top 10 payment trends to watch in 2012 (whitepaper) | vantiv

TRANSCRIPT

Top 10 payment trends to watch in 2012

Part of the Vantiv Insight Series 2012, featuring proprietary research performed by Vantiv Inc., and Mercator Advisory Group

© 2012 by Vantiv LLC. All rights reserved.

3

Business is changing on virtually every front, and the world of

payments is no exception. Today, merchants, financial institutions,

and processors all face an evolving landscape that is being re-

shaped by an array of forces. The use of credit and debit cards is

changing. Emerging payment methods, based on everything from

smartphones to social networks, are rapidly gaining traction, as are

innovative point-of-sale systems and a growing number of e-

wallet-based methods. At the same time, more familiar factors—

such as shifting security threats and ever-changing laws and regu-

lations—have to be factored into the equation. Altogether, these

currents promise a fundamental transformation comparable to the

shift from cash to electronic payments more than a decade ago.

In this publication, Vantiv focuses on these varying and often over-

lapping currents. These have been distilled into 10 trends that are

underway and, in many cases, likely to have an even greater impact

in the near future.

These observations are based on Vantiv’s experience and on dis-

cussions with clients and others in the industry. Perhaps most

important, we draw on the insights of consumers. Working with the

Mercator Advisory Group, Vantiv has researched consumer atti-

tudes about these trends—what they want, what they worry about.

That perspective is key, because consumers’ views and behaviors

will shape the future as much as new technologies and policies.

Top 10 Payment Processing Trends for 2012

1. Share of wallet

2. Security

3. Prepaid

4. Smartphone

payments

5. Merchant tablets

6. Mobile banking

7. P2P payments

8. E-commerce

9. Social payments

10. Legislation

Shaping the future of payment processing

4

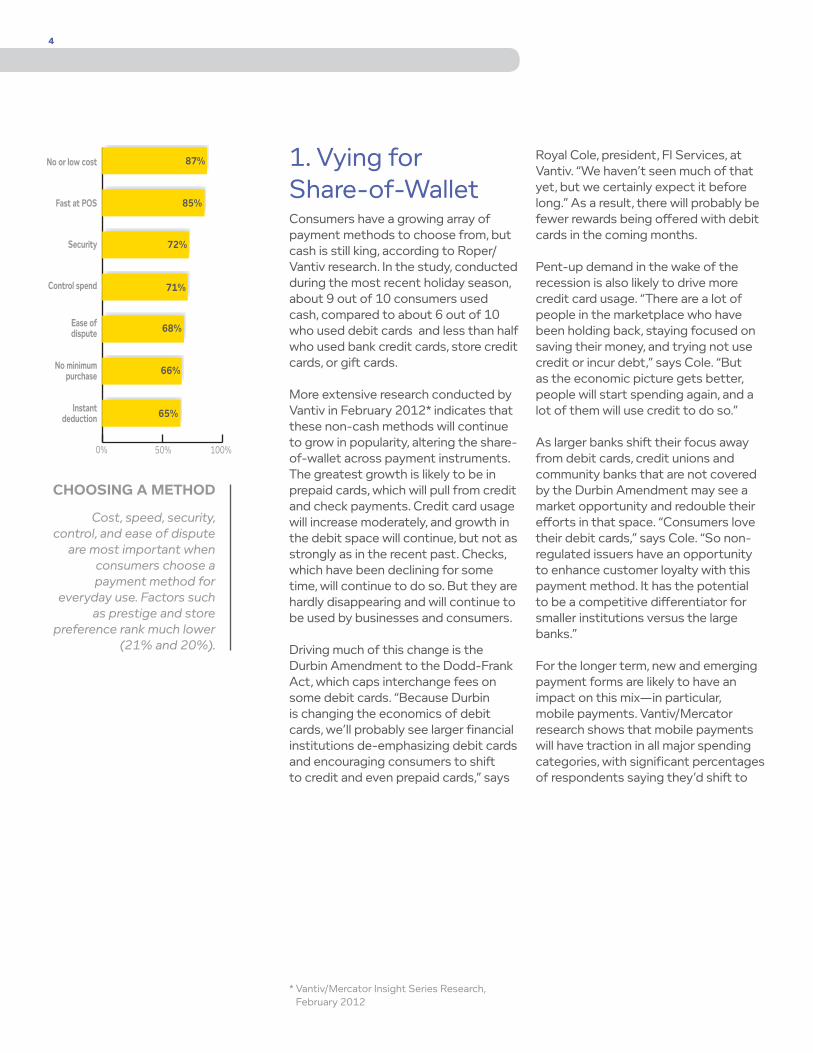

0% 50% 100%

87%No or low cost

Fast at POS

Security

Control spend

Ease of dispute

No minimum purchase

Instant deduction

85%

72%

71%

68%

66%

65%

1. Vying for Share-of-WalletConsumers have a growing array of payment methods to choose from, but cash is still king, according to Roper/Vantiv research. In the study, conducted during the most recent holiday season, about 9 out of 10 consumers used cash, compared to about 6 out of 10 who used debit cards and less than half who used bank credit cards, store credit cards, or gift cards.

More extensive research conducted by Vantiv in February 2012* indicates that these non-cash methods will continue to grow in popularity, altering the share-of-wallet across payment instruments. The greatest growth is likely to be in prepaid cards, which will pull from credit and check payments. Credit card usage will increase moderately, and growth in the debit space will continue, but not as strongly as in the recent past. Checks, which have been declining for some time, will continue to do so. But they are hardly disappearing and will continue to be used by businesses and consumers.

Driving much of this change is the Durbin Amendment to the Dodd-Frank Act, which caps interchange fees on some debit cards. “Because Durbin is changing the economics of debit cards, we’ll probably see larger financial institutions de-emphasizing debit cards and encouraging consumers to shift to credit and even prepaid cards,” says

Royal Cole, president, FI Services, at Vantiv. “We haven’t seen much of that yet, but we certainly expect it before long.” As a result, there will probably be fewer rewards being offered with debit cards in the coming months.

Pent-up demand in the wake of the recession is also likely to drive more credit card usage. “There are a lot of people in the marketplace who have been holding back, staying focused on saving their money, and trying not use credit or incur debt,” says Cole. “But as the economic picture gets better, people will start spending again, and a lot of them will use credit to do so.”

