or URL link in chat box

• You can type questions to the presenter from your screen• Podcast will be made available of all questions

following webinar

• Webinar recording• Available to SMSF Academy members within

the resource library

• Will be made available to purchase online from the SMSF Academy website for $55 (incl. GST)

HOUSEKEEPING

GENERAL ADVICE WARNING

This presentation provides general advice only. No direct or implicit recommendations aregiven in this presentation. This means that the general advice provided has not beenprepared taking into account any individual’s financial circumstances (i.e. investmentobjectives, financial situation and particular investment needs).

The SMSF Academy Pty Ltd believes that the information in this presentation is correct at thetime of compilation but does not warrant the accuracy of that information. Save for statutoryliability which cannot be excluded, The SMSF Academy disclaims all responsibility for any lossor damage which any person may suffer from reliance on this information or any opinion,

conclusion or recommendation in this presentation whether the loss or damage is caused byany fault or negligence on the part of presenter or otherwise.

© The SMSF Academy, 2013

What is an ‘superannuation income stream’?

‘Income’ + ‘Stream’ given their ordinary meaning

TR 2013/5 states:

Trustee has a liability to make a series of periodic payments that relate to each

other over an identifiable period of time

Need not be

paid at same,

recurring

intervals

Can also

vary in

amount

What does

periodic

payments

mean?

Must meet

pension

requirements

of SIS Reg

1.06(1)

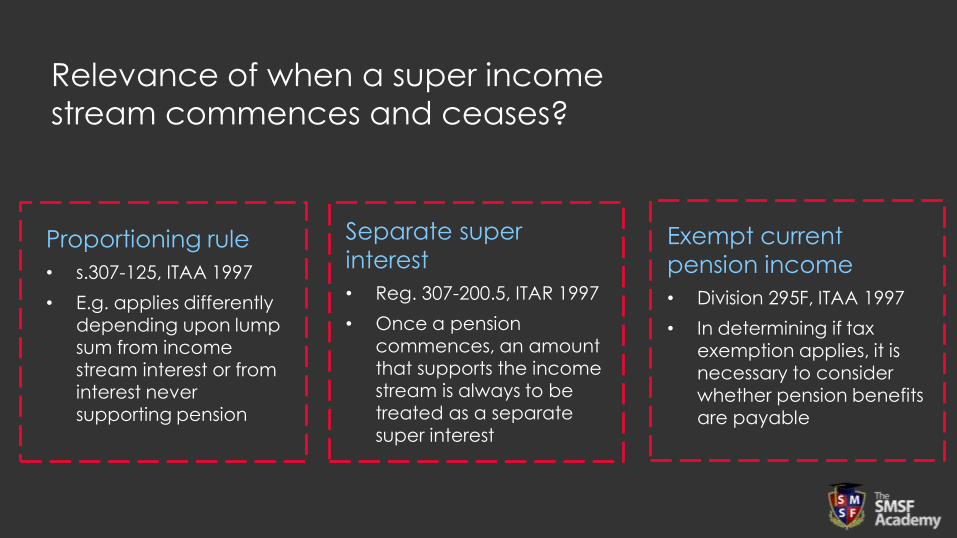

Relevance of when a super income

stream commences and ceases?

Proportioning rule

• s.307-125, ITAA 1997

• E.g. applies differently depending upon lump sum from income stream interest or from interest never

supporting pension

Separate super

interest

• Reg. 307-200.5, ITAR 1997

• Once a pension

commences, an amount that supports the income stream is always to be treated as a separate super interest

Exempt current

pension income

• Division 295F, ITAA 1997

• In determining if tax exemption applies, it is necessary to consider

whether pension benefits are payable

Meet Kerry

The trustees of her SMSF dispose of a property triggering large

capital gain

Kerry receives a monthly pension from her

transition to retirement income stream

Do we have an income stream?

Kerry has been drawing a pension annually

for the past 3 years

Kerry commences a pension to eliminate

the capital gain and rolls back to

accumulation in the following income year

Super

income

stream

Each periodic payment made from a pension account is a super income stream benefit (pension) unless an election is

made under regulation 995-1.03 of ITAR 1997 for amount not to be treated as an income stream benefit

Is the payment a super income stream or a lump sum amount?

