total issuance amount: rmb 16,795,364,059

TRANSCRIPT

i

Total Issuance Amount: RMB 16,795,364,059.35

Jianyuan 2018-21 Residential Mortgage-Backed Securities

China Construction Bank Corporation

(a joint-stock company established in accordance with PRC laws)

Originator/Servicer

CCB Trust Co., Ltd.

(a limited liability company established in accordance with PRC laws)

Trustee/Issuer

Tranche Rating

CBR/CCXI

Issuance Amount

(RMB) Percentage

Coupon

Rate

Repayment

Method

Expected

Maturity

Date*

Legal

Maturity

Date

Class A-1

Notes AAAsf/AAAsf 3,000,000,000.00 17.86% Fixed rate

Scheduled

Amortization 26/12/2020 26/11/2041

Class A-2

Notes AAAsf/AAAsf 3,800,000,000.00 22.63% Fixed rate

Scheduled

Amortization 26/01/2022 26/11/2041

Class A-3

Notes AAAsf/AAAsf 7,820,000,000.00 46.56%

Floating

rate Pass-through 26/08/2024 26/11/2041

Subordinated

Notes - 2,175,364,059.35 12.95% - - 26/11/2038 26/11/2041

Total 16,795,364,059.35 100.00%

*The given Expected Maturity Date is under the assumption that CPR = 10%/year. If CPR = 0%/year and there is

no default, the Expected Maturity Date of Class A-1 Notes, Class A-2 Notes, Class A-3 Notes and Subordinated

Notes are 26/12/2020, 26/04/2023, 26/04/2029 and 26/11/2038, respectively.

The Securities are issued by the Issuer on the China Interbank Bond Market (“CIBM”) through a book

building process. The dedicated book building room is located at 7F Financial Street Center, 9A Financial

Street, Xicheng District, Beijing, People’s Republic of China. The Originator will hold all the

Subordinated Notes, accounting for 12.95% of the issuance size. The holding term is no shorter than the

term of the Subordinated Notes.

Investing in these Securities may involve various risks. Please refer to the section called “RISK

DISCLOSURE TO INVESTORS” in this Offering Circular for more information.

Interest on Securities shall accrue starting on the date 13/12/2018. The Issuer shall pay the interest and

ii

principal on each Payment Date which shall accrue on the beginning balance of the Outstanding Principal

Amount of each of the Class A-1 Notes, Class A-2 Notes and the Class A-3 Notes in the period. The first

Payment Date is 26/02/2019 (if such date is not a Working Day, the Payment Date shall be the first

“Working Day” after that date). More information concerning the Interest Rate of the Securities is

included in the Fifth Chapter of this Offering Circular titled “Summary of the Securities”.

China Central Depository and Clearing Co., Ltd. (“CCDC”) will credit the Securities to the custody

accounts of the Noteholders no later than the Working Day following the Trust Effective Date. After the

Issuer completes the establishment of a Debtor-creditor relationship and after completing registration,

the Securities can then be traded on the CIBM.

Abstracts of opinions of the intermediary agencies in this Offering Circular, including the rating reports,

legal opinion, accounting opinion and tax opinion etc., have been verified by relevant intermediary

agencies, and the Issuer shall ensure the authenticity and accuracy of its references.

China Bond Rating Co., Ltd. and China Chengxin International Credit Rating Co., Ltd. offer rating

services for the Securities. An abstract of the rating reports for Class A Notes is included in Chapter Six

of this Offering Circular titled “Opinions of the Intermediary Agencies”.

Investors purchasing the Securities should carefully read this Offering Circular and relevant disclosure

documents and make independent investment judgments. The approval of this issuance by the People’s

Bank of China, China Banking and Insurance Regulatory Commission and other government agencies,

does not suggest any opinion over the investment value of the Securities, nor does it show any judgment

over the investment risks of the Securities.

The disclosure date of this Offering Circular is 3/12/2018.

China Merchants Securities Co., Ltd.

Lead Underwriter/Book Runner

China International Capital Corporation Limited

Joint Lead Underwriter

HSBC Bank (China) Company Limited

Joint Lead Underwriter

Standard Chartered Bank (China) Limited

Joint Lead Underwriter

iii

Contents

IMPORTANT NOTICE .............................................................................................. 1

PARTICIPATING INSTITUTIONS .......................................................................... 2

A. Originator/Servicer: China Construction Bank Corporation (“CCB”) .................... 2

B. Trustee/Issuer: CCB Trust Co., Ltd. (“CCB Trust”) ................................................... 2

C. Financial Advisor: CCB Principal Capital Management Co., Ltd. (“CCBPCM”) .. 2

D. Fund Custodian: Industrial Commercial Bank of China Ltd. Beijing Branch

(“ICBC Beijing”) ................................................................................................................. 3

E. Securities Custodian/Paying Agent: China Central Depository and Clearing Co.,

Ltd. (“CCDC”) ..................................................................................................................... 3

F. Lead Underwriter/Book Runner: China Merchants Securities Co., Ltd. (“CMS”).. 3

G. Joint Lead Underwriters: .............................................................................................. 4

H. Rating Agencies: ............................................................................................................. 5

I. Auditor/Tax Advisor: Ernst & Yong Hua Ming LLP. (“EY”) ...................................... 6

J. Transaction Counsel: Zhong Lun Law Firm (“Zhong Lun”)................................... 6

Chapter I RISK DISCLOSURE AND STATEMENT OF INFORMATION

CHANGES 7

A. Risk Disclosure for Investors ......................................................................................... 7

B. Statement of Information Changes ............................................................................. 13

Chapter II TRANSACTION BASICS .................................................................. 18

A. Transaction Parties Diagram ....................................................................................... 18

B. Overview of the Participating Institutions ................................................................. 19

C. Abstract of Transaction Documents and Main Rights and Obligations of the Parties

iv

30

D. Priority of Payments ..................................................................................................... 46

E. Credit Enhancement Measures ................................................................................... 52

F. Organizational Structure and Rights of Meetings of the Noteholders ..................... 54

G. Cash Flow Table ........................................................................................................... 57

H. Taxes and Fees, Payment and Priority Required for Trust Property Cash Flow ... 69

Chapter III GENERAL INFORMATION OF THE UNDERLYING ASSETS

73

A. The Number of Loan Contracts and the Features of Principal Amounts ............ 73

B. Features of Loan Term .............................................................................................. 73

C. Features of Interest Rates ......................................................................................... 74

D. Features of Mortgaged Assets ................................................................................... 74

E. Features of Borrowers ............................................................................................... 75

Chapter IV DISTRIBUTION INFORMATION OF THE UNDERLYING

ASSETS 76

A. Distribution Information of the Loans ....................................................................... 76

B. Distribution Information of the Borrowers ................................................................ 81

C. Distribution Information of the Mortgaged Assets .................................................... 86

Chapter V GENERAL INFORMATION OF THE SECURITIES .................... 96

A. Fees................................................................................................................................. 96

B. Date Information .......................................................................................................... 98

C. Summary of the Securities ......................................................................................... 100

D. Risk Retention Information ........................................................................................ 110

v

Chapter VI OPINION OF THE INTERMEDIARY AGENCIES .................. 111

A. Abstract of the Due Diligence and Legal Opinion .................................................... 111

B. Summary of the Transaction and Accounting Treatment Opinion ........................ 121

C. Summary of Credit Rating Reports .......................................................................... 122

Chapter VII FOLLOW-UP ARRANGEMENTS FOR SECURITIES ............ 134

A. Arrangement of Follow-up Ratings ........................................................................... 134

B. Arrangements of Information Disclosure for Securities.......................................... 135

C. Rights of Trust Beneficiaries ...................................................................................... 137

D. Method for Accessing Information About the Underlying Assets .......................... 137

1

IMPORTANT NOTICE

The issuance of Class A-1 Notes, Class A-2 Notes, Class A-3 Notes and Subordinated Notes (The “Issue”)

has been approved by the People’s Bank of China under the Decision of the People’s Bank of China to

Grant Administrative Permission (ref. Yin Shi Chang Xu Zhun Yu Zi 2018 No.216) and filed under the

Filing Notice of the China Banking and Insurance Regulatory Commission’s Innovation Department on

Jianyuan 2018-21 Residential Mortgage Backed Securitization with the China Banking and Insurance

Regulatory Commission.

The Issuer guarantees that there are no false records, misleading statements or material omissions in this

Offering Circular by the disclosure date.

