tp march 26

TRANSCRIPT

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 1/67

By:CA.Gaurav Garg

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 2/67

Back-GroundApplicabilityResponsibility of the Taxpayer

Role of a Chartered Accountant – Form 3CEBTransfer Pricing MethodsTransfer Pricing DocumentationHandle With CareOpen House

03/26/2011 2JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 3/67

Back-Ground

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 4/67

The provisions relating to Transfer Pricing (“TP”) are there intreaties since long.TP regulation is there in almost all the major economies of theWorld.TP regulations in India

March 1999 – Observation of the Standing Committee on FinanceNovember 1999 – Formation of Expert Group on TPJanuary 2001 – Submission of report by Expert Group on TPFinance Act 2001 – Introduction of TP provisions in the Income TaxAct

DTC will also bring provisions relating to CFC, GAAR, Thin Cap andAPA.

03/26/2011 4JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 5/67

Applicability

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 6/67

Section 92 of the Act“ 92. (1) Any income arising from an international transaction shall becomputed having regard to the arm’s length price.Explanation. — For the removal of doubts, it is hereby clarified that theallowance for any expense or interest arising from an international transaction shall also be determined having regard to the arm’s length price.”

Income/ expense or interestArising from an international transactionShall be computed having regard to the arm’s length price

03/26/2011 6JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 7/67

Meaning of “income”“Section 92 obviously is not intended to bring in a new head of income or to charge the tax on income which is not otherwise

chargeable under the Act.” AAR – 2010 - Dana Corporation

03/26/2011 7JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 8/67

Meaning of International Transaction – Section 92B (1)Transaction between two or more associated enterprises ,either or both of whom are non-residents ,

in the nature of purchase, sale or lease of tangible or intangibleproperty,or provision of services,or lending or borrowing money,or any other transaction having a bearing on the profits, income,losses or assets of such enterprises,

03/26/2011 8JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 9/67

Meaning of International Transaction – Section 92B (1)and shall include a mutual agreement or arrangement betweentwo or more associated enterprises for the allocation orapportionment of, or any contribution to, any cost or expenseincurred or to be incurred in connection with a benefit, service orfacility provided or to be provided to any one or more of suchenterprises.

03/26/2011 9JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 10/67

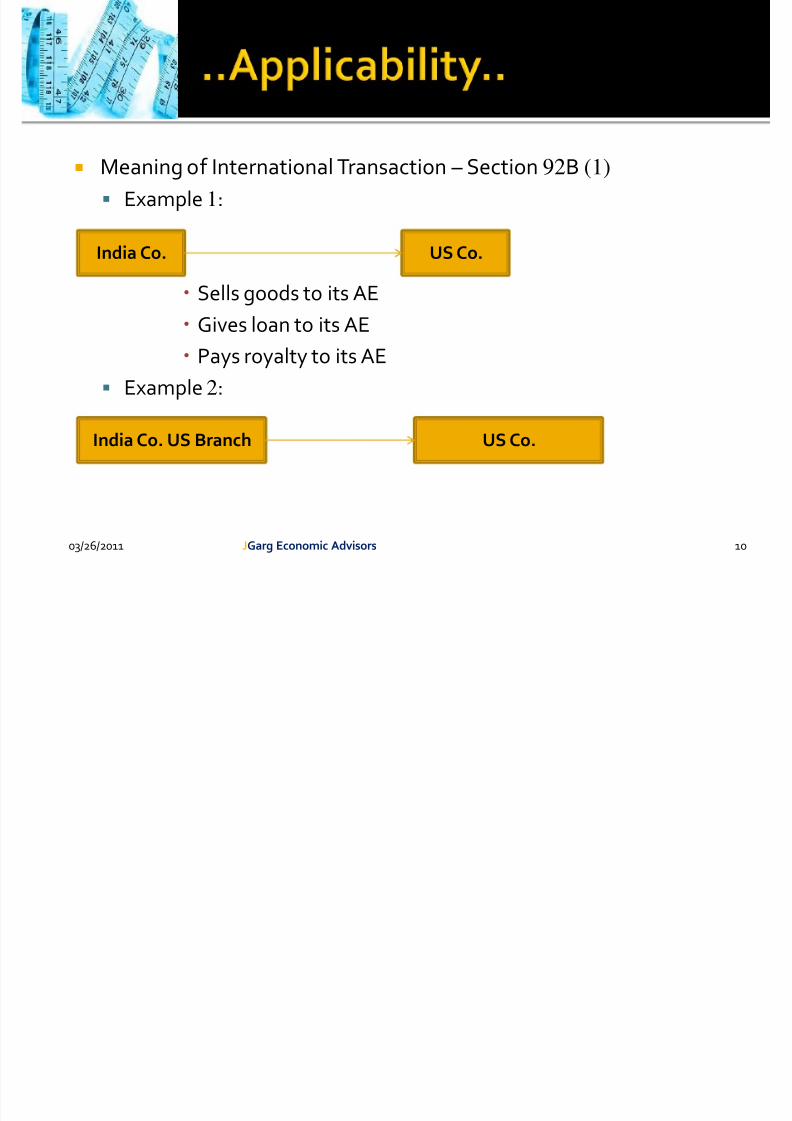

Meaning of International Transaction – Section 92B (1)Example 1:

Sells goods to its AEGives loan to its AEPays royalty to its AE

Example 2:

03/26/2011 10JGarg Economic Advisors

India Co. US Co.

