towards a retail development strategyarchitektura.um.warszawa.pl/sites/default/files/files/grow...

TRANSCRIPT

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

13 December 2017, Targowa Creative Center

Content

Description, organisers and addressees of the workshop

Issues discussed during the first meeting

Presentations by representatives of Warsaw – city plans in a close-up

Presentations by the Urban Land Institute Poland – proven models from abroad

A discussion between investors, developers and tenants – business needs enabling retail in Warsaw to develop not only in shopping malls and the outskirts but also in the centre, along the main streets

Summary – conclusions and proposals of workshop participants

Grow with Warsaw – what’s next

Page

2

3

4

6

7

16

17

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

2

1. Description, organisers and addressees of the workshop

Grow with Warsaw is a series of workshop meetings for real estate investors. The goal is to present Warsaw’s spatial policy and to develop, through open exchange with the key players in the real estate sector, proposals of systemic solutions to serve as guidance for the Study of conditions and directions of spatial development for the City of Warsaw, a document regulating the city’s spatial policy.

Grow with Warsaw is organised by: the Architecture & Spatial Planning Department and the Economic Development Department of the City of Warsaw. The project partner is the Urban Land Institute Poland, responsible for the preparation of the content and organisation of the workshop and also for moderating the discussions.

“We launched a series of workshop meetings for the industry under the title Grow with Warsaw, during which we discuss the current and future spatial policy of the city and the needs of the companies which not only would like to invest in Warsaw but also are able to create resident-friendly spaces to become the city’s showcase,” said Michał Olszewski, Deputy Mayor of Warsaw. “We would like to use the experience and ideas of investors and to develop recommendations and systemic solutions for the city’s retail strategy.

Representatives of the authorities of Warsaw, Marlena Happach, Director of the Architecture & Spatial Planning Department and Katarzyna Włodek-Makos, Director of the Economic Development Department (see photo above), invited to discussions management board members of developer companies constructing retail establishments and areas and counselling companies.

The workshop is not limited to presentations and exchanging ideas. After each meeting a report is created and published on the dedicated website www.architektura.um.warszawa.pl/content/grow-warsaw. Each meeting will create an impulse for the City’s authorities to take specific action. Conclusions from the meetings will also be used for creating Warsaw’s spatial policy. The series of workshops will be concluded with the visit of Grow with Warsaw’s special guest, Professor Greg Clark, Senior Fellow, Urban Land Institute Europe, who carries out studies on cooperation between cities, investors and residents. He has provided counselling for the United Kingdom, Ireland, Canada, China, India, Columbia, South Africa, New Zealand, Italy, Slovakia, Lithuania and Sri Lanka.

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

3

2. What was the subject matter of the first workshop?

The meeting Grow with Warsaw – Towards a Retail Development Strategy was held on 13 December 2017 in the Targowa Creativity Centre in Warsaw. The city organised it to be able to draw from the knowledge of companies which invest in retail units and areas and hire them not only to shops but also create space for services and recreation.

“This workshop is an unprecedented event. It integrates the good practices used by world metropolises with the strategy of Warsaw’s authorities. It is worth using the experience of other cities and investors. I do not recall an industry meeting with such importance and valuable content,” emphasised John Banka, President of Urban Land Institute Poland.

What were the issues discussed by experts during the first workshop in the series? The topics were as follows:

• What should a retail development strategy include from the point of view of investors?

• How to revive the heart of the city with retail and catering outlets by combining them with recreation and culture?

• Which places in the city are the most attractive for investors and tenants from the retail sector?

• Shopping streets versus malls – why does retail flourish on the outskirts and not in the city centre?

• Urban transport and retail projects – are large parking lots necessary to attract customers?

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

4

3. Presentations by representatives of Warsaw

Piotr Sawicki, Deputy Director of the Architecture & Spatial Planning Department of the City of Warsaw (see photo above) made a presentation during the workshop with the title “From the new Strategy to the new Study – how to incorporate the real estate market in city planning?”