The Securities in this Issue only represents corresponding shares of the “Trust Beneficiary Interest” of

the special purpose trust and do not constitute liabilities of the Originator, the Trustee or any other

organization towards the investors. The recourse of the Securities’ obligations in this Issue is limited to

the Trust Property. The Originator assumes no obligation or liability for any losses that may arise

throughout the course of the credit asset securitization other than the duties it may be required to assume

as the Settlor under the Trust Agreement and as the Servicer under the Servicing Agreement. The Issuer’s

obligation to investors for payment of the principal of and benefits from the Securities is limited to the

Trust Property. The Servicer assumes no obligation or liability for any losses that may arise throughout

the course of the credit asset securitization other than the duties required by the Servicing Agreement.

For offshore investors participating in the subscription of the securities through the “Northbound Trading”

channel of "Bond Connect", the specific arrangements concerning registration, custody, settlement,

remittance and conversion of funds will follow the "Interim Measures for the Connection and

Cooperation between the Mainland and the Hong Kong Bond Market" issued by the People's Bank of

China and other relevant laws and regulations. China Central Depository & Clearing Co., Ltd.(“CCDC”)

provides services concerning registration, custody and remittance for the offering of securities. Hong

Kong Monetary Authority- Central Money markets Unit (HKMA-CMU) provides the corresponding

services for offshore investors.

Investors purchasing the Asset Backed Securities should carefully read this Offering Circular and

relevant disclosure documents and make independent investment judgments. The approval of this Issue

by relevant administrations does not suggest any opinion of the investment value of the Issue, nor does

it show any judgment to the investment risks of the Issue.

2

PARTICIPATING INSTITUTIONS

A. Originator/Servicer: China Construction Bank Corporation (“CCB”)

Registered address: No. 25, Financial Street, Xicheng District, Beijing, PRC.

Legal representative: Guoli Tian

Contacts: Hongyuan Zhang, Min Li, Bo Wang, Dejian Chang, Tianya Hui, Xuefei

Chen

Phone umbers: +8610-67596282/67596283/67596333/67596340/67596307

Zip code: 100032

Website: www.ccb.com

B. Trustee/Issuer: CCB Trust Co., Ltd. (“CCB Trust”)

Registered address: No. 45 JiuShiQiao Road, Hefei City, Anhui Province, PRC.

Legal representative: Baokui Wang

Contacts: Xiaofei Yan, Xinyu Zhi, Cheng Wang

Phone number: +8610-67594377

Zip code: 100031

Website: www.ccbtrst.com.cn

C. Financial Advisor: CCB Principal Capital Management Co., Ltd. (“CCBPCM”)

Registered address: #2-232, No. 738 Guangji Road, Hongkou District, Shanghai, PRC

Legal representative: Yong Ma

Contacts: Sheng Li, Decheng Chen, Lu Shi

Phone number: +8610-58527770

Zip code: 100031

Website: www.ccbapital.cn

3

D. Fund Custodian: Industrial Commercial Bank of China Ltd. Beijing Branch (“ICBC

Beijing”)

Registered address: Block B, Tianyin Building, No. 2 Fuxingmen South Street, Xicheng

District, Beijing, PRC

Legal representative: Zhenjun Wang

Contact: Yuan Wei

Phone number: +8610-63950873

Zip code: 100045

Website: www.bj.icbc.com.cn

E. Securities Custodian/Paying Agent: China Central Depository and Clearing Co., Ltd.

(“CCDC”)

Registered address: No. 10, Financial Street, Xicheng District, Beijing, PRC

Legal representative: Ruqing Shui

Contact: Chengxiang Liu

Phone number: +8610-88170738

Zip code: 100033

Website: www.chinabond.com.cn

F. Lead Underwriter/Book Runner: China Merchants Securities Co., Ltd. (“CMS”)

Registered address: 38F-45F, Block A, Jiangsu Building, Yitian Road, Futian District,

Shenzhen, Guangdong, PRC

Legal representative: Da Huo

Contacts: David Cao, Qian Zheng, Kaiyu Yang, Qicheng Deng, Yijia Ren

Phone number: +8610-60840885

Zip code: 100033

4

Website: www.newone.com.cn

G. Joint Lead Underwriters:

1. China International Capital Corporation Limited(“CICC”)

Registered address: 27th and 28th Floor, China World Office 2, No.1 Jianguomenwai

Avenue, Chaoyang District, Beijing

Legal representative: Mingjian, Bi

Contacts: Zhouqi Jia, Yingxue Li, Xinyang Tian, Ji Li, Yue Fei

Phone number: +8610-65051166

Zip code: 100004

Website: www.cicc.com

2. HSBC Bank (China) Company Limited (“HSBC China”)

Registered address: Unit 01-05, 07-09 of 20/F, Unit 01-03 of 22/F, 23/F, Unit 01- 04, 12-16 of

25/F, Unit 01-12, 15, 16 of 26/F, Unit 01-11 of 27/F, Unit 01-09, 12-16

of28/F, 29/F, Unit 04-08 of 30/F, Unit 01, 03-16 of 31/F, 32/F, Unit 01-03,

15, 16 of 33/F,35/F, Unit 01-02, 04-16 of 36/F, 37/F and Unit 01-08, 10-

16 of 38/F, HSBC Building, Shanghai IFC, 8 Century Avenue, China

(Shanghai) Pilot Free Trade Zone

Legal representative: Yijian Liao

Contacts: Chao Ye, Zhao Yang, Jiawen Zhang, Zheyi Zhu

Phone number: +8621-38881248/3888 2847

Zip code: 200120

Website: www.hsbc.com.cn

3. Standard Chartered Bank (China) Limited (“SCB China”)

Registered address: 16F (actually 15F), 17F/Room 1, 2, 4 (actually 16F/Room 1, 2, 4),

18F/Room 1, 2, 3 (actually 17F/Room 1, 2, 3), 19F (actually 18F),

22F/Room1, 2 (actually 21F/Room 1, 2), 23F/Room 1 (actually

22F/Room 1), 25F/Room 1 (actually 23F/Room 1), and 28F (actually

5

26F), Standard Chartered Tower, 201 Century Blvd., Pu Dong New Area,

Shanghai, People’s Republic of China

Legal representative: Zhang Xiaolei (张晓蕾)

Contacts: LAI, Haisu (来海粟), SI, Yiqing (斯逸卿), LIANG, Jiamin (梁嘉敏)

Phone number: +8621-38518896/38518923/38518637

Zip code: 200120

Website: www.sc.com

H. Rating Agencies:

1. China Chengxin International Credit Rating Co., Ltd. (“CCXI”)

2. China Bond Rating Co., Ltd. (“China Bond Ratings” or “CBR”)

Registered address: Tower 6, Galaxy SOHO, Nanzhugan Hutong, Chaoyangmennei Street,

Dongcheng District, Beijing

Legal representative: Yan Yan

Contacts: Xuan Liu, Yi Kang, Li Wang, Tianwei Wang, Bo Lv

Phone number: +8610-66428877

Zip code: 100010

Website: www.ccxi.com.cn

Registered address: 6/F, Tower 2, 28 Financial Street, Xicheng District, Beijing, PRC

Legal representative: Guanghua Feng

Contacts: Bo Liu

Phone number: +8610-88090164

Zip code: 100032

Website: www.chinaratings.com.cn

6

I. Auditor/Tax Advisor: Ernst & Yong Hua Ming LLP. (“EY”)

Registered address: Unit 01-02, 17th Floor, EY Tower, Oriental Plaza, 1 East Chang An

Avenue, Beijing, China

Legal representative: Anning Mao

Contacts: Suoteng Feng, Yi Ma, Jian Lou, Shuyan Gao, Mingyan Wei

Phone numbers: +8610-58153103/58184411/58185459

Zip code: 100738

Website: www.ey.com

J. Transaction Counsel: Zhong Lun Law Firm (“Zhong Lun”)

Registered address: 28, 31, 33, 36, 37/F, SK Tower, 6A Jianguomenwai Ave., Chaoyang

Dist., Beijing, PRC

Legal representative: Xuebing Zhang

Contacts: Borong Liu, Xiaoli Liu, Jingyi Lu, Wei Xu, Honglei Zhao, Liang Shi,

Wenting Yuan, Yuxi Zhang, Yifan Tong

Phone number: +8610-59572288

Zip code: 100022

Website: www.zhonglun.com

7

Chapter I RISK DISCLOSURE AND STATEMENT OF

INFORMATION CHANGES

The Securities in this Issue only represent corresponding shares of the “Trust Beneficiary Interest”

of the special purpose trust and do not constitute liabilities of the Originator, the Trustee or any

other organization towards the investors. The recourse of investors under the Securities in this

Issue is limited to the Trust Property.