India Co. US Branch US Co.

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 11/67

Meaning of International Transaction – Section 92B (1)Example 3:

Example 4:

03/26/2011 11JGarg Economic Advisors

India Co. US Co. India

Branch

German Co. US Co.

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 12/67

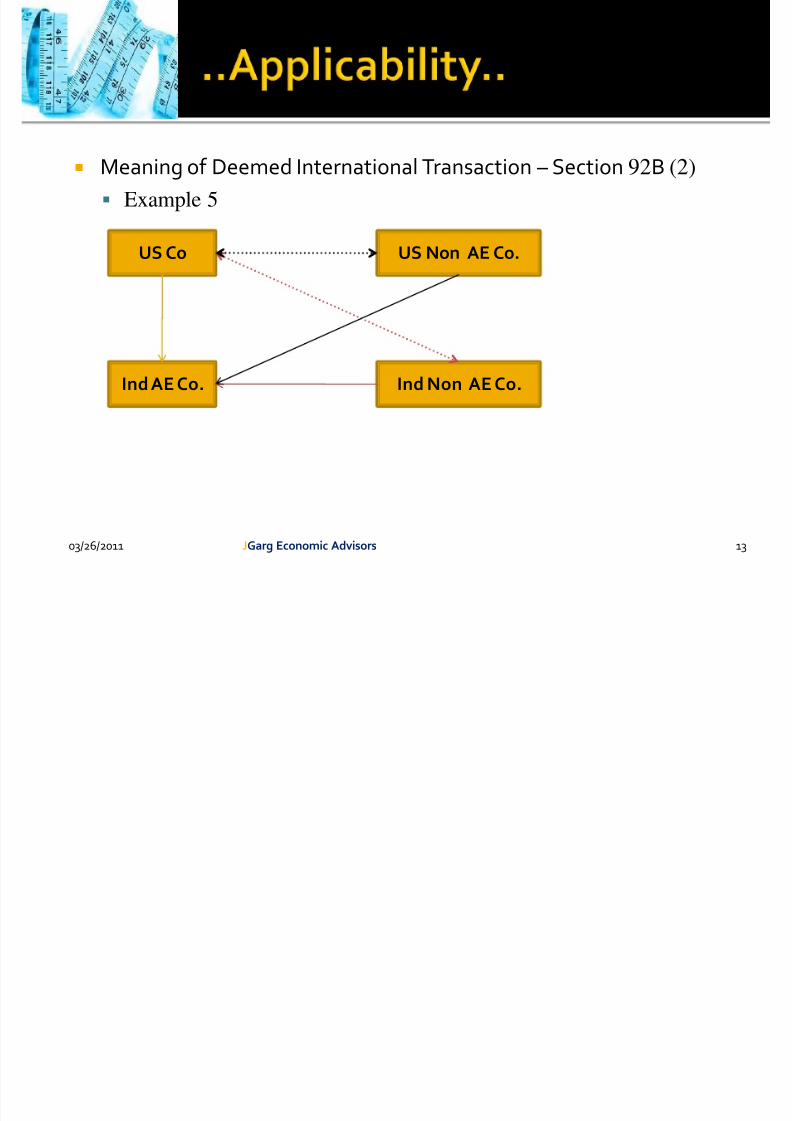

Deemed to be transaction between associated enterprises –Section 92B (2)

A transaction entered into by an enterprise with a person other

than an associated enterprise, shall,for the purposes of sub-section (1),be deemed to be a transaction entered into between twoassociated enterprises,if there exists a prior agreement in relation to the relevanttransaction between such other person and the associatedenterprise , orthe terms of the relevant transaction are determined insubstance between such other person and the associatedenterprise .

03/26/2011 12JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 13/67

Meaning of Deemed International Transaction – Section 92B (2)Example 5

03/26/2011 13JGarg Economic Advisors

US Co

Ind AE Co.

US Non AE Co.

Ind Non AE Co.

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 14/67

Meaning of Deemed International Transaction – Section 92B (2)Example 6

03/26/2011 14JGarg Economic Advisors

Ind Parent Co.

Ind Subs Co.

US Non AE Co.

