total cost of ownership - appa, leadership in … note this is pre -decisional tco material and not...

TRANSCRIPT

Deke Smith & Ana ThiemerCo-Chairs of APPA TCO Working Group

Copyright ©APPA 2017. All rights reserved.

Total Cost of Ownership

Copyright ©APPA 2017. All rights reserved.

The proposed ANSI approved standard has two parts. The first part is Under Public Review. The

second part of the standard has not been written.

All material contained in this presentation is subject to change.

Slide deck

TCO Definition

Copyright ©APPA 2017. All rights reserved.

The proposed ANSI approved TCO Standard

1 - TCO Key Principles

2 - TCO Implementation & Data

A holistic approach to maximizing return on investment of managed physical assets that includes the summation of all known and estimated costs to include first, recurring, renewal / replacement and end-of-useful life costs revised at critical decision points to aid in life-cycle asset management decisions.

TCO – PROPOSED - Definition

Copyright ©APPA 2017. All rights reserved.

Please note this is a pre-decisional TCO definition and not yet the product of the APPA 1000 committee.

A Total Cost of Ownership Culture Focus Shift – Information Thread

As-Is - Paper/PDF Approach To InformationMinimal information gain

To-Be - Data Focused Cumulative Information

Information not lost

Value of Improvement (ROI)Information collected one time

Supports decision makingover the life of the facility

Info

rmat

ion

Valu

e

Time

PlanningDesign

Construction

Operation

Copyright ©APPA 2017. All rights reserved.

The TCO APPA 1000 –Proposed ANSI Standard

Draft APPA 1000-1: Total Cost of Ownership (TCO)

Copyright ©APPA 2017. All rights reserved.

Total Cost of Ownership Committee

24 members - Working Groups Producers, Users General Interest

Modified Delphi approachworking separately & together

Assigned to Sub Working Group based on experience balanced as possible

Copyright ©APPA 2017. All rights reserved.

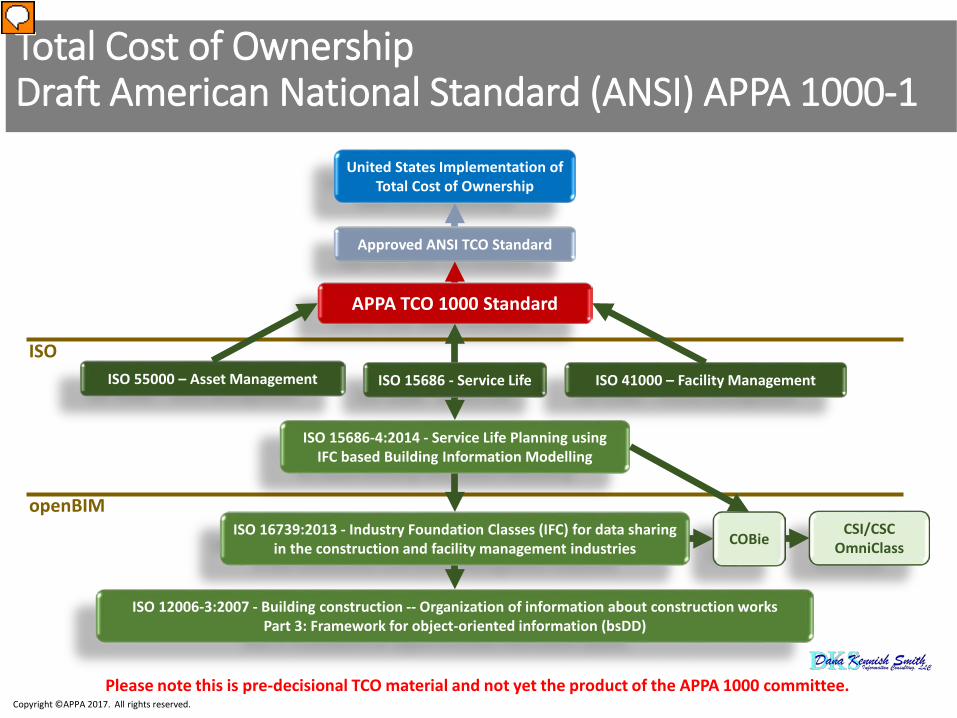

Total Cost of Ownership Draft American National Standard (ANSI) APPA 1000-1

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.