Super lump sum includes:• Payment from pension where member elects

before payment is made to not treat as super

income stream benefit; or• Payment made from super interest that as

ceased to support a pension

Pension payments

WHEN DOES A PENSION COMMENCE?

Can never commence before

all capital has

been added to support the income

stream

Commencement

date is determined by reference to T&Cs of pension,

governing rules & SIS Regs.

Commencement can occur before due date of first payment, but

cannot precede

member’s date of request

Pension once commenced is

always an income stream until ceased.

Remains true even if member dies before

payment is due

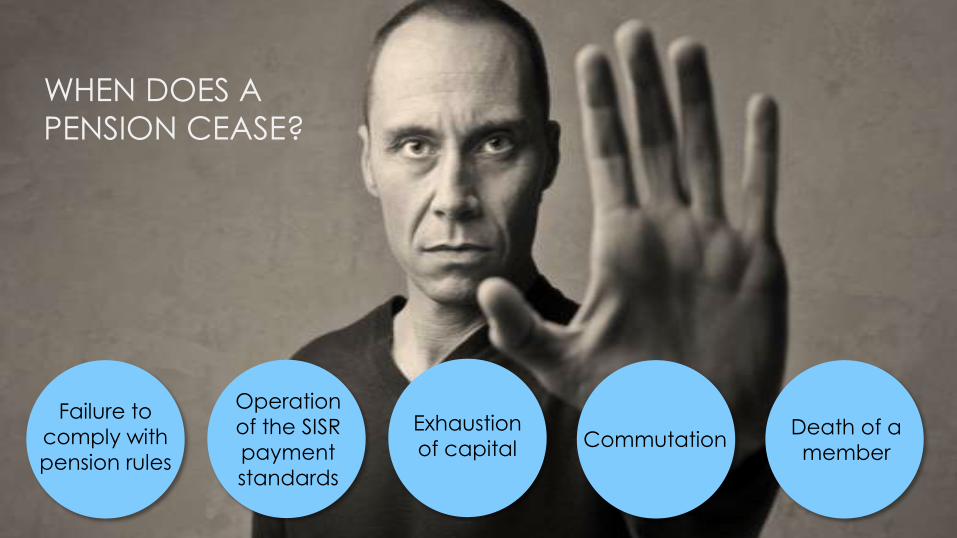

WHEN DOES A

PENSION CEASE?

Failure to

comply with

pension rules

Operation

of the SISR

payment

standards

Exhaustion

of capital CommutationDeath of a

member

FAILURE TO COMPLY WITH PENSION RULES

Super Income

Stream

SISR 1.06(1)

SISR 1.06(9A)

SISR 1.07D

=

+

+

Requirements not metIncome stream will have ceased at the

start of the income year for tax purposes

Any withdrawals

are Lump Sums

Failure to meet TRIS

requirements

(under or over payment)

is a big problem!