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 15/67

“These are again machinery provisions which would not apply inthe absence of liability to pay tax”

Vanenburg Group B.V. vs CITAAR– 289 ITR464

Meaning of Associated Enterprise – Section 92AParticipation in the management or control or capitalCommon participation in the management or control or capital12 specific conditions when two enterprises can be deemed to beassociated enterprises – section 92A(2)

03/26/2011 15JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 16/67

Responsibility of the Taxpayer

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 17/67

Taxpayer must compute the arm’s length price of internationaltransactions as per the methods prescribed under section 92C.Burden of proof is on the taxpayer to establish the arm’s length priceand to maintain related documents . [Bangalore ITAT – Aztec Software& Technology Services Ltd. ]Must obtain a report under Form 3CEB from a CharteredAccountant and file it before tax authorities within due date of filing of return of income.

For assessment year 2011-12 and onwards, due date would be 30November [ Finance Bill 2011 ]Tax payer must submit the transfer pricing document to the taxauthorities, within 30 days of the receipt of notice from thedepartment.

03/26/2011 17JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 18/67

PenaltiesNon maintenance of documents – 2% of the value of internationaltransaction – Section 271 AA

Non filing of Form 3CEB– Rs.100,000/- - Section 271 BAFailure to furnish information or document to tax authorities – 2%of the value of international transaction – Section 271G

03/26/2011 18JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 19/67

Role of a Chartered Accountant – Form 3CEB

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 20/67

Scope of examination under section 92 E of the ActForm 3CEB & Annexure to Form 3CEBForm 3CEB Para 1

“*I/we have examined the accounts and records of ………………..(name and address of the assessee with PAN) relating to theinternational transactions entered into by the assessee during the previous year ending on 31st March, ……….”

03/26/2011 20JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 21/67

Scope of examination under section 92 E of the ActGuidance Note on Transfer Pricing issued by the ICAI

“36.9 Ensuring completeness of the listing of international transactionsis the responsibility of the assessee….”

“36.10 The accountant should obtain a written representation from theassessee providing him with the name, address, legal status and

country of tax residence of each of the enterprises with whominternational transactions have been entered into by the assessee, and association linkages among them.”

03/26/2011 21JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 22/67

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 23/67

Scope of examination under section 92 E of the ActGuidance Note on Transfer Pricing issued by the ICAI

“36.12 …… I t should however be noted that the accountant is not responsible for the content of the transactions and documentationmaintained by the assessee. ”

“36.13 ….If any document is not maintained, then the accountant

should suitably qualify his report or disclose the same in his report depending upon the facts and circumstances of each case. Theaccountant should state the qualification in the report making it comprehensive and self explanatory …”

03/26/2011 23JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 24/67

Scope of examination under section 92 E of the ActForm 3CEB Para 2“ 3. The particulars required to be furnished under section 92 E are given in the Annexure to this Form. In *my/our opinion and to thebest of my/our information and according to the explanations givento *me/us, the particulars given in the Annexure are true and correct ”.

03/26/2011 24JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 25/67

Scope of examination under section 92 E of the ActGuidance Note on Transfer Pricing issued by the ICAI

“36.16… As mentioned above, the particulars should be obtained fromthe assessee, duly authenticated, which should be reviewed by theaccountant. In case of any negative remark or qualification about thismatter, the same should be properly reported.”

03/26/2011 25JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 26/67

Scope of examination under section 92 E of the ActGuidance Note on Transfer Pricing issued by the ICAI

“36.17 The accountant must limit his scope of work and the review procedures to the extent certified in Form No.3CEB . For e.g. in the Annexure the method which has been used to determine the arm’slength price needs to be stated. In this context the accountant is onlyrequired to ensure that the method stated as being used to determinethe arm’s length price by the assessee has actually been used and it isnot the accountant’s responsibility to ensure that the method so used isthe most appropriate method as prescribed by the Board.”

03/26/2011 26JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 27/67

Scope of examination under section 92 E of the ActAnnexure to Form 3CEB

13 Clauses

Clause 1 – Name of the assesseeClause 2 – AddressClause 3 – Permanent account numberClause 4 – Status

Clause 5 – Previous year endedClause 6 – Assessment year

03/26/2011 27JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 28/67

Scope of examination under section 92 E of the ActAnnexure to Form 3CEB

Clause 7 – List of the associated enterprises with whom the

assessee has international transactionsClause 8 – Particulars in respect of transactions in tangiblepropertyClause 9 – Particulars in respect of intangible property

Clause 10 – Particulars in respect of providing servicesClause 11 - Particulars in respect of lending or borrowing of money

03/26/2011 28JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 29/67

Scope of examination under section 92 E of the ActAnnexure to Form 3CEB

Clause 12 – Particulars in respect of mutual agreement or

arrangementClause 13- Particulars in respect of any other transactions

03/26/2011 29JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 30/67

Transfer Pricing Methods

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 31/67

OECD Guidelines

JGarg Economic Advisors 31

TP Methods

Indian Regulations

CUP Methods

Resale Price Method

Cost Plus Method

Profit Split Method

Transactional Net Margin Method

CUP Methods

Resale Price Method

Cost Plus Method

Profit Split Method

Transactional Net Margin Method

03/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 32/67

In generalComparable Uncontrolled Price (“CUP”) Method compare pricesResale Price Method (“RPM”) compares gross margins