Investors purchasing the Asset-Backed Securities (Securities) should carefully read this Offering

Circular and relevant disclosure documents and make independent investment judgments. The

approval of this Issue by relevant administrations does not suggest any opinion of the investment

value of the Issue, nor does it show any judgment to the investment risks of Issue.

The following context summarizes potential risks within the Securities, each of which might causes

significant adverse effects to all or part of the Noteholders. Therefore, investors purchasing the Securities

should carefully consider the following risk factors.

A. Risk Disclosure for Investors

1. Credit Risk

If any borrowers under the Trust Property fail to fulfill their obligations of repaying the principal and

interest fully or on time, the cash flows of Trust Property may fall below the expectation, impairing the

ability of the Securities to pay interest or repay the principal amount when they come due, and

consequently Investors could suffer losses.

In response to these risks, the Rating Agencies has considered the situation such as default events occur

in advance and collateral value depreciation etc., while conducting the cash flow stress test. The

Originator has also set the Eligibility Criteria for the underlying asset, and has made an asset guarantee

for each loan transferred. If any loan is found non-conformity to the Eligibility Criteria on the cut-off

date or the Trust Effective Date, then the Originator is obliged to repurchase such asset from the Trustee,

such arrangement will relieve the credit risk of the borrowers to a certain extent.

2. Structural Risk

The transaction structure of the Issue involves various parties, including but not limited to the

Originator/Settlor, Issuer/Trustee, Servicer, Fund Custodian, Financial Advisor, Lead Underwriter, Joint

8

Lead Underwriters, Auditor/Tax Advisor, Legal Advisor, Rating Agencies, Notes Custodian/Paying

Agent, etc. This complex structure might have flaws due to potentially inadequate communications.

In response to these risks, the Transaction Documents clearly stipulate the rights and obligations of the

Originator / Settlor, the Trustee / Issuer, Servicer, Fund Custodian, etc., and stipulate the responsibility

of default and the responsibility of compensation of the losses caused by the misconduct or breach of

contract from each institution, etc. In addition, the participants in this transaction have relatively adequate

experience in asset-backed securitization, which to some extent, reduces the risk of transaction structure.

3. Risk Concerning the Collateral of the Underlying Assets

Concentration Risk

The collateral of the underlying assets are real estate properties concentrated in several regions, which

makes them vulnerable to the regional real estate market fluctuation. Any fluctuations in the real estate

price or value may cause an adverse effect to the LTV and consequently influence the investment return

of the Securities. Specifically, the collaterals of the underlying assets are concentrated in Guangdong

Province, Jiangsu Province, Fujian Province, Zhejiang Province and Shandong Province, accounting for

51.32% of the total Outstanding Principal Balance. In case of large fluctuations in the real estate markets

of these regions, the credit performance of underlying assets would be adversely affected.

Value Fluctuation Risk of the Collateral

The underlying assets of the Securities are residential mortgage loans. Due to the features of the

underlying assets, the Securities have a relatively long term to maturity, which might span multiple

economic cycles. As a result, the value of the collateral could be influenced by multiple factors and the

value could fluctuate.

Risk of the Trustee’s Failure to Claim the Mortgage in Special Situations

On the Trust Effective Date, instead of directly transferring the Right to Mortgage of the underlying

assets to the Trustee, the Originator choose to make an agreement with the Trustee that the Right to

Mortgage of the underlying assets will not be transferred to the Trustee until Individual Notification

Event occurs.

When a borrower defaults and the Trustee needs to exercise the mortgage, such a situation might prevent

the Trustee from exercising the mortgage in time since the process of transferring the Right to Mortgage

differs in every region of PRC. Furthermore.

The above factors, causing the Trustee to be unable to exercise their claim on the mortgage in time, would

9

influence the loan recovery progress and recovery amount, and the Trust Property may suffer losses

consequently.

In response to these risks, the Trustee will continually pay attention to the real estate market in these

areas. Meanwhile, in order to reflect the downside risk due to macro market, the Rating Agencies will

consider the situation such as default events occur in advance and collateral value depreciation etc., while

conducting the cash flow stress test. According to the transaction structure, once any of the Individual

Notification Event occur, CCB is required to submit all compulsory documents of application that are

relative to the residential mortgage transfer registration to the relevant government authorities within 30

Business Days; and complete the mortgage transfer registration within 9 months, to ensure the Right to

Mortgage is registered under the name of the Trustee.

4. Liquidity Risk

The Securities are still innovative financial products in China; investors are unfamiliar with such

products. So the transfer of securities might entail liquidity risk since it might be difficult to find trading

counterparties.

In line with market development, the scale of asset securitization product offerings will further increase,

the trade platform will become richer, the courage of repurchase transactions, etc. will cause the liquidity

of asset securitization products to improve. With the development of securitization on trial, the investors

are more familiar with the securitization products, more and more qualified investors will bring ABS

products into the scope of investment and liquidity of which will be improved.

5. Interest Rate Risk

All underlying assets bear interest at floating rates. Class A-1 Notes and Class A-2 Notes are floating rate

(the coupon rate is equal to the sum of the Benchmark Interest Rate and the Spread). Underlying assets

and Senior Notes are different in the time and range of interest rate adjustments. As a result, interest rate

risk might occur due to interest rate fluctuations and time mismatch. As the Securities have a long term

to maturity, changes in residential mortgage policies and interest rate policy may happen. Interest rate

risk might rise when Benchmark Interest Rate policies and residential mortgage interest rate policies

change asynchronously.

Interest rate risk of fixed income securities cannot be avoided, the investors should use their own analysis

of market trends, combined with interest rate risk management tools and hedging tools to reduce the

possibility of losses. Class A-1 and Class A-2 asset backed securities use fixed interest rate, which could

reduce the impact of interest rate fluctuation on the price of these securities.

10

6. National Real Estate Policy Risk

The PRC is a developing country, and the market mechanism is gradually improving. At this stage, the

macro-control of the government has played a significant role in preventing market failure and promoting

the economy in a healthy and rapid direction. At different stages of the economic cycle, the macro-control

measures generally taken by the PRC include monetary policy, fiscal policy, legal policy and

administrative measures.

First, from the perspective of the buyers, because the investment channels are relatively narrow and real

estate has value-adding characteristics, many people regard the purchase of real estate as an effective

means of maintaining and increasing personal wealth. Therefore, the speculative demand for real estate

far exceeds the actual demand, and excessive speculative demand further causes real estate prices to rise.

Majority of the funds utilized by the speculative buyers are from commercial banks, which increases the

risk borne by the banks. According to this situation, the government could regulate this risk by using two

methods. First, by increasing the proportion of down payment, the government would add restrictions on

the requirements of purchasing real estate. Second, the government could formulate various policies to

allow buyers to form expectations of the changes in real estate prices in order to regulate their purchasing

behaviors.

Second, from the perspective of real estate developers, with the macro regulation and control of the

government, the approval process for real estate developers to obtain loans from commercial banks has

become stricter and purchasers lack the motivation to buy houses; thus, developers face a more severe

situation.

Third, from the commercial bank’s point of view, as the main source of funds for real estate developers

and buyers, they regard residential mortgage loans as high quality assets and provide long-term loans to

real estate developers. They serve as a very important link in the real estate capital chain.

The impact of macroeconomic regulation and control on real estate credit risk in commercial banks is

reflected in two aspects. Firstly, the loans provided by banks are mostly mid-term and long-term loans,

which are more difficult to adjust quickly according to the state’s macro-control policies. Secondly, with

further and strengthened macroeconomic regulation and control of the real estate market, previous loan

risks are gradually revealed and the risk of residential mortgage loans is more pronounced.

Policy risk cannot be avoided through pre-set trading mechanisms due to its unpredictability and

irresistibility. But the Trustee will promptly communicate with investors in face of unfavorable policy

changes and initiate the Noteholders conference to set up a response plan if necessary.

11

7. Prepayment Risk

In addition to the factors such as delinquency, default and recovery, borrower's prepayment behavior and

loan modification under the negotiation between borrower and sponsor are more likely to cause the

changing of initial underlying cash flow planning, which will result in cash flow changes of trust property

and also will make the actual underlying cash flow different from the expected cash flow announced in

the Offering Circular. Interest rate, political, economic, social, demographic and other factors may have

an impact on the mortgage prepayment. Because of many uncertain factors, it is difficult to accurately

predict the time and amount of borrower’s prepayment. On the premise that all other factors being equal,

if a large number of mortgages are repaid in advance, the weighted average life and maturity of Asset

Backed Notes will be shortened. At the same time, the return of the note holders may be affected by the

level of reinvestment yield of the market at that time. If the actual mortgages prepayment exceeds

expectations, it may result in the actual maturity of Asset Backed Notes shorter than expected and the

actual weighted average life shorter than expected; if the actual mortgages prepayment fails to meet

expectation, it may result in the actual maturity of Asset Backed Notes longer than expected and the

actual weighted life longer than expected, which may adversely affect the fund planning of the note

holders.

