topic - refpet.com petchem integration - vinay gupta...delayed coker ebulated bed residue...

TRANSCRIPT

Topic

Integration Opportunities in

Refineries - Petrochemicals

Presented by :

VINAY GUPTA Engineers India Limited

Complexity of Indian refineries

Gross Refinery Margin

Stand Alone

Integrated Complex

Pricing of petrochemical & Refinery products w.r.t crude

Integration Opportunities between refineries & petrochemical

Case Study

AGENDA

3

Lines of Business

Oil & Gas Chemicals & Metallurgy

Infrastructure Power

Oil and Gas

Processing

Offshore & Onshore

Strategic Storage,

Terminals and

Pipelines

Refinery Petrochemicals Fertilizer Mining and

Metallurgy

Solar Thermal Nuclear City Gas Urban

Development

Water and Waste

Management

4

Service Offering - From Concept to Commissioning

Pre-feasibility studies

Technology and licensor selection

Conceptual design & feasibility

Process design package

Process Design

Residual engineering and FEED

Detailed engineering

Engineering for procurement

Engineering for construction

Engineering

Supplier and contractor management

Expediting and inspection

Vendor development

Procurement

Materials and warehouse management

Quality assurance and health, safety &

environment

Progress monitoring/ Scheduling

Mechanical completion

Site closure

Construction Management

Pre-commissioning and commissioning

assistance

Safety audit

Hazard and operability studies

Risk analysis

Commissioning

Integrated project management services with

focus on cost, quality and schedule

Project Management

Environment engineering

Heat and mass transfer

Plant operations and safety management

Specialist materials and maintenance services

Specialized Services

Certification and re-certification services

EIL subsidiary – Certification Engineers

International Limited (CEIL)