“We are interested in the problems you are facing on the real estate market, the obstacles to your investing in Warsaw. We also hope that you will share with us your ideas for good solutions for the city, which will make shopping streets lively and attractive for passers-by, like in other capital cities. We are looking for ideas not only for the Praga District, where this meeting is held, where we are investing in development and revitalisation and where we wish to create a district of innovation. We are just a few hundred metres from the Google campus, one of six such places in the world. We are looking for ideas for retail in the city. It is impossible to create a good retail development plan without the input from those active on this market,” Piotr Sawicki stated during the workshop.

He emphasised that today retail defines lifestyle, as it is not only about buying and selling. This is a way to spend time in the city.

“For this reason we would like to move retail back to the city centre, which it left in the 1990s and has since been located in the outskirts, mainly in hypermarkets,” Piotr Sawicki emphasised. “Today we would like to locate retail in department stores, shopping streets and public spaces associated with culture and entertainment. We are thinking about turning some streets into footpaths, which is a solution successfully applied in Vienna. Market halls, markets and local retail centres are all needed in various parts of the city.

Deputy Director of the Architecture & Spatial Planning Department of the City of Warsaw pointed out that this is about places that can be reached by foot. “Trade, restaurants and cafés and culture – all this is to be within reach, at the same time creating high-quality public space which encourages people to stay in a given place,” Piotr Sawicki explained.

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

5

Grzegorz Okoński, Director of the Housing Policy Department of the City of Warsaw (see photo below) spoke about the policy for renting city-owned real-estate units.

“The central areas of Warsaw cannot be limited to offices and places which are closed after 5-6 p.m. A mix of residential and retail use is needed,” Grzegorz Okoński emphasised.

He said that the city’s goal is to increase the number of Local Action Hubs (Miejsce Aktywnosci Lokalnej, MAL), i.a. through utilising local social infrastructure, the Warsaw Local Centres (Warszawskie Centra Lokalne, WCL) and other public and semi-public spaces to function as meeting points for neighbours and for various activities.

“It is crucial for us to combine the residential and utilitarian uses, in particular to create the so-called active ground floors, which revive the streets and create space for everyday meetings, such as cafés, restaurants, pubs and retail and services outlets,” Director Okoński explained.

He also pointed out to the need to support the development of commercial services for residents (innovative services such as car or electric scooters rental, multiple services).

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

6

4. Presentation by the Urban Land Institute Poland (ULI Poland)

John Banka, President of the Urban Land Institute Poland (see photo above), talked about solutions applied by other countries to combine retail with recreation and culture. He demonstrated how local government bodies in other countries, in such cities as Vienna, Barcelona, Toronto and Miami, dealt with problems currently faced by Warsaw.

“Today investors and developers are changing the city. They are aware that currently retail is not just about sales but about the experience. This should be taken into account in retail use planning in cities,” John Banka pointed out.

He mentioned Vienna as one of the examples of cities which have managed to create model retail streets by cooperating with investors. “This is where the beautiful historic Old Town is combined with new buildings and new functions have been introduced to attract pedestrians,” the President of the Urban Land Institute Poland explained.

Also in Barcelona a combination of projects by private investors and local government bodies has been highly beneficial for shopping streets. The city even created a digital platform to show the combined range. “Such integrated actions of the public and private sector make it possible for the retail product and service range to remain competitive. However, this was the public sector that developed the plan for increasing the competitiveness of local shops near shopping malls to promote digitalisation and access to new technologies and to encourage closer contacts between retailers and shopping malls,” John Banka pointed out.

A similar type of cooperation between the business sector and city authorities can be observed in Toronto, where the board of entrepreneurs cooperates with the city. “This body not only takes care of the cleanness and safety on shopping streets but also co-manages them when it comes to the selection of tenants and measures to attract retail customers. Why shouldn’t this work for Marszałkowska Street in Warsaw? John Banka asked.

He also provided the example of Miami, where shopping streets have gained a new life thanks to cultural initiatives. “Retail trade has been integrated with cultural institutions, and shopping streets are promoted as an alternative and an addition to large shopping malls, which are losing their appeal,” the President of the Urban Land Institute Poland stated.

In Miami 70 art galleries were created, along with several private museums, the Institute of Contemporary Art, Miami and 100 luxury boutiques. Their activities are accompanied by entertainment events – concerts, wellness activities and cultural events.