Cost Plus Method (“CPM” compares profit mark -ups on costsProfit Split Method (“PSM”) refers to the (total) profits fromtransactions and splits them among the parties based on the levelof contributionTransactional Net Margin Method (“TNMM”) analyses net profit inrelation to an appropriate base, such as costs, sales or assets

JGarg Economic Advisors 3203/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 33/67

CUP MethodMost direct way of determining an ALPIt compares the price charged for goods or services transferred in

an international transaction to the price charged for property orservices transferred in a comparable uncontrolled transaction.Price is adjusted to account for differences, if any, between theinternational transaction and the comparable uncontrolledtransactions or between the enterprises entering into such

transactions, which could materially affect the price in the openmarket.

JGarg Economic Advisors 3303/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 34/67

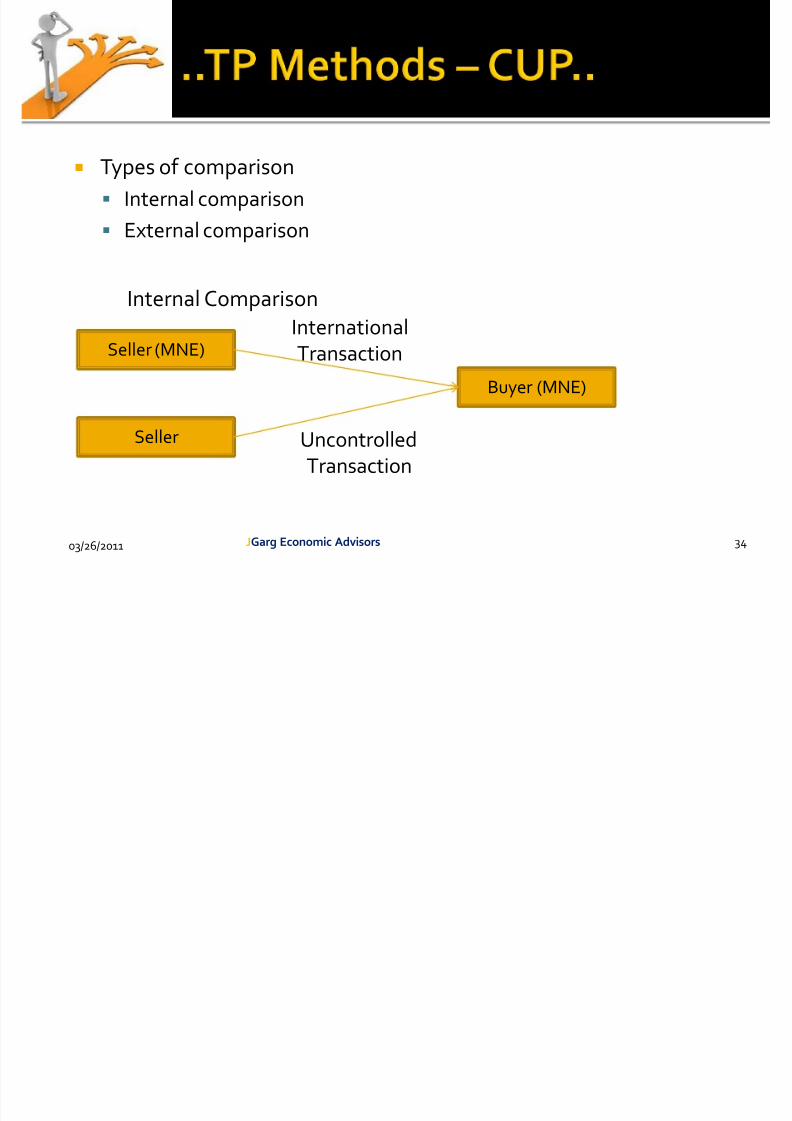

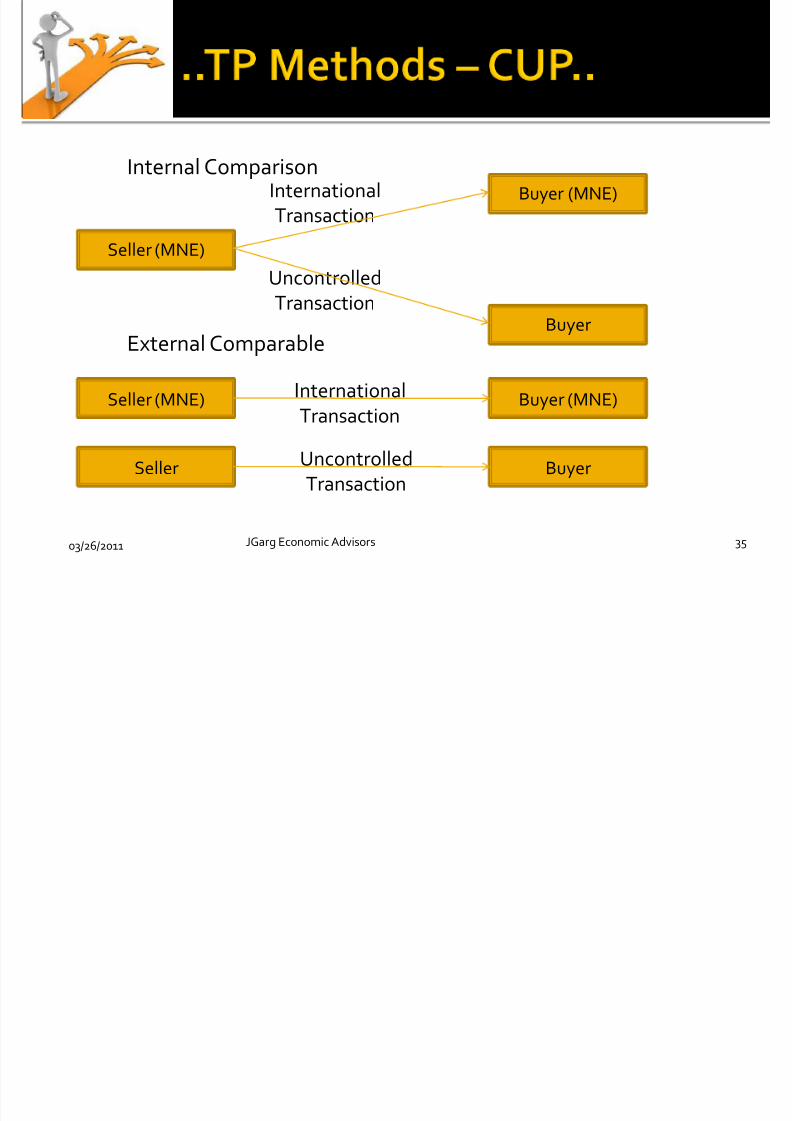

Types of comparisonInternal comparisonExternal comparison

Internal Comparison

JGarg Economic Advisors 34

Seller (MNE)

Buyer (MNE)

Seller

InternationalTransaction

UncontrolledTransaction

03/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 35/67

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 36/67

ComparabilityThe comparability of property transferred in an internationaltransaction and an uncontrolled transaction is most decisive forthe application.Intended purpose of use, branding or customer perception andpreference would impact applicability.Market comparability is another important factor to be considered.Contractual term including quantity of property sold or acquired,

volume discounts, applicable currency, marketing, advertising,after sale support, duration of contract, terms of delivery, terms of payment etc can not be ignored.