As larger banks shift their focus away from debit cards, credit unions and community banks that are not covered by the Durbin Amendment may see a market opportunity and redouble their efforts in that space. “Consumers love their debit cards,” says Cole. “So non-regulated issuers have an opportunity to enhance customer loyalty with this payment method. It has the potential to be a competitive differentiator for smaller institutions versus the large banks.”

For the longer term, new and emerging payment forms are likely to have an impact on this mix—in particular, mobile payments. Vantiv/Mercator research shows that mobile payments will have traction in all major spending categories, with significant percentages of respondents saying they’d shift to

Cost, speed, security, control, and ease of dispute

are most important when consumers choose a payment method for

everyday use. Factors such as prestige and store

preference rank much lower (21% and 20%).

CHOOSING A METHOD

* Vantiv/Mercator Insight Series Research, February 2012

5

mobile payments as follows:

• 10% for small in-store purchases, displacing mostly cash

• 11% for grocery/everyday, displacing mostly debit

• 8% for large in-store purchases, displacing mostly credit

• 7% for online purchases, displacing credit/debit

• 6% for education expenses, displacing mostly checks

• 9% for household expenses, displacing mostly debit

• 8% for doctor visits/co-pays, displacing mostly cash and checks

These percentages may be underestimated, since consumers tend to minimize their own likelihood of using alternate payment methods.

The study also looked at the factors that drive and will drive consumers’ choice of payment method. Consumers are very interested in low- or no-cost methods, security, and the ability to control spending—and are less interested in the prestige of payment type and store preferences. An understanding of these perspectives can help institutions focus on payment methods that will appeal to consumers and encourage greater adoption and usage.

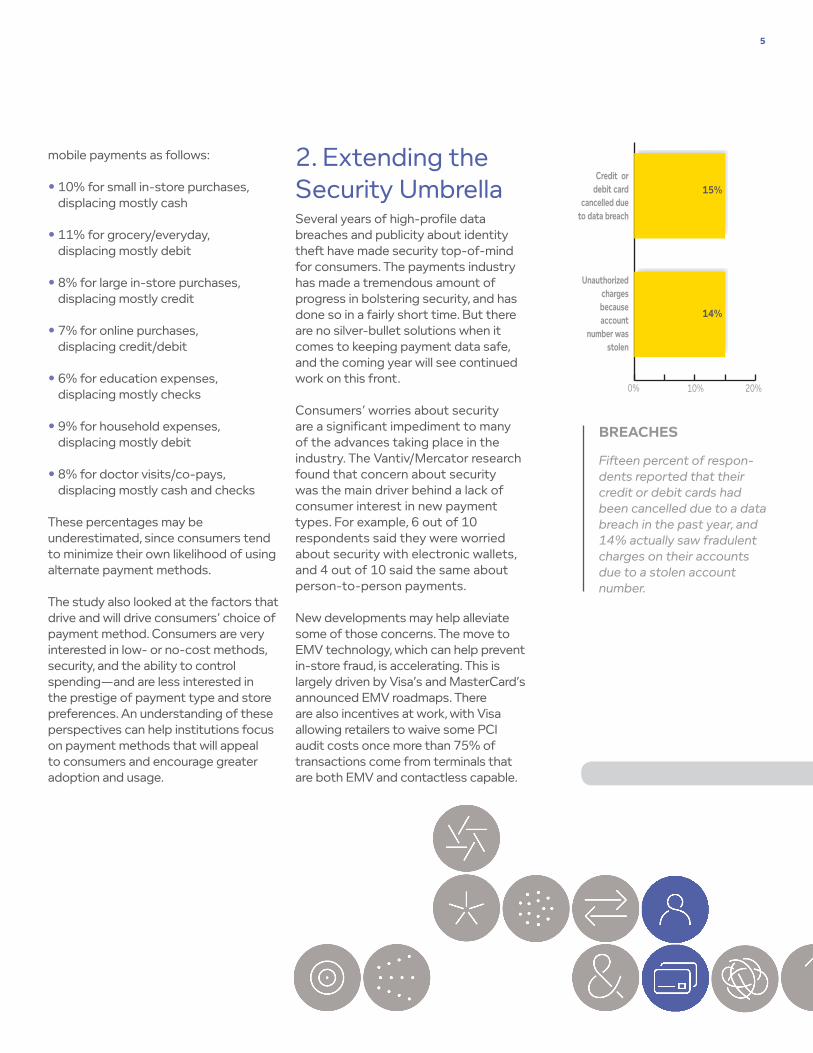

2. Extending the Security Umbrella Several years of high-profile data breaches and publicity about identity theft have made security top-of-mind for consumers. The payments industry has made a tremendous amount of progress in bolstering security, and has done so in a fairly short time. But there are no silver-bullet solutions when it comes to keeping payment data safe, and the coming year will see continued work on this front.

Consumers’ worries about security are a significant impediment to many of the advances taking place in the industry. The Vantiv/Mercator research found that concern about security was the main driver behind a lack of consumer interest in new payment types. For example, 6 out of 10 respondents said they were worried about security with electronic wallets, and 4 out of 10 said the same about person-to-person payments.

New developments may help alleviate some of those concerns. The move to EMV technology, which can help prevent in-store fraud, is accelerating. This is largely driven by Visa’s and MasterCard’s announced EMV roadmaps. There are also incentives at work, with Visa allowing retailers to waive some PCI audit costs once more than 75% of transactions come from terminals that are both EMV and contactless capable.

0% 10% 20%

15%Credit or

debit card cancelled due

to data breach

Unauthorized charges because account

number was stolen

14%

Fifteen percent of respon-dents reported that their credit or debit cards had been cancelled due to a data breach in the past year, and 14% actually saw fradulent charges on their accounts due to a stolen account number.

BREACHES

6

As more institutions adopt EMV, consumers will also be pushing for adoption. “It will basically be mandated by the market,” says Patty Walters, senior vice president, merchant product security, at Vantiv. “Consumers are interested in security, and when one bank starts marketing its EMV product as being more secure, other banks will no doubt want to keep up.” In recent Vantiv/Roper research, only 20% of consumers said they would be interested in tapping or waving their phones at terminals to make a payment this year—a fairly lukewarm response. But more than twice that number (43%) were interested in EMV smart cards, which consumers see as more secure.