Prepayment risk cannot be avoided as to RMBS. Investors should anticipate the fluctuation of cash flow

of underlying assets according to their own statistical analysis. With the development and innovation of

China's asset securitization market, innovative financial instruments or trading structures may emerge in

the future to mitigate the risks associated with such risk. In case that, there is any significant adverse

impact on the holders of the asset-backed securities, the investor will be notified immediately.

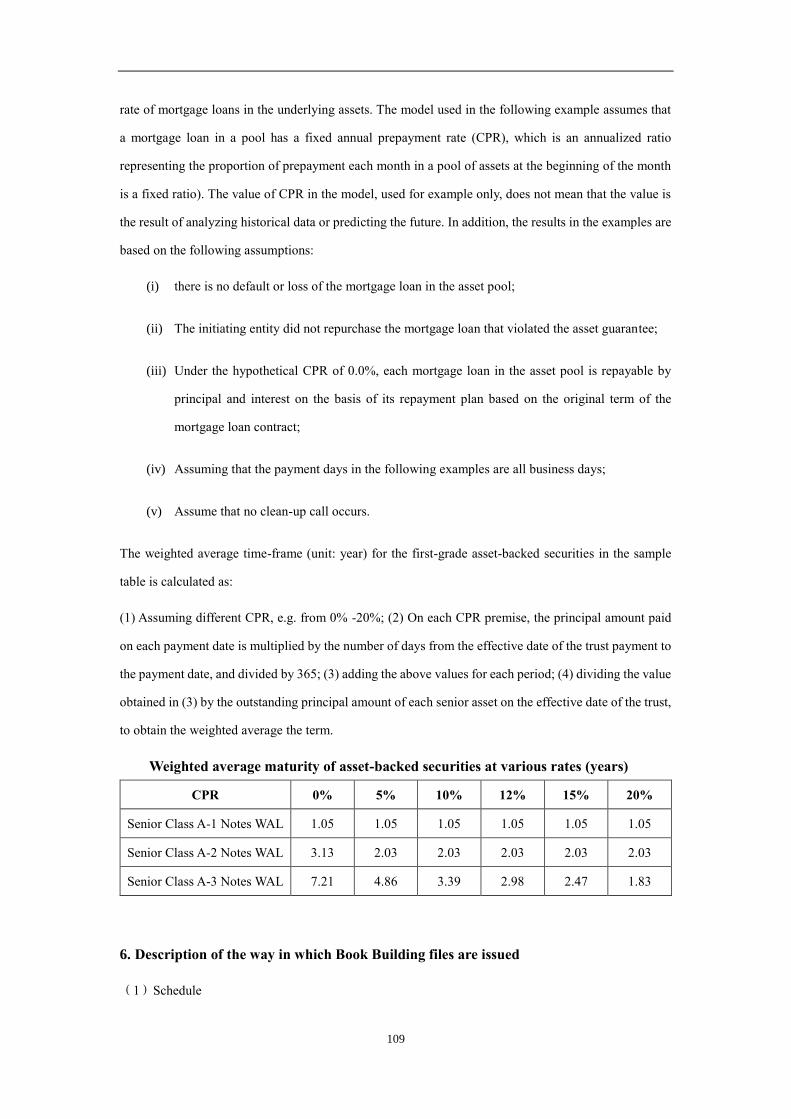

8. The Risk that Actual Maturity Date and Actual Principal Amortization Schedule of the

Senior Asset Backed Notes Differ From those of the Expected Values

The actual maturity date and weighted average life of individual Residential Mortgage Asset Backed

Notes are closely related to the actual performance of the underlying asset pool. The related factors

include, but are not limited to, underlying’s prepayment, delinquency, default and recovery. The actual

performance of asset pool may be affected by many factors, such as the national real estate policy

regulation, national macroeconomic changes, residents' consumption level and financial management

concepts, which make the trust property’s actual cash flow hard to predict. Through statistics and analysis

of the static data of CCB’s residential mortgage and the actual performance of the underlying asset pool

of Jianyuan Series RMBS deals, this Offer Circular uses the cashflow under the assumption of zero

default rate and annualized conditional prepayment rate equals to 5%, to derive Senior Class A-1 Notes

12

and Senior Class A-2 Notes’ principal amortization schedule. It also uses the cashflow under the

assumption of zero default rate and annualized conditional prepayment rate equals to 10% and the

cashflow under the assumption of zero default rate and zero prepayment rate, to derive the expected

maturity dates for information disclosure respectively. Due to the difference between the actual

underlying cash flow and expected underlying cash flow, the actual maturity date of each Asset Backed

Notes may be different from expected, and the actual principal amortization schedule may be different

from the planned principal amortization schedule, which will have a negative impact on the note holders.

9. Operational Risk

Operational risk refers to the risk of losses due to inappropriate or failed internal procedures, employees

and system, or external events. As the post-issuance management work is complex, delays in making

payments could occur.

Operation risk may originate from investors' own operational risks and from the agencies involved,

resulting in the defects in the design of asset-backed securities. For the latter, this securitization

transaction adopts the following measures to reduce operational risks faced by investors: (1)Strictly

establish the legal rights and obligations of all parties to the transaction, and ensure the legitimacy,

integrity and strictness of the transaction; (2)Information disclosure shall be carried out in strict

accordance with relevant laws, regulations and policies; (3) Public issuance documents to investors with

a full range of information disclosure; (4) During the lifetime of Asset-backed Securities, the Trustee will

regularly issue Trustee Report and disclose major events that may affect the interests of investors from

time to time. (5) Rating Agencies will conduct initial ratings and follow-up ratings for the Notes. In

addition, the participants in this transaction have relatively mature experience in asset securitization

business, which could reduce operation risks to certain extent.

10. Legal Risk

Legal risk refers to the risk that the contracts would not be implemented due to certain defects of financial

regulations, misunderstanding of provisions by relevant parties, lack of enforcement or ambiguity of

provisions etc., as well as other risks in connection with litigation, adverse judgment and deficiency of

legal instruments. Legal risk exists throughout the life of a contract, including the signing of the contract,

the performance of the contract and any dispute resolution proceedings in relation to the contract.

In the view of the above risk, in conjunction with the problems encountered during the previously issued

Jianyuan series of RMBS, the relevant parties of this securitization transaction have fully discussed and

communicated the contents of the transaction documents, and will make their best to to avoid

13

misunderstanding or poor execution or even non-execution events due to poor quality of the transaction

documents.

11. The Default Risk and the Risk of Material Adverse Change of the Counterparty

The transaction structure of the Issue involves various parties. Though the Rights and Obligations of

each party are regulated in the Transaction Documents, the Issuer cannot guarantee that there will not be

a default or a material adverse change in any party.

In the view of such risk, the relevant transaction documents of this project clearly stipulated the rights

and obligations of the Trustee, the Servicer and the Fund Custodian, and agreed on the default or

compensation responsibility for the loss due to their improper conduct or breach of contract. In addition,

in this transaction, accelerated payment event, termination event and selection criteria/ process of

replacement agent etc. are linked to the performance of the Servicer, Fund Custodian, Trustee and their

natural endowment, in order to minimize the adverse impact on asset-backed securities and investors

when a counterparty defaults or a material adverse change occurs.

B. Statement of Information Changes

Compared to the information of registrations report for applying the“Jianyuan”series RMBS, extra

credit enhancement measures including Liquidity reserve account and offset reserve account are

introduced. The Trust Reserve Account (Offset): is used to pay the deficiency at the time of cash flow

transfer payment of the trust when the borrower claims offsetting rights. Trust Reserve Account

(Liquidity): is used to make up the deficiencies in paying the agency service charge and interest of senior

notes which are caused by default of underlying asset or fluctuations of repayment. Definition of event

of default are adjusted for this issue of securities by adding triggering condition of offset reserve

withdrawal event. Transaction process stated above will enhance the credits of the senior notes. Details

are as followings:

1. Trust account setup

As on or before the Cut-Off Date, the Trustee should set up an independent Trust Account in the Fund

Custodian in its full name, “CCB Trust LLC”, pursuant to the Fund Custody Agreement. The Trust

Account includes Collection Accounts (Interest Sub-Account and Principal Sub-Account), Trust

Payment Account (Allocation Principal Account, Allocation Interest Account and Allocation Expenses

Account), Service Transfer Reserve Account, Tax Reserve Account, Offset Reserve Account, and

Liquidity Reserve Account;

14

The Trustee set a series of Reserve Account in order to prevent risk of trading structure:

• The Trust Reserve Account (Service Transfer and Notice), is used to pay special expenses occurred

because of change of servicer or sending the Right Completion Notice.