JGarg Economic Advisors 3603/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 37/67

Resale Price Method (‘RPM’)The resale price method measures an arm's length price bysubtracting the appropriate gross profit from the applicable resaleprice for the property involved in the controlled transaction underreview.The price is adjusted to take into account the functional and otherdifferences, including differences in accounting practices, if any,between the international transaction and the comparable

uncontrolled transactions, or between the enterprises enteringinto such transactions, which could materially affect the amount of gross profit margin in the open market.

JGarg Economic Advisors 3703/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 38/67

Example 7

International Transaction

Uncontrolled Transaction

JGarg Economic Advisors 38

Seller (MNE)

Buyer/Seller(MNE)

Buyer100

120

Buyer105 130

Seller

03/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 39/67

ApplicabilityReseller should not make any material alterations to the producttraded.

ComparabilityProduct comparability not very important, however better theproduct comparability better would be the resultsMore functions and asset, higher risk would require higher grossmarginAccounting variations should be taken careOther factors like geographical differences, volume, highoperating cost may effect comparison

JGarg Economic Advisors 3903/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 40/67

Cost Plus Method (‘CPM’)The cost plus method tests whether a profit mark-up charged in ainternational transaction is at arm’s length by reference to themark-up charged in uncontrolled transactions.Transfer pricing is calculated by adding a mark-up, earned inuncontrolled transactions, to a direct and indirect cost of production/ services relating to international transaction.

JGarg Economic Advisors 4003/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 41/67