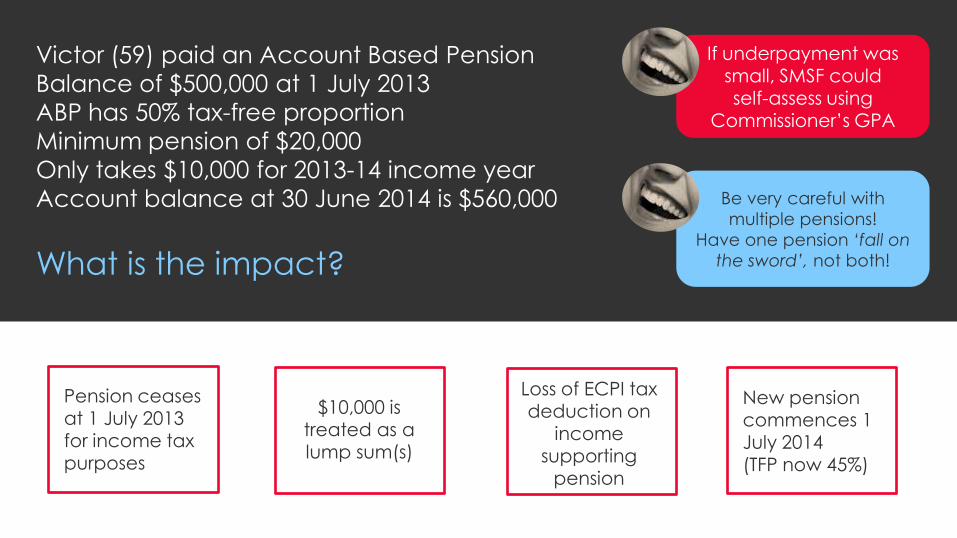

Victor (59) paid an Account Based Pension

Balance of $500,000 at 1 July 2013

ABP has 50% tax-free proportion

Minimum pension of $20,000

Only takes $10,000 for 2013-14 income year

Account balance at 30 June 2014 is $560,000

Pension ceases at 1 July 2013 for income tax

purposes

$10,000 is treated as a lump sum(s)

Loss of ECPI tax deduction on

income supporting

pension

New pension commences 1 July 2014

(TFP now 45%)

If underpayment was

small, SMSF could self-assess using

Commissioner’s GPA

What is the impact?

Be very careful with

multiple pensions!

Have one pension ‘fall on

the sword’, not both!

To ‘commute’ is to change (one kind

of payment) into or for another, as by

substitution

When has there been a full commutation?

COMMUTATION

1No longer a

liability to

provide super

income stream

benefits

2Income stream

ceases before

the lump sum

payment is

made (election)

3As payment is

made after full

commutation,

payment is a

lump sum for tax

purposes

Commissioner

considered facts of both Hammerton’s &

Cooper’s cases

4Must meet

SIS Reg 1.07D

requirements on

pro-rata

minimum prior to

commutation

PARTIAL COMMUTATION

Conscious decision to exercise right to

exchange an amount (less than entire balance)

from income stream to be paid as a lump sum

As obligation remains to continue to pay pension, partial

commutation does not cease the income stream

If partial commutation

occurs, the resulting

payment is a income

stream benefit for

income tax purposes

Unless, an election is made

under para 995-1.03(b) of

ITAR 1997 not to treat

payment as pension, but

rather a lump sum

Won’t apply to

Transition to Retirement Income Streams

WHEN TO CONSIDER THE ELECTING

TO TAX AS A LUMP SUM?

Under 60

Taxable Income is greater than

$46,110*

Over 60

Minimum is greater than member requirements (in-

specie asset transfer

* Taxable Income $46,110 - Tax $6,533 + Medicare levy $691 – Pension

offset ($6,916) – LITO ($308) = $0

SMSFD 2013/2:

Does a payment made as a result of a

commutation of an

account based pension count towards the

minimum annual pension amount required to be

paid under SISR 1.06(9A)?

DEATH OF A MEMBER

Tax

DependantIncome

Stream

Does the

pension

automatically

transfer?

How does

the pension

continue?

If allowed

under fund’s

governing rules

Other rules

governing the

income stream

Rules must specify:• Person to whom the

benefit will become

payable; and• In the form of an income

stream

(may also specific

class of person, i.e.

spouse)