• The Tax Reserve Account, is used to pay taxes to tax authorities and other competent authorities.

• The Trust Reserve Account (Offset), is used to pay the deficiency at the time of cash flow transfer

payment of the trust when the borrower claims offsetting rights.

• The Trust Reserve Account (Liquidity), is used to make up the deficiencies in paying the agency

service charge and interest of senior notes which are caused by default of underlying asset or

fluctuations of repayment.

(1) Trust Reserve Account (Liquidity) setup and fund application

Before the occurrence of any Event of Default and the completion of the payment of the principal and

interest of senior notes,the Trustee should allocate the Collections, On each Trust Allocation Date, the

Trustee should transfer the entirety of the funds from the Trust Reserve Account (Liquidity) to the

Principal Sub-Account, and the funds will be allocated according to the Trust Agreement. After the

occurrence of any Event of Default and the completion of the payment of the principal and interest of

senior notes, the Trustee should transfer the balance of the Trust Reserve Account (Liquidity) to the

Principal Sub-Account.

Necessary (liquidity) refers to the reserve amount allocated day, became a trust before (a) in the event of

default occurs and in all the priority file before complete payment of the principal and interest of asset-

backed securities, for the distribution of the trust, in accordance with the trust contract item 9.2 (a) (I) to

the first item (vi) all payments (not included are payments for trustee, and the agencies can reimburse

the total amount of spending cap to be the priority for computing) two more in a year to cope with a

trustee of the sum of the total compensation;(b) zero after the event of default or after the completion of

principal and interest payments on all underlying asset-backed securities

On Trust Allocation Date, the Required(liquidity)reserve amount indicates:(1)Before the occurrence

of any Event of Default and the completion of the payment of the principal and interest of senior notes,

twice the mount according to the Trust Agreement item (i) to item (vi) of clause 9.2(a) (income of Trustee

excluded and ceiling at total amount of reimbursable expenses of each organization calculated on the

basis of the priority expenditure ) plus total annual remuneration payable to the trustee; (2)zero, after

15

the occurrence of any Event of Default and the completion of the payment of the principal and interest

of senior notes.

(2) Trust Reserve Account (Offset) setup and fund application

In case of offset reserve withdrawal event, the Trustee should transfer the fund equal to the amount

withdrawn from the Trust Reserve Account (Offset) to the Trust Account. In any of the following

circumstances: (1) Settlor has the rating recovered to its necessary grade and the Trustee has reasonable

justification that the deterioration in credit conditions of the Settlor disappeared and the Settlor is

informed;(2) Both principal and interest of senior notes are paid off; or (3) On Trust Termination Date,

the Trustee should follow instructions of the Fund Custodian to transfer the amount in Trust Reserve

Account (Offset) to the account indicated by the special beneficiary of trust.

According to statistical results of the Originator complied to the Trust Agreement, the amount in the Trust

Reserve Account (Offset) exceeds required (offset) reserve amount, the Originator could apply to the

Fund Custodian to withdraw the excess amount on the Servicer Report Performance Date. The Fund

Custodian should transfer the amount to the account indicated by the special beneficiary of trust.

(offset) reserve amount indicates, on the next Trust Allocation Date after the offset reserve withdrawal

event, the amount by which any borrower exercises offsetting rights with respect to the amounts owned

by the Trustee (including but not limited to deposits) and the loans in the asset pool.

Required (offset) reserve amount indicates: (1) when the Settlor loses the necessary rating grade or the

Trustee has reasonable grounds to think that the Settlor's credit status has significantly deteriorated and

has notified the Settlor, the sum of the amount ( Including, but not limited to, current deposit, fixed time

deposits, etc., but subject to the outstanding principal balance of the pooled loan of the corresponding

borrower at that time) of all borrower deposited at the Settlor at the time when the Notice of rights

perfection is sent by the Settlor or the Trustee; (2) under circumstance after (1) and before (2), the

required (offset) reserve amount shall be adjusted once after each collection period finished, required

(offset) reserve amount is the sum of the Offsetting amount of each borrower at the end of the collections

period, i.e., the lowest of the following three items: (i) the amount that the borrower deposited at the

Settlor at the time when the Notice of rights perfection is sent by the Settlor or the Trustee, (ii)

Outstanding Principal Balance of the borrower by the end of the collection period, (iii) the sum of the

amount ( Including, current deposit and fixed time deposits) that borrower deposited at the Settlor; (4)

when the Settlor has the rating recovered to its necessary grade and the Trustee has reasonable

16

justification that the deterioration in credit conditions of the Settlor disappeared and the Settlor is

informed or the principal and interest of the senior notes are paid/the Trustee Determination date, the

required (offset) reserve amount equals to zero.

2. Additional Triggering Mechanism

Comparing to the trading provisions set in the Application Report for Registration, there are

modifications to the definition of Event of Default, and additional Fund Custodian Termination Event

and Withdrawal of Reserve (Offset) Event are designed in this transaction. The modifications goes below:

(1). Event of Default

It shall trigger the Event of Default if,

a) The Trustee fails to pay the interests of the highest level of the Senior Class Notes, of which the

principals shall be reimbursed but not yet paid at that time, in 10 business days (or in the grace period

granted by the Controlling Noteholders Meeting) after the Date of Payment, provided that the outstanding

balance of the highest class of the Senior Class Notes shall remain and the Trustee cannot pay the interests

of other classes of the Senior Class Notes nor the benefits of the Subordinated Class Notes due to the

lack of funds,

b) The Trustee fails to reimburse the principals of the Senior Class Notes in 10 business days (or in

the grace period granted by the Controlling Noteholders Meeting) after the Legal Maturity Date,

c) The Trustee breaches the material duties, conditions or provisions regulated in the Provisions and

Conditions of the Securities, the Trust Agreement or the transaction documents in which the Trustee signs

as a party, and the Controlling Noteholders Meeting reasonably believes that such breach of duties (i)

cannot be cured , or (ii) can be cured but the Trustee fails to recover in 30 business days after the

Controlling Noteholders Meeting send a written notice to recover, or (iii) can be cured by means of

replacing the Trustee according to the transaction documents but it fails to replace the Trustee in 90

business days after the occurrence of the Event of Default, or

d) The Controlling Noteholders Meeting reasonably believes that the Trustee makes significantly

untruthful and misleading statements and guarantees in the Trust Agreement or other transaction

documents in which the Trustee signs as a party, and the Controlling Noteholders Meeting reasonably

believes that such significantly untruthful and misleading statements and guarantees (i) cannot be cured ,

or (ii) can be cured but the Trustee fails to recover in 30 business days after the Controlling Noteholders

17

Meeting send a written notice to recover, or (iii) can be cured by means of replacing the Trustee according

to the transaction documents but it fails to replace the Trustee in 90 business days after the occurrence

of the Event of Default.

e) When any of the events listed in (a) to (b) above occurs, the Event of Default is deemed to have

occurred on the date of that event. When any of the events listed in (c) to (d) above occurs, the Controlling

Noteholders Meeting shall determine whether to announce the occurrence of the Event of Default and to

notify the Trustee to inform the Servicer, the Fund Custodian, the Securities Custodian, the Paying Agent,

and the Rating Agents such occurrence by written notice or not. Before the Controlling Noteholders

Meeting making such decision, the Trustee shall allocate the Collections pursuant to the order in § 9.2 of

the Trust Agreement as the Accelerated Payment Event having occurred. After the Controlling

Noteholders Meeting announcing the Event of Default occurs, the Trustee shall allocate the Collections

pursuant to the order in § 9.3 of the Trust Agreement.

f) Upon the Event of Default, the Noteholders enjoy the rights regulated in § 10 of Provisions and

Conditions of the Securities.

(2). Withdrawal of Reserve (Offset) Event

It shall trigger the Withdrawal of Reserve (Offset) Event if any of the Borrowers claims to exercise the

right to offset the Originator’s debts to the Borrower (including but not limited to the Borrowers deposits

in the Originator) and loans in the Assets Pool, when the Originator fails to meet any Required Rating

Levels or the Trustee reasonably believes and informs the Originator that the credit level of the Originator

significantly deteriorates.