United States Implementation of Total Cost of Ownership

Approved ANSI TCO Standard

APPA TCO 1000 Standard

ISO 15686 - Service Life

ISO 15686-4:2014 - Service Life Planning using IFC based Building Information Modelling

ISO 16739:2013 - Industry Foundation Classes (IFC) for data sharing in the construction and facility management industries COBie

CSI/CSC OmniClass

ISO 41000 – Facility ManagementISO 55000 – Asset Management

ISO 12006-3:2007 - Building construction -- Organization of information about construction works Part 3: Framework for object-oriented information (bsDD)

openBIM

ISO

Copyright ©APPA 2017. All rights reserved.

Total Cost of Ownership Draft American National Standard (ANS) APPA 1000-1

Part 1 Establish the 13 Key Principles

Part 2 Establish TCO Implementation Plan & Data Elements

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

Asset ReportingAsset Sharing

Total Cost of Ownership Part 1 – Key Principles

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.

Asset ReportingAsset Infor. Sharing

Data Management & Verification

Copyright ©APPA 2017. All rights reserved.

Total Cost of Ownership Draft American National Standard (ANS) APPA 1000-1

Part 1 Establish the 13 Key Principles

Part 2 Establish TCO Implementation Plan & Data Elements

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

Implementation Goals

BasicBeginning effortSmaller portfolio

IntermediateBusiness processes changedData focusedLarger portfolio

AdvancedData integrated with BIMBusiness processes support long term budgetingFocus on long term stewardship of assets

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.

Copyright ©APPA 2017. All rights reserved.

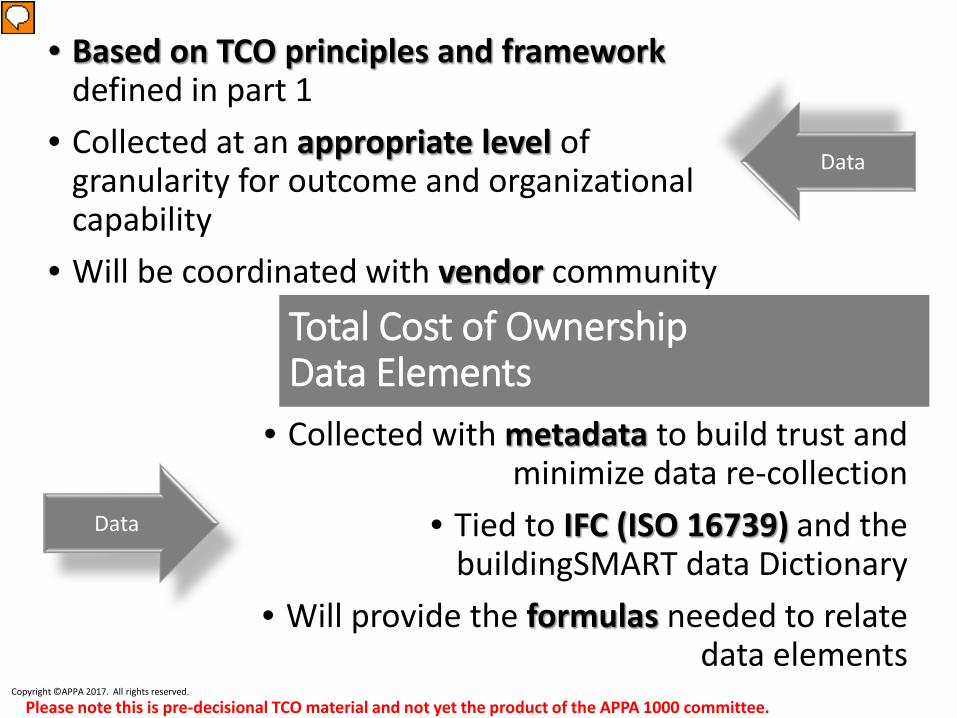

Total Cost of Ownership Data Elements

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.