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

7

5. A discussion about retail in Warsaw – what is it like today, what should be quickly changed?

The moderator of the discussion was Grażyna Błaszczak, editor of “Nieruchomości z górnej półki”. The debate was accompanied by slides prepared especially for the meeting by the Knowledge Partners of the workshop. Advisory agencies provided the results of their research on retail and communication in Warsaw.

I. WHICH BRANDS LEFT WARSAW’S SHOPPING STREETS? WHY DO THEY PREFER SHOPPING MALLS OVER INNER-CITY LOCATIONS?

The map showing the rotation of retail chains as tenants of units along the main shopping streets in Warsaw (Chmielna, Nowy Świat, Mokotowska, Trzech Krzyży Square) was prepared by experts from the Colliers International agency. The map demonstrates that the top brands are withdrawing from first-rate locations along shopping streets to move to shopping malls and department stores.

What kind of tenants are leaving shopping streets? “These are mainly fashion and health & beauty brands and jeweller’s stores. They prefer shopping malls which are able to offer a superior environment. Some brands have moved to Złote Tarasy because the mall has more customers. It also provides a wider selection of stores, parking space and additional services in one place,” explained Małgorzata Kobziakowska, Associate Director, Retail Agency Colliers International.

She emphasised that companies paid comparable rental charges for units along top shopping streets and in the best shopping malls, but turnover was by 30-40% higher in shopping malls.

Karel Zeman, Head of Investment Operations Poland at CBRE Global Investors also discussed why shopping streets were abandoned by top brands to be replaced with lower-end health & beauty stores and discount chains.

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

8

“I work in the company which owns the Centrum Department Store in Warsaw. It is no secret that H&M, which had a store at Nowy Świat Street, moved to a different location, where the rent is higher. The Douglas perfume shop did the same. Brands prefer paying higher rent if the location gives them higher turnover. This cannot be achieved with a location at Nowy Świat Street,” Karel Zeman explained. “For me Nowy Świat and Krakowskie Przedmieście are walkways, not shopping streets. Food outlets open there, not stores. These streets are filled with tourists, not shoppers. The problem with them is that they lack major transfer nodes and convenient urban transport connections, which is why turnover in stores along such streets is lower. There is no natural movement of people there. However, Marszałkowska Street is quite different because there is an underground and a tram stop, so a shopping street makes sense there.

The expert of CBRE Global Investors asked during the workshop why between the Centrum underground station and the Central Station there is a rather unappealing park while there should be a shopping street. “It would certainly have tenants because of the natural movement of people, so retailers could count on considerable turnover,” he assured.

Patrick Delcol, President of BNP Paribas Real Estate, President of the Polish Council of Shopping Centres, said during the workshop that the entire area between Jana Pawła and Nowy Świat streets to Krakowskie Przedmieście and Konstytucji Square requires a uniform plan of retail revitalisation.

“Rotterdam and Lyon managed to cope with a similar challenge. I don’t see why Warsaw wouldn’t. I love Praga as a district, but Śródmieście, which is the heart of Warsaw, should be a priority for the city’s authorities. This is where the critical mass of retail should be, centred around the Palace of Culture,” emphasised the expert from BNP Paribas Real Estate.

He added that it is crucial to attract young people to the centre of Warsaw so that they would live, spend time and money there, not on the outskirts. In demographic terms, Śródmieście is continuously ageing.