Besides of the above, no other information change has occurred.

18

Chapter II TRANSACTION BASICS

A. Transaction Parties Diagram

The following diagram shows the role of each transaction party and provides a brief summary of each

principal transaction document in the Issue.

Transaction Process is summarized as follows:

According to the Trust Agreement, CCB, as the Originator, transfers certain residential mortgage loans

as the Trust Property to CCB Trust, as the Trustee, to establish the Special Purpose Trust for the Issue.

The Trustee issues the Securities to Investors and pays the principal and interest of the Securities subject

to the cash flow generated by the Trust Property. The amount of principal and interest of each Note and

Trust Asset Transfer

Statutory agreement signed by relevant parties

Capital

Sales of ABS

CCB

(Originator / client)

Borrower Loan

contract

Repay

Principal

Trust

Agreement

Trust

Asset

Issuance

Proceeds

CCBPCM

(Financial Advisor)

Financial Advisor

Agreement

Underwriting

Notes

CMS, CICC, HSBC(China),

SCB(China)

(Lead Underwriters)

Inter-bank Bond Investors

(including qualified Offshore

Investors)

Subscription

Funds

CCB

(Servicer)

CCB TRUST

(Trustee / Issuer)

CCDC

(Notes Custodian / Paying

Agency)

Lead Underwriting Agreement

Notes Principal

and Interest ICBC Beijing Branch

(Fund Custodian)

Service

Agreemen

t

Transfer

Collections

Fund Custodian

Agreement

Notes Custody

Agreement

Fund

Notes

Principal and

Interest Registration and

Depositary

19

the payment order are regulated by the Trust Agreement.

The Issuer signs the Underwriting Agreement with the Originator and Lead Underwriters, and the Lead

Underwriters sign the Syndication Agreement with other syndicate members to establish a syndication

in relation to the underwriting of the Securities (except for Subordinated Notes retained by the

Originator).

CCBPCM is responsible for financial advisory services for the whole trust.

Through the valid period of the Trust, the Trustee appoints the Servicer for the collection of Trust Property.

For the cash flow generated by the Trust Property, the Trustee appoints a Fund Custodian for fund storage

services.

All the Notes except for Subordinated Notes held by the Originator are traded on the CIBM.

CCDC or other agencies appointed by the administration as the Securities Custodian/paying agent of the

Issue are responsible for providing registration services, custody and transfer according to the Agency

Agreement.

B. Overview of the Participating Institutions

1. Servicer: China Construction Bank Corporation

China Construction Bank Corporation, headquartered in Beijing, is a large-scale joint stock commercial

bank in China. It was established in October 1954 and listed on Hong Kong Stock Exchange in October

2005 (stock code: 939) and the Shanghai Stock Exchange in September 2007 (stock code: 601939).

At the end of 2017, CCB had 14,890 domestic banking stores, including its head office, 37 tier-one

branches, 341tier-two branches, 13,297 sub-branches, 1,213 outlets and a specialized credit card center

at the head office. In 2017, CCB speeded up the layout of key regions and increased 94 outlets in

economic hotspots concerning the Belt and Road initiative, Beijing-Tianjin-Hebei integration, the

Yangtze River Economic Belt and the “Made in China 2025”. CCB implemented the national strategy of

inclusive finance and set up new outlets at the county level and entered 50 new counties. By of the end

of 2017, CCB opened a total of 306 private bank franchised institutions with 1,840 employees,

accumulatively established 288 small business centers, and built more than 1,500 individual loan centers.

The overall layout has become increasingly sophisticated, business processes continue to be optimized,

and the brand effect has become increasingly prominent.

CCB has overseas branches in Hong Kong, Macau, Singapore, Frankfurt, Johannesburg, Tokyo, Osaka,

Seoul, New York, Ho Chi Minh City, Sydney, Melbourne, Taipei, Luxembourg, Brisbane and Toronto as

20

well as subsidiaries including CCB Asia, CCB International, CCB London, CCB Russia, CCB Dubai,

CCB Europe, CCB New Zealand CCB Principal Asset Management, CCB Financial Leasing, CCB Trust,

CCB Life, CCB Futures, Sino-German Bausparkasse, etc., which enables it to provide comprehensive

financial services for clients.

CCB aims to uphold customer-oriented and market-oriented operation philosophy as well as accelerate

its transformation towards integration, multi-functionality, intensive management, innovation and

intelligence. It provides excellent and comprehensive financial services to its clients through innovation

on products, channels and its service model. CCB works to be a bank that is aimed to serve the public,

promote the people’s livelihood, and to be environment-friendly and develop sustainably. CCB leads the

market in many core operating indicators and develops emerging businesses such as investment banking,

credit card, electronic banking, private banking, consumer finance, etc., while maintaining the traditional

advantages present in infrastructure, residential mortgage, etc. CCB optimizes business and management

flow, increases investment across various infrastructures, and promotes effective risk management and

competition in markets.

At the end of 2017, the total assets of CCB reached RMB 22.12 trillion. Its gross balance of loans and

advances to customers was RMB 12.90 trillion, its total liabilities were RMB 20.33 trillion, and the total

deposits from customers reached RMB 16.36 trillion. By the five-category loan classification, NPLs of

CCB were RMB 0.19 trillion and NPL ratio stood at 1.49%, a decrease of 0.03% from the end of 2016.

Provision coverage was 171.08% which was an increase of 20.72% over 2016 and loan-to-deposit ratio

was 70.73%, an increase of 2.56% over 2016. In accordance with the requirements of the Administrative

Measures for Liquidity Risk Management of Commercial Banks (Provisional), total capital ratio, tier-

one ratio and common equity tier-one ratio were 15.50%, 13.71% and 13.09%, respectively. 0.56, 0.56

and 0.11 percentage points higher than those as at the end of 2016, respectively.

In order to support demand concerning people’s livelihood such as housing demand, CCB has been

focusing on supporting people to buy their principal residence. By the end of 2017, its balance of

residential mortgage loans was RMB 4.21 trillion, an increase of RMB 0.63 trillion over 2016 and

remains the largest among its peers in PRC.

In 2017, the total profit and net profit of CCB were RMB 299.79 billion and RMB 243.62 billion, an

increase of 1.55% and 4.83% from 2016, respectively. Average ROA and Weighted Average ROE were

1.13% and 14.80%. In 2017, CCB achieved operating income of RMB 621.66 billion, up by /2.74% from

2016. Specifically, net interest income amounted to RMB 452.46 billion, net interest margin was 2.21%.

Fee and commission income was RMB 117.80 billion and cost-to-income ratio stood at 26.95%, a

21

decrease of 0.60% and 0.54 percentage points compared to those as at the end of 2016, respectively.

2. Financial Advisor: CCB Principal Capital Management Co., Ltd.

Approved by China Securities Regulatory Commission (“CSRC”) (ref. Zheng Jian Xu Ke 2013 No. 693),

CCB Principal Capital Management Co., Ltd. was established on 26/6/2013 with a registered capital of

RMB 50 million. CCBPCM was funded by CCB Principal Asset Management Co., Ltd. (“CCBPAM”)

and CCB International (China) Co., Ltd., holding 51% and 49% of the shares respectively. On January

2, 2018, CCBPCM successfully increased its registered capital to RMB 1,350 million, with the

proportion of shareholders unchanged. On July 5, 2013, CSRC granted the Qualification Certificate for

the Specific Client Asset Management Business to CCBPCM, allowing the scope of business to include

the specific client asset management and other business approved by CSRC.

CCBPCM closely relies on the advantages of shareholders and CCB, the actual controller, in terms of

brand, channel, management and project resources. With the mission of “serving the real economy and

building a wealthy life”, CCB adheres to the principles of “Honesty, Professionalism, Standardization

and Innovation”. Utilizing its effective corporate governance, strict risk control, standardized business

process, professional staff and open company culture, CCBPCM takes comprehensive use of equity, debt,

benefits and other business mechanisms of shareholders and investors to provide comprehensive and

professional financial services.

3. Lead Underwriter/Book Runner: China Merchants Securities Co., Ltd.

As part of the China Merchants Group whose history can be traced back to the early 1900s, CMS has

grown to become a leading full-service investment bank after 20 years of entrepreneurial development.

CMS successfully went public on the Shanghai Stock Exchange in November 2011 (Ticker: 600999).

CMS has now been selected as a constituent stock for CSI 100, SSE 180, SHSE-SZSE 300 Index and

FTSE Xinhua China A50 Index, etc.