• Based on TCO principles and framework defined in part 1

• Collected at an appropriate level of granularity for outcome and organizational capability

• Will be coordinated with vendor community

• Collected with metadata to build trust and minimize data re-collection

• Tied to IFC (ISO 16739) and the buildingSMART data Dictionary

• Will provide the formulas needed to relate data elements

Copyright ©APPA 2017. All rights reserved.

Data

Data

Copyright ©APPA 2017. All rights reserved.

Douglas Keith ChristensenSeptember 23, 1947 – August 20, 2016

Dedicated To Our Dear

Friend, Leader, and

Mentor

Contact Billie Zidek at [email protected] for information on how to obtain a copy of the draft standard.

Thank youAna Thiemer & Deke Smith

Co-Chairs of APPA TCO Working Group

Copyright ©APPA 2017. All rights reserved.

Study Guide of the 13 TCO Key Principles

Copyright ©APPA 2017. All rights reserved.

Review of the Key Principles1. Provide an overall review of the Key Principle(s)

a) Does this Key Principle(s) make sense?b) Do you agree with this Key Principle?c) Is the Key Principle(s) missing anything?

2. Provide a review of the Key Principle(s) relationships a) Are the relationships between the Key Principles noted appropriately?

Why or why not?b) Are the relationships between other standards noted appropriately?

Why or why not?3. Provide a review of the Key Principles as it relates to implementation at

your organizationa) What is your perception on how easy the TCO Key Principle would be to

implement at your institution/organization? Why?b) What will be needed to implement TCO at your institution/organization?c) What is vital to include in the implementation phase of the TCO

standard?

This standard establishes the foundational elements and structure required to implement the principles of Total Cost of Ownership (TCO). TCO is a transparent, holistic, and efficient approach to asset management and resource allocation. This standard outlines the process for owners and managers of built assets to produce the greatest possible return on investment and allows for effective use of limited resources. This TCO standard is designed for Owners, Financial Operators, and Facility Professionals. This TCO standard has a focus on critical data elements needed to make well-timed, current and predictive decisions. This common framework would support forecasting investment needs, and simplify data decision requirements by creating and utilizing a standard data set, for purposes of maintaining a financially sustainable future for all asset investments. These TCO critical data elements are designed to be neutral and adapt to any system or process. This standard is comprised of two parts: (1) Key Principles (this document) and (2) Implementation (future part). Making the TCO standard a part of the way your business and management process treats investments and asset management is an important step in the stewardship of any organization’s capital assets.

Standard Abstract

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.

Executive Summary• Facilities have become increasingly more complex as the needs of organizations,

communities, individuals, and relationships transform to remain current with major trends in higher education, business enterprise, and commercial development. Rising construction and operational costs, regulatory requirements, increasing competition to attract and retain personnel, increasing programmatic needs, more complex requirements, and technological developments make for many opportunities and challenges. The often-limited financial investments made in the past add complexity to these opportunities and challenges for the future built environment. Current facility financial plans face extreme cost imbalances, largely because of the insufficient strategies of the past. Facilities professionals face a challenging financial management arrangement - supporting an organization’s mission by sustaining and optimizing the facilities and general site and infrastructure of a portfolio within an inadequate budget. For both the new built environment and the care of existing facilities and assets, a new approach is required to match new opportunities and challenges.

• Total Cost of Ownership (TCO) provides a comprehensive approach to balancing both financial management and facilities management of an organization. While TCO has long been a vision, few have implemented the concept. One reason may be a lack of standards for TCO. With a TCO standard, institutions can develop policy to mandate a more holistic approach to the financial management of assets. Since facility owners finance, build, operate, maintain and ultimately dispose of their facilities; a TCO approach is a natural and critical step for sound fiscal management. A trusted TCO standard will provide a transparent, holistic, and efficient approach to financial management, asset management, and resource allocation. This helps to optimize Return on Investment (ROI) for the effective and sustainable use of capital resources by improving owners’ resource allocation decision-making processes.

A holistic approach to maximizing return on investment of managed physical assets that includes the summation of all known and estimated costs to include first, recurring, renewal / replacement and end-of-useful life costs revised at critical decision points to aid in life-cycle asset management decisions.

TCO – PROPOSED - Definition

Copyright ©APPA 2017. All rights reserved.