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

9

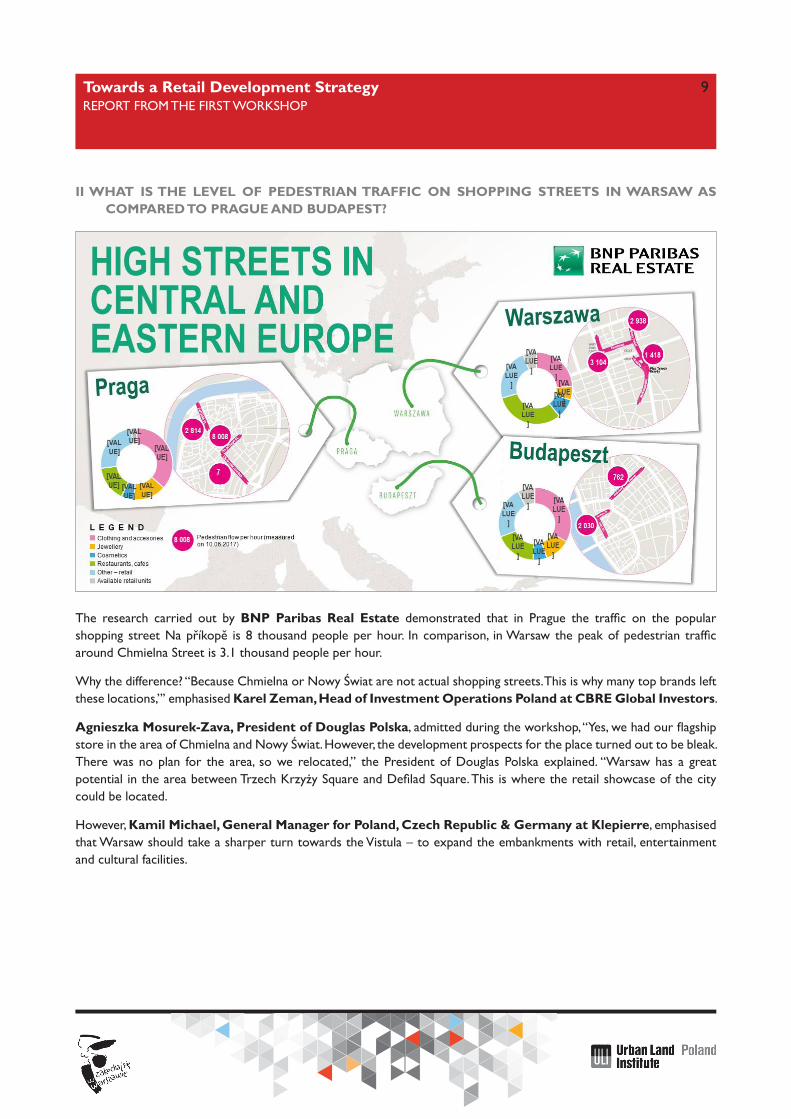

II WHAT IS THE LEVEL OF PEDESTRIAN TRAFFIC ON SHOPPING STREETS IN WARSAW AS COMPARED TO PRAGUE AND BUDAPEST?

The research carried out by BNP Paribas Real Estate demonstrated that in Prague the traffic on the popular shopping street Na příkopě is 8 thousand people per hour. In comparison, in Warsaw the peak of pedestrian traffic around Chmielna Street is 3.1 thousand people per hour.

Why the difference? “Because Chmielna or Nowy Świat are not actual shopping streets. This is why many top brands left these locations,”’ emphasised Karel Zeman, Head of Investment Operations Poland at CBRE Global Investors.

Agnieszka Mosurek-Zava, President of Douglas Polska, admitted during the workshop, “Yes, we had our flagship store in the area of Chmielna and Nowy Świat. However, the development prospects for the place turned out to be bleak. There was no plan for the area, so we relocated,” the President of Douglas Polska explained. “Warsaw has a great potential in the area between Trzech Krzyży Square and Defilad Square. This is where the retail showcase of the city could be located.

However, Kamil Michael, General Manager for Poland, Czech Republic & Germany at Klepierre, emphasised that Warsaw should take a sharper turn towards the Vistula – to expand the embankments with retail, entertainment and cultural facilities.

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

10

III. WARSAW’S MAIN PROBLEMS: THE OWNERSHIP STRUCTURE OF REAL ESTATE UNITS AND THE MANAGEMENT OF SHOPPING STREETS

What should be done to attract famous brands to main streets? Cushman & Wakefield pointed to the most urgent problems that need to be solved.

“The varied ownership structure of real estate, complicated public procurement procedures and invitations to tender for municipal real estate, unsuitable technical conditions and the lack of high-quality commercial space are the major problems faced by tenants,” explained Lucyna Śliż, Head of Retail Development Team at Cushman & Wakefield.

On the other hand, C&W agents assess that approx. 317 units along main shopping streets in Warsaw have a potential. Unfortunately, as stated by the discussion participants, there is no management strategy developed for them.

Another issue: Nowy Świat, Krakowskie Przedmieście and Konstytucji Square are predominantly used as locations for restaurants and cafés. From the point of view of clothing brands, this is a disadvantage. The range should be diversified. Further streets with unused potential are Jana Pawła II Avenue, Bankowy Square and Marszałkowska Street, from Jerozolimskie Avenue to Konstytucji Square.