CMS maintains sustainable and stable profitability, a scientific and reasonable risk management structure

and a comprehensive array of professional services. CMS has multi-layer servicing channels for the

clients and operates almost 200 domestic securities business offices and branches in Mainland China and

Hong Kong. Leveraging its ownership of CMS International, China Merchants Futures, China Merchants

Capital, Bosera Asset Management, and China Merchants Asset Management, CMS has truly developed

into a securities service platform that aims to comprehensively integrate international and domestic

financial services.

CMS is devoted to comprehensively enhance the core competency and create the best-in-class investment

22

bank of China. CMS delivers remarkable financial services to achieve the growth of value of clients, to

lead the advancement of the securities industry, and is determined to be an international financial

institution with enriched products, top-level services, outstanding competency and remarkable branding

and an excellent enterprise that is embodied with trust from clients, respect from the society, satisfaction

from shareholders, pride of employees. CMS has been rated Class A AA level by the Securities

Association of China as a securities company for the past eleven years.

As an experienced market participant in credit asset securitization, by the end of September 2018, CMS

has participated in the issuance of 165 credit asset-backed securities as Lead Underwriter, consisting of

7 in 2014, 23 in 2015, 37 in 2016, 61 in 2017 and 57 in 2018.

At the end of 2017, total assets of CMS reached RMB 285.6bn with total liabilities at RMB 206.3bn.

The revenue, profit and net income in 2017 were RMB 13.4bn, RMB 7.10bn and RMB 5.81bn,

respectively.

4. Joint Lead Underwriter

(1) China International Capital Corporation Limited.

Set up in July 1995, China International Capital Corporation Limited (CICC) is China’s first joint-

venture investment bank founded on basis of strategic partnership among reputable financial institutions

and companies throughout the world. CICC had a registered capital of 4,192,667,868 RMB by the end

of June 2018. CICC’s largest shareholder is Central Huijin Investment Limited. Since its inception, CICC

has always been committed to providing high quality value-added financial services to clients. CICC has

established a full-service business model consisting of investment banking, equities, FICC, wealth

management and investment management on the basis of strong research coverage.

Headquartered in Beijing, CICC has established subsidiaries in Mainland China, branch companies in

major cities including Shanghai and Shenzhen, and over 200 securities branches in 28 provinces and

municipalities across China. CICC has also actively ventured into the overseas markets and has

established subsidiaries in Hong Kong, New York, Singapore, London and Germany. Leveraging the

extensive network and outstanding cross-border capabilities, CICC is well-positioned to provide all-

round financial services to clients.

By the end of 2017, CICC’s total assets amounted to 237.81 billion RMB, the total liabilities amounted

to 200.92 billion RMB, and the total equity amounted to 36.71 billion RMB. In 2016 and 2017, CICC

reached a total revenue of 8.94 billion RMB and 15.26 billion RMB, profit before income tax of 2.33

billion RMB and 3.60 billion RMB, and profit of 1.82 billion RMB and 2.77 billion RMB, respectively.

23

CICC is experienced with long-term preparations in the asset-backed securitization business. By the end

of June 2018, CICC has finished 54 issuances of Credit Asset-backed Securities as the role of Lead

Underwriter.

(2) HSBC Bank (China) Company Limited

As of December 31, 2017, HSBC Bank (China) Company Limited (“HSBC China”) had total assets of

RMB 467.936 billion, net assets of RMB 46.871 billion; and operating income for the 2017 financial

year was RMB 10.738 billion, with net profit of RMB 3.824 billion. The registered capital of HSBC

China was RMB 15.4 billion. As of December 31, 2017, The Hongkong and Shanghai Banking

Corporation Limited holds 100% shares of HSBC China.

HSBC China has been involved in the underwriting of ABS in the China Interbank Bond Market

(“CIBM”) since 2014. As of September 30, 2018, a total of 35 ABS have been underwritten by HSBC

China. HSBC China's strong underwriting ability has been proven and reinforced by the successful

issuance of each of the ABS in which HSBC China acted as an underwriter. In BaSky China 2015-2 Auto

Mortgage Loan Asset Backed Securities originated by BMW Automotive Finance (China) Limited in

Nov 2015, HSBC China acted as the Joint Lead Underwriter and became the first foreign bank to lead

underwrite China onshore ABS. Since then, HSBC China has joint lead underwritten Fuyuan 2016-1

Auto Mortgage Loan Asset Backed Securities, VINZ 2016-1 Auto Mortgage Loan Asset Backed

Securities, Driver China Four Auto Mortgage Loan Asset Backed Securities, Silver Arrow China 2016-

2 Auto Mortgage Loan Asset Backed Securities, Driver China Five Auto Mortgage Loan Asset Backed

Securities, Fuyuan 2017-1 Auto Mortgage Loan Asset Backed Securities, Autopia China 2017-1 Auto

Mortgage Loan Asset Backed Securities, Fuyuan 2017-2 Auto Mortgage Loan Asset Backed Securities,

Rongfa 2017-1 Auto Mortgage Loan Asset Backed Securities, Huitong 2017-1 Retail Auto Mortgage

Loan Asset Backed Securities, Huitong 2018-1 Retail Auto Mortgage Loan Asset Backed Securities,

Jianyuan 2018-11 Residential Mortgage Backed Securities and Fuyuan 2018-2 Auto Mortgage Loan

Asset Backed Securities. HSBC China does not have any historical default record related to ABS

underwriting in the CIBM.

(3) Standard Chartered Bank (China) Limited

Standard Chartered Bank is a leading international banking group with more than 86,000 employees and

a 150-year history in some of the world’s most dynamic markets. Standard Chartered Bank provides

financial services for people and companies in relation to investment, trade and creation of wealth across

Asia, Africa and the Middle East, where it earns around 90 per cent of income and profits. Its heritage

24

and values are expressed in its brand promise, Here for good. Standard Chartered PLC is listed on the

London and Hong Kong Stock Exchanges as well as the Bombay and National Stock Exchanges in India.

In China, Standard Chartered Bank set up its first branch in Shanghai in 1858 and has remained in

operation. SCB is one of the first foreign banks to locally incorporate in China in April 2007. This

demonstrates the Bank’s commitment to the Chinese market, and its leading position as a foreign bank

in the banking industry. SCB has 28 branches, 77 sub-branches and 1 Village Bank, totally 106 outlets,

including the China (Shanghai) Pilot Free Trade Zone Sub-Branch opened in March 2014.

Standard Chartered Bank is the leading player in Asian securitization market and has successfully helped

many Asian countries for the closing of their first securitization deals, such as China, Thailand, Indonesia,

Philippines, etc. Standard Chartered Bank was awarded the Asian Best Securitization House ten times

over the past 12 years, including the latest 2016 Asian Best Securitization House awarded by the Asset

magazine in February 2017. In 2015, Standard Chartered Bank finished 20 securitization deals in Asia,

the scale of which was over 14 million dollars. Since 2002, Standard Chartered Bank has actively

participated in the development of the Chinese securitization market. Standard Chartered Bank, acting

as the financial consultant, assisted the public offering of China’s first ever housing mortgage loans

backed notes (i.e. the 2005 CCB’s Housing Mortgage Loans Backed Notes, the amount of which is RMB

3 billion), and then successfully assisted 9 securitization deals for other well-known Chinese financial

institutions (these deals including housing mortgage loans backed notes, enterprise credit asset backed

notes, lease receivables backed notes and auto loans backed notes, etc.). In December 2015, SCB, acting

as the lead underwriter and joint bookrunner, has successfully assisted Ford Automotive Finance (China)

Ltd to issue “Fuyuan 2015-2 Retail Auto Mortgage Loan Securitization Trust” product in the National

Interbank Bond Market. Furthermore, in February 2016, SCB, acting as the lead underwriter, bookrunner

and sole financial consultant, has successfully assisted Beijing Hyundai Auto Finance Co., Ltd. to issue

its first credit securitization product—“Autopia China 2016-1 Retail Auto Mortgage Loan

Securitization”. After that, Standard Chartered Bank, acting as joint lead underwriter, arranged “Autopia

China 2016-2 Retail Auto Mortgage Loan Securitization” for Beijing Hyundai Auto Finance Co., Ltd

and “Fuyuan 2016-2 Retail Auto Mortgage Loan Securitization” for Ford Automotive Finance Company

in August 2016. In November 2016 and March 2017, Standard Chartered Bank, acting as Joint Lead

Underwriter and Financial Advisor, arranged “Shanghai 2016-1 Retail Auto Mortgage Loan