Please note this is a pre-decisional TCO definition and not yet the product of the APPA 1000 committee.

Vision TCO begins with identifying the assets to be included. Every asset associated with the management of facilities and infrastructure is candidates considered for inclusion in a TCO analysis. MissionA complete set of defined assets aligned with the organization’s mission creates the foundation of TCO. This foundation serves as the starting point for all TCO principles to support organizational objectives, goals, and organizational value (such as profit and customer satisfaction).PurposeThe purpose of this principle is to identify the assets that become the foundation for TCO. To manage assets effectively, assets shall be identified, inventoried, and prioritized. While organizations exist at various levels of maturity and with various needs, the purpose of this principle enables the organization to manage assets, thus enabling methods to track TCO and provide significant value for the organization.When RequiredThis principle is foundational to TCO and shall be implemented as the first planned program of TCO. Without this principle, TCO cannot be implemented.

Principle 1 - Managed Asset (Sect 3.3.1)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

Vision

A complete asset inventory provides the foundation for owners to track cost and performance of assets over time to make the right decision regarding the life-cycle of the asset. The asset inventory provides the central repository of all assets, identified in Assets Managed (3.3.1), from which all other data points and information connect [Global Location Hierarchy (3.3.3), Asset Classification (3.3.4), Asset Costing (3.3.5), Asset Inspection (3.3.6), and Asset Performance (3.3.7)], and from which decisions and strategies are derived (Asset Decision (3.3.8), Asset Annual Funding (3.3.9), Asset Comprehensive Plan (3.3.10), Asset Reporting (3.3.12).

Mission

The foundation established in the asset inventory allows for the joining of all other data and / or for the development of strategies. Each organization’s mission will vary. The asset inventory supports a strategic plan aligned with that mission.Assets shall be housed in a comprehensive database or central repository so that all other principles build onto the asset to make data driven decisions from a financial, risk and ROI perspective.Purpose

The purpose of this principle is to identify every asset that will become the basis for all other principles and house them within a central repository. The Asset Inventory is the foundation to support all other TCO principles. The assets identified in this principle become the source from which all other information, data, and strategies are bound.

A comprehensive asset inventory is required to determine staffing requirements as well as other O&M needs, renewal or replacement costs, end of life costs and expectancy or other timeline projections from a life-cycle perspective.When Required

A comprehensive Asset Inventory is the basis for TCO and is a requisite to implement and execute all other TCO Principles. The Asset Inventory should include every asset managed.

Principle 2 - Asset Inventory (Sect 3.3.2)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

Vision

Location is a key element of an asset and differentiates similar assets from other assets. The hierarchical aspect of location identifies that an asset is part of a larger entity. The Global Location Hierarchy Principle allows for a similar asset in a different location to have different parameters associated with the respective asset, allowing costs to differ over the individual asset’s life-cycle. Such as a room is part of a floor, is part of a structure, is part of a campus, is partof a county or locality, is part of a state, and is part of a country.

Mission

Each organization’s mission varies; and therefore, aspects of their mission track independently. However, spatial information provides an organizational structure that allows for variance while still providing a roll up of information to a higher level of asset management, which provides an overview of the entire portfolio. In addition, some assets may have multiple roles. Location will identify the asset as a unique entity even though it may have multiple functions. Such as a room assigned to a department or college and assigned to a project, it is still the same unique room.

Purpose

The purpose of this standard is to define ALL spaces associated with a facility / campus in a global hierarchy geographic plane. All fixed assets need a location. Managing multiple properties or campuses in various global locations require a unique identifier for each asset. Similar to space management in a structure, location is required outside the structure for roads, parking, utility distribution lines, sidewalks, etc. All properties and assets would include a global location hierarchy to ensure the management and tracking of each asset.

When Required

This principle is required in all cases since each asset’s location and instance needs to be uniquely identified.

Principle 3 - Global Location Hierarchy (Sect 3.3.3)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

Vision

Standardized classification provides the means to increase the ease of access and use of information by providing consistency to compare and benchmark similar or dissimilar assets in an organization’s portfolio. Asset Classification will enhance the trust and transparency of information and data by enabling drill down, roll up, and grouping for comparison, leveraging the ability to support the best decisions across the life-cycle of the asset. With a standardized approach, a broader and easier understanding of information and analysis is achieved, and there is a potential for reductions in implementation (i.e. training costs) due to consistent tools across all settings. These outcomes will reduce costs and time, and improve asset information quality, resulting in increased ROI.