“Warsaw lacks a commercial approach to shopping streets, to managing them in such a way that they would be able

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

11

to compete with shopping malls,” Jarosław Lipiński, Letting and Development Director at TK Development said during the workshop. “There are also other, seemingly insignificant issues that need improvement, such as the condition of pavements, which deters the main customer group of stores along shopping streets, i.e. women wearing high heels. It should also be specified what windows on shopping streets should look like to create a consistent whole. In Vienna, for instance, the external appearance of stores is described to the minutest detail. In order for all this to be possible, a continuous exchange between the city and the real estate sector is needed. We can make evaluations and say, for instance: “this solution is wrong, it’s not going to work, because the needs of retail companies are different,” Jarosław Lipiński explained.

The expert said that many cities abroad do not deal with shopping streets management on their own but hire professional companies. This also applies to places where city and private units are located side by side.

“Professionals determine the policy for these streets as they are in continuous contact with store tenants, know what they need and how to attract customers,” Jarosław Lipiński emphasised.

What other expectations do investors and tenants have? Krzysztof Cybruch, organiser of the Breakfast Market, the Fish Market and of the retail activities at the Gwardia Hall , pointed out that the market and fair initiatives are not supported by the city authorities.

“It is very hard to organise such projects in Warsaw because of the ever-present obstacles, such as no infrastructure on a given square, the restorer’s determining rental conditions with orders and restrictions, the necessity to arrange security guards, etc.,” Krzysztof Cybruch explained. “Why is there no holiday market in Warsaw, like on other European cities? Because the city is not interested in projects which revive the streets. Its role is limited to renting the area and collecting charges for occupying the square and infrastructure. However, such fairs are not only a commercial initiative.

Lucyna Śliż of Cushman & Wakefield drew our attention to other problems faced by tenants: finding and renting a unit in the city takes up to a year and a half, and the maximum rental time is three years.

“The high expenditures will not be compensated in three years. Agreements with the city are too limited in time. In shopping malls agreements are long-term and tenants are able to predict what the nearest surroundings will look like. This is the reason for some brands to move out of shopping streets,” the C&W expert said.

Laurence Paquet, General Manager at Immochan Polska also contributed to the discussion.

“I came to Warsaw in 2013 and I was surprised that there was no vision for shopping streets in this city, and that brands located in various places were not in any way related but rather scattered. Customers must visit many locations, many streets and make a lot of effort to do shopping, to find quality brands, which have their stores in the middle of nowhere. There is no management, no common concept, so none of the streets functions as it should. This is why brands and customers choose shopping malls,” Laurence Paquet stated.

The workshop participants also considered the issue which requires statutory solutions, i.e. the problems with the legal status of real estate.

“The Reprivatisation Act could substantially improve the situation. I remember when in the Czech Prague in early 1990s my office was so busy that the doors would not close. The owners of recovered real estate would come to me and ask what they could do with their units. In Warsaw the problem has been growing for years”, noticed Monika A. Dębska- Pastakia, President of Knight Frank in Poland. “In Prague 50% of real estate units are the property of institutions, 30% – of private owners and only 20% belong to the city . This makes it easier to create a uniform strategy for shopping streets.

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

12

Patrick Delcol, President of BNP Paribas Real Estate in Poland, pointed to another problem. “Why doesn’t the city allow investors to create large stores in the centre, limiting their size to one thousand square metres? Supermarkets are not affected by this restriction and enter the main streets, and quality brands must move away,” he stated during the discussion.

In turn, Jan Dębski, President of Unibail-Rodamco Poland (the company owning Złote Tarasy), emphasised that redeveloping the heart of the city is the best idea for retail in the centre of Warsaw.

“Defilad Square is a phenomenal place on a European scale, probably the best. You can do amazing things there. But a new plan for the area is needed to make it like Paris. A competition should be arranged to give the place new quality. Otherwise everyone will go shopping to Złote Tarasy and not to shopping streets. I’m not complaining, for me this situation is beneficial. There is even a queue of tenants for our centre. But this is not what is about,” he emphasised.