Securitization” and “Shanghe2017-1 Retail Auto Mortgage Loan Securitization” for Shanghai

Automotive Group Finance Company Co., Ltd, respectively. In March 2017 and May 2017, as Joint Lead

Underwriter and Financial Advisor, Standard Chartered Bank arranged “Rongteng 2017-1 Retail Auto

25

Mortgage Loan Securitization” and “Rongteng 2017-2 Retail Auto Mortgage Loan Securitization” for

SAIC-GMAC Automotive Finance Co., Ltd. As joint lead underwriter and financial advisor, Standard

Chartered Bank arranged “Driver China six Retail Auto Mortgage Loan Securitization” in May 2017 and

“Driver China seven Retail Auto Mortgage Loan Securitization” in September 2017 for Volkswagen

Finance (China) Co., Ltd. In August 2017, as lead underwriter and financial advisor, Standard Chartered

Bank arrange “Bavarian Sky 2017-2 Asset Backed-Notes” for BMW Automotive Finance (China) Co.,

Ltd. As lead underwriter, Standard Chartered Bank arranged “Fuyuan 2017-2 Retail Auto Mortgage Loan

Asset-backed Securities” in August 2017 and “Fuyuan 2018-1 Retail Auto Mortgage Loan Asset-backed

Securities” in January 2018. In September 2017, Standard Chartered Bank arranged “Autopia China

2017-2 Retail Auto Loan Asset-backed Securities” for Beijing Hyundai Auto Finance Co., Ltd. as lead

underwriter and financial advisor, and “Silver ArrowChina 2017-2 Retail Auto Loan Asset-backed

Securities” for Mercedes-Benz Financial Services as lead underwriter and financial advisor. In August

2018, SCB arranged “Generation 2018-1 Retail Auto Mortgage Loan Securitization” as joint lead

underwriter and financial advisor.

Moreover, in February 2015, SCB as the originator, has successfully issued its first credit securitization

trust in China—“Zhen Cheng Credit Asset Securitization 2015-1 Asset-back Securities” and became the

first batch of foreign banks to participate in the credit asset securitization pilot program in China.

5. Fund Custodian: Industrial Commercial Bank of China Ltd., Beijing Branch

The Industrial and Commercial Bank of China was established on 1/1/1984. On 28/10/2005, the Bank

was wholly restructured to a joint-stock limited company. On 27/10/2006, the Bank was successfully

listed on both the Shanghai Stock Exchange and the Hong Kong Stock Exchange. Through steady

expansion and stable development, the Bank has developed into one of the top banks in the world,

possessing an excellent customer base, a diversified business structure, strong innovational capabilities

and market competitiveness and providing comprehensive financial products and services to 5,784

thousand corporate customers and 530 million personal customers. With serving the real economy as the

foundation of its operation and management, the Bank has adhered to new ideas, new financing and new

services to support China’s supply-side structural reform, economic transformation, and upgrading as

well as to achieve its own healthy and sustainable development. The Bank has further promoted reform

and innovation as well as business transformation, developing retail finance, asset management, financial

market and other businesses into important engines of profit growth. The pattern of internationalized and

diversified operation was further improved, covering 42 countries and territories, and contributed more

to the Bank’s profit-making. In 2016, the Bank ranked 1st place on The Banker’s Top 1000 World Banks,

26

Forbes’ Global 2000 and Fortune Global’s 500 Sub-list of Commercial Banks for the fourth consecutive

year.

ICBC was one of the earliest fund custodians to participate in the trial of China's asset-backed

securitization business. Since then, ICBC has successively provided funds custody services for 51 ABS

projects. ICBC has established good cooperative relations with various intermediary agencies and

accumulated rich experience in capital custody. Currently, ICBC has the largest number of cooperating

institutions, and manages the most comprehensive types of securitised assets among the fund custodians

in the market.

6. Rating Agencies

(1) China Chengxin International Credit Rating Co., Ltd.

China Chengxin International Credit Rating Co., Ltd. is a pioneer of domestic rating business and a

leading independent credit rating services provider.

CCXI was established in October 1992 as the rating business division of China Chengxin Securities

Evaluation Co., Ltd. (now renamed as "China Credit Management Co., Ltd."). China Credit Management

Co., Ltd. is a national credit rating agency approved by the People's Bank of China.

In 2006, CCXI was invested by Moody’s Investors Services, combing advanced international rating

techniques with domestic rating practices of more than ten years, successfully localizing advanced

international rating techniques.

CCXI has servicing qualifications promulgated by People’s Bank of China, National Development and

Reform Commission, China Insurance Regulation Committee, National Economics and Trade

Commission, etc., and has great reputations in the market.

(2) China Bond Rating Co., Ltd.

China Bond Rating Co., Ltd. was founded in 2010 by National Association of Financial Market

Institutional Investors (NAFMII) on behalf of all membership, and the registered capital was RMB 50

million. CBR is not only the first credit rating company adopting the business model that investors make

payment, while other business models reinforce each other simultaneously, but also the only credit rating

agency authorized by PBOC to adopt this business model. Following the principles of independence,

objectivity and impartiality, CBR will provide investors with services such as re-rating and double rating.

An array of analysts with abundant experience of credit rating and of industry research joined CBR in

the early years; at the same time, talented graduates from top universities were selected as candidates

27

through campus recruiting. Currently, CBR, by industrial categories, has established 6 departments and

40 specialized industry research and analysis teams. Based on the staff structure, CBR has built a team

supported by senior analysts with abundant industrial experience as well as backed up by outstanding

graduates specializing in economics, finance, laws, and etc. The credit rating team structure is rational

and the division is clear. In terms of the company scale, CBR is running the team of more than 200

professional analysts, and has become one of the largest professional credit rating companies in the bond

market.

CBR values the establishment of credit rating system. On the basis of comprehensive investigation of

domestic and foreign credit rating system, it took CBR 4 months to develop and complete the research

of rating definitions, rating principles, rating symbol system, rating methods, rating policy-making, rating

model-building, rating report styles, and rating quality control; then CBR organized external experts to

prepare thematic certification, and to, preliminarily, specify the rating technical standards, management

standards, and orientation of information system establishment. Later on, CBR completed the rating

methods reasoning, industrial rating methods, debt rating methods, as well as the research and

formulation of innovative products’ rating models and methods. Currently, CBR has developed a set of

advanced rating technology system and methods that is suitable to China’s national conditions.

After the establishment of CBR, through a series of recruitment and selection, CBR selected a team of

senior analysts with more than 5 years’ experience in innovative financial products research and

development. After the talent team was built up, it took CBR 1 year to complete the development of

rating models of innovative products, establishment of the rating systems, and formulation of the rating

methods. Currently, CBR has accomplished the technology system of ABS rating as well as developed

the rating models suitable to China’s ABS products.

Since the expansion of asset securitization, CBR has participated in all of the successfully issued projects

and accumulated more than 500 projects, which covered all asset types of China Interbank Bond Market;

CBR acquired abundant experience of ABS projects and built up a mature team of professional analysts.

CBR discloses the credit risks by following the objective standards consistently, and provides investors

with comprehensive, sustained, and comparable credit rating information services.

7. Auditor/Tax Advisor: Ernst & Young Hua Ming LLP

Ernst & Young is a leading global professional service firm providing audit, tax and financial transaction

advisory services with a history of more than 100 years. Ernst & Young employed more than 212,000

people in more than 150 countries and 730 offices around the globe. Our 24 offices are located in Beijing,

28

Hong Kong, Shanghai, Guangzhou, Shenzhen, Chengdu, Dalian, Hangzhou, Macau, Qingdao, Suzhou,

Tianjin, Wuhan, Xiamen, Nanjing, Changsha, Shenyang, Xian, Taipei, Taichung, Tainan, Taoyuan,

Hsinchu and Kaohsiung. Ernst & Young employs nearly 14,000 people in Greater China. As a large

independent audit institution, Ernst & Young has many internationally renowned corporate clients. In

Greater China, there are also many domestic first-class corporate customers.

Ernst & Young was permitted by the People’s Republic of China ("PRC") government to establish a

representative office in Beijing in 1981. It was also one of the first firms approved by the PRC

government to establish a joint venture firm, Ernst & Young Hua Ming (“Ernst & Young”), in Beijing in

1992. Ernst & Young Hua Ming was approved by PRC Ministry of Finance to be switched from a joint

venture firm to a special general partnership firm in 2012.

Ernst & Young has established an experienced industry team in China. With an in-depth understanding

of all walks of life and domestic conditions, Ernst & Young can deploy the right team members at the