Mission

A standardized asset classification establishes a common method to store and view data and information to best enable full life-cycle asset management, timely and accurate decision-making, and increased cost efficiencies through cost and time reductions. Standardized asset classification leverages the comparison of data and information between buildings, empowering communication, and data sharing between participants, organizations, and projects.

Purpose

The purpose of this principle is to provide a uniform approach and standard throughout the facility or project life-cycle and to deliver useful and usable methods for establishing a consistent level of asset classification. Asset Classification directly links to Managed Asset (3.3.1), Asset Costing (3.3.5), Asset Inspection (3.3.6), and Asset Performance (3.3.7). With Asset Classification, the information is organized and categorized to manage the asset to inform decision making across the entire portfolio.

Asset Classification enables conducting longitudinal studies that support different types of TCO analysis and measurement [see also Asset Decision (3.3.8), Asset Annual Funding (3.3.9), Asset Comprehensive Plan (3.3.10), and Asset Reporting (3.3.13). Uniformity enables the organization to ensure data management and verification (see also Data Management and Verification (3.3.13)] is uncomplicated, easy to update and easy to use. The Asset Information Sharing (3.3.11) principle integrates with this principle. Asset Information Sharing (3.3.11) is most effectively implemented when the data classification remains consistent across the organization.

When Required

This standard benefits all assets throughout an asset’s life-cycle. Asset Classification should apply to all Managed Assets (3.3.1).

Principle 4 - Asset Classification (Sect 3.3.4)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

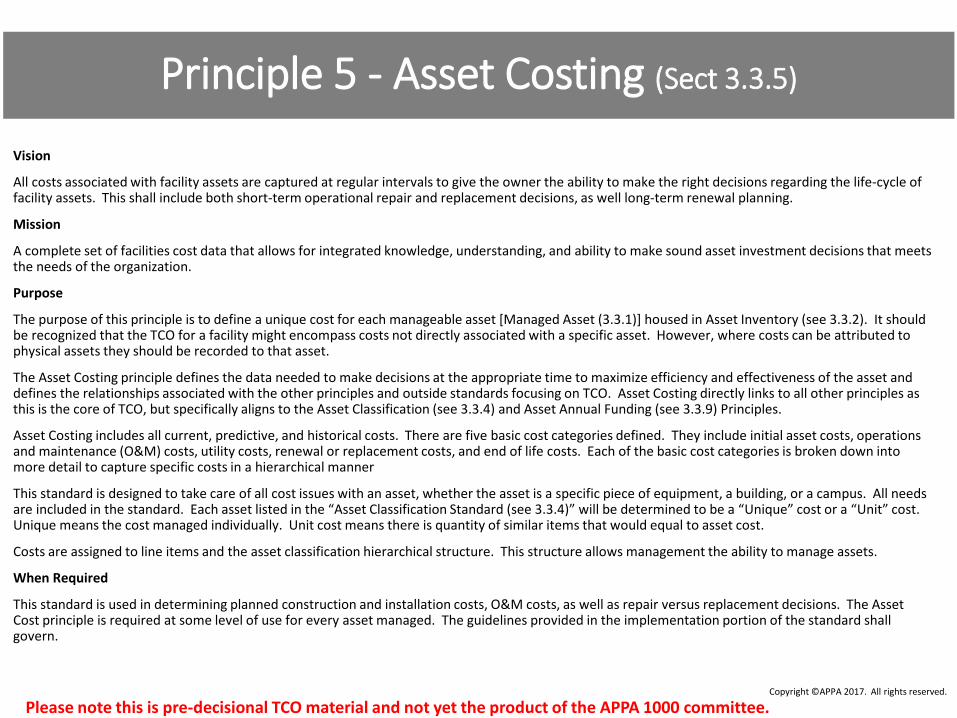

Vision

All costs associated with facility assets are captured at regular intervals to give the owner the ability to make the right decisions regarding the life-cycle of facility assets. This shall include both short-term operational repair and replacement decisions, as well long-term renewal planning.