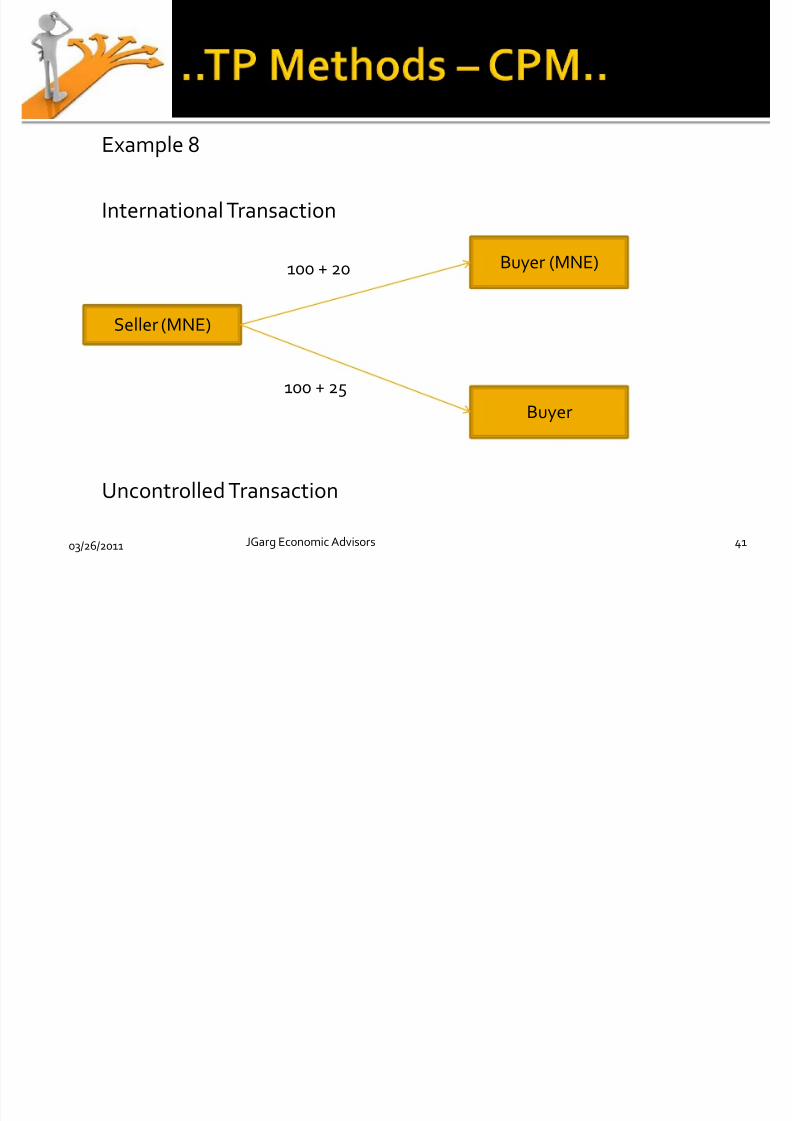

Example 8

International Transaction

Uncontrolled Transaction

JGarg Economic Advisors 41

Seller (MNE)

Buyer (MNE)

Buyer

100 + 20

100 + 25

03/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 42/67

ApplicabilityCPM is useful in case of long-term buy-and-supply agreements,pricing of semi-finished goods, toll or contract manufacturing,services of purchasing agents, contract research etc.

ComparabilityProduct comparability not very important, however better theproduct comparability better would be the resultsMore functions and asset, higher risk would require higher grossmarginAccounting variations should be taken careOther factors like geographical differences, volume, highoperating cost may effect comparison

4203/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 43/67

Profit Split Method (‘PSM’)This method aims to determine what division of total profitsindependent enterprise would expect in relation to the relevanttransactions.The profits should be split on an economically valid basis thatreflects the functions and risks of each of the parties.In order to apply this method, it is necessary to identify the totalprofit arising from the related party transactions and split that

profit between the parties according to their respectivecontributions.

JGarg Economic Advisors 4303/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 44/67

ApplicabilityIn certain very complex trading relationships involving veryinterrelated transactions, it is sometimes genuinely difficult toevaluate those transactions on a separate basis.

ApproachesThere are two approaches to this method;

▪ Total profits split, and▪

Residual profit split

4403/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 45/67

Total Profit SplitTotal profits from the controlled transactions made by all theenterprises involved in earning those profits are split betweenthose enterprises based on the relative value of the functions thateach carries out.

Residual Profit SplitTotal profit of the overall trade made by the associated enterprisesis considered.Firstly, each participant is allocated sufficient profit to provide it

with a basic return appropriate to the functions carried out.Secondly, any profit (or loss) left after the allocation of basicreturns would be split as appropriate between the parties – basedon an analysis of how this residual would have been split betweenthird parties.

4503/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 46/67

Transactional Net Margin Method (‘TNMM’)The TNMM examines the net profit margin relative to anappropriate base that a tax payer realizes from an internationaltransactions vis-à-vis comparable uncontrolled transactions.Thus, the TNMM operates in a manner similar to the cost plus andresale price methods.The TNMM is based on the economic theory that returns earned byan enterprise operating under similar conditions, in the same

market and industry, tend to become more equal after some time.