EMV is also setting the stage for the use of dynamic CVV, which is included in the Visa roadmap. With this approach, the card’s chip automatically generates a security code for each transaction, as opposed to the current approach of having a code for the card itself. “With the dynamic data being required, the card number is no longer enough to use for fraud,” says Walters. “The fraudsters really can’t guess the dynamic CVV, as they can with the traditional fixed security code. You need the card with the chip itself. So this has the potential to dramatically improve security.”

The coming year may also see a heightened focus on strengthening security among smaller retailers, which are often a “soft target” for data thieves. “Reports show that fraud is moving

downstream,” says Walters. “Smaller shops can be very vulnerable because they usually don’t have the technical sophistication the larger retailers have.” Expect to see more industry interest in moving security solutions down to the small merchant, and making them affordable and easy to install. These efforts may extend beyond technology, she adds: “The industry is looking at how it might offer indemnification programs, so that if the small retailer is compromised, the resulting forensics and legal costs are at least somewhat covered and don’t end up putting the retailer out of business.”

3. Prepaid Cards: Wider Appeal, Increasing VarietyPrepaid cards will continue to increase in popularity and variety—in large part because of the Credit Card Act and the Dodd-Frank Act. “Those two acts together are making it so that, in many cases, a large portion of the U.S. population is unable to obtain a credit card, a debit card, or even a checking account,” says Ed Paciolla, product management director at Vantiv. A prepaid card gives these consumers a more convenient and controllable payment method than cash, especially for paying bills and making online purchases. Overall, the Vantiv/Mercator research found that 15.5% of

0% 40% 80%

78%Criminal

hacking to get payment data

Losing phone

Would still carry credit/

debit cards

Battery life

77%

67%

53%

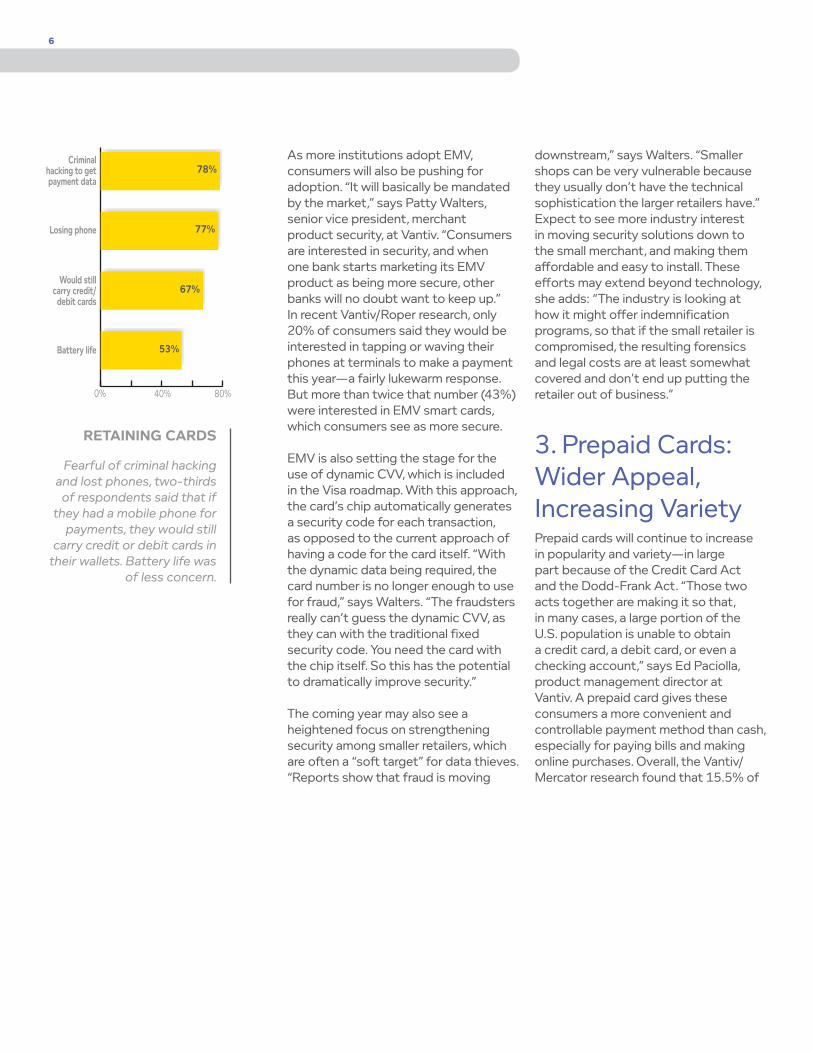

RETAINING CARDS

Fearful of criminal hacking and lost phones, two-thirds of respondents said that if

they had a mobile phone for payments, they would still

carry credit or debit cards in their wallets. Battery life was

of less concern.

7

consumers expect to substitute debit/DDA accounts with prepaid cards in the next 12 months.

Many consumers also like the security of prepaid cards compared to that of emerging mobile and contactless payment methods. As those methods become more widespread, prepaid can offer a comfortable alternative because the cardholder’s liability is limited if the card is lost or compromised. But faith in prepaid cards is not absolute: While most consumers trust network-branded prepaid cards (62%) and retailer cards (57%), only 38% see prepaid as being safer than cash, according to the Vantiv/Mercator research.

General-purpose reloadable cards are likely to see strong growth in the coming year—perhaps 25%. What’s more, large financial institutions may become more involved in the effort to convert more consumers as debit card usage slows.* However, this may take time, as banks sort out fee structures and look for convenient, multichannel approaches to card-loading, which is inhibited because 58% of bank customers are still not involved in online banking.

The prepaid-card arena has been growing more diverse, with various types of cards serving different needs—and that trend continues. The coming year will see growth in the 15% to 20% range for customer rebate and incentive cards and employee-reward cards. Disbursement cards, often

used in the public sector to provide funds to constituents, present a mixed picture. For example, unemployment-card usage has ballooned in recent years, but that market is now slowing because most large states have completed the transition to such cards. Universities, on the other hand, are showing increased interest in disbursement cards because it provides a cheaper, faster alternative to writing checks for tuition rebates.

Meanwhile, the gift-card segment will continue to see modest growth, compared to the significant 2011 market rebound driven by post-recession consumers’ renewed confidence in the stability of retailers. This is a mature market, and the trend toward merchants seeing gift cards as marketing tools designed to drive traffic to the business will continue. As a result, we are likely to see more incentives associated with gift cards, as well as efforts by merchants to integrate gift-card programs with their marketing/promotions functions—areas that are still separate silos at many companies.