Mission

A complete set of facilities cost data that allows for integrated knowledge, understanding, and ability to make sound asset investment decisions that meets the needs of the organization.

Purpose

The purpose of this principle is to define a unique cost for each manageable asset [Managed Asset (3.3.1)] housed in Asset Inventory (see 3.3.2). It should be recognized that the TCO for a facility might encompass costs not directly associated with a specific asset. However, where costs can be attributed to physical assets they should be recorded to that asset.

The Asset Costing principle defines the data needed to make decisions at the appropriate time to maximize efficiency and effectiveness of the asset and defines the relationships associated with the other principles and outside standards focusing on TCO. Asset Costing directly links to all other principles as this is the core of TCO, but specifically aligns to the Asset Classification (see 3.3.4) and Asset Annual Funding (see 3.3.9) Principles.

Asset Costing includes all current, predictive, and historical costs. There are five basic cost categories defined. They include initial asset costs, operations and maintenance (O&M) costs, utility costs, renewal or replacement costs, and end of life costs. Each of the basic cost categories is broken down into more detail to capture specific costs in a hierarchical manner

This standard is designed to take care of all cost issues with an asset, whether the asset is a specific piece of equipment, a building, or a campus. All needs are included in the standard. Each asset listed in the “Asset Classification Standard (see 3.3.4)” will be determined to be a “Unique” cost or a “Unit” cost. Unique means the cost managed individually. Unit cost means there is quantity of similar items that would equal to asset cost.

Costs are assigned to line items and the asset classification hierarchical structure. This structure allows management the ability to manage assets.

When Required

This standard is used in determining planned construction and installation costs, O&M costs, as well as repair versus replacement decisions. The Asset Cost principle is required at some level of use for every asset managed. The guidelines provided in the implementation portion of the standard shall govern.

Principle 5 - Asset Costing (Sect 3.3.5)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

Vision

The continuous assessment of the condition of assets aligns the anticipated condition of an asset to the actual condition of an asset to provide clarity for the management of those assets and the allocation of resources.

Mission

The Asset Inspection shall determine the current physical condition and the life-cycle / service life of assets to provide baseline data, benchmarks and metrics by which the organization can efficiently plan and cost effectively manage the following aspects of the asset:

Executive Management (capital funding, strategic planning, risk analysis)

Fiscal Planning (program oversight, budget projections, scenarios planning, asset disposal)

Strategic Management (program execution, cost accounting, procurement)

Asset Management (condition management, project planning, needs prioritization)

Purpose

Asset Inspection is the task of surveying or assessing the physical condition of an asset, to create data that can be used in the efficient and effective management (governance) of that asset over its life-cycle. Regularly updating asset condition assessment data will ensure that the decision-making process will improve the governance of the life-cycle of assets and increase an asset’s return on investment.

When Required

Asset inspection is a continuing task that can be performed in isolation or along with other tasks when visiting an asset in the field. Having accurate condition assessments is critical to accurate TCO evaluations and is performed after the procurement of an asset and the identification of the asset in Managed Asset (3.3.1). Thereafter, continuous asset inspections should occur on a regularly scheduled interval appropriate to the organization.

Principle 6 - Asset Inspection (Sect 3.3.6)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

VisionAssessing an asset’s performance throughout an asset’s life-cycle provides the metrics to improve resource allocation and strategic decision-making processes. MissionA comprehensive and complete set of performance definitions, metrics, and references that meet the needs of the organization enables sound asset investment decisions. These decisions rely on true and accurate asset condition. PurposeThe purpose of this principle is to define processes for collecting asset performance data and metrics. Performance data provides transparency for business decisions related to an asset’s position in its life-cycle, and business decisions related to current and anticipated costs. Understanding the point within the asset life-cycle is critical for making key strategic financial decisions, and understanding reliability of assets or asset systems. Performance metrics are also critical in defining when assets warrant additional maintenance, refurbishment, rehabilitation, or replacement. Asset Performance has a direct correlation to Asset Costing (3.3.5), particularly (but not inclusive) to utility cost, operations and maintenance cost, replacement / renewal cost, and end of life cost (refer to section 3.3.5 for definitions). When RequiredAsset Performance is required for continuous evaluation of all assets during the operational life-cycle. Performance metrics will provide feedback on asset state / stage of life-cycle, operating cost (includes utility use, routine maintenance, unscheduled repair maintenance, etc.), reliability, and deviation from expected outcomes.