JGarg Economic Advisors 4603/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 47/67

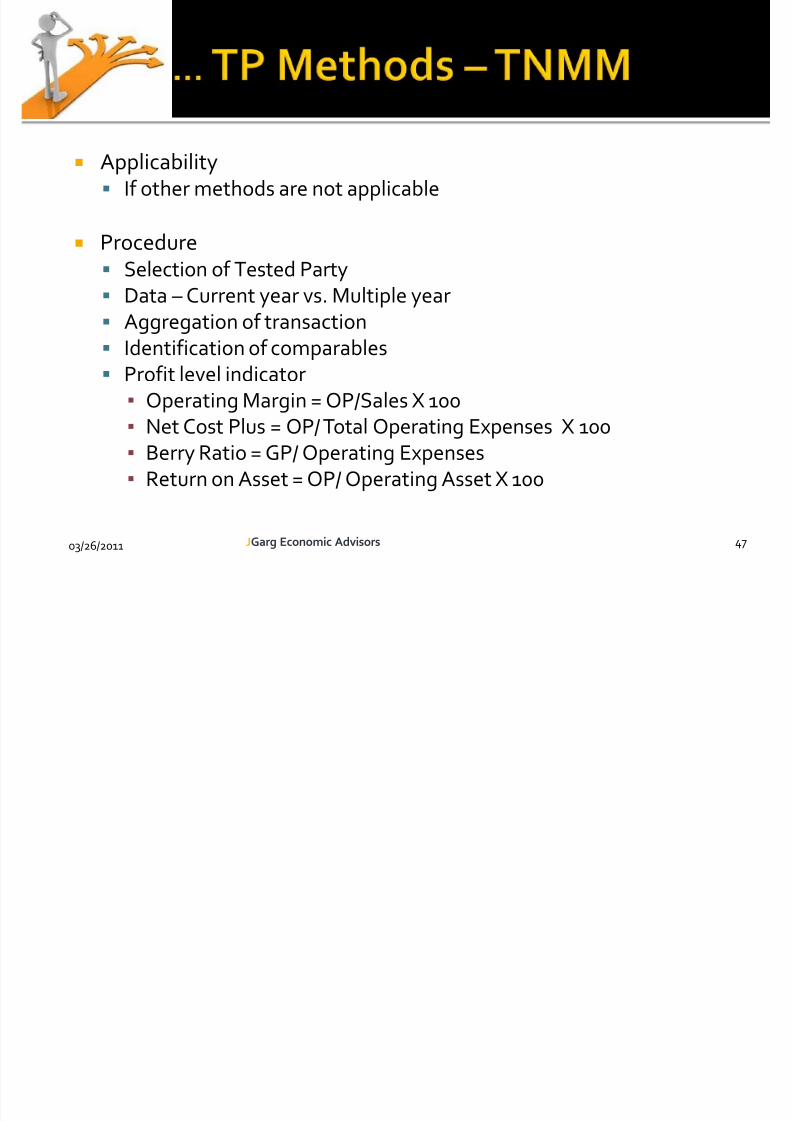

ApplicabilityIf other methods are not applicable

Procedure

Selection of Tested PartyData – Current year vs. Multiple yearAggregation of transactionIdentification of comparablesProfit level indicator

▪ Operating Margin = OP/Sales X 100▪ Net Cost Plus = OP/ Total Operating Expenses X 100▪ Berry Ratio = GP/ Operating Expenses▪ Return on Asset = OP/ Operating Asset X 100

JGarg Economic Advisors 4703/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 48/67

Transfer Pricing Documentation

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 49/67

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 50/67

Enterprise-wise documentsOwnership structure of the taxpayerProfile of the Group

Name of Associated Enterprises, address,, legal status, country of tax residence, ownership linkage and businessBusiness of the taxpayer, description of industry

03/26/2011 50JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 51/67

Transaction-specific documentsDescription of transactionFunctional Asset & Risk Analysis

Industry / market condition, forecasts/ budget, financial estimatesUncontrolled transactions and comparability analysis

03/26/2011 51JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 52/67

Computation – related documentsMost appropriate methodComputation of arm’s length price