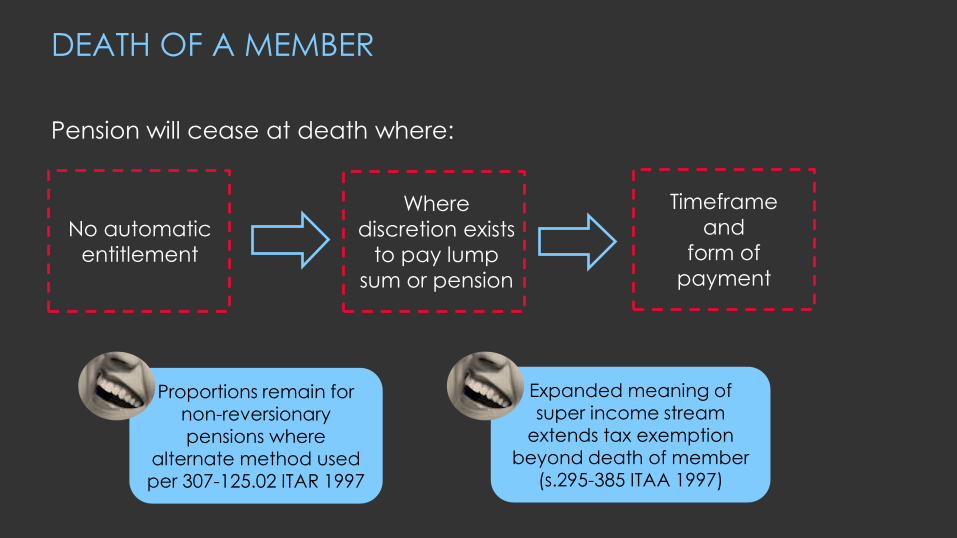

DEATH OF A MEMBER

Pension will cease at death where:

No automatic

entitlement

Where

discretion exists

to pay lump

sum or pension

Timeframe

and

form of

payment

Proportions remain for non-reversionary

pensions where alternate method used per 307-125.02 ITAR 1997

Expanded meaning of

super income stream extends tax exemption

beyond death of member (s.295-385 ITAA 1997)

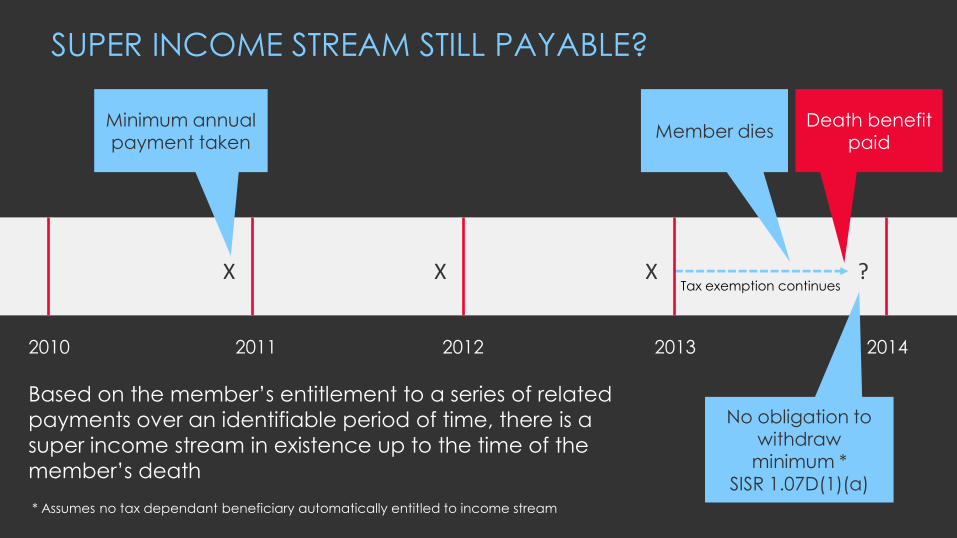

2010 2011 2012 2013 2014

X X X ?

Minimum annual payment taken

Member dies

SUPER INCOME STREAM STILL PAYABLE?

Based on the member’s entitlement to a series of related

payments over an identifiable period of time, there is a

super income stream in existence up to the time of the

member’s death

Death benefit paid

Tax exemption continues

No obligation to withdraw

minimum *SISR 1.07D(1)(a)

* Assumes no tax dependant beneficiary automatically entitled to income stream

Changing Face of SMSFs

• Quarterly Technical & Regulatory

Update

• Included for members

• Non-members: $99 (incl. GST)

– Keep an eye out for special offers!

NEXT WEBINAR

DATE:

Thursday, 22 August 2013

11am, AEDST

Podcast created

with webinar

questions in follow

email as wellFollow up email

with survey for your

valuable feedback

Any final questions?

www.thesmsfacademy.com.au/webinar-survey

Aaron DunnThe SMSF Academywww.thesmsfacademy.com.au

SMSF Dunn Right,

http://thedunnthing.com

Follow, Like or connect with Aaron and the SMSF Academy:FOLLOW, LIKE OR CONNECT WITH US