Principle 7 - Asset Performance (Sect 3.3.7)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

Vision TCO analysis enables organizations to make efficient and effective use of their assets achieving desired goals and objectives. This analysis requires clearly defined decision-making objectives and methodologies in order manage risk and resources delivering needed asset capabilities and performance enabling organizational goals and objectives achievement.MissionDevelopment and delivery of a TCO analysis within a well-defined decision-making context and methodology will measurably advance achievement of organizational goals and objectives dependent on built assets. PurposeThe purpose of this principle is to ensure risk and resource management activities are focused and well organized at every decision making level and integrated throughout the decision-making spectrum in order to deliver mission enabling capabilities and performance most helpful to achieving desired organizational goals and objectives.When RequiredThis principle is required whenever TCO is being used for decision making at any stage of the facility or asset life.

Principle 8 - Asset Decision (Sect 3.3.8)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

VisionAsset Annual Funding identifies an annual asset cost budget and actual asset expenses for the planned / expected and actual life of the asset. The period is typically a rolling twenty-five-year period. This is a projection and although it supports an annual budget request, it is not limited by any annual funding limitations.MissionOrganizations require a planned and deliberate approach to utilize the funding allocations they receive. Asset Annual Funding identifies the required annual asset management budget and expenses that supports the intended use, expected life, and level of service required from the asset.

PurposeThe purpose of this principle defines and projects annual operations and maintenance (O&M) and capital funding needs for any required planning horizon (typically 25 years) for the life of the asset. This principle utilizes data from Asset Costing (3.3.5), Asset Inspection (3.3.6), and Asset Performance (3.3.7) to develop an Asset Annual Funding plan. When RequiredAsset Annual Funding is the plan to identify the necessary funding to cover the TCO of the asset for the next fiscal year and is developed annually for an organization. The plan will identify annual expenses and periodic renewal investments. The plan will anticipate the level of maintenance services and expense to support the asset’s life.

Principle 9 - Asset Annual Funding (Sect 3.3.9)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

VisionAn Asset Comprehensive Plan provides a total view of the assets by providing a look at the current conditions, projected future growth, maintenance, and space needs. Asset Comprehensive Plan is the key output for owners’ resource allocation decision-making process.MissionThe Asset Comprehensive Plan aligns with the organization’s mission to identify and prioritize the required projects needed to reach the organization’s target asset performance metrics. For example, some facilities professionals may use a target Facilities Condition Index (FCI) will others may use a target asset performance rating. PurposeThe Asset Comprehensive Plan aligns with the organization’s mission to dictate the required projects needed to reach the organization’s target asset performance metrics. For example, some facilities professionals may use a target Facilities Condition Index (FCI) will others may use a target asset performance rating. When RequiredAn asset comprehensive plan is critical to taking on a TCO strategy as one needs to understand the overall plan in order to be effective.

Principle 10 - Asset Comprehensive Plan (Sect 3.3.10)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

VisionA core set of data about each asset that is required across an organization is common, including such things as cost, age, and capacity, where some is unique to specific purposes and these purposes include sensitive, confidential uses such as those that could influence safety and security. Data that is not sensitive or confidential should be available for use by staff with a need in order to produce (a) the greatest efficiencies and effectiveness in the use of resources and (b) accuracy in data use. Sharing of asset data as needed enhances transparency and improves trust in resource allocation and other decision-making processes. Sharing of core data, as needed, will also alleviate duplication of efforts and produce the greatest possible ROI. MissionAsset data sharing will optimize the use of organizational resources including data from legacy systems and be the basis of building trust, when metadata is also shared, among staff, customers, and other organizational stakeholders by:

• Minimizing data entry• Eliminating duplication of effort• Enhancing accuracy• Improving accessibility

The resulting organizational efficiencies reduce cost, minimize the time to access and validate data, and improve effectiveness and accuracy in decision-making and resource allocation.Asset data sharing also facilitates performance reporting to improve stakeholder outcomes and ROI.Sensitive and confidential asset data cannot be shared; and as a result, unauthorized individuals must adopt appropriate precautions to protect the data from access. The resulting framework for data sharing will address the security imperative.PurposeThe purpose of this principle is to define a framework with associated processes to share current, reliable information aboutassets and the organization to authorized individuals for planning and decision-making so that organizational resources are optimized, and assets effectively meet their intended functionality at any point in time to deliver optimum ROI.