IV. MIXED-USE DEVELOPMENTS IN SHOPPING STREETS AS INVESTMENT PRODUCTS

What characteristics does a retail establishment need to have in order to attract investor interest? A clear legal status, a varied retail environment, a good pedestrian traffic flow, good public transport accessibility and a parking facility close by – CBRE’s experts explained. Other important assets include a good quality of the establishment, well-selected tenants and long-term lease agreements. Are there any such investment products in Warsaw today?

“In Warsaw, these requirements are currently met primarily by office buildings with ground floors intended for retail use,” said Wioleta Wojtczak, Associate, Head of Research at Savills. “There are no investment products with a retail focus, which is why shopping streets should be managed like shopping malls. You have to put together a good mix of tenants, develop auxiliary uses and provide customers with access to multiple services in one place – in other words, you need to have a coherent street management policy in place. But this requires a city-wide strategy.

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

13

Magdalena Frątczak, Senior Director, Head of Retail Agency at CBRE, pointed out that the so-called urban fabric should be considered an investment product. “A good building location is useless if you don’t have a good public-transport connection. So, you have to make sure it’s in place and it’s as convenient as possible. The range of retail uses is also very important. Sizes of units must vary from 20 sq. m for watchmaker’s shops to 4,000 sq. m for major tenants like Zara. You won’t find it in Warsaw today, though” said CBRE’s expert. The solution to regenerate shopping streets, she claims, is the following: “First things first – let’s develop strategies for individual sections of the streets and then manage them. We should start from the area near the Palace of Culture and Science. It’s also worth extending Chmielna Street to the Central Railway Station. These solutions have worked well in other cities, so why wouldn’t they in Warsaw? However, two years ago our client asked us for a unit in Warsaw. Requirements? A prestigious location, not in a shopping mall, 700 sq. m, in a good spot with a large, fine shop window facing the street. We still haven’t found it. Actually, at this point we can only dream of such a location in Warsaw, as it is non-existent,” Magdalena Frątczak deplored.

V. PUBLIC TRANSPORT ACCESSIBILITY TO SHOPPING CENTRES

What is the fastest way to get to a shopping mall if you don’t have a car? According to JLL’s data, it takes an average of 20 minutes for a Warsaw resident to get to the nearest fashion retail centre by public transportation.

“The longest journey times are faced by residents of the Wesoła (49 minutes), Rembertów (36 minutes) and Wilanów (33 minutes) districts. The shortest journey times are available from the Praga-Północ (13 minutes) and Śródmieście (14 minutes) districts,” explained Jan Jakub Zombirt, Associate Director, Strategic Consulting at JLL.

According to JLL’s research, Galeria Wileńska has the best transport connection of all shopping centres in Warsaw. The largest journey time differences between private cars and public transport are for the following establishments: Ferio Wawer, Designers Outlet Piaseczno and Atrium Promenada.

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

14

VI. RETAIL AND TRANSPORT – HOW MANY PARKING SPACES ARE AVAILABLE IN SHOPPING CENTRES AND DO WE NEED THIS MANY?

Workshop participants also looked on Savills’s proposal: could shopping centres (e.g. Galeria Mokotów, Blue City, Atrium Reduta, Jupiter) “share” parking spaces with the neighbouring office buildings on weekends, when these centres see the largest numbers of visitors?

“It’s also worth considering whether it’s necessary to build so many parking spaces in retail establishments which can be reached by most means of public transport available in Warsaw,” said Wioleta Wojtczak, Associate, Head of Research at Savills.

Meanwhile, new retail projects are still planning to build thousands of parking spaces for cars. Are they really needed?

“At Złote Tarasy, the lowest storeys, car parks at Floors -3 and -4, are empty on weekdays. They’re at full capacity only on holidays,” said Jan Dębski, President of Unibail-Rodamco Poland.

Karel Zeman from CBRE Global Investors offered a different perspective, arguing for more pedestrian space in the heart of the Capital City. “Public parking spaces in Warsaw are too cheap. It looks as if the entire city was designed for cars. The streets in the centre are too wide and what’s on Defilad Sq., the large square in the middle of Warsaw? A large car park. It’s unheard of,” says Karel Zeman, providing a telling comparison with the Czech Prague.