Finally, several emerging approaches to prepaid bear watching. These include digital, downloadable prepaid cards, which essentially give the user a card number online; and micro-lending prepaid cards, which allow consumers to borrow small amounts from their financial institution and apply them to their card, on the spot, when they need to make a larger purchase.

0% 35% 70%

62%I can trust

general-purpose prepaid cards

I can trust retailer prepaid

cards

Useful for online purchases

Safer than cash

Substitute for checking

account

57%

49%

38%

16%

TRUSTING PREPAID CARDS

Consumers trust prepaid cards, particularly general-purpose cards. Nearly half consider them useful in online purchases, a trust-worthy way to hedge e-commerce risks with limited personal data and account separation.

* Due to Durbin-related costs and controls, financial institutions are encouraging customers to roll from debit to prepaid cards by offering rewards/prewards for keeping cards loaded.

8

4. Smartphone Payments: On the VergeSmartphones are being used for a growing range of applications in daily life—and that includes making payments. But so far, there has been more buzz than actual usage.

In the Vantiv/Mercator research, just 1.5% of consumers said that they have made mobile payments. Interest and awareness are there—61% believe that mobile payments will be common in five years. But consumers appear to have difficulty applying that to their own situations: only 38% see themselves making mobile payments in five years.

There are several reasons for this gap. Consumers have doubts about smartphone security and see the devices as vulnerable to hacking and easy to lose. They’re also concerned about practical limitations, such as short battery life and forgetting to carry their phones. As a result, most consumers say even if they used a phone for payments, they would keep a traditional card as a backup.

The upshot: Smartphone payments are not likely to take off in the next year. But longer term, the picture is different due to several factors, including marketplace buzz. The increasing ubiquity of the devices is also creating momentum.

Mercator’s own research shows that smartphone ownership at the beginning of 2012 was 45%, up from 28% in 2011. In addition, in the Vantiv/Mercator study, consumer awareness of mobile payments is now above 50%, and interest is at 20%—levels that typically represent a tipping point for a technology’s widespread acceptance. By 2017, about 10% of consumers expect to be using mobile payments for small in-store and grocery purchases.

Merchant activities, too, will drive increased usage. There is a lack of in-store infrastructure for smartphone payments. But as the push for EMV compliance drives merchants to upgrade equipment, some may bring on NFC capabilities, which are required for smartphone payments, as part of the upgrade. However, it is still not clear that NFC will be the winning technology, as a battle is raging between a number of gatekeeping mechanisms, and some merchants wait for a clear victor.

Another driver is represented by solutions such as “Square”—a card-reader attachment for smartphones that lets retailers use their phones to accept credit-card payments. Smartphone-based card acceptance has reached 33.5% awareness and 5% usage. For such a relatively new tool, this represents a strong foundation for growth and the beginning of a significant user base. Consequently, says Ben Love, Vantiv’s vice president, product, “We think phone-based card

Mobile payments will be common

31%

30%10%

22% 7%

■ 1-2 years ■ 2-5 years ■ 5+ years

■ No idea

■ Never

I will use mobile payments

18%

19%

37%

18%

8%

USING MOBILE PAYMENTS

While 62% of respondents expect that mobile pay-

ments will be common within the next five years,

only 36% expect that they themselves will be mak-

ing those payments. Not surprisingly, this percentage

is higher among younger respondents.

9

acceptance is an early incarnation of the merchant world by 2015.”

Ultimately, the actions of issuers will be key to bringing consumers around. Today, many users simply don’t see a reason to change. Just 1 in 4 regard mobile wallets as convenient, and 1 in 8 would prefer to use smartphone payment rather than a card. But issuers are taking steps to pique consumer interest with features such as coupon programs, location- and proximity-based marketing, and tools to help consumers budget and manage spending.

Rewards, too, may help: In the Vantiv research, 27.5% of consumers regarded them as a potentially effective way to encourage the use of mobile payments. The research also found that for many consumers, a 1% rebate from merchants at the point of sale would be an effective incentive for adopting a new payment method. In short, says Love, “You can’t make things any easier than using a card, so you have to add value. You have to offer something more than convenience and provide a compelling consumer experience.”

5. Merchants: The Advent of the POS TabletOver the past year, merchants have embraced iPads and other tablets

at a pace that has surprised many observers. Merchants are finding a number of in-store uses for the devices, allowing salespeople to gather customer data and help customers find what they need, or letting shoppers browse through inventory themselves. “Merchants are finding them useful for streamlining in-store processes and engaging customers to increase sales,” says Donald Boeding, president, merchant services, at Vantiv.

Increasingly, merchants are also looking at the tablet as a mobile point-of-sale (POS) device that can be used to accept payments and provide an effective alternative to the traditional cash register—at perhaps a tenth of the price. While the use of tablets to handle payments is still relatively new, the Vantiv/Mercator research found that 17% of consumers have already used roving POS for in-store payments—and that figure should grow significantly, and quickly.

Tablet-based payments are appealing not just because of lower costs, but also because they can increase salespeople’s efficiency, shorten checkout lines, and contribute to a satisfying customer experience. In a shoe store, for example, a salesperson could use a tablet to check inventory without running to a storeroom, quickly locate the right type of shoe, and then have it retrieved for the customer. “If the customer likes the product, the salesperson can just

0% 15% 30%

27%Convenient

Reliable

Secure

23%

17%

MOBILE PERCEPTIONS

Consumers are taking a “wait and see” approach to payments via smartphone, seeing phones as a some-what convenient way to pay—but not quite as reliable or secure.

10

hand the tablet to the customer, who can then fill out payment information and complete the sale online with secure, encrypted card acceptance,” says Boeding. The customer spends less time waiting, and the salesperson spends more time selling.

As this trend unfolds, we are likely to see tablets continue to evolve to fit the often demanding requirements of various retail environments. An iPad might not be suitable for a restaurant where people are spilling drinks and getting food on the device, for example. This is leading to specialized forms of tablets, with different functions and levels of physical “hardening” for each type of retail environment. That specialization may also help with another tablet issue. “If you have a specialized device for, say, ordering and paying in a restaurant,” says Boeding, “customers are going to be less tempted to walk away with it, compared to a new, general-purpose iPad.”

6. Heading Toward Mobile Banking 3.0Mobile banking is garnering a great deal of attention, with nearly half the banks in an internal Vantiv survey saying they expect to invest in it in the coming year. But banks have a significant opportunity to take things to the next level—and that may have an impact on how mobile

banking evolves in the near future.

“So far, many banks have essentially just transferred PC-based Internet banking to mobile banking, so you can do things like check balances and transfer funds from your phone,” says Ben Love, vice president, product, at Vantiv. “It’s a utility that provides convenience, but it doesn’t really take advantage of the device’s mobility. So we are going to see a lot of innovation in this space in the near future, as banks try to make mobile banking more compelling for consumers.”

One such innovation is mobile check deposit, which lets consumers use their smartphones to photograph and deposit a check. This approach moves beyond basic mobile banking and lets the customer avoid a trip to the bank branch, and it provides a proven value proposition for banks. USAA, a pioneer in mobile check deposit, has seen rapid acceptance of the process, reporting that customers used the feature to deposit 7.8 million checks totaling $4.3 billion in 2011. Not surprisingly, there is a lot of interest in this method among consumers and banks alike, and it is expected to become increasingly widespread in the coming months.

Meanwhile, many observers see the addition of wallet-based payment capabilities as a logical next step in mobile banking. “The industry is already starting on that path, and we will

0% 30% 60%

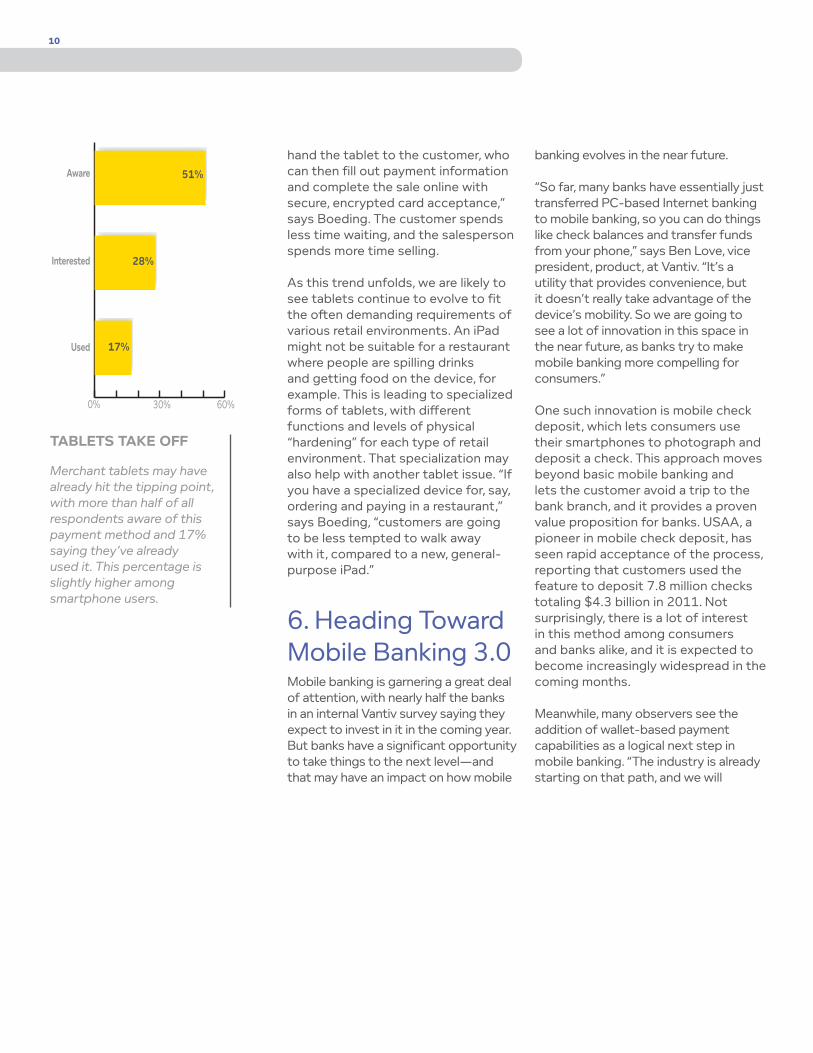

51%Aware

Interested

Used

28%

17%

TABLETS TAKE OFF

Merchant tablets may have already hit the tipping point, with more than half of all respondents aware of this payment method and 17% saying they’ve already used it. This percentage is slightly higher among smartphone users.

11

see much more of that,” says Love. Banks’ interest in wallets is certainly growing—but so is the interest of other parties, from Google and Amazon to numerous large retailers. Vantiv estimates that there are more than 80 wallets in development or on the market and that there may be as many as 250 by the end of the year. The result is an often-confusing array being presented to consumers.

But banks have strengths that may stand out in that mix. Consumers—worried, as always, about security—may see their banks as a safe and simple wallet option. “The bank already has your personal and financial information, so there is a level of trust already established,” says Love. “And if you have a mobile banking application, it makes a lot of sense to just seamlessly add payments to that, rather than use a number of other wallets.”

All of this can be seen as the emergence of “mobile banking 3.0,” says Love. “We’re moving toward mobile personal financial management, where the consumer not only has banking functions, but can also use the phone to do budgeting, receive alerts about overspending, get offers from third parties, and so on. At that point, mobile banking starts to really contribute to the customer relationship and loyalty. And this will probably happen sooner than a lot of people expect.”

7. P2P: Getting Consumers to Come AlongThere has been much discussion about person-to-person payments for several years. Indeed, P2P is already a common form of payment in much of the world, with consumers in many countries able to easily make account-to-account transfers (A2A) to other individuals and businesses. In the U.S., however, P2P—a key form of A2A—has not taken off.

Part of the problem is that consumers don’t seem sure how mobile P2P would fit into their lives. Forty-seven percent said that they don’t see a need for it, 38.5% have security concerns, and just 22% said they were interested.

Many observers think that increased familiarity will, in the long run, make P2P a common tool in the U.S. “There is real potential for P2P payments, especially for unanticipated transactions that need to happen rapidly, such as paying medical bills or car repairs,” says Dean Seifert, senior vice president, product strategy, at Vantiv. Interestingly, P2P has gained some traction among individuals making payments to tradespeople and other small businesses. “The original thought was that two individuals might use P2P to split the check at lunch, that sort of thing,” says Seifert. “But so far it’s been a consumer-to-small-business

0% 15% 30%

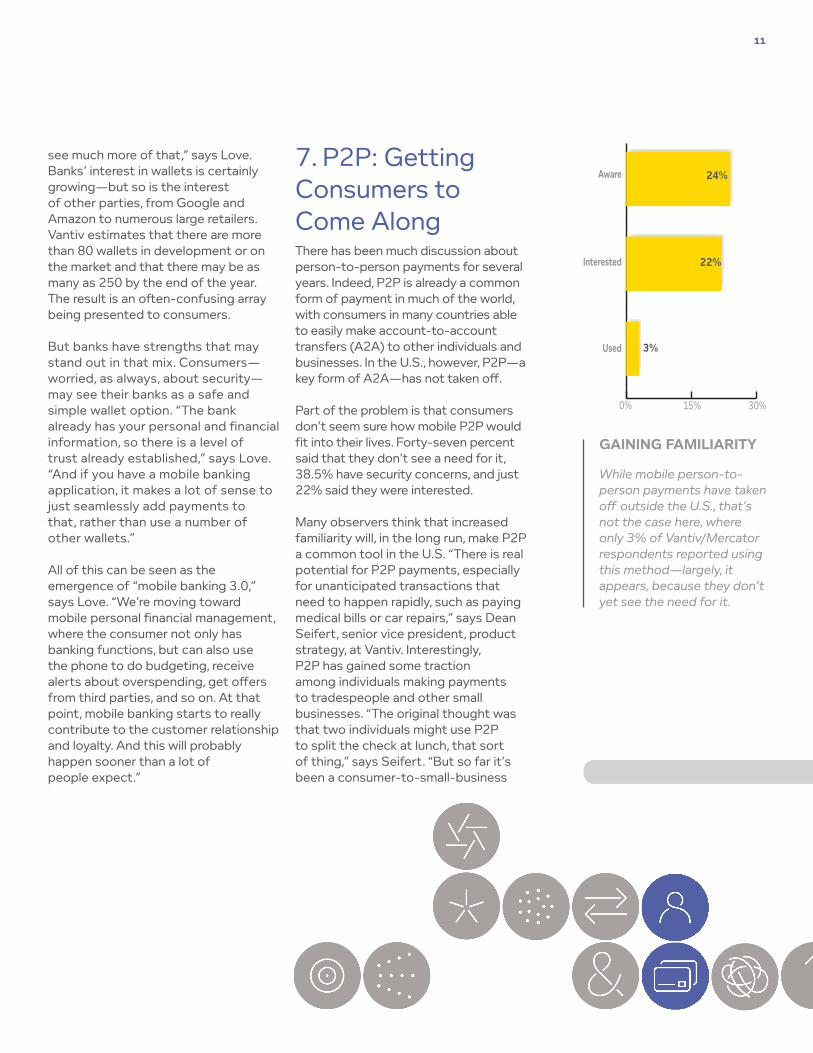

24%Aware

Interested

Used

22%

3%

GAINING FAMILIARITY

While mobile person-to-person payments have taken off outside the U.S., that’s not the case here, where only 3% of Vantiv/Mercator respondents reported using this method—largely, it appears, because they don’t yet see the need for it.

12

tool. The average transaction value is more than $300, rather than, say, $20.”

The coming year should see consumer awareness of P2P increase considerably. There are a growing number of providers, from Paypal to Amazon, and many observers see the possibility of players such as Google and Facebook moving into the space. Many banks have started to embrace P2P and A2A in earnest, and last year Bank of America, Chase, and Wells Fargo created “clearXchange,” a back-end system for processing P2P payments.

Nevertheless, there are some obstacles. One issue is time: Many P2P payment services rely on the ACH network, which means that it can take a few days for payments to clear. Payments made through services such as PayPal can go through in minutes, but only if both parties have accounts with the service—which makes it fairly unsuitable for everyday, one-off transactions. Otherwise, such transfers can take days. Consumers may also feel that current P2P services require too much effort, with the need to open accounts, go online to approve incoming transfers, and so forth.

The industry is working to address such issues. Already, some institutions allow consumers to send payments to credit cards using a common bill payment network, such as MasterCard’s RPPS. Others are seeing value in using their debit “rails” in reverse for real-time

money movement, and charging a fee for these premium, faster transactions. Ultimately, banks will also need to provide P2P capabilities across channels—on-line, in-branch, mobile, and ATM—for consumer convenience. “Right now, P2P is really a blip in the overall payments market, but it will eventually grow quickly,” says Seifert. “As long as the fees are lower than wire transfers and the speed is faster, it will catch on.“

8. Online Heads Into OfflineWhen it comes to making payments online, consumers have a clear sense of their options. The Vantiv/Mercator research found high levels of awareness (more than 80%) for online methods of credit and debit, PayPal, ACH debit, and online bill payment. Credit and charge cards are still the preferred way to purchase online, but other options will gain ground in the near future.

For consumers paying online, security and the risk of identity theft are top of mind. Credit cards provide some comfort: More than half the respondents cited the “zero liability” of cards as a key factor behind their online use. Roughly the same proportion said that prepaid cards, which limit exposure, are useful in making online payments. But looking ahead, worries about security are likely to increase

0% 25% 50%

41%Credit/charge card

Debit card

Online payment (e.g., PayPal)

General-purpose prepaid

31%

16%

3%

SECURITY STILL IMPORTANT ONLINE

For purchases made online, respondents said they pre-ferred credit cards, in large

measure due to “zero li-ability.” Debit cards followed closely, with online payment

methods such as PayPal showing potential.

13

the appeal of intermediaries, such as Amazon, because they allow consumers to enter their card number once for use with multiple vendors, rather than separately with different vendors. In the Vantiv/Mercator research, 45.5% of consumers said that they view PayPal online security as being better than that of credit or debit cards.

Indeed, there is growing interest in such online payment methods, including e-wallet initiatives such as Google Checkout that let consumers make purchases without having to enter credit card numbers. What’s more, those methods are moving from their e-commerce roots into the brick-and-mortar world. “PayPal, Amazon, and iTunes are cloud-based wallets and have the potential to take their e-commerce approach down to the in-store point of sale,” says Bill Weingart, chief product officer at Vantiv. With financial information stored by these intermediaries in the cloud, shoppers could check out with minimal risk using an ID number and PIN, he explains.

“It’s highly probable that we will be seeing more of the e-commerce wallets being used in brick and mortar,” Weingart continues. “PayPal clearly has a vision to be an acceptance option at the retail point of sale, and there’s an expectation that Amazon and Apple will want to do the same and take their brands from the virtual to the real world.” That trend is also proving to be a two-way street: Visa, for example,

has launched its V.me wallet for online shopping, which lets consumers pay using MasterCard, Discover, or American Express, as well as Visa cards.

Those moves are part of a larger trend toward the increasing overlap of physical commerce and e-commerce—a trend that is likely to accelerate in the coming months. With mobile smartphone payments, tablets being used in stores, ubiquitous wireless connections, and changing consumer payment behaviors, “e-commerce is no longer something you do from your PC at home—it’s now taking place in the store itself,” says Weingart.

9. Social Network Payments: Entering the Real World?Consumers are buying a growing number of virtual goods used in online social network games—things like swords and magic wands for multi-player games, or cows and tractors for Farmville. Nevertheless, only 36% of consumers have heard of these social network payments; 12% say they are interested in them, and just 4% are using them, according to the Vantiv/Mercator research. Nonetheless, this is a rapidly growing area, with U.S. consumers spending more than $2.3 billion on virtual goods last year, up from $1.8 billion in 2009, according to

0% 20% 40%

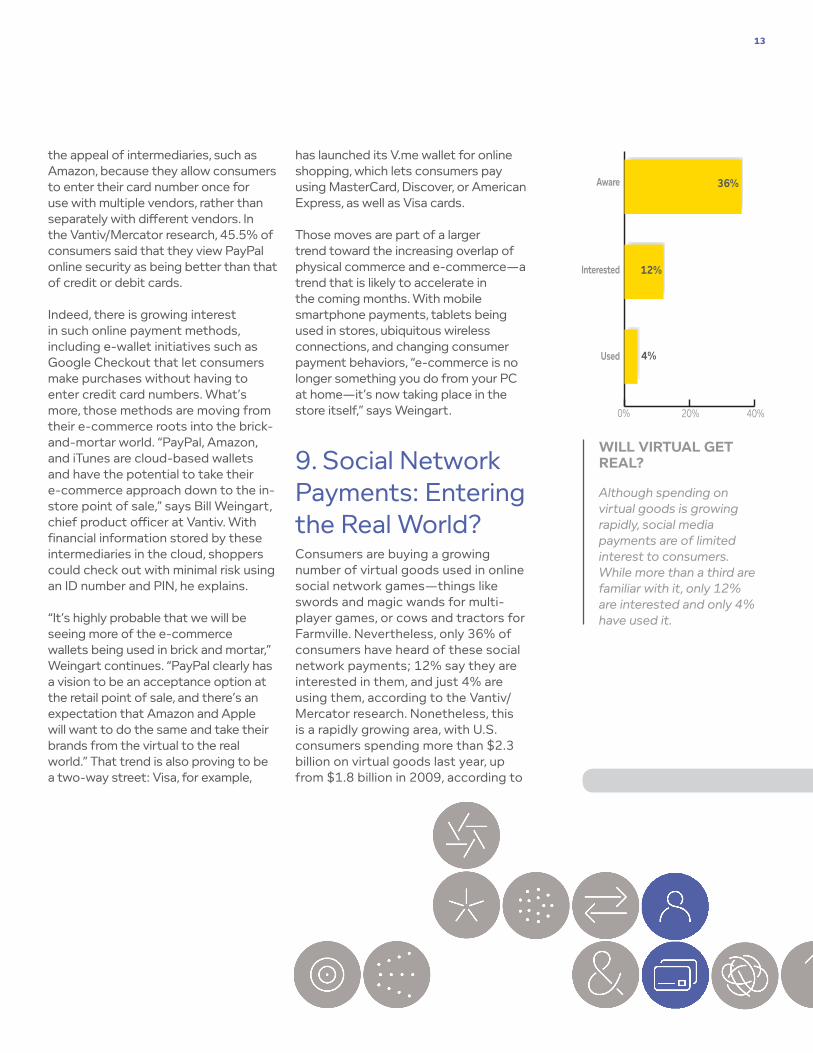

36%Aware

Interested

Used

12%

4%

WILL VIRTUAL GET REAL?

Although spending on virtual goods is growing rapidly, social media payments are of limited interest to consumers. While more than a third are familiar with it, only 12% are interested and only 4% have used it.

14

the Frank N. Magid Associates con-sulting firm.

The question is, how will this play out in the non-virtual world of paying for actual goods and services? Already, there is beginning to be some overlap of the virtual and the real. “Facebook, for example, is allowing people to use Facebook credits to purchase real goods from merchants,” says Ben Love, vice president, product, at Vantiv. “They are doing this in a small way so far, but that may grow.”

However, virtual payments will need to overcome some obstacles to become widespread in the real world. Because virtual transactions are relatively high-risk, providers typically charge 30% or more to handle them. “That also means that sellers have to wait days for pay-ment while the intermediary makes sure there are no chargebacks,” says Love. Thus, social-network payment methods will need to find approaches to pricing and timing that will appeal to broader audiences. Security, too, will need to be more robust. “As virtual currencies are used for more real goods, they become more valuable to more people—and that is likely to increase the potential for fraud to a level they aren’t dealing with today,” says Love.

These challenges are significant but not insurmountable, Love adds: “This is a fast-changing area, and social net-works have a history of innovation. So this bears watching.”

10. The Regulatory Landscape: Unending ChangeThe past several years have seen heightened regulatory scrutiny and new legislation affecting financial activities; this year, those changes are having a significant impact. The ramifications of the CARD Act and the Durbin Amendment are being sorted out, while new 1099-K rules placing significant reporting requirements on payment providers and merchants are being rolled out through 2013.

Even as companies work through these changes, new ones are appearing on the horizon—and it can be difficult to keep track of it all. The Financial Crimes Enforcement Network, for example, has issued new reporting and record-keeping requirements that affect the use of open-loop prepaid cards. And a number of observers expect to see government agencies start tailoring regulations to the emerging use of social media in financial activities.

A key development to watch will be the activities of the Consumer Financial Protection Bureau, created last July and now getting into full swing. The CFPB presents an especially big question mark because of its exceptionally broad mandate. “It essentially looks at anyone who provides financial services to consumers or businesses—which

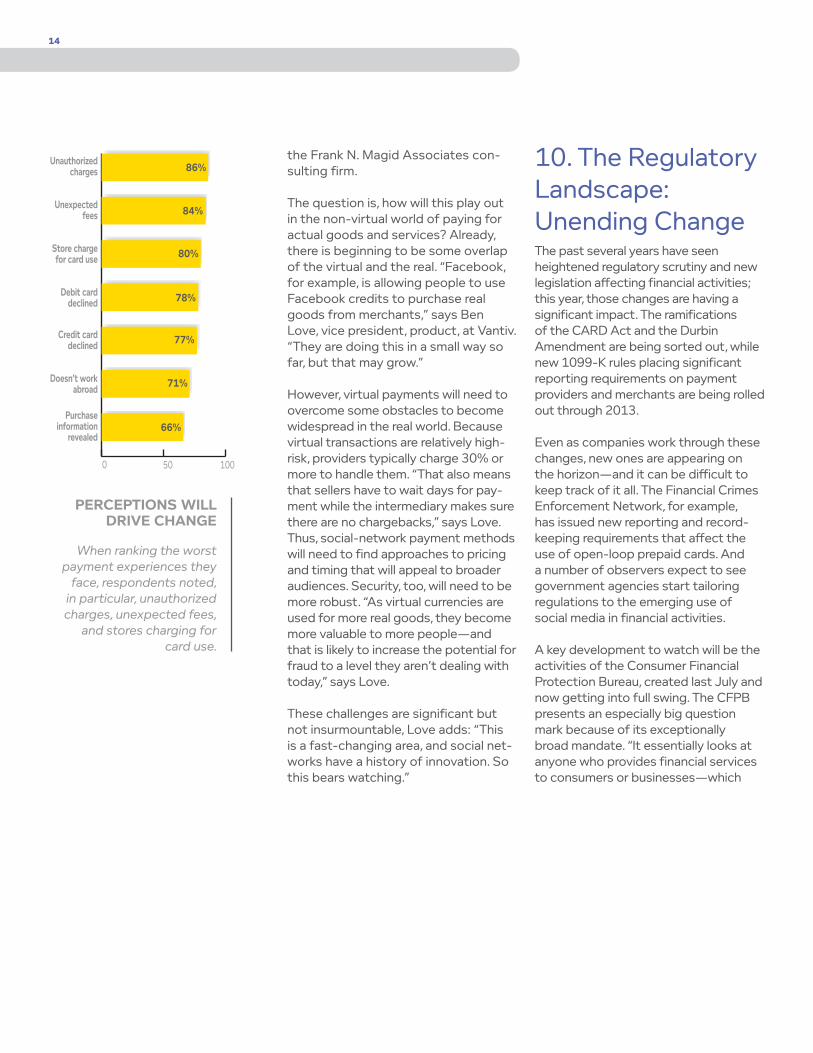

0 50 100

86%Unauthorized

charges

Unexpected fees

Store charge for card use

Debit card declined

Credit card declined

Doesn’t work abroad

Purchase information

revealed

84%

80%

78%

77%

71%

66%

PERCEPTIONS WILL DRIVE CHANGE

When ranking the worst payment experiences they

face, respondents noted, in particular, unauthorized charges, unexpected fees,

and stores charging for card use.

15

is just about anything that touches a transaction,” says David Herron, product legal counsel at Vantiv. “It is staffing up and will be looking in a lot of directions.” The CFPB has been hearing credit card complaints since it was launched, and it recently expanded its efforts into checking accounts. By early 2012, the bureau announced that it had received more than 20,000 complaints on various topics, including some 12,000 about credit cards.

Consumer perceptions may also drive change. Herron says that consumers generally see the increased bank fees that have resulted from recent legislation, but they haven’t seen the expected benefits of lower costs being passed along from retailers. “That may produce a backlash against the existing legislation, as well as drive more complaints to regulators,” he says. The Vantiv/Mercator research provides some insight into the potential nature of those complaints. Among the most-cited bad-payment experiences: unexpected fees for using credit/debit (84%), and being charged extra by stores to use a payment type (80%).

Finally, the U.S. presidential elections are also likely to affect the regulatory landscape, one way or another. “There have already been minority calls in Congress to repeal parts of Durbin,” says Herron. “A new Congress might be open to those calls. And depending on the eventual makeup of Congress, we may see another run at credit card legislation when the dust settles from the elections.”

Conclusion The currents moving through the indus-try are complex, intertwined, and often disruptive. However, two things are crystal clear: New challenges are arising on the operational and regulatory fronts, and cus-tomer expectations for ease of use and security are rising. By assessing the situ-ation, exploring consumer attitudes, and continuing the discussion, we can contend with developments as they unfold.

As these 10 trends demonstrate, success will require deeper expertise, the ability to learn from broad experience, innovation, and the agility to stay in step with chang-ing customer attitudes and technologies.

It’s no longer just about share of wallet. It’s about owning a customer relation-ship by creating value. As a result, com-panies will need to heighten their focus on consumers. A key lesson in the Vantiv/Mercator research is that “build it and they will come” is not effective in the world of payments. Early adopters may rush to try new methods, but most consumers want something more. They want to see how new approaches will improve upon what they have now—how they will save time and money, make payments more con-venient, and strengthen their confidence that information and funds are safe.

It is up to the industry to help consum-ers reach that understanding—and to keep driving improvements that work for consumers while enabling merchants and financial institutions to thrive.

Early adopters may rush to try new methods, but most consumers want something more. They want to see how new approaches will improve upon what they have.

Vantiv Corporate Headquarters

8500 Governors Hill Drive, Cincinnati, OH 45249866-622-2880 | www.vantiv.com

About Vantiv

Vantiv LLC is one of the leading integrated payment processors in the United States. Known as Fifth Third Processing Solutions since 1971, the company, headquartered in Cincinnati, Ohio, changed its name to Vantiv in 2011, and became a public company in 2012. Vantiv’s credit, debit, prepaid, and data security solutions help businesses and financial institutions of all sizes get the most out of payment activities.

TL0001 4/12