Assumptions, policies and price negotiationTransfer pricing adjustment

03/26/2011 52JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 53/67

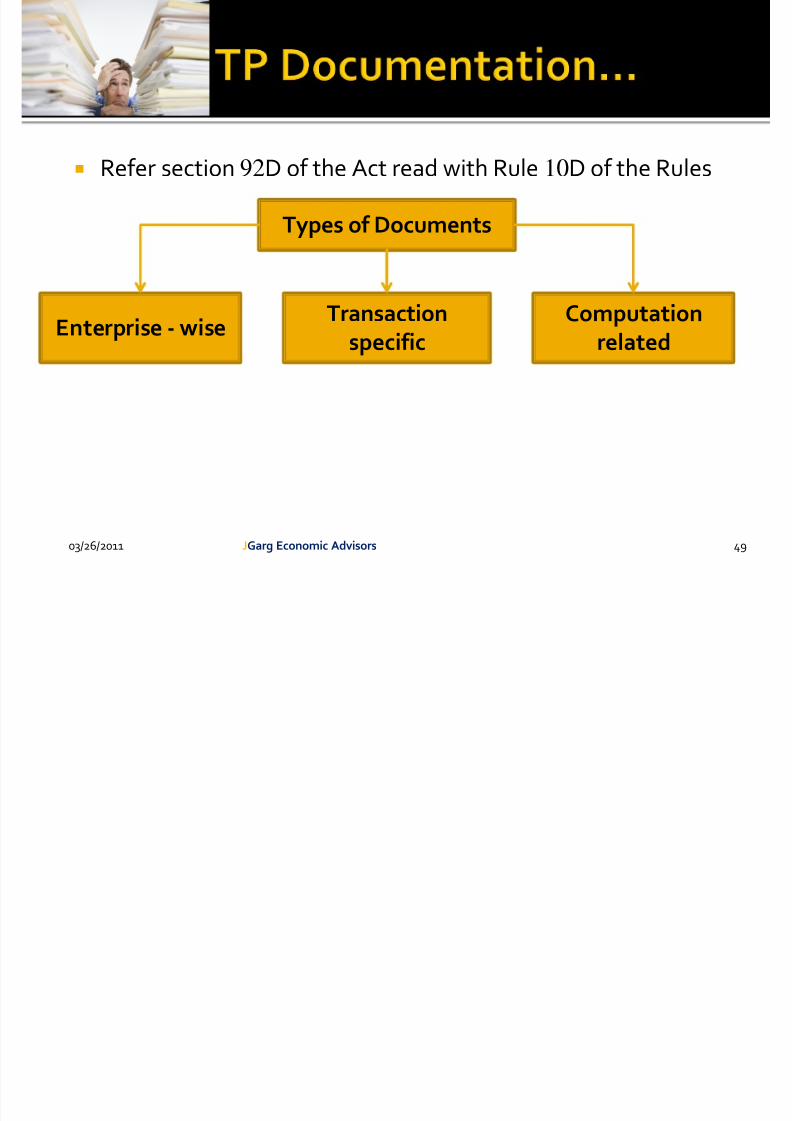

Section 92 D of the Act read with Rule 10E of the RulesDocumentation requirement not applicable if value of international transaction does not exceeds one crore rupees

▪ Practically the above provision is ineffective

Should be prepared on contemporaneous basisShould be kept and maintained for 8 years from the end of therelevant assessment yearNo fresh documentation required for continuing transactionsunless there is some significant change which can have impact onpricing

03/26/2011 53JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 54/67

Sufficiency

Reasonableness

Accuracy

Contemporaneous

Regulation

JGarg Economic Advisors 5403/26/2011

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 55/67

Handle With Care

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 56/67

Handle with careLoss making AssesseePayment for inter-company management charges

Intangibles

03/26/2011 56JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 57/67

Loss Making AssesseeStart-up lossesLosses due to new or excess capacityLosses due to marketing strategyLess than normal salesAbnormal circumstancesOther reasons

03/26/2011 57JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 58/67

Management Charges

Facts of the CaseUS based international group is having subsidiaries in all the majoreconomiesIs having regional head offices in Singapore, Germany, USIn Asia Pacific region, the group is having subsidiaries in India,China, Sri Lanka, Australia & JapanSubsidiary company in India receives invoice for management feesof USD 100,000

03/26/2011 58JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 59/67

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 60/67

Questions that require answer:Have intra-group services been provided?Would an independent company pay for the services?

Are the activities shareholder activities?What is the arm’s length price of a service?

03/26/2011 60JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 61/67

General management charges includes:Charges for use of brand nameSalary of regional CEO, Director Operations and there teamCharge back policy – 2% of Sales

Market support fee includes:Salary of regional Marketing Director, sales co-ordination staff,marketing material etc.Charge back policy – 2% of Sales

03/26/2011 61JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 62/67

IT charges includes:Charges for use of common server, email account, softwares,co-ordination team etc.Charge back policy – Allocation based on number of email ids

plus mark-upAccounting and Tax support charges includes:

Salary of regional CFO, Tax head and there teamCharge back policy – Allocation based on sales plus mark-up

03/26/2011 62JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 63/67

Intangibles

03/26/2011 63JGarg Economic Advisors

Identify the IP

Define Ownership

Find value/ price

Document it

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 64/67

Types of Intangibles AssetsManufacturing Intangibles – technical know howMarketing Intangibles – trade mark, trade name, customer list etc.

OwnershipLegalEconomic

ValuationCost Approach

Market ApproachIncome Approach

03/26/2011 64JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 65/67

Points to rememberBe sure on who is doing what, why and for whomWhether an independent party would have paid for these

services/ intangibles or notDocument, Document, Document

03/26/2011 65JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 66/67

03/26/2011 66JGarg Economic Advisors

8/7/2019 TP March 26

http://slidepdf.com/reader/full/tp-march-26 67/67

CA. Gaurav Garg

JGarg Economic Adviso

Email: [email protected]: +91 9899994934

www.jgarg.com