When RequiredThe framework and processes for data sharing should be developed as early as possible, especially in the design / specification / scoping phase, and preferably before an asset is acquired. The principle should be revisited periodically and updated as necessary to meet the organization’s need for data analysis and reporting and to maintain appropriate levels of confidentiality and security throughout the life-cycle of the asset. If ownership of assets is transferred, accommodation should be made for the transfer inownership of data as well.

Principle 11 - Asset Information Sharing (Sect 3.3.11)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee.Copyright ©APPA 2017. All rights reserved.

VisionTimely and meaningful asset reporting ensures that accurate information about assets is available to decision-makers at strategic, tactical, and operating levels to satisfy organizational needs for effective planning, efficient resource management, risk management, resiliency, continuous improvement, and to produce the greatest possible ROI. MissionAsset Reporting provides alignment between organizational mission and the asset’s contribution to that mission. Asset Reporting ensures asset value is accurately assessed throughout an asset’s life-cycle and that decision-making is appropriate to current condition, performance, expectations, and corporate contribution. This principle establishes a means for validation, or modification, of plans and decisions, just in time, to achieve the greatest ROI at the lowest cost and an asset-centric framework for performance measurement. PurposeThe purpose of the principle is to define a framework with associated processes that facilitates the continuous availability of current, reliable information about assets and the organization for planning and decision-making so that an asset meets its intended functionality at any point in time and delivers optimum ROI. Asset Reporting provides transparency to personnel responsible for assets at each level within the organization and shares data (Asset Information Sharing 3.3.11) among interested parties to improve the management of the built asset throughout its life-cycle. Frequent, meaningful asset reporting ensures responsibility in the care of corporate and / or public assets.When RequiredAsset Reporting shall be for internal or external use and / or for regulatory or non-regulatory requirements. Requirements of the individual Asset Reports shall be determined in some cases by external and / or regulatory requirements. For each asset, this principle begins to be applied before the asset is acquired, especially during the design / specification / scoping phase, and is intended to end when ownership of the asset has been transferred outside of the enterprise.

Principle 12 - Asset Reporting (Sect 3.3.12)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee. Copyright ©APPA 2017. All rights reserved.

VisionThe successful management and verification of data collected produces the best and most accurate long and short-term decision-making, for first cost, life-cycle projections, renewal, and operations and maintenance. Accurate data and the maintenance of the data convey trust. Trust produces greater efficiencies and opportunities for timely and appropriate decision making, funding and risk mitigation.MissionAccurate data and the continued maintenance of that data provide the ability to meet an organization’s mission. Organizations strive for transparency and a reliable basis for comparative analysis. When an organization bases decisions on accurate, reliable and transparent information or data, trust is gained to make the best decisions in alignment with an organization’s mission. PurposeThe purpose of this standard is to establish trust in the information by managing and verifying data to increase access of information to owners and responsible parties on the impact of decisions at all stages of building conception, design, construction, operations, renewal, and disposal. Trust of the information is required to understand the full impact of choices in building design and operations for transparency and accountability of the decision makers and in understanding and minimizing the total cost of ownership.

When NeededThis principle ensures the integrity of data and is needed at all times from the onset of a buildings conception, through design, during budgeting consideration, through maintenance and operations, during renewal decision making processes, and to the end of the life of the asset. Data integrity is essential to the implementation of TCO.

Principle 13 - Data Management and Verification(Sect 3.3.13)

Please note this is pre-decisional TCO material and not yet the product of the APPA 1000 committee. Copyright ©APPA 2017. All rights reserved.