Third party inspection

Certification

5

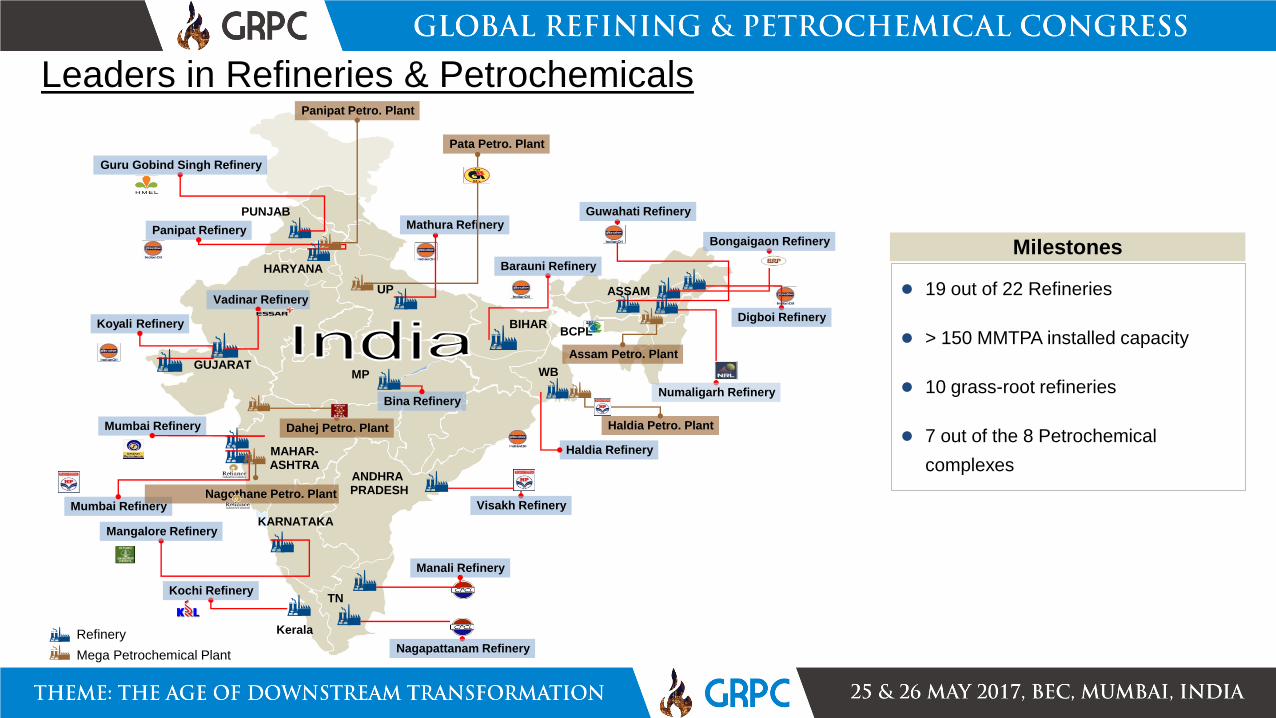

Leaders in Refineries & Petrochemicals

Milestones

19 out of 22 Refineries

> 150 MMTPA installed capacity

10 grass-root refineries

7 out of the 8 Petrochemical

complexes

Refinery

Mega Petrochemical Plant

Koyali Refinery

ASSAM

BIHAR

GUJARAT WB

Haldia Refinery

UP

Panipat Refinery

HARYANA

MAHAR- ASHTRA

Mumbai Refinery

Mumbai Refinery

ANDHRA PRADESH

Visakh Refinery

Kochi Refinery

Manali Refinery

TN

Kerala

Nagapattanam Refinery

Guwahati Refinery

Barauni Refinery

Mathura Refinery

Bongaigaon Refinery

Numaligarh Refinery

Digboi Refinery

Mangalore Refinery KARNATAKA

Vadinar Refinery

PUNJAB

Guru Gobind Singh Refinery

Bina Refinery

MP

Assam Petro. Plant

BCPL

Haldia Petro. Plant

Panipat Petro. Plant

Dahej Petro. Plant

Pata Petro. Plant

Nagothane Petro. Plant

Complexity of Indian refineries

Gross Refinery Margin

Stand Alone

Integrated Complex

Pricing of petrochemical & Refinery products w.r.t crude

Integration Opportunities between refineries & petrochemical

Case Study

AGENDA

1 2

3 4

5 6

7

9

11 12

13 14

15 16

17 18

19 20

21 22

Total number

0.5 1.6

2.6 3.0

4.3 4.6

7.0

8.2

9.4

10.8

6.5

8.3

0

2

4

6

8

10

12

19

01

19

54

19

55

19

57

19

62

19

63

19

65

19

67

19

69

19

74

19

78

19

79

19

82

19

83

19

85

19

88

19

89

19

93

19

95

19

96

19

97

19

98

19

99

20

00

20

02

20

05

20

06

20

08

20

09

20

10

20

11

20

12

20

16

Average Capacity Total Average Capacity PSU

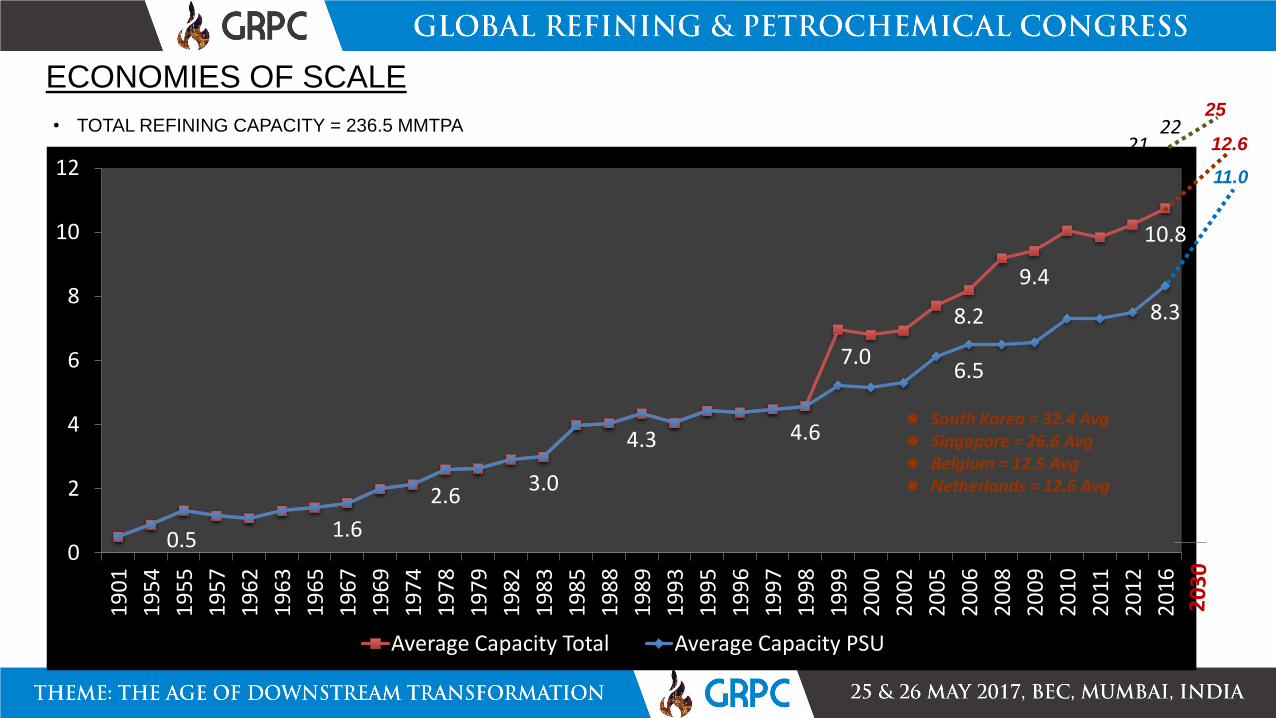

ECONOMIES OF SCALE

• TOTAL REFINING CAPACITY = 236.5 MMTPA

South Korea = 32.4 Avg Singapore = 26.6 Avg Belgium = 12.5 Avg Netherlands = 12.6 Avg

25

12.6

11.0

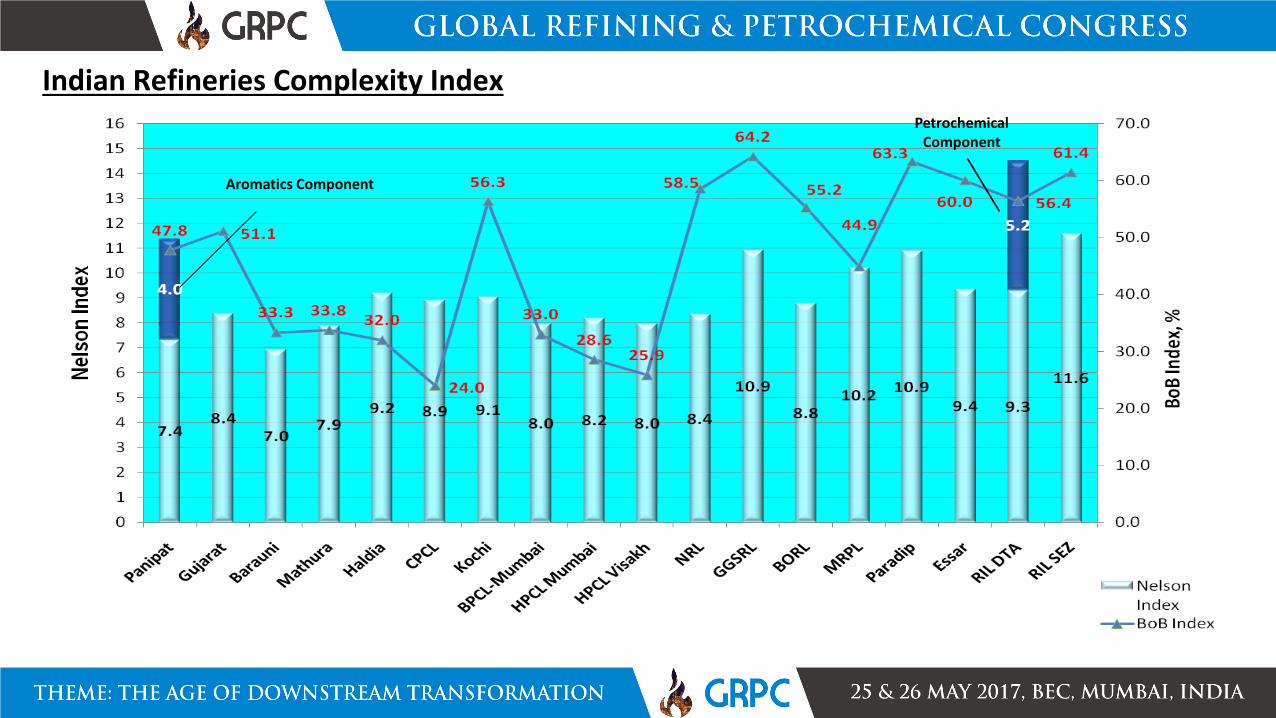

Indian Refineries Complexity Index

Aromatics Component

Petrochemical Component

Complexity of Indian refineries

Gross Refinery Margin

Stand Alone

Integrated Complex

Pricing of petrochemical & Refinery products w.r.t crude

Integration Opportunities between refineries & petrochemical

Case Study

AGENDA

Refinery Margin

ITEM $/ bbl % Contribution

Refined Product Revenue $ 80

Raw Material (Crude) Cost $ 70 87.5 %

Gross Margin $ 10

Energy Cost $ 0.8

2.5 % Marketing Cost $ 0.3

Environmental Operating Cost $ 0.2

Other Refining Costs (Wages, etc) $ 0.7

Net Refining Margin $ 8

Gross Refinery Margin = Price of refined product – Price of crude oil

Net Refinery Margin = Gross Refinery Margin – Refinery Operating Costs – Transportation and Storage

Refining Margin Impact

1

1

$ / B

arre

l

Crude

Pipeline /

COT

Crude Cost Refinery

Configuration

Operating

Expenses

Net Margin PetChem

Integration

+

-

Illustrative Only

Evolution of Value Addition

Hydro skimming Refinery

Secondary Processing

Complex Refinery

Complex Refinery

Residue Upgradation

Petrochemicals Integration

Integrated Refinery-Cum-Petrochemical Complex

Hydrogen Chemicals

Petrochemicals Gasification

Hydrocracker

FCCU

Delayed Coker

Ebulated Bed

Residue Hydrocrackers

PetCoke , Biomass

Aromatics and Olefins

Configuration Impact

Hydro skimming Refinery (1)

Secondary Processing (2)

Residue Upgradation (3)

47

70

84

30

40

50

60

70

80

90

1 2 3

Distillate yield wt% on Crude

Value Addition Through Integration

Complex Refinery (1)

Aromatics Integration (2)

Petrochemical Integration (3)

Integration of refinery & Petrochemicals also improve ROI significantly by ~ 4-5%.

7 8.7

15.7

0

2

4

6

8

10

12

14

16

18

1 2 3

GR

M $

/bb

l

Complexity of Indian refineries

Gross Refinery Margin

Stand Alone

Integrated Complex

Pricing of petrochemical & Refinery products w.r.t crude

Integration Opportunities between refineries & petrochemical

Case Study

AGENDA

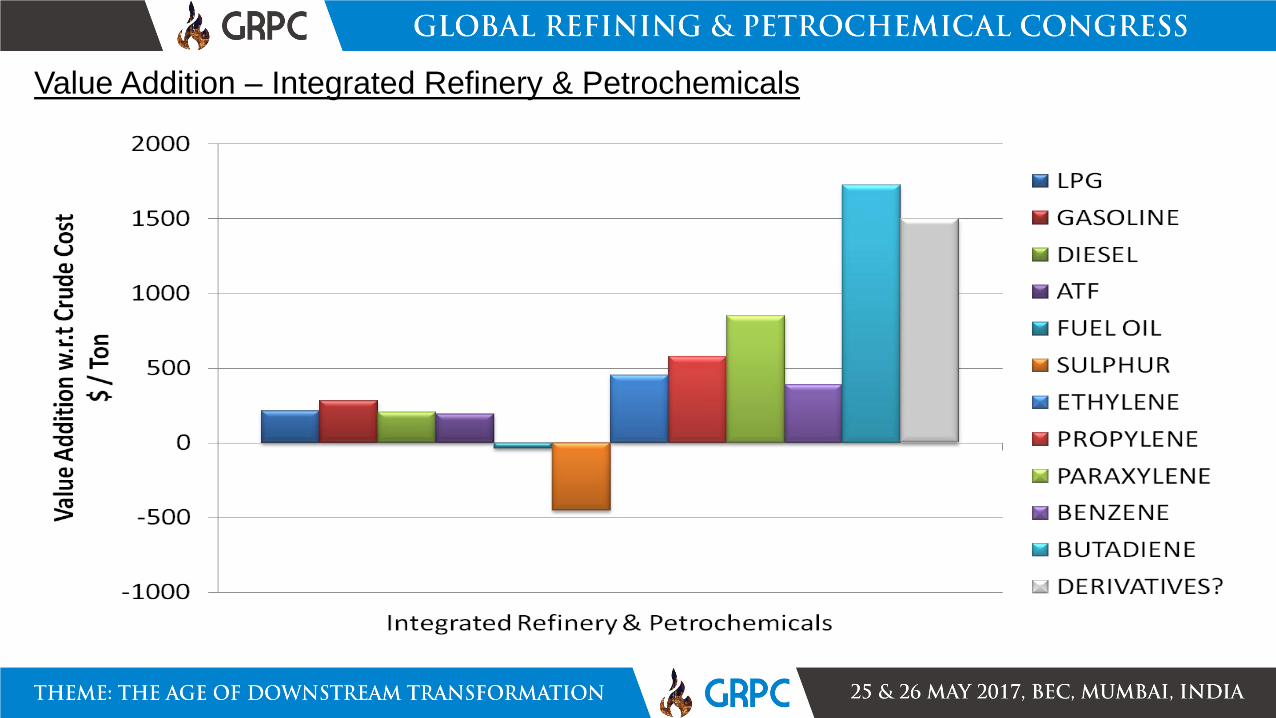

Value Addition – Stand Alone Refinery

Value Addition – Integrated Refinery & Petrochemicals

Complexity of Indian refineries

Gross Refinery Margin

Stand Alone

Integrated Complex

Pricing of petrochemical & Refinery products w.r.t crude

Integration Opportunities between refineries & petrochemical

Case Study

AGENDA

Drivers for Refinery Petrochemical Integration

Premium available in olefins vis-à-vis transportation fuels

Stability over Value chain

Flexibility to the dynamic market demand and Prices

Feedstock and product flexibility

Assured Feedstock's Availability

Absorption of return streams

Upgrade low value refinery streams to high value products

Capital, OPEX and Resource Optimization

Shared Infrastructure, storage & Utilities

Lower logistic & Energy cost

Minimize overhead and waste

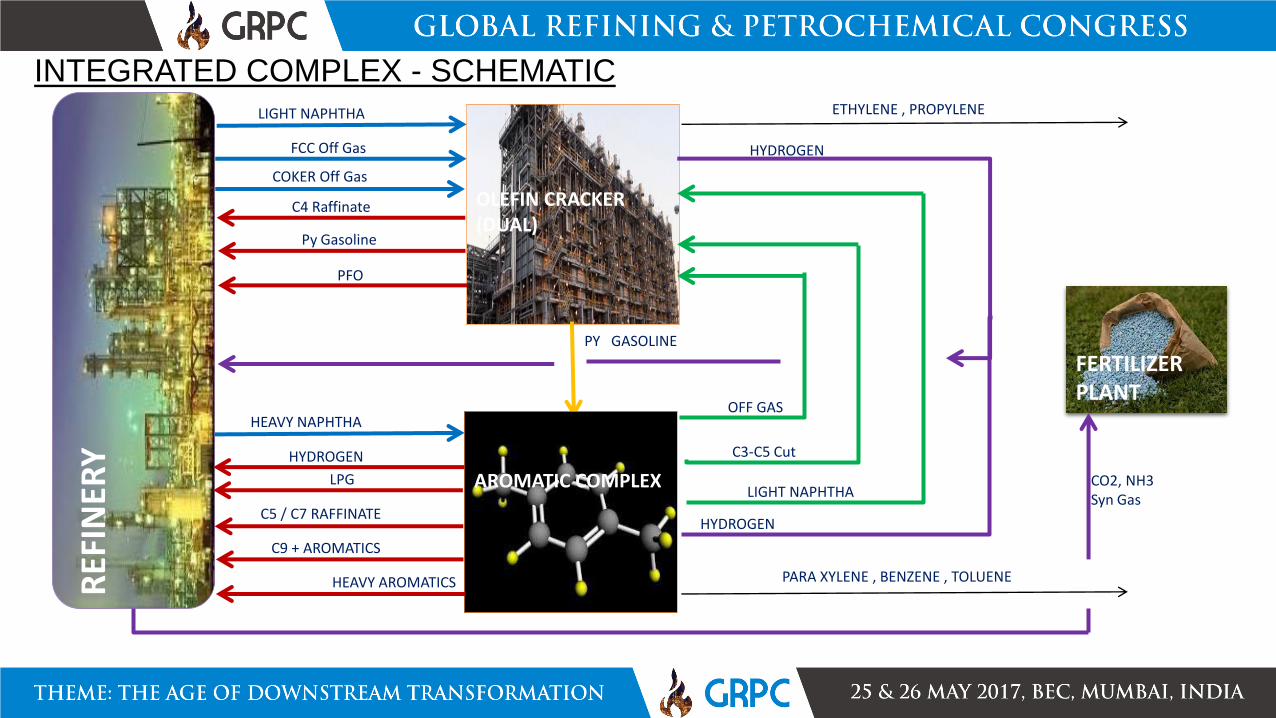

FUEL PETCHEM

INTEGRATED COMPLEX - SCHEMATIC R

EFIN

ERY

OLEFIN CRACKER (DUAL)

LIGHT NAPHTHA

FCC Off Gas

COKER Off Gas

Py Gasoline

PFO

C4 Raffinate

PY GASOLINE

OFF GAS

C3-C5 Cut

LIGHT NAPHTHA

HYDROGEN

HYDROGEN

FERTILIZER PLANT

AROMATIC COMPLEX

HEAVY NAPHTHA

HYDROGEN

LPG

C5 / C7 RAFFINATE

C9 + AROMATICS

HEAVY AROMATICS

ETHYLENE , PROPYLENE

PARA XYLENE , BENZENE , TOLUENE

CO2, NH3 Syn Gas

Complexity of Indian refineries

Gross Refinery Margin

Stand Alone

Integrated Complex

Pricing of petrochemical & Refinery products w.r.t crude

Integration Opportunities between refineries & petrochemical

Case Study

AGENDA

CASE STUDY -1

LNG INTEGRATION TO REFINERIES

POINTERS FOR CASE STUDY

Indian Refineries – Low Margins and High Operating Costs

Operating on High Valued Fuel

Inflexibility towards volatile Crude prices and quality

• Low Capacities - Economies of scale

• Insufficient feedstock for downstream petrochemical complex

• LNG Availability

Stand Alone Refineries -

Lack of Expansion Plot Area

Emergence Of “Make in India”, PCPIR’s and Smart Cities Concepts

LNG Integration – Impact on Refinery Fuels Product Pool

24

Hydrogen Generation

Units

Captive Power Plant

Naphtha

LCO (Diesel)

FUEL OIL

H2

Power and

Steam

Furnace Firing

FUEL GAS Refinery Fuel Pool

LNG Integration – Impact on Refinery Fuels Product Pool

25

Hydrogen Generation

Units

MS-Block

Captive Power Plant

Refinery Fuel Pool

Diesel

Hydro-Treating Unit

Bottoms Processing Unit

Refinery Gasoline Pool

Refinery Diesel Pool

Naphtha

LNG

LCO

LNG

RFO

LNG

H2

Power and

Steam

Furnace Firing

RFG

C2 / C2= Rich Gas

Petrochemical / Cracker

Location & Capacities

Refinery A Capacity – 8.0 MMTPA

•Paucity of Space

•Excess Naphtha available

•HGU 90 KTPA – Naphtha Feed

•CPP – 90 MW – Naphtha Feed

Refinery B Capacity – 6.5 MMTPA

•Paucity of Space

•Excess Naphtha available

•HGU 54 KTPA – Naphtha Feed

•CPP – 54 MW – Naphtha Feed

Refinery C Capacity– 15.0 MMTPA

•Plans for Capacity Expansion

•Space Available

•HGU 73 KTPA – Naphtha Feed

•CPP 204 MW – Naphtha Feed

•Proximity to Natural Gas Import Terminals

•Opportunity for PCPIR and Smart City Development

Refinery

A

Refinery

B

Refinery

C

Refinery

A

Refinery

B

Refinery

C

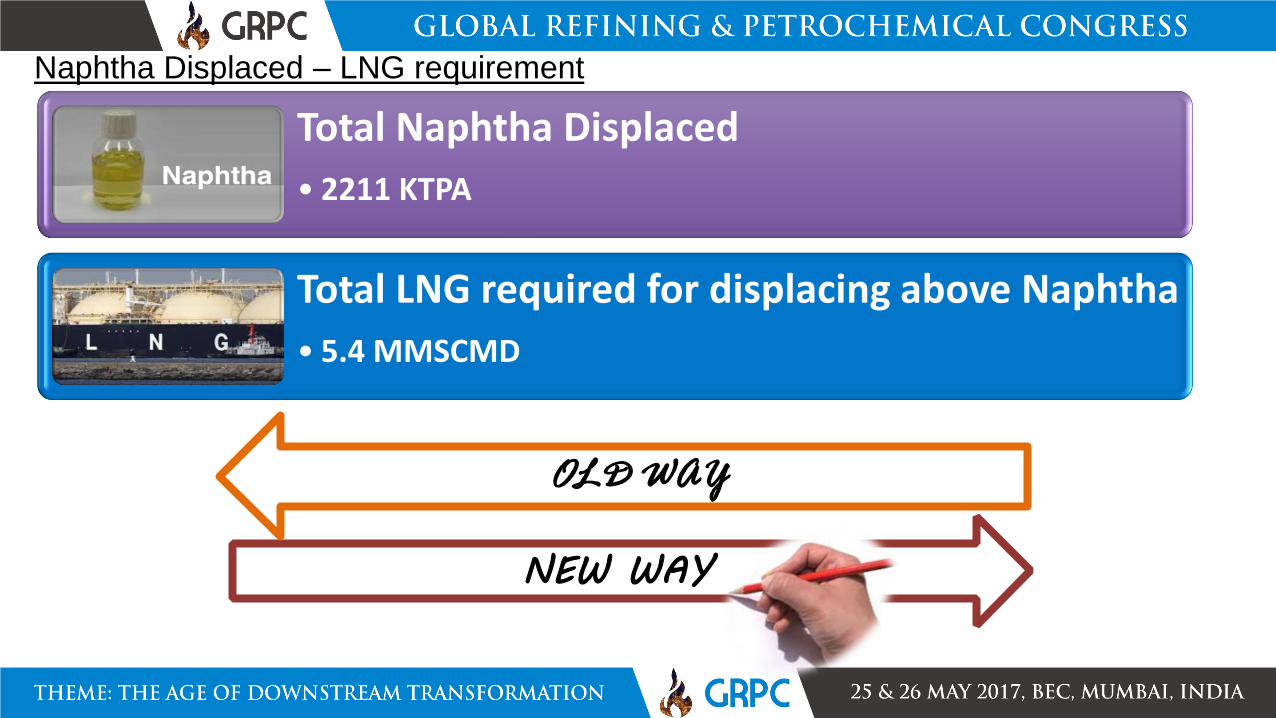

Naphtha Displaced – LNG requirement

Total Naphtha Displaced

• 2211 KTPA

Total LNG required for displacing above Naphtha

• 5.4 MMSCMD

NEW WAY

OLD WAY

Pipeline Integration - Schematic

Map Source: IOCL

Naphtha LNG

Dhamra port

Integration Opportunities

Excess & Displaced Naphtha through LNG integration at Refineries A , B and C

Proximity and availability of Natural Gas in the region

Ethane & Ethylene rich DCU / FCC off gasses

Availability of Land

Announced Plastic Park can be envisaged in the region

Logistics

Utilities

Plastic Park

Derivatives

Basic Petrochem

Refinery

Conclusion

LNG INTEGRATION

&

REFINERY INTEGRATION

Efficiency improvement

Value addition.

LNG to Petrochem

Make in India

Feedstock ensured

Refinery Flexibility

Thank you The information upon which this presentation is based comes from our own experience, knowledge and databases, supplemented by reference to primary sources and published industry data. Any opinions expressed are those of the author as of this date. They have been arrived at following careful consideration and enquiry but we do not guarantee their fairness , completeness or accuracy. We do not

accept any liability for your reliance upon them.