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

15

VII. E-MOBILITY IN WARSAW – CHALLENGES

Experts from Knight Frank thought it was essential for Warsaw to pursue innovations in electricity storage and car propulsion technologies. Also, retail projects would benefit from an integrated network infrastructure across transport, power supply and ICT.

“The City’s strategy towards 2030 must incorporate these elements. The central question is, then: will Warsaw’s authorities include new transport technologies in this strategic document?” asked Monika A. Dębska - Pastakia, President, Knight Frank Poland.

Łukasz Ciesielski, Head of Development at Strabag AG Real Estate Development, noted one other problem related to public transport in Warsaw: “I live just a few stops from Galeria Mokotów, but I’ve never gone there by tram. Why? Because the location of interchanges in Warsaw is a disaster. Pedestrians have to walk hundreds of metres to get to a bus stop from a tram. Is there any reason why these stops shouldn’t be located close to each other to facilitate changing between modes and thus render cars a less affordable option? It’s worth considering this change”, the expert recommended.

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

16

6. Summary

During the debate, as well as in questionnaires completed during workshops, investors and tenants stressed the need, among other things, to direct the heavy car traffic away from the very centre of Warsaw (Marszałkowska Street, Aleje Jerozolimskie Ave.).

They also suggested narrowing the main streets and restricting car traffic to create more space for pedestrians and build new pedestrian precincts – e.g. along Aleje Jerozolimskie Ave. towards the Central Railway Station. To support this, they mentioned examples of similar solutions from such cities as Copenhagen, Stockholm, Berlin and Vienna.

The debaters emphasised that it was necessary to start managing shopping streets based on practices similar to those applied in shopping malls. In shopping centres, where certain management measures are in place, tenants will know what to expect from the area adjoining their stores. Street retail outlets, however, might face a high risk of unwanted changes.

Workshop participants suggested that tenants of street outlets should be provided with the same benefits that are offered in shopping malls – for instance, temporary rent waivers for major investors.

Another conclusion was that lease agreements must be on a multi-year basis rather than on a three-year basis. The current legal status of city-owned properties essentially prevents any investment in them. From the investor’s point of view, even a ten-year tenancy is too short.

Also, the units available are too small. Would any respectable business lease a 30-50 sq. m unit? So, development plans and strategies should not impose surface area limitations – such as the 1,000-sq. m limit on Defilad Sq.

Moreover, the heritage conservation officer could be less strict with regard to old-building renovations. In many cities abroad, protection concerns only building façades and window shops may be wide.

Finally, a reprivatisation law should be passed to help resolve property ownership issues.

Towards a Retail Development Strategy REPORT FROM THE FIRST WORKSHOP

17

7. Discussion and questionnaire proposals

• A new industry body comprising city and business representatives should be set up to coordinate the joint management of shopping streets, as well as to offer advice for the city in its planning decisions related to retail development in Warsaw.

• A street should be singled out for a pilot project in which the street would be managed jointly in the same fashion as a shopping centre.

• There is an urgent need for developing a spatial planning policy and adopting/revising local development plans. Among other issues, the city authorities should define the areas in which large-format retail is allowed.

• The city should make the strategic decision on whether to continue owning so many commercial and retail units on the main streets.

• Also, shopping-street safety should be taken care of – march-throughs, protests, etc. mean trouble for tenants.

• Finally, the city should come up with a public-private partnership proposal for marketplaces.

8. What’s next?

Why is the city seeking opinions from the industry and how is it planning to act on the suggestions and recommendations of real-property experts?

“The city needs insights from market insiders, as in 2018 we will start working on a new core strategy document. Addressing retail issues is one of our priorities, since they are very important for the residents of Warsaw and for the development of the heart of Warsaw,” concluded Deputy Mayor of Warsaw Michał Olszewski.

Starting February 2018, Grow with Warsaw will take on new subjects. There are five more meetings in the pipeline. Each meeting will deal with a different sector of the property market.

Coming up in February 2018 is a discussion on the challenges involved in regenerating various parts of the Capital City and the ideas for their regeneration. Next meetings will address the development of mixed-use property, public spaces and green infrastructure in Warsaw, the development of the residential market and the economic development of Warsaw.

KNOWLEDGE PARTNERS ARE: