topper sample paper 4 - k.ramasamy's blog for cbse ... · 236 accounts–xii topper sample...

TRANSCRIPT

236 237Accounts–XII TOPPER Sample Papers236 237Accounts–XII TOPPER Sample Papers

TOPPER SAMPLE PAPER 4

ACCOUNTANCY XII

Time Allowed - 3 Hrs. Max. Marks - 80

General Instructions:-1. This question paper contains two parts A & B only.2. All parts of questions should be attempted at one place.3. There is internal choice in some questions.

PART – A

Q 1. How & where would you record ‘Match expenses’ if ‘Match fund’ is maintained in the books of Not- for- profit organisation? (1)

Q 2. In the absence of any provision in the partnership deed, at what rate, interest on capital and interest on loan will be allowed? (1)

Q 3. Give the circumstances, when there is a need to change the profit sharing ratio. (1)

Q 4. Explain the accounting treatment of goodwill when a new partner brings his share of goodwill in cash. (1)

Q 5. What is meant by issue of debentures as “collateral security”? (1)

Q 6. On the basis of the following information calculate the amount that will be shown against the item “sports material used” in the income and expenditure account of the sports club for the year ended 31-03-02.

1-4-01 31-03-02

Stock of sports material 12,000 5,200

Creditors of sports material 8,000 2,000

Amount paid for the sports material during the year 2001-2002= Rs 43,200 (3)

Q 7. State the exceptions to the creation of Debentures Redemption Reserve as per SEBI guidelines. (3)

Q 8. 300 equity shares of Rs 100 each (Rs 80 called up) were forfeited for the non – payment of allotment money of Rs 40 per share. The forfeited shares were reissued for Rs 90 as fully paid up. (3)

Q 9. A,B and C have fixed capital of Rs 36,000, Rs 27,000 and Rs 18,000 respectively. For the year 2006 profit amounting to 36000 were distributed but interest on capital was credited to them @12% instead of 10%. Give necessary adjusting entry. Show your workings clearly. (4)

Q 10. X, Y and Z are partners in the firm sharing profits in the ratio of 3:2:1. Z retired and the new profit sharing ratio between X and Y was 1:2. On Z’s retirement the goodwill of the firm was valued at Rs 30,000. Pass the necessary journal entry for the treatment of goodwill on Z’s retirement and also calculate the gaining ratio Of remaining partners. (4)

Q 11. Y ltd. with an authorised capital of Rs 1,00,000 in Shares of Rs 100 each ,issued 500 of such shares, payable Rs 25 per share on application, Rs 25 on allotment , Rs 20 on first call and balance payable as and when required. All money payable on application and allotment was duly received but when the call of Rs 20 per share was made, one shareholder holding 25 shares failed to pay the amount due and another shareholder holding 50 shares paid the entire amount due on shares along with the first call. Journalise. (4)

238 239Accounts–XII TOPPER Sample Papers238 239Accounts–XII TOPPER Sample Papers

Q 12. (a) R Ltd acquired assets of RS 20,00,000 and took over creditors of Rs 2,00,000 from K Ltd. R Ltd issued 8% debentures of Rs. 100 each at a premium of 25%, as purchase consideration. Journalise.

(b) What journal entries should be made for the issue and redemption of debentures if X ltd issued 30,000,12% debentures of Rs 100 each at par redeemable at a premium of 5%. (3+3)

Q 13. From the following Receipts & Payment A/c of Ronic club and additional information, prepare Income & Expenditure A/c for the year ending 31st December 2006 and balance sheet as on that date:

RECEIPTS AMT (Rs.) PAYMENT AMT (Rs.)

To balance b/d 14,350 By salaries 20,280

To subscription 61,450 By sports Equipment 46,785

To Interest on Investment @ 9%p.a.

9,000 By balance c/d

17,735

84,800 84,800

(6)

Q 14. A , B and C were partners in a firm sharing profits in a ratio of 5:3:2. On 31.03.06 their balance sheet was as under:

LIABILITIES AMT (Rs.) ASSETS AMT

Creditors 11000 Buildings 20000

Reserves 6000 Machinery 30000

A’s capital 30000 Stock 10000

B’s capital 25000 Patents 11000

C’s capital 15000 Debtors 8000

Cash 8000

87000 87000

A died on October 1,2006. It was agreed between his executors and the remaining partners that

a) goodwill of the firm valued at Rs 37500.

b) patents be valued at Rs 8000; machinery at Rs 28000 and Building at Rs 25000.

c) profits for the year 2006-07 be taken as having accrued at the same rate as that of the previous year which was Rs 15000.

d) interest on capital @ 10%p.a.

Prepare A’s capital a/c & Revaluation a/c. (6)

Q 15. R Ltd offered 20,000 shares of Rs 10 each at 10% discount payable as

On application – Rs 6

On allotment – Rs3

Public has applied for 32500 shares. Shares were allotted on pro-rata basis to the applicants of 25000 shares .Money overpaid on application was adjusted against sum due on allotment.All the shareholders have paid the amount due except Mohan , the allotee of 4000 shares. His shares were forfeited, all the forfeited shares were reissued for Rs 35,000 as fully paid up. Journalise the above transactions.

238 239Accounts–XII TOPPER Sample Papers238 239Accounts–XII TOPPER Sample Papers

OR

K ltd invited applications for 20,000 shares of Rs 10 each, payable Rs 3 on application & balance on allotment. Applications were received for 25000 shares. It was decided

a) to refuse allotment to the applicants of 1000 shares.

b) to allot in full to the applicants of 4000 shares.

c) to allot balance of the available shares pro rata among the other applicants.

d) to utilise excess application money in part payment of allotment money.

Ramesh , holder of 100 shares to whom shares was allotted on pro rata basis failed to pay the allotment money. His shares were forfeited and subsequently reissued as fully paid up for Rs 9 per share. Journalise . (8)

Q 16. The balance sheet of A,B and C who were partners sharing profits in ratio 2:1:1 as on 31.03.03 was as follows:

LIABILITIES AMT ASSETS AMT

Creditors 21000 Buildings 100000

reserves 20000 Machinery 50000

A’s capital 80000 Stock 18000

B’s capital 40000 Debtors 20000

C’s capital 40000 Less P/D/D 1000 19000

Cash 14000

201000 201000 On that date B decided to retire from the firm on the following terms:

a) Buildings to be appreciated by 20%.

b) P/D/D to be increased to 15% on debtors.

c) Machinery to be depreciated by 20%.

d) Goodwill of the firm valued at Rs 72000.

e) The capital of the new firm be fixed at Rs 1,20,000.

Prepare Revaluation A/c , Capital A/c’s of the partners and Balance sheet after B’s retirement.

OR

A & B were partners in a business sharing profits & losses in the ratio of 3:1. They decided to dissolve the partnership on 31.03.03. On that date, their capital stood at Rs.1,00,000 and Rs.50,000 respectively. Amount owing by A to the firm was Rs.42,000 and the amount owed by the firm to B was Rs.15,000; Creditors were Rs.25,000 and cash Rs.5,000. The assets other than the amount owing by A to the firm realized Rs.64,000. The expenses of realization amounted to Rs.1,000.

Prepare Memorandum Balance Sheet. Realisation A/c , Partners’ Capital A/c’s and Cash A/c. (8)

PART – BANALYSIS OF FINANCIAL STATEMENT

Q 17. The Quick Ratio of a company is 2:1, State giving reasons whether the ratio will improve, decline or will have no change in case of purchase of goods for cash. (1)

240 241Accounts–XII TOPPER Sample Papers240 241Accounts–XII TOPPER Sample Papers

Q 18. Mention the net amount of ‘Source’ or ‘Use’ of cash when Rs19000 was received from a debtor and discount allowed to him was Rs 1000. (1)

Q 19. Payment of income tax is classified under which activity while preparing cash flow statement? (1)

Q 20. What is a contingent liability? Where is it shown in the Balance sheet? Give two examples. (3)

Q 21. Prepare a comparative income statement from the following:

(Rs) 2005 (Rs) 2006

Sale 800000 1000000

Cost of goods sold 480000 620000

Indirect expenses 80000 110000

Income tax 50% 50% (3)

Q 22. A) Calculate Total Assets to Debt ratio

Total Debts : Rs 900000 , Capital employed : Rs 1100000, Current liabilities: Rs 100000.

B) Calculate stock if:

Current Ratio = 4, Quick Ratio = 3 and Working capital Rs 108000. (4)

Q 23. From the following Balance Sheets, prepare a Cash Flow Statement.

Liabilities 2005 2006 Assets 2005 2006

Eq. share capitalProfit& Loss A/cGeneral ReserveLoanCreditors

45,000 --- 5,00010,00018,700

65,00015,000 7,50020,00011,000

Fixed AssetsStockDebtorsBankPreliminary Exp. Profit& Loss A/c

46,000 6,00018,000 2,000 1,700 5,000

83,00013,00019,500 2,500 500

__

78,700 1,18,500 78,700 1,18,500

Additional Information:

During the year depreciation on fixed assets was Rs.11,700

1. Match expenses will be deducted from Match Fund in Liabilities side of the closing Balance Sheet. (1)

2. No interest is allowed on capital and interest is allowed on partner’s loan @ 6% p.a. (1)

3. (a) At the time of admission of a partner

(b) At the time of retirement or death of a partner (1/2 x 2)

4. Journal Entries

Date Particulars L.F. Rs.(Dr.) Rs.(Cr.)

Cash A/c Dr. To Premium A/c(Being cash brought in by new partner for his share of goodwill)

240 241Accounts–XII TOPPER Sample Papers240 241Accounts–XII TOPPER Sample Papers

Premium A/c Dr. To Sacrificing partners’ capital A/c (Being new partner’s share of goodwill distributed by the sacrificing partners in sacrificing ratio)

(1/2 x 2)

5. Collateral Security means secondary(additional) security in addition to the principal security.

(1)

6. Income & Expenditure A/c for the year ended 31st March, 2002

Expenditure Rs. Income Rs.

Amount paid for sports material 43,200Add: Opening stock 12,000Add: Closing creditors 2,000Less: Closing stock (5,200)Less: Opening creditors (8,000) 44,000

(1/2 x 6)

7. (a) Company which has issued debentures with a maturity period of 18 months or less.

(b) Infrastructure companies are exempted from creating Debenture Redemption Reserve.

(3)

8. Journal Entries

Date Particulars L.F. Rs.(Dr.) Rs.(Cr.)

Share Capital A/c Dr. To Share Forfeited A/c To Calls in Arrears A/c (being shares forfeited)

24,00012,00012,000

Bank A/c Dr.Share Forfeited A/c Dr.To Share Capital A/c (being 80 shares reissued)

27,0003,000

30,000

Share Forfeited A/c Dr. To Capital Reserve A/c (being balance of shares forfeited A/c transferred to capital reserve A/c )

9,0009,000

(1 x 3)

9.

ARs.

BRs.

CRs.

TotalRs.

Amt. already credited (2%)Amt. to be credited (1:1:1)

720540

540540

360540

1,6201,620

Difference (Dr./Cr.) 180(Dr.)

---- 180(Cr.

---

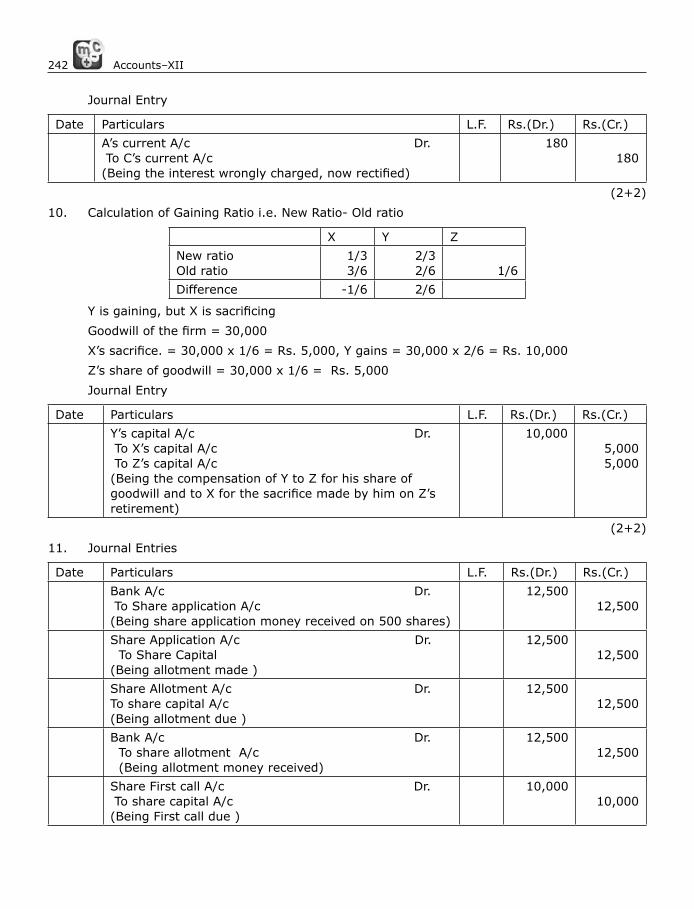

242 243Accounts–XII TOPPER Sample Papers242 243Accounts–XII TOPPER Sample Papers

Journal Entry

Date Particulars L.F. Rs.(Dr.) Rs.(Cr.)

A’s current A/c Dr. To C’s current A/c (Being the interest wrongly charged, now rectified)

180180

(2+2)

10. Calculation of Gaining Ratio i.e. New Ratio- Old ratio

X Y Z

New ratioOld ratio

1/33/6

2/32/6 1/6

Difference -1/6 2/6

Y is gaining, but X is sacrificing

Goodwill of the firm = 30,000

X’s sacrifice. = 30,000 x 1/6 = Rs. 5,000, Y gains = 30,000 x 2/6 = Rs. 10,000

Z’s share of goodwill = 30,000 x 1/6 = Rs. 5,000

Journal Entry

Date Particulars L.F. Rs.(Dr.) Rs.(Cr.)

Y’s capital A/c Dr. To X’s capital A/c To Z’s capital A/c (Being the compensation of Y to Z for his share of goodwill and to X for the sacrifice made by him on Z’s retirement)

10,0005,0005,000

(2+2)

11. Journal Entries

Date Particulars L.F. Rs.(Dr.) Rs.(Cr.)

Bank A/c Dr. To Share application A/c(Being share application money received on 500 shares)

12,50012,500

Share Application A/c Dr. To Share Capital(Being allotment made )

12,50012,500

Share Allotment A/c Dr. To share capital A/c (Being allotment due )

12,50012,500

Bank A/c Dr. To share allotment A/c (Being allotment money received)

12,50012,500

Share First call A/c Dr. To share capital A/c (Being First call due )

10,00010,000

242 243Accounts–XII TOPPER Sample Papers242 243Accounts–XII TOPPER Sample Papers

Bank A/c Dr.Calls in arrears A/c Dr. To share First call A/c To calls in advance A/c (Being First call money received on 475 shares@ Rs.20 per share and Rs. 30 per share on 50 shares received in advance))

11,000500

10,0001,500

(4)

12. (a) Journal Entries

Date Particulars L.F. Rs.(Dr.) Rs.(Cr.)

Assets A/c Dr. To Creditors A/c To K Ltd. (Being R ltd. took over the assets & liabilities of K ltd.)

20,00,0002,00,000

18,00,000

K Ltd. Dr. To 8% Debentures A/c To Securities Premium A/c(Being 8% debentures issued to K Ltd. at premium)

18,00,00014,40,0003,60,000

Note: Debentures issued at premium= 18,00,000/125= 14,400 Debentures

(b) Journal Entries

Date Particulars L.F. Rs.(Dr.) Rs.(Cr.)

Bank A/c Dr. To Debenture application & allotment A/c(Being Debenture application money received)

30,00,00030,00,000

Debenture application & allotment A/c Dr.Loss on issue of debenture A/c Dr. To 12% Debentures A/c To Premium on Redemption A/c(Being application money transferred to Debenture A/c.)

30,00,0001,50,000

30,00,0001,50,000

Profit & Loss Appropriation A/c Dr. To Debenture Redemption Reserve A/c(being Debenture Redemption Reserve created)

15,00,00015,00,000

12% Debentures A/c Dr.Premium on redemption of debenture A/c Dr. To Debentures holders A/c(Being debentures redeemed)

30,00,0001,50,000

31,50,000

Debentures holders A/c Dr. To Bank A/c(Being Debentures holders paid)

31,50,00031,50,000

Debenture Redemption Reserve A/c To general reserve(Being D.R.R. transferred to general reserve)

15,00,000

(3+3)

Income & Expenditure A/c

244 245Accounts–XII TOPPER Sample Papers244 245Accounts–XII TOPPER Sample Papers

13. For the year ending 31.12.06

Particulars Rs. Particulars Rs.

To salariesTo sports Equipment usedOpening stock 21,800Add: purchases 46,785Less: Closing stock 29,700 ________To surplus

20,280

38,88511,405

By Subscription 61,450Add: O/s (end) 560Less: O/s (Beg) 480Add: Adv.(Beg.) 80Less: Adv. (End) 40 ________By interest on investment

61,570

9,000

70,570 70,570

Balance Sheet

As on 31.12. 2006

Liabilities Rs. Assets Rs.

Advance subscription Capital Fund

801,36,550

Cash O/S Subscription Sports EquipmentInvestment(9,000 x 100/9)

14,350480

21,8001,00,000

1,36,630 1,36,630

Balance Sheet

As on 31.12. 2007

Liabilities Rs. Assets Rs.

Advance subscription Capital Fund 1,36,550Add: Surplus 11,405

40

1,47,955

Cash O/S Subscription Sports EquipmentInvestment(9,000 x 100/9)

17,735560

29,7001,00,000

1,47,995 1,47,995

(6)

14. A’s Capital A/c

Particulars Rs. Particulars Rs.

To A’s executor A/c 57,000 By balance b/dBy General reserveBy B’s capital A/cBy C’s capital A/cBy P & L suspense A/cBy Interest on capital(30,000 x 10/100 x 6/12)

30,0003,000

11,2507,5003,750

1,500

57,000 57,000

Revaluation A/c

Particulars Rs. Particulars Rs.

PatentsMachinery

3,0002,000

Buildings 5,000

244 245Accounts–XII TOPPER Sample Papers244 245Accounts–XII TOPPER Sample Papers

5,000 5,000

Goodwill = 37,500

A’s share of goodwill = 37,500 x 5/10 = 18,750

A’s share of profit = 15,000 x 5/10 x 6/12 = 3,750 (6)

15. Journal Entries

Date Particulars L.F. Rs.(Dr.) Rs.(Cr.)

Bank A/c Dr. To Share application A/c(Being share application money received on 32,500 shares)

1,95,0001,95,000

Share Application A/c Dr. To Share Capital To Share Allotment To Bank(Being allotment made to 20,000 shares)

1,95,0001,20,000

30,00045,000

Share Allotment A/c Dr. Discount of issue of shares A/c Dr. To share capital A/c (Being allotment due on 20,000 shares @ Rs3 at a discount of Rs.1)

60,00020,000

80,000

Bank A/c Dr.Calls in arrears A/c Dr. To share allotment A/c (Being allotment money received)

44,0006,000

50,000

Share Capital A/c Dr. To Share Forfeited A/c To Calls in arrears A/c To Discount on issue of shares(Being shares forfeited)

40,00030,0006,0004,000

Bank A/c Dr.Discount on issue of shares A/c Dr.Share Forfeited A/c Dr. To Share Capital A/c(Being forfeited shares reissued)

35,0004,0001,000

40,000

Share Forfeited A/c Dr. To Capital Reserve A/c(Being balance of the forfeited A/c transferred to Capital Reserve)

29,00029,000

Working notes:

Calculation of amount not paid by Mohan on allotment:

i) No. of shares applied by Mohan:

25,000/20,000 x 4,000 = 5,000 shares

ii) Mohan paid application money @ Rs. 6 on 5,000 shares = Rs. 30,000

Less: Application adjusted @ Rs.6 on 4,000 shares = Rs.(24,000)

Money adjusted in allotment 6,000

246 247Accounts–XII TOPPER Sample Papers246 247Accounts–XII TOPPER Sample Papers

iii) Money due on allotment (12,000 – 6,000) = Rs 6,000

Calculation of amount due on allotment:

Total amount due on allotment @Rs 4 on 20,000 shares = Rs. 80,000

Less adjusted from application = Rs.(30,000)

50,000

Less money due form Mohan (6000)

Total money received on allotment Rs. 44,000

OR

Journal Entries

Date Particulars L.F. Rs.(Dr.) Rs.(Cr.)

Bank A/c Dr. To Share application A/c(Being share application money received on 25,000 shares)

75,00075,000

Share Application A/c Dr. To Share Capital To Share Allotment To Bank(Being application money transferred)

75,00060,00012,0003,000

Share Allotment A/c Dr. To share capital A/c (Being allotment due on 20,000 shares )

1,40,0001,40,000

Bank A/c Dr.Calls in arrears Dr. To share allotment A/c (Being allotment money received)

1,27,375625

1,28,000

Share capital A/c Dr. To Share forfeiture A/c To Calls in arrears A/c(Being shares forfeited)

1,000375625

Bank A/c Dr.Share Forfeited A/c Dr. To Share capital A/c(Being shares reissued)

900100

1,000

Share forfeited A/c Dr. To Capital Reserve A/c( Being share forfeited A/c transferred to capital reserve A/c)

275275

(8)

Working notes:

Calculation of amount not paid by Ramesh on allotment:

ii) No. of shares applied by Mohan:

20,000/16,000 x 100 = 125 shares

246 247Accounts–XII TOPPER Sample Papers246 247Accounts–XII TOPPER Sample Papers

ii) Ramesh paid application money @ Rs. 3 on 125 shares = Rs. 375

Less: Application adjusted @ Rs.3 on 100 shares= Rs.(300)

Money adjusted in allotment 75

Money due on allotment (100x7- 75) = Rs 625

75

Calculation of amount due on allotment:

Total amount due on allotment @Rs 7 on 20,000 shares = Rs 1,40,000

Less adjusted from application = Rs. (12,000)

1,28,000

Less money due form Mohan (625)

Total money received on allotment Rs. 1,27,375

16. Revaluation A/c

Particulars Rs. Particulars Rs.

To Provision for doubtful debtsTo MachineryTo profit transferred to

A- 4,000B- 2,000C- 2,000

2,00010,000

8,000

By Buildings 20,000

20,000 20,000

Partners’ Capital A/c

Particulars ARs.

BRs.

CRs.

Particulars ARs.

BRs.

CRs.

To B’s capital To B’s Loan A/c To Cash

To balance c/d

12,000

2,000

80,000

65,0006,000

1,000

40,000

By balance b/d By revaluation ProfitBy A’s capital By C’s capital By ReservesBy Cash (B/fig)

80,000 4,000

10,000

40,000 2,000

12,000 6,000 5,000

40,000 2,000

5,000

94,000 65,000 47,000 94,000 65,000 47,000

Balance Sheet

As on 31.03. 2008

Liabilities Rs. Assets Rs.

CreditorsA’s capital C’s capital B’s Loan A/c

21,00080,00040,00065,000

CashDebtors 20,000Less: P/D/D 3,000 Stock MachineryBuilding

11,000

17,00018,00040,000

1,20,000

2,06,000 2,06,000

Working Notes:

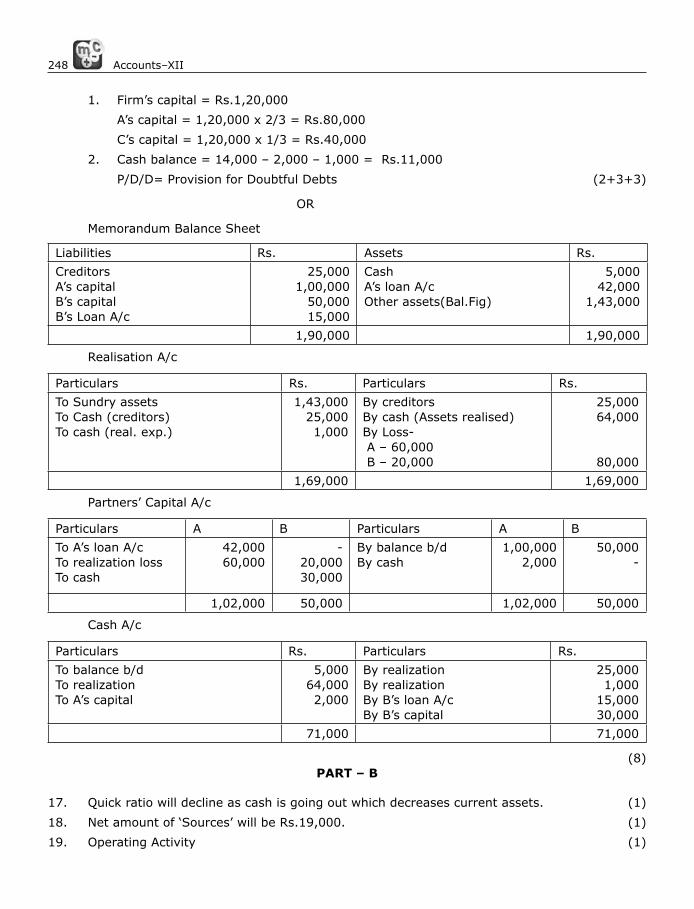

248 249Accounts–XII TOPPER Sample Papers248 249Accounts–XII TOPPER Sample Papers

1. Firm’s capital = Rs.1,20,000

A’s capital = 1,20,000 x 2/3 = Rs.80,000

C’s capital = 1,20,000 x 1/3 = Rs.40,000

2. Cash balance = 14,000 – 2,000 – 1,000 = Rs.11,000

P/D/D= Provision for Doubtful Debts (2+3+3)

OR

Memorandum Balance Sheet

Liabilities Rs. Assets Rs.

CreditorsA’s capital B’s capital B’s Loan A/c

25,0001,00,000

50,00015,000

CashA’s loan A/cOther assets(Bal.Fig)

5,00042,000

1,43,000

1,90,000 1,90,000

Realisation A/c

Particulars Rs. Particulars Rs.

To Sundry assetsTo Cash (creditors)To cash (real. exp.)

1,43,00025,0001,000

By creditorsBy cash (Assets realised)By Loss- A – 60,000 B – 20,000

25,00064,000

80,000

1,69,000 1,69,000

Partners’ Capital A/c

Particulars A B Particulars A B

To A’s loan A/cTo realization lossTo cash

42,00060,000

-20,00030,000

By balance b/dBy cash

1,00,000 2,000

50,000 -

1,02,000 50,000 1,02,000 50,000

Cash A/c

Particulars Rs. Particulars Rs.

To balance b/dTo realizationTo A’s capital

5,00064,0002,000

By realizationBy realizationBy B’s loan A/cBy B’s capital

25,0001,000

15,00030,000

71,000 71,000

(8) PART – B

17. Quick ratio will decline as cash is going out which decreases current assets. (1)

18. Net amount of ‘Sources’ will be Rs.19,000. (1)

19. Operating Activity (1)

248 249Accounts–XII TOPPER Sample Papers248 249Accounts–XII TOPPER Sample Papers

20. Contingent liabilities are liabilities which have not arisen, but may arise upon the happening of a certain event. The amount of contingent liabilities is never shown in the amount column of the liabilities side. These are always stated in the form of a foot-note on the liabilities side. Some examples

(i) Claim against the company not acknowledged as debt

(ii) Uncalled liability on shares partly paid

(iii) Arrears of fixed cumulative dividend (3)

21. Comparative Income Statement

Particulars 2005(Rs.) 2006(Rs.) Absolute change

Percentage

SalesLess: Cost of goods sold

8,00,0004,80,000

10,00,0006,20,000

2,00,0001,40,000

2529.16

Gross profitLess: Indirect expenses

3,20,00080,000

3,80,0001,10,000

60,00030,000

18.7537.5

Net profit before taxLess: Tax payable

2,40,0001,20,000

2,70,0001,35,000

30,00015,000

12.512.5

Net profit after tax 1,20,000 1,35,000 15,000 12.5

(1 x 4)

22. (a) Total assets to debt ratio = Total assets / debts

Debts = Total debts – current liabilities

= 9,00,000 – 1,00,000 = 8,00,000

Total assets = Total debts + capital employed

= 9,00,000 + 11,00,000 = 20,00,000

Total assets to debt ratio = 20,00,000 / 8,00,000 = 2.5 : 1

(b) Working capital = current assets – current liabilities

1,08,000 = C/A – C/L

C/A = 1,08,000 + C/L

Current ratio = C/A / C/L= 1,08,000 + C/L / C/L

4C/L = 1,08,000 + C/L

C/L = 1,08,000/3 = 36,000

C/A = 1,08,000 + 36,000 = 1,44,000

Liquid ratio = L/A / C/L

3 = L/A / 36,000

L/A = 1,08,000

Stock = C/A – L/A = 1,44,000 – 1,08,000 = 36,000 (2+2)

23.

Calculation of Profit before tax

Profit earned during the year = Rs. 20,000

Add: Transfer to reserve = Rs. 2,500

________

= Rs. 22,500

250 251Accounts–XII TOPPER Sample Papers250 251Accounts–XII TOPPER Sample Papers

Cash Flow Statement

Particulars Amount(Rs.) Amount(Rs.)

(A) Cash flow from Operating ActivitiesNet profit before taxAdd: Non operating expenses Depreciation 11,700 Preliminary Expenses 1,200Less: Increase in stockLess: Increase in debtorsLess: Decrease in creditorsOperating profit before taxLess: tax paidCash flow from Operating Activities

12,900(7,000)(1,500)(7,700)

22,500

(3,300)

19,200-------

19,200

(B) Cash Flow from Investing ActivitiesPurchase of MachineryCash used in Investing Activities

(48,700)(48,700)

(C) Cash flow from Financing Activities Issue of share capital Bank loan raisedCash used in Financing Activities

20,00010,000

30,000

Net increase in cash ( A+B+C)Add: Opening balance of cash & equivalentsClosing balance of cash & equivalents

5002,0002,500

Machinery A/c

Particulars Rs. Particulars Rs.

To Balance b/dTo Bank (purchase.)

46,00048,700

By DepreciationBy balance c/d

11,70083,000

94,700 94